1. Introduction

Technology-based innovations in the bio-economy are expected to provide new market opportunities for investments addressing resource depletion, food security or climate change [

1,

2]. The growing global demand for sustainable agribusiness presents areas of opportunities for investments in agro-industrial plants to produce bio-inputs such as bio-fertilizers and bio-pesticides made from microorganisms such as bacteria and fungi as they reduce farming costs and are considered eco-friendly [

3,

4].

Agricultural bio-inputs are deemed a strategic sector for investments worldwide [

5,

6,

7], and as a market opportunity for developing countries [

8,

9,

10,

11] that can participate in the bio-economy by investing in open-source biotechnology [

12] and in biotech alliances [

13]. The new bio-based technologies are seen as a path to value chain transformation while creating new business opportunities [

14]. Technological developments in the field of agricultural bio-inputs promise sustainable alternatives to replace synthetic fertilizers and pesticides [

6].

Agribusiness growing sectors that deploy locally available technology provide areas of opportunities for investments that build agro-industrial capabilities in developing countries [

15]. Developments in agricultural bio-inputs range from average technology used for isolating and reintroducing specific microorganisms to promote beneficial interactions with plants up to high-tech phytomicrobiome engineering based on gene transfer [

16]. Bio-input technologies have gone through continued technological developments [

17] made by private investments that often collaborate with public innovation centers [

18].

Agricultural bio-inputs gained initial market momentum by addressing demands from organic and agroecological farmers [

19] and its importance grew recently in conventional agriculture as an alternative for dealing with pests not controlled by chemical pesticides [

20] and also as an alternative for fertilizers whose prices grew given to the COVID-19 pandemic-related trade disturbances and the war in Ukraine [

21]. Agricultural bio-inputs market growth is also driven by increased demand for sustainable agriculture worldwide [

5]. However, in the agro-industrial regime based on the use of chemical inputs, bio-inputs still represent a niche market [

22].

The production of agricultural bio-inputs is seen as a strategic sector to foster new business models based on the bio-economy in developing countries such as Argentina [

23]. However, despite the profile of the few well-known companies producing bio-inputs, very little is known about the actual entrepreneurial ecosystem operating in the Argentinean market [

23,

24,

25,

26]. This study aims to explore how domestic entrepreneurs have benefited from the thriving market for agricultural bio-inputs by establishing themselves in this sector and also to learn lessons on areas of opportunity for agro-industrial growth in developing countries. Specifically, this study seeks to:

Characterize the agricultural bio-input sector in Argentina with a main focus on domestic companies;

Identify the conditions for domestic companies’ emergence in terms of capital invested, technological developments, support received and market strategies adopted;

Determine the main successful business models in agricultural bio-inputs considering the focus on market, innovation and industrial areas of expertise.

By determining the key factors in the success of domestic players building agro-industrial capabilities and resilience in developing countries, this paper adds new insight into how local agri-business firms can grow in domestic and international markets. The overall study aims to provide lessons to business establishment and development in the bio-input sector of the agriculture industry in Argentina and other developing countries.

2. Literature Review

Structural change towards a more sophisticated industrial and technological economy is considered a sine qua non condition for an emerging economy to converge with developed ones [

27]. A crucial challenge in developing countries is to build agro-industrial capabilities and resilience that go beyond the farming sector based on domestic investments in the industrial segments of the supply chains [

15,

28].

This challenge, certainly, ought to consider identifying the business arrangements most capable of absorbing the benefits of both domestic and foreign investments given the asymmetry in the levels of financial investments and technological developments between developed and developing nations [

29]. By investing in the agro-industrial sectors that better remunerate capital and labor, and going beyond the current focus on the primary production of commodities, developing countries can benefit from agribusiness expansion for their industrial development [

30,

31].

The growing demand for bio-inputs represents an opportunity for investments by domestic companies in developing countries. Agricultural bio-inputs are seen as the most relevant impulse for the development of bio-based technologies, with which developing countries can rely on their scientific–technological and business capacities to become technology developers, producers and exporters in sectors such as bio-based pest control [

24]. Contextual local aspects can underpin entrepreneurship and innovation management [

32].

However, agricultural bio-inputs is a sector where global corporations also have stakes. For example, the global bio-based leading company Koppert is already established in Argentina via Nitrasoil Argentina. Also, the traditional agrochemical global giants have begun to venture into the production of bio-inputs, relying on a range of strategies that encompass alliances with or the acquisition of local companies and the use of bio-inputs combined with their conventional agrochemical package as a marketing strategy [

24]. For example, Syngenta now markets bio-inputs for treating seeds produced by the Argentinean Rizobacter. With this global move by multinational corporations into the bio-inputs market (

Table 1), domestic companies face growing competition.

Technological development is a key issue to be addressed by local companies to become competitive in the bio-economy growing market [

1]. Argentina has a long trajectory in terms of the adoption of bio-inputs, but largely limited to the incorporation of bacterial-based inoculants for nitrogen fixation in soybean crops. Only recently companies started investing in more sophisticated products such as bio-fertilizers and bio fungicides as well as in new business models that attract foreign investors [

23]. The agro-industrial sector in Argentina traditionally invests more in improving industrial processes than in the development of new products [

24,

34].

The development of an entrepreneurial ecosystem as part of a global value chain requires the presence of framework conditions, which allow firms to improve their processes and upgrade their products [

35]. The establishment of domestic industrial clusters can benefit from government support to private ventures to improve technological transformation [

36,

37,

38]. Policies can also increase the distributional effects of bio-based innovation among value chain members and prevent market concentration [

14,

24].

Argentina is an upper middle-income country with a dynamic agricultural sector that has been making a growing contribution to the countries’ Gross Domestic Product (GDP), from 4.7% of the GDP in 2000 to 5.9% in 2020 [

39]. Argentina is one of the world’s largest agricultural exporters, and agro-food exports have been growing significantly in recent decades, representing 41% of total exports in 2000, and 61% in 2020. The agricultural production units range from basic and traditional production forms to complex business ventures that use sophisticated technology, in particular digital and biotechnology applications. The Argentine Agricultural Bio-inputs Program (PROBIAAR) was created in 2021 to promote, encourage and strengthen the bio-inputs sector [

39].

Progress in the agricultural bio-inputs sector is also reported in other developing countries [

6,

7,

8,

9,

10,

11,

12], particularly in Brazil which also has a large number of companies with bio-inputs registered for agricultural use [

20]. By December 2022 in Argentina, a total of 123 companies had registered 824 inoculants or bio-fertilizers and 22 companies had registered 39 products for plant therapeutics, adding up to 131 companies in total since some companies had both types of products [

37,

38]. In Brazil, a total of 45 companies had registered 436 inoculants and bio-fertilizers and 114 companies had registered 546 bio-pesticides by December 2022, adding up to 137 companies with agricultural bio-inputs registered since some companies had both types of products [

40].

Reducing the use of synthetic agricultural inputs has become a goal shared by several countries due to the negative impacts that agrochemicals have on the environment and human health [

41]. Bio-inputs are one of the main potential alternatives to agrochemicals whenever technological developments provide solutions that can replace synthetic fertilizers, pesticides and herbicides. Agricultural bio-inputs are biological products developed from enzymes, extracts (from plants or microorganisms), microorganisms, macroorganisms (invertebrates) and secondary metabolites, which are intended for nutrition, biological control and biotic and abiotic stress relief [

42].

3. Materials and Methods

To explore how developing countries can build country agro-industrial capabilities that go beyond farming, we conducted a case study of domestic companies in Argentina giving the country’s large domestic market for agricultural inputs. We used data published online by the Argentinean National Service for Agrifood Health and Quality (Servicio Nacional de Sanidad y Calidad Agroalimentaria—SENASA) that lists the companies with agricultural products registered in Argentina. The study encompassed two complementary data basis, which are the list of fertilizers (Registro de Productos fertilizantes, enmiendas y otros) [

37] and the list of pesticides (Registro nacional de terapéutica vegetal) [

38]. For the first data basis, we selected all companies that registered bio-fertilizers under the titles biological amendment (enmienda biológica) and biological fertilizer (fertilizante biológico). For the second data basis, we selected all companies that registered bio-pesticides based on bacteria, fungi or viruses. Companies that had both bio-fertilizers and bio-pesticide products (i.e., were listed in both databases) were not counted twice but only once.

These two lists add up to 131 companies since 124 companies registered bio-fertilizers, 22 companies registered bio-pesticides and 15 companies registered both types of products. Out of the 131 companies, 101 are listed as being from Argentina by the classification made by SENASA. Foreign multinational corporations with branch offices in Argentina were excluded, which resulted in 97 Argentinean companies. We then searched online for the 97 Argentinean companies and found that 78 of them were operational in 2022 and had a website, social media or Unique Tax Identification Code (CUIT) with basic information about the companies, while the other companies had no such information available. From the companies’ websites and CUIT, we collected initial information such as the creation date and types of products as well as e-mail or WhatsApp contacts.

We contacted all the 78 operational Argentinean companies by e-mail and/or WhatsApp and 14 of them replied and agreed to take part in the study. We interviewed small-, medium- and large-size companies as case studies. We classified as small companies those with only one product registered by SENASA, while medium companies were the ones with two to nine products registered and large companies as the ones with more than ten products. We only conducted interviews with companies that already have products registered by SENASA.

Interviews were conducted between October 2022 and January 2023 with representatives of fourteen companies (

Table 2), eight of which were in person and included a visit to the companies’ facilities and six were via online video calls. Interviewees were informed that the interviews would not be recorded nor their names would be made available. All interviewees provided informed consent when taking part in the survey, following Argentina’s ethics protocols for research with human beings. The interview protocol addressed five topics: 1. The characteristics of the bio-inputs marketed by the company, 2. The development process for their products, 3. The companies’ commercial strategy, 4. The origin of the capital invested in the company and 5. The current volume of production and markets accessed (

Appendix A).

A principal component analysis was performed to determine the main business models among the studied companies. For such, we used the 15 variables of the survey that represent measurements that are either ordinal or scalar. The scalar variables measured the levels of research and development components given by the number of researchers in the companies’ team; the number of salespeople working in the company; the sales volume per year in L; the year the company began to work with bio-inputs; the company’s expectations to grow in sales in the next year; the number of products the companies had approved by SENASA market by 2022 and the number of bio-inputs as informed in the interview.

For the ordinal variables, the level of industrial development was given by the installed infrastructure ranging from 0 for companies with no industry, 1 for companies with small industrial plants, 2 for companies with average industrial plants with homemade bioreactors, 3 for complete industrial plants with industrial bioreactors plus packing equipment to 4 for complete industry plus laboratory for tests. The coverage of companies’ sales ranged from 1 for local markets in the province the company is based plus neighbor provinces, 2 for nationwide markets, 3 for regional markets including Argentina and neighboring countries to 4 for international markets beyond South America. The level of technological development of the main commercial product as well as of the other secondary bio-inputs ranged from 1 Enmienda (liquid roundworm humus), 2 Inoculant, 3 Bio-fertilizer to 4 Bio-pesticide. The technological development of the products considering the microorganisms used either individually or in pools ranged from 0 no microorganism, 1 not isolated microorganism, 2 isolated microorganisms, 3 pools of isolated microorganisms to 4 bacteria plus fungi or non-conventional organisms. The focus on bio-inputs was given by the percentage of bio-inputs’ sales in comparison with chemical products ranging from 1% to 100% and the level of production of bio-inputs to other companies was given by the percentage of industrial production provided to other companies as “white label products” ranging from 0% to 100%. The types of products which register in Senasa included 1 for bio-fertilizer, 2 for bio-pesticide (terapeutica vegetal) and 3 for bio-fertilizer and bio-pesticide. The principal component analysis (PCA) was performed by FactoMineR, FactoExtra and corrplot packages of the R software version 4.3.1 [

43].

4. Results

4.1. Description of the Sector

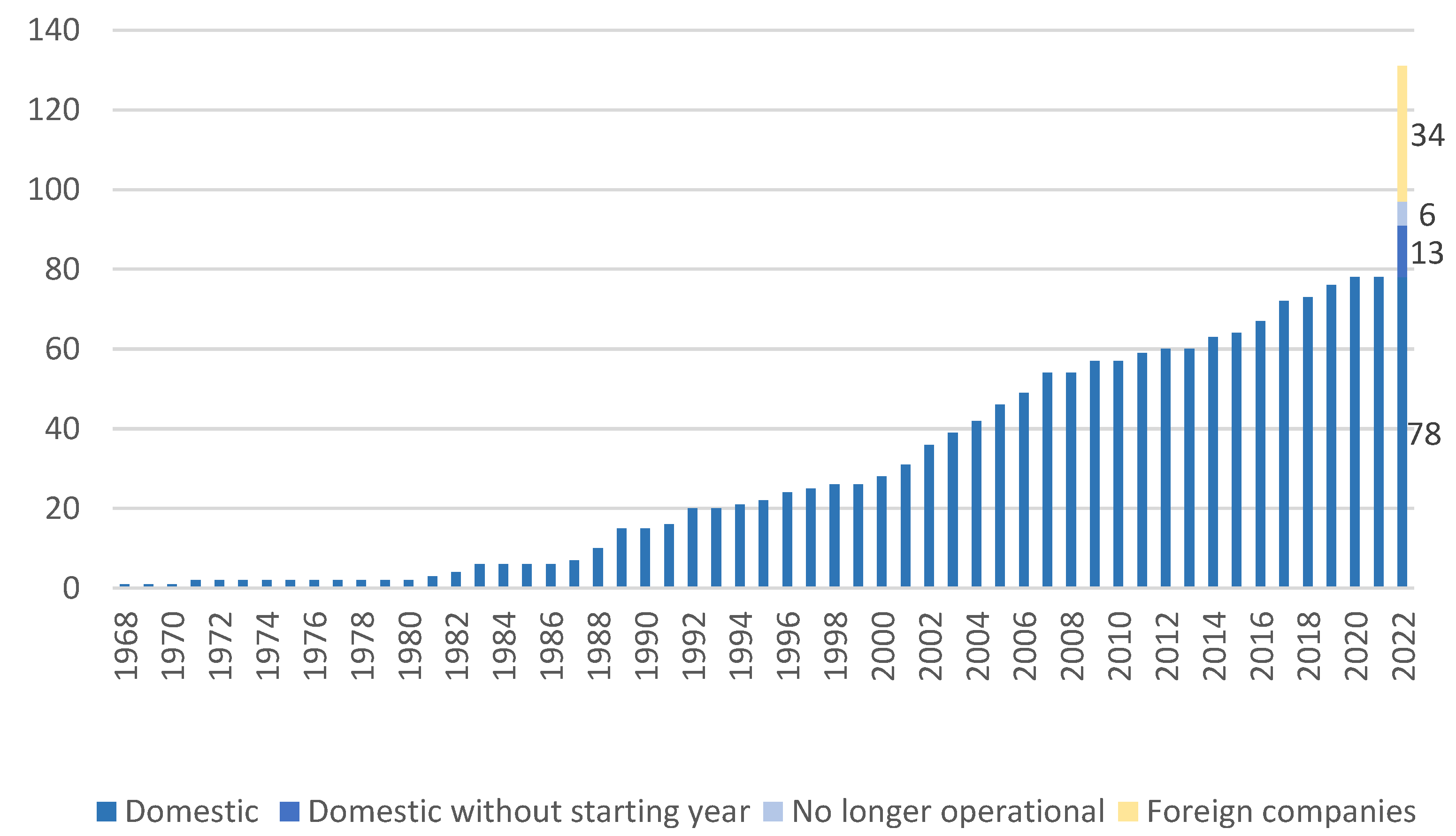

By the end of 2022, there were 131 agricultural bio-input companies with products registered in Argentina, of which 97 (74%) were domestic since their owners and investors were mainly from Argentina. In comparison, the sector of chemical fertilizers in Argentina had only 33.8% of domestic companies among the ones with products approved by SENASA by 2022. Out of the 97 domestic companies, 78 had their information such as postal address and e-mail address publicly available online, 13 did not have such information available and 6 were no longer operational by 2022 (

Figure 1). Out of the 78 domestic companies with an identified address, 42.7% were based in the Province of Buenos Aires, 30.2% in the Province of Santa Fé, 17.7% in the Province of Córdoba and the others in other provinces. The set of Argentinean companies had a total of 714 (684 bio-fertilizers and 30 bio-pesticides) products approved by SENASA as of 2022, which represented 84.3% of the 847 products approved by both domestic and foreign companies (808 bio-fertilizers and 39 bio-pesticides). Out of the 97 domestic companies, 82 only have bio-fertilizers, 3 only have bio-pesticides and 12 have both bio-fertilizers and bio-pesticides as products registered by SENASA.

There were 22 companies (19 of which were listed by SENASA as Argentinean) that registered ten or more bio-inputs in SENASA, with the leading ones being Rizobacter (part of the Argentina-born holding Bioceres Crop Solutions), Nitrasoil (part of the Dutch group Koppert) and Novozymes (a Danish company), which registered 142, 49 and 43 products, respectively. Among all, the sample group for interviews included Rizobacter, Fragraria and Prodinsa, which had 142, 17 and 10 products registered by the end of 2022, respectively. There were 63 other companies (45 of which were listed by SENASA as Argentinean) that registered from 2 to 9 products. Among these, the sample group included Microvidas, Desarrollos Biotecnologicos/Summabio, Terragene/Protergium, Grin Roberto/Mycophos, Ceres Demeter, Induagro, Formulagro, Tropfen and Bionet with 9, 7, 5, 4, 4, 3, 3, 3 and 3 products, respectively. Finally, the list included 66 companies (45 of which were listed as Argentinean) with 1 product registered. In this group, our sample included Braem Conrado Manuel/FFO and Sociedad Agropecuaria de Productos Humicos S.R.L./Hampi.

The search on the companies’ website revealed that many domestic companies began their operations decades ago, but some cases started recently.

Figure 1 shows in dark blue bars the cumulative number of domestic companies in the bio-inputs market in Argentina year by year based on the information provided on the companies’ website and CUIT register. For the year 2022, we also have the number of domestic companies without the date of creation as well as the number of companies that were not operational in 2022. The figure in this yellow last bar also shows the number of foreign companies with products registered by SENASA. Since a company takes around three years to have a product approved in Argentina, there is a time lapse between the registry of the company itself and its products by SENASA.

The interviewed experts reported that the first bio-input companies in Argentina were focused on the production of inoculants and grew in pace with the expansion of soybean plantations in the country. According to the experts, the early 2000s’ experienced the rapid growth of transgenic soybean seeds in Argentina which led to further expansion of the areas planted with soya. Responding to the growing demand for inoculants using the bacteria

Bradyrhizobium spp., the biological sector grew in Argentina, particularly after the creation in 2004 of the Inoculant Quality Control Network (REDCAI—Red de Control de Calidad de Inoculantes) that demonstrated the effectiveness of inoculation in soybeans in 80 field plots established nationwide. By 2022, according to the interviewed experts, Argentina had 20 million hectares planted with soybeans, 80% of which were inoculated. Particularly since 2017 companies started to develop other products beyond inoculants such as bio-fertilizers and bio fungicides, which resulted in the most recent wave of growth in the number of companies in the bio-inputs sector (

Figure 1). This development for large-scale crops went in parallel to the steadily growing demand for bio-inputs for organic and peri-urban farming where chemicals were not allowed.

4.2. Conditions for the Emergence

This section presents how the studied companies managed to mobilize capital to invest, the technological developments of their products and their market strategies.

4.2.1. Capital

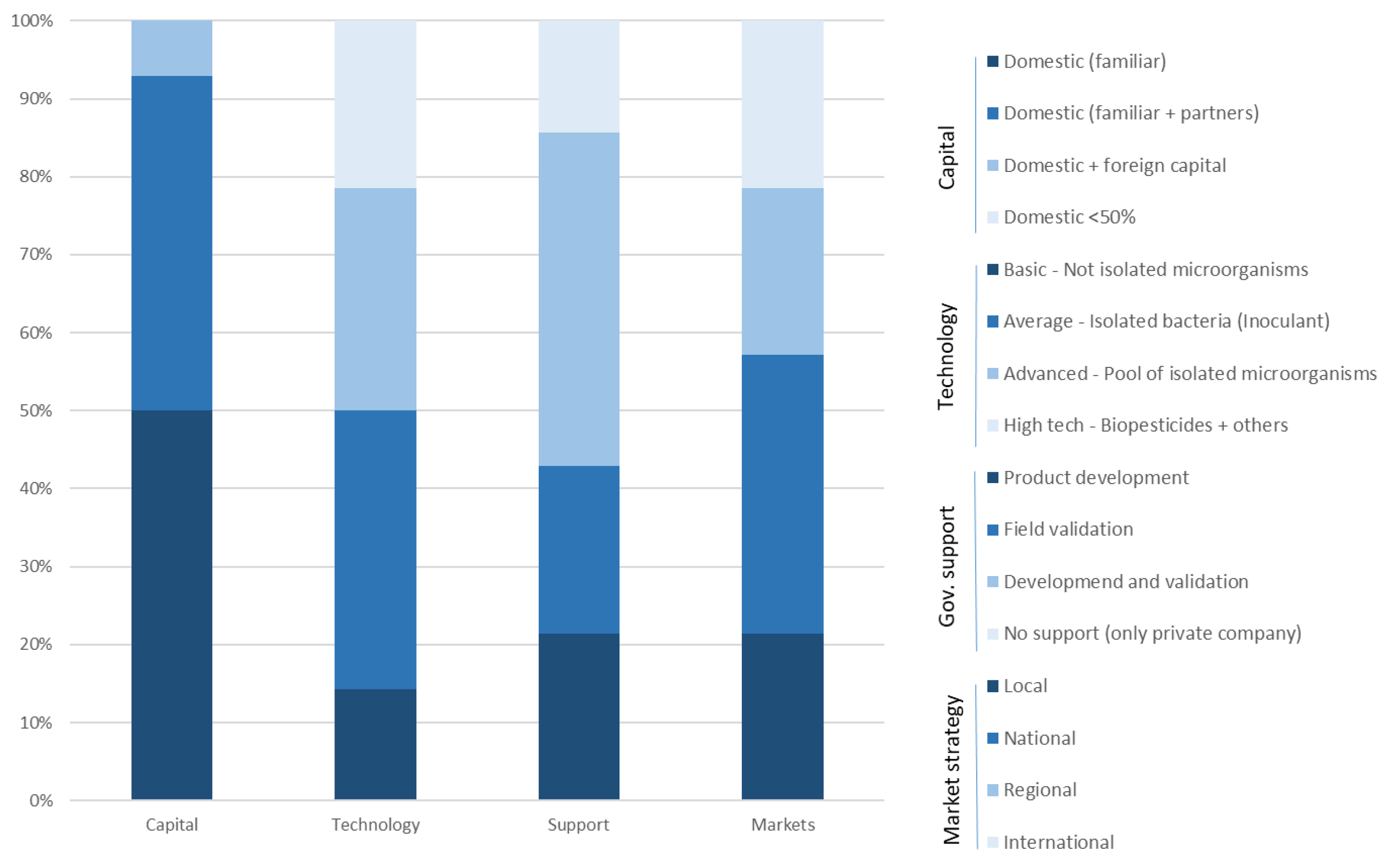

All interviewed companies began with private/family capital and most of them remain as family companies that grow mainly with revenues from the sale of their products. Some entrepreneurs invited local partners to invest in their company, which were often friends or colleagues (

Figure 2). Rizobacter is the only interviewed company that went public in Nastaq as part of the Bioceres Crop Solutions holding. Prodinsa mentioned plans to go public as a means to have resources to register products in foreign markets.

The assessed companies had little or no contribution to public policies or investments by the financial sector to establish themselves in the market. However, Prodinsa, Fragraria and Tropfen mentioned having accessed credits at some point. Governmental policies such as the Programa de Fomento del Uso de Bioinsumos Agropecuarios (PROFOBIO) and the Hub de Bioeconomia de Santa Fé were not mentioned by the interviewed people, but Microvidas mentioned to have received the Argentine Bio-product labels provided by the Argentine Agricultural Bio-inputs Program (PROBIAAR).

The main costs for starting in business include the development of the products, the office and industrial plant in some cases, the costs for having the product registered and the costs for marketing the products in the marketplace. The cost for registering a product in Argentina in 2022 was around USD 20 thousand since the whole process required three years of field tests with three different crops in different regions whose results were checked in the field by SENASA experts. However, there were cases of companies that began with small investments by marketing products developed, produced and registered by other companies or by registering and marketing only one to a few products. As detailed in the

Supplementary Material (File S1), two of the interviewed companies had no industrial plant, three had small to average plants and nine had complete industrial plants with bioreactors, packaging equipment and labs for testing their products.

4.2.2. Technology

Companies presented different technological developments for their products ranging from liquid roundworm humus which provide not-isolated microorganisms to fungicides based on a mix of selected and isolated bacteria and fungi (

Table 3,

Figure 2). While some companies were focused on conventional products such as inoculants made of conventional strains of single microorganisms (such as bacteria of the gender

Bradyrhizobium), other companies focused on cutting-edge products such as bio-fertilizers and bio fungicides using unconventional microorganisms (such as bacteria of the gender

Pseudomonas or

Bacillus and fungi of the gender

Trichoderma). Some companies mentioned also having products based on amino acids and proteins extracted from bacteria and products for livestock made of bacteria of the gender

Lactobacillus. On-going developments not yet in the market reported by companies included lyophilization processes to prepare solid instead of liquid bio-products and investments in molecular biology to produce recombinant proteins. No company reported to be developing bio herbicides or working with genetically modified organisms.

For example, FFO used a mix of non-isolated microorganisms, while Prodinsa and Fragraria were more focused inoculants based on isolated bacteria and were developing new products such as bio-fertilizers and bio-pesticides. Other companies such as Summabio prepared fertilizers based on pools of isolated bacteria and/or fungi while companies such as Ceres Demeter focused on bio fungicides and other products combining different organisms. Protergium focused on bio-fertilizers and bio-pesticides and was developing products based on molecular biology, whose active ingredients are recombinant proteins, which was seen by the company as a new generation of bio-inputs. Rizobacter is a global leader in inoculants and is now investing in bio fungicides/pesticides after the merger with the US-based Marrone Bio Innovations in 2022. The list of the principal commercial products for each company and the microorganisms used either individually or in pools are detailed in the

Supplementary Material (see type of main and secondary products and active ingredient).

Some characteristics of biological products lead to competitive advantages for local production. For example, there may be patents for the products but not for the microorganisms, a short storage period of six months in some cases, and the relatively small scale of the sales that limits large-scale production. Most companies use locally available inputs such as bacteria and fungi isolated by private companies or national research centers, although companies were working with imported inputs. The availability of local inputs reduces costs with imported raw materials and risks related to the variable dollar exchange rates. Industrial equipment (e.g., bioreactors) is also available in the local market manufactured by domestic companies.

4.2.3. Governmental Support

While private investments were fundamental for the development and validation of all products in all companies, most of the surveyed companies relied on some point of support provided by public innovation centers either at universities or research agencies such as the Instituto Nacional de Tecnología Agropecuaria (INTA) or the Consejo Nacional de Investigaciones Científicas y Técnicas (CONICET) (

Figure 2). The

Supplementary Material details the list of innovation centers every company collaborates with either for the development or for the field experiment for validation and registration of their products.

For developing their products, companies had support from different research and development (R&D) agencies. For example, FFO had support from the National University of Litoral (UNL) for the initial evaluations of the characteristics of their product, while Protergium had initial support from INTA Castellar in the supply of some strains of microorganisms. Chemical companies like Prodinsa and Fragraria also bought INTA strains to start with biological inoculants.

Support was also provided for field trials which were fundamental for validating the product for both register and commercial purposes. For example, Summabio and Mychophos developed their products but had partnerships with the National University of Cordoba (UNC) and the University of Rosario (UNR), respectively, for the validation of their products. Ceres Demeter had alliances with R&D agencies as part of its business model, and a long-term collaboration with the National University of Río Cuarto. Rizobacter used strains developed by INTA in their two leading commercial products (the inoculant Rizoliq and the bio fungicide Rizoderma) and collaborated with 22 public and private organizations for field validations.

4.2.4. Market Strategies

Companies adopted different strategies to explore distinct market niches. All interviewed companies mentioned that although the market for bio-inputs is much smaller than that of chemical inputs, the profit margins in bio-inputs were greater given to smaller competition in this segment. The market for agrochemicals in Argentina in 2022 was estimated at USD 3 billion while the bio-input companies estimate their market at USD 100 million per year, according to the interviewed experts. While the market for chemicals was expected to grow 2% per year in sales, the bio-inputs companies expect their market to grow 15% a year in the coming years.

Some of the companies were focused on markets of the provinces where they were located and neighboring provinces, while others tended to cover the whole country benefiting from the fact that the products are approved to be used nationwide in Argentina. Some companies also registered products in neighboring countries such as Paraguay, Uruguay, Bolivia and Brazil while a few became international and already sold in North America and Europe (

Figure 2). Companies exporting bio-inputs from Argentina benefit from favorable exchange rates since most of their costs were in local currency while their revenues for exported products were in US dollars.

Market strategies also varied in terms of the crops the products were directed to. Some companies had products for fruits and vegetables such as grapes and strawberries, targeting the demand for bio-inputs for organic farming and for peri-urban areas where synthetic chemical products were banned (locally known as cultivos intensivos), while other companies focused on large-scale farming of crops such as soybeans, wheat and corn (locally known as cultivos extensivos). Summabio, FFO, Hampi and Microvidas mentioned focusing on both small-scale (intensivos) and large-scale (extensivos) crops, while the other companies were mainly focused on large-scale crops.

Differences were also found in terms of companies focusing solely on bio-inputs, while others marketing both bio and synthetic chemical products as a strategy to reduce marketing costs. Finally, while some companies were focused on products such as inoculants, others invested in new products such as bio-fertilizers and packs of different products to increase their profit margin. Detailed information on companies’ market strategies is provided in the

supplementary material. The next section explores how these different strategies result in alternative business models.

4.3. Business Models

Based on the interviews and visits in situ, different business models were identified related to the pipeline of products’ development phases, with some companies focusing on research and development of new products, others on industrial production and others on establishing a marketing network to sell bio-inputs either directly to farmers or via supply stores (

Figure 3). This creates a scenario of companies accessing different market niches and in many cases collaborating with each other such as in the case of companies developing and manufacturing products to be sold to other companies that are market experts (these companies manufacturing products sold by others under their own commercial name are locally known as fasón).

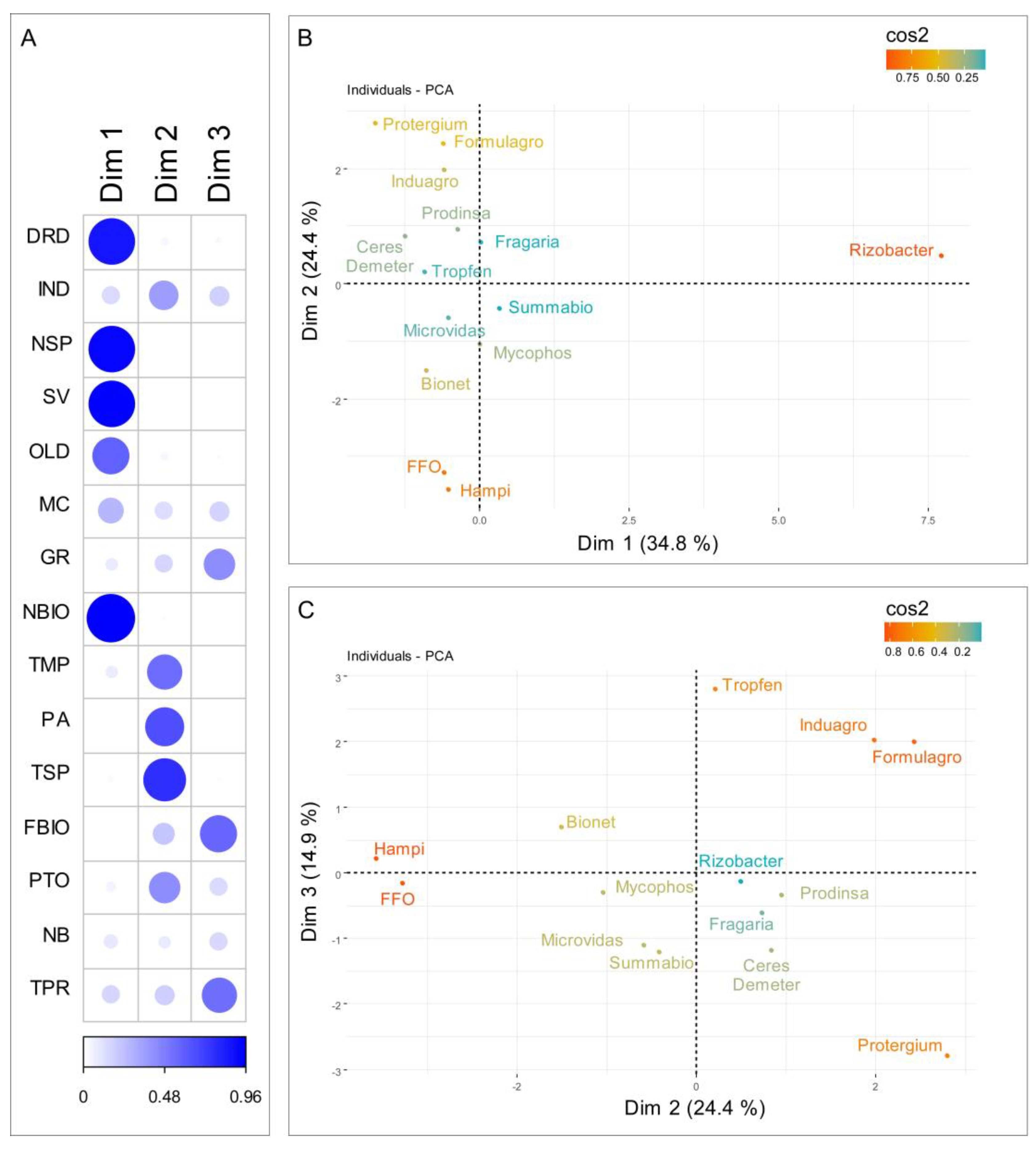

The principal component analysis comprehensively characterized the set of bio-input companies and identified patterns and relationships between the variables that describe these companies (

Figure 4). The first principal component (Dim 1) explained 34.8% of the total variability (

Figure 4B) and it was highly correlated to the high number of products registered (NBIO), the number of salespeople working in the company (NSP), sales volume per year (SV) and the number of researchers in the company’s team (DRD), those variables with bigger blue circles in

Figure 4A. The second principal component (Dim 2) explains 24.4% of the variability and it was correlated to the type of main product (TMP), active ingredient (PA) and type of sec product (TSP) variables. The third principal component (Dim 3,

Figure 4C) explains 14.9% of the total variability and it was correlated to focus on biological products, (FBIO), type of products with register in SENASA (TPR), and the company’s expectations to grow in sales in the next year (GR).

The interpretation of the PCA allows us to define different business models for these companies. The biplot Dim1 vs. Dim 2 shows Rizobacter, Fragraria and Summabio and to a lesser extent Prodinsa, Formulagro and Induagro as large-scale industrial production. Characteristically, these companies produced bio-inputs for themselves (to be sold with their brand) and also provided “white label” products to other companies interested in having bio-inputs in their portfolio of products. They have a higher number of salespeople, volume of sold and number of different products in their portfolio.

Both biplots (

Figure 4B,C) show that some companies such as Protergium and Ceres Demeter were focused on

product development. Characteristically, these companies had relatively more complex products (TSP) and active ingredients (PA) as reflected by the projection of Dim 2. Protergium had a strong laboratory arm to develop its own technologies while Ceres Demeter worked in close collaboration with public innovation centers (at universities and research agencies) for the joint development of products. In both cases, these companies were solely focused on bio-inputs (had no chemical products in their portfolio) and their products were provided to other companies with a strong commercial strategy to reach out to farmers.

There were all-encompassing companies such as Hampi, FFO, Bionet, Microvidas and Mycophos. Characteristically, these were companies solely focused on bio-inputs that developed, produced and marketed their products using their salespeople to market either directly to farmers or through supply stores. Some were small companies, with a smaller number of products (for example, Hampi and FFO had only one product in their portfolio), operating in local markets. Others such as Microvidas and Mycophos had a relatively larger number of products and a larger industrial component. None of these companies produced “white label” products for other companies.

Finally, the fourth identified business model was adopted by Tropfen and less extended by Bionet which was focused on resale. Characteristically, these companies did not have an R&D component nor an industrial plant for producing bio-inputs but had strong commercial sectors with a relatively high number of salespeople in comparison with other areas. Based on clients’ demands, they contracted other companies with industrial plants to produce bio-inputs to be sold with their label (private label). They often worked with both bio-inputs and synthetic chemical products and included packs of different and complementary products in their portfolio. While some companies had their own hired personnel for marketing their products, others had independent salespeople who earned a commission on the sold products.

5. Discussion

By going beyond the current focus on the primary production of commodities, developing countries can benefit from agribusiness expansion for their development [

30]. Agricultural bio-inputs is a growing technology-based economic sector that represents an opportunity for investments in agro-industrial development that remunerates capital and labor better than agricultural primary production [

24,

31].

This study revealed that domestic companies play an important role in the agricultural bio-inputs sector, different from other agro-industrial sectors such as agrochemicals that are largely controlled by foreign multinational corporations [

15,

23]. Results show that the technology and industrial processes used for preparing bio-inputs are to a large extent affordable and mastered by domestic companies established in the context of Argentina and other developing countries [

30].

Characteristically, agricultural bio-inputs is a sector deploying average and open source technology based on living microorganisms in which the entry of domestic companies is not prevented by property rights such as in patents of chemical molecules [

12,

17]. Studied companies isolate and reintroduce specific microorganisms but we found no case of companies deploying cutting-edge and subject to patent technologies such as phytomicrobiome engineering [

16].

This study revealed that small-to-large domestic companies consolidated in the bio-inputs sector in Argentina competing with multinational corporations. Much of this achievement by domestic companies was due to private entrepreneurship that benefited from collaborations with local public innovation centers, as also revealed in other studies [

24,

25]. As a key contextual aspect in Argentina, public innovation centers such as universities or dedicated research agencies licensed innovations that allowed local private companies to first venture into the agricultural bio-inputs business. Companies’ market strategies included cases of pure bio-inputs companies as well as cases where biological and chemical technologies became an integrated business model, as also highlighted elsewhere [

22].

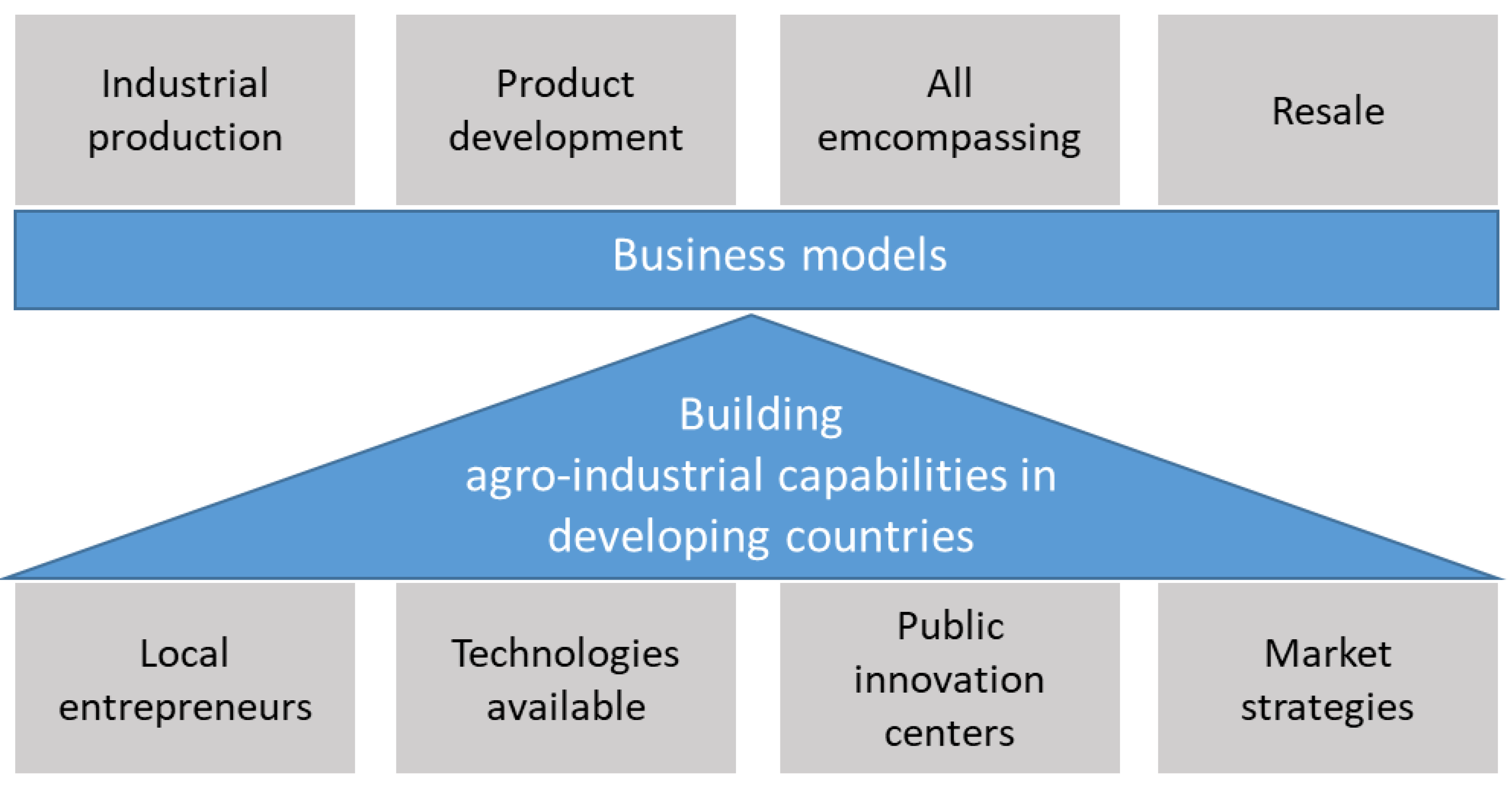

In summary, contextual aspects that favored domestic companies in the agricultural bio-inputs sector were private investments made by local entrepreneurs, the use of locally available technologies, support from public innovation centers and assertive market strategies (

Figure 5). Whenever these aspects are present, they can potentially underpin the development of agro-industrial capabilities in developing countries, although the impacts are sometimes limited to the agro-industrial sectors domestic companies are more competitive such as in the case of bio-inputs not protected by patents.

However, the current success of domestic companies does not preclude future competition or acquisitions by large foreign corporations, which may lead to market concentration. Acceleration in the rate of bioeconomy innovation is associated with more vertically coordinated value chains, bigger companies with higher market shares, increasing knowledge-sharing among value chain members, and a leading role of firms with core research capabilities [

14].

Other experiences reveal that the long-term development of an entrepreneurial ecosystem requires the presence of framework contextual conditions which allow firms to improve product upgrading [

32,

35]. In some cases, the development of industrial clusters requires government support for technological innovations [

36] and to increase the distributional effects of bio-based innovation among value chain members [

14]. Investments made in science and technology tend to support the development of the supply chain as a whole, not only specific companies, generating win–win situations [

30].

6. Conclusions

This study found major statistics on the growing number of domestic companies in the agriculture bio-input business sector and analyzed different business models based on principal component analysis, including companies focusing on the R&D of new products, industrial production, marketing focus and comprehensive strategies. By determining the key factors in the success of domestic players, this paper adds new insights into how local agri-business firms in developing countries can grow in both domestic and international markets.

The characterization of the Argentinean technology-based industries of agricultural bio-inputs revealed 97 domestic companies (74% of the total number of companies in this sector in Argentina) which were operational by the year 2022. Most of these companies have been in the market for a relatively long time and all interviewed companies expected continued growth for the next years particularly with the growing demand for new products such as bio-fertilizers and bio-pesticides, besides the traditional demand for inoculants.

Contextual aspects that favored the emergence of domestic companies in Argentina included the fact that local entrepreneurs managed to obtain the necessary capital to start in business often from private/familiar sources and then grew organically, i.e., using revenues to reinvest in the company throughout the years, with some cases of companies that contracted credits from local banks. Rizobacter was the only interviewed company to go public as a means to attract foreign investments. Domestic companies used average technologies that were locally available (such as isolated strains of microorganisms) and counted on support from local innovation centers (from universities to R&D agencies) for the development and field trials (validation) of their products. Finally, companies developed different strategies to access market niches with attractive profit margins.

Taken together, these domestic companies built different business models for establishing themselves in the marketplace. While some companies developed a strong commercial component to reach out to farmers, others specialized in the development of new products (focused on innovation) and others invested in professional industrial plants for large-scale production of bio-inputs. The four main business models identified were companies focused on product development, industrial production, resale and all-encompassing business models, that in many cases, collaborated with each other.

The results of this study revealed areas of opportunities for domestic investments in cleaner agro-industrial sectors in developing countries that can benefit from dynamic economic segments such as agribusiness. By benefiting from these opportunities for investments in technology-based sectors, developing countries can go beyond the primary production of commodities and build agro-industrial capabilities. However, despite some initiatives, there is still little structured governmental support for agro-industrial development in developing countries such as Argentina.

Lessons from Argentina reveal that when local demand for agricultural bio-inputs is met by local entrepreneurs who can rely on support from innovation centers for initial technological developments and manage to develop assertive market strategies, this can result in an entrepreneurial ecosystem that can transform agricultural bio-inputs in an innovative area of opportunities for agro-industrial growth. These lessons can be useful for other developing countries with similar opportunities for investments in strategic bio-economy-related industrial sectors.

Author Contributions

G.d.S.M.—Conceptualization; Data curation; Formal analysis; Funding acquisition; Investigation; Methodology; Project administration; Resources; Validation; Visualization; Roles/Writing—original draft; Writing—review and editing. R.R.—Conceptualization; Data curation; Formal analysis; Investigation; Methodology; Supervision. G.R.R.—Conceptualization; Data curation; Formal analysis; Investigation; Methodology; Software; Supervision; Writing—review and editing. All authors have read and agreed to the published version of the manuscript.

Funding

This research received external funding from the Fundação de Apoio à Pesquisa do Distrito Federal (FAPDF), call DPG/UnB Nº 0004/2022, Programa de Bolsas de Pós-Doutorado no Exterior/FAPDF.

Institutional Review Board Statement

Not applicable since interviewees were informed that the interviews would not be recorded nor their names would be made available. All interviewees provided informed consent when taking part in the survey, following Argentina’s ethics protocols for research with human beings.

Informed Consent Statement

Informed consent was obtained from all subjects involved in the study.

Data Availability Statement

All the data used in this manuscript will be made available under request.

Conflicts of Interest

The authors declare no conflict of interest. The funders had no role in the design of the study; in the collection, analyses or interpretation of data; in the writing of the manuscript; or in the decision to publish the results.

Appendix A. Interview Protocol

Survey of bio-input companies—Questions for the personal visit

What are the company’s main products (or services) in the market today?

- ○

( ) biodefenses ( ) biofertilizers ( ) other _________

- ○

Name of the main commercial product ____________________

- ○

Active ingredients (name of fungi, bacteria, etc.)________

- ○

Main commercial application (e.g., disease control x soybean)_________

- ○

Comments____________

How has the development of these main products been?

- ○

Technological development (product creation)—( ) in the company, ( ) next to the research center _________ ( ) Other ____

- ○

Validation (field tests)—( ) in the company, ( ) next to the research center __________________ ( ) Other ____

- ○

Certification—( ) there is no ( ) certification. Name of the certifier ________

- ○

Comments_________

What is the company’s main commercial strategy?

- ○

( ) Direct sales to the producer

- ○

( ) Sold through input distributors

- ○

( ) Development of cutting-edge products for others (research and development)

- ○

( ) Other _____

- ○

Comments

What is the current composition of the company’s capital?

- ○

( ) 100% Argentinean with ( ) family control o ( ) control by local investors

- ○

( ) Mainly Argentine—Control by Argentine groups with investors from ( ) South America ( ) others

- ○

( ) Mainly foreign with investors from ( ) South America ( ) others

- ○

( ) 100% foreign from ( ) South America ( ) others

- ○

Comments___________

What is the current sales volume of your set of products and the growth perspective?

- ○

Current sales _________ ( ) Liters per year ( ) Other___

- ○

Over the next 2 years, they will continue ( ) increase ( ) maintain ( ) decrease a ___ %

- ○

Comments_________

Number of people in research

Number of people in sales

Local/national/international sales

References

- Wydra, S. Measuring innovation in the bioeconomy—Conceptual discussion and empirical experiences. Technol. Soc. 2020, 61, 101242. [Google Scholar] [CrossRef]

- Jiang, Y.; Li, K.; Chen, S.; Fu, X.; Feng, S.; Zhuang, Z. A sustainable agricultural supply chain considering substituting organic manure for chemical fertilizer. Sustain. Prod. Consum. 2022, 29, 432–446. [Google Scholar] [CrossRef]

- Prasad, R.D.; Poorna Chandrika, K.S.; Desai, S.; Greeshma, K.; Vijaykumar, S. Development, Production, and Storage of Trichoderma Formulations for Agricultural Applications. In Advances in Trichoderma Biology for Agricultural Applications; Springer International Publishing: Cham, Switzerland, 2022; pp. 371–385. [Google Scholar]

- Oguntuase, O.J. Advancing a Framework for Entrepreneurship Development in a Bioeconomy. In Handbook of Research on Nascent Entrepreneurship and Creating New Ventures; IGI Global: Hershey, PA, USA, 2021; pp. 295–315. [Google Scholar]

- Laibach, N.; Börner, J.; Bröring, S. Exploring the future of the bioeconomy: An expert-based scoping study examining key enabling technology fields with potential to foster the transition toward a bio-based economy. Technol. Soc. 2019, 58, 101118. [Google Scholar] [CrossRef]

- Lee, D.-H. Bio-based economies in Asia: Economic analysis of development of bio-based industry in China, India, Japan, Korea, Malaysia and Taiwan. Int. J. Hydrogen Energy 2016, 41, 4333–4346. [Google Scholar] [CrossRef]

- Ahn, M.J.; Hajela, A.; Akbar, M. High technology in emerging markets. Asia-Pac. J. Bus. Adm. 2012, 4, 23–41. [Google Scholar] [CrossRef]

- Russo, R.O.; Berlyn, G.P. Agricultural and forestry extension in biostimulants and bioinputs in Costa Rica: A short review/Extensión agrícola y forestal en bioestimulantes y bioinsumos en Costa Rica: Una breve reseña. Braz. J. Anim. Environ. Res. 2021, 4, 5290–5296. [Google Scholar] [CrossRef]

- López, M.D.R.; Vera, M.; Arias, M.I. Estrategia de CRM en el caso de las empresas colombianas de bioinsumos. Rev. Gestión Ambient. 2012, 15, 93–100. [Google Scholar]

- Lima, G.T.C.; Montezuma, M.A.A. Gestión sostenible para la producción de biofungicidas y fortalecimiento del sector de bioinsumos agrícolas venezolano. Enfoque UTE 2019, 10, 26–40. [Google Scholar] [CrossRef]

- Zambrano-Moreno, D.C.; Ramón-Rodríguez, L.F.; Strahlen-Pérez, V.; Bonilla-Buitrago, R.R. Industria de bioinsumos de uso agrícola en Colombia. Rev. UDCA Actual. Divulg. Científica 2015, 18, 59–67. [Google Scholar] [CrossRef]

- Adenle, A.A.; Sowe, S.K.; Parayil, G.; Aginam, O. Analysis of open source biotechnology in developing countries: An emerging framework for sustainable agriculture. Technol. Soc. 2012, 34, 256–269. [Google Scholar] [CrossRef]

- Szogs, A.; Wilson, L. A system of innovation?: Biomass digestion technology in Tanzania. Technol. Soc. 2008, 30, 94–103. [Google Scholar] [CrossRef]

- Mac Clay, P.; Sellare, J. Value chain transformations in the transition to a sustainable bioeconomy. SSRN Electron. J. 2022, 1, 1–34. [Google Scholar] [CrossRef]

- da Silva Medina, G.; Pokorny, B. Agro-industrial development: Lessons from Brazil. Land Use Policy 2022, 120, 106266. [Google Scholar] [CrossRef]

- Ke, J.; Wang, B.; Yoshikuni, Y. Microbiome Engineering: Synthetic Biology of Plant-Associated Microbiomes in Sustainable Agriculture. Trends Biotechnol. 2020, 39, 244–261. [Google Scholar] [CrossRef] [PubMed]

- Garcia, M.V.C.; Nogueira, M.A.; Hungria, M. Combining microorganisms in inoculants is agronomically important but industrially challenging: Case study of a composite inoculant containing Bradyrhizobium and Azospirillum for the soybean crop. AMB Express 2021, 11, 1–13. [Google Scholar] [CrossRef]

- Toruño, P.J.; Zuniga-Gonzalez, C.A.; Castellón, J.D.; Hernández-Rueda, M.J.; Gutierrez-Espinoza, E.I. Bioeconomia de las Universidades del CNU y sus senderos productivos. Rev. Iberoam. Bioecon. Cambio Clim. 2022, 8, 1929–1946. [Google Scholar] [CrossRef]

- Parewa, H.P.; Joshi, N.; Meena, V.S.; Joshi, S.; Choudhary, A.; Ram, M.; Meena, S.C.; Jain, L.K. Role of biofertilizers and biopesticides in organic farming. In Advances in Organic Farming; Elsevier: Amsterdam, The Netherlands, 2021; pp. 133–159. [Google Scholar]

- Meyer, M.C.; de Freitas Bueno, A.; Mazaro, S.M.; da Silva, J.C. Bioinsumos na Cultura da Soja; Embrapa Soja: Londrina, Brazil, 2022. [Google Scholar]

- Keswani, C.; Dilnashin, H.; Birla, H.; Singh, S.P. Obstacles in the Adaptation of Biopesticides in India. In Bio#Futures; Springer International Publishing: Cham, Switzerland, 2021; pp. 301–318. [Google Scholar]

- Goulet, F. Characterizing alignments in socio-technical transitions. Lessons from agricultural bio-inputs in Brazil. Technol. Soc. 2021, 65, 101580. [Google Scholar] [CrossRef]

- Bisang, R.; Trigo, E. Bioeconomía Argentina: Modelos de Negocios para una Nueva Matriz Productive; Bolsa de Cereales de Buenos Aires y Ministerio de Agroindustria de Argentina: Buenos Aires, Argentina, 2018. [Google Scholar]

- Starobinsky, G.; Monzón, J.; Di Marzo Broggi, E.; Braude, E. Bioinsumos para la Agricultura que Demandan Esfuerzos de Investigación y Desarrollo, 1st ed.; Ministerio de Desarrollo Productivo Argentina: Buenos Aires, Argentina, 2021. [Google Scholar]

- Sili, M.; Dürr, J. Bioeconomic Entrepreneurship and Key Factors of Development: Lessons from Argentina. Sustainability 2022, 14, 2447. [Google Scholar] [CrossRef]

- Goulet, F.; Hubert, M. Making a Place for Alternative Technologies: The Case of Agricultural Bio-Inputs in Argentina. Rev. Policy Res. 2020, 37, 535–555. [Google Scholar] [CrossRef]

- Bresser-Pereira, L.C.; Araújo, E.C.; Peres, S.C. An alternative to the middle-income trap. Struct. Chang. Econ. Dyn. 2019, 52, 294–312. [Google Scholar] [CrossRef]

- Kano, L.; Tsang, E.W.K.; Yeung, H.W.-C. Global value chains: A review of the multi-disciplinary literature. J. Int. Bus. Stud. 2020, 51, 577–622. [Google Scholar] [CrossRef]

- Economou, F. Economic freedom and asymmetric crisis effects on FDI inflows: The case of four South European economies. Res. Int. Bus. Financ. 2019, 49, 114–126. [Google Scholar] [CrossRef]

- Cruz, J.E.; Medina, G.d.S.; Júnior, J.R.d.O. Brazil’s Agribusiness Economic Miracle: Exploring Food Supply Chain Transformations for Promoting Win–Win Investments. Logistics 2022, 6, 23. [Google Scholar] [CrossRef]

- Wang, C.; Lu, Y. Can economic structural change and transition explain cross-country differences in innovative activity? Technol. Forecast. Soc. Chang. 2020, 159, 120194. [Google Scholar] [CrossRef]

- Dana, L.P.; Salamzadeh, A.; Ramadani, V.; Palalic, R. Understanding Contexts of Business in Western Asia: Land of bazaars and high-tech booms. World Sci. 2022, 4, 200. [Google Scholar]

- Olson, S. An Analysis of the Biopesticide Market Now and Where it is Going. Outlooks Pest Manag. 2015, 26, 203–206. [Google Scholar] [CrossRef]

- Leonardi, V.; Casal, I.G.; Cristiano, G. Desempeño innovador de un grupo de Mipymes agroindustriales argentinas. Econ. Soc. 2009, 14, 45–64. [Google Scholar]

- Reis, G.G.; Villar, E.G.; Gimenez, F.A.P.; Molento, C.F.M.; Ferri, P. The interplay of entrepreneurial ecosystems and global value chains: Insights from the cultivated meat entrepreneurial ecosystem of Singapore. Technol. Soc. 2022, 71, 102116. [Google Scholar] [CrossRef]

- Yin, Y.; Yan, M.; Zhan, Q. Crossing the valley of death: Network structure, government subsidies and innovation diffusion of industrial clusters. Technol. Soc. 2022, 71, 102119. [Google Scholar] [CrossRef]

- Senasa, “Registro de Productos Fertilizantes, Enmiendas y otros”, Servicio Nacional de Sanidad y Calidad Agroalimentaria-Dirección de Tecnología de la Información. 2023. Available online: https://aps2.senasa.gov.ar/vademecumFertilizantes/app/publico (accessed on 18 January 2023).

- Senasa, “Registro Nacional de Terapéutica Vegetal”, Servicio Nacional de Sanidad y Calidad Agroalimentaria-Dirección de Tecnología de la Información. 2023. Available online: https://aps2.senasa.gov.ar/vademecum/app/publico/formulados (accessed on 18 January 2023).

- OECD. Agricultural Policy Monitoring and Evaluation. 2022. Available online: https://www.oecd-ilibrary.org/sites/4e0e6eaf-en/index.html?itemId=/content/component/4e0e6eaf-en (accessed on 20 October 2023).

- MAPA. Agrofit-Sistema de Agrotóxicos Fitossanitários”. In MAPA (Ministério Da Agricultura Pecuária e Abastecimento); 2023. Available online: https://agrofit.agricultura.gov.br/agrofit_cons/principal_agrofit_cons (accessed on 20 October 2023).

- Jacquet, F.; Jeuffroy, M.H.; Jouan, J.; Le Cadre, E.; Litrico, I.; Malausa, T.; Reboud, X.; Huyghe, C. Pesticide-free agriculture as a new paradigm for research. Agron. Sustain. Dev. 2022, 42, 8. [Google Scholar] [CrossRef]

- Kaushik, B.D.; Kumar, D.; Shamim, M. (Eds.) Biofertilizers and Biopesticides in Sustainable Agriculture; Apple Academic Press: Palm Bay, FL, USA, 2019. [Google Scholar] [CrossRef]

- Core Team, R: A Language and Environment for Statistical Computing. 2023. Available online: http://www.r-project.org/ (accessed on 20 October 2023).

| Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}