The Russia-Ukraine Conflict: Its Implications for the Global Food Supply Chains

,

,  ,

,  ,

,  , ,

, ,  ,

,  ,

,  ,

,  ,

,  and

and

Abstract

:1. Introduction

2. Methodology

3. Results

3.1. Results of the e-Delphi

3.2. Results of the Review Synthesis

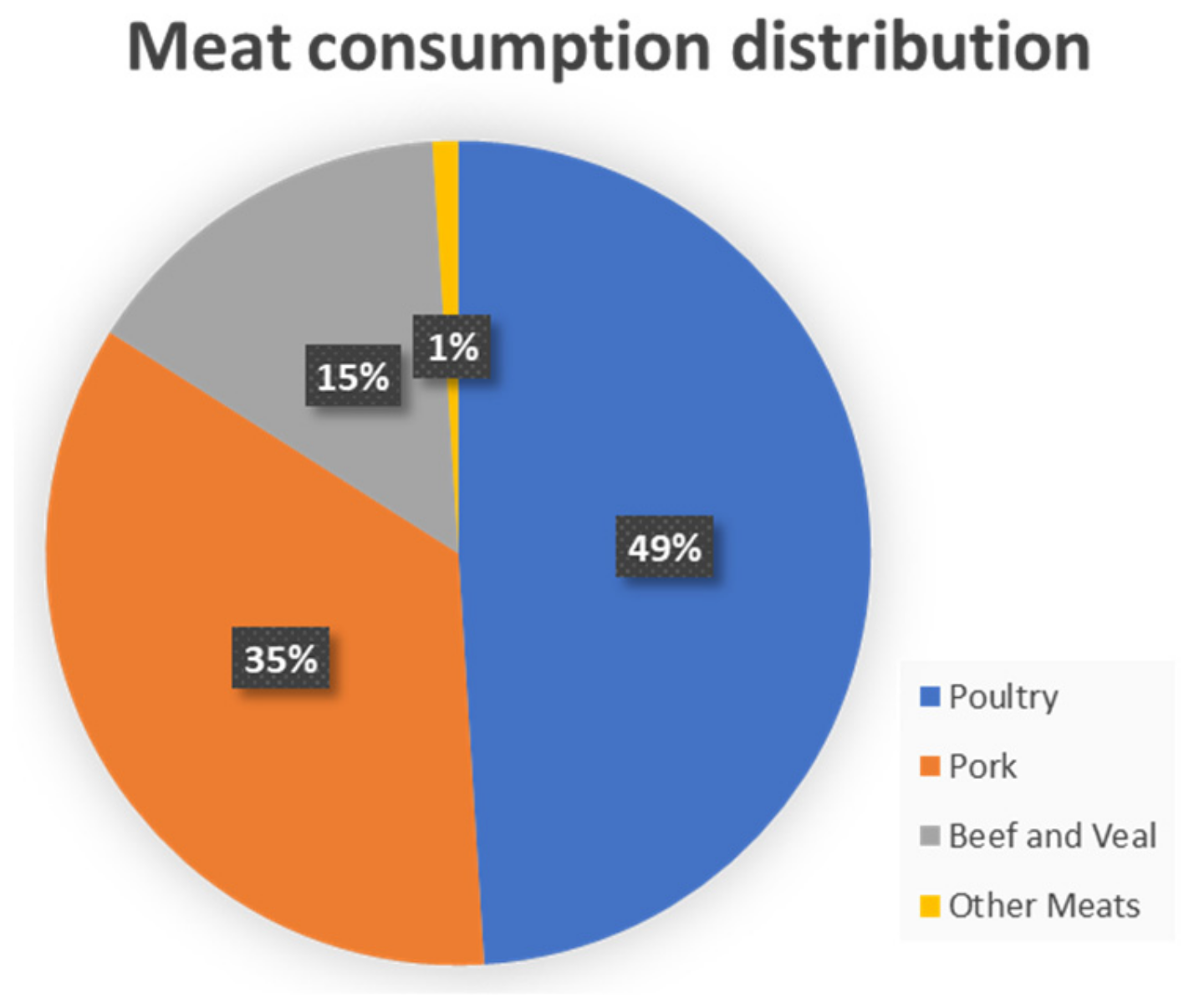

3.2.1. Impact on Food Production, Processing, and Storage

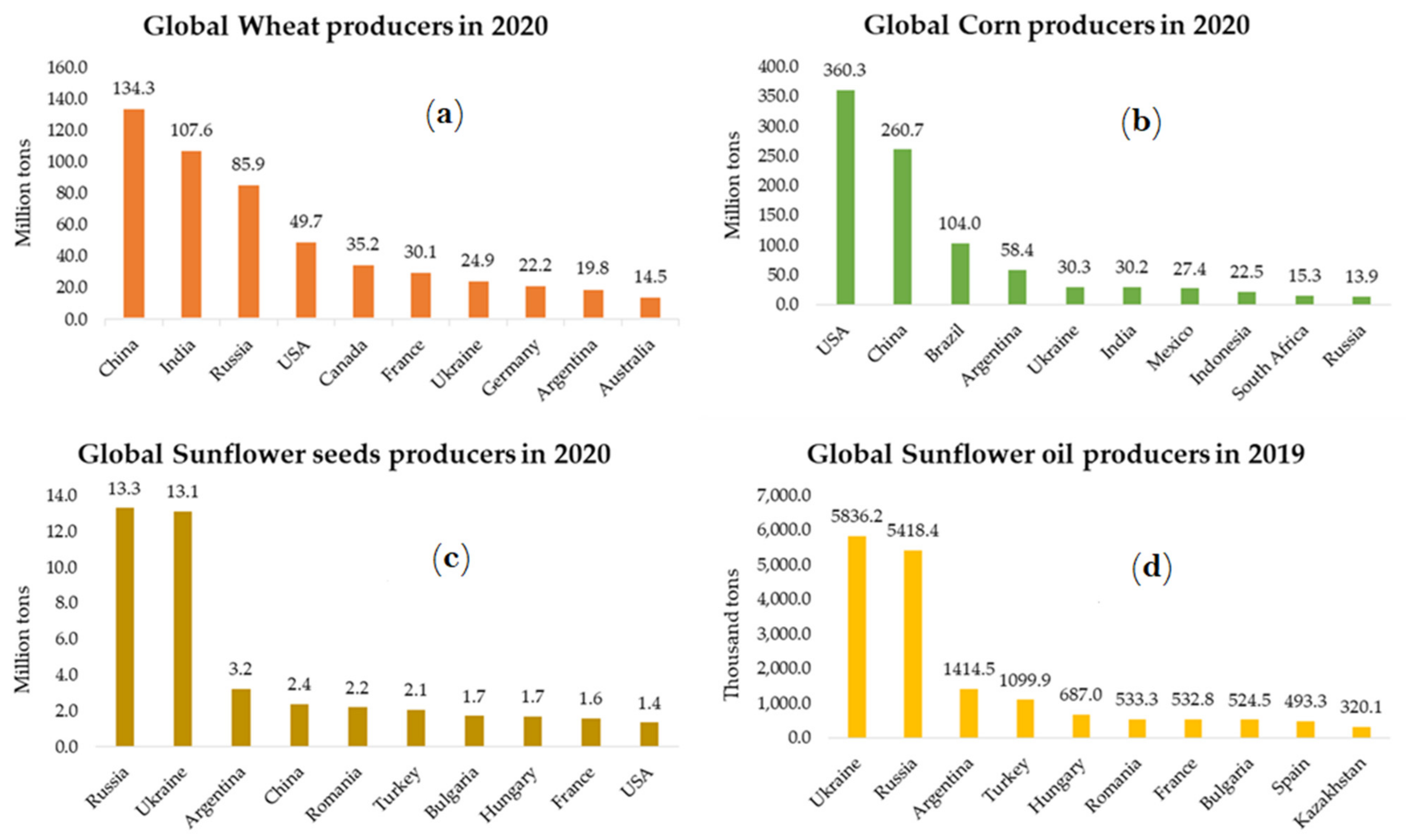

- Ukraine maize production is 2.6% of global production exporting Ukraine exports around 15% of the global maize and is 5th ranked behind USA, Argentina, and Brazil;

- Ukraine barley production is 4.9% of global production and it is the 2nd ranked global exporter behind France with 13.2% of the total world exports;

- Ukraine produces 29.1% of the global sunflower oil, and exports 44% of the global supply of sunflower oil. Ukraine is the largest exporter of sunflower seeds globally.

3.2.2. Impact on Food Transport Logistics

3.2.3. Impact on the Food Supply Markets

3.2.4. Impact on Consumer

3.2.5. Impact on Food Dependent Services

3.2.6. Impact on Food Quality

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Leon, D.A.; Jdanov, D.; Gerry, C.J.; Grigoriev, P.; Jasilionis, D.; McKee, M.; Meslé, F.; Penina, O.; Twigg, J.; Vallin, J.; et al. The Russian Invasion of Ukraine and Its Public Health Consequences. Lancet Reg. Health Eur. 2022, 15, 100358. [Google Scholar] [CrossRef] [PubMed]

- McKenna, M. The War in Ukraine Is Threatening the Breadbasket of Europe. Wired. 2022. Available online: https://www.wired.com/story/the-war-in-ukraine-is-threatening-the-breadbasket-of-europe/ (accessed on 2 May 2022).

- Horton, J.; Palumbo, D.; Bowler, T. Russia Sanctions: Can the World Cope without Its Oil and Gas? BBC News. 2022. Available online: https://www.bbc.co.uk/news/58888451 (accessed on 2 May 2022).

- Borrell, J. Food Insecurity: The Time to Act Is Now. Available online: https://www.eeas.europa.eu/eeas/food-insecurity-time-act-now_en (accessed on 2 May 2022).

- Timmer, C.P. Reflections on Food Crises Past. Food Policy 2010, 35, 1–11. [Google Scholar] [CrossRef]

- Anderson, J.D.; Mitchell, J.L.; Maples, J.G. Invited Review: Lessons from the COVID-19 Pandemic for Food Supply Chains. Appl. Anim. Sci. 2021, 37, 738–747. [Google Scholar] [CrossRef]

- Welsh, C. The Russia-Ukraine War and Global Food Security: A Seven-Week Assessment, and the Way Forward for Policymakers. CSIS. 2022. Available online: https://www.csis.org/analysis/russia-ukraine-war-and-global-food-security-seven-week-assessment-and-way-forward#:~:text=Food%20price%20increases%20due%20to,percent%20of%20their%20wheat%20imports (accessed on 2 May 2022).

- Godin, K.; Stapleton, J.; Kirkpatrick, S.I.; Hanning, R.M.; Leatherdale, S.T. Applying Systematic Review Search Methods to the Grey Literature: A Case Study Examining Guidelines for School-Based Breakfast Programs in Canada. Syst. Rev. 2015, 4, 138. [Google Scholar] [CrossRef] [Green Version]

- Higgins, J.; Green, S. Cochrane Handbook for Systematic Reviews of Interventions; Version 5.1.0.; The Cochrane Collaboration: Chichester, UK, 2011. [Google Scholar]

- Moher, D.; Liberati, A.; Tetzlaff, J.; Altman, D.G.; PRISMA Group. Preferred Reporting Items for Systematic Reviews and Meta-Analyses: The PRISMA Statement. Ann. Intern. Med. 2009, 151, 264–269. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Trollman, H.; Colwill, J. The Imperative of Embedding Sustainability in Business: A Model for Transformational Sustainable Development. Sustain. Dev. 2021, 29, 974–986. [Google Scholar] [CrossRef]

- Liu, S.; Li, Y.; Fu, S.; Liu, X.; Liu, T.; Fan, H.; Cao, C. Establishing a Multidisciplinary Framework for an Emergency Food Supply System Using a Modified Delphi Approach. Foods 2022, 11, 1054. [Google Scholar] [CrossRef]

- FAO. Note on the Impact of the War on Food Security in Ukraine; FAO: Rome, Italy, 2022. [Google Scholar]

- World Data Center. Ukraine: Agricultural Overview. Available online: http://wdc.org.ua/en/node/29 (accessed on 10 May 2022).

- Barklie, G. The Impact of the Russia-Ukraine Conflict on Trade. Available online: https://www.investmentmonitor.ai/special-focus/ukraine-crisis/ukraine-russia-conflict-impact-trade (accessed on 10 May 2022).

- The World Bank. Agriculture, Forestry, and Fishing, Value Added (% of GDP)—Ukraine. Available online: https://data.worldbank.org/indicator/NV.AGR.TOTL.ZS?locations=UA (accessed on 10 May 2022).

- Traspaderne, M. Sacar Adelante sus Cosechas, el Reto de los Agricultores Ucranianos. Heraldo. 2022. Available online: https://www.heraldo.es/noticias/internacional/2022/03/31/reto-agricultores-ucraniano-sacar-adelante-sus-cosechas-1563930.html (accessed on 10 May 2022).

- Bentley, A. Broken Bread—Avert Global Wheat Crisis Caused by Invasion of Ukraine. Nature 2022, 603, 551. [Google Scholar] [CrossRef]

- Ritchie, H. How Could the War in Ukraine Impact Global Food Supplies? Our World in Data. 2022. Available online: https://ourworldindata.org/ukraine-russia-food (accessed on 10 May 2022).

- Lainez Andrés, M. Una Primera Aproximación del Impacto de la Guerra en Ucrania en el Sector Agroalimentario Español. Tiberra. Available online: https://www.plataformatierra.es/innovacion/el-impacto-de-la-guerra-en-ucrania-en-el-sector-agroalimentario/ (accessed on 10 May 2022).

- FAO. FAOSTAT Statistical Database. Available online: https://www.fao.org/faostat/en/#data/QC (accessed on 21 April 2022).

- Leiva, M. Which Countries Are Most Exposed to Interruption in Ukraine Food Exports? Investment Monitor. 2022. Available online: https://www.mining-technology.com/special-focus/countries-exposed-ukrainian-food-exports/ (accessed on 21 April 2022).

- Martinez, E. La Falta de Grano de Ucrania se Compensará con 600.000 Hectáreas más de Cultivos. Heraldo. 2022. Available online: https://www.lavozdegalicia.es/noticia/somosagro/agricultura/2022/04/16/falta-grano-ucrania-compensara-600000-hectareas-cultivos/00031650126669699416159.htm (accessed on 10 May 2022).

- Every, M.; Erken, H.; van der Veen, M.; Fitzmaurice, R.; Vogel, S. How We Would Pay for the War—The Macro Impact of Ukraine War/Sanctions; Rabobank: Utrecht, The Netherlands, 2022. [Google Scholar]

- US Energy. Information Administration Ukraine. Available online: https://www.eia.gov/international/analysis/country/UKR (accessed on 18 April 2022).

- AFP. As Ukraine Sowing Season Starts, Fuel Shortages Threaten Food Supply. The News. 2022. Available online: https://www.france24.com/en/live-news/20220329-as-ukraine-sowing-season-starts-fuel-shortages-threaten-food-supply (accessed on 18 April 2022).

- Copernicus. Copernicus Global Land Service—Providing Bio-Geophysical Products of Global Land Surface. Available online: https://land.copernicus.eu/global/products/vci (accessed on 18 April 2022).

- FAO. FAO Agricultural Stress Index System (ASIS); FAO: Rome, Italy, 2018. [Google Scholar]

- FAO. Open GIS. Available online: https://io.apps.fao.org/gismgr/api/v1/ASIS/VCI_M/2/wms?request=GetCapabilities&service=WMS&version=1.3.0 (accessed on 18 April 2022).

- IPAD. World Agricultural Production (WAP) Circular. Available online: https://ipad.fas.usda.gov/Default.aspx (accessed on 18 April 2022).

- FAO. The Future of Food and Agriculture—Trends and Challenges. 2017. Available online: https://www.fao.org/3/i6583e/i6583e.pdf (accessed on 3 May 2022).

- IGC. Databank: Ukraine Production and Trade (Main Grains & Oilseeds/Products). Available online: https://www.igc.int/en/downloads/2022/gen2122misc1.pdf (accessed on 21 April 2022).

- IGC. Grain Market Report. Available online: https://www.igc.int/en/gmr_summary.aspx (accessed on 21 April 2022).

- European Commission. Agri-Food Trade Statistical Factsheet—European Union—Ukraine. Available online: https://ec.europa.eu/info/sites/default/files/food-farming-fisheries/farming/documents/agrifood-ukraine_en.pdf (accessed on 21 April 2022).

- European Commission. Trade Monitoring through Customs Surveillance Data. Available online: https://circabc.europa.eu/sd/a/8df1b7d8-1098-42b3-b29b-366d9c77192e/OILSEEDS%20TAXUD_Surv.pdf (accessed on 21 April 2022).

- Putsenteilo, P.; Klapkiv, Y.; Kostetskyi, Y. Modern Challenges of Agrarian Business in Ukraine on the Way to Europe. In Proceedings of the 2018 International Scientific Conference ‘Economic Sciences for Agribusiness and Rural Economy’, Warsaw, Poland, 7–8 June 2018; pp. 250–258. [Google Scholar]

- Graham, N.; Pe’er, I. Putin’s Invasion of Ukraine Threatens a Global Wheat Crisis. Available online: https://www.atlanticcouncil.org/blogs/econographics/putins-invasion-of-ukraine-could-spark-a-global-food-crisis/ (accessed on 21 April 2022).

- Das, K.B. Ukraine: Stand-of Threatens Europe Breadbasket. Int. J. Soc. Sci. 2014, 3, 375. [Google Scholar] [CrossRef]

- Gallagher, I. Key Port at Odessa Is Blasted by 50 Cruise Missiles as Russia Moves to Cut Ukraine off from Overseas Trade. Available online: https://opera.news/za/en/military/cd987d5514de2f78b12b07933654ce92 (accessed on 4 May 2022).

- European Commission. Cereals Statistics. Available online: https://ec.europa.eu/info/food-farming-fisheries/farming/facts-and-figures/markets/overviews/market-observatories/crops/cereals-statistics_en (accessed on 21 April 2022).

- Destatis. Diesel Fuel Prices Averaged 2.16 Euros per Litre on 20 March 2022. Available online: https://www.destatis.de/EN/Press/2022/03/PE22_132_611.html (accessed on 21 April 2022).

- EURACTIV. In Spain, Soaring Prices Fuel Growing Social Unrest. Available online: https://www.euractiv.com/section/energy/news/in-spain-soaring-prices-fuel-growing-social-unrest/ (accessed on 21 April 2022).

- Macrotrends. Wheat Prices—40 Year Historical Chart. Available online: https://www.macrotrends.net/2534/wheat-prices-historical-chart-data (accessed on 18 April 2022).

- Sobolev, D. Grain and Feed Update. 2021. Available online: https://apps.fas.usda.gov/newgainapi/api/Report/DownloadReportByFileName?fileName=Grain%20and%20Feed%20Update_Kyiv_Ukraine_10-15-2021.pdf (accessed on 18 April 2022).

- Weiland, P.; Zachmann, G. The Impact of the War in Ukraine on Food Security. Available online: https://www.bruegel.org/2022/03/the-impact-of-the-war-in-ukraine-on-food-security/ (accessed on 18 April 2022).

- OEC. Observatory of Economic Complexity. Available online: https://oec.world/en/home-b (accessed on 18 April 2022).

- AMIS. Market Monitor. Available online: http://www.amis-outlook.org/fileadmin/user_upload/amis/docs/Market_monitor/AMIS_Market_Monitor_current.pdf (accessed on 18 April 2022).

- Dutton, J. US Corn Production by State: The Top 11 Rankings. 2022. Available online: https://www.cropprophet.com/us-corn-production-by-state/ (accessed on 18 April 2022).

- Swinnen, J.; Burkitbayeva, S.; Schierhorn, F.; Prishchepov, A.V.; Müller, D. Production Potential in the “Bread Baskets” of Eastern Europe and Central Asia. Glob. Food Secur. 2017, 14, 38–53. [Google Scholar] [CrossRef]

- Index Mundi. Available online: https://www.indexmundi.com/facts/ukraine (accessed on 18 April 2022).

- Maciejewska, A.; Skrzypek, K. Ukraine Agriculture Exports—What Is at Stake in the Light of Invasion? Available online: https://ihsmarkit.com/research-analysis/ukraine-agriculture-exports-what-is-at-stake.html (accessed on 18 April 2022).

- Ebrahim, N. Egypt Caps Bread Prices as Shockwaves of Ukraine War Hit Middle East. CNN Business. 2022. Available online: https://edition.cnn.com/2022/03/23/business/mideast-summary-03-23-2022-intl/index.html (accessed on 18 April 2022).

- Strapchuk, S. Condition and Trends of Pharmaceutical Production in Ukraine. Econ. Theory Law 2017, 820, 62. [Google Scholar]

- Politics.co.uk. Staff Ukraine’s Water Wars. Available online: https://www.politics.co.uk/partner-content/2021/12/29/ukraines-water-wars/ (accessed on 18 April 2022).

- United Nations. Update on the UN Work in Ukraine. Available online: https://ukraine.un.org/en/175756-update-un-work-ukraine-23032022 (accessed on 18 April 2022).

- OECD. Poland—Country Report. Available online: https://ec.europa.eu/environment/water/water-framework/economics/pdf/Poland%20report.pdf (accessed on 18 April 2022).

- Tarassevych, O. Poultry and Products Annual; USDA & GAIN. 2020. Available online: https://apps.fas.usda.gov/newgainapi/api/Report/DownloadReportByFileName?fileName=Poultry%20and%20Products%20Annual_Kyiv_Ukraine_09-01-2020 (accessed on 18 April 2022).

- Trollman, H.; Jagtap, S.; Garcia-Garcia, G.; Harastani, R.; Colwill, J.; Trollman, F. COVID-19 Demand-Induced Scarcity Effects on Nutrition and Environment: Investigating Mitigation Strategies for Eggs and Wheat Flour in the United Kingdom. Sustain. Prod. Consum. 2021, 27, 1255–1272. [Google Scholar] [CrossRef] [PubMed]

- Vasylieva, N. Food Security in Times of COVID-19: Price Aspects in Ukraine and Neighboring EU Countries. Montenegrin J. Econ. 2021, 17, 21–30. [Google Scholar] [CrossRef]

- Mudrak, R. Consumer Behavior as a factor of the household’s food security. Econ. Ann.-XXI 2014, 3, 27–30. [Google Scholar]

- Hinote, B.P.; Cockerham, W.C.; Abbott, P. Psychological Distress and Dietary Patterns in Eight Post-Soviet Republics. Appetite 2009, 53, 24–33. [Google Scholar] [CrossRef]

- Sheather, J. As Russian Troops Cross into Ukraine, We Need to Remind Ourselves of the Impact of War on Health. BMJ 2022, 376, o499. [Google Scholar] [CrossRef]

- UN News. UN Alarm over Mounting Ukraine Casualties, amid Desperate Scenes in Mariupol. Available online: https://news.un.org/en/story/2022/03/1114692 (accessed on 18 April 2022).

- Aysa-Lastra, M. Integration of Internally Displaced Persons in Urban Labour Markets: A Case Study of the IDP Population in Soacha, Colombia. J. Refug. Stud. 2011, 24, 277–303. [Google Scholar] [CrossRef]

- Dummett, M. Bangladesh War: The Article That Changed History. BBC News. 2011. Available online: https://www.bbc.co.uk/news/world-asia-16207201 (accessed on 18 April 2022).

- Tanaka, H. North Korea: Understanding Migration to and from a Closed Country. Available online: https://www.migrationpolicy.org/article/north-korea-understanding-migration-and-closed-country/ (accessed on 18 April 2022).

- Basu, K. Why Is Bangladesh Booming? Available online: https://www.brookings.edu/opinions/why-is-bangladesh-booming/ (accessed on 18 April 2022).

- CIA. The World Factbook—Moldova. Available online: https://www.cia.gov/the-world-factbook/countries/moldova/ (accessed on 18 April 2022).

- CIA. The World Factbook—Georgia. Available online: https://www.cia.gov/the-world-factbook/countries/georgia/ (accessed on 18 April 2022).

- Winsor, M. What’s the Cost of Damage to Ukraine’s Infrastructure amid Russia’s Invasion? ABC News. 2022. Available online: https://abcnews.go.com/International/cost-damage-ukraines-infrastructure-amid-russias-invasion/story?id=83719126 (accessed on 18 April 2022).

- AFP. Ukraine Estimates Damage Caused by Russian Invasion at $565 Billion. The Times of Israel. 2022. Available online: https://www.timesofisrael.com/liveblog_entry/ukraine-estimates-damage-caused-by-russian-invasion-at-565-billion/ (accessed on 18 April 2022).

- Suprun, I.; Dovha, O. Development of Beef Cattle Breeding Status in Ukraine. Bull. Sumy Natl. Agrar. Univ. Ser. Livest. 2021, 1, 92–97. [Google Scholar] [CrossRef]

- Attaché Report (GAIN). Ukraine: Livestock and Products Annual; USDA: Washington, DC, USA, 2020.

- CIWF. The Life of: Broiler Chickens. Available online: https://www.ciwf.org.uk/media/5235306/The-life-of-Broiler-chickens.pdf (accessed on 18 April 2022).

- Peterson Farm Brothers. The Life Cycle of Beef Cattle Production. Available online: https://petersonfarmbrothers.com/the-life-cycle-of-beef-cattle-production/ (accessed on 18 April 2022).

- Gayduk, A. Fertilizer Production in Ukraine. Available online: https://good-time-invest.com/blog/fertilizer-production-in-ukraine/ (accessed on 18 April 2022).

- OEC. Ukraine. Available online: https://oec.world/en/profile/country/ukr (accessed on 18 April 2022).

- News Desk Food Safety. News FSA and Others Monitoring Potential Food Impacts of Ukraine Invasion. Available online: https://www.foodsafetynews.com/2022/03/fsa-and-others-monitoring-potential-food-impacts-of-ukraine-invasion/#:~:text=FSA%20and%20others%20monitoring%20potential%20food%20impacts%20of%20Ukraine%20invasion,-By%20News%20Desk&text=The%20Food%20Standards%20Agency%20(FSA,risks%20have%20yet%20been%20detected (accessed on 1 May 2022).

- Mbah, R.E.; Wasum, D. Russian-Ukraine 2022 War: A Review of the Economic Impact of Russian-Ukraine Crisis on the USA, UK, Canada, and Europe. Adv. Soc. Sci. Res. J. 2022, 9, 144–153. [Google Scholar] [CrossRef]

- Li, X.-Y.; Li, X.; Fan, Z.; Mi, L.; Kandakji, T.; Song, Z.; Li, D.; Song, X.-P. Civil War Hinders Crop Production and Threatens Food Security in Syria. Nat. Food 2022, 3, 38–46. [Google Scholar] [CrossRef]

- Dureab, F.; Al-Falahi, E.; Ismail, O.; Al-Marhali, L.; Al Jawaldeh, A.; Nuri, N.N.; Safary, E.; Jahn, A. An Overview on Acute Malnutrition and Food Insecurity among Children during the Conflict in Yemen. Children 2019, 6, 77. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Robson, S.; Bengoechea, I.; Blackall, M.; Wood, P.; Sandhu, S.; Gye, H. Ukraine: Three More Nuclear Power Plants and Nine Reactors Remain in Putin’s Sights after Zaporizhzhia Attack. INews. 2022. Available online: https://inews.co.uk/news/ukraine-more-nuclear-power-plants-reactors-putin-sights-zaporizhzhia-attack-1498695 (accessed on 1 May 2022).

- Petkova, M. Is a Nuclear Disaster Likely in Ukraine? Aljazeera. 2022. Available online: https://www.aljazeera.com/news/2022/3/17/is-a-nuclear-disaster-likely-in-ukraine (accessed on 1 May 2022).

- Matvieieva, I.; Rudyak, Y.; Zabulonov, Y.; Iatsyshyn, A.; Taraduda, D.; Taras, K. Formation of Radiation Doses of Ukraine’s Population in Areas Contaminated by Radionuclides after the Accident at the Chernobyl Nuclear Power Plant. In Systems, Decision and Control in Energy III; Springer: Cham, Switzerland, 2022; pp. 157–169. [Google Scholar]

- Mpoke Bigg, M. Radiation Levels near the Chernobyl Plant Are within Safe Limits, the Nuclear Agency Chief Says. The New York Times. 2022. Available online: http://english.news.cn/20220429/7ff4441842ca4b3a8951a302ced5ea74/c.html (accessed on 1 May 2022).

- United Nations. Heightened Security Fears on Chernobyl Disaster Anniversary. United Nations. 2022. Available online: https://news.un.org/en/story/2022/04/1116962 (accessed on 1 May 2022).

- FAO. The Importance of Ukraine and the Russian Federation for Global Agricultural Markets and the Risks Associated with the Current Conflict; FAO: Rome, Italy, 2022. [Google Scholar]

- Flores Martinez, P.; Heron, T. Russia-Ukraine Conflict: Spiking Prices and the Threat to Global Food Security. Food Matters Live. 2022. Available online: https://foodmatterslive.com/article/russia-ukraine-conflict-spiking-prices-and-the-threat-to-global-food-security/ (accessed on 1 May 2022).

- Berkhout, P.; Bergevoet, R.; van Berkum, S. A Brief Analysis of the Impact of the War in Ukraine on Food Security; Wageningen Economic Research: Wageningen, The Netherlands, 2022. [Google Scholar]

- Whitworth, J. National Agencies Allow Flexibility Because of Ukraine-Related Supply Issues. Food Safety News. 2022. Available online: https://www.foodsafetynews.com/2022/04/national-agencies-allow-flexibility-because-of-ukraine-related-supply-issues/ (accessed on 1 May 2022).

- Ntontis, E.; Vestergren, S.; Saavedra, P.; Neville, F.; Jurstakova, K.; Cocking, C.; Lay, S.; Drury, J.; Stott, C.; Reicher, S.; et al. Is It Really “Panic Buying”? Public Perceptions and Experiences of Extra Buying at the Onset of the COVID-19 Pandemic. PLoS ONE 2022, 17, e0264618. [Google Scholar] [CrossRef] [PubMed]

- Pappalardo, G.; Cerroni, S.; Nayga, R.M., Jr.; Yang, W. Impact of COVID-19 on Household Food Waste: The Case of Italy. Front. Nutr. 2020, 7, 585090. [Google Scholar] [CrossRef] [PubMed]

- Ballesteros-Bejarano, J.; González-Calzadilla, A.C.; Ramón-Jerónimo, J.M.; Flórez-López, R. Impact of COVID-19 on the Internationalisation of the Spanish Agri-Food Sector. Foods 2022, 11, 938. [Google Scholar] [CrossRef]

- Hong, E.; Lee, S.Y.; Jeong, J.Y.; Park, J.M.; Kim, B.H.; Kwon, K.; Chun, H.S. Modern Analytical Methods for the Detection of Food Fraud and Adulteration by Food Category. J. Sci. Food Agric. 2017, 97, 3877–3896. [Google Scholar] [CrossRef]

- Hassoun, A.; Måge, I.; Schmidt, W.F.; Temiz, H.T.; Li, L.; Kim, H.-Y.; Nilsen, H.; Biancolillo, A.; Aït-Kaddour, A.; Sikorski, M.; et al. Fraud in Animal Origin Food Products: Advances in Emerging Spectroscopic Detection Methods over the Past Five Years. Foods 2020, 9, 1069. [Google Scholar] [CrossRef]

- Brooks, C.; Parr, L.; Smith, J.M.; Buchanan, D.; Snioch, D.; Hebishy, E. A Review of Food Fraud and Food Authenticity across the Food Supply Chain, with an Examination of the Impact of the COVID-19 Pandemic and Brexit on Food Industry. Food Control 2021, 130, 108171. [Google Scholar] [CrossRef]

- European Commission. Honey—Detailed Information on Honey Production in the European Union. Available online: https://ec.europa.eu/info/food-farming-fisheries/animals-and-animal-products/animal-products/honey (accessed on 1 May 2022).

- Johnson, A. Food Manufacture Food Fraud and the Ukraine War. Available online: https://www.foodmanufacture.co.uk/Article/2022/03/28/Food-fraud-and-the-Ukraine-war# (accessed on 1 May 2022).

- Zhang, G.; Abdulla, W. On Honey Authentication and Adulterant Detection Techniques. Food Control 2022, 138, 108992. [Google Scholar] [CrossRef]

- Roberts, M.; Viinikainen, T.; Bullon, C. International and National Regulatory Strategies to Counter Food Fraud; FAO: Rome, Italy, 2022; ISBN 978-92-5-135904-4. [Google Scholar]

- Huq, A.K.O.; Uddin, I.; Ahmed, E.; Siddique, M.A.B.; Zaher, M.A.; Nigar, S. Fats and Oils Adulteration: Present Scenario and Rapid Detection Techniques. Food Res. 2022, 6, 5–11. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Inclusion Criteria | Exclusion Criteria |

|---|---|

| Available in English | Unavailable in English |

| Published by a government, NGO, or broadsheet | Published by a tabloid |

| Published by an expert in the field | Published as a generic blog |

| Related to identified impact categories | Unrelated to identified impact categories |

| Agricultural Product | Seasonality | Major Concerns and Impacts |

|---|---|---|

| Grains | Winter grain: planting from September to October, harvesting from July to August | Half of the winter wheat and 38% of rye to be harvested in summer 2022 are in occupied or war-affected areas |

| Oilseeds | Sunflowers: planting in April, harvesting from mid-September to mid-October | Sunflowers planting will be seriously affected in at least nine Oblasts (regions). Sown under sunflowers in 2022 may be 35% lower compared to 2021 |

| Vegetables | Land preparation for vegetables from late February to March, sowing from mid-March to mid-May, harvesting from July to mid-September | Disruptions due to lack of inputs, lack of access to land and concerns over safety for workers will affect summer harvest |

| Livestock | Seasonal with respect to availability of feeds and forage, and breeding cycles with respect to eggs, dairy, and meat | Disruptions due to lack of feed, feed additives, veterinary medicine, and breeding stock; insecurity of livestock transportation; as well as damage to infrastructure; will affect the livestock sector for as long as the war continues |

| Country | Imported Wheat (tonnes) | Maize (tonnes) | Sunflower Seed (tonnes) | Sunflower Oil (tonnes) | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Total | EU | Ukraine | Total | EU | Ukraine | Total | EU | Ukraine | Total | EU | Ukraine | |

| Austria | 1,151,669 | 1,151,302 (99.97%) 1 | 286 (0.02%) 1 | 967,258 | 887,402 (91.74%) | 30 (0.003%) | 156,041 | 150,733 (96.60%) | 29 (0.02%) | 76,115 | 59,975 (78.80%) | 6579 (8.64%) |

| Belgium | - | - | - | 1,922,955 | 1,502,583 (78.14%) | 418,921 (21.79%) | 119,686 | 112,493 (93.99%) | 2536 (2.12%) | 586,818 | 574,233 (97.86%) | 10,738 (1.83%) |

| Bulgaria | - | - | - | 27,844 | 20,454 (73.46%) | 209 (0.75%) | 1,020,755 | 457,030 (44.77%) | 182,539 (17.88%) | 41,875 | 12,635 (30.17%) | 25,992 (62.07%) |

| Croatia | - | - | - | - | - | - | - | - | - | 69,080 | 23,905 (34.60%) | 104 (0.15%) |

| Cyprus | - | - | - | 289,032 | 188,490 (65.21%) | 29,570 (10.23%) | - | - | - | 7234 | 4663 (64.46%) | 2517 (34.79%) |

| Czech | - | - | - | - | - | - | 210,192 | 198,102 (94.25%) | 2789 (1.33%) | 58,985 | 50,830 (86.17%) | 6690 (11.34%) |

| Denmark | - | - | - | - | - | - | 16,348 | 15,369 (94.01%) | 211 (1.29%) | 17,944 | 14,997 (83.58%) | 104 (0.58%) |

| Estonia | - | - | - | 25,984 | 23,985 (92.31%) | 777 (2.99%) | 6066 | 872 (14.38%) | 4515 (74.43%) | 7036 | 1378 (19.58%) | 2355 (33.47%) |

| France | - | - | - | 661,440 | 641,541 (96.99%) | 6 (0.001%) | 325,638 | 234,358 (71.97%) | 501 (0.15%) | 298,341 | 126,944 (42.55%) | 154,758 (51.87%) |

| Germany | 3,999,369 | 3,978,627 (99.48%) | 5066 (0.13%) | 3,802,900 | 3,378,093 (88.83%) | 393,290 (10.34%) | 389,117 | 363,570 (93.43%) | 2478 (0.64%) | 495,001 | 477,005 (96.36%) | 14,854 (3.00%) |

| Greece | 894,928 | 625,470 (69.89%) | 86,892 (9.71%) | - | - | - | - | - | - | 69,435 | 53,988 (77.75%) | 14,388 (20.72%) |

| Hungary | - | - | - | 168,688 | 110,533 (65.53%) | 25,675 (15.22%) | 131,494 | 108,742 (82.70%) | 7 (0.01%) | 46,795 | 14,170 (30.28%) | 21,874 (46.745) |

| Ireland | - | - | - | 1,313,414 | 118,007 (8.98%) | 415,402 (31.63%) | - | - | - | - | - | - |

| Italy | 7,994,393 | 4,894,209 (61.22%) | 233,869 (2.93%) | 5,994,600 | 4,586,124 (76.50%) | 770,245 (12.85%) | 159,738 | 139,130 (87.10%) | 2667 (1.67%) | 589,558 | 185,720 (31.50%) | 346,749 (58.82%) |

| Latvia | - | - | - | 93,839 | 17,912 (19.09%) | 5462 (5.82%) | 5988 | 1822 (30.43%) | 208 (3.47%) | 14,014 | 7649 (54.58%) | 3194 (22.79%) |

| Lithuania | - | - | - | 321,350 | 10,321 (3.21%) | 217,387 (67.65%) | 7626 | 3989 (52.31%) | 728 (9.55%) | 36,950 | 4185 (11.33%) | 17,155 (46.43%) |

| Malta | - | - | - | - | - | - | - | - | - | 2573 | 1063 (41.31%) | 1408 (54.72%) |

| Netherlands | 4,296,917 | 4,189,485 (97.50%) | 30,920 (0.72%) | 5,945,756 | 2,748,433 (46.23%) | 3,027,455 (50.92%) | 768,103 | 738,468 (96.14%) | 1421 (0.19%) | 885,606 | 202,459 (22.86%) | 679,591 (76.74%) |

| Poland | 869,332 | 860,548 (98.99%) | 3946 (0.45%) | 421,653 | 379,173 (89.93%) | 1500 (0.36%) | 65,622 | 49,675 (75.70%) | 5555 (8.47%) | 219,866 | 77,360 (35.19%) | 140,210 (63.77%) |

| Portugal | - | - | - | 1,899,504 | 370,484 (19.50%) | 732,523 (38.56%) | - | - | - | 67,220 | 39,710 (59.07%) | 14,929 (22.21%) |

| Romania | - | - | - | 1,348,879 | 1,238,860 (91.86%) | 689 (0.05%) | 242,832 | 59,545 (24.52%) | 1877 (0.77%) | 54,517 | 27,425 (50.31%) | 12,645 (23.19%) |

| Slovakia | - | - | - | 88,878 | 85,213 (95.88%) | 3549 (3.99%) | - | - | - | 43,068 | 38,045 (88.34%) | 3929 (9.12%) |

| Slovenia | - | - | - | 776,976 | 191,535 (24.65%) | 1598 (0.21%) | - | - | - | - | - | - |

| Spain | 4,151,812 | 3,436,105 (82.76%) | 373,294 (8.99%) | 8,067,136 | 2,512,059 (31.14%) | 2,719,175 (33.71%) | 402,353 | 331,560 (82.41%) | 983 (0.24%) | 604,241 | 125,497 (20.77%) | 430,633 (71.27%) |

| Sweden | - | - | - | - | - | - | - | - | - | 38,728 | 33,502 (86.51%) | 1795 (4.63%) |

| Products | Global Export: Combined Russia/Ukraine | Short Term Impact | Long Term Impact | Risks | Reference |

|---|---|---|---|---|---|

| Wheat | 30% | Reasonable supplies | Serious shortages | Adulteration with high protein flour, allergens, lower quality grains, and mycotoxins | [98] |

| Maize | 20% | Shortages | Uncertain | Lower quality grains and mycotoxins | [98] |

| Pulses | Among the top 5 producers | Reduced supplies | Shortages | Adulteration, allergens | [98] |

| Sunflower Oil | 80% | Pressure on alternative vegetable oil sources | Uncertain | Adulteration with other less expensive oils such as palm oil, mineral oil, and rapeseed oil | [98,101] |

| Honey | Number one producer in Europe | Pressuring supply and demand | Contamination from conflict chemicals (e.g., heavy metals/biological hazards) | Adulteration with many cheaper substances (such as sugar syrups or other alternatives) and health risks due to contaminants | [98,99] |

| Fish | 40% whitefish (e.g., 30% Atlantic cod and 25% haddock) | Price increases and reduced supply | Impact on seafood processing industries | Substitution of species, incorrect origin, etc. traceability) | [98,100] |

| Fertilizer | The largest exporter of urea and potash | Price increases | Reduce crop yields | Fertilizer adulteration | [87,98] |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Jagtap, S.; Trollman, H.; Trollman, F.; Garcia-Garcia, G.; Parra-López, C.; Duong, L.; Martindale, W.; Munekata, P.E.S.; Lorenzo, J.M.; Hdaifeh, A.; et al. The Russia-Ukraine Conflict: Its Implications for the Global Food Supply Chains. Foods 2022, 11, 2098. https://doi.org/10.3390/foods11142098

Jagtap S, Trollman H, Trollman F, Garcia-Garcia G, Parra-López C, Duong L, Martindale W, Munekata PES, Lorenzo JM, Hdaifeh A, et al. The Russia-Ukraine Conflict: Its Implications for the Global Food Supply Chains. Foods. 2022; 11(14):2098. https://doi.org/10.3390/foods11142098

Chicago/Turabian StyleJagtap, Sandeep, Hana Trollman, Frank Trollman, Guillermo Garcia-Garcia, Carlos Parra-López, Linh Duong, Wayne Martindale, Paulo E. S. Munekata, Jose M. Lorenzo, Ammar Hdaifeh, and et al. 2022. "The Russia-Ukraine Conflict: Its Implications for the Global Food Supply Chains" Foods 11, no. 14: 2098. https://doi.org/10.3390/foods11142098