1. Introduction

Many theories from traditional finance are rooted in the rationality premise, constraining market agents as maximizers with consistent beliefs. For instance, the efficient market hypothesis (EMH) assumes that every investor is entirely rational and that speculative asset prices always reflect all information available [

1]. A few other examples that have flourished in this ground are: arbitrage theory [

2], the portfolio selection framework [

3], the capital asset pricing model [

4]; and option-pricing theory [

5]. For an historical perspective on this subject the reader is referred to the work of [

6]. Nevertheless, several anomalies, or market inefficiencies, have been reported ever since: long-run reversals, seasonal patterns, speculative bubbles, etc. Even in the seminal work of [

1] slight serial dependencies in returns were reported, even though understated.

Several studies (e.g., [

7,

8,

9,

10]) have criticized or relaxed the tenets that every agent in the market is a rational optimizer, and argue that decision-makers that maximize linear expected utility—a premise of the neoclassical microeconomic theory [

11]—are unrealistic in real-world circumstances. Indeed, human behavior is guided by simplified procedures or heuristics [

8]. The main argument is that in a real-world situation, due to the limited capacity of investors, agents are unable to obtain and optimally analyze all relevant information; they thus face cruel difficulties in solving complex problems and issues. In addition, investors face difficulties in compiling a comprehensive list of alternative courses of action and determining and assigning values and probabilities to each of many possible courses of action. Because of these aspects they are forced to rely on heuristics which in some circumstances result in good decisions and performance, but not in all situations.

Behavioral finance [

12] has emerged as a compelling theory seeking to bridge the gap between traditional finance on the one hand and psychology and sociology on the other to explain how and why markets, and ultimately agents, behave as they do. This theory is intended to shed light on the investment decision-making process of real people, based on cognitive psychology and biases related to investors beliefs [

10,

13,

14]. A recent survey in [

15] studied 25 profiling characteristics associated with risk-aversion in a sample of a national population in the UK, including some characteristics not previously investigated in the literature. A noticeable loss aversion is reported, correlated with many of the investigated characteristics and substantially different for the subset of graduate students, a social group normally used in other research. In a natural experiment, the entry of domestic individual investors in the B-share market in China, from 2001 onward, was investigated in [

16], showing that this type of investors is more prone to framing bias than the institutional decision-makers. Evidence of investors using the historical returns distribution of stocks as a proxy of future pricing instead of trying to predict the actual future value are laid out in [

17]. The influence of cultural aspects concerning this hypothesis is further investigated in [

18] for emerging markets.

To operate in financial markets, an alternative to discretionary trading is based on the trading system (TS), in which investments are made objectively using so-called technical trading rules (TTRs) [

19] or quantitative trading [

20] to support the decision-making process. In short, a trading system aggregates some input signals and, based on a set of parameters and algorithms, creates buy/sell recommendations of a given security as outputs [

21].

Even in this more systematic scenario, there are many variables to consider. As data size and number of attributes are increasing in finance-related applications, the need to extract value from data grows proportionally. This relevance is shown by [

22] in a survey of numerous studies in computational intelligence for financial markets. An introduction to this theme is presented by [

23], emphasizing the pitfalls of overfitting when using noisy data. These machine learning (ML) studies rely on multiple factors and leverage complex algorithms to gain insight into particular finance problems. Moreover, many studies report the challenges associated with the endless changes in markets as well the complexity of the time series. In this respect, multicriteria decision aid methods, which are based on simpler algorithms compared to the ML field, may offer useful results in a more interpretable fashion [

24].

In this paper, we proposed a new TS merging technical and behavioral aspects. It uses the historic time series of securities as inputs. A pool of classic technical indicators (TI) and TTRs, comprising distinct methods and parameters sets, were employed for back-tested analysis. A group of risk-adjusted and profit-based metrics was considered to evaluate the performance. Periodically, the proposed TS used MCDA (Multiple-criteria decision-making) to reevaluate the trading model, adapting to the input, market condition and desired performance.

The innovative aspect here is the usage of TODIM [

25], a Portuguese acronym for interactive and multicriteria decision-making, which is an MCDA rooted in behavioral finance, based on prospect theory [

7]. The idea is to incorporate behavioral aspects in the adaptation stage of the TS, aiming towards risk reduction while keeping a profitable portfolio. The proposed TS was tested in eight stocks from Brazil, exhibiting different dynamics and having strong relevance for the market. The results were compared against a purely technical Ensemble TS, proposed by [

21], and also the benchmark Buy-and-Hold. Moreover, simulations were carried out to investigate the effects of the parameters of the TODIM algorithm related to the risk aversion behavior, and are also reported in this manuscript.

This paper is organized as follows:

Section 1 lays out fundamental concepts; the proposed approach and the experimental framework is detailed in

Section 2, leading to the results in

Section 3, which are discussed in

Section 4; conclusions and future lines of work are given in

Section 5.

1.1. Background

This section presents some of the theoretical background of this paper. Firstly, we review the literature on applications of MCDA to finance. Secondly, we briefly explain prospect theory; and finally, we review an MCDA method that is based on prospect theory known as TODIM and its application to finance.

1.1.1. Multicriteria Decision Aid

Multicriteria decision aid (MCDA) is an area of operational research that seeks to select the optimal alternative from a finite set of solutions by taking several attributes (multiple criteria) and their relationship into account [

26]. Roughly speaking, MCDA has been used with four different aims [

27]: (1) to select, classify and sort alternatives in the presence of conflicting criteria; (2) to learn through the decision-making process; (3) to find out an alternative or a set of alternatives that present themselves as a set of solutions to the problem; and (4) to clarify the decision.

Different authors have proposed the use of MCDA to solve financial problems. For instance, [

28] reviews the literature of MCDA applications in finance. His work argues that there are three different areas of interest for the application of MCDA to finance: capital budgeting, corporate financing and financial investment, which is the purpose of this work. According to these authors, the main reason for applying MCDA to finance is that traditional financial theory has been challenged for largely using a single-criterion approach.

As data size and the number of attributes are increasing in finance-related applications, the need to extract value from data by using multiple data attributes has increased as well. The authors of [

22] contend that this is crucial for extracting value from data by using multiple data attributes from a different perspective and by surveying numerous studies in computational intelligence for financial markets. These computational intelligence studies rely on multiple factors and highlight the importance of complex algorithms to gain insight into particular financial problems.

In this paper, we propose an emerging technique for MCDA known as TODIM [

25]. To the best of our knowledge, this is the first paper that proposes the use of TODIM as a tool of MCDA to solve TS questions.

The reasons for using TODIM are the following. The first reason is that TODIM may be considered simpler, easier to apply and more readily comprehensible for practitioners than other MCDA methods, such as evolutionary algorithms [

29]. The second reason is that this method is based on prospect theory, which has been proposed as applied to model agents’ behavior when facing different risk scenarios [

30]. Finally, the last reason is that research on applications of TODIM and prospect theory have been carried out in the recent literature [

29,

31].

1.1.2. Prospect Theory

Briefly, prospect theory, as proposed by [

7], aims at modeling the human decision-making process under risk. This theory incorporates three significant aspects to model the agent’s utility function. The first aspect is the reference dependence, i.e., agents compare their outcomes to some reference point. This means that different situations cause different agents’ reactions in the face of gains and/or losses. Further, the agent’s utility function is usually concave at the level of wealth, i.e., the utility increases as they get wealthier, but at a decreasing rate. Hence, the utility function parameters have to change the agents’ focus from levels of wealth to changes in wealth [

14]. They argue that changes are the way humans experience life.

The second aspect is the concept of diminishing sensitivity. These authors argue that there is an enormous amount of wisdom about human nature captured in the S-shaped curve presented in

Figure 1. The upper portion, for gains, is similar to the risk-averse utility function. However, it should be noticed that the lower portion also captures diminishing sensitivity. This is different from the standard model. The reason is that by starting from a given level, losses are captured by moving down the utility of the wealth line, meaning that each loss becomes increasingly painful. The fact that agents have diminishing sensitivity to both gains and losses has another implication. On the one hand, agents are risk-averse for gains, but on the other hand, they are risk-seeking for losses.

Finally, the third aspect is that agents are much more sensitive to losses than to gains. By examining the value function in

Figure 1 at the origin, where both curves begin, it should be noticed that the loss part of the value function is steeper than the gain part: it decreases more quickly than the gain increases. Roughly speaking, losses hurt about twice as much as gains make one feel good.

Therefore, in summary, the authors of prospect theory argue that agents experience life in terms of changes. The value function is concave for gains and convex for losses. Furthermore, agents’ utility is asymmetric, because losses sting more than equivalently sized gains feel good. For an in-depth discussion of this theory, see, for instance, [

7,

8].

1.1.3. TODIM

Based on prospect theory, TODIM seeks to quantify the evaluation of outcomes (which are called alternatives) in three different situations (gains, indifference and loss). In summary, TODIM compares different pairs of alternatives aiming at building an outranking of them.

This method is similar to the previous MCDA method known as PROMETTHEE II [

32]. However, there are two main differences between both TODIM and PROMETTHEE II. The first difference is that TODIM splits off the equation of the partial dominance matrix into a conditional equation to replicate the main concepts behind prospect theory (see Equation (1). These conditions serve to represent the situations of gains, indifference and loss, respectively.

The second difference is that TODIM incorporates a mitigation factor, θ, to the condition of losses (See Equation (1). The reason is that θ is intended to represent the different sensitivity of losses and gains as proposed by prospect theory.

TODIM works as follows. Let us suppose a matrix X = (xij) n × m in which xij indicates an alternative Ai, i = {1, 2, ⋯, n}, evaluated by a criterion Cj, j = {1, 2, ⋯, m}. Associated with each criterion Cj, there is a corresponding weight, wj, thereby forming a vector w = [w1, w2, ⋯, wj, ⋯, wm]T of the same length as vector C. In the sequence, let wcr = wc/wr be defined as the relative weight of the criterion Cc with respect to the reference criterion Cr, and wr = max {wc||c = 1, 2, ⋯, m}.

In the next step, this matrix is normalized, resulting in a transformed matrix called the matrix of partial desirabilities, P = (pij) n × m. Based on this matrix, TODIM outranks the alternatives by using the preferences expressed as the criteria weights. There are different approaches for determining these parameters [

33]. In the present manuscript, however, these weights are employed as a set of parameters to be explored in our simulations. Moreover, an improved version of the original TODIM [

25] has been employed in the literature (see the discussion presented by [

29]). Finally, the steps performed in this method are reported in Algorithm 1. The equations used are detailed in the next sections.

| Algorithm 1: The TODIM method |

| Input: Vector of weights, w; set of alternatives A; vector of criteria C; mitigation factor θ |

| Result: Ranked alternatives |

| Initialization: construct a matrix X; calculate P by normalization of X for all pairs (Ai,Aj), (i,j = 1, 2, ⋯, n) do |

![Processes 10 00609 i001]() |

| end |

| end |

Calculate δ(Ai,Aj), using Equation (2). Calculate ξi, i ∈ {1, 2, ⋯, n} using Equation

(3). Rank the alternatives according to ξi, i ∈ {1, 2, ⋯, n} |

The Partial Dominance Matrix

where Φ

c (

Ai,

Aj) indicates the partial dominance matrix given by the criterion

c. In other words, the factor Φ

c (

Ai,

Aj) represents the contribution of the criterion

c to the function

δ (

Ai,

Aj) when comparing alternative

i to alternative

j.

The Final Dominance Matrix

The Final Dominance Matrix is given by:

The Normalized Dominance Matrix

The Normalized Dominance Matrix is given by:

The alternative with the maximum value

ξi,

i ∈ {1, 2, ⋯, n} is the most desirable one. Therefore, the decision-maker might select it or rank all alternatives following

ξi. The global value of each alternative is the result of its dominance over the others in the set. To calculate this global value, the method is based on the projections of differences in the result of the pairwise comparison of the alternatives, considering the performance of each one in the criterion referring to the reference criterion [

34]. By incorporating prospect theory, the method uses an attenuation factor (θ) that allows the method to consider that the alternatives with losses have a greater absolute value compared to equal gain levels in the calculation of overall performance. Different values of θ represent different forms of the value function of prospect theory in the negative quadrant. When θ < 1, this indicates the preference behavior of a risk-averse individual, while when θ > 1 the behavior indicates an individual with more attenuated preferences concerning risk [

35]. Thus, the method can incorporate in its mathematical basis the real behavior of a person in decision-making involving risks.

2. Proposed Approach

In an overview, the proposed TS aggregates many trading strategies from the literature on technical analysis (TA). Given a few risk and profit metrics (criteria), the TODIM method is used to select the best among the many trading strategies (alternatives) within a given time frame.

The trading system constantly adapts to the new incoming data, the time series of a given security. Since the relation between risk and reward varies over time according to the adaptive market hypothesis (AMH), the idea is that the continuous application of TODIM confers some adaptation capability on the proposed TS, leveraging profit and hedging risks. Similarly, an ensemble approach has been proposed by [

21], comparing classical and more modern TTRs.

The proposed TS consists of two alternating stages. In the first, the same input is supplied to a set of TTRs comprising a portion of the historic time series of a given security, which is labeled as training or in-sample data. This study focuses on classical TTRs, both trend-following and range-breakout types. For a given TTR, several parameters are considered. Each TTR tries to exploit TTRs operating in parallel, simulating buy/sell decisions in a smaller portion of the in-sample data. The performance of the entire set of TTRs is evaluated according to eight performance metrics. As described in C, there are many ways to assess the performance of an investment, so that it is natural to consider distinct criteria. Then, the TODIM method is applied to outrank the TTRs and the one that guarantees the first position is selected.

In the second stage, out-of-sample or validation data is fed for the synthetic operation of the chosen TTR, emulating the result that would occur in real time. The performance of this simulated operation of the TTR within a given time frame is evaluated according to several metrics.

The validation data is concatenated with the previous training data, forming a new set of training data for the next iteration. After the initial iterations, some of the older data is discarded, keeping constant the training data size. This procedure is commonly known as walking forward.

An interesting feature of the proposed TS is an automated decision-making process for choosing a single trading strategy from a pool to operate in the market during a specific given time frame. This pool can represent an ecology of strategies competing among themselves and prioritizing some ratio of risk/reward. Prospect-theory-based models, such as TODIM, may include some of the asymmetry of the risk aversion regarding losses and gains observed by behavioral economics in the complex scenario of deciding the best trading strategy. Therefore, according to the market condition the individual failures can be minimized by changing the trading strategy, which can be very interesting from the risk-adjustment standpoint [

36].

The TODIM method is non-compensatory, i.e., advantages of one attribute/criterion cannot be traded off against disadvantages of another, meaning that each attribute/criterion must stand on its own. This idea corresponds with some premises of the AMH that trading strategies are competing against each other. In TODIM, rank reversal is minimized—another advantage—because of the normalization procedure embedded in the method. Therefore, if similar market conditions reappear, a winning strategy from the past may be more likely to be selected (or to have a higher rank). This MCDA rooted in behavioral finance is the major contribution of the proposed method.

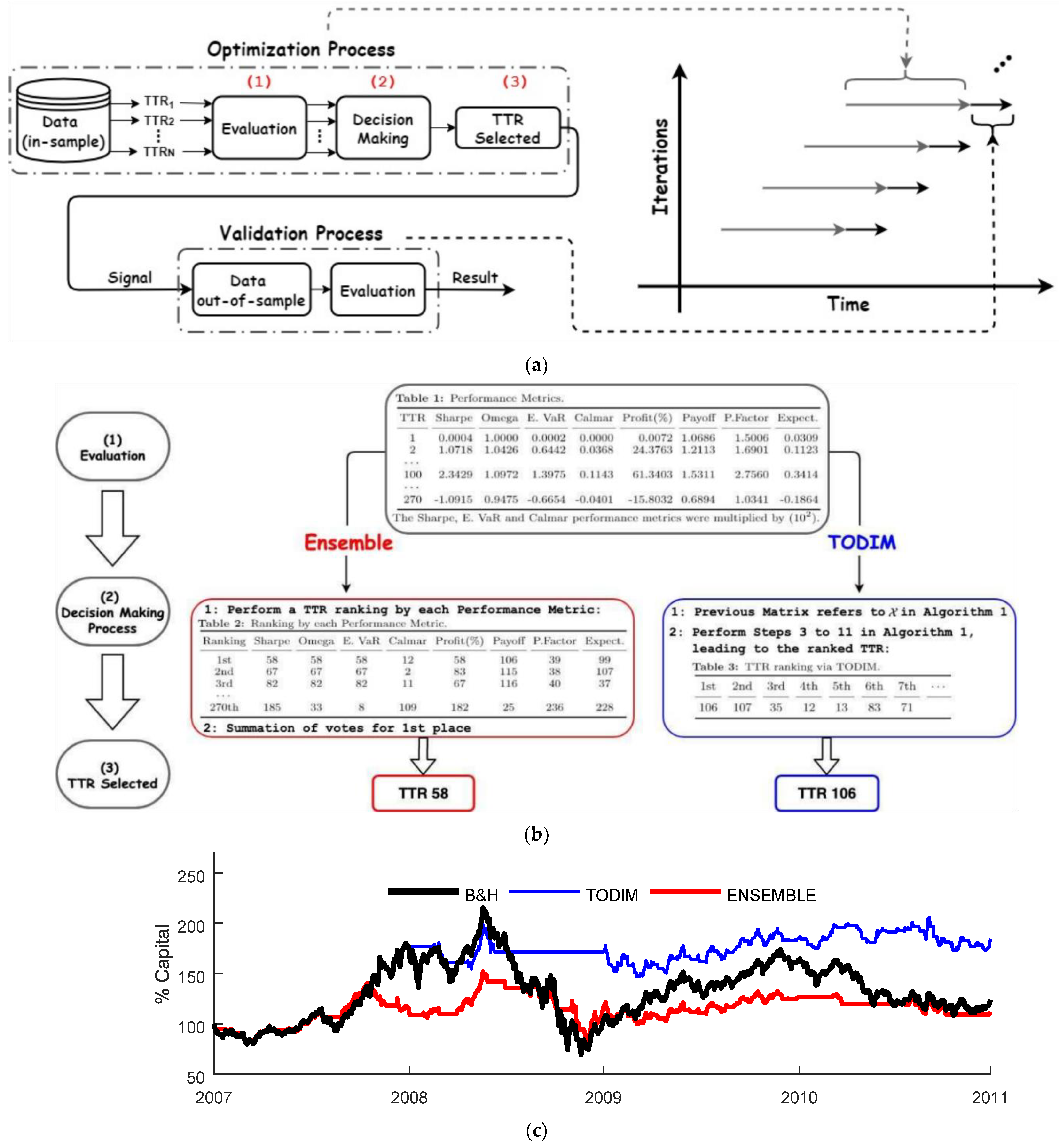

Figure 2 illustrates the key ingredients for the trading system simulation based on the walk forward method. On the left of

Figure 2a, a schematic of the key steps for one iteration is presented. On the right of this figure, some iterations of the walk forward method are presented. The grey and black arrows refer to the in-sample (training) and out-of-sample (validation) dataset, respectively. Some details regarding the optimization process are provided in

Figure 2b. In this Figure one can observe that, although the two methods are based on the same matrix (computed by the performance metrics evaluated for each TTR), the two multicriteria approaches might choose different TTRs at each iteration. Finally, the resulting capital curves for the first iterations of the simulated TS based on these two approaches are depicted in

Figure 2c.

Experimental Framework

This investigation intends to follow neither the EMH nor the AMH in full, but rather to provide a more systematic, yet simple, framework that can be used by investors and practitioners. In this sense, these experiments are intended to analyze the benefits of using a decision-making process based on prospect theory, which is more closely related to behavioral economics, rather than a standard process less rooted in economic and financial theories. The proposed approach is compared to another TS using a distinct MCDA method, which was inspired by the ensembles method and was presented in [

21]. As usual, the benchmark strategy of B&H is also compared.

The dataset comprises the recent time series of eight major stocks from Brazil’s main stock market. The set is detailed in

Appendix A.

The beginning of new presidential mandates in Brazil were used as time-stamps to divide the entire dataset into three periods: 2007–2010, 2011–2014 and 2015–2017. Moreover, an analysis of the entire dataset was performed. Therefore, there were four time frames under analysis. Only long positions were considered in the results presented; when the TS emits a sell signal, the trader does not invest the capital elsewhere.

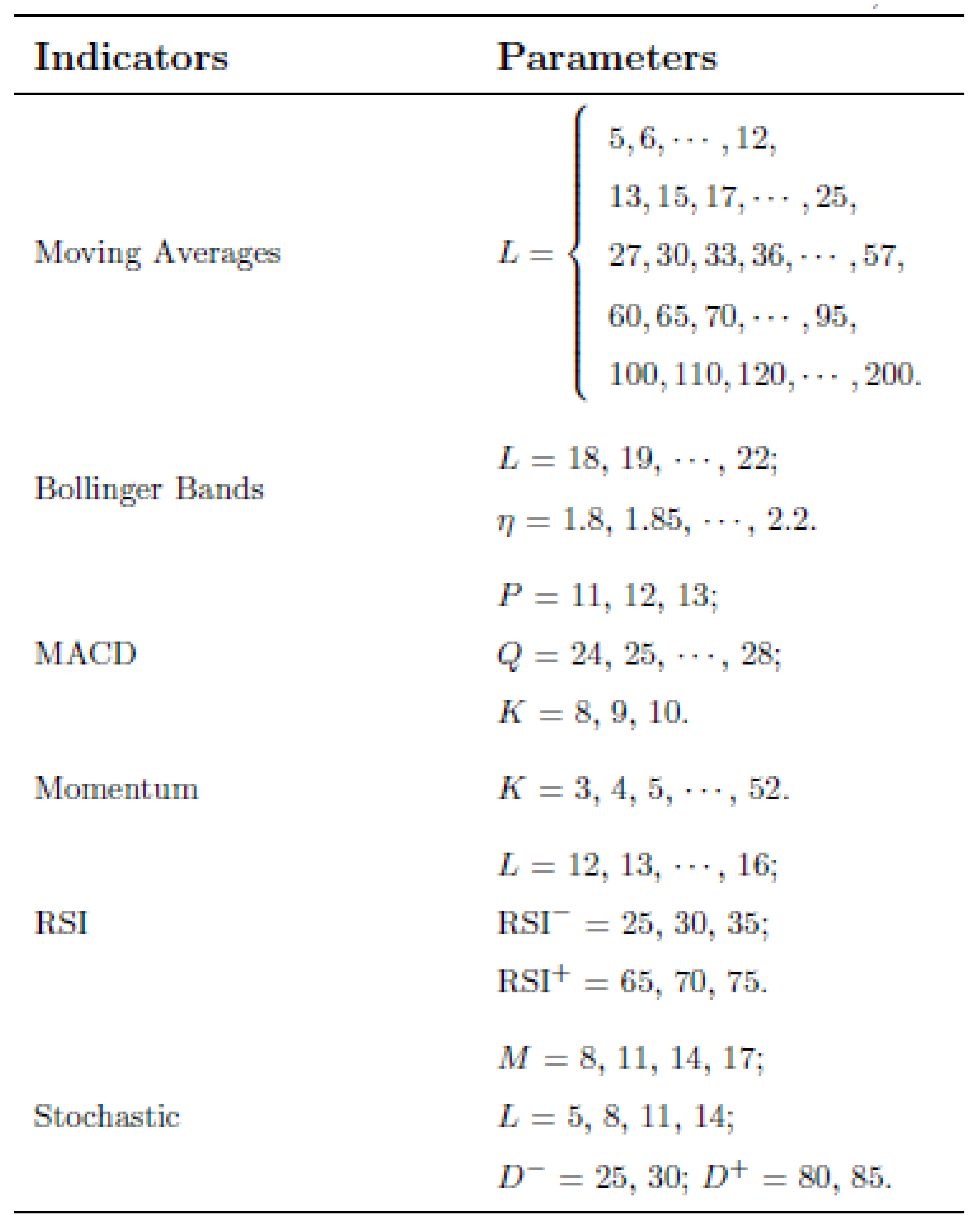

In this paper, widely used TTRs were considered, as described in

Appendix B. The reason is that the emphasis is placed on the MCDA’s capacity to choose the best TTRs from a given pool of choices, instead of discussing the overall quality of the TTRs themselves.

Forecasting the power of the proposed TS and the ensemble-based TS was tested following the methodology proposed by [

37] (

Section 3.2). Such a test checks whether the mean returns of the proposed TS are different, with statistical relevance, from the mean return of the B&H method. The matter of risk adjustment was investigated considering the performance metrics described in

Appendix C. The idea is that the returns perceived cannot be fairly measured without considering the attendant risks. In other words, if two trading strategies provide similar returns, the strategy that exposed the invested capital to lower risk is preferable. These results are presented in

Section 3.1.

TODIM relies on prospect theory, which conjectures that individuals respond asymmetrically to gains and losses. This asymmetry can be quantitatively embedded in TODIM with an attenuation factor, parameter θ in Equation (1). Moreover, simulations were conducted changing the weighting factors. As this tuning may depend on the investor profile, different levels of this parameter were used in this study, as detailed in

Section 3.1.1.

4. Discussion

In terms of pure profitability, none of the decision-making processes were able to stand out (

Section 3.1.1). Nevertheless, the results are quite different when the returns are observed from the viewpoint of risk adjustment and performance metrics. The results show that the main contribution of this work is the proposal of a trading strategy, known as TODIM TS, that provides an identical level of returns with less risk exposition compared to the Buy-and-Hold strategy and ensemble TS. Consequently, the risk-adjustment parameters outperformed both benchmarks.

As described in

Section 3.1.2, the proposed modification produces a noticeable improvement in performance in terms of risk. In approximately 70% of the scenarios investigated, the TTRs selected by TODIM outperformed those chosen by the ensemble method. This result corroborates the idea that an MCDA based on prospect theory, such as TODIM, can reflect decisions with greater risk aversion.

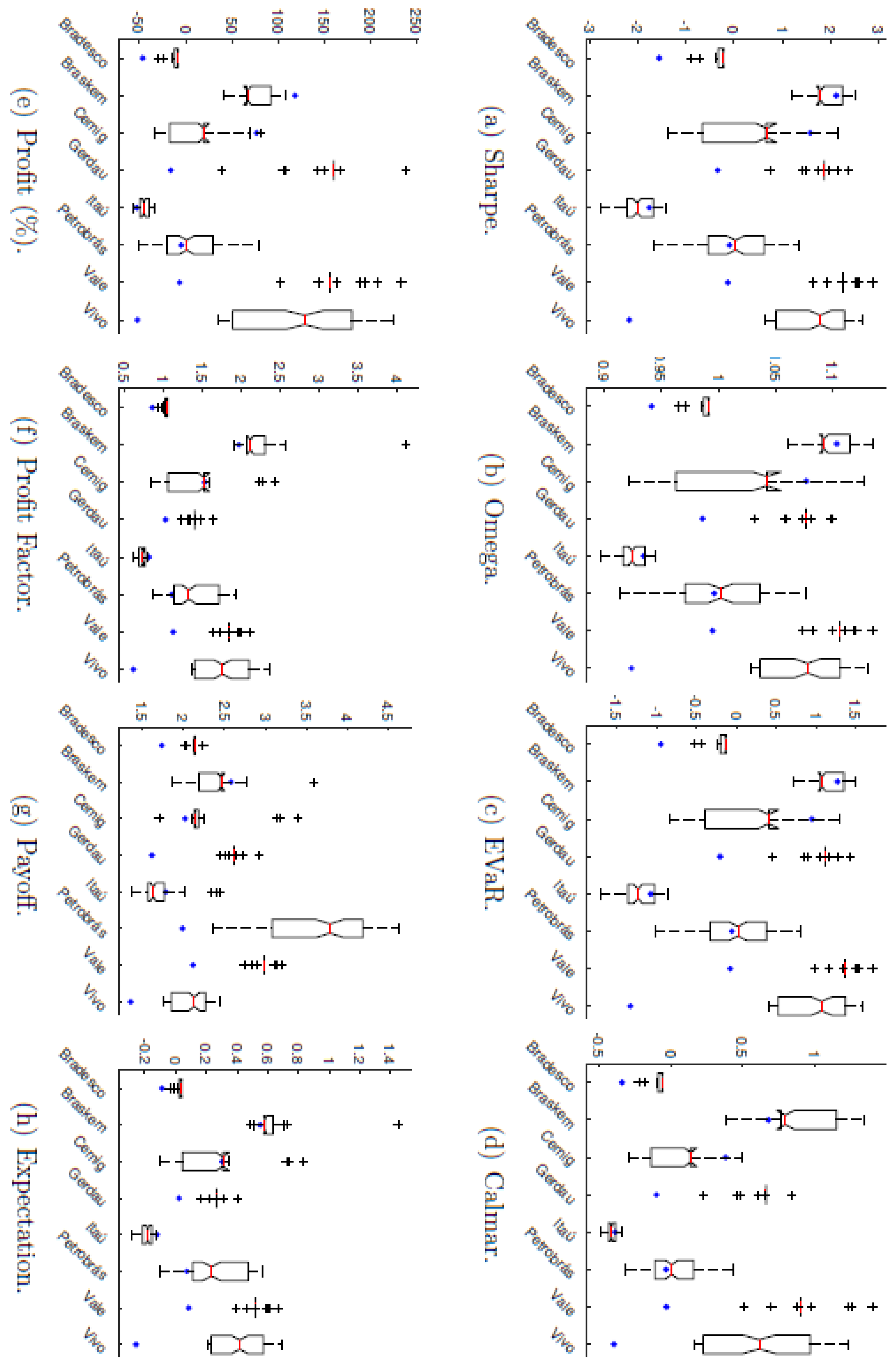

Regarding the weighting factor, interesting results appear. For all metrics, the results for GGBR4 and VALE3 present very small risk. The results tend toward a pronounced repeatability, except for a few outliers. On the one hand, for those securities, the entire distribution outperformed the ensemble TS. On the other hand, concerning risk, CMIG4 results present a superior statistical dispersion with a large distribution for Omega and a very small one for Payoff, for instance. Alternatively, the application of the proposed TS for PETR4 or VIVT4 tends to generate large distributions across all metrics. Even so, for VIVT4, the majority of the distribution was able to outperform the ensemble TS.

Another striking result is that it was always possible to combine a set of parameters such that the proposed TS outperformed the ensemble TS. The only exception occured for the combination of BRKM5 and Profit. In this case, the result of the ensemble TS fell above the top whisker. The analysis reveals that in many scenarios the central tendency of the proposed TS falls above the result produced by the ensemble TS. This is the case for security PETR4 for all the metrics analyzed.

The proposed approach can be regarded as less sensitive to variations in the mitigation factor. For instance, in comparison with the nominal experiment (θ = 0.5), there was a change in the selected TTR in only 10% of the scenarios. In

Table 4 and

Table 5 one can observe that the different values of θ did not result in striking modifications at the ranking order. As a conjecture, it may be pointed out that all the metrics, except Profit, already take risk factors into account. Since the mitigation factor is the same for all metrics, the effect of weighting more on the negative part of the S-curve becomes less relevant. In other words, it gives more weight to a factor that has already been penalized.

Figure 3 shows the dominance curve obtained empirically for the Sharpe Index. This is also consistent with the theory, with a noticeable S-shaped aspect reflecting the loss aversion principle (losses with the same level of gains have higher absolute value).

The proposed method shares the following advantages of the MCDA method class over other method classes: (i) it is more appealing to practitioners, as there is no single criterion to optimize within the constraints; (ii) it is easier and quicker to solve, as it does not require an optimization tool in general; (iii) it is easier to configure by changing weights and adding new criteria to the system; (iv) it incorporates prospect theory into the TS architecture, thereby providing a compromise solution between aspects of human decision-making and the objective decision-making process of the TTRs.

5. Conclusions

This article proposed a TS that adapts its strategy to the underlying data. In this algorithm, multiple TTRs are trained in parallel and evaluated against risk-adjusted and profitability-based performance metrics. Since several criteria are possible, a decision-making method based on prospect theory, TODIM, was employed to classify the TTRs, and the best placed was chosen as the trading strategy for a given period of time. Using the walk forward method, a new dataset fed TODIM TS with data for comparisons with B&H models and the comparison TS. Due to its methodology, as expected, TODIM TS obtained superior results according to the criteria aimed at analyzing risk. The experimental results suggest that the proposed ST has strong generalization and adaptability capabilities, providing improvements, or at least comparable results, in relation to an alternative ST based on a different decision-making method. The simple application, which can be used by beginner practitioners, and the low computational requirement for the analysis and selection of the TS also serve to differentiate the method. The results reinforce the suitability of a method based on prospect theory to select alternatives with lower risk, due to its greater aversion to the risk of loss.

In future work, the authors will seek to investigate an optimization method to select the parameters of the proposed decision-making process and consider improved TTRs. They will also propose to increase the study database so as to include more stocks for the comparison of methods.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}