Sustainable Development and Business Strategies: An Exploratory Study of Greek Businesses

Abstract

:1. Introduction

2. Literature Review

2.1. The Concept of Sustainable Development and SDGs

- Economic pillar: SD goals 1, 2, 3, 8, and 9.

- Social Pillar: SD goals 4, 5, 10, 11, 16, and 17.

- Environmental Pillar: SD goals 6, 7, 12, 14, 13, and 15.

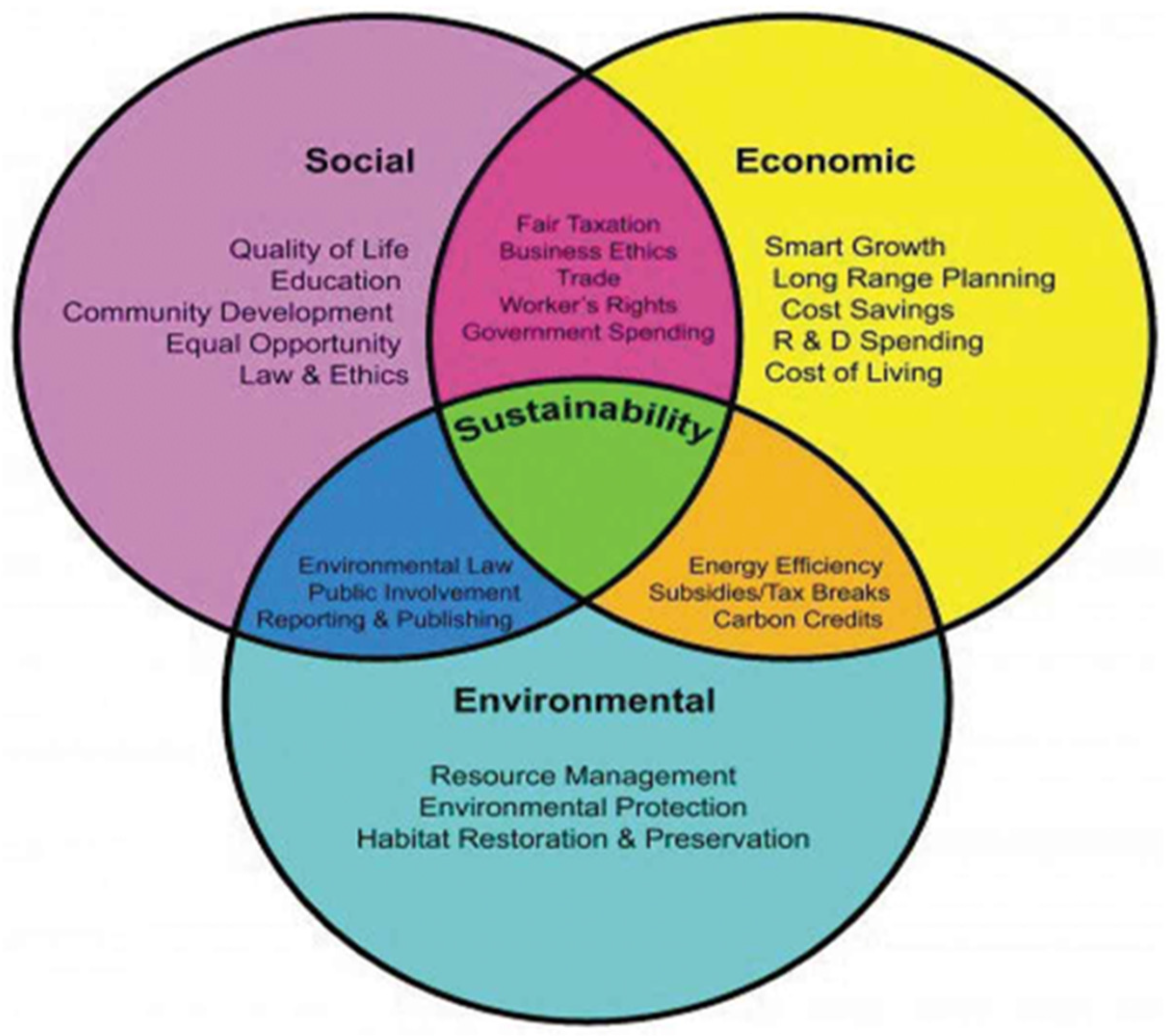

2.2. Sustainable Development and the TBL (Triple Bottom Line)

- Corporate Social Responsibility (CSR), which is a business performance measurement system that integrates social and environmental concerns regarding the activities of businesses. Despite not being compulsory, it shows a positive commitment toward society [32]. Reforestation of an area by planting trees to improve the environment is an indicative example of CSR.

- Environmental management system (EMS), which are guidelines that a company may use to protect the environment. The EMS supports the environment through the prevention of pollution and the use of a management system, which provides guidance and usually a third-party certification (e.g., ISO 14001) [28].

- A specific sustainable development performance measurement system called ESG (Environment, Social, Governance), which has been used by companies in recent years. Companies that adhere to ESG criteria are considered less risky, with a good long-term course, future, and organizational structure [6]. Today, many companies are using ESG to publicly inform shareholders and society about their actions towards sustainability.

2.3. Sustainable Development and Business Strategies

3. Materials and Methods

3.1. Research Hypotheses

- SP: social pillar;

- EP: economic pillar;

- ENP: environmental pillar;

- CA: competitive advantage;

- BP: business performance.

3.2. Research Design and Methodology

4. Data Analysis and Results

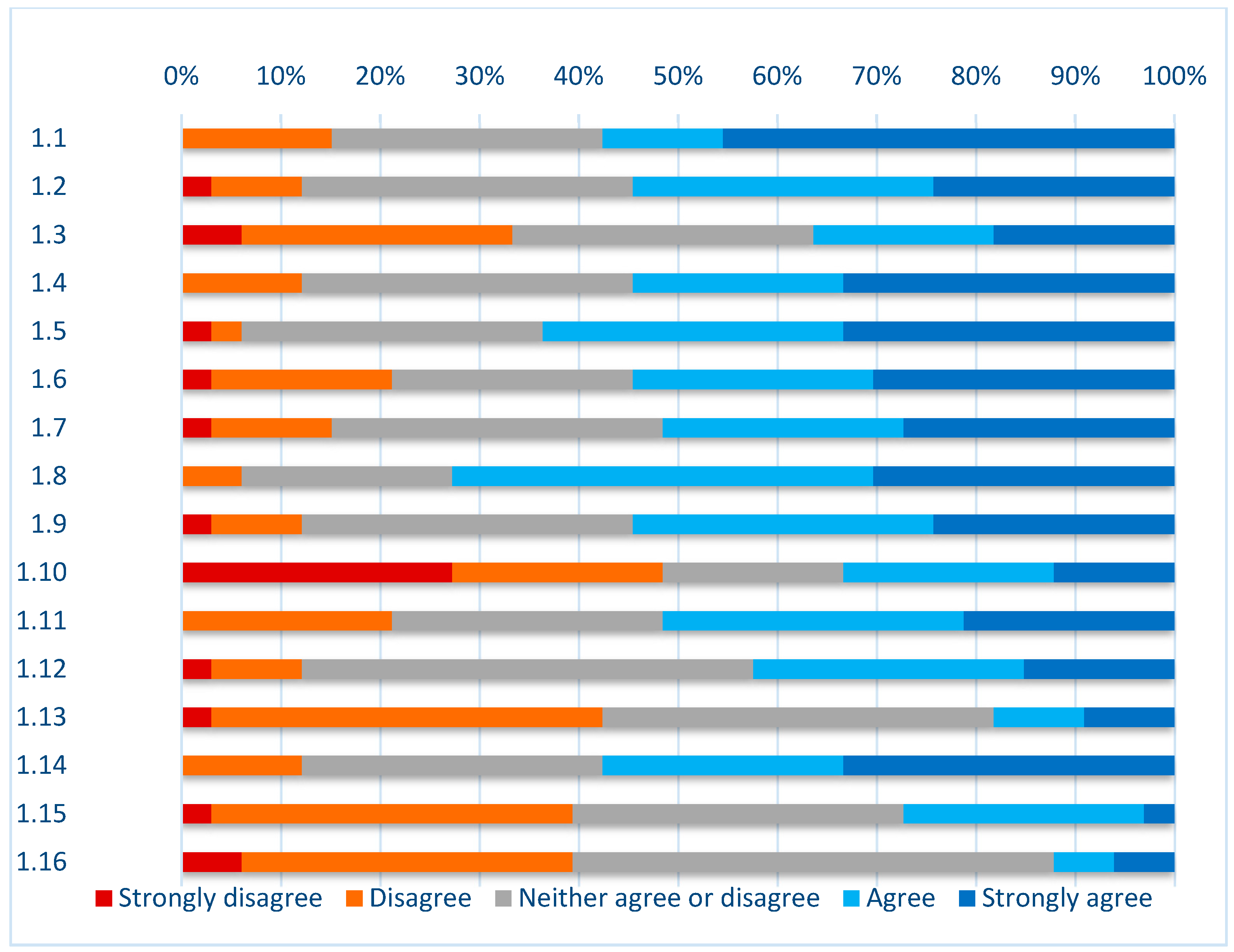

4.1. Univariate Statistics

- Positive: includes the categories ‘agree’ and ‘strongly agree’;

- Neutral: includes the category ‘neither agree nor disagree’;

- Negative: includes the categories ‘disagree’ and ‘strongly disagree’.

- Environmental: “Would you adopt systems to reduce environmental impact like packaging?”, “Your business practices focus on environmental issues”.

- Social: “Your business practices focus on social issues”, “Are you considering the social welfare of society as a whole?”, “Do your HR processes exceed legal requirements?”.

- Economic: “Your business practices focus on financial issues”, “Is sustainable development a means of focusing on market survival?”, “Do most of your competitors take environmental protection measures?”.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Section 1 | Strongly Disagree | Disagree | Neither Agree nor Disagree | Agree | Strongly Agree |

|---|---|---|---|---|---|

| 1.1 Do you know what sustainable development is? | 0.00% | 15.15% | 27.27% | 12.12% | 45.45% |

| 1.2 What is the value of sustainable business practices to your company? | 3.03% | 9.09% | 33.33% | 30.30% | 24.24% |

| 1.3 Is implementing sustainable practices within the business and its business network complex and time consuming? | 6.06% | 27.27% | 30.30% | 18.18% | 18.18% |

| 1.4 Would you use sustainability key performance metrics? | 0.00% | 12.12% | 33.33% | 21.21% | 33.33% |

| 1.5 Would you adopt systems to reduce environmental impact like packaging? | 3.03% | 3.03% | 30.30% | 30.30% | 33.33% |

| 1.6 Your business practices focus on environmental issues | 3.03% | 18.18% | 24.24% | 24.24% | 30.30% |

| 1.7 Your business practices focus on social issues | 3.03% | 12.12% | 33.33% | 24.24% | 27.27% |

| 1.8 Your business practices focus on financial issues | 0.00% | 6.06% | 21.21% | 42.42% | 30.30% |

| 1.9 Are you considering the social welfare of society as a whole? | 3.03% | 9.09% | 33.33% | 30.30% | 24.24% |

| 1.10 Do your HR processes exceed legal requirements? | 27.27% | 21.21% | 18.18% | 21.21% | 12.12% |

| 1.11 Sustainable development is a means of advertising | 0.00% | 21.21% | 27.27% | 30.30% | 21.21% |

| 1.12 Sustainable development is a means of focusing on market survival | 3.03% | 9.09% | 45.45% | 27.27% | 15.15% |

| 1.13 Sustainable development is known in the market | 3.03% | 39.39% | 39.39% | 9.09% | 9.09% |

| 1.14 Would you use Sustainable Performance Measurement Systems? | 0.00% | 12.12% | 30.30% | 24.24% | 33.33% |

| 1.15 Do customers, suppliers, government, and other stakeholders encourage the organization to identify itself as a green business? | 3.03% | 36.36% | 33.33% | 24.24% | 3.03% |

| 1.16 Do most of your competitors take environmental protection measures? | 6.06% | 33.33% | 48.48% | 6.06% | 6.06% |

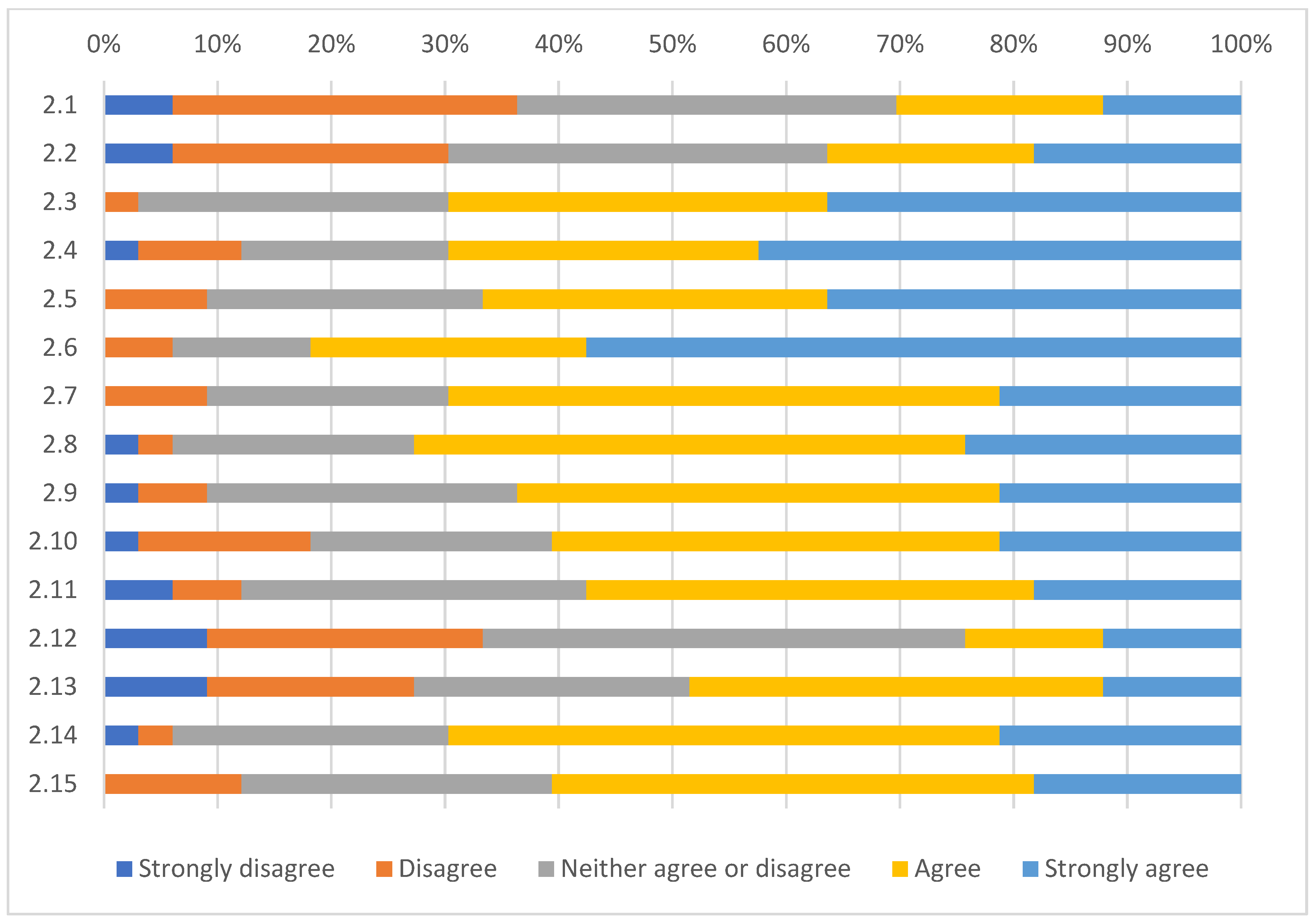

- Social: “Do you provide procedures that help ensure the health and safety of our employees?”, “Do you support your employees who wish to pursue further education?”, “Do you provide your employees with salaries that properly and fairly reward them for their work?”, “Do you treat all employees fairly and respectfully, regardless of gender or ethnic background?”

- Environmental: “Have you adopted processes to reduce energy consumption?”, “Have you adopted processes to reduce and recycle waste?”, “Have you adopted processes to reduce water consumption?”, “Have you implemented systems to reduce harmful emissions?”, “Have you adopted systems to reduce packaging environmental effects?”

- Economic: “Do you involve all suppliers in new products or services development?”, “Do you inform all suppliers of products and services about organizational changes affecting purchasing decisions?”, “Do you provide all customers with the information needed to make sound purchasing decisions?”.

| Section 2 | Strongly Disagree | Disagree | Neither Agree nor Disagree | Agree | Strongly Agree |

|---|---|---|---|---|---|

| 2.1 Performance measurement systems, including sustainability key performance indicators? | 6.06% | 30.30% | 33.33% | 18.18% | 12.12% |

| 2.2 Social, environmental or sustainability reporting? | 6.06% | 24.24% | 33.33% | 18.18% | 18.18% |

| 2.3 Do you provide procedures that help ensure the health and safety of our employees? | 0.00% | 3.03% | 27.27% | 33.33% | 36.36% |

| 2.4 Do you support your employees who wish to pursue further education? | 3.03% | 9.09% | 18.18% | 27.27% | 42.42% |

| 2.5 Do you provide your employees with salaries that properly and fairly reward them for their work? | 0.00% | 9.09% | 24.24% | 30.30% | 36.36% |

| 2.6 Do you treat all employees fairly and respectfully, regardless of gender or ethnic background? | 0.00% | 6.06% | 12.12% | 24.24% | 57.58% |

| 2.7 Have you adopted processes to reduce energy consumption? | 0.00% | 9.09% | 21.21% | 48.48% | 21.21% |

| 2.8 Have you adopted processes to reduce and recycle waste? | 3.03% | 3.03% | 21.21% | 48.48% | 24.24% |

| 2.9 Have you adopted processes to reduce water consumption? | 3.03% | 6.06% | 27.27% | 42.42% | 21.21% |

| 2.10 Do you implement systems to reduce harmful emissions? | 3.03% | 15.15% | 21.21% | 39.39% | 21.21% |

| 2.11 Have you adopted systems to reduce packaging’s environmental effects? | 6.06% | 6.06% | 30.30% | 39.39% | 18.18% |

| 2.12 Do you involve all suppliers in new products or services development? | 9.09% | 24.24% | 42.42% | 12.12% | 12.12% |

| 2.13 Do you inform all suppliers of products and services about organizational changes affecting purchasing decisions? | 9.09% | 18.18% | 24.24% | 36.36% | 12.12% |

| 2.14 Do you provide all customers with the information needed to make sound purchasing decisions? | 3.03% | 3.03% | 24.24% | 48.48% | 21.21% |

| 2.15 The level of customer satisfaction is higher than that of competitors | 0.00% | 12.12% | 27.27% | 42.42% | 18.18% |

4.2. Reliability and Validity Testing, Correlation

- r ≤ 0.29 No correlation.

- 0.30 < r < 0.49 No significant correlation.

- 0.50 < r < 0.69 Medium correlation.

- 0.70 < r < 0.79 High correlation.

- 0.80 < r < 0.99 Very high correlation.

5. Discussion, Conclusions, and Future Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Ranjbari, M.; Shams Esfandabadi, Z.; Zanetti, M.C.; Scagnelli, S.D.; Siebers, P.-O.; Aghbashlo, M.; Peng, W.; Quatraro, F.; Tabatabaei, M. Three Pillars of Sustainability in the Wake of COVID-19: A Systematic Review and Future Research Agenda for Sustainable Development. J. Clean. Prod. 2021, 297, 126660. [Google Scholar] [CrossRef] [PubMed]

- United Nations. Transforming Our World: The 2030 Agenda for Sustainable Development; United Nations: San Francisco, CA, USA, 2015; Available online: https://sustainabledevelopment.un.org/content/documents/21252030%20Agenda%20for%20Sustainable%20Development%20web.pdf (accessed on 27 May 2022).

- Dhahri, S.; Omri, A. Entrepreneurship Contribution to the Three Pillars of Sustainable Development: What Does the Evidence Really Say? World Dev. 2018, 106, 64–77. [Google Scholar] [CrossRef] [Green Version]

- Zhai, T.; Chang, Y.-C. Standing of Environmental Public-Interest Litigants in China: Evolution, Obstacles and Solutions. J. Environ. Law 2018, 30, 369–397. [Google Scholar] [CrossRef]

- Elkington, J. Towards the Sustainable Corporation: Win-Win-Win Business Strategies for Sustainable Development. Calif. Manag. Rev. 1994, 36, 90–100. [Google Scholar] [CrossRef]

- Nelson, M. Investor Sentiment on ESG and Nonfinancial Reporting. Available online: https://www.ey.com/en_gl/assurance/how-will-esg-performance-shape-your-future (accessed on 27 May 2022).

- Scheyvens, R.; Banks, G.; Hughes, E. The Private Sector and the SDGs: The Need to Move Beyond ‘Business as Usual’: The Private Sector and the SDGs: Moving Beyond ‘Business-as-Usual’. Sust. Dev. 2016, 24, 371–382. [Google Scholar] [CrossRef]

- Tulder, V. Rob Business & The Sustainable Development Goals: A Framework for Effective Corporate Involvement; Erasmus University Rotterdam: Rotterdam, The Netherlands, 2018. [Google Scholar]

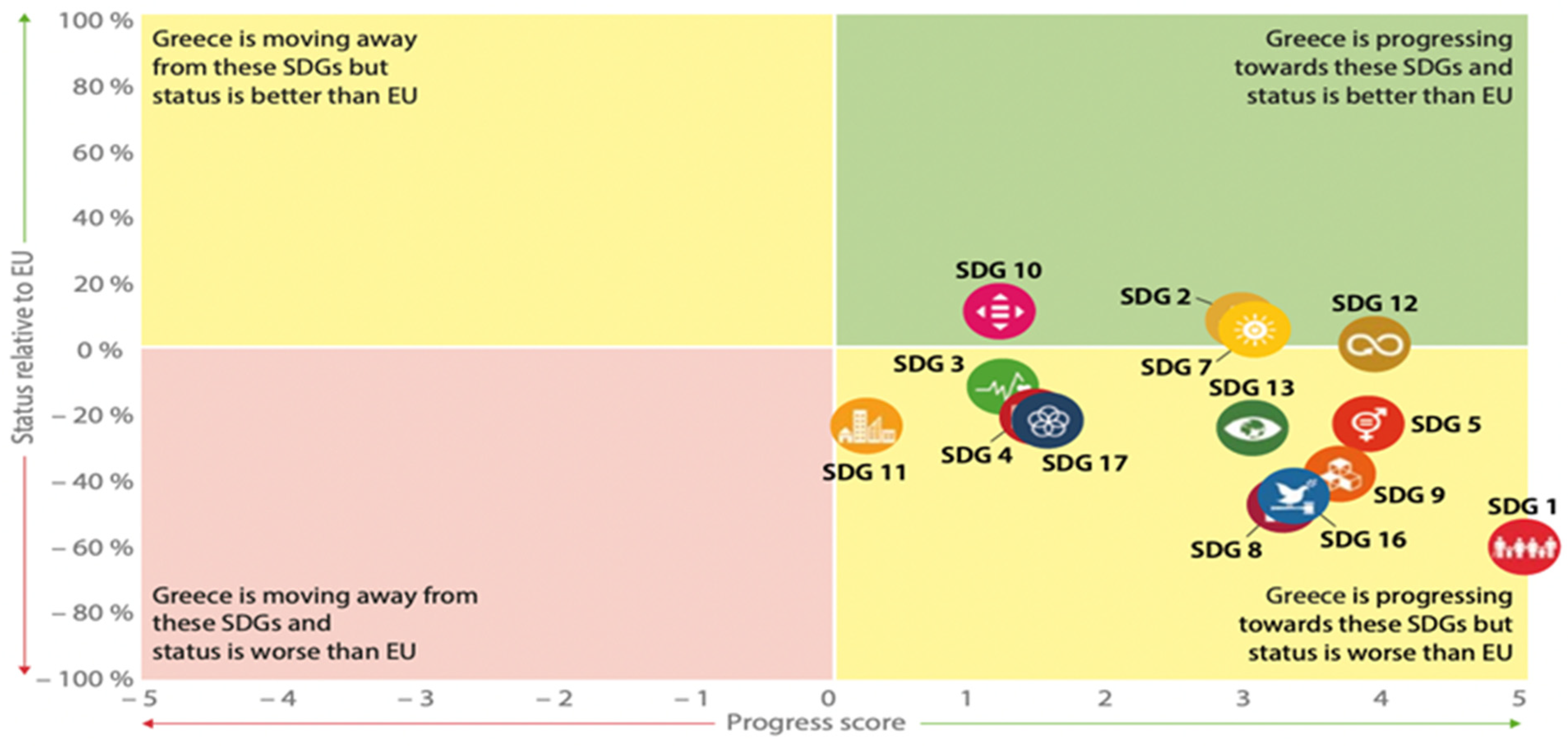

- European Commission; Eurostat. Sustainable Development in the European Union: Monitoring Report on Progress towards the SDGs in an EU Context: 2022 Edition; Publications Office of the European Union: Luxembourg, 2022; Available online: https://data.europa.eu/doi/10.2785/313289 (accessed on 27 May 2022).

- European Commission; Eurostat. Sustainable Development in the European Union: Monitoring Report on Progress towards the SDGs in an EU Context: 2021 Edition; Publications Office of the European Union: Luxembourg, 2021; Available online: https://data.europa.eu/doi/10.2785/195273 (accessed on 27 May 2022).

- Graedel, T.E.; Allenby, B.R. Industrial Ecology and Sustainable Engineering; Prentice Hall: Upper Saddle River, NJ, USA, 2010; ISBN 978-0-13-600806-4. [Google Scholar]

- Du Pisani, J.A. Sustainable Development—Historical Roots of the Concept. Null 2006, 3, 83–96. [Google Scholar] [CrossRef]

- Mebratu, D. Sustainability and Sustainable Development: Historical and Conceptual Review. Environ. Impact Assess. Rev. 1998, 18, 493–520. [Google Scholar] [CrossRef]

- Waas, T.; Hugé, J.; Verbruggen, A.; Wright, T. Sustainable Development: A Bird’s Eye View. Sustainability 2011, 3, 1637–1661. [Google Scholar] [CrossRef] [Green Version]

- Clark, W.; Harley, A. Sustainability Science: Towards a Synthesis. In Sustainability Science Program Working Paper 2019-01; John F. Kennedy School of Government, Harvard University: Cambridge, MA, USA, 2019. [Google Scholar]

- Van Tulder, R.; Rodrigues, S.B.; Mirza, H.; Sexsmith, K. The UN’s Sustainable Development Goals: Can Multinational Enterprises Lead the Decade of Action? J. Int. Bus. Policy 2021, 4, 1–21. [Google Scholar] [CrossRef]

- UN THE 17 GOALS|Sustainable Development. Available online: https://sdgs.un.org/goals (accessed on 23 June 2022).

- Kanie, N.; Griggs, D.; Young, O.; Waddell, S.; Shrivastava, P.; Haas, P.M.; Broadgate, W.; Gaffney, O.; Kőrösi, C. Rules to Goals: Emergence of New Governance Strategies for Sustainable Development: Governance for Global Sustainability Is Undergoing a Major Transformation from Rule-Based to Goal-Based. But with No Compliance Measures, Success Will Require an Unprecedented Level of Coherency of Action Founded on New and Reformed Institutions Nationally and Internationally. Sustain. Sci. 2019, 14, 1745–1749. [Google Scholar] [CrossRef] [Green Version]

- European Commission. Eurostat EU SDG Indicator Set 2021 Result of the Review in Preparation of the 2021 Edition of the EU SDG Monitoring Report; European Commission: Brussels, Belgium, 2021; Available online: https://ec.europa.eu/eurostat/documents/276524/12239692/SDG_indicator_set_2021.pdf (accessed on 27 May 2022).

- Bali Swain, R.; Yang-Wallentin, F. Achieving Sustainable Development Goals: Predicaments and Strategies. Null 2020, 27, 96–106. [Google Scholar] [CrossRef] [Green Version]

- Hellenic Republic. Voluntary National Review 2018 on the Implementation of the 2030 Agenda for Sustainable Development; General Secretariat of the Government Office of Coordination, Institutional, International & European Affairs: Thessaloniki, Greece, 2018; p. 160. Available online: https://sustainabledevelopment.un.org/content/documents/19378Greece_VNR_Greece_2018_pdf_FINAL_140618.pdf (accessed on 27 May 2022).

- Hellenic Republic. Voluntary National Review 2022—On the Implementation of the 2030 Agenda for Sustainable Development; General Secretariat of the Government Office of Coordination, Institutional, International & European Affairs: Thessaloniki, Greece, 2022; p. 364. Available online: https://www.statistics.gr/documents/20181/13491320/VNR+2022+Greece+Report.pdf/d0b97502-84b4-866f-e32e-2d91dff2538a (accessed on 27 May 2022).

- Hellenic Ministry of Environment, Energy and Climate Change, Press Releases. Available online: https://ypen.gov.gr/kostas-skrekas-me-200-ekat-evro-anavathmizoume-tin-energeiaki-apodosi-mikromesaion-epicheiriseon-tis-rachokokalias-tis-ethnikis-mas-oikonomias/ (accessed on 27 May 2022). (In Greek)

- Alhaddi, H. Triple Bottom Line and Sustainability: A Literature Review. BMS 2015, 1, 6. [Google Scholar] [CrossRef]

- Smith, P.A.C.; Sharicz, C. The Shift Needed for Sustainability. Learn. Organ. 2011, 18, 73–86. [Google Scholar] [CrossRef]

- Mensah, J. Sustainable Development: Meaning, History, Principles, Pillars, and Implications for Human Action: Literature Review. Cogent Soc. Sci. 2019, 5, 1653531. [Google Scholar] [CrossRef]

- Høgevold, N.M.; Svensson, G.; Klopper, H.B.; Wagner, B.; Valera, J.C.S.; Padin, C.; Ferro, C.; Petzer, D. A Triple Bottom Line Construct and Reasons for Implementing Sustainable Business Practices in Companies and Their Business Networks. Corp. Gov. 2015, 15, 427–443. [Google Scholar] [CrossRef]

- Mao, J.; Li, C.; Pei, Y.; Xu, L. Circular Economy and Sustainable Development Enterprises, 1st ed.; Springer: Singapore, 2018; ISBN 978-981-10-8524-6. [Google Scholar]

- Bordoli, L.; Scire’, G.; Rossi, F. Designing Dynamic Sustainable Business Models to Assess the Feasibility of an Industrial Symbiosis: The Case of the Retro-Port Area of Trieste. Businesses 2023, 3, 368–381. [Google Scholar] [CrossRef]

- Boiral, O. Sustainability Reports as Simulacra? A Counter-Account of A and A+ GRI Reports. Account. Audit. Account. J. 2013, 26, 1036–1071. [Google Scholar] [CrossRef]

- Belkhir, L.; Bernard, S.; Abdelgadir, S. Does GRI Reporting Impact Environmental Sustainability? A Cross-Industry Analysis of CO2 Emissions Performance between GRI-Reporting and Non-Reporting Companies. MEQ 2017, 28, 138–155. [Google Scholar] [CrossRef]

- Boccia, F.; Sarnacchiaro, P. The Impact of Corporate Social Responsibility on Consumer Preference: A Structural Equation Analysis. Corp. Soc. Responsib. Environ. Manag. 2018, 25, 151–163. [Google Scholar] [CrossRef]

- Gimenez, C.; Sierra, V.; Rodon, J. Sustainable Operations: Their Impact on the Triple Bottom Line. Int. J. Prod. Econ. 2012, 140, 149–159. [Google Scholar] [CrossRef]

- Fowler, S.J.; Hope, C. Incorporating Sustainable Business Practices into Company Strategy. Bus. Strat. Env. 2007, 16, 26–38. [Google Scholar] [CrossRef]

- Wheelen, T.L.; Hunger, J.D.; Hoffman, A.N.; Bamford, C.E. Strategic Management and Business Policy: Globalization, Innovation, and Sustainability, 15th ed.; Pearson Education Limited.: London, UK, 2018; ISBN 978-1-292-21548-8. [Google Scholar]

- Tien, N.H.; Anh, D.B.H.; Ngoc, N.M. Corporate Financial Performance Due to Sustainable Development in Vietnam. Corp Soc. Responsib. Env. 2020, 27, 694–705. [Google Scholar] [CrossRef]

- Aragón-Correa, J.A.; Hurtado-Torres, N.; Sharma, S.; García-Morales, V.J. Environmental Strategy and Performance in Small Firms: A Resource-Based Perspective. J. Environ. Manag. 2008, 86, 88–103. [Google Scholar] [CrossRef] [PubMed]

- Larrán Jorge, M.; Herrera Madueño, J.; Martínez-Martínez, D.; Lechuga Sancho, M.P. Competitiveness and Environmental Performance in Spanish Small and Medium Enterprises: Is There a Direct Link? J. Clean. Prod. 2015, 101, 26–37. [Google Scholar] [CrossRef]

- Saeidi, S.P.; Sofian, S.; Saeidi, P.; Saeidi, S.P.; Saaeidi, S.A. How Does Corporate Social Responsibility Contribute to Firm Financial Performance? The Mediating Role of Competitive Advantage, Reputation, and Customer Satisfaction. J. Bus. Res. 2015, 68, 341–350. [Google Scholar] [CrossRef]

- Porter, M.E.; Kramer, M.R. The Link between Competitive Advantage and Corporate Social Responsibility. Harv. Bus. Rev. 2006, 84, 78–92. [Google Scholar]

- ElAlfy, A.; Palaschuk, N.; El-Bassiouny, D.; Wilson, J.; Weber, O. Scoping the Evolution of Corporate Social Responsibility (CSR) Research in the Sustainable Development Goals (SDGs) Era. Sustainability 2020, 12, 5544. [Google Scholar] [CrossRef]

- Fallah Shayan, N.; Mohabbati-Kalejahi, N.; Alavi, S.; Zahed, M.A. Sustainable Development Goals (SDGs) as a Framework for Corporate Social Responsibility (CSR). Sustainability 2022, 14, 1222. [Google Scholar] [CrossRef]

- Garrido-Ruso, M.; Aibar-Guzmán, B.; Monteiro, A.P. Businesses’ Role in the Fulfillment of the 2030 Agenda: A Bibliometric Analysis. Sustainability 2022, 14, 8754. [Google Scholar] [CrossRef]

- Khaled, R.; Ali, H.; Mohamed, E.K.A. The Sustainable Development Goals and Corporate Sustainability Performance: Mapping, Extent and Determinants. J. Clean. Prod. 2021, 311, 127599. [Google Scholar] [CrossRef]

- Sekaran, U.; Bougie, R. Research Methods for Business: A Skill-Building Approach, 7th ed.; Wiley: Chichester, UK, 2016; ISBN 978-1-119-16555-2. [Google Scholar]

- Demertzi, E. Top 40 Sectors of the Greek Economy 2020, 11th ed.; ICAP: New York, NY, USA, 2020; Available online: https://dir.icap.gr/mailimages/flipbooks/LS/2020/ (accessed on 27 May 2022).

- Demertzi, E. Top 40 Sectors of the Greek Economy 2018; ICAP: New York, NY, USA, 2018; Available online: https://dir.icap.gr/mailimages/flipbooks/LS/2020/ (accessed on 27 May 2022).

- Bagur-Femenias, L.; Llach, J.; del Mar Alonso-Almeida, M. Is the Adoption of Environmental Practices a Strategical Decision for Small Service Companies? An Empirical Approach. Manag. Decis. 2013, 51, 41–62. [Google Scholar] [CrossRef]

- Cantele, S.; Zardini, A. Is Sustainability a Competitive Advantage for Small Businesses? An Empirical Analysis of Possible Mediators in the Sustainability–Financial Performance Relationship. J. Clean. Prod. 2018, 182, 166–176. [Google Scholar] [CrossRef]

- López-Pérez, M.E.; Melero, I.; Javier Sese, F. Management for Sustainable Development and Its Impact on Firm Value in the SME Context: Does Size Matter?: Management for Sustainable Development: Doses Size Matter? Bus. Strat. Env. 2017, 26, 985–999. [Google Scholar] [CrossRef]

- Tavakol, M.; Dennick, R. Making Sense of Cronbach’s Alpha. Int. J. Med. Educ. 2011, 2, 53–55. [Google Scholar] [CrossRef] [PubMed]

- Yong, A.G.; Pearce, S. A Beginner’s Guide to Factor Analysis: Focusing on Exploratory Factor Analysis. TQMP 2013, 9, 79–94. [Google Scholar] [CrossRef] [Green Version]

- Kaiser, H.F. An Index of Factorial Simplicity. Psychometrika 1974, 39, 31–36. [Google Scholar] [CrossRef]

- Aczel, A.D.; Sounderpandian, J. Complete Business Statistics, 7th ed.; The McGraw-Hill/Irwin series Operations and decision sciences; McGraw-Hill/Irwin: Boston, MA, USA, 2009; ISBN 978-0-07-337360-7. [Google Scholar]

- Roussos, P.L.; Tsaouses, G. Statistike Stis Epistemes Tes Symperiphoras Me te Chrese tou SPSS; Topos: Athena, Belgium, 2011; ISBN 978-960-6863-69-1. [Google Scholar]

- Haseeb, M.; Hussain, H.I.; Kot, S.; Androniceanu, A.; Jermsittiparsert, K. Role of Social and Technological Challenges in Achieving a Sustainable Competitive Advantage and Sustainable Business Performance. Sustainability 2019, 11, 3811. [Google Scholar] [CrossRef] [Green Version]

- Herrera Madueño, J.; Larrán Jorge, M.; Martínez Conesa, I.; Martínez-Martínez, D. Relationship between Corporate Social Responsibility and Competitive Performance in Spanish SMEs: Empirical Evidence from a Stakeholders’ Perspective. BRQ Bus. Res. Q. 2016, 19, 55–72. [Google Scholar] [CrossRef] [Green Version]

- Chang, C.-H. The Influence of Corporate Environmental Ethics on Competitive Advantage: The Mediation Role of Green Innovation. J. Bus. Ethics 2011, 104, 361–370. [Google Scholar] [CrossRef]

- Chen, Y.-S.; Lai, S.-B.; Wen, C.-T. The Influence of Green Innovation Performance on Corporate Advantage in Taiwan. J. Bus. Ethics 2006, 67, 331–339. [Google Scholar] [CrossRef]

- Fousteris, A.; Didaskalou, E.; Tsogas, M.-M.; Georgakellos, D. The Environmental Strategy of Businesses as an Option under Recession in Greece. Sustainability 2018, 10, 4399. [Google Scholar] [CrossRef] [Green Version]

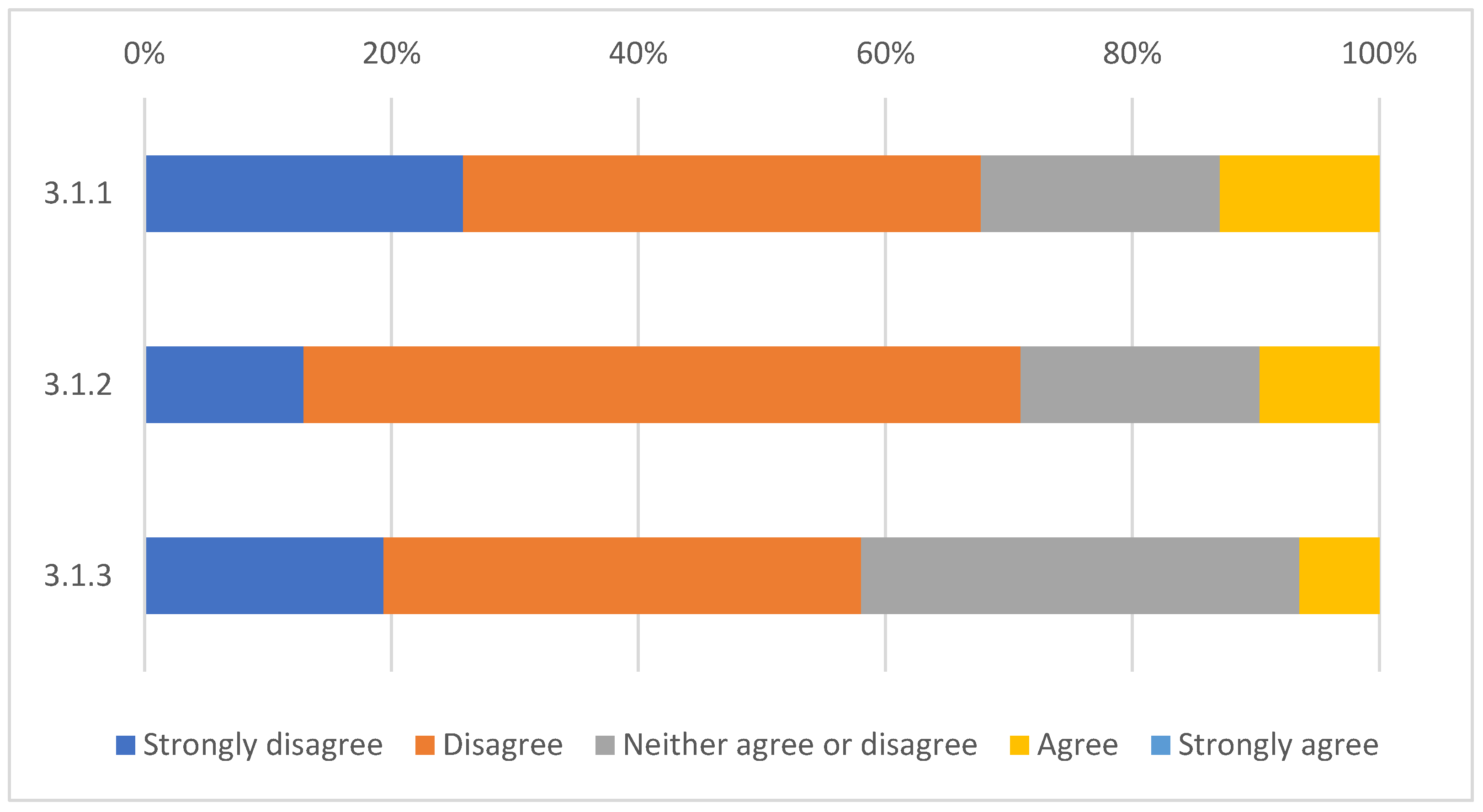

| Section 3.1 | Strongly Disagree | Disagree | Neither Agree nor Disagree | Agree | Strongly Agree |

|---|---|---|---|---|---|

| 3.1.1 The net profit margin of our organization increased. | 25.81% | 41.94% | 19.35% | 12.90% | 0.00% |

| 3.1.2 Profitability growth has been outstanding. | 12.90% | 58.06% | 19.35% | 9.68% | 0.00% |

| 3.1.3 Profitability has exceeded our competitors. | 19.35% | 38.71% | 35.48% | 6.45% | 0.00% |

| Section 3.2 | Strongly Disagree | Disagree | Neither Agree nor Disagree | Agree | Strongly Agree |

|---|---|---|---|---|---|

| 3.2.1 The company’s image has improved | 3.23% | 16.13% | 41.94% | 35.48% | 3.23% |

| 3.2.2 The customer satisfaction level is higher than that of competitors | 3.23% | 12.90% | 45.16% | 35.48% | 3.23% |

| 3.2.3 The employee satisfaction level is higher than that of competitors | 6.45% | 16.13% | 41.94% | 25.81% | 9.68% |

| 3.2.4 Ability to maintain a market presence in times of crisis is higher | 0.00% | 19.35% | 32.26% | 41.94% | 6.45% |

| 3.2.5 Sales have increased more than those of competitors | 3.23% | 32.26% | 48.39% | 16.13% | 0.00% |

| Variable | Questions | Reference |

|---|---|---|

| Social Pillar (SP) | [49] | |

| S.P 1 | Do you provide procedures that help ensure the health and safety of our employees? | |

| S.P 2 | Do you support your employees who wish to pursue further education? | |

| S.P 3 | Do you provide your employees with salaries that properly and fairly reward them for their work? | |

| S.P 4 | Do you treat all employees fairly and respectfully, regardless of gender or ethnic background? | |

| Environmental Pillar (ENP) | [49] | |

| ENP 1 | Have you adopted processes to reduce energy consumption? | |

| ENP 2 | Have you adopted processes to reduce and recycle waste? | |

| ENP 3 | Have you adopted processes to reduce water consumption? | |

| ENP 4 | Have you implemented systems to reduce harmful emissions? | |

| ENP 5 | Have you adopted systems to reduce packaging’s environmental effects? | |

| Economic Pillar (EP) | [49] | |

| EP 1 | Do you involve all suppliers in new products or services development? | |

| EP 2 | Do you inform all suppliers of products and services about organizational changes affecting purchasing decisions? | |

| EP 3 | Do you provide all customers with the information needed to make sound purchasing decisions? | |

| Βusiness management | ||

| Sustainable Business Performance (S.B.P) | [56] | |

| S.B.P 1 | The net profit margin of our organization increased. | |

| S.B.P 2 | Profitability growth has been outstanding. | |

| S.B.P 3 | Profitability has exceeded our competitors. | |

| Sustainable Competitive Advantage (SCA) | [48] | |

| S.C.A 1 | The company’s image has improved | |

| S.C.A 2 | Customer satisfaction level is higher than that of competitors | |

| S.C.A 3 | Employee satisfaction level is higher than that of competitors | |

| S.C.A 4 | Ability to maintain a market presence in times of crisis is higher | |

| S.C.A 5 | Sales have increased more than those of competitors | |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Bafas, S.A.; Alexandropoulou, A.P.; Fousteris, A.E.; Didaskalou, E.A.; Georgakellos, D.A. Sustainable Development and Business Strategies: An Exploratory Study of Greek Businesses. Businesses 2023, 3, 441-459. https://doi.org/10.3390/businesses3030027

Bafas SA, Alexandropoulou AP, Fousteris AE, Didaskalou EA, Georgakellos DA. Sustainable Development and Business Strategies: An Exploratory Study of Greek Businesses. Businesses. 2023; 3(3):441-459. https://doi.org/10.3390/businesses3030027

Chicago/Turabian StyleBafas, Spyridon A., Alexandra P. Alexandropoulou, Andreas E. Fousteris, Eleni A. Didaskalou, and Dimitrios A. Georgakellos. 2023. "Sustainable Development and Business Strategies: An Exploratory Study of Greek Businesses" Businesses 3, no. 3: 441-459. https://doi.org/10.3390/businesses3030027