Mapping Risks Faced by Startup Investors: An Approach Based on the Apriori Algorithm

, , and

, , and

Abstract

:1. Introduction

2. Methodological Procedures

2.1. Review Protocol

2.2. Meta-Analysis

3. Results and Discussions

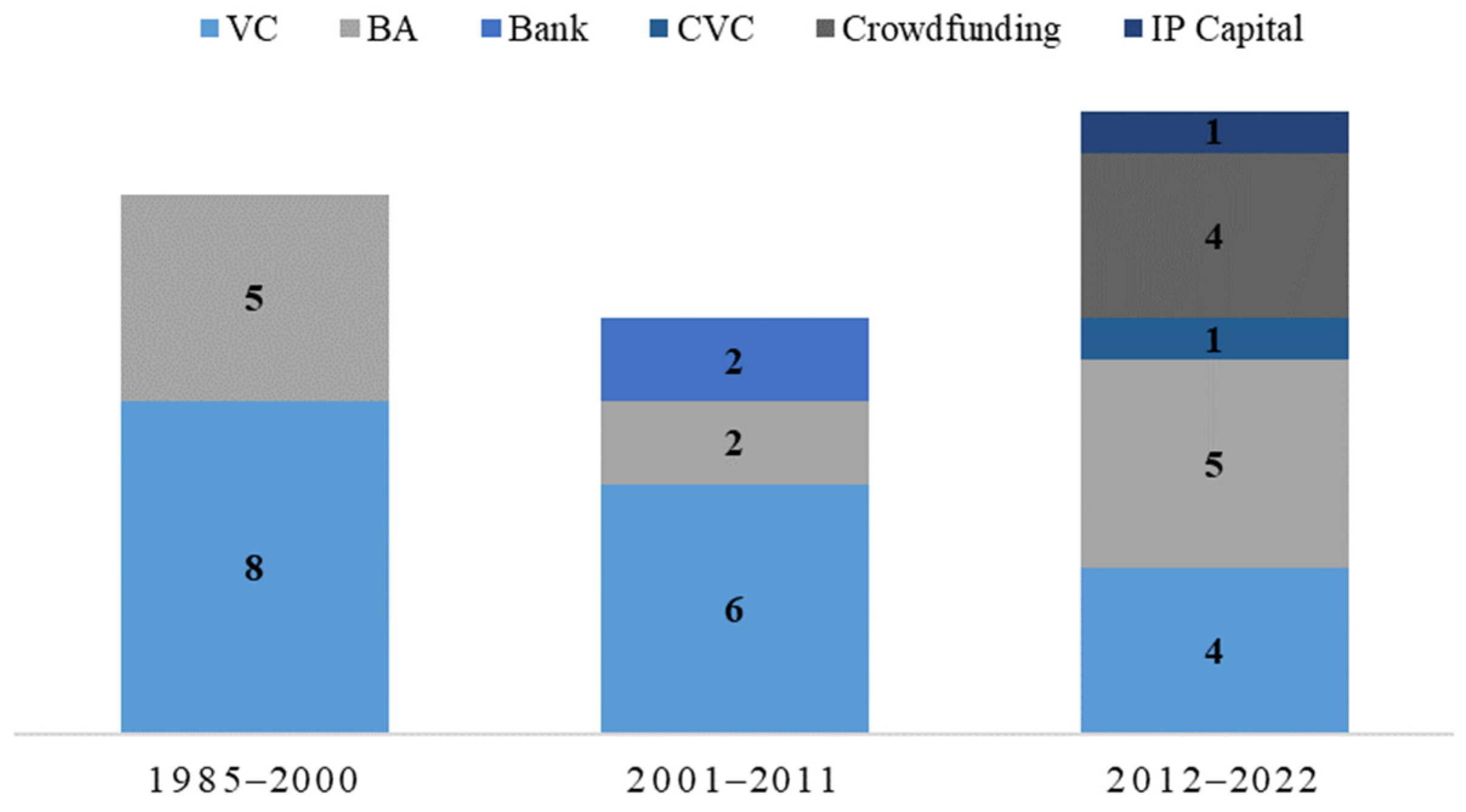

3.1. Overview of the Textual Corpus

3.2. Investment Risks in Startups

3.2.1. External Dimension

3.2.2. Internal Dimension

3.2.3. Human Dimension

3.2.4. Capital Dimension

3.3. Relationship Network between Investment Risks

4. Conclusions

Author Contributions

Funding

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

| References | Journal | Method | Sample | Country |

|---|---|---|---|---|

| Angerer et al. (2018) | Journal of Small Business Strategy | Quantitative | 210 crowdfunding investors | Germany, Switzerland, Austria, and Liechtenstein |

| Bellavitis et al. (2017) | Journal of General Management | Quantitative | 265 investments made in 127 companies by 90 VCs | Belgium, France, Germany, Sweden, Netherlands, UK, and US |

| Carpentier and Suret (2015) | Journal of Business Venturing | Quantitative | 636 projects submitted to a group of BAs | Canada |

| Cowden et al. (2020) | Journal of Small Business Strategy | Theoretical | None | N/A |

| Cumming (2006) | Entrepreneurship: Theory and Practice | Quantitative | 4114 first rounds of investment in startups and growth companies | Canada |

| Cumming et al. (2005) | Financial Management | Quantitative | 18,774 investment rounds taken from the VentureXpert dataset of Venture Economics | US |

| Dugar and Basant (2021) | Journal of Emerging Market Finance | Quantitative | 5782 deals in startups by VCPE (Venture Capital-Private Equity) firms. | India |

| Fiet (1995a) | Journal of Business Venturing | Quantitative | 245 VCs e 849 BAs | US |

| Fiet (1995b) | Journal of Management Studies | Quantitative | 245 VCs e 849 BAs | US |

| Frias et al. (2020) | Journal of Macromarketing | Quantitative | Sample 1: 41 exploratory interviews; Sample 2: 36 angel investors and 70 startup entrepreneurs | US |

| Haar et al. (1988) | Journal of Business Venturing | Quantitative | 121 BAs | US |

| Harrison and Mason (2017) | International Review of Entrepreneurship | Quantitative | 127 BAs | UK |

| Huyghebaert and Van De Gucht (2007) | European Financial Management | Quantitative | 244 manufacturing startups | Belgium |

| Jarchow and Röhm (2020) | Journal of Small Business Management | Qualitative | 6 intellectual property-based investment funds | UK and US |

| Kaplan and Strömberg (2004) | Journal of Finance | Quantitative | 67 investments made by 11 VC firms | US |

| Kleinert and Volkmann (2019) | Venture Capital | Quantitative | 574 discussions in 2258 days of Crowdcube observation | UK |

| Knyphausen-Aufse and Westphal (2008) | Venture Capital | Multiple case studies | 42 investments from a BAs network | Germany |

| Macmillan et al. (1985) | Journal of Business Venturing | Quantitative | 102 VCs | US |

| Mamonov and Malaga (2019) | Venture Capital | Quantitative | 337 startups posted on the Crowdfunder platform | US |

| Mason and Harrison (2004) | Venture Capital | Quantitative | 127 BAs | UK |

| Norton and Tenenbaum (1993) | Journal of Business Venturing | Quantitative | 98 VCs | US |

| Parhankangas and Hellström (2007) | Venture Capital | Quantitative | 90 Investment Managers in 58 VC Firms | Sweden and Finland |

| Polzin et al. (2018) | Technological Forecasting and Social Change | Quantitative | Sample 1: 4 entrepreneurs and 12 investors (VCs and BAs); Sample 2: 6 entrepreneurs and 13 investors (VCs and BAs) | Sweden and Netherlands |

| Rea (1989) | Journal of Business Venturing | Quantitative | 89 VCs | US |

| Reid (1996) | Small Business Economics | Case study | 1 VC and 1 startup | UK |

| Ruhnka and Young (1987) | Journal of Business Venturing | Quantitative | 73 VC firms | US |

| Sapienza et al. (1996) | Journal of Business Venturing | Quantitative | Sample 1: 65 VCs; Sample 2: 76 VCs; Sample 3: 43 VCs; Sample 4: 37 VCs | US, UK, France, and Netherlands |

| Schäfer et al. (2004) | Industry and Innovation | Quantitative | 228 investment observations from KFW bank (45% loan and 55% equity) | Germany |

| Söderblom et al. (2016) | Venture Capital | Multiple case studies | 4 BAs and 4 startup founders | Sweden |

| Van Osnabrugge (2000) | Venture Capital | Quantitative | 119 VCs e 143 BAs | UK |

| Wasiuzzaman et al. (2022) | Journal of Entrepreneurship in Emerging Economies | Quantitative | 169 Equity Crowdfunding investor responses | Malaysia |

| Widyasthana et al. (2017) | Journal of Entrepreneurship Education | Quantitative | 3 startups and 5 support agents (CVC, VCs, government, customer and agent portfolio company) | Indonesia |

| Witt and Brachtendorf (2006) | Financial Markets and Portfolio Management | Quantitative | 89 VC-funded startups | Germany |

References

- Abelha, Marta, Sandra Fernandes, Diana Mesquita, Filipa Seabra, and Ana Teresa Ferreira-Oliveira. 2020. Graduate Employability and Competence Development in Higher Education—A Systematic Literature Review Using PRISMA. Sustainability 12: 5900. [Google Scholar] [CrossRef]

- Agrawal, Rakesh, and Ramakrishnan Srikant. 1994. Fast Algorithms for Mining Association Rules. Paper presented at 20th VLDB Conference, Santiago de Chile, Chile, September 12–15; pp. 487–99. [Google Scholar]

- Akter, Beauty, and Asif Iqbal. 2020. Failure Factors of Platform Start-Ups: A Systematic Literature Review Nordic Journal of Media Management Failure Factors of Platform Start-Ups: A Systematic Literature Review. Nordic Journal of Media Management 1: 433–59. [Google Scholar] [CrossRef]

- Alhammad, Muna M., Chekfoung Tan, Noha Alsarhani, and Izzal Asnira Zolkepli. 2022. What Impacts Backers’ Behavior to Fund Reward-Based Crowdfunding Projects? A Systematic Review Study. Pacific Asia Journal of the Association for Information Systems 14: 90–110. [Google Scholar] [CrossRef]

- Alviz-Meza, Anibal, Juan Orozco-Agamez, Diana C. P. Quinayá, and Antistio Alviz-Amador. 2023. Bibliometric Analysis of Fourth Industrial Revolution Applied to Material Sciences Based on Web of Science and Scopus Databases from 2017 to 2021. ChemEngineering 7: 2. [Google Scholar] [CrossRef]

- Angerer, Martin, Thomas Niemand, Sascha Kraus, and Ferdinand Thies. 2018. Risk-Reducing Options in Crowdinvesting: An Experimental Study. Journal of Small Business Strategy 28: 1–17. Available online: https://www.scopus.com/inward/record.uri?eid=2-s2.0-85062184110&partnerID=40&md5=20be90906585604a651508d319af2189 (accessed on 3 November 2021).

- Asubiaro, Toluwase Victor, and Sodiq Onaolapo. 2023. A Comparative Study of the Coverage of African Journals in Web of Science, Scopus, and CrossRef. Journal of the Association for Information Science and Technology 74: 745–58. [Google Scholar] [CrossRef]

- Audretsch, David B., Max C. Keilbach, and Erik E. Lehmann. 2006. Entrepreneurship and Economic Growth. New York: Oxford University Press. [Google Scholar] [CrossRef]

- Baum, Joel A. C., and Brian S. Silverman. 2004. Picking Winners or Building Them? Alliance, Intellectual, and Human Capital as Selection Criteria in Venture Financing and Performance of Biotechnology Startups. Journal of Business Venturing 19: 411–36. [Google Scholar] [CrossRef]

- Bellavitis, Cristiano, Dzidziso Samuel Kamuriwo, and Ulrich Hommel. 2017. Mitigating Agency Risk between Investors and Ventures’ Managers. Journal of General Management 43: 33–43. [Google Scholar] [CrossRef]

- Bhattacharjee, Jayashree, Ranjit Singh, and K. Kajol. 2021. Risk Perception in Respect of Equity Shares: A Literature Review and Future Research Agenda. DLSU Business and Economics Review 30: 101–19. Available online: https://www.scopus.com/inward/record.uri?eid=2-s2.0-85115745579&partnerID=40&md5=1c3ba11d8404dd863b3dbcc799588051 (accessed on 15 August 2022).

- Bouwman, Harry, Timber Haaker, and Mark de Reuver. 2012. Some Reflections on the High Expectations as Formulated in the Internet Bubble Era. Futures 44: 420–30. [Google Scholar] [CrossRef]

- Brown, Ross, Augusto Rocha, and Marc Cowling. 2020. Financing Entrepreneurship in Times of Crisis: Exploring the Impact of COVID-19 on the Market for Entrepreneurial Finance in the United Kingdom. International Small Business Journal: Researching Entrepreneurship 38: 380–90. [Google Scholar] [CrossRef]

- Bygrave, William D. 1988. The Structure of the Investment Networks of Venture Capital Firms. Journal of Business Venturing 3: 137–57. [Google Scholar] [CrossRef]

- Carpentier, Cécile, and Jean Marc Suret. 2015. Angel Group Members’ Decision Process and Rejection Criteria: A Longitudinal Analysis. Journal of Business Venturing 30: 808–21. [Google Scholar] [CrossRef]

- CB insights. 2021. The Top 12 Reasons Startups Fail. Available online: https://www.cbinsights.com/research/startup-failure-reasons-top/ (accessed on 24 March 2023).

- CB insights. 2022. State of Venture 2022 Recap. Available online: https://www.cbinsights.com/research/report/venture-trends-2022/ (accessed on 20 March 2023).

- Cheng, Maocai, Kaiyong Xu, and Xuerong Gong. 2016. Research on Audit Log Association Rule Mining Based on Improved Apriori Algorithm. Paper presented at 2016 IEEE International Conference on Big Data Analysis (ICBDA), Hangzhou, China, March 12–14; pp. 1–7. [Google Scholar] [CrossRef]

- Cowden, Birton J., Joshua S. Bendickson, Jerrica Bungcayao, and Simona Womack. 2020. Unicorns and Agency Theory: Agreeable Moral Hazard? Journal of Small Business Strategy 30: 17–25. Available online: https://www.scopus.com/inward/record.uri?eid=2-s2.0-85085902928&partnerID=40&md5=6d5d3aecfe432ee0381be6fbf1755ded (accessed on 15 March 2023).

- Criaco, Giuseppe, Tommaso Minola, Pablo Migliorini, and Christian Serarols-Tarrés. 2014. ‘To Have and Have Not’: Founders’ Human Capital and University Start-up Survival. The Journal of Technology Transfer 39: 567–93. [Google Scholar] [CrossRef]

- Cumming, Douglas. 2006. Adverse Selection and Capital Structure: Evidence from Venture Capital. Entrepreneurship: Theory and Practice 30: 155–83. [Google Scholar] [CrossRef]

- Cumming, Douglas, Grant Fleming, and Armin Schwienbacher. 2005. Liquidity Risk and Venture Capital Finance. Financial Management 34: 77–105. [Google Scholar] [CrossRef]

- Da Costa, Matheus Becker, Leonardo Moraes Aguiar Lima Dos Santos, Jones Luís Schaefer, Ismael Cristofer Baierle, and Elpidio Oscar Benitez Nara. 2019. Industry 4.0 Technologies Basic Network Identification. Scientometrics 121: 977–94. [Google Scholar] [CrossRef]

- Dai, Xiaoyong, Gary Chapman, and Hao Shen. 2022. Late-Stage Venture Capital and Firm Performance: Evidence from Small and Medium-Sized Enterprises in China. Applied Economics 54: 2356–72. [Google Scholar] [CrossRef]

- de Carvalho, Patrícia Stefan, Julio Cezar Mairesse Siluk, and Jones Luís Schaefer. 2022. Mapping of Regulatory Actors and Processes Related to Cloud-Based Energy Management Environments Using the Apriori Algorithm. Sustainable Cities and Society 80: 103762. [Google Scholar] [CrossRef]

- Dugar, Poonam, and Rakesh Basant. 2021. Antecedents of Stage-Wise Investment Preferences of Venture Capital and Private Equity Firms in India: An Empirical Exploration. Journal of Emerging Market Finance 20: 264–89. [Google Scholar] [CrossRef]

- Erdogan, Ece, and Somayeh Koohborfardhaghighi. 2019. Delivering a Systematic Framework for the Selection and Evaluation of Startups. In Lecture Notes in Computer Science (Including Subseries Lecture Notes in Artificial Intelligence and Lecture Notes in Bioinformatics). Edited by Massimo Coppola, Emanuele Carlini, Jörn Altmann, José Ángel Banares and Daniele D’Agostino. LNCS. Berlin/Heidelberg: Springer, vol. 11113, pp. 151–59. [Google Scholar] [CrossRef]

- Ferrary, Michel, and Mark Granovetter. 2009. The Role of Venture Capital Firms in Silicon Valley’s Complex Innovation Network. Economy and Society 38: 326–59. [Google Scholar] [CrossRef]

- Ferrati, Francesco, and Moreno Muffatto. 2019. A Systematic Literature Review of the Assessment Criteria Applied by Equity Investors. In Proceedings of the European Conference on Innovation and Entrepreneurship, ECIE. Edited by Panagiotis Liargovas and Alexandros Kakouris. Manchester: Academic Conferences and Publishing International Limited, vol. 1, pp. 304–12. [Google Scholar] [CrossRef]

- Fiet, James O. 1995a. Reliance upon Informants in the Venture Capital Industry. Journal of Business Venturing 10: 195–223. [Google Scholar] [CrossRef]

- Fiet, James O. 1995b. Risk Avoidance Strategies in Venture Capital Markets. Journal of Management Studies 32: 551–74. [Google Scholar] [CrossRef]

- Francescatto, Matheus, Alvaro Neuenfeldt Júnior, Flávio Issao Kubota, Gil Guimarães, and Bruna de Oliveira. 2022. Lean Six Sigma Case Studies Literature Overview: Critical Success Factors and Difficulties. International Journal of Productivity and Performance Management 72: 1–23. [Google Scholar] [CrossRef]

- Freeman, John, and Jerome S. Engel. 2007. Models of Innovation: Startups and Mature Corporations. California Management Review 50: 94–119+4. Available online: https://www.scopus.com/inward/record.uri?eid=2-s2.0-36749077460&partnerID=40&md5=8d97efa222b3488c892f30ba40bd083c (accessed on 3 January 2020). [CrossRef]

- Frias, Kellilynn M., Deidre L. Popovich, Dale F. Duhan, and Robert F. Lusch. 2020. Perceived Market Risk in New Ventures: A Study of Early-Phase Business Angel Investment Screening. Journal of Macromarketing 40: 339–54. [Google Scholar] [CrossRef]

- Garcia, Fabiane Tubino, Carla Schwengber Ten Caten, Elaine Aparecida Regiani de Campos, Aline Marian Callegaro, and Diego Augusto de Jesus Pacheco. 2022. Mortality Risk Factors in Micro and Small Businesses: Systematic Literature Review and Research Agenda. Sustainability 14: 2725. [Google Scholar] [CrossRef]

- Haar, Nancy E., Jennifer Starr, and Ian C. MacMillan. 1988. Informal Risk Capital Investors: Investment Patterns on the East Coast of the U.S.A. Journal of Business Venturing 3: 11–29. [Google Scholar] [CrossRef]

- Harrison, Richard, and Colin Mason. 2017. Backing the Horse or the Jockey? Due Diligence, Agency Costs, Information and the Evaluation of Risk by Business Angel Investors. International Review of Entrepreneurship 15: 269–90. [Google Scholar]

- Hoegen, Andreas, Dennis M. Steininger, and Daniel Veit. 2018. How Do Investors Decide? An Interdisciplinary Review of Decision-Making in Crowdfunding. Electronic Markets 28: 339–65. [Google Scholar] [CrossRef]

- Howcroft, Debra. 2001. After the Goldrush: Deconstructing the Myths of the Dot.Com Market. Journal of Information Technology 16: 195–204. [Google Scholar] [CrossRef]

- Huyghebaert, Nancy, and Linda M. Van De Gucht. 2007. The Determinants of Financial Structure: New Insights from Business Start-Ups. European Financial Management 13: 101–33. [Google Scholar] [CrossRef]

- Jarchow, Svenja, and Andrea Röhm. 2020. Business Builders, Contractors, and Entrepreneurs—An Exploratory Study of IP Venturing Funds. Journal of Small Business Management 61: 1451–96. [Google Scholar] [CrossRef]

- Kaczam, Fabíola, Julio Cezar Mairesse Siluk, Gil Eduardo Guimaraes, Gilnei Luiz de Moura, Wesley Vieira da Silva, and Claudimar Pereira da Veiga. 2022. Establishment of a Typology for Startups 4.0. Review of Managerial Science 16: 649–80. [Google Scholar] [CrossRef]

- Kaplan, Steven N., and Per Strömberg. 2004. Characteristics, Contracts, and Actions: Evidence from Venture Capitalist Analyses. Journal of Finance 59: 2177–210. [Google Scholar] [CrossRef]

- Kleinert, Simon, and Christine Volkmann. 2019. Equity Crowdfunding and the Role of Investor Discussion Boards. Venture Capital 21: 327–52. [Google Scholar] [CrossRef]

- Knyphausen-Aufse, Dodo Zu, and Rouven Westphal. 2008. Do Business Angel Networks Deliver Value to Business Angels? Venture Capital 10: 149–69. [Google Scholar] [CrossRef]

- Landström, Hans, and Roger Sørheim. 2019. The Ivory Tower of Business Angel Research. Venture Capital 21: 97–119. [Google Scholar] [CrossRef]

- Lei, Jiasu, Ning Cao, Jiazhen Zhu, and Zhihui Dai. 2000. Innovation Risks of Hi-Tech Start-Ups and the Key Factors to Success. Paper presented at 2000 IEEE International Conference on Management of Innovation and Technology, Singapore, November 12–15; Beijing: Institute of Electrical and Electronics Engineers Inc., vol. 1, pp. 390–96. [Google Scholar] [CrossRef]

- Ljungqvist, Alexander, and William J. Wilhelm. 2003. IPO Pricing in the Dot-Com Bubble. The Journal of Finance 58: 723–52. [Google Scholar] [CrossRef]

- Macmillan, Ian C., Robin Siegel, and P. N. Subba Narasimha. 1985. Criteria Used by Venture Capitalists to Evaluate New Venture Proposals. Journal of Business Venturing 1: 119–28. [Google Scholar] [CrossRef]

- Mamonov, Stanislav, and Ross Malaga. 2019. Success Factors in Title II Equity Crowdfunding in the United States. Venture Capital 21: 223–41. [Google Scholar] [CrossRef]

- Mason, Colin, and Richard Harrison. 2004. Does Investing in Technology-Based Firms Involve Higher Risk? An Exploratory Study of the Performance of Technology and Non-Technology Investments by Business Angels. Venture Capital 6: 313–32. [Google Scholar] [CrossRef]

- Mason, Colin, Tiago Botelho, and Joe Duggett. 2022. Promoting Cross-Border Investing by Business Angels in the European Union. Regional Studies 56: 1391–403. [Google Scholar] [CrossRef]

- McConnell, Patrick. 2022. The Strategic Risks Facing Start-Ups in the Financial Sector. Journal of Risk Management in Financial Institutions 15: 114–41. Available online: https://www.scopus.com/inward/record.uri?eid=2-s2.0-85128629895&partnerID=40&md5=264f53be039640a7cd2c96f36ac64b51 (accessed on 3 October 2022).

- Min, Hokey, John Caltagirone, and Adrea Serpico. 2008. Life after a Dot-Com Bubble. International Journal of Information Technology and Management 7: 21–35. [Google Scholar] [CrossRef]

- Moher, David, Alessandro Liberati, Jennifer Tetzlaff, and Douglas G. Altman. 2009. Preferred Reporting Items for Systematic Reviews and Meta-Analyses: The PRISMA Statement. BMJ 339: b2535. [Google Scholar] [CrossRef]

- Monte, Karolina. 2023. O Que Foi a Crise de 2008, Quando Grandes Bancos Americanos Faliram. Available online: https://guiadoestudante.abril.com.br/atualidades/o-que-foi-a-crise-de-que-tambem-resultou-na-falencia-de-bancos-americanos/ (accessed on 27 March 2023).

- Neuenfeldt Júnior, Alvaro, Elsa Silva, Matheus Francescatto, Carmen Brum Rosa, and Julio Siluk. 2022. The Rectangular Two-Dimensional Strip Packing Problem Real-Life Practical Constraints: A Bibliometric Overview. Computers & Operations Research 137: 105521. [Google Scholar] [CrossRef]

- Norton, Edgar, and Bernard H. Tenenbaum. 1993. Specialization versus Diversification as a Venture Capital Investment Strategy. Journal of Business Venturing 8: 431–42. [Google Scholar] [CrossRef]

- Obregon, Sandra Leonara, Luis Felipe Dias Lopes, Fabiola Kaczam, Claudimar Pereira da Veiga, and Wesley Vieira da Silva. 2022. Religiosity, Spirituality and Work: A Systematic Literature Review and Research Directions. Journal of Business Ethics 179: 573–95. [Google Scholar] [CrossRef]

- Page, Matthew J., Joanne E. McKenzie, Patrick M. Bossuyt, Isabelle Boutron, Tammy C. Hoffmann, Cynthia D. Mulrow, Larissa Shamseer, Jennifer M. Tetzlaff, and David Moher. 2021. Updating Guidance for Reporting Systematic Reviews: Development of the PRISMA 2020 Statement. Journal of Clinical Epidemiology 134: 103–12. [Google Scholar] [CrossRef] [PubMed]

- Parhankangas, Annaleena, and Tomas Hellström. 2007. How Experience and Perceptions Shape Risky Behaviour: Evidence from the Venture Capital Industry. Venture Capital 9: 183–205. [Google Scholar] [CrossRef]

- Pereira, Luís, Alexandra Tenera, João Bispo, and João Wemans. 2013. A Risk Diagnosing Methodology Web-Based Tool for SME’s and Start-up Enterprises. Paper presented at International Conference on Knowledge Discovery and Information Retrieval and the International Conference on Knowledge Management and Information Sharing, Algarve, Portugal, September 19–22; Lisbon: SCITEPRESS—Science and and Technology Publications, pp. 308–17. [Google Scholar] [CrossRef]

- Polzin, Friedemann, Mark Sanders, and Ulrika Stavlöt. 2018. Do Investors and Entrepreneurs Match?—Evidence from The Netherlands and Sweden. Technological Forecasting and Social Change 127: 112–26. [Google Scholar] [CrossRef]

- Pranckutė, Raminta. 2021. Web of Science (WoS) and Scopus: The Titans of Bibliographic Information in Today’s Academic World. Publications 9: 12. [Google Scholar] [CrossRef]

- Rea, Robert H. 1989. Factors Affecting Success and Failure of Seed Capital/Start-up Negotiations. Journal of Business Venturing 4: 149–58. [Google Scholar] [CrossRef]

- Reid, Gavin C. 1996. Fast Growing Small Entrepreneurial Firms and Their Venture Capital Backers: An Applied Principal-Agent Analysis. Small Business Economics 8: 235–48. [Google Scholar] [CrossRef]

- Reuther, Kevin, Christina Ungerer, Thorsten Posselt, and Guido H. Baltes. 2022. Evaluation and Assessment of Technology-Based Startups: Venture Capitalists’ Approaches in the Seed- and Early-Stage. Betriebswirtschaftliche Forschung und Praxis 74: 371–82. [Google Scholar]

- Ruhnka, John C., and John E. Young. 1987. A Venture Capital Model of the Development Process for New Ventures. Journal of Business Venturing 2: 167–84. [Google Scholar] [CrossRef]

- Santisteban, José, and David Mauricio. 2017. Systematic Literature Review of Critical Success Factors of Information Technology Startups. Academy of Entrepreneurship Journal 23: 1–23. Available online: https://www.scopus.com/inward/record.uri?eid=2-s2.0-85038122680&partnerID=40&md5=4616f548f20faf567f610191694cb622 (accessed on 23 June 2022).

- Sapienza, Harry J., Sophie Manigart, and Wim Vermeir. 1996. Venture Capitalist Governance and Value Added in Four Countries. Journal of Business Venturing 11: 439–69. [Google Scholar] [CrossRef]

- Schäfer, Dorothea, Axel Werwatz, and Volker Zimmermann. 2004. The Determinants of Debt and (Private) Equity Financing: The Case of Young, Innovative SMEs from Germany. Industry and Innovation 11: 225–48. [Google Scholar] [CrossRef]

- Silva Júnior, Claudio Roberto, Álvaro Luiz Neuenfeldt Júnior, Julio Siluk, Vinicius Gerhardt, and Cláudia Michelin. 2022a. Evolution of Start-up Investments: An Overview and Future Research Directions. International Journal of Business Innovation and Research 1: 1. [Google Scholar] [CrossRef]

- Silva Júnior, Claudio Roberto, Julio Cezar Mairesse Siluk, Alvaro Neuenfeldt Júnior, Carmen Brum Rosa, and Cláudia de Freitas Michelin. 2022b. Overview of the Factors That Influence the Competitiveness of Startups: A Systematized Literature Review. Gestão & Produção 29: 1–23. [Google Scholar] [CrossRef]

- Silva Júnior, Claudio Roberto, Julio Cezar Mairesse Siluk, Alvaro Neuenfeldt Júnior, Matheus Francescatto, and Cláudiade Michelin. 2022c. A Competitiveness Measurement System of Brazilian Start-Ups. International Journal of Productivity and Performance Management. ahead-of-print. [Google Scholar] [CrossRef]

- Söderblom, Anna, Mikael Samuelsson, and Pär Mårtensson. 2016. Opening the Black Box: Triggers for Shifts in Business Angels’ Risk Mitigation Strategies within Investments. Venture Capital 18: 211–36. [Google Scholar] [CrossRef]

- Sohl, Jeffrey. 2022. Angel Investors: The Impact of Regret from Missed Opportunities. Small Business Economics 58: 2281–96. [Google Scholar] [CrossRef]

- Song, Michael, Ksenia Podoynitsyna, Hans Van Der Bij, and Johannes I. M. Halman. 2008. Success Factors in New Ventures: A Meta-Analysis. Journal of Product Innovation Management 25: 7–27. [Google Scholar] [CrossRef]

- Tennant, Jonathan. 2020. Web of Science and Scopus Are Not Global Databases of Knowledge. European Science Editing 46: 1–3. [Google Scholar] [CrossRef]

- Tranfield, David, David Denyer, and Palminder Smart. 2003. Towards a Methodology for Developing Evidence-Informed Management Knowledge by Means of Systematic Review Introduction: The Need for an Evidence- Informed Approach. British Journal of Management 14: 207–22. [Google Scholar] [CrossRef]

- Turčínek, Pavel, and Jana Turčínkova. 2015. Exploring Consumer Behavior: Use of Association Rules. Acta Universitatis Agriculturae et Silviculturae Mendelianae Brunensis 63: 1031–42. [Google Scholar] [CrossRef]

- Van Osnabrugge, Mark. 2000. A Comparison of Business Angel and Venture Capitalist Investment Procedure s: An Agency Theory-Based Analysis. Venture Capital 2: 91–109. [Google Scholar] [CrossRef]

- Vazirani, Ashish, and Titas Bhattacharjee. 2021. Entrepreneurial Finance in the Twenty-First Century, a Review of Factors Influencing Venture Capitalist’s Decision. Journal of Entrepreneurship 30: 306–35. [Google Scholar] [CrossRef]

- Wang, Tengfei, Baorong Xiao, and Weixiao Ma. 2022. Student Behavior Data Analysis Based on Association Rule Mining. International Journal of Computational Intelligence Systems 15: 1–9. [Google Scholar] [CrossRef]

- Wasiuzzaman, Shaista, Lee Lee Chong, and Hway Boon Ong. 2022. Influence of Perceived Risks on the Decision to Invest in Equity Crowdfunding: A Study of Malaysian Investors. Journal of Entrepreneurship in Emerging Economies 14: 208–30. [Google Scholar] [CrossRef]

- Widyasthana, G. N. Sandhy, Dermawan Wibisono, Mustika Sufiati Purwanegara, Manahan Siallagan, and Pratiwi Sukmawati. 2017. Corporate Venture Capital Strategy for Selecting Start-up Investments in Indonesia Using an Agent-Based Model: Cases of a Mobile Application Start-up, Payment Solution Start-up and Digital Advertising Start-Up. Journal of Entrepreneurship Education 20: 1–22. Available online: https://www.scopus.com/inward/record.uri?eid=2-s2.0-85031501451&partnerID=40&md5=4ee4f94045a90396b5b72854ccb9eb26 (accessed on 3 November 2021).

- Wink, Rudiger. 2004. Commercialisation of Bio-Pharmaceutical Therapies and Risk Management: The Impact on the Sustainability of Markets for Recombinant Drugs. International Journal of Biotechnology 6: 186–201. [Google Scholar] [CrossRef]

- Witt, Peter, and German Brachtendorf. 2006. Staged Financing of Start-Ups. Financial Markets and Portfolio Management 20: 185–203. [Google Scholar] [CrossRef]

- Yu, Ya-Wen, Yu-Shing Chang, Yu-Fu Chen, and Li-Sheng Chu. 2012. Entrepreneurial Success for High-Tech Start-Ups—Case Study of Taiwan High-Tech Companies. Paper presented at 6th International Conference on Innovative Mobile and Internet Services in Ubiquitous Computing, IMIS, Palermo, Italy, July 4–6; Taichung: Asia University, pp. 933–37. [Google Scholar] [CrossRef]

| Filter | Scopus | Web of Science |

|---|---|---|

| Type | Articles and conference papers | Articles and conference papers |

| Search in | Title, abstract, or keywords | Topic |

| Subject areas | Engineering; Decision Sciences; Business, Management, and Accounting; Economics, Econometrics, and Finance | Economics; Management; Business; Business Finance; Operations Research Management Science; Engineering Industrial; Engineering Manufacturing: Engineering Multidisciplinary |

| Years | No filter | No filter |

| Dimension | Code | Risks | Citations | Percentage |

|---|---|---|---|---|

| External | R1 | Market | 17 | 51.5% |

| R2 | Location | 1 | 3.0% | |

| R3 | Political–Regulatory | 2 | 6.1% | |

| R4 | Intermediary | 1 | 3.0% | |

| Internal | R5 | Valuation | 5 | 15.2% |

| R6 | Product | 16 | 48.5% | |

| R7 | Business model | 2 | 6.1% | |

| R8 | Performance | 5 | 15.2% | |

| Human | R9 | Management | 6 | 18.2% |

| R10 | Credibility | 3 | 9.1% | |

| R11 | Agency | 18 | 54.5% | |

| R12 | Know-how | 3 | 9.1% | |

| Capital | R13 | Financial | 8 | 24.2% |

| R14 | Liquidity | 4 | 12.1% |

| Associations | Rules | ||||

|---|---|---|---|---|---|

| Antecedent | Occurrences as the Antecedent | Successor | Occurrences as the Successor | Confidence | Lift |

| R13—Financial risk | 8 | R6—Product risk | 8 | 1.00 | 2.06 |

| R9—Management risk | 6 | R6—Product risk | 6 | 1.00 | 2.06 |

| R5—Valuation risk | 5 | R6—Product risk | 5 | 1.00 | 2.06 |

| R14—Liquidity risk | 4 | R6—Product risk | 4 | 1.00 | 2.06 |

| R12—Know-How risk | 3 | R9—Management risk | 3 | 1.00 | 5.50 |

| R12—Know-How risk | 3 | R6—Product risk | 3 | 1.00 | 2.06 |

| R10—Credibility risk | 3 | R6—Product risk | 3 | 1.00 | 2.06 |

| R9—Management risk | 6 | R1—Market risk | 5 | 0.83 | 1.62 |

| R5—Valuation risk | 5 | R9—Management risk | 4 | 0.80 | 4.40 |

| R5—Valuation risk | 5 | R1—Market risk | 4 | 0.80 | 1.55 |

| R13—Financial risk | 8 | R1—Market risk | 6 | 0.75 | 1.46 |

| R14—Liquidity risk | 4 | R13—Financial risk | 3 | 0.75 | 3.09 |

| R6—Product risk | 16 | R1—Market risk | 10 | 0.63 | 1.21 |

| R8—Performance risk | 5 | R6—Product risk | 3 | 0.60 | 1.24 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Silva Júnior, C.R.; Siluk, J.C.M.; Neuenfeldt-Júnior, A.L.; Francescatto, M.B.; Michelin, C.d.F. Mapping Risks Faced by Startup Investors: An Approach Based on the Apriori Algorithm. Risks 2023, 11, 177. https://doi.org/10.3390/risks11100177

Silva Júnior CR, Siluk JCM, Neuenfeldt-Júnior AL, Francescatto MB, Michelin CdF. Mapping Risks Faced by Startup Investors: An Approach Based on the Apriori Algorithm. Risks. 2023; 11(10):177. https://doi.org/10.3390/risks11100177

Chicago/Turabian StyleSilva Júnior, Claudio Roberto, Julio Cezar Mairesse Siluk, Alvaro Luis Neuenfeldt-Júnior, Matheus Binotto Francescatto, and Cláudia de Freitas Michelin. 2023. "Mapping Risks Faced by Startup Investors: An Approach Based on the Apriori Algorithm" Risks 11, no. 10: 177. https://doi.org/10.3390/risks11100177