4.1. An ARDL Approach to Assess Financial Stability and Human Well-Being

The ARDL model is a versatile tool for analyzing time series data and exploring the relations between the research variables. Its ability to deal with short-term and long-term dynamics, cointegration, and robustness make it essential for empirical research. In this section, we will go through the main steps of the ARDL model applied to our data. Descriptive statistics are important for understanding and preparing data before applying the ARDL model.

Table 3 contains the summary statistics of the initial data. According to the Jarque–Bera normality test, HDI, UR, and MC are normally distributed, while FFI is not normally distributed. HDI has a platykurtic distribution, while FFI has a leptokurtic distribution. MC and UR have mesokurtic distributions.

In terms of the relative variability of the data series, the HDI variable exhibits a low level of variation. However, the variable was retained in the analysis despite its low variation because we employed the common technique of logarithmic transformation on the series. This technique helps spread out the values and reduce the impact of outliers, as referenced in the study by (

Lütkepohl and Xu 2012). Additionally, in our study, the theoretical rationale for including variables with a low coefficient of variation is supported by the use of the ARDL model, which analyzes the long-term relationships between variables. Even variables with relatively low variations can play a significant long-term role, especially if they hold economic or political significance. For instance, in a study conducted by (

Yumashev et al. 2020), the research examines the impact of the population’s quality and volume of energy consumption on the Human Development Index (HDI). Even though the summary statistics table in the same study reveals that the coefficient of variation (CV) for HDI is 0.04 (

Yumashev et al. 2020), the study’s findings indicate that the magnitude and rating of HDI are influenced by several factors. These factors encompass the rate of urbanization growth, gross domestic product (GDP), gross national income (GNI) per capita, the proportion of “clean” energy utilization by both the population and businesses within the overall energy consumption, the level of socio-economic development, and the expenditures dedicated to research and development (R&D). Additionally, in the specialized literature, there are other research studies that incorporate variables with low variability into their models (

Abdul Razak and Asutay 2022;

Cristian et al. 2022;

Mare et al. 2019;

Jin and Jakovljevic 2023).

Furthermore, from a short-term dynamics’ perspective, variables with low CV can still exhibit significant short-term dynamics or changes over time. ARDL models capture both short-term and long-term relationships (

Nkoro and Uko 2016), allowing variables with a low CV to contribute to the short-term dynamics of the model. This perspective is crucial for capturing the immediate changes that may be relevant to our research. These variables, even with a low CV, make a substantial contribution to addressing our research question. They enhance the model’s ability to explain the relationships we are investigating and provide a comprehensive perspective on the impact of various variables on our dependent variable, HDI.

Prior to conducting the ARDL bounds test, it is essential to assess the stationarity of the times series. The objective of this stationarity assessment is to ascertain whether the variables maintain a constant mean and variance over time. In

Table 4, the notations LHDI, LUR, LMC, and LFFI represent the logarithmic values of the variables HDI, UR, MC, and FFI. The ADF unit root test (

Dickey and Fuller 1979) is used on both the levels and the first differences. As seen in

Table 4a,b, the ADF unit toot test is computed for trend and intercept, and for intercept, respectively. From both tables, it follows that LHDI and LUR are integrated at order 1, I(1), while LMC and LFFI are integrated at order 0, I(0).

The next stage consists in identifying the appropriate lag structure for the ARDL model, as reported in

Table 5. According to

Enders (

2014), choosing the optimal lag length before applying the ARDL model is essential for several reasons. The optimal lag length selection ensures that the ARDL model is well-fitted to the data. If the lag length is too short, the model may not capture important dynamics, leading to omitted variable bias. On the other hand, if the lag length is too long, it can result in overfitting, making the model overly complex and less interpretable. An optimal lag length strikes a balance between capturing the underlying patterns in the data while avoiding unnecessary complexity. This leads to more efficient parameter estimation and better model performance. Finally, choosing the correct lag length reduces the likelihood of finding spurious relationships in the data. All criteria indicate that the optimal number of lags is 2.

Table 6 presents the results of the cointegration bounds test, aimed at investigating the presence of long-term causality. With an F-statistic calculated at 11.32, surpassing the critical upper bounds denoted by I(1), this indicates the presence of cointegration among the variables under examination. In this case, the selected model is ARDL(2, 2, 1, 0). Thereby, n = 2, p = 2, q = 1, r = 0 in formula (5).

As seen in

Table 7, LFFI and LMC have a long-term positive impact on LHDI. A 1% increase in LMC contributes to a 0.03% increase in LHDI, validating hypothesis H1. When MC increases, it can be a sign of a growing economy. Individuals will have increased incomes, potentially contributing positively to HDI. A stock market with a high MC can attract both domestic and foreign investment. Job and business creation will decrease unemployment and increase income and education levels, raising HDI scores. A robust stock market can encourage financial inclusion through opportunities to invest in stocks and bonds. This would lead to greater financial literacy and long-term savings, contributing to higher HDI scores.

According to

Table 7, a 1% increase in LFFI exerts a 0.05% increase in HDI in the long run, confirming hypothesis H2. As FFI measures the ease of doing business, access to financial services, and government intervention in the economy, greater scores of FFI are associated with better human development outcomes. In general, countries that prioritize policies in favor of financial freedom create an environment conducive to economic growth, investments, and new jobs. This may lead to better education, improved healthcare, and higher incomes, thereby improving HDI. A higher degree of financial freedom might suggest greater resilience to financial contagions and, consequently, a positive impact on human development.

A 1% increase in LUR exerts a 0.005% decrease in LHDI, which makes hypothesis H3 true. Unemployment can have a detrimental effect on HDI by affecting its three components: health, education, and income. When people are unemployed, their income level decreases, resulting in a lower HDI score. Poverty is a consequence of unemployment, creating social inequality. Access to education is reduced, leading also to social instability. Life expectancy can also diminish because of poor health outcomes. Hypothesis H3 is also confirmed in the study by (

Sumaryoto and Hapsari 2020) who found a negative relationship between UR and HDI for Indonesia during 2010–2019. An increased unemployment rate can be a consequence of financial contagion, potentially having a negative impact on human development. An unstable economy leads to fewer job opportunities, thus affecting the overall well-being of the population.

Regarding market capitalization, a 1% increase is associated with an average rise of 3% in the HDI. A healthy capital market, indicated by high market capitalization, positively contributes to human development. This suggests that economies resilient to financial contagion might have a higher HDI due to financial stability and opportunities.

In summary, the coefficients suggest that both the stability of the capital market and financial freedom are associated with a better HDI, while an increased unemployment rate (which may be linked to financial contagion) has a negative impact on human development. These relationships underscore the interconnectedness between a country’s financial health and the overall well-being of its population.

The short-term output of the ARDL-ECM model is displayed in

Table 8. ECT is −0.23, belonging to the interval [−1, 0] and statistically significant, which confirms the existence of a long-term causality from LFFI, LMC, and LUR to LHDI. The rate at which the system corrects itself to reach long-term equilibrium after a temporary deviation is 23%. From

Table 8, one can see that in the short term, a 1% increase in LFFI contributes to a 0.007% decrease in LHDI. Greater financial freedom can create economic volatility in the short run, negatively influencing HDI. Financial freedom can create speculative behavior in financial markets. This can result in the occurrence of speculative bubbles, affecting overall well-being.

Table 9 reports the null hypotheses for four diagnostic tests, along with their

p-values. Notably, the

p-values for the ARCH heteroscedasticity test, the Breusch–Godfrey serial correlation LM test, and the Jarque–Bera normality test all surpass the 5% threshold level. Additionally, the Ramsey RESET test confirms the accurate specification of the model.

To further investigate the stability of long- and short-run parameters in the ARDL model, we used the CUSUM test (

Brown et al. 1975).

Figure 2 presents a graphical representation of the CUSUM test, where the CUSUM values consistently fall within the 5% significance level of critical boundaries.

Before analyzing the VD and IRFs, we first assess the stability of the VAR model. As shown in

Figure 3, it is obvious that all the roots of the AR characteristic polynomial fall within the unit circle. All the roots of the AR characteristic polynomial represented by blue dots.

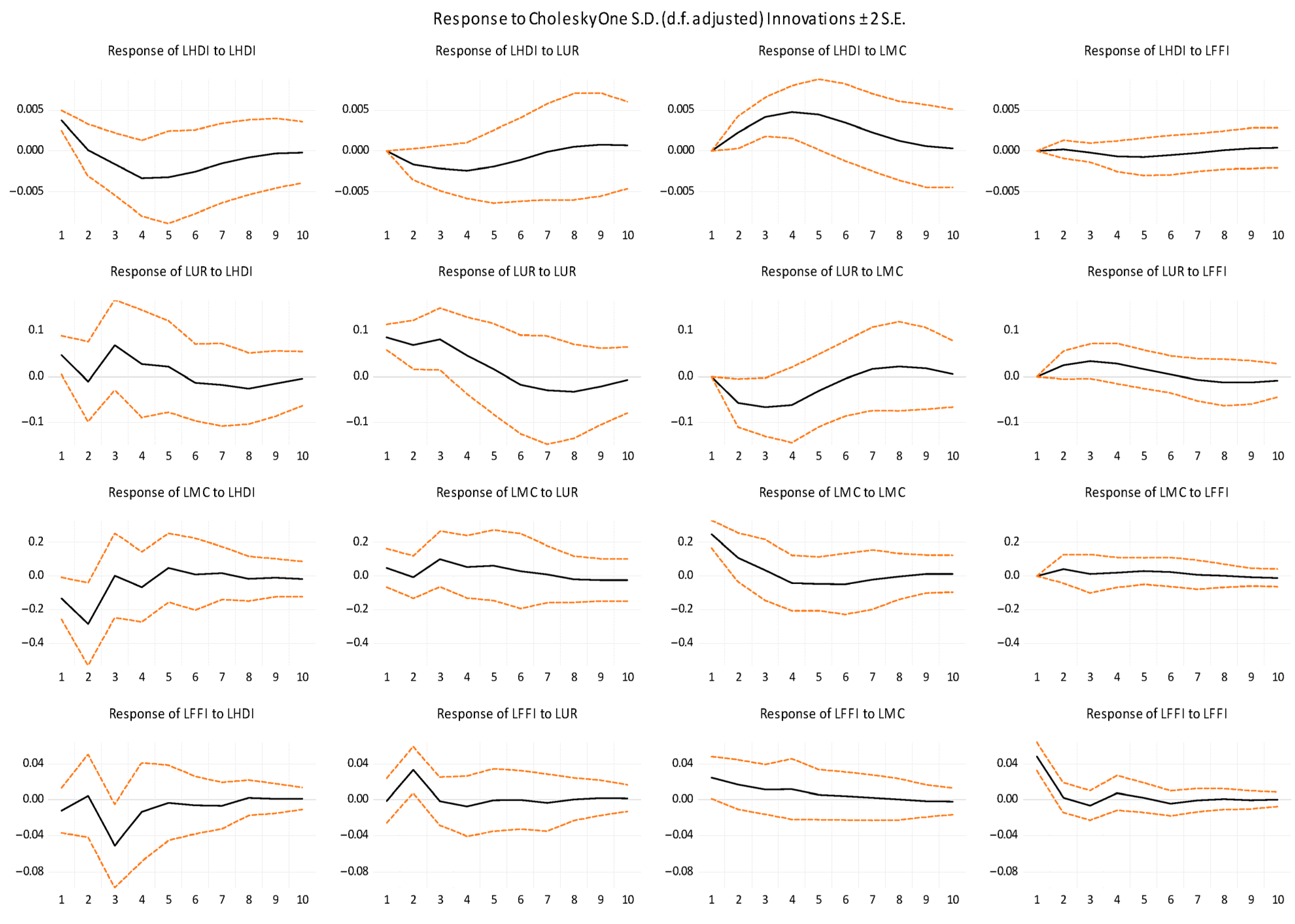

Figure 4 illustrates how one variable reacts to variations in another variable by means of the Cholesky IRFs. In most cases, IRFs show that one variable responds significantly to shocks in another variable. Especially in column 4 of

Figure 5, one can see that the responses of LHDI and LMC to LFFI are characterized by small fluctuations around the zero line, the shock effects dying out. The response of LMC to LFFI can suggest that changes in FFI have a relatively limited impact on MC. MC tends to remain relatively stable, with small fluctuations not strongly correlated with changes in financial freedom. The response of LHDI to LFFI suggests that changes in financial freedom alone are not sufficient to drive significant changes in HDI.

According to

Table A1 from

Appendix A, in the short term, LHDI is explained only by its own shocks. The forecast variance error of LHDI is explained in the 20th period by LMC (55.29%), followed by LUR (12.5%) and LFFI (1.11%). The substantial influence of LMC on LHDI suggests that the stock market’s relation with HDI indicates the strong confidence of investors in the Romanian economy, bringing overall prosperity.

In the long run, LMC has the most important contribution to LUR (27.25%), followed by LHDI (19.71%) and LFFI (6.44%). The high percentage (27.25%) points out that MC is an influential factor of UR. Changes in MC influence investor’s confidence and, consequently, job creation and economic growth.

In the long run, the contribution of LHDI to LMC is the highest (49.42%), followed by LUR (10.49%) and LFFI (1.97%). A prosperous economy has a higher MC. The stability induced by a prosperous economy instills confidence in national and international investors. UR is an economic indicator reflecting the situation of the labor market. High unemployment has a direct impact on MC. Consumer spending decreases, leading to a decline in companies’ revenues and profits, causing a fall in stock prices.

LHDI, LUR, and LMC explain LFFI through their innovative shocks. Economic development, measured by HDI, can have a positive impact on FFI. It leads to more job opportunities, easier access to financial services and financial stability, components of FFI. MC measures the total value of the stock market. MC is indirectly connected to FFI by economic development. A higher MC reflects more investment opportunities, which can enhance financial freedom by increasing wealth through investment.

4.2. A Multiple Linear Regression Approach to Evaluating Financial Stability and Human Well-Being

The multiple linear regression model we constructed examines the impact of financial contagion on human well-being in Romania. Given the current state of knowledge in the field, our analytical approach is valuable for assessing complex relationships in this context.

Before constructing the multiple linear regression model, an important step in preparing the data for regression analysis is to conduct a summary statistics analysis. This analysis aims to understand the data, its distribution, variability, and the relationships between the variables that will be used in the regression. In other words, summary statistics allow us to describe the data in straightforward terms, such as the mean, median, minimum, maximum, standard deviation, skewness, kurtosis, and so on. These measurements provide an overview of the central values, variability, and shape of the data distribution.

Summary statistics, including tests such as Jarque–Bera or Shapiro–Wilk, can help us assess whether the data follows a normal distribution. This is important for regression methods that assume a normal distribution of errors. By examining the correlations between the independent variables and the dependent variable, we can gain an initial understanding of potential regression relationships. Furthermore, summary statistics can reveal data issues, such as missing values or inconsistencies. Proper data cleaning is essential before creating a regression model.

Table 10 presents the summary statistics results for the variables to be used in the regression model. We observe that for the variable GDP, skewness has a value of 0.15, indicating a slight positive skewness (a longer right tail). For HDI, skewness is −1.00, indicating negative skewness (a longer left tail), suggesting that the data are skewed towards smaller values. For VOL and BET-FI, skewness is close to zero, indicating relatively low skewness. For all variables, Kurtosis is less than 3, suggesting that the data distribution is flatter (platykurtic) than a normal distribution, meaning there are fewer data points in the distribution tails.

The Jarque–Bera test is a test of data normality. The higher the value, the less likely the data follow a normal distribution (

Gel and Gastwirth 2008). In the case of GDP, Jarque–Bera has a value of 0.73 with a probability of 0.69, suggesting that the data is approximately normally distributed. For HDI, the value is 3.54, with a probability of 0.17, indicating a significant deviation from normality. For VOL and BET-FI, the values are lower, indicating that the data are closer to a normal distribution. The probability associated with the Jarque–Bera test shows how likely the data is to follow a normal distribution. The lower the probability, the less likely the data is to be normal. While the probability is relatively high for GDP, it is lower for HDI, indicating a significant deviation from normality. For VOL and BET-FI, the probabilities are higher, suggesting a closer resemblance to a normal distribution.

The multiple linear regression model could help quantify how these variables influence human well-being in Romania and identify specific relationships among them. By evaluating these effects, our study can provide a better understanding of how financial contagion can impact people’s lives and contribute to the development of strategies and policies to safeguard human well-being in the face of financial risks.

Given the different units of measurement of the selected variables for the MLR model, we logarithmically transformed all the data. This process is a common technique used in data analysis to transform them into a suitable form to rectify the asymmetry, stabilize the variance, address the issue of data scaling, and transform proportion data. To ensure the stationarity of the time series data used, non-stationary data were transformed into stationary data using the logarithm transformation technique (

Metcalf and Casey 2016). This helps in reducing the large differences between the values in the time series, making it easier to observe underlying trends or patterns. This is particularly useful for data with high variations or exponential growth trends. To perform model estimation, we utilized RStudio software (version 2023.09.1+494, developed by Posit, PBC), following a sequence of steps: data loading into the system, defining the dependent and independent variables, standardizing the dataset to establish a common metric, executing the multicriteria regression within the system, scrutinizing the results through the assessment of critical indicators like

, t-Statistic, or

p-value, and subsequently interpreting the outcomes.

In

Table 11, the ADF test was performed using the adf.test function in R Studio (

Mushtaq 2011;

Jalil and Rao 2019). Considering the

p-value, which is lower than the significance level of 0.05, the data series are stationary.

It’s important to highlight that in the tables that follow, the values presented are rounded to two decimal places. However, when it comes to the mathematical equations based on these results, the coefficients will include all decimal points. In the output of

Table 12, “***” signifies that the

p-value is extremely low (less than 0.001), “**” indicates a

p-value less than 0.01, indicating a moderately high level of statistical significance, and “*” indicates a

p-value less than 0.05, suggesting statistical significance, but at a lower confidence level.

Following the analysis of multiple linear regression (MLR) results from

Table 12, we can draw the following conclusions:

- ➢

The intercept is 9.82 with an extremely low p-value, indicating its significance in the model. It represents the GDP value when all other independent variables are zero.

- ➢

The coefficient for LHDI is 5.73, with a t-value of 13.30 and a very low p-value, suggesting a significant relationship between the level of human development (HDI) and GDP. With a positive coefficient, an increase in HDI is associated with a significant increase in GDP.

- ➢

The coefficient for Lvol is −0.13 with a t-value of −3.48 and a very low p-value, indicating a significant relationship between transaction volume (Lvol) and GDP. With a negative coefficient, an increase in transaction volume is associated with a significant decrease in GDP.

- ➢

The coefficient for LBETFI is 0.06, with a t-value of 2.34 and a p-value of 0.03, suggesting a significant relationship between the BET-FI index and GDP. With a positive coefficient, an increase in the BET-FI index is associated with a significant increase in GDP.

Performance metrics of the model indicate a satisfactory explanation of GDP variability:

- ➢

Residual standard error: It measures how closely predicted values align with actual values. A low standard error indicates a good fit of the model to the data.

- ➢

Multiple R-squared: It stands at 0.94, indicating that approximately 94% of the variance in GDP is explained by the independent variables in the model.

- ➢

Adjusted R-squared: This value is 0.93, suggesting that the model fits the data well and that the independent variables significantly contribute to explaining the variance in GDP.

- ➢

F-statistic: A high F-statistic and low p-value indicate the overall significance of the model.

- ➢

p-value: Low p-values for each coefficient suggest the significance of all independent variables in the model.

In conclusion, the results indicate a significant relationship between HDI, transaction volume, the BET-FI index, and GDP. The coefficients and model statistics provide insights into the direction and significance of these relationships.

Regarding model validation, we conducted a series of additional analyses. Firstly, we examined the model residuals (

Ye and Liu 2023;

Wagner 2023) to ensure that they meet the assumptions of multiple linear regression.

To examine the model’s residuals, we used four methods (

Arkes 2019): the residuals vs. fitted plot, normal Q-Q plot, scale-location plot, and residuals vs. leverage plot. The circles represent the residuals for each observation in the multiple linear regression model. The numeric values next to the circles represent observation identifiers or indices. The red curve represents the multiple linear regression line. According to

Figure 5, Residuals vs. Fitted Plot is used to check linearity and homoscedasticity. In an ideal situation, residuals should be randomly distributed around the horizontal line at zero without a specific pattern. If you observe a distinct pattern or if residuals seem to spread as predicted values increase, this may indicate a violation of linearity or heteroscedasticity. The normal Q-Q plot helps assess the normality of residuals. In an ideal situation, points should follow a straight line. Deviations from the line suggest that residuals may not be normally distributed. Deviations at the ends of the Q-Q plot indicate possible outliers. Scale-Location Plot is used to check homoscedasticity and identify the presence of outliers. It is similar to the residuals vs. fitted values plot, but focuses on the distribution of residuals concerning predicted values. In a homoscedastic model, the distribution of residuals should be relatively constant across the entire range of predicted values. If you observe a pattern, it may indicate heteroscedasticity. Residuals vs. Leverage Plot helps identify influential data points (outliers). Points located far from the center of the plot (with high influence) can significantly impact the regression model. It is essential to check for observations with high influence and, if necessary, decide whether to exclude them from the analysis. These graphical methods aid in assessing the model’s assumptions and identifying potential issues in the regression analysis. Considering the observed distributions, we cannot definitively confirm or refute linearity and homoscedasticity. At this point, the decision was made to retain all variables as initially defined and incorporated into the MLR model.

Next, we will test the collinearity of the independent variables, as this can affect the interpretation of the coefficients. We have employed both the correlation matrix (

Table 11) and the Variance Inflation Factor (VIF) (

Marcoulides and Raykov 2019) values.

We can observe in

Table 13 that the LBETFI and Lvol have a correlation coefficient of 0.46, suggesting a moderate positive correlation between the logarithm of the BET-FI index and the logarithm of transaction volume. When one increases, the other tends to increase as well, but the correlation is not very strong. Lvol and LHDI have a correlation coefficient of 0.27, indicating a relatively weak positive correlation between the logarithm of transaction volume and the logarithm of the Human Development Index (HDI). This suggests that there is a tendency for higher transaction volume to be associated with higher HDI, but the relationship is not very strong. LBETFI and LHDI have a correlation coefficient of 0.57, indicating a moderate positive correlation between the logarithm of the BET-FI index and the logarithm of the Human Development Index (HDI). This suggests that as one of these variables increases, the other tends to increase as well, and the correlation is moderately strong.

Variance Inflation Factor (VIF) values are used to assess the collinearity among the independent variables in your regression (

Marcoulides and Raykov 2019). The higher the VIF, the greater the collinearity. Typical VIF values are under 5. According to

Table 14, for the LHDI variable, the VIF is 1.49. This indicates relatively low collinearity with the other independent variables. With a VIF below 5, there is not a significant collinearity for this variable. For the Lvol variable, the VIF is 1.27. This also suggests low collinearity with the other independent variables. A VIF under 5 for Lvol indicates that there is no significant collinearity for this variable. For the LBETFI variable, the VIF is 1.76. This VIF also demonstrates relatively low collinearity with the other independent variables. A value below 5 indicates that this variable does not exhibit significant collinearity. According to

Table 14, the results suggest that collinearity among the independent variables in the model is low, meaning that they do not significantly affect the model’s ability to estimate the correct coefficients for each independent variable. This supports the robustness of our multiple linear regression model.

Continuing further, to identify whether there are cointegration relationships among our time series, especially to assess if the variables are integrated at the same order and if there are long-term equilibrium relationships among them, we employed cointegration analysis using the Johansen procedure (

Johansen and Juselius 1990;

Yussuf 2022).

The results obtained from the cointegration analysis using the Johansen procedure are presented in

Table 15. The eigenvalues (lambda) indicate that there are four eigenvalues or four cointegration relationships among the variables. The test and critical values show the number of significant cointegration relationships. In our case,

and

show the number of significant cointegration relationships, along with their associated critical values. The test values indicate that all four variables are cointegrated. The eigenvectors represent cointegration relationships, showing how the variables are correlated within these relationships. For instance, the values in the first column (y1.l2) depict the relationship between the variable LGDP and the other variables in each cointegration relationship. The loading matrix W displays the weights of each variable in each cointegration relationship. For example, in the first cointegration relationship, the LGDP variable is negatively influenced by the other variables, as indicated by the negative weights.

In order to analyze the long-term equilibrium relationships between the variables in our model, we will perform cointegration regression. Cointegration involves a statistical relationship that allows multiple time series to move together in the long term, even though they may have different short-term movements (

Perron and Campbell 1994;

Pascalau et al. 2022). The main idea behind cointegration regression is to model the long-term relationship between the series, considering that they may have stochastic trends or short-term fluctuations.

Overall, the results from

Table 16 suggest a strong cointegration relationship between the variables. The coefficients of LHDI, Lvol, and LBETFI are statistically significant, indicating their impact on the dependent variable (likely LGDP). The high R-squared value implies that the model explains a significant portion of the variance in the dependent variable. The intercept (C) is also highly significant, representing the constant term in the cointegration relationship.

These results suggest that there are significant cointegration relationships among the variables in our model, and cointegration analysis is crucial for understanding how these variables mutually influence each other over time. This outcome indicates that while the variables may be correlated over time, they are not merely dependent on each other. Instead, they evolve together over time due to a long-term relationship. In our context, cointegration implies that the LGDP, Lvol (volume of transactions), LHDI, and LBETFI have long-term relationships among them. This means that changes in one of these variables can have a significant and persistent impact on the others. In other words, they evolve together over time and are not independent of each other. Therefore, we can conclude that changes in GDP are related to changes in the volume of transactions, HDI, and the BET-FI index in the long run.

Our analysis results are significant, indicating that significant changes in GDP, which may be influenced by financial contagion, have a lasting impact on the other variables included in our study, such as human well-being measured by HDI. This can provide an important perspective on how financial events can affect economic development and human well-being in Romania. The cointegration among these variables may suggest a long-term interdependence between economic, financial, and human development aspects, thus contributing to a comprehensive understanding of how financial contagion can affect Romania in terms of sustainable development and human well-being.

4.3. Analyzing Financial Contagion Effects on Human Well-Being: The Role of the BET-FI Index and Altreva Adaptive Modeler

Considering the concept of financial contagion and our objective to analyze its effects on human well-being in Romania, the BET-FI index, which measures financial performance in Romania, was introduced into the multiple linear regression model. It reflects the evolution of listed stocks on the Bucharest Stock Exchange. By including the BET-FI index in our study, you can explore its relationship with other variables, particularly GDP and the Human Development Index (HDI), to gain a better understanding of how financial contagion can influence financial market performance. To do this, we utilized Altreva Adaptive Modeler software (version 1.6.0 Evaluation Edition) on BET-FI data to conduct a comprehensive analysis and evaluate its behavior and interactions with other economic and social indicators. The Altreva Adaptive Modeler (

Chiriță et al. 2021;

Marica 2015) is a powerful computational tool that brings a unique perspective to data analysis and modeling (

Altreva Adaptive Modeler 2023). Its adaptability and versatility set it apart from conventional modeling tools. By incorporating this innovative software into our study, we gained the ability to explore complex relationships and analyze dynamic data patterns effectively.

The initial premises we considered regarding how financial contagion can be highlighted through the evolution of the BET-FI index are as follows:

- ➢

Price Effects: A financial crisis or a significant change in another financial market can lead to a decrease in stock prices in the Romanian financial market. Investors, especially foreign investors, may sell assets in the Romanian market, leading to a decrease in stock values and, consequently, the BET-FI index.

- ➢

Economic Effects: Financial contagion can impact Romania’s economy. A decline in financial markets can lead to reduced investor and consumer confidence. This can have a negative impact on economic growth, employment, and the overall development of the country.

- ➢

Trade Effects: If other countries are affected by a financial crisis, Romania’s exports and imports can be influenced. For instance, a decrease in the global demand for goods and services can negatively affect Romanian exports, which can lead to reduced economic activity and an impact on the BET-FI index.

- ➢

Foreign Capital Effects: Financial contagion can prompt foreign investors to withdraw capital from Romania or reduce new investments. This can affect the capital market and the BET-FI indicator.

- ➢

Psychological Effects: Sometimes, financial contagion has a psychological aspect. Investors may become more inclined to sell as they see global markets affected, leading to price reductions and a decline in the BET-FI index, even if economic fundamentals are sound.

These premises serve as a foundation for understanding how financial contagion and the BET-FI index may be interconnected.

The daily closing price data for the BET-FI index were retrieved from the Bucharest Stock Exchange website, maintaining the same time period as in the previous models, from 2000 to 2022.

The simulation conducted in Altreva Adaptive Modeler is carried out for 2000 agents/investors, each with an initial capital of 100,000 monetary units. This perspective can provide a framework for understanding how financial contagion affects a diverse range of investors in Romania. The simulation involves a large number of agents representing a diverse base of investors. This diversity may reflect the real-world scenario where various types of investors, such as retail, institutional, and foreign investors, participate in the capital market. Understanding how the behavior of these agents affects the index can offer insights into market dynamics.

An initial capital of 100,000 for each agent can help assess risk tolerance and exposure to different risks for various investors. A decline in the index can trigger different reactions among these investors, with some reducing their positions, while others might take advantage of the downturn. This can reflect how market volatility and risk aversion influence investor decisions. The simulation can capture investor sentiment, which can be influenced by news, economic events, or global financial developments. Sudden changes in the index can reflect shifts in market sentiment, which do not always align with fundamental economic factors.

Observing how changes in other financial markets or global economic events affect the simulated BET-FI index can provide insights into potential contagion effects. When agents respond to external shocks, they can trigger chain reactions on the index, demonstrating how financial contagion can spread. The simulation reveals how the trading behavior of different agents influences market dynamics. Some agents may employ strategies such as trend-following, value-based investments, or contrarian trading, which can lead to diverse price movements in the index.

The Altreva Adaptive Modeler enables us to understand how various economic and financial indicators, such as the BET-FI index, interact with one another and evolve over time. The software’s adaptive nature allows it to adjust and refine models based on the changing data landscape, providing insights into the relationships between variables and helping us identify patterns and trends that might not be evident through traditional statistical methods.

With Altreva Adaptive Modeler, we have a comprehensive and holistic approach to analyzing financial contagion and its effects on human well-being in Romania. It empowers us to make informed assessments and predictions regarding the intricate dynamics between financial market behavior and broader socio-economic outcomes, contributing to a deeper understanding of sustainable development in the context of economic volatility.

In

Figure 6, a time snapshot of the simulation results can be observed. The first graph tracks how the forecast line compares to real prices. It is evident that the forecast aligns well with trading prices, indicating the model’s strong capability to anticipate market behavior. Specifically, the yellow line represents the real prices of the BET-FI index. The red line represents the forecasted future prices based on the model employed. This forecast is calculated using historical data and the model’s algorithms. The white line is a notation or indication of decision points or actions. The signal can vary depending on the objectives of the analysis. For instance, a “Buy” signal could indicate an opportune moment to purchase stocks, while a “Sell” signal might suggest the right time to sell.

The Wealth Distribution chart suggests that most of the agents or investors in the simulation have wealth levels that cluster around the central value of 417,666. However, there are a few agents with significantly larger wealth levels, indicating that a small portion of investors hold a substantial share of the total wealth. This interpretation may also suggest that there are significant disparities in wealth distribution among investors, which can be relevant in the context of risk analysis or when studying the effects of financial contagion on the market. The substantial wealth of a small number of investors can influence market dynamics and the spread of financial contagion in the simulation.

The third graph, Buy-Sell Orders, shows the number of buy orders and sell orders placed on the market at the same time. The differences between the two lines (the yellow line—buy orders, and the red line—sell orders) indicate the imbalance between the demand (buying) and supply (selling) of financial assets. If the “Buy Orders” line is greater than the “Sell Orders” line, it may indicate an increased interest in buying, potentially leading to a price increase. Conversely, if the “Sell Orders” line is greater, it may suggest a higher interest in selling and possibly exert downward pressure on prices. The significant fluctuations observed indicate market volatility and potential changes in the prices of financial assets.

The VM Trades—VM Trades MA (100) chart compares the trading volume in the market (VM Trades) with the moving average (MA) of trading volume over a 100-day period. It is observed that VM Trades (yellow line) exhibits fluctuations both above and below the VM Trades MA (100) line (red line). When it crosses above the red line, it highlights an increase in short-term trading activity compared to the longer-term average. This could indicate a surge in short-term market activity. Conversely, when VM Trades falls below VM Trades MA (100), it may indicate a decline in trading activity compared to the longer-term average.

The Population Position graph reflects the position of the population of agents or investors at a given moment. When significant variations are observed in this position, it may suggest changes in the structure or composition of the agents within the simulation.

The Avg Genome Size graph shows the average size of the genome or characteristics of the agents in the simulated population. This graph can provide insights into the diversity or complexity of agents in terms of the characteristics they use.

The Right–Wrong Forecasted Price Changes graph compares the number of correct forecasts with the number of incorrect forecasts of price changes. This analysis can offer a perspective on agents’ ability to accurately predict price movements.

The FDA–FDS (Trailing 100 bars) graph shows the difference between the FDA (First Difference Average) and FDS (First Difference Standard Deviation) indicators for the last 100 periods. This can indicate the volatility or stability of market dynamics.

The TS Wealth graph reflects the evolution of wealth or the total capital of agents over the course of the simulation. This graph can provide cumulative insights into the performance of agents in terms of profitability and risk exposure over time.

Based on the results presented in

Table 17, the following discussion can be elaborated:

- ➢

The cumulative return of 90.91% indicates the total growth of the initial investment of 100,000 monetary units to 190,906 monetary units at the end of the period. This suggests a significant increase in investment over time.

- ➢

The compound return/sp of 5.72% indicates the average return over one-year sub-periods within the entire simulation. This shows how efficiently your investment performs in the short term.

- ➢

The cumulative excess return of −24.47% reflects the total return in excess of a benchmark or risk-free rate. In your case, it indicates a negative return compared to the benchmark or risk-free rate, suggesting that your investment may not have performed as well as the benchmark or risk-free rate.

- ➢

The compound excess return/sp of −1.10% shows the average excess return in one-year sub-periods within the simulation. This indicates how your investment has fared compared to the benchmark or risk-free rate in the short term.

- ➢

The Historical Volatility of 11.2% measures the historical volatility or risk associated with returns. The higher this value, the more volatile or risky the investment is.

- ➢

The Value at Risk (VaR) of 1.825 represents the maximum expected loss at a 95% confidence level. In other words, there is a 95% probability that the loss will not exceed this value during the simulation period.

- ➢

The maximum drawdown of 31.2% indicates the largest decline in the investment value compared to the previous peak during the simulation period.

- ➢

The Sharpe ratio of 0.51 evaluates the return in relation to the assumed risk. The higher the value, the more efficient the investment is in relation to the assumed risk.

- ➢

The Sortino ratio of 0.75 is a measure of return in relation to downside volatility. The higher the value, the better the investment performs concerning its downside volatility.

- ➢

The risk-adjusted return of 4.75% is the return adjusted for the assumed risk level. A higher value indicates greater efficiency in relation to the assumed risk.

- ➢

The MAR ratio of 0.18 represents the ratio of annualized return to the highest annualized decline, thus measuring the efficiency of the investment concerning its downside risk. A higher value suggests greater efficiency relative to downside risk.

Given that the analyzed period encompasses events with financial contagion effects, such as the economic crisis of 2007–2009, disruptions like the COVID-19 pandemic, and even the Russia–Ukraine armed conflict, we can argue that the growth recorded in investments despite the impact of financial contagion may suggest that, despite market volatility, Romania’s economy has managed to sustain sustainable growth. A historical volatility of 11.2% indicates a level of risk associated with your investment. This can be interpreted in the context of assessing the risks related to financial contagion on human well-being and sustainable development. With a Sharpe ratio of 0.51, the investment in the BET-FI index demonstrates efficiency concerning the assumed risk, implying effective risk management in the face of financial contagion. A Sortino ratio of 0.75 signifies adept handling of negative volatility, and this efficiency can be considered within the context of sustainable development and human well-being.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}