2.1. Modeling under Complete Information

Based on the research of [

25], we first establish a basic common agent model. Suppose a game space

.

represents the participants set: principals

and

(both principals are homogeneous), and

represents the common agent.

denotes the possible outcomes (each associate with specific monetary payoffs for the various principals).

is the agent’s payoff set, where the element

is assumed as follows:

,

, and we have a linear operator

, which denotes the monetary payoffs for the

th outcome paid by an agent for the

th principal, which is a mapping from effort set

to

. Assuming

and

, the agent obtains the corresponding output through their own efforts for principal

.

is the basic wage set, where the superscript

represents the base wage paid to the agent by the

th principal.

is the performance wage set.

is the compensation from the principal to the agent (it can be regarded as the agent’s payoff).

We also assume that the principals are risk-neutral, and their gross payoff is a linear function of the agent’s

:

where the

characterizes the marginal effect of the agent’s output

on

, and

is a noise term with zero mean [

26]. There are personal costs for the agent due to the effort exerted, and we assume that the cost function is a quadratic function:

, where

is the cost coefficient. We follow the assumption by [

26] that the agent’s preferences are represented by the negative exponential utility function

, where

represents the agent’s absolute risk aversion and

is their net payoff (

.).

We assume a linear relationship for the total payoff of a principal:

where

represents the performance coefficient for the

th task. It can capture the marginal output of the agent’s output

with their effort

on the performance measure

.

is the white noise with zero mean and variance

. The

th principal compensates the agent’s output through a linear contract:

Under the above compensation, the net payoff of

th principal is:

. The agent’s certainty equivalent can be expressed as follows:

We design a contract to maximize the principal’s payoff. In this contract, we first guarantee the participation of the agent. Second, under the truthful direct revelation mechanism (Definition 1: The direct revelation mechanism is truthful, if and only if it can guarantee each type of agent reports his real type. It is worth noting that here we are constructing an optimal programming under complete information conditions. That is, the principals know the type of agent. Therefore, we can use truthful direct revelation mechanism.), we guarantee that the agent will exert the maximum effort to maximize the output. Based on our research background, we add a default agreement based on the above basic assumptions. Before signing the contract with the agent, principal

and the agent reach a default agreement: once the agent breaches the contract, principal

will require the agent to pay liquidated damages

, where

is the liquidated damages coefficient. When the agent breaches the contract,

; when the agent does not breach the contract,

. Let

. Therefore, the optimal programming can be expressed as follows:

Proposition 1. There exists an optimal contract if the condition is satisfied.

represents the participation constraint of the agent, and it guarantees that the agent will at least participate. represents the incentive compatibility constraints of the agent. According to the truthful direct revelation mechanism, the agent will truthfully report their type. Proposition 1 reflects two important results: first, the LD coefficient significantly affects the optimal contract; second, the LD coefficient is affected by the type of agent risk. When , the optimal contract degenerates into the standard moral hazard model solution.

To further simulate the default problem of a common agent, we need to make more assumptions about the outputs. Assuming that there is a total output , the sum of each principal’s payoff is equal to —that is, , . However, the more realistic situation is that principal obtains the optimal output relative to principal —namely, a zero-sum game. The interests of the principals are unevenly distributed (a common agent cannot maximize the interests of all principals at the same time). We take football clubs as an example. A good football player is a target for every football club. When a club signs a contract with the player, the football player will represent the football club to participate in football matches and bring maximum benefits to the football club. Therefore, signing for a club will create a conflict of interest with other clubs. In other words, a non-cooperative game will be formed between clubs because of the common agency problem. A football player’s contract is an agreement that sets out the rights and obligations between a player and their employer. A player who terminates the contract without good reason will be liable for a breach of contract. Therefore, one club will play a non-cooperative game with another club.

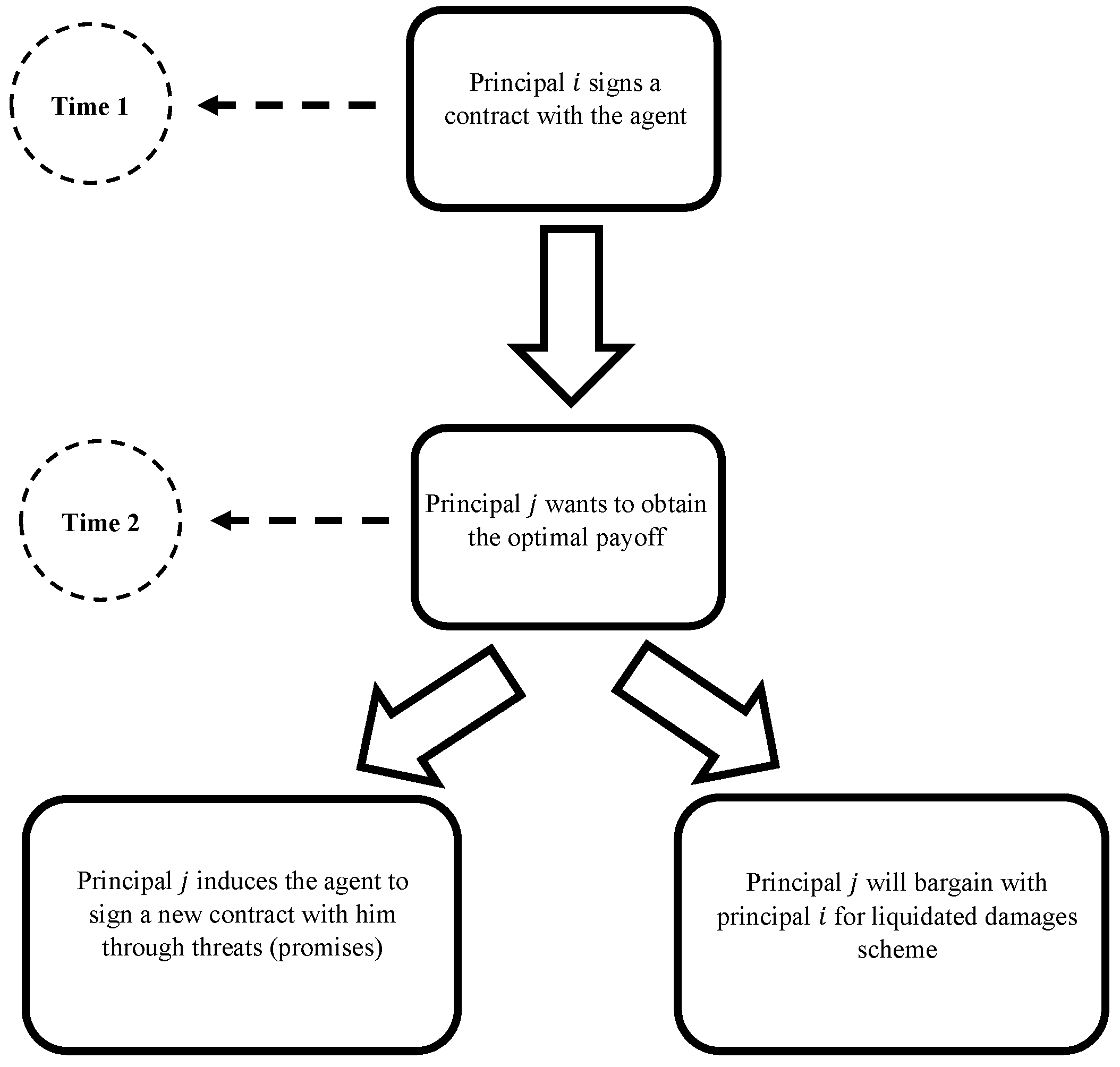

Figure 1 illustrates the entire game and delegation process. First, principal

signs a contract with the agent at time 1. If the agent breaches the contract, they will pay liquidated damages. Second, in order to obtain the optimal payoff at time 2, principal

will persuade the agent to sign a new contract with them and pay LDs to principal

(We use a vivid metaphor: “poaching” and “job-hopping” process. Whether the principal

can successfully “poach” (or whether the agent is willing to “job-hop”) depends on whether the principal

can provide the agent with sufficient “job-hopping” incentives). Meanwhile, principal

will negotiate with principal

regarding LDs until a mutually satisfactory LDs scheme arises.

We show the optimal contract between principal and the agent, and how LDs affect the optimal contract in Proposition 1. We analyze the game process among principal , principal , and agent at time 2 in the following paragraphs.

First of all, it is important to note that our assumptions are within the context of a zero-sum game. There is only one agent, and they can only sign a contract with one principal at a time. That means if they sign a contract with one principal, the other principal will receive zero payoff. Therefore, principal needs to persuade the agent to break the contract and sign a new contract with them.

In order to obtain the optimal payoff, at time 2, principal

will try to persuade the agent to join them.

Figure 2 shows the process of principal

’s persuasions of the agent. The game is divided into four stages. In the first stage, principal

has two choices: resistance or non-resistance. If principal

chooses non-resistance, the payoff between principal

and the agent would be

; if principal

chooses to resist, they would pay the resistance cost

. In the second stage, principal

uses threats to impose a fixed cost

on the agent. In the third stage, the agent faces two choices: acceptance of the requirements from principal

at the second stage or rejecting them. If the agent accepts, the payoff between principal

and the agent will be

, where

and

represents the optimal net payoff of principal

and the agent, respectively. If the agent rejects, the game process goes to the fourth stage. In the fourth stage, principal

chooses to act to fulfil their threat or to give up. If principal

chooses action, they will pay corresponding action costs

. Therefore, when the agent chooses rejection at the third stage and principal

chooses to take action at the fourth stage, the payoffs of both parties are

. In addition, if principal

wants to sign a contract with the agent, they need to pay LDs to principal

. When the agent chooses to reject and principal

chooses to give up, the final payoff would be

. By taking action, principal

forces the agent to sign a contract with them. Since an agent can only have one contract at a time, the agent should first withdraw from the contract signed with principal

and pay LDs before completing the contract with principal

. We summarize the results from the above game with Proposition 2.

Proposition 2. The agent will ultimately choose acceptance if the following conditions are met:.

Two important implications can be obtained from Proposition 2. First, if the cost of resistance is too large, namely , it will cause principal to lose incentives. As long as the principal can create a large resistance cost, it can ensure that other principals choose non-resistance. Second, the agent wants principal to provide a sufficiently high-risk subsidy for the default. That is, the net payoff received by the agent from principal is higher than that received by the agent from principal . When principal and the agent come to an agreement, the agent will choose to default on their contract with principal . Principal will pay LDs to principal .

We thus describe the game between principal

and principal

. Considering the Nash equilibrium in case 2 and substituting

,

, and

into the contract signed between the agent and principal

, we can obtain the following program:

Proposition 3. The optimal wage contract is given byonly if the conditionis satisfied.

Proposition 1 states that there is an optimal contract within the LDs coefficient range . The value of is positively related to the output , basic wage , and performance wage . Therefore, a change in will not only affect the output of the principal, but also affect the net payoff of the agent. is the key coefficient that can affect the whole contract.

Whether the agent can sign a new contract with principal depends on whether principal accepts the LDs proposed by principal . Therefore, principal and principal form a bargaining game (It is an offer-counter-offer process). Principal and need to negotiate an LD to make sense.

Principal

offers principal

an LD scheme. Principal

chooses to accept or reject it. If principal

chooses to accept it, the game ends; if principal

chooses to reject, principal

will put forward a new LD scheme in the next stage, and then principal

chooses to accept or reject it; if principal

chooses to accept, the game ends. If principal

chooses to reject it, principal

will continue to propose another LD scheme, and so on. Therefore,

represent the net output of principal

and

represents the net output of principal

.

and

are the outputs of principal

and principal

when principal

offers the LD scheme, respectively;

and

are the outputs of principal

and principal

when principal

offers the LD scheme, respectively. Suppose the discount factor of principal

and principal

is

and

, respectively. If the game ends at period

, where

is principal

’s bid stage, the payoff discount value of principal

is

,

; the payoff discount value of principal

is

,

.

Figure 3 shows the bargaining game.

We first consider a two-stage bargaining game . In the second stage, principal proposes an LD scheme: . Principal will accept because they have no ability to reject. Therefore, principal ’s payoff in stage 2 is equivalent to their payoff in stage 1. If principal proposes the LD scheme in the first stage, principal will choose to accept it. The subgame perfect Nash equilibrium is . Considering another three-stage bargaining game , in the last stage, principal proposes an LD scheme: . Principal will accept because they have no ability to reject. Therefore, principal ’s payoff in stage 3 is equivalent to their payoff in stage 2. If principal proposes the LD scheme in the second stage, principal will accept. The payoff of principal is . In other words, if principal proposes an LD scheme in the first stage, principal will accept. The subgame perfect Nash equilibrium is .

Theorem 1. , there exists infinite subgame perfect Nash equilibriums in the bargaining game under the common agent situation in two situations:

If, the subgame perfect Nash equilibrium is;

If, the subgame perfect Nash equilibrium is

Theorem 1 shows important implications: when principal puts forward the LD scheme at the last stage, that is, , the LD coefficient presents a positive relationship with the net payoff of principal . Therefore, when principal puts forward the liquidated damage scheme at the last stage, they will increase the coefficient value to maximize their net payoff. Similarly, when principal puts forward the LD scheme at the last stage, that is, , the LD coefficient presents a negative relationship with the net payoff of principal . Therefore, when principal puts forward the LD scheme at the last stage, they will lower the coefficient value to maximize their net payoff.

When principal proposes the LD scheme at the last stage, the LD coefficient they propose will be . This liquidated damage coefficient ensures the maximization of payoffs from their new contract with the agent (see Proposition 1). Moreover, this LD coefficient also influences the agent’s performance wage. However, when principal proposes the LD scheme at the last stage, the LD coefficient they propose may be not in the range: . Under this situation, for principal , the LD proposed by principal will affect their contract with the agent, even though they have to accept such an LD scheme (because it is a subgame perfect Nash equilibrium result). According to the Proposition 1, such results will have a significant impact on the agent’s optimal payoff. Therefore, in the , for principal , how to formulate the LD scheme such that proposed by principal is a problem to be solved. In other words, motivating principal to propose the LD scheme is the problem that principal needs to think about. We first present the following corollary to prove that when , there is a unique subgame perfect Nash equilibrium in the bargaining game.

Corollary 1. When , there exists a unique subgame perfect Nash equilibrium in the bargaining game under a common agent, if the following conditions are satisfied:

Through proof of Corollary 1, can be obtained by ensuring that principal ’s net payoff when principal proposes the LD scheme is equal to the present value of their net payoff : The corollary further states the uniqueness of the subgame perfect Nash equilibrium on the basis of Theorem 1. Since the domain is , there is a conjecture that , . The mapping essentially shifts into . Therefore, the existence of the mapping means that the following assertion can be created.

Corollary 2. When, the infinite subgame perfect Nash equilibrium in the bargaining game under a common agent is Pareto optimal.

Theorem 2. Let. There is a mechanism, such that a unique subgame perfect Nash equilibrium in the bargaining game under a common agent situation exists, ifis a bounded linear operator and bijection.

Figure 4 shows the path of the mapping of principal

. If principal

’s LD coefficient is not in the scope of principal

’s optimal LD coefficient, principal

will enable the mechanism to ensure that principal

’s LD coefficient is within the expected range. After that, both participants will reach an agreement in

through mapping

(Principal

can obtain the payoff in the subgame Nash equilibrium through the mapping

). The process by which principal

reaches a subgame Nash equilibrium is essentially a complex mapping

. Thus, we need to use a mechanism

that causes principal

to believe that principal

’s optimal LD coefficient is at least as good as other LD coefficients. Therefore, we prove homeomorphism between

and

by Theorem 2.

Theorem 2 is a further complement to Theorem 1. We find that for principal , after the introduction of the mechanism , their LD scheme is the same as principal ’s in topological property. In fact, is a mechanism to ensure that the LD coefficient proposed by principal (the first mover) is in agreement with that proposed by principal , because for any situation where , the first-mover always has an incentive to put forward a scheme (see Proposition 1). The late-mover must devise a mechanism to force the first-mover to act in accordance with the late-mover’s LD scheme.

Theorem 2 ensures that there is a mechanism such that the principal has an incentive to choose . Combined with Corollary 2, we can conclude that only when can the LD generate the Pareto optimal solutions to solve the principal–principal conflicts under common agency.

We have completed the discussion of the whole process presented in

Figure 1 under the condition of complete information. We discuss how the liquidated damage mechanism affects the optimal contract and principal–principal conflicts in the case of a common agent. In the

Section 3, we will discuss the effect of the liquidated damage mechanism under incomplete information on the optimal contract in the case of a common agent.

2.2. Modeling under Incomplete Information

We assume that the agent’s real risk aversion

is private information, where

is the upper bound of

and

is the lower bound of

. The principals do not know the real risk aversion of agent, only its distribution function

and probability density function

. We assume that principal

’s real type

is private information to principal

. Principal

does not know the real type of principal

, only its distribution function

and probability density function

. For agents, the real type of principals is public information [

26].

Reconsider

Figure 1. At time 1, principal

signs a contract with the agent and due to the incomplete information, program (1) can be changed to the following (following the method from [

26]):

When , substituting into IR, let , and , we introduce the Lemma 1 (Meng and Tian, 2013):

Lemma 1. The surplus functionand performance wage functionare implementable ([

26]

explained convex in detail: “Defining the convex functions is through representing them as maximum of affine functions, that is,is convex if and only if, for someand some″). if and only if: Substituting

into the

, we get:

Thus, based on the Lemma 1, the program (3) can be changed to the following form:

We summarize the optimal solution of program (4) as follows:

Proposition 4. When default occurs, there exists an optimal contractunder unobservable risk aversion of the agent, if.

Proposition 4 implies another condition: . The common feature of Proposition 1 and 4 is that the LD coefficient significantly affects output and performance wage. However, Proposition 3 requires more stringent conditions. Under incomplete information, the optimal contract between principal and the agent should be based on the risk-seeking type of agent. This means that the agent needs to have greater tolerance for risk under an incomplete information situation.

At time 2, principal

will start a game with the agent under the condition of incomplete information. Before analyzing this game, we first need to analyze the types of agents. If principal

finally forces the agent to cancel the contract with principal

and sign a new contract, under incomplete information, principal

and the agent obtain the optimal contract through the following planning:

Using Lemma 1, we summarize the optimal contract as the following proposition:

Proposition 5. If, then there exists an optimal contract.

Proposition 5 shows that only when will the optimal contract be generated between principal and the agent. There is no constraint on in the necessary conditions of Proposition 4. Therefore, principal can accept any LD scheme when . Using Proposition 4, we obtain the possible types of agent in time 2.

Figure 5 shows the game between principal

and the agent under incomplete information. With incomplete information, the game between principal

and the agent transforms into a typical signaling game. Again, in the first stage, principal

has two choices: resistance or non-resistance. If principal

chooses non-resistance, the payoff between principal

and the agent is

; if principal

chooses to resist, they will pay a resistance cost

. In the second stage, principal

requests a fixed cost

from the government to end resistance. However, in the next stage, it is different from the stage in the game we described in

Section 2. Nature [

27] first chooses the type of agent. Principal

only knows the probability density function

of the agent’s type. The agent then has two signals, rejection or acceptance, while principal

has two choices, action or giving up.

Our other assumptions are the same as in

Section 2. In particular, when the agent type is

and if the principal chooses to take an action, their final payoff will be

. Similarity, their final payoff will be

, when the agent type is

.

Theorem 3. There exists a subgame perfect Bayesian Nash equilibrium, if the following conditions are satisfied:.

Theorem 3 shows a very important implication: there exists a subgame perfect Bayesian Nash equilibrium under incomplete information, and this equilibrium enables principal to sign a new contract with the agent. The conditions for denote that as long as principal pays a high enough amount to the agent, they will have an incentive to sign a new contract. In other words, the agent has an incentive to “job-hop.” This is important because it means that even though the information is incomplete, the agent can reach an agreement with principal through the signaling mechanism.

Figure 6 shows the negotiation game between principal

and principal

on the LD scheme. One practical issue we need to emphasize is that the information type for principal

is public information (the reason for this is that principal

learns about principal

through the common agent), while principal

’s information is private information. Suppose that the probability of principal

choosing rejection is

and the probability of choosing acceptance is

,

. After

negotiations, the negotiations are entirely completed. According to the sequential equilibrium, if

. At stage

, principal

provides a quotation, principal

chooses whether to reject it, and then the game ends. Similar to the situation under perfect information, there exists a subgame perfect Nash equilibrium in the multi-principal negotiation mechanism under incomplete information. We describe it in Theorem 4.

Theorem 4. There is an optimal liquidated damage, such that a sequential equilibrium exists, if the following conditions are satisfied:,andis a bijection.

Theorem 4 proves that there is also an LD scheme which ensures that both sides come to an agreement under incomplete information. The two conditions in Theorem 4 ensure the existence of a maximum and the existence of inverse operators, respectively. We divided the proof of Theorem 4 into two cases: the game ending with principal and the game ending with principal . These two different situations correspond to two different LDs. The most important reason is that the information of principal is private to principal , which leads to the need for principal to guess the action of principal through the distribution function. Through the backward recursion method, we determine the optimal liquidated damages in the first stage, which means that as long as the LD coefficient provided by principal (or ) in the first stage is not less than or ), principal (or ) will choose to accept. Furthermore, combining Proposition 4, we find that if , principal will choose to accept the LD scheme at the first stage. However, for principal , there is no constraint at the first stage of the proposed LD scheme, being in the range . Thus, if the negotiation time increases, the negotiation cost will increase. If principal makes an offer first, since principal knows principal ’s information, principal ’s LD scheme in the first stage can make principal accept. As a result, negotiation costs will be significantly reduced. This means that the negotiation initiated by principal has a cost advantage. The conclusion of Theorem 4 also implies that LDs can effectively resolve principal–principal conflicts because of the existence of a sequential equilibrium which ensures that both parties reach a consensus agreement. Applying the findings of Corollary 2, there is also a mechanism that enables principal to choose to accept the scheme in the first stage.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}