1. Introduction

Portfolio selection is a research topic of primordial importance in financial markets [

1]. It aims to optimally allocate limited resources to a set of assets in order to attain a targeted level of return. The first mathematical formulation of the portfolio selection problem was developed by Markowitz [

2]. The latter defines efficient portfolios as those minimizing the risk for a given expected return or those maximizing the expected return for a chosen level of risk. Despite its several advantages, Markowitz’s model has been criticized since it overlooks many other requirements beyond risk and return [

3,

4,

5]. In order to help investors make sound decisions on portfolio selection, various extensions of Markowitz’s model have been developed over the last few decades. Nevertheless, most of them are still based on quantitative data [

6,

7].

In some cases, historical data are unavailable or are not accurate enough to predict the evolution of the market [

5,

8]. Thus, consulting financial reports and the judgements of expert and/or investor preferences may be an alternative solution. However, such information is often subjective, incomplete, uncertain, or qualitative in nature [

7]. Fuzzy logic theory developed by Zadeh [

9] is a valuable tool for dealing with the epistemic uncertainty resulting from limited or vague information. The basic idea is to transform linguistic variables into fuzzy sets via appropriate membership functions [

10,

11].

Gorzałczany [

12] states that formal fuzzy set representation is not often adequate. It may be difficult for a decision maker (DM) to provide an exact value of the degree of membership of an element. Indeed, in many real-world issues, DMs may express their opinions even when they are not certain about them, inducing a potential hesitation degree between membership and non-membership [

13,

14]. To tackle this challenge, Atanassov [

15,

16] introduces the intuitionistic fuzzy set (IFSs) as another extension of the fuzzy set. To handle uncertain and qualitative information in portfolio selection, many fuzzy decision-making approaches have been developed [

3,

7]. The introduction of fuzzy set theory and its extensions into portfolio selection methods have been an interesting topic of research, especially when it comes to dealing with uncertain parameters [

17].

Tiryaki et al. [

18] compared the performance of two fuzzy-AHP approaches for portfolio selection in the Istanbul Stock Exchange (ISE). Pandey et al. [

19] presented several applications of fuzzy logic in finance that included portfolio optimization. The authors of [

20,

21] incorporated fuzzy set theory and expert opinions regarding traditional allocation asset models such as modern portfolio theory (MPT). Rahiminezhad Galankashi et al. [

1] investigated many other decision-making criteria beyond risk and return, and then they applied a fuzzy analytic network process (FANP) for portfolio selection.

Portfolio selection is a multi-objective optimization (MOO) problem, where the objectives generally conflict with each other. In the real world, one investor may also be interested in choosing her/his preferences for each objective.

Li and Xu [

20] suggested a multi-objective fuzzy portfolio selection model based on a genetic algorithm. Mansour et al. [

22] also proposed a fuzzy multi-objective portfolio selection method considering investor preferences regarding risk, return, and liquidity. Deep et al. [

8] used a fuzzy interactive multi-objective optimization model for portfolio selection. Yu et al. [

23] developed multi-objective linear programming for portfolio selection under an intuitionistic fuzzy environment. The goal was to consider the degrees of nonsatisfaction and the hesitation of DMs regarding different objectives.

The participation of well-informed decision maker is usually required in order to solve a MOO problem [

24,

25]. Depending on his (her) participation in the solving process, MOO methods are generally divided into three categories [

26,

27,

28,

29]: a priori methods, posteriori methods, and interactive methods.

We talk about an a priori method when the DM’s preferences are expressed before the optimization phase. In a posteriori method, the DM provides his/her preferences after the optimization phase. The pareto front is first approximated, and then the DM has to make a choice among the generated solutions. The final category is the interactive method, where the DMs progressively provide their feedback during the optimization process.

The main idea of interactive optimization methods is to dynamically involve the DM in the solving process. Meignan et al. [

27] proposed the so called “human-in-the-loop approach for optimization”, that enables generating intermediate solutions that the DM could assess in order to bring out their biases. Consequently, the preferences are extracted so that the DM’s expectations are reinforced. After the update, the selected preferences are processed within the optimization framework.

Various interactive MOO methods have been suggested over the years. However, no method has outperformed the others in all aspects, seeing that each one has its own pros and cons. The choice may depend on the features of the problem and the decision maker [

28]. Interactive methods may differ from each other according to the type of information given by the DM during the optimization process [

24,

28,

30,

31]. A DM can express his/her preferences as aspiration levels, i.e., desirable values of the objective functions. The DM may also provide a classification of objective functions to specify which function value should be reduced, ameliorated, or preserved. The basic idea of this method is that only some objective values could be improved. An alternative approach is that the DM makes comparisons between several Pareto optimal solutions and then chooses the most appropriate one [

25].

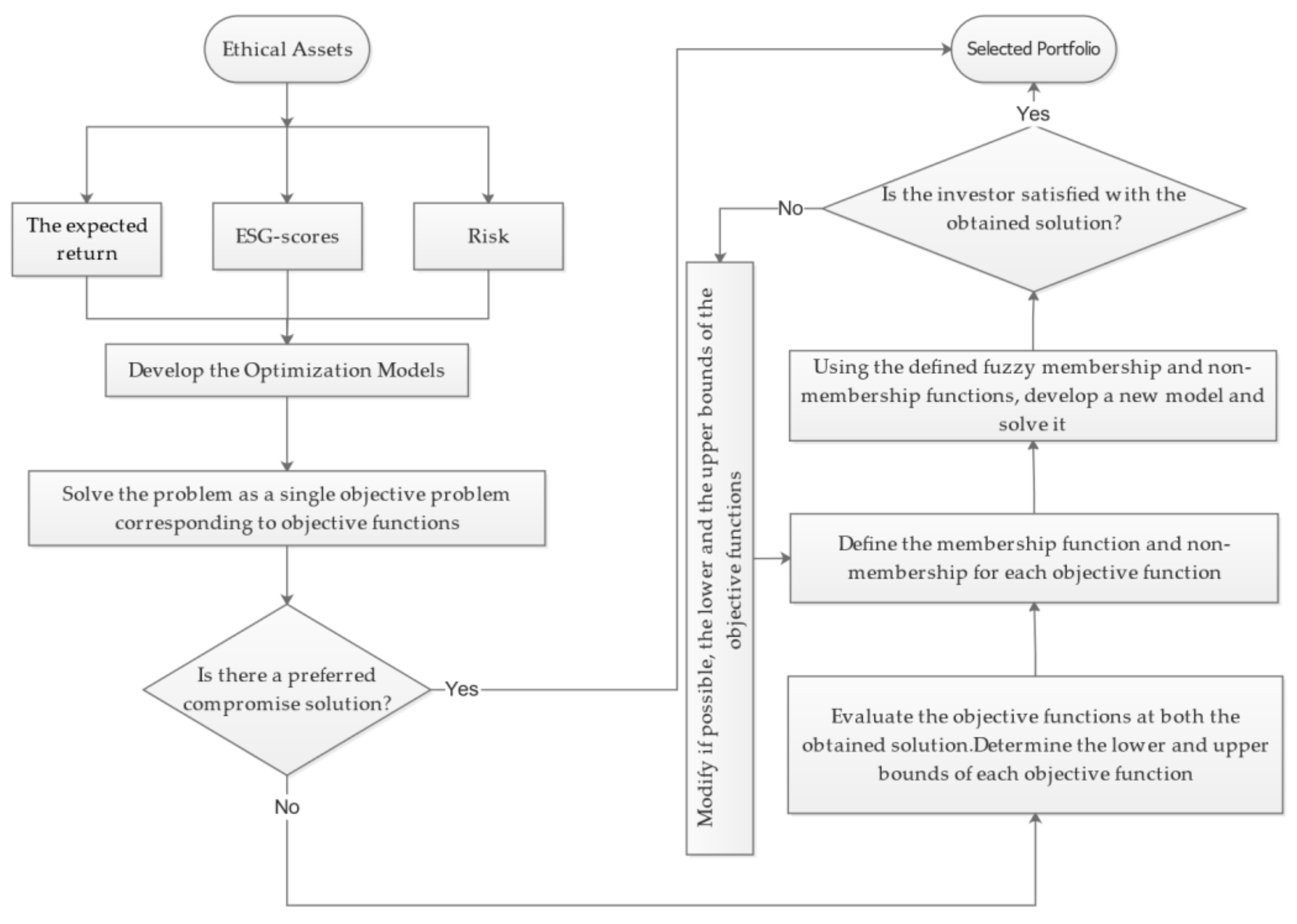

An interactive method usually comprises the following steps:

Show the initial objective vectors to the DM;

Ask the DM to give his/her preferences;

Generate new solution(s) based on the updated preferences;

Go back to step 2 if the DM is dissatisfied or stop.

Interactive approaches have shown their superiority in solving MOO problems compared to many other approaches [

29,

31]. Adopting an interactive approach allows the DM to learn about the feasible solutions progressively and to gain a better understanding of the problem [

25]. The DM can adjust his/her preferences adequately and may also have the ability to directly guide the solving process toward relevant solutions [

27,

29,

30].

According to [

25,

29,

32], coming up with new methods that better support the characteristics of both the decision makers and the studied problem is always required. In many cases, deterministic optimization models are very limited and may not be able to correctly describe real-world problems Angelov [

33].

Combining the desirable features of both fuzzy set theory and interactive multi-objectives methods may provide more chances to achieve a desirable solution, especially when the DM has fuzzy goals for each objective function [

33,

34]. Fuzzy logic can allow a better representation of vagueness and the impreciseness of a DM’s preferences. In a fuzzy environment, the aim of an optimization problem is to find a satisfying solution that maximizes the membership degree [

35].

Garai et al. [

36] emphasized that despite the advantages of fuzzy interactive multi-objective optimization, it could be further ameliorated since other extensions of classical fuzzy set have appeared. Using a multi-objective interactive approach under an intuitionistic fuzzy environment may be more practical, as it considers not only the satisfaction degree (membership) of objectives but the dissatisfaction degree (non-membership) as well [

33,

35]. The ultimate goal of an intuitionistic fuzzy interactive multi objective optimization approach is to find an optimal solution that maximizes the satisfaction degree and that minimizes the dissatisfaction degree [

35]. The DM is progressively asked to update his/her reference level of both the membership and non-membership of a chosen objective function, as determined by Razmi et al. [

35].

Besides risk and return, information about the social policies of companies has become an important determinant of an investor’s decision. Socially responsible investment (SRI) is attracting more and more attention, both in practice and in academia. According to EuroSIF [

37,

38], SRI has increased in recent years, moving from being marginal in the market to being a highly attractive tool for individual investors. In the context of the worldwide growth of SRI worldwide, we have gathered and presented some articles that investigate different aspects of the portfolio optimization process. In particular, Hanine et al. [

6] provide investors that seek to invest only in the ethical assets with a reference tool that meets their needs. The authors use a fuzzy interactive approach to solve a proposed portfolio selection problem. Finally, they prove that investors who are interested in SRI must be ready to pay a minimal financial cost in exchange for ethical goals.

Hallerbach [

39] suggested a multi-criteria decision framework for managing an investment portfolio in which the investment opportunities are described in terms of a set of attributes, and part of this set is intended to capture the effects on society. Calvo et al. [

40,

41] suggested a fuzzy multi-criteria model for mean-variance portfolio selection by considering the social responsibility of the portfolio as an additional secondary non-financial goal. Gasser et al. [

42] revisited Markowitz’ portfolio selection theory and proposed a modification allowing the incorporation of a social responsibility measure into the investment decision making process by proposing a three-objective model based on return, risk, and ESG scores. The authors found that ethical investors prefer to maximize the social impact of their investments when facing a statistically significant decrease in the expected returns. Landi et al. [

43] tried to identify a direct causal relationship between the ESG rating and financial performances, but no evidence was found.

The aim of this study was to suggest a fuzzy intuitionistic interactive approach in order to solve a socially responsible portfolio selection problem and then to compare the finding results with a fuzzy interactive approach [

6,

8]. So far, a very small number of studies have investigated optimal ways to construct socially responsible portfolios by employing optimization methods. This study covers this gap by suggesting an alternative approach that simultaneously maximizes the degree of satisfaction and that minimizes the degree of dissatisfaction of each objective function. The proposed approach allows an investor to control the search direction during the solution procedure and, as a result, to achieve his/her most preferred compromise solution. In addition, if an investor is not satisfied with the obtained portfolio, more portfolios can be generated by updating the lower (upper) bounds of the objective functions. Thus, an investor may have greater confidence in the obtained solution. To the best of our knowledge, this study is the first of its kind, seeing that it uses the interactive intuitionistic fuzzy approach to solve an SR portfolio selection problem.

The remainder of this paper is organized as follows:

Section 2 presents the mathematical model.

Section 3 presents the methodology and research approach.

Section 4 carries out an empirical study applied to the top 10 Stocks for ESG values worldwide and compares the results of the proposed approach with the fuzzy interactive approach.

Section 5 summarizes the main features and findings of the proposed approach and suggests some directions for future research.

5. Conclusions

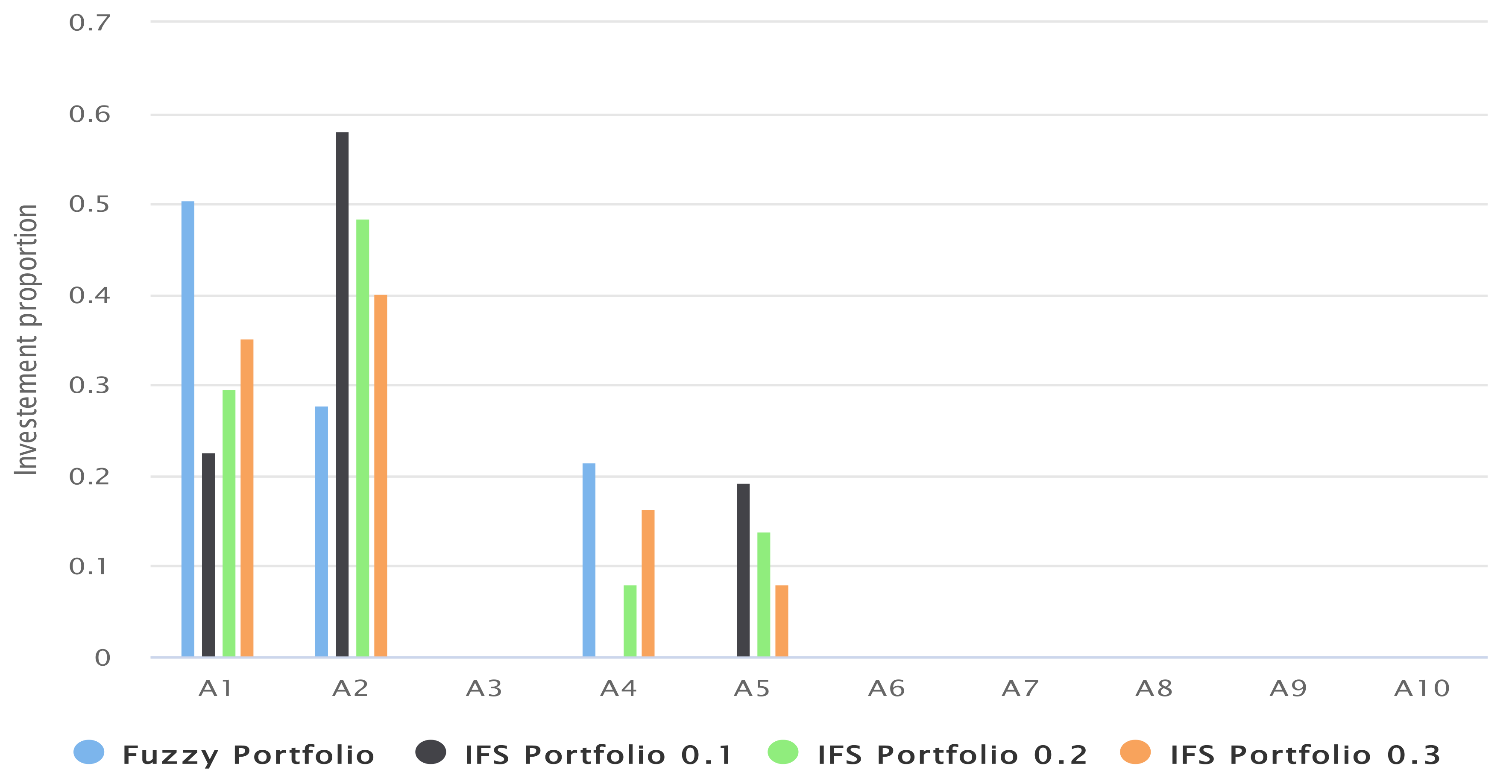

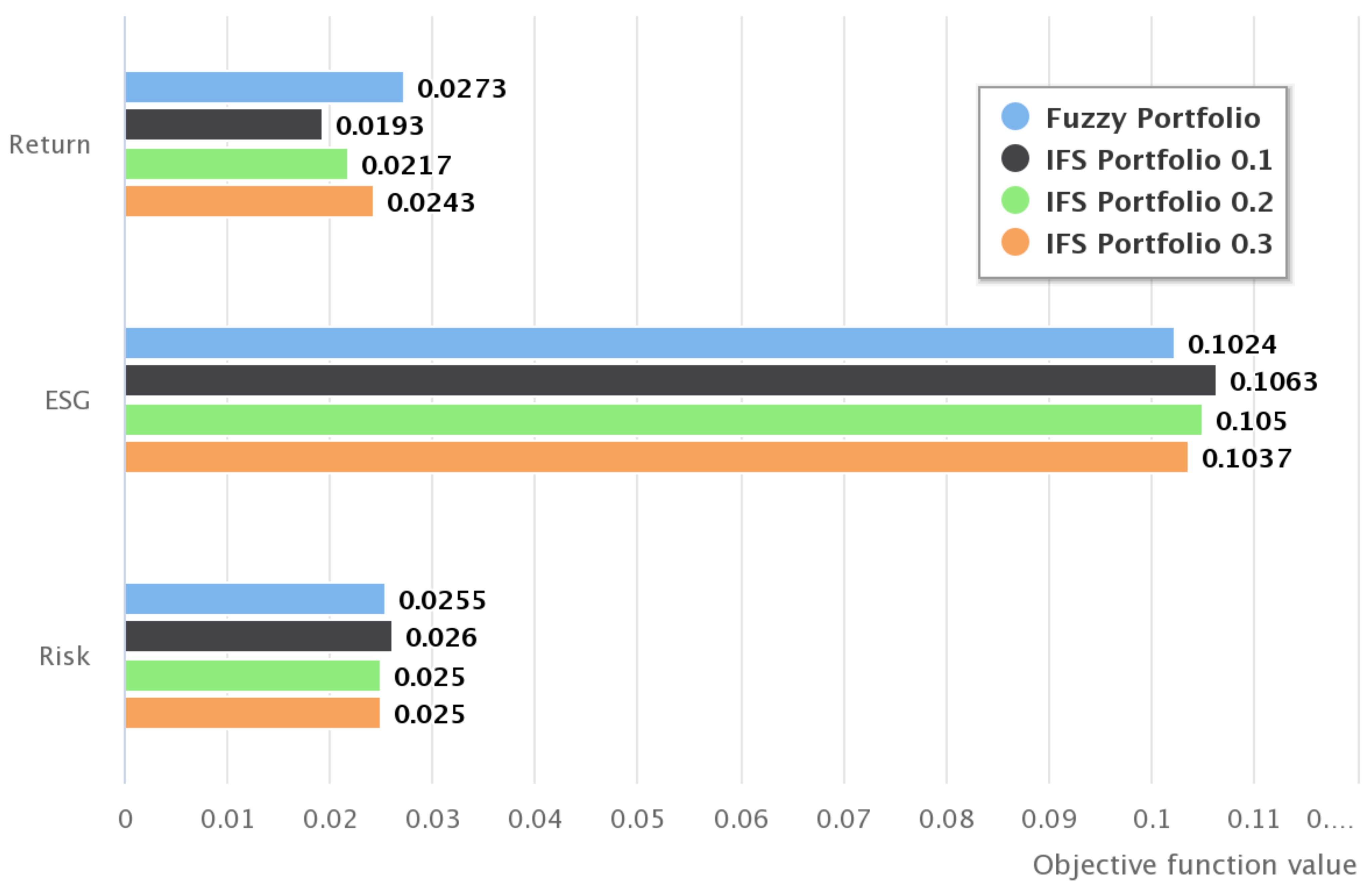

In summary, we have presented an interactive intuitionistic fuzzy approach to solve the SR portfolio selection problem. Besides financial performance, the adopted approach considers the ethical goals of investors as well. Furthermore, it allows DMs to progressively further their understanding of the problem. They will be asked to adjust both their degree of satisfaction and dissatisfaction during the solving process until they reach a preferred compromise solution. In this work, a sample of the 10 top socially responsible stocks was selected to test the robustness of our approach. We compared our approach with the interactive fuzzy approach (one). The results show that the selected assets differ from one approach to another. However, we deem the interactive intuitionistic fuzzy optimization to be more reasonable since it provides a more practical representation of the DM’s uncertainty. For the same degree of acceptance, several optimal solutions could be generated according to the investor’s hesitation. Thus, an investor may have greater confidence in the obtained solution.

This study, however, is not without its limitations; the DM needs to make more effort compared to when using other existent techniques. Additionally, the DM needs to have insight into the problem, be able to adequately express his preferences, and make a comparison between solutions or objectives when necessary. Otherwise, the outcome(s) of the final solution may be undesirable.

Future work should focus on advanced techniques such as deep learning and reinforcement learning that can be used to predict the future returns of stocks [

47]. Predicted returns and past returns could be used together to construct the SRI portfolio. When quantitative data are not available, further research on how to include qualitative evaluation from investors and experts is needed [

7].

Finally, it is worth pointing out that research on intuitionistic fuzzy portfolio selection is only at an early stage. Therefore, we believe that a great deal of future work remains.

{kind=link}

{kind=link}

{kind=link}