Evolutionary Game Analysis of Blockchain Technology Preventing Supply Chain Financial Risks

Abstract

:1. Introduction

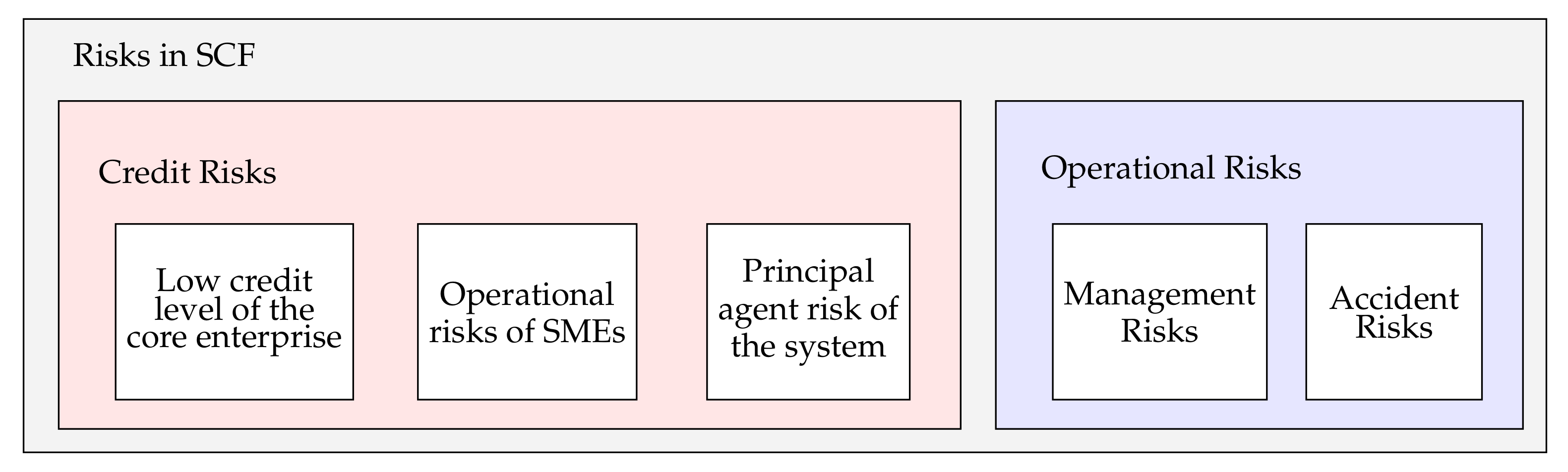

2. Problem Description and Basic Assumptions

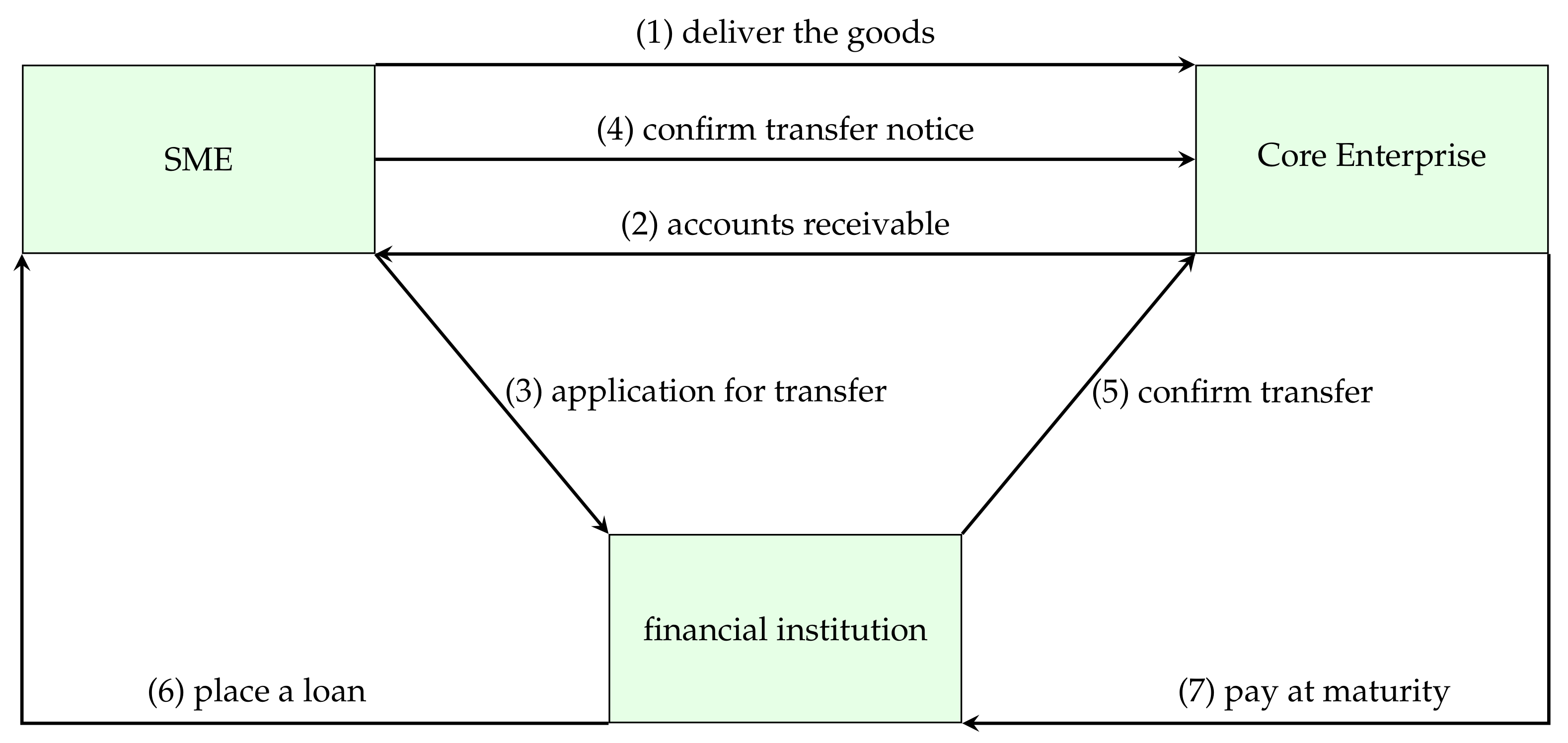

2.1. Problem Description

2.2. Basic Assumptions and Model Parameters

- R: the amount of accounts receivable;

- k: the bank pledge rate;

- : the return rate after successful financing of SMEs;

- : the default costs of SMEs;

- : the default cost of SMEs driven by blockchain technology;

- C: the production costs of SMEs;

- : the credit investigation cost of financial institutions;

- : the deposit rate of financial institutions;

- : the loan interest rate of financial institutions;

- x: the probability when financial institutions choose to accept the factoring application;

- y: the probability of SMEs choosing to keep the contract;

- : the probability that SMEs choose to collude when they do not comply;

- P: the ratio of profit distribution to SMEs in collusion;

- M: the blockchain platform maintenance fee.

3. The Model

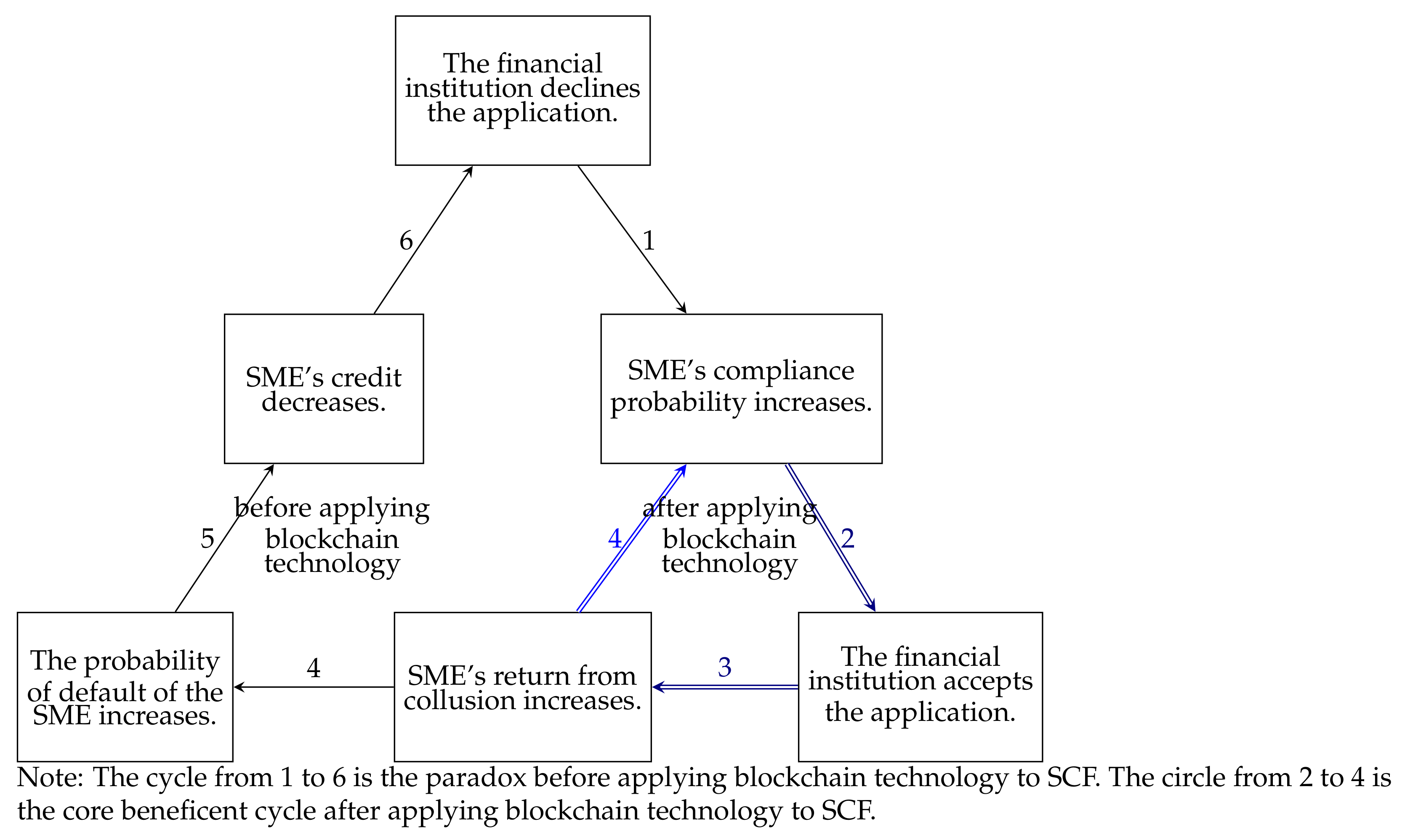

3.1. Before Applying Blockchain Technology

3.1.1. Construction of the Game Matrix

3.1.2. Replication Dynamic Equation of the Financial Institution

3.1.3. Replication Dynamic Equation of the SME

3.1.4. Analysis of Equilibrium State and Stability Strategy of Evolutionary Game

3.2. After Applying Blockchain Technology

3.3. Comparative Analysis

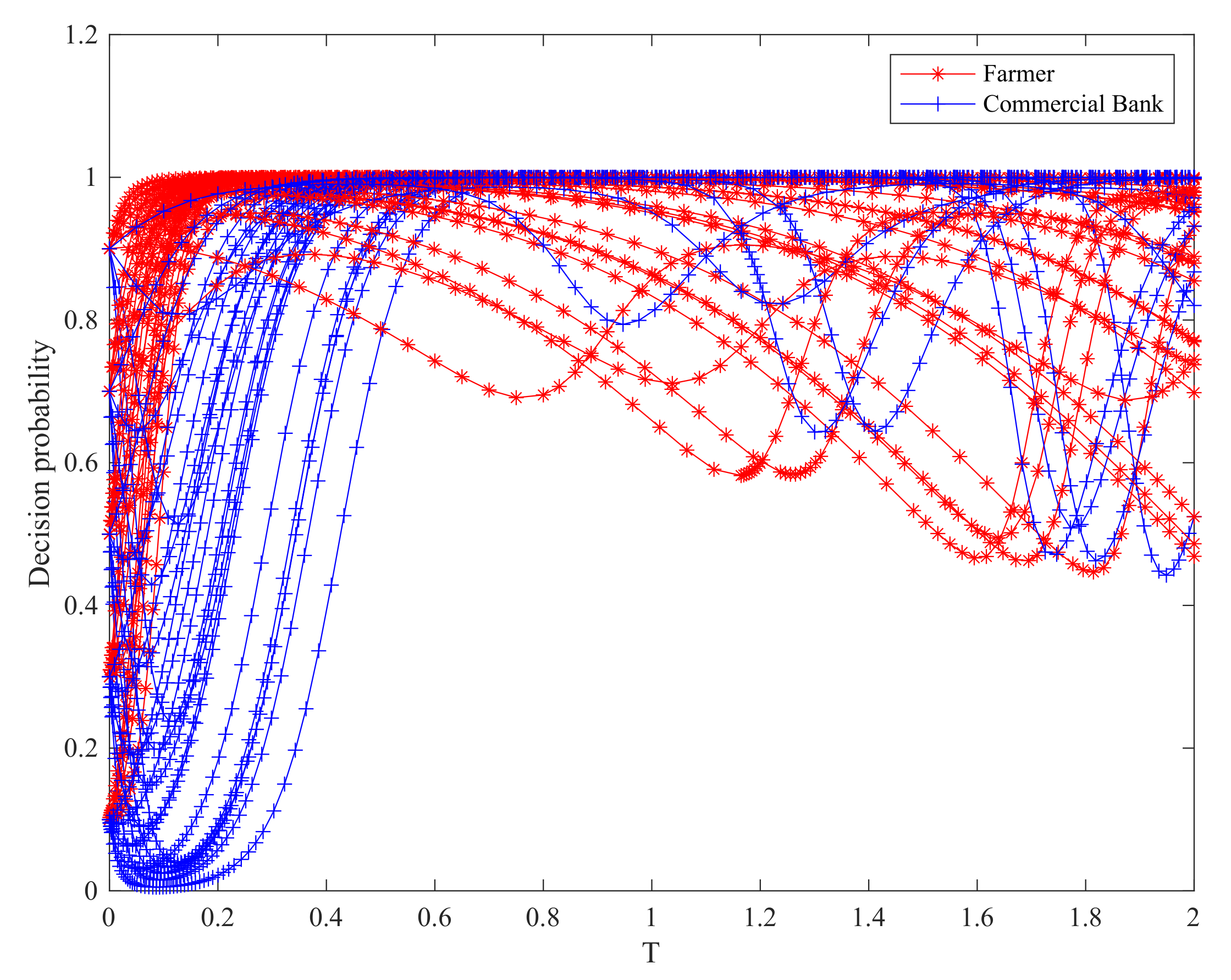

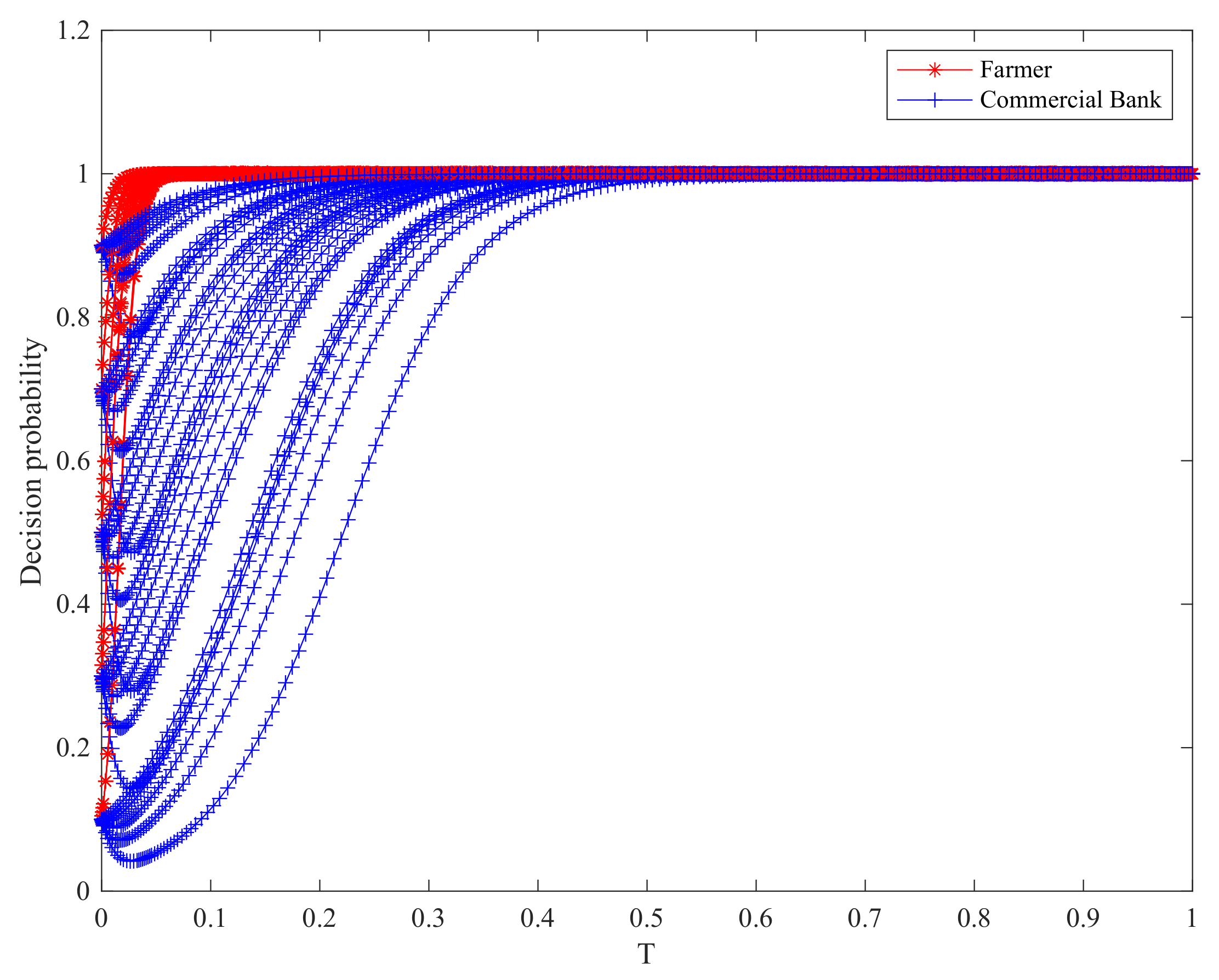

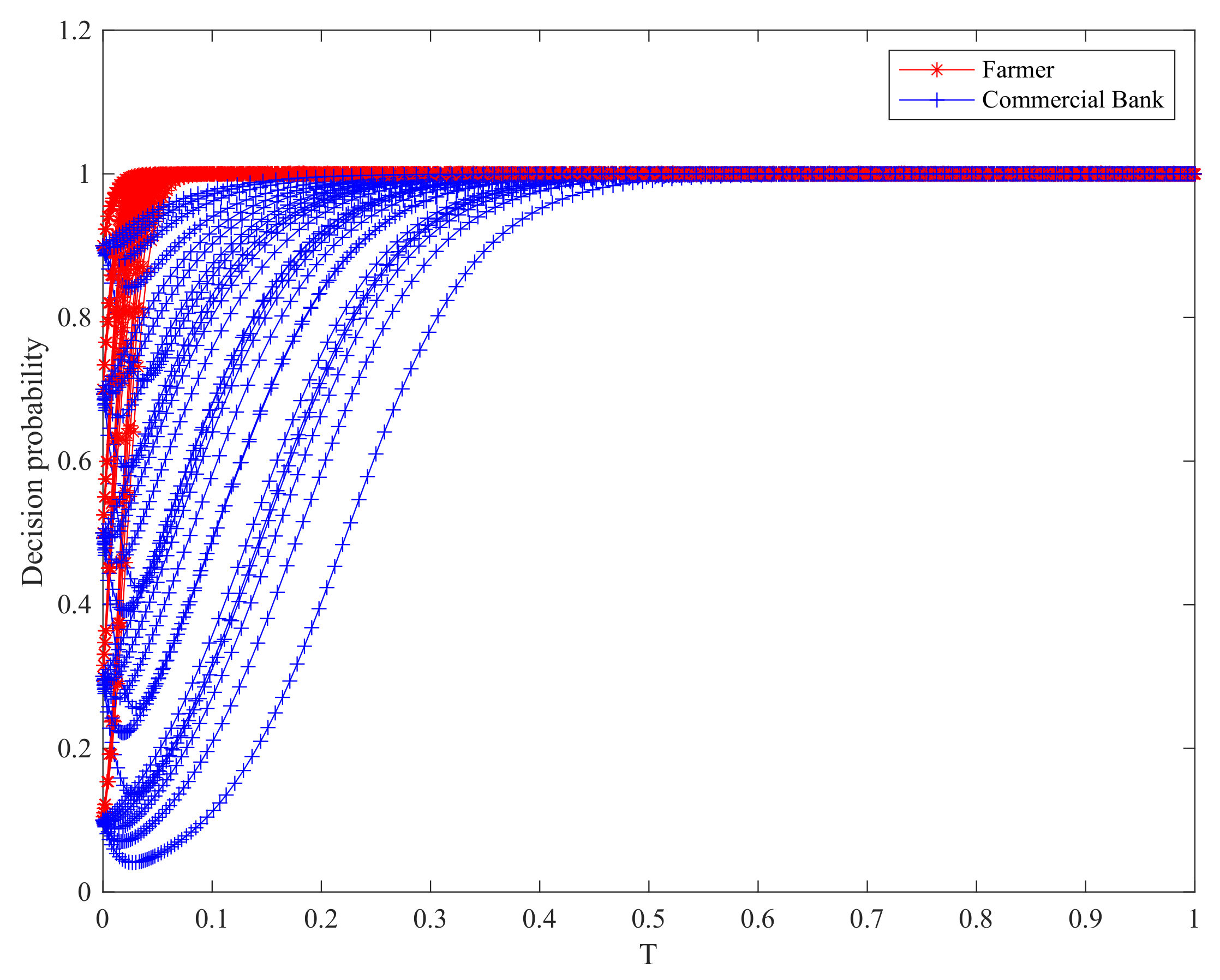

4. A Numerical Example

4.1. Background

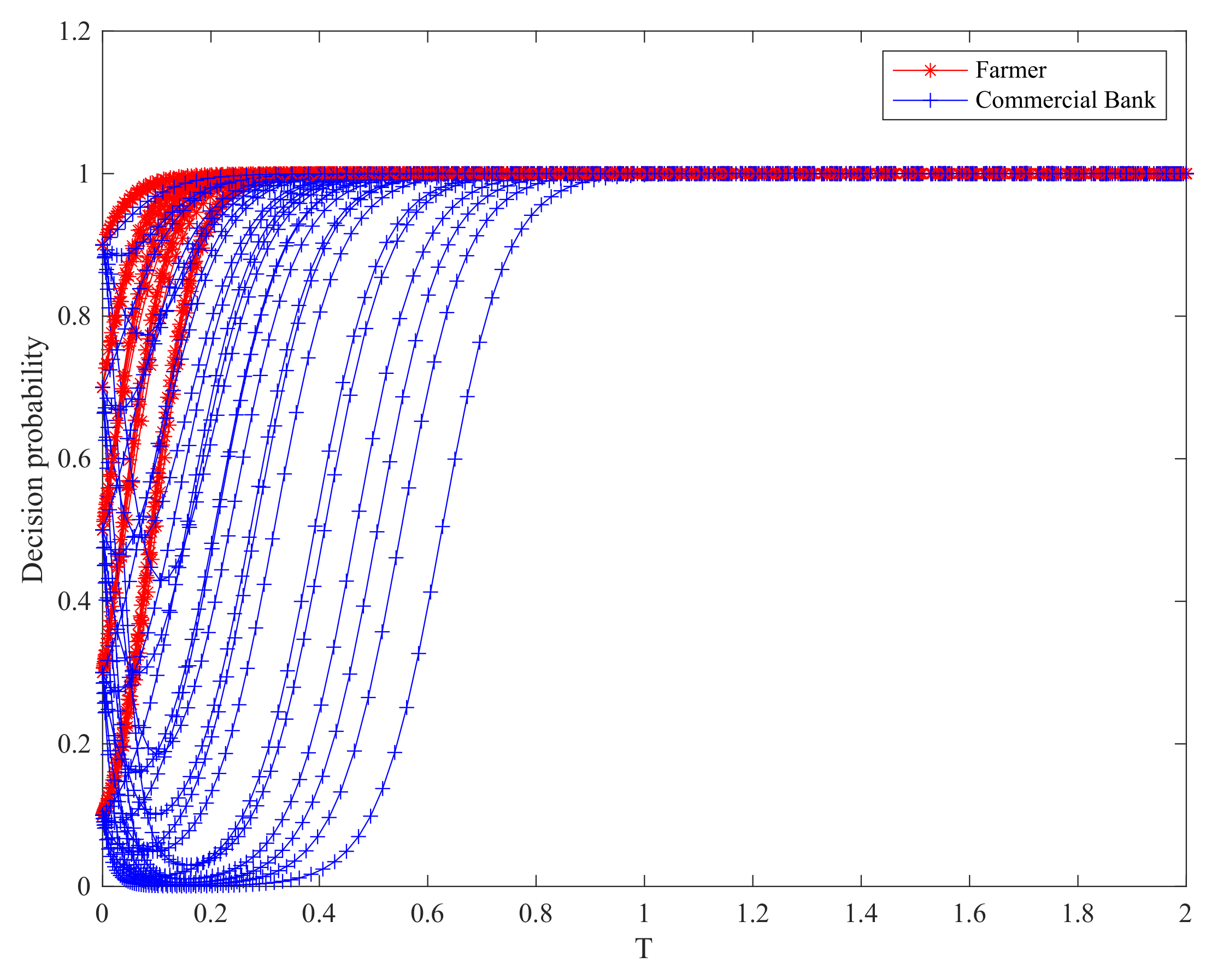

4.2. Stability Analysis of Accounts Receivable Financing Mode before Introducing Blockchain Technology

4.3. Stability Analysis of Accounts Receivable Financing Mode after Introducing Blockchain Technology

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Conflicts of Interest

References

- Li, J.; Wang, Y.; Feng, G.; Wang, S.; Song, Y. Supply chain finance review: Current situation and future trend. Syst. Eng. Theory Pract. 2020, 40, 1977–1995. [Google Scholar]

- Chai, Z.; Huang, X. Review. Mod. Manag. 2020, 40, 115–121. [Google Scholar]

- Huang, Y.; Liang, Z.; Wang, Y.; Lu, G. Research on the Application of Blockchain in Supply Chain Finance. Comput. Sci. Appl. 2018, 8, 78–88. [Google Scholar]

- Rui, H.; Lai, G. Sourcing with Deferred Payment and Inspection under Supplier Product Adulteration Risk. Prod. Oper. Manag. 2015, 24, 934–946. [Google Scholar] [CrossRef]

- Ehrenberg, A.J.; King, J.L. Blockchain in Context. Inf. Syst. Front. 2020, 22, 29–35. [Google Scholar] [CrossRef]

- Li, J.; Ananda, M.; Matthew, S.; Tony, G. Blockchain for supply chain quality management: Challenges and opportunities in context of open manufacturing and industrial internet of things. Int. J. Comput. Integr. Manuf. 2020, 33, 1321–1355. [Google Scholar] [CrossRef]

- Saberi, S.; Kouhizadeh, M.; Sarkis, J.; Shen, L. Blockchain technology and its relationships to sustainable supply chain management. Int. J. Prod. Res. 2019, 57, 2117–2135. [Google Scholar] [CrossRef] [Green Version]

- Gong, Q.; Ban, M.; Zhang, Y. Blockchain, enterprise digitalization and supply chain finance innovation. Manag. World 2021, 37, 22–34. [Google Scholar]

- Fang, Q.; Yang, X.; Li, Z. A Study on the Application of Blockchain Technology in Supply Chain Finance. J. Glob. Econ. Bus. Financ. 2020, 2, 43–47. [Google Scholar]

- Li, J.; Zhu, S.; Zhang, W.; Yu, L. Blockchain-driven supply chain finance solution for small and medium enterprises. Front. Eng. Manag. 2020, 7, 500–511. [Google Scholar] [CrossRef]

- Eyal, I. Blockchain technology: Transforming libertarian cryptocurrency dreams to finance and banking realities. Computer 2017, 50, 38–49. [Google Scholar] [CrossRef]

- Thurner, T. Supply chain finance and blockchain technology–the case of reverse securitisation. Foresight 2018, 20, 447–448. [Google Scholar] [CrossRef]

- Volodymyr, B.; Gilles, H. Distributed Ledgers and Operations: What Operations Management Researchers Should Know About Blockchain Technology. Manuf. Serv. Oper. Manag. 2019, 22, 223–240. [Google Scholar]

- Chen, J.; Cai, T.; He, W.; Chen, L.; Zhao, G.; Zou, W.; Guo, L. A blockchain-driven supply chain finance application for auto retail industry. Entropy 2020, 22, 95. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Tang, C.S.; Yang, S.A.; Wu, J. Sourcing from suppliers with financial constraints and performance risk. Manuf. Serv. Oper. Manag. 2018, 20, 70–84. [Google Scholar] [CrossRef] [Green Version]

- Xie, P.; Chen, Q.; Qu, P.; Fan, J.; Tang, Z. Research on financial platform of railway freight supply chain based on blockchain. Smart Resilient Transp. 2020, 2, 69–84. [Google Scholar] [CrossRef]

- Chod, J.; Trichakis, N.; Tsoukalas, G.; Aspegren, H.; Weber, M. On the financing benefits of supply chain transparency and blockchain adoption. Manag. Sci. 2020, 66, 4378–4396. [Google Scholar] [CrossRef]

- Tunca, T.I.; Zhu, W. Buyer intermediation in supplier finance. Manag. Sci. 2018, 64, 5631–5650. [Google Scholar] [CrossRef] [Green Version]

- Bal, M.; Pawlicka, K. Supply chain finance and challenges of modern supply chains. LogForum 2021, 17, 71–82. [Google Scholar]

- Hellwig, D.P. The Feasibility of Blockchain for Supply Chain Operations and Trade Finance: An Industry Study. 2019. Available online: https://www.acgusa.org/wp-content/uploads/2019/08/ACG-Final-Report-Daniel-Hellwig.pdf (accessed on 10 October 2021).

- Liu, Y.; Liu, C. Research on the influencing factors of supply chain enterprises’ compliance with contracts from the perspective of game. J. Hubei Univ. Technol. 2020, 35, 39–44. [Google Scholar]

- Gao, G.J.; Feng, Y.Y. Game analysis of factoring financing of accounts receivable from the perspective of limited rationality. Manuf. Autom. 2020, 42, 33–38. [Google Scholar]

- Chen, D.; Tian, C.; Chen, Z. A supply chain non-recourse factoring finance model considering the quality of the accounts receivable. J. Ind. Eng. Eng. Manag. 2020, 34, 101–108. [Google Scholar]

- Yan, N.; Sun, B.; Zhang, H.; Liu, C. A partial credit guarantee contract in a capital-constrained supply chain: Financing equilibrium and coordinating strategy. Int. J. Prod. Econ. 2016, 173, 122–133. [Google Scholar] [CrossRef]

- Yang, H.; Zhuo, W.; Shao, L. Equilibrium evolution in a two-echelon supply chain with financially constrained retailers: The impact of equity financing. Int. J. Prod. Econ. 2017, 185, 139–149. [Google Scholar] [CrossRef]

- Tang, D.; Zhuang, X. Financing a capital-constrained supply chain: Factoring accounts receivable vs a BCT-SCF receivable chain. Kybernetes 2020, 50, 2209–2231. [Google Scholar] [CrossRef]

- Min, P.J.; Yong, L.H.; Hyun, P.S.; Ingoo, H. Value relevance of accounts receivable factoring and its impact on financing strategy under the K-IFRS after COVID-19 from the perspective of accounting big data. Sustainability 2020, 12, 10287–10302. [Google Scholar]

- Van der Vliet, K.; Reindorp, M.J.; Fransoo, J.C. The price of reverse factoring: Financing rates vs. payment delays. Eur. J. Oper. Res. 2015, 242, 842–853. [Google Scholar] [CrossRef] [Green Version]

- Wu, Y.; Li, X.; Liu, Q.; Tong, G. The Analysis of Credit Risks in Agricultural Supply Chain Finance Assessment Model Based on Genetic Algorithm and Backpropagation Neural Network. Comput. Econ. 2021, 1–24. [Google Scholar] [CrossRef]

- Nguema, J.N.B.B.; Bi, G.; Ali, Z.; Mehreen, A.; Rukundo, C.; Ke, Y. Exploring the factors influencing the adoption of supply chain finance in supply chain effectiveness: Evidence from manufacturing firms. J. Bus. Ind. Mark. 2021, 36, 706–716. [Google Scholar] [CrossRef]

- Deng, A.; Yu, B. Research overview of risk management of SMEs accounts receivable financing based on supply chain finance. World J. Res. Rev. 2017, 4, 16–20. [Google Scholar]

- Wu, M. Research on Bank Credit Financing Model and Benefit Distribution Based on the Agricultural Value Chain. Ph.D. Thesis, Anhui University of Finance & Economics, Zhuhai, China, 2017. [Google Scholar]

- Kramer, M.P.; Bitsch, L.; Hanf, J. Blockchain and its impacts on agri-food supply chain network management. Sustainability 2021, 13, 2168. [Google Scholar] [CrossRef]

- Ni, J.; Zhao, J.; Chu, L.K. Supply contracting and process innovation in a dynamic supply chain with information asymmetry. Eur. J. Oper. Res. 2021, 288, 552–562. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| SME | ||||

|---|---|---|---|---|

| Non Compliance | Compliance | |||

| Collusion | Non Collusion | |||

| B | Accept | |||

| A | (x) | |||

| N | Decline | |||

| K | 0 | |||

| Conditions | Equilibrium Point | Sign of | Sign of | Judgement | |

|---|---|---|---|---|---|

| Case I | − | U | SP | ||

| − | U | SP | |||

| + | U | UP | |||

| + | − | ESS | |||

| + | 0 | CP | |||

| Case II | − | U | SP | ||

| − | U | SP | |||

| − | − | SP | |||

| − | U | SP | |||

| + | 0 | CP | |||

| SME | ||||

|---|---|---|---|---|

| Non Compliance | Compliance | |||

| Collusion | Non Collusion | |||

| B | Accept | |||

| A | (x) | |||

| N | Decline | |||

| K | 0 | |||

| Conditions | Equilibrium Point | Sign of | Sign of | Judgement |

|---|---|---|---|---|

| − | U | SP | ||

| − | U | SP | ||

| + | U | UP | ||

| + | − | ESS | ||

| + | 0 | CP |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sun, R.; He, D.; Su, H. Evolutionary Game Analysis of Blockchain Technology Preventing Supply Chain Financial Risks. J. Theor. Appl. Electron. Commer. Res. 2021, 16, 2824-2842. https://doi.org/10.3390/jtaer16070155

Sun R, He D, Su H. Evolutionary Game Analysis of Blockchain Technology Preventing Supply Chain Financial Risks. Journal of Theoretical and Applied Electronic Commerce Research. 2021; 16(7):2824-2842. https://doi.org/10.3390/jtaer16070155

Chicago/Turabian StyleSun, Rui, Dayi He, and Huilin Su. 2021. "Evolutionary Game Analysis of Blockchain Technology Preventing Supply Chain Financial Risks" Journal of Theoretical and Applied Electronic Commerce Research 16, no. 7: 2824-2842. https://doi.org/10.3390/jtaer16070155