1. Introduction

The

Sukuk rating is crucial, especially in Indonesia, which aggressively promotes

Sukuk investment for infrastructure development. The issues according to

Sukuk investment are primarily related to the success of the problems in integrity, accountability, transparency, and trust of a country to convince investors. Indonesia is still low in terms of good corporate governance (GCG), as seen in the GCG rating. It ranked 57 globally and placed fourth in ASEAN (

World Economic Forum 2019) according to those indicators. The study of the

Sukuk rating cannot be separated from those aspects, especially in the field of accountability, integrity, and transparency of state financial management.

Many previous studies on

Sukuk (Islamic bonds) have been carried out, but not as much on bonds. The determinants of

Sukuk are determined mainly by the firm’s endogenous factors. Meanwhile, in addition to endogenous factors, bonds are also determined by interest rate as the exogenous factors. According to

Zhou (

2021), bond yields, which are an essential determinant in the bond rating, are strongly influenced by short-term interest rates, inflation rates, and economic growth. However, in this study, the interest rate is excluded because

Sukuk and bonds have different values.

Sukuk does not accept interest rates because there is no term interest in Islam. Furthermore,

Dang and Huynh (

2020) postulated that bank credit risk influences people to invest in government bonds, whereas credit and bonds are the most determinants to support economic growth.

Some studies connected

Sukuk ratings with transparency, accountability, and earnings management. They are, however, still partial, studies conducted by

Hassan and Marston (

2019), and

Al-Homsi et al. (

2017). They only discussed the relationship between

Sukuk rating on leverage and current ratio variables.

Agustia and Suryani (

2018) demonstrated the relationship among financial disclosure quality (FDQ), leverage ratio, and interest coverage on the

Sukuk rating, and focused on return on asset,

Sukuk structures, and the

Sukuk rating. In comparison,

Prastiani (

2018),

Ulfa (

2019),

Hassan and Marston (

2019) observed the role of return on investment (ROI), FDQ on bond rating.

Qizam and Fong (

2019) emphasized FDQ, ABRs, and ROI on

Sukuk ratings.

Arundina et al. (

2016) examined total assets, leverage ratio, and current ratio on the

Sukuk rating.

When discussing the Sukuk rating, one needs to explore the asymmetry theory approach that describes the relationship between investors and Sukuk issuing. Both parties have different information; one party has more information than another. For example, the firm’s management has more information than investors about the capital market. The level of this information asymmetry varies from very high to very low. Information asymmetry has a real effect on finance and financial decisions Elements of asymmetry theory include trust, moral hazard, reputation, and opportunistic behavior.

Furthermore, accounting and financial data are expected to minimize conflicts of interest between parties obsessed with interest in the firm (

Jensen and Meckling 1976;

Watts and Zimmerman 1986). Nonetheless, it is generally accepted that accounting and financial data can cause management discretion and is expected to reduce the gap between the relationship of the principal and agent where information asymmetry or information imbalance (asymmetrical information) prevails.

Additionally, the

Sukuk rating needs to be studied from theoretical agency that describes the relationship or contract between the principal and the agent. The principal employs the agent to perform tasks for the principal’s interest, including delegating decision-making authority from the principal to the agent (

Melzatiaa et al. 2019). Agency theory is appropriate to apply to

Sukuk issues, including investment,

Sukuk issuance, and

Sukuk rating. It is similar to the relationship between the principal and agent in agency theory. Agency theory contains many elements, including risk performance, moral hazard, information asymmetry, incentives, cost, and monitoring. The decrease in the theoretical model resulted in the FDQ and ABRs and earnings management variables. The model refers to the asymmetry and agency theories, which affect these three variables and the

Sukuk rating. The theoretical derivation of the model will be explained in

Section 2.

According to

Qizam and Fong (

2019), research on

Sukuk ratings rarely focuses on aspects of FDQ and ABRs. He added that the ABRs variable in the

Sukuk rating was still floating. Unfortunately, these studies mostly adopted short-term measures of FDQ (e.g., information content, accrual quality, or other measures). They did not utilize a large potential of long-term financial information.

Research on the relationship between FDQ and

Sukuk ratings is still mostly focused on the short-term financial information quality in the capital market, the downtrends of

Sukuk ratings, and bond ratings amid the rapid growth of

Sukuk presumably related to the FDQ. Thus, future research needs to develop the determinants of disclosure quality that involve important attributes of financial disclosure and fundamental or ABRs. Further research is needed involving FDQ, ADQ (accounting disclosure quality) and earnings management variables. Previous research shows an inconsistent/unclear relationship between FDQ and

Sukuk ratings, i.e.,

Qizam and Fong (

2019) and

Al-Homsi et al. (

2017) stated that financial reporting quality has a significant negative effect on

Sukuk ratings.

Further research by

Ningrum et al. (

2019),

Prastiani (

2018), and

Ulfa (

2019) shows that there is an indefinite relationship between earnings management and

Sukuk ratings where inconsistencies are still found in the relationship between earnings management and

Sukuk ratings.

Additionally, the imprecise relationship between FDQ and earnings management is shown by

Hassan and Marston (

2019), who assert that if the FDQ is low, the tendency to make earnings management adjustments is higher. In addition, the relationship between the ABR variable and earnings management is indistinct, as found in research by (

Yuwono and Aurelia 2021),

Astuti (

2020),

Ningrum et al. (

2019), and

Ulfa (

2019). They concluded that financial leverage as an indicator of ABRs had an effect on earnings management.

Motivated by these previous studies and research gaps, this research intended to examine the determinants of FDQ on employing proxies of the relevance of ratio (represented by the CMH variable). It reflects the covariant of intrinsic value and market value divided by intrinsic value and book value. Meanwhile, the reliability of the ratio (represented by the VMH variable) demonstrates a variant of market value divided by a variant of book value on the Sukuk rating. Furthermore, this research is aimed to observe ABRs proxied by total debt ratio (total debt/equity) on the Sukuk rating. This research also examines earnings management proxied by the modified Jones model on the Sukuk rating.

This research was conducted in Indonesia because the growth of Sukuk in Indonesia has been increasing from year to year, especially after the Financial Services Authority Regulation (POJK) No. 18/POJK.04/2015 concerning Sukuk Issuance and Requirements.

According sharia capital market statistics—2021 issued by

The Financial Services Authority (

OJK–

Otoritas Jasa Keuangan) the number of

Sukuk issuances increased after the 2015 Financial Services Authority Regulation (

https://www.ojk.go.id/id/kanal/syariah/data-dan-statistik/data-produk-obligasi-syariah/Default.aspx, accessed on 28 February 2022). In 2015, there were 47 outstanding

Sukuk with a total value of IDR 9.9 billion. In 2016, there were 53 outstanding

Sukuk with a total value of IDR 11.8 billion. Then, up to January 2020, the total issuance of

Sukuk was the highest with a total of 142

Sukuk and still outstanding with a total value of IDR 29.66 billion. However, from 2019 to 2020, the growth was quite stagnant, and based on the same source until July 2021, the growth declined, whereas the requirements of

Sukuk fund were very high (

OJK 2021).

Elhaj et al. (

2017) stated that with the increasing growth of significant

Sukuk from year to year, the issue of

Sukuk rating became decisive. Furthermore, there are two types of

Sukuk issued in Indonesia, namely those issued by the government called state

Sukuk or SBSN (State Sharia Bonds) and those issued by companies called corporate

Sukuk. According to

Astuti (

2020), a study on GCG, which consisted of default risk, accountability, disclosure, and transparency, is considered crucial (

Pranoto et al. 2017).

Most of a firm’s assets in the past were tangible assets, such as buildings and machinery. Now ‘magic assets’ (the intangible assets), including brands, corporate image or goodwill, intellectual property, and human assets, are increasingly dominant. In addition, the evolution of modern companies, proliferating into conglomerates, subsidiaries, or leased assets, is also increasingly blurring the firm’s traditional boundaries.

The development of investment models due to the disruptive evolution of ‘magic firms’ requires adjustments in the accounting systems. It needs to reveal relevant and reliable financial information. Islamic Financial Institutions (AAOIFI) is the authorized global institution for developing Sharia Standard (

Bouheraoua et al. 2014) and IAS 38 (

International Accounting Standards Board 2016). In the capital market, most empirical evidence indicates that the quality of financial disclosures, relevance, reliability, and ABRs are highly valued empirically (

Botosan and Plumlee 2013;

Qizam 2011; etc.). However, most studies related to these variables adopted short-term measures and did not utilize the great potential of long-term financial information.

Meanwhile, the current global economy, especially Islamic finance, is growing rapidly, including Sukuk. It is suspected that Sukuk is a safe Sharia fund that does not engage in excessive speculation and has a low trading turnover. It makes Sukuk less volatile than conventional bonds. Therefore, issuers of Sukuk are global and are not only from Islamic countries but also from other Western, African, and Asian countries. Previous issuers of conventional instruments were the UK, South Africa, Luxembourg, and Hong Kong. Currently, the volatility of Sukuk developments is primarily due to the volatility of oil prices. It results in a decline in revenues of USD 300 billion, pushing the budget deficits of the Gulf Cooperation Council (GCC) countries, offering future opportunities and new challenges for Sukuk growth. Consequently, most GCC countries tried to switch to the capital market through the issuance of bonds and Sukuk.

Optimistic future developments for

Sukuk growth have an average of 10% per year. Additionally, it has a positive gap between supply and demand for

Sukuk in upcoming years, i.e., USD 143 billion (2017), USD 178.4 billion (2018), USD 221.1 billion (2019), USD 256.9 billion (2020), and USD 271.3 billion (2021) (

Reuters 2017). Therefore, it needs the quality of Jolly’s financial information to guarantee and support opportunities for a positive response and an optimistic global growth of

Sukuk/bond rating, to ensure trust, transparency, accountability, and credibility. Hence, every country that wants to develop

Sukuk requires globally accepted standards and rules.

Sukuk is regulated by The Accounting Board (AAB) of the Accounting and Auditing Organization for AAOIFI, which has officially issued the financial accounting standard (FAS). FAS 33 (which supersedes earlier FAS 25) that sets out the improved principles for classification, recognition, measurement, presentation, and disclosure of investment in Sukuk, shares, and other similar instruments of investments made by Islamic financial institutions (IFIs/the institutions), in line with Sharia principles. It defines the key types of instruments of Sharia-compliant investments and defines the primary accounting treatments commensurate to the characteristics and business model of the institution under which the investments are made, managed, and held. FAS 34 aims to establish the principles of accounting and financial reporting for assets and businesses underlying the Sukuk to ensure transparent and fair reporting to all relevant stakeholders, particularly including Sukuk holders.

In Indonesia, Sukuk products refer to the Statement of Financial Accounting Standards (PSAK). PSAK 110 was established in 2011 (and revised in 2015). These accounting standards refer to the IFRS (International Financial Reporting Standard) as the reference standard for financial accounting in Indonesia. The government expects the comparability of financial reports between countries to be recognized globally and to be of higher quality through internationally accepted standards.

It is crucial to ensure efficiency in a global competition that requires reliability and relevancy (

Qizam and Fong 2019). Moreover, in the globalization era, every country that wants to be an international business player must pay attention to the above-mentioned issues. It is also essential for policymakers to determine the role of institutions, policy instruments, and factors, which are necessary for attaining higher productivity, efficiency, and profitability and for better withstanding forces of competition on global and regional markets (

Zeibote et al. 2019).

6. Conclusions

The problem in this study was initiated by the inconsistency of the results in previous research, and phenomena gaps which is corporate Sukuk has increased in several year therefore this study employed several variables that is derived from three theory and resulted three variables FDQ, ABRs and EM.

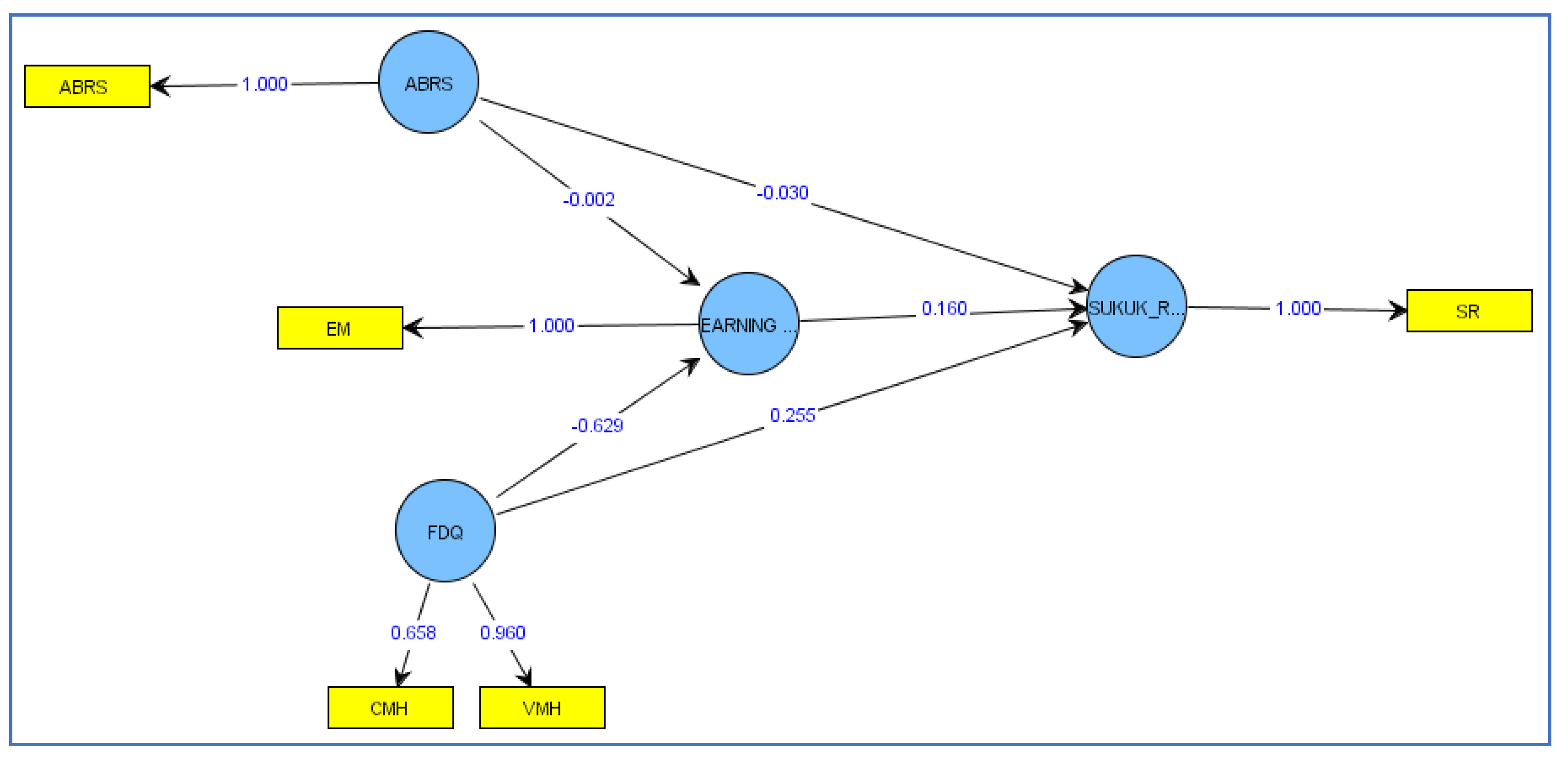

In general, the result of this study in line with agency, asymmetry, and signaling theory. This theory assumed that all stakeholders (especially investor as agent and management as principal) should focus, interest, and pay more attention to their corporate inn order to achieve GCG, so that better firm performance (indicated by its Sukuk rating) can be acquired. This research approved that FDQ and ABRs have significant and positive effects on the Sukuk rating, while earnings management that is misleading or a bad moral hazard has negative effects on the Sukuk rating. This result means giving the signal to firms management to maintain and increase the trust, transference, accountability, and credibility as habit in the corporate culture.

In the context of Sukuk investments as part of Sharia bonds, investors may consider looking at the completeness and quality of the company’s financial statements disclosed to the public compared to measuring earnings management practices and company leverage. Moreover, FDQ represented by the proxy of relevance and reliability of financial statements has a positive and significant effect on Sukuk rating.

Moreover, ABRs represented by the leverage ratio proxy and calculated by the debt-to-equity ratio formula have a keen and significant effect on the Sukuk rating. Earnings management calculated by the modified Jones model affects the Sukuk rating. FDQ, represented by the proxy of relevance and reliability of financial statements, has a negative and significant effect on earnings management. In addition, ABRs affect earnings management. Earnings management cannot correctly mediate the relationship between ABRs and Sukuk ratings. However, it can mediate the relationship between FDQ and Sukuk ratings. The relationship theory used, namely agency and asymmetry theories, including signaling theory, have an essential and significant role in developing the Sukuk rating. All variables derived from the relationship theory significantly affect the Sukuk rating. The next study could add another approach related to investors and principals on the Sukuk investment.

6.1. Research Limitations

This research is still far from perfect. The research object in this study is very varied and heterogeneous. It is homogeneous, consisting of various industries (manufacturing, finance, services, etc.) with different characteristics, but they are treated the same. Hence, the research results can be biased. The FDQ variable is calculated using the market value of the firm’s stock with a limited period of 3 years because the data were not available online before 2018. The number of samples in this study has not reached 1000. Thus, it is not satisfactory to generalize the conclusions.

6.2. Suggestions for Future Research

Based on the limitations of the research and analysis of the tests, several future research plans are the result of increasing Sukuk issuance from year to year and can be interpreted as expanding the firm’s preference to raise business capital from instrument debt in the form of Sukuk. It needs to be balanced with research on Sukuk itself to contribute both theoretically and managerially, especially for investors in choosing investment instruments to avoid the risk of default. Based on the study results, we know that the heterogeneity of the type of industry at the firm affects the hypothesis testing. Hence, it is expected to group the companies for the following research based on the type of industry. Furthermore, it is necessary to explore data to start in 2015, like other countries, and develop comparative studies with other countries such as Malaysia, Bahrain, and the United Arab Emirates.

Future research can add other variables that have not been examined in this study, for example, the

Sukuk structure stated in the rating methodology by

PEFINDO (

Pefindo 2018). There are 2 (two) types of

Sukuk schemes, namely asset-based

Sukuk and asset-backed

Sukuk. In addition, there are also other variables related to guarantees for

Sukuk, according to PEFINDO publications. However, the existence of warranties or guarantees does not significantly affect the possibility of default on bonds/

Sukuk. Even so, the guarantees can immediately recover from the occurrence of defaults with a claim mechanism. Further research is also advised to try other methods of measuring earnings management, such as the

Dechow et al. (

2011) measurement model or real earnings management (REM) calculations instead of the discretionary accrual method. Based on the relationship theory derived from the agency and asymmetry theories, the researchers propose expanding the number of variables in a more detailed way in future research.

and

and

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}