An Asymptotic Solution for Call Options on Zero-Coupon Bonds

Abstract

:1. Introduction

2. Previous Literature: Interest Rate Models

Therefore, while today’s models are indubitably more effective (at least in certain respects) than the early ones, and, therefore, one can certainly speak of an ‘evolution’ of interest-rate models, this does not necessary imply that certain choices, abandoned in the past, might not have ultimately led a more fruitful description of interest-rate derivatives products if they had been pursued more actively.[14] (p. 672)

As for the log-normal assumption for the bond price, this was partly satisfactory, because it did not constrain the price to be smaller than face value, thereby assigning a non-zero probability to negative interest rates…What gave greater discomfort, however, was the so-called pull-to-par problem.[14] (p. 683)

Although this is not necessary for what follows, we may suppose that it is a stochastic process–defined on a complete probability space –from which some realization is observed.[15] (p. 82)

3. Derivation of Bond Options on Zero-Coupon Bonds

3.1. A Process for Zero-Coupon Bonds

3.2. Model Definition

4. Solution

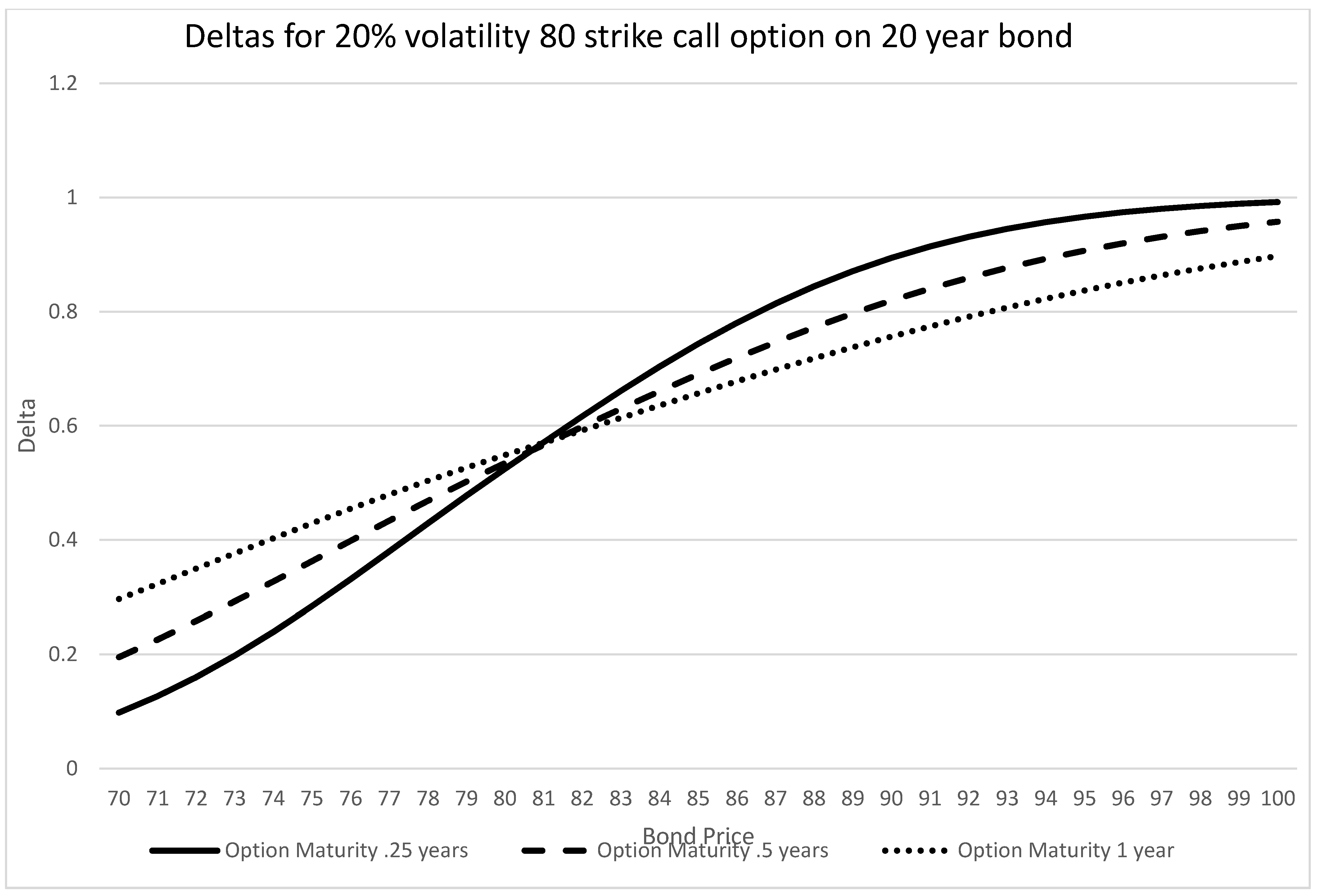

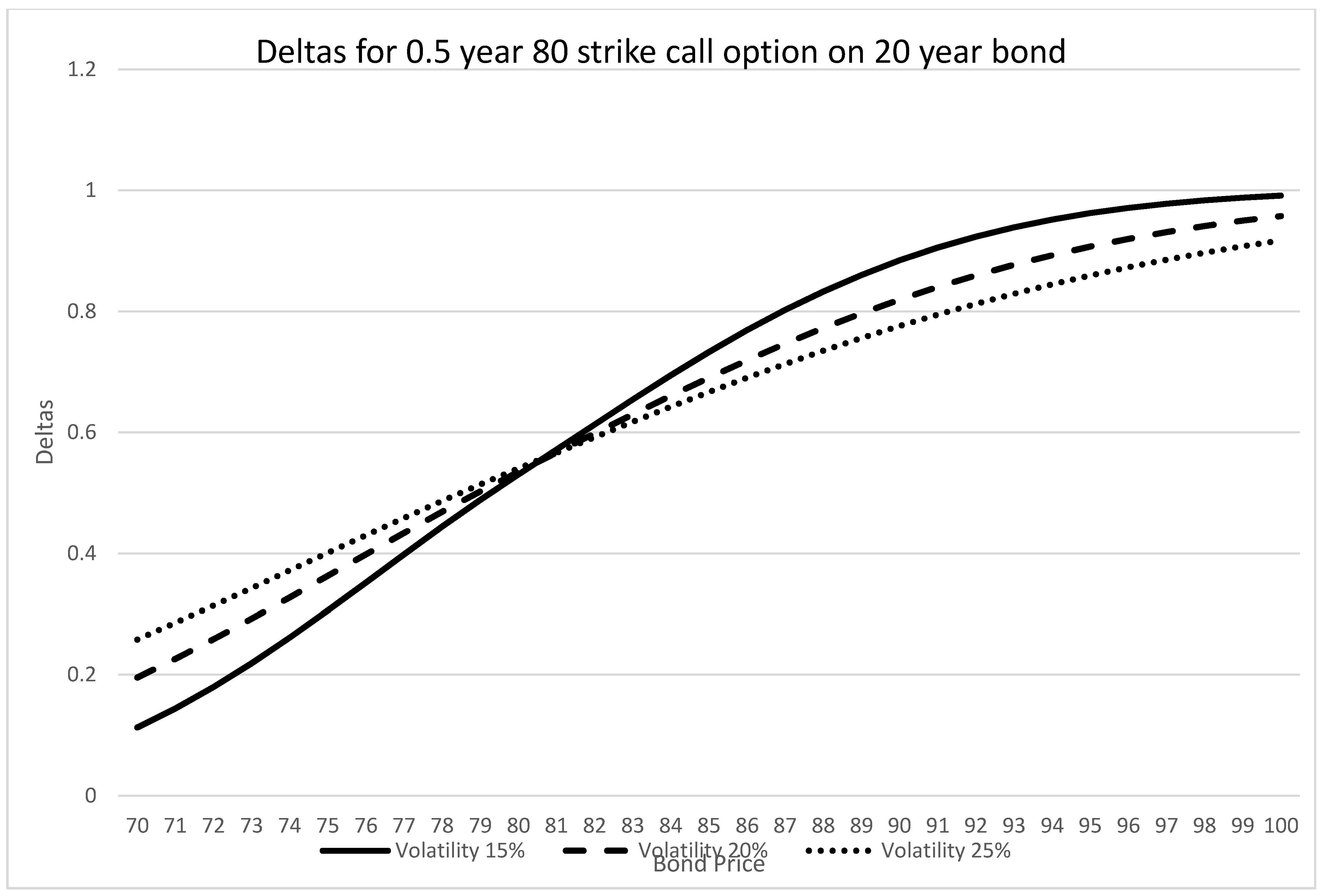

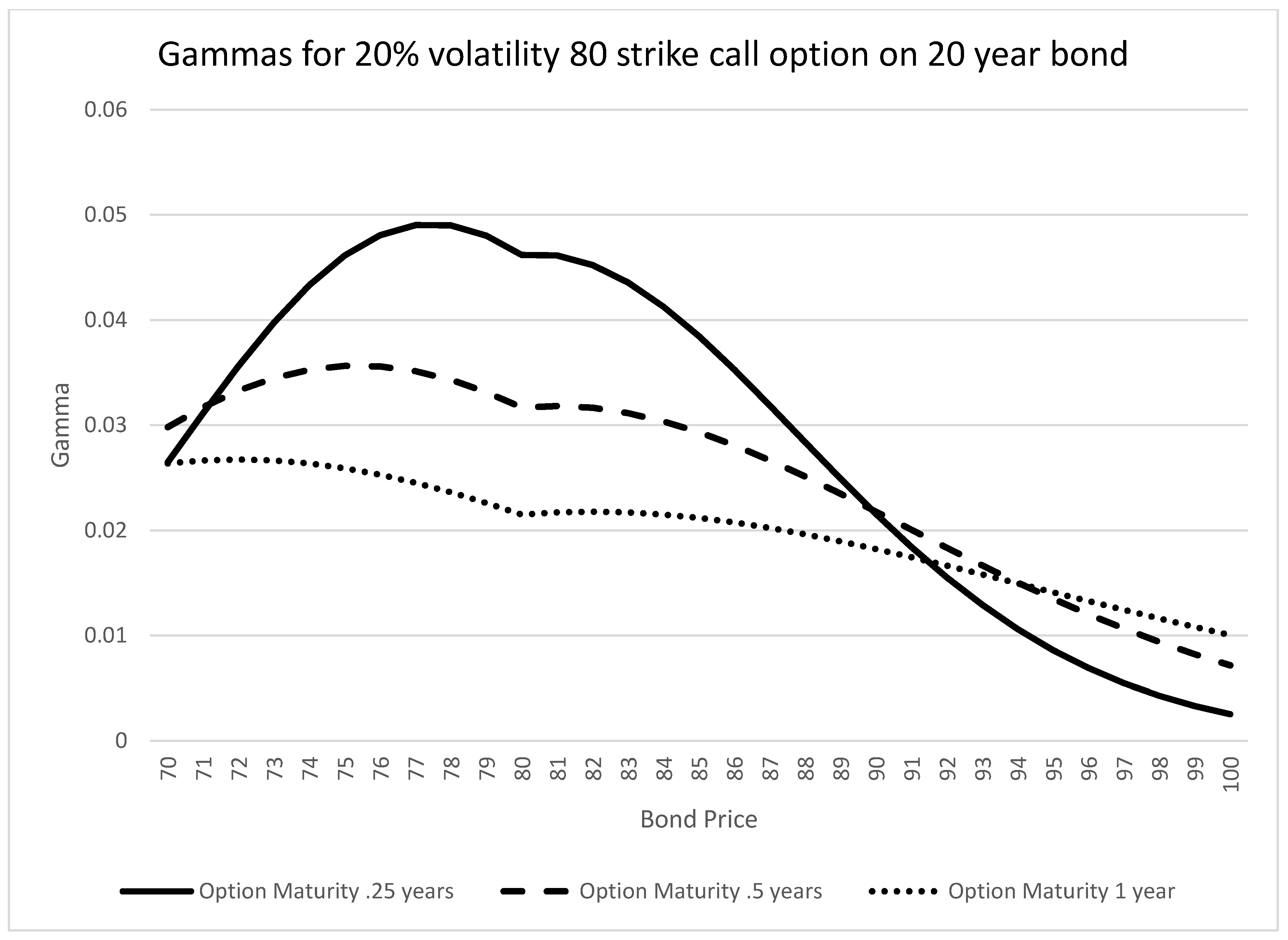

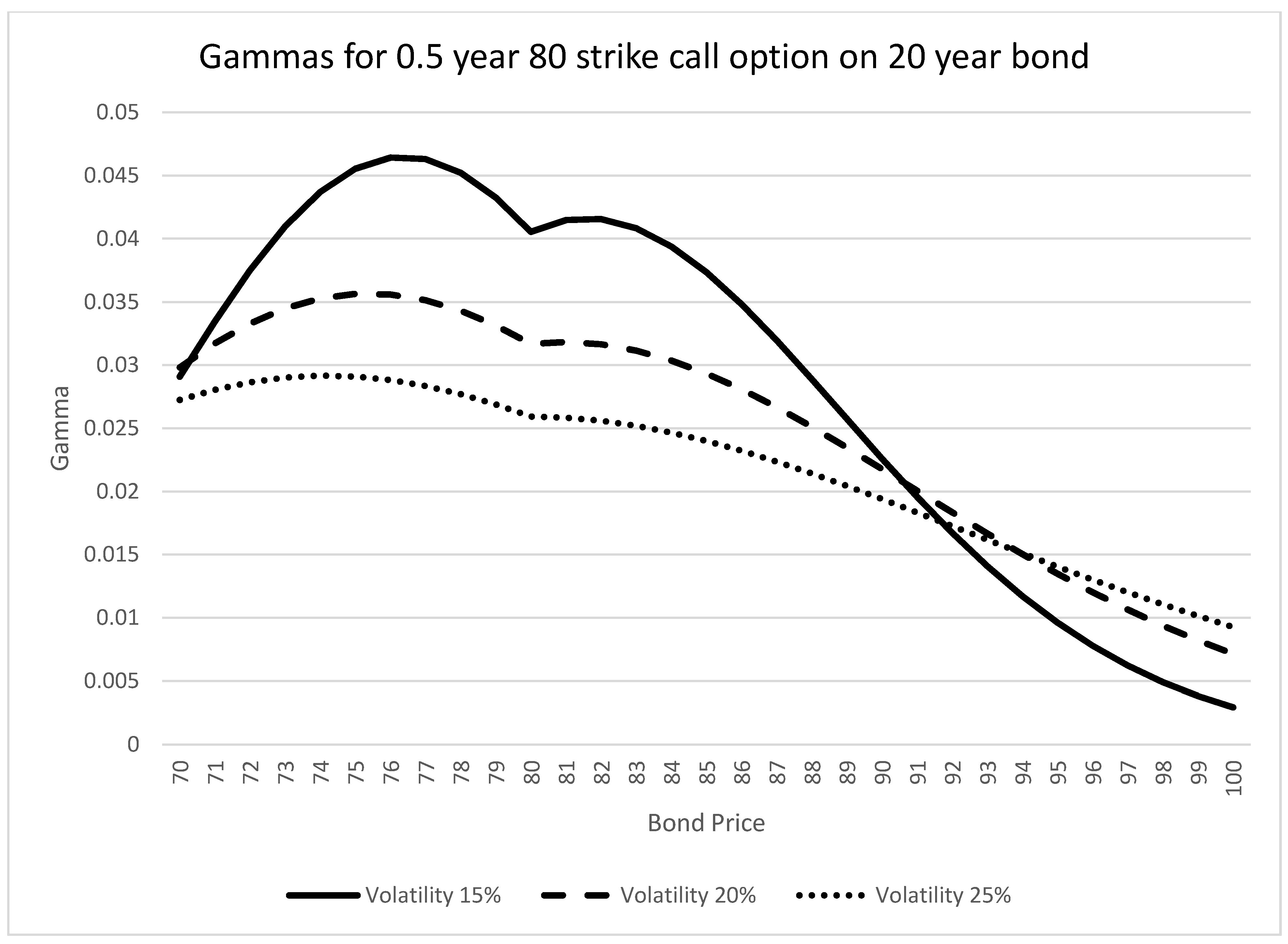

Discussion of Results

5. Properties of Greeks

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A. Derivation of Asymptotic Solution

References

- Black, F.; Scholes, M. The Pricing of Options and Corporate Liabilities. J. Political Econ. 1973, 81, 637–654. [Google Scholar] [CrossRef] [Green Version]

- Vasicek, O.A. An Equilibrium Characterization of the Term Structure. J. Financ. Econ. 1977, 5, 177–188. [Google Scholar] [CrossRef]

- Rendleman, R.; Bartter, B. The Pricing of Options on Debt Securities. J. Financ. Quant. Anal. 1980, 15, 11–24. [Google Scholar] [CrossRef]

- Black, F.; Derman, E.; Toy, W. A One-Factor Model of Interest Rates and Its Application to Treasury Bond Options. Financ. Anal. J. 1990, 46, 24–32. [Google Scholar] [CrossRef]

- Black, F.; Karasinski, P. Bond and Option pricing when Short rates are Lognormal. Financ. Anal. J. 1991, 47, 52–59. [Google Scholar] [CrossRef]

- Jamshidian, F. An Exact Bond Option Formula. J. Financ. 1989, 44, 205–209. [Google Scholar] [CrossRef]

- Ho, T.S.; Lee, S. Term Structure Movements and Pricing Interest Rate Contingent Claims. J. Financ. 1986, 41, 1011–1028. [Google Scholar] [CrossRef]

- Heath, D.; Jarrow, R.; Morton, A. Bond Pricing and the Term Structure of Interest Rates: A Discrete Time Approximation. J. Financ. Quant. Anal. 1990, 25, 419–439. [Google Scholar] [CrossRef]

- Heath, D.; Jarrow, R.; Morton, A. Bond Pricing and the Term Structure of Interest Rates: A New Methodology. Econometrica 1992, 60, 77–105. [Google Scholar] [CrossRef]

- Duffie, D.; Kan, R. A Yield-Factor Model of Interest Rates. Math. Financ. 1996, 6, 379–406. [Google Scholar] [CrossRef] [Green Version]

- Brace, A.; Gatarek, D.; Musiela, M. The Market Model of Interest Rate Dynamics. Math. Financ. 1997, 7, 127–154. [Google Scholar] [CrossRef] [Green Version]

- Musiela, M.; Rutkowski, M. Continuous-time term structure models: Forward measure approach. Financ. Stoch. 1997, 1, 261–291. [Google Scholar] [CrossRef] [Green Version]

- Björk, T.; Gaspar, R.M. Interest rate theory and geometry. Port. Math. 2010, 67, 321–367. [Google Scholar] [CrossRef]

- Rebonato, R. Interest-rate term-structure pricing models: A review. Proc. R. Soc. Lond. Ser. A Math. Phys. Eng. Sci. 2004, 460, 667–728. [Google Scholar] [CrossRef]

- Esquível, M.; Gaspar, R.M.; Beleza Sousa, J. Default Propensity Implicit in Pulled to Par VaR for Bonds. Discuss. Math. Probab. Stat. 2017, 37, 79–99. [Google Scholar] [CrossRef] [Green Version]

- Cox, J.C.; Ingersoll, J.E.; Ross, S.A. A Theory of the Term Structure of Interest Rates. Econometrica 1985, 53, 385–407. [Google Scholar] [CrossRef]

- Kevorkian, J.; Cole, J.D. Perturbation Methods in Applied Mathematics. In Applied Mathematical Sciences; John, F., LaSalle, J.P., Sirovich, L., Eds.; Springer: New York, NY, USA, 1981; Volume 34. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Volatility 15% | ||||||

|---|---|---|---|---|---|---|

| Option Maturity 0.25 Years | Option Maturity 0.5 Years | Option Maturity 1 Year | ||||

| Bond Price | PTP | Black–Scholes | PTP | Black–Scholes | PTP | Black–Scholes |

| 72 | 0.1635 | 0.2140 | 0.6151 | 0.7087 | 1.6037 | 1.7065 |

| 76 | 0.8201 | 0.8820 | 1.6655 | 1.7368 | 3.0303 | 3.0701 |

| 80 | 2.3971 | 2.4419 | 3.4379 | 3.4801 | 4.9730 | 4.9730 |

| 84 | 4.9643 | 5.0273 | 5.8893 | 5.9606 | 7.3626 | 7.4004 |

| 88 | 8.3351 | 8.3938 | 8.9581 | 9.0560 | 10.1888 | 10.2867 |

| Volatility 20% | ||||||

| 72 | 0.5158 | 0.5835 | 1.3647 | 1.4599 | 2.9080 | 2.9788 |

| 76 | 1.4694 | 1.5393 | 2.6761 | 2.7496 | 4.5372 | 4.5614 |

| 80 | 3.1787 | 3.2384 | 4.5485 | 4.6047 | 6.5580 | 6.5580 |

| 84 | 5.6463 | 5.7183 | 6.9416 | 7.0165 | 8.9257 | 8.9488 |

| 88 | 8.7695 | 8.8449 | 9.8153 | 9.9148 | 11.6266 | 11.6935 |

| Volatility 25% | ||||||

| 72 | 0.9935 | 1.0738 | 2.2248 | 2.3227 | 4.2850 | 4.3357 |

| 76 | 2.1610 | 2.2414 | 3.7128 | 3.7936 | 6.0542 | 6.0704 |

| 80 | 3.9599 | 4.0345 | 5.6578 | 5.7280 | 8.1394 | 8.1394 |

| 84 | 6.3730 | 6.4564 | 8.0254 | 8.1087 | 10.5079 | 10.5233 |

| 88 | 9.3322 | 9.4207 | 10.7848 | 10.8881 | 13.1461 | 13.1937 |

| Bond Maturity | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Bond Price | Volatility | Option Maturity | 5 Years | 5 Years | 10 Years | 10 Years | 20 Years | 20 Years | 30 Years | 30 Years |

| O(1) | O(1/T_B) | O(1) | O(1/T_B) | O(1) | O(1/T_B) | O(1) | O(1/T_B) | |||

| 72 | 15% | 0.25 | 57.42% | 42.58% | 72.95% | 27.05% | 84.36% | 15.64% | 89.00% | 11.00% |

| 72 | 20% | 0.50 | 79.32% | 20.68% | 88.47% | 11.53% | 93.88% | 6.12% | 95.84% | 4.16% |

| 72 | 25% | 1.0 | 82.91% | 17.09% | 90.66% | 9.34% | 95.10% | 4.90% | 96.68% | 3.32% |

| 80 | 15% | 0.25 | 97.61% | 2.39% | 98.79% | 1.21% | 99.39% | 0.61% | 99.59% | 0.41% |

| 80 | 20% | 0.50 | 95.35% | 4.65% | 97.62% | 2.38% | 98.79% | 1.21% | 99.19% | 0.81% |

| 80 | 25% | 1.00 | 91.16% | 8.84% | 95.37% | 4.63% | 97.63% | 2.37% | 98.41% | 1.59% |

| 88 | 15% | 0.25 | 97.90% | 2.10% | 98.94% | 1.06% | 99.47% | 0.53% | 99.64% | 0.36% |

| 88 | 20% | 0.50 | 96.14% | 3.86% | 98.03% | 1.97% | 99.01% | 0.99% | 99.34% | 0.66% |

| 88 | 25% | 1.00 | 93.25% | 6.75% | 96.51% | 3.49% | 98.22% | 1.78% | 98.81% | 1.19% |

| Volatility 15% | ||||||

|---|---|---|---|---|---|---|

| Option Maturity 0.25 Years | Option Maturity 0.5 Years | Option Maturity 1 Year | ||||

| Bond Price | PTP | Black–Scholes | PTP | Black–Scholes | PTP | Black–Scholes |

| 72 | 0.0807 | 0.0884 | 0.1794 | 0.1796 | 0.2890 | 0.2762 |

| 76 | 0.2674 | 0.2644 | 0.3518 | 0.3420 | 0.4238 | 0.4076 |

| 80 | 0.5214 | 0.5216 | 0.5304 | 0.5305 | 0.5431 | 0.5431 |

| 84 | 0.7558 | 0.7595 | 0.6945 | 0.7042 | 0.6527 | 0.6677 |

| 88 | 0.9127 | 0.9074 | 0.8328 | 0.8353 | 0.7583 | 0.7715 |

| Volatility 20% | ||||||

| 72 | 0.1567 | 0.1608 | 0.2586 | 0.2557 | 0.3554 | 0.3439 |

| 76 | 0.3288 | 0.3262 | 0.3986 | 0.3919 | 0.4581 | 0.4477 |

| 80 | 0.5246 | 0.5249 | 0.5350 | 0.5352 | 0.5497 | 0.5497 |

| 84 | 0.7057 | 0.7090 | 0.6607 | 0.6676 | 0.6342 | 0.6439 |

| 88 | 0.8470 | 0.8451 | 0.7726 | 0.7771 | 0.7151 | 0.7263 |

| Volatility 25% | ||||||

| 72 | 0.2182 | 0.2205 | 0.3140 | 0.3108 | 0.4003 | 0.3911 |

| 76 | 0.3695 | 0.3677 | 0.4301 | 0.4256 | 0.4832 | 0.4760 |

| 80 | 0.5285 | 0.5289 | 0.5405 | 0.5408 | 0.5576 | 0.5576 |

| 84 | 0.6757 | 0.6783 | 0.6425 | 0.6475 | 0.6264 | 0.6331 |

| 88 | 0.7986 | 0.7981 | 0.7351 | 0.7395 | 0.6919 | 0.7006 |

| Volatility 15% | ||||||

|---|---|---|---|---|---|---|

| Option Maturity 0.25 Years | Option Maturity 0.5 Years | Option Maturity 1 Year | ||||

| Bond Price | PTP | Black–Scholes | PTP | Black–Scholes | PTP | Black–Scholes |

| 72 | 0.0311 | 0.0297 | 0.0375 | 0.0343 | 0.0335 | 0.0310 |

| 76 | 0.0601 | 0.0574 | 0.0464 | 0.0456 | 0.0328 | 0.0341 |

| 80 | 0.0607 | 0.0664 | 0.0405 | 0.0469 | 0.0261 | 0.0331 |

| 84 | 0.0516 | 0.0494 | 0.0394 | 0.0388 | 0.0277 | 0.0288 |

| 88 | 0.0266 | 0.0251 | 0.0289 | 0.0266 | 0.0245 | 0.0229 |

| Volatility 20% | ||||||

| 72 | 0.0356 | 0.0339 | 0.0333 | 0.0316 | 0.0263 | 0.0256 |

| 76 | 0.0485 | 0.0474 | 0.0356 | 0.0357 | 0.0247 | 0.0260 |

| 80 | 0.0468 | 0.0498 | 0.0317 | 0.0351 | 0.0209 | 0.0247 |

| 84 | 0.0417 | 0.0408 | 0.0304 | 0.0306 | 0.0210 | 0.0222 |

| 88 | 0.0284 | 0.0271 | 0.0251 | 0.0240 | 0.0193 | 0.0189 |

| Volatility 25% | ||||||

| 72 | 0.0342 | 0.0329 | 0.0286 | 0.0278 | 0.0214 | 0.0213 |

| 76 | 0.0402 | 0.0397 | 0.0288 | 0.0292 | 0.0198 | 0.0210 |

| 80 | 0.0380 | 0.0398 | 0.0259 | 0.0281 | 0.0173 | 0.0197 |

| 84 | 0.0345 | 0.0341 | 0.0247 | 0.0250 | 0.0169 | 0.0179 |

| 88 | 0.0265 | 0.0256 | 0.0214 | 0.0209 | 0.0157 | 0.0158 |

| Volatility 15% | ||||||

|---|---|---|---|---|---|---|

| Option Maturity 0.25 Years | Option Maturity 0.5 Years | Option Maturity 1 Year | ||||

| Bond Price | PTP | Black–Scholes | PTP | Black–Scholes | PTP | Black–Scholes |

| 72 | −1.5080 | −1.7614 | −1.9599 | −2.0625 | −1.9409 | −1.8967 |

| 76 | −3.7232 | −3.8260 | −3.0916 | −3.0815 | −2.4562 | −2.3523 |

| 80 | −4.9471 | −4.9767 | −3.6125 | −3.5700 | −2.6910 | −2.5720 |

| 84 | −4.1172 | −4.2153 | −3.3577 | −3.3438 | −2.6396 | −2.5313 |

| 88 | −2.2974 | −2.5464 | −2.5534 | −2.6368 | −2.3466 | −2.2848 |

| Volatility 20% | ||||||

| 72 | −3.3608 | −3.5703 | −3.3246 | −3.3592 | −2.8699 | −2.7585 |

| 76 | −5.5126 | −5.5952 | −4.3018 | −4.2647 | −3.3007 | −3.1532 |

| 80 | −6.5250 | −6.5644 | −4.7436 | −4.6870 | −3.5121 | −3.3538 |

| 84 | −5.9483 | −6.0294 | −4.6004 | −4.5597 | −3.5103 | −3.3563 |

| 88 | −4.3202 | −4.5199 | −3.9859 | −4.0052 | −3.3198 | −3.1907 |

| Volatility 25% | ||||||

| 72 | −5.2361 | −5.4112 | −4.6030 | −4.5959 | −3.7367 | −3.5750 |

| 76 | −7.2097 | −7.2880 | −5.4659 | −5.4090 | −4.1214 | −3.9336 |

| 80 | −8.1003 | −8.1493 | −5.8709 | −5.8000 | −4.3274 | −4.1301 |

| 84 | −7.7012 | −7.7795 | −5.8065 | −5.7458 | −4.3632 | −4.1667 |

| 88 | −6.3302 | −6.4976 | −5.3428 | −5.3222 | −4.2452 | −4.0632 |

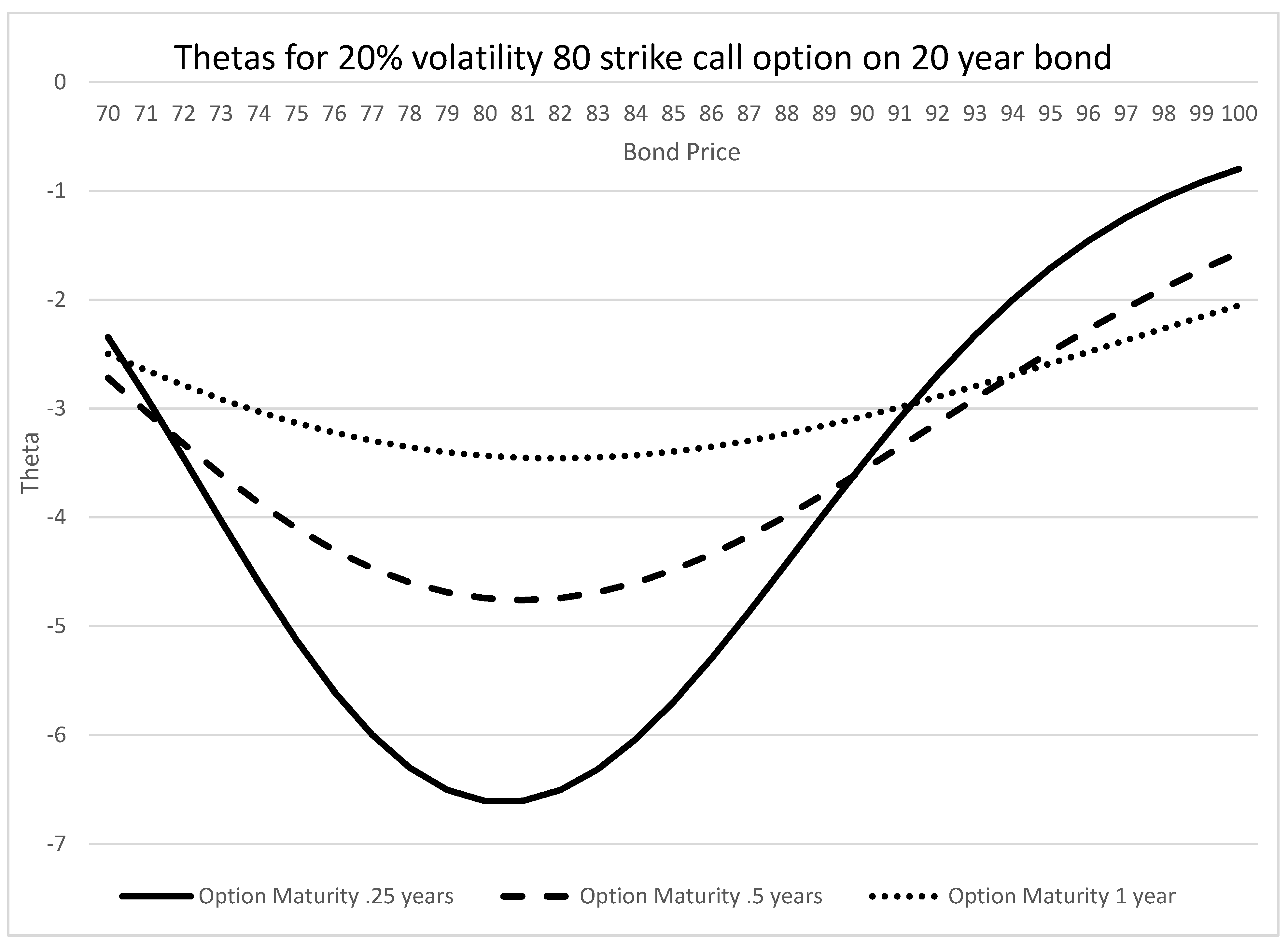

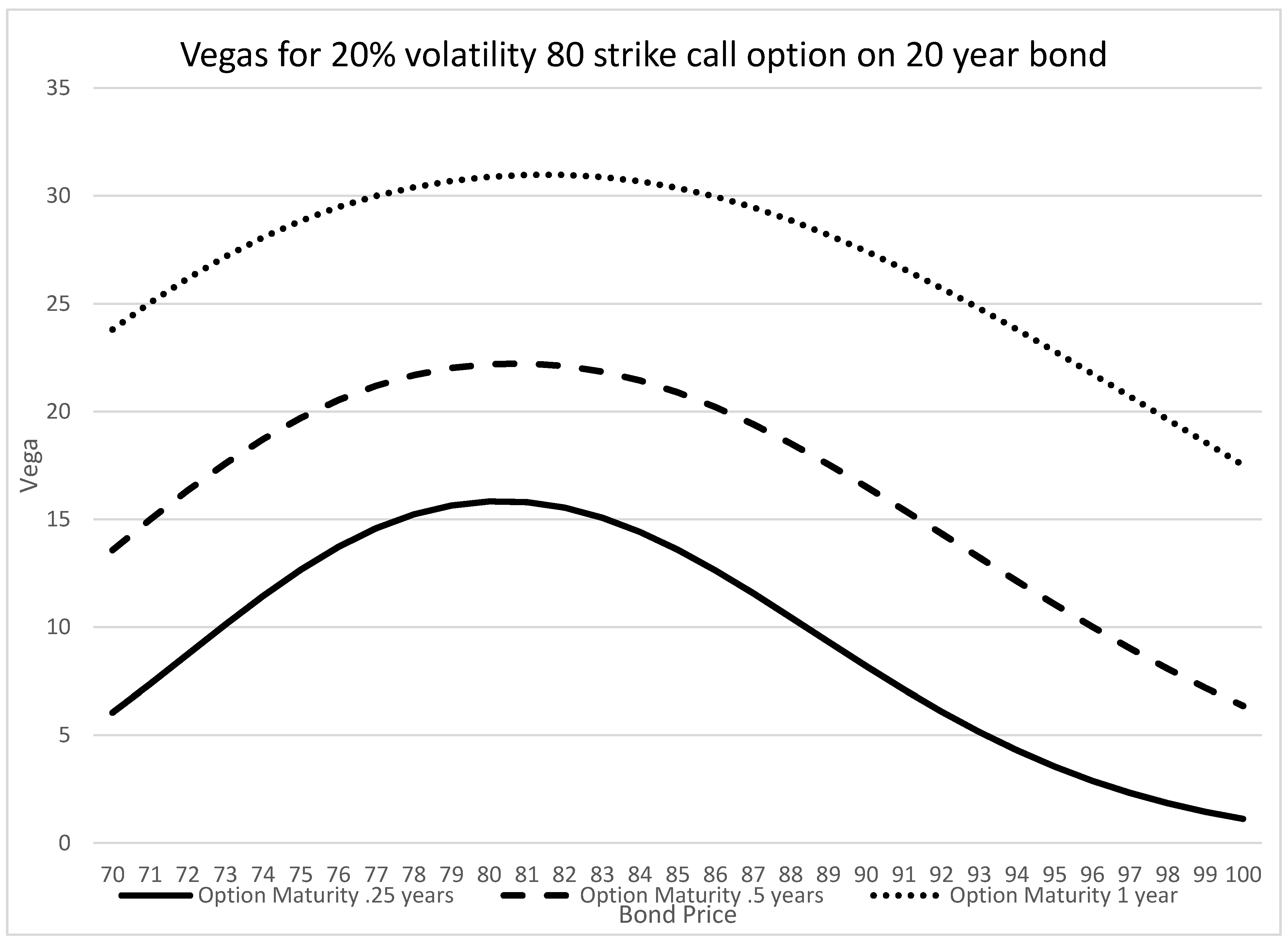

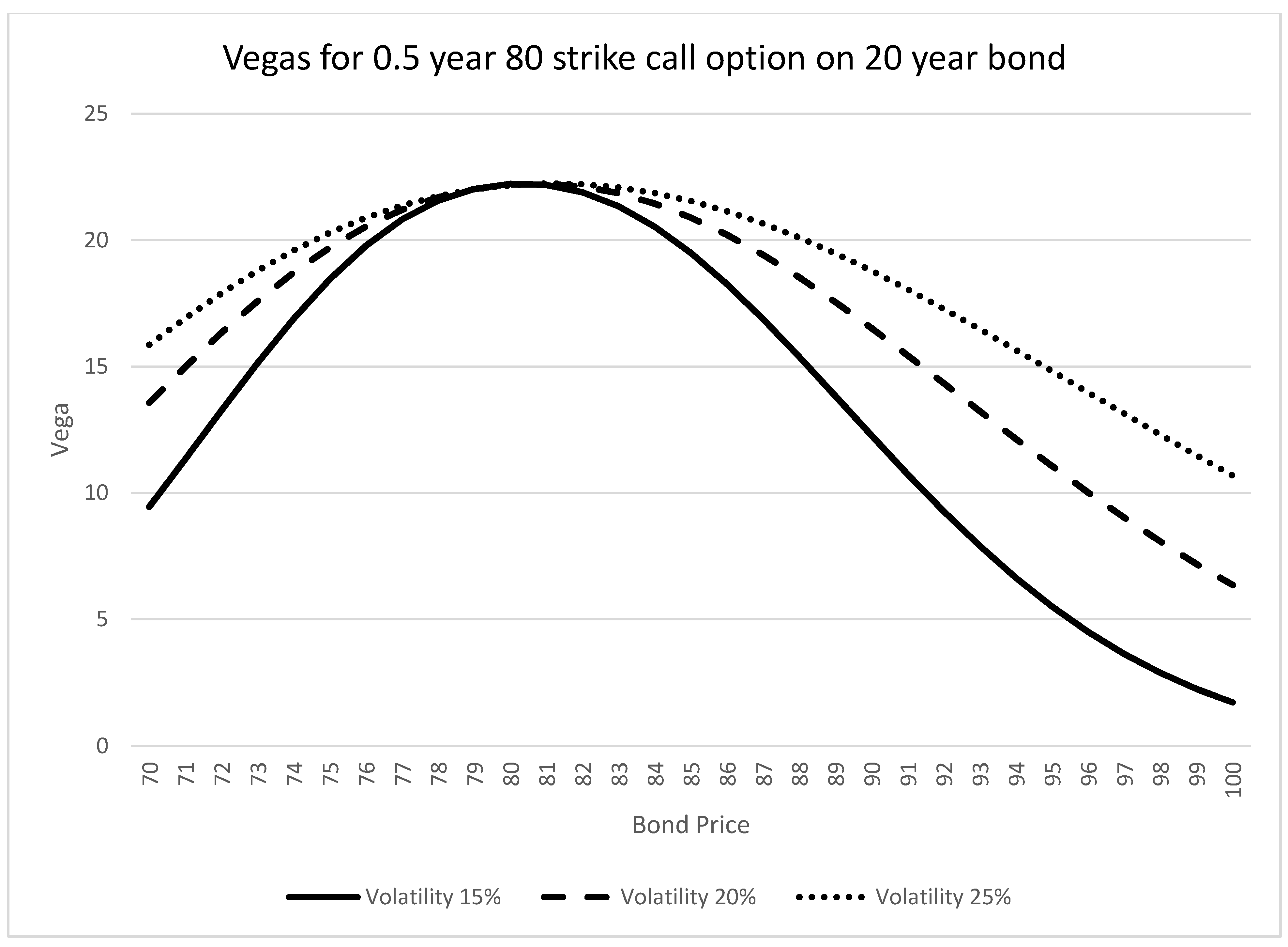

| Volatility 15% | ||||||

|---|---|---|---|---|---|---|

| Option Maturity 0.25 Years | Option Maturity 0.5 Years | Option Maturity 1 Year | ||||

| Bond Price | PTP | Black–Scholes | PTP | Black–Scholes | PTP | Black–Scholes |

| 72 | 5.3239 | 5.7688 | 13.2655 | 13.3423 | 24.8610 | 24.0773 |

| 76 | 12.3032 | 12.4331 | 19.7749 | 19.7351 | 29.9482 | 29.5034 |

| 80 | 15.6359 | 15.9343 | 22.2208 | 22.5015 | 31.7286 | 31.7286 |

| 84 | 12.9213 | 13.0714 | 20.5244 | 20.5186 | 30.9206 | 30.5045 |

| 88 | 6.8675 | 7.2971 | 15.3781 | 15.4301 | 27.3902 | 26.6244 |

| Volatility 20% | ||||||

| 72 | 8.5109 | 8.7884 | 16.3433 | 16.3721 | 27.0008 | 26.4963 |

| 76 | 13.5092 | 13.6974 | 20.5392 | 20.6476 | 30.2736 | 30.0587 |

| 80 | 15.6286 | 15.9266 | 22.1999 | 22.4796 | 31.6670 | 31.6670 |

| 84 | 14.1929 | 14.4005 | 21.4398 | 21.5719 | 31.5097 | 31.3062 |

| 88 | 10.2028 | 10.4806 | 18.5209 | 18.5645 | 29.7817 | 29.2965 |

| Volatility 25% | ||||||

| 72 | 10.4378 | 10.6743 | 17.9003 | 17.9824 | 27.9662 | 27.6470 |

| 76 | 14.0918 | 14.3189 | 20.8875 | 21.0651 | 30.3834 | 30.2648 |

| 80 | 15.6185 | 15.9158 | 22.1708 | 22.4493 | 31.5816 | 31.5816 |

| 84 | 14.8086 | 15.0538 | 21.8605 | 22.0577 | 31.7404 | 31.6274 |

| 88 | 12.1349 | 12.3871 | 20.0960 | 20.2053 | 30.8716 | 30.5674 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Tomas, M.J., III; Yu, J. An Asymptotic Solution for Call Options on Zero-Coupon Bonds. Mathematics 2021, 9, 1940. https://doi.org/10.3390/math9161940

Tomas MJ III, Yu J. An Asymptotic Solution for Call Options on Zero-Coupon Bonds. Mathematics. 2021; 9(16):1940. https://doi.org/10.3390/math9161940

Chicago/Turabian StyleTomas, Michael J., III, and Jun Yu. 2021. "An Asymptotic Solution for Call Options on Zero-Coupon Bonds" Mathematics 9, no. 16: 1940. https://doi.org/10.3390/math9161940