Can FinTech Applied to Payments Improve Consumer Financial Satisfaction? Evidence from the USA

Abstract

:1. Introduction

2. Previous Literature Review and Hypotheses

2.1. Financial Satisfaction

2.2. Mobile Payments and Consumer Financial Satisfaction

2.3. The Mediating Role of Financial Education and Financial Capability

3. Methodology

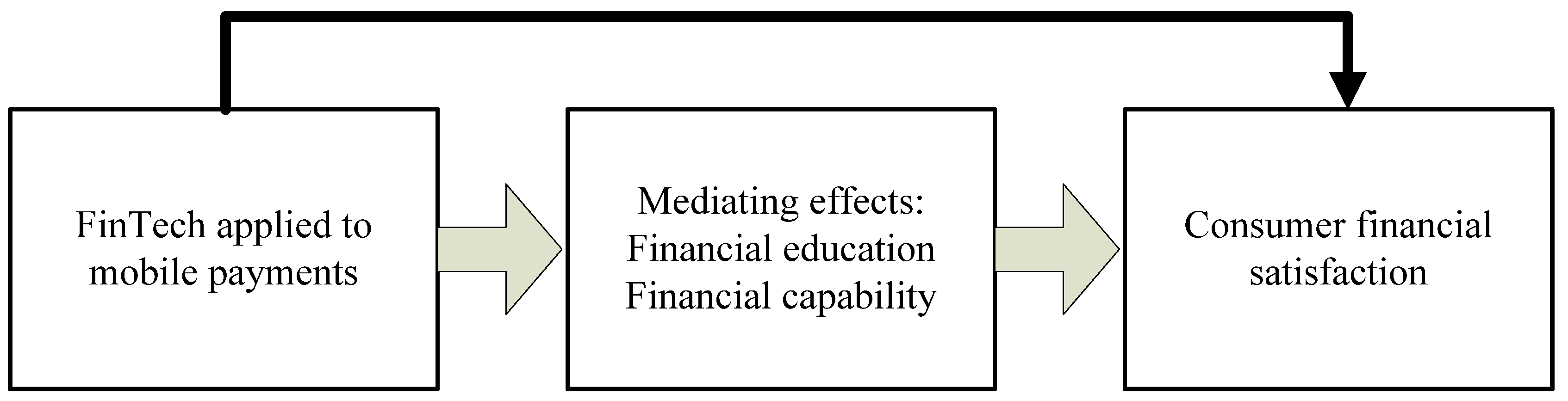

3.1. The Conceptual Framework

3.2. Data

3.3. Variables

3.4. Estimation Method

3.5. Statistical Description

4. Empirical Results

4.1. Results of Correlation Analysis

4.2. Results of Multiple OLS and Ordered Probit Regression

4.3. Robustness Check

4.4. Mediating Effects of Financial Education and Financial Capability

5. Conclusions and Implications

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Agarwal, S.; Zhang, J. FinTech, lending and payment innovation: A review. Asia Pac. J. Financ. St. 2020, 49, 353–367. [Google Scholar] [CrossRef]

- Alkhowaiter, W.A. Use and behavioural intention of m-payment in GCC countries: Extending meta-UTAUT with trust and Islamic religiosity. J. Innov. Knowl. 2022, 7, 100240. [Google Scholar] [CrossRef]

- Teo, A.-C.; Tan, G.W.-H.; Ooi, K.-B.; Hew, T.-S.; Yew, K.-T. The effects of convenience and speed in m-payment. Ind. Manag. Data Syst. 2015, 115, 311–331. [Google Scholar] [CrossRef]

- Agarwal, S.; Chua, Y.H. FinTech and household finance: A review of the empirical literature. China Financ. Rev. Int. 2020, 10, 361–376. [Google Scholar] [CrossRef]

- Zhang, L.; Kim, H. The influence of financial service characteristics on use intention through customer satisfaction with mobile fintech. J. Syst. Manag. Sci. 2020, 10, 82–94. [Google Scholar]

- Chen, M.A.; Wu, Q.; Yang, B. How valuable is FinTech innovation? Rev. Financ. Stud. 2019, 32, 2062–2106. [Google Scholar] [CrossRef] [Green Version]

- Patel, K.J.; Patel, H.J. Adoption of internet banking services in Gujarat: An extension of TAM with perceived security and social influence. Int. J. Bank Mark. 2018, 36, 147–169. [Google Scholar] [CrossRef]

- Rahman, M.; Ismail, I.; Bahri, S. Analysing consumer adoption of cashless payment in Malaysia. Digit. Bus. 2020, 1, 100004. [Google Scholar] [CrossRef]

- Liao, S.-H.; Ho, C.-H. Mobile payment and mobile application (app) behavior for online recommendations. J. Organ. End User Com. 2021, 33, 1–26. [Google Scholar] [CrossRef]

- Ali, A.; Rahman, M.S.A.; Bakar, A. Financial satisfaction and the influence of financial literacy in Malaysia. Soc. Indic. Res. 2015, 120, 137–156. [Google Scholar] [CrossRef]

- Ngamaba, K.H.; Armitage, C.; Panagioti, M.; Hodkinson, A. How closely related are financial satisfaction and subjective wellbeing? Systematic review and meta-analysis. J. Behav. Exp. Econ. 2020, 85, 101522. [Google Scholar] [CrossRef]

- Hsieh, C.-M. Correlates of financial satisfaction. Int. J. Aging Hum. Dev. 2001, 52, 135–153. [Google Scholar] [CrossRef] [PubMed]

- Chen, F.; Hsu, C.-L.; Lin, A.J.; Li, H. Holding risky financial assets and subjective wellbeing: Empirical evidence from China. N. Am. J. Econ. Financ. 2020, 54, 101142. [Google Scholar] [CrossRef]

- Joo, S.-h.; Grable, J.E. An exploratory framework of the determinants of financial satisfaction. J. Fam. Econ. Iss. 2004, 25, 25–50. [Google Scholar] [CrossRef]

- Plagnol, A.C. Financial satisfaction over the life course: The influence of assets and liabilities. J. Econ. Psychol. 2011, 32, 45–64. [Google Scholar] [CrossRef] [Green Version]

- De Meza, D.; Irlenbusch, B.; Reyniers, D. Financial capability: A behavioural economics perspective. Consum. Res. 2008, 69, 192–193. [Google Scholar]

- Xiao, J.J.; Chen, C.; Chen, F. Consumer financial capability and financial satisfaction. Soc. Indic. Res. 2014, 118, 415–432. [Google Scholar] [CrossRef]

- Lusardi, A. Financial literacy and the need for financial education: Evidence and implications. Swiss J. Econ. Stat. 2019, 155, 1. [Google Scholar] [CrossRef] [Green Version]

- Remund, D.L. Financial literacy explicated: The case for a clearer definition in an increasingly complex economy. J. Consum. Aff. 2010, 44, 276–295. [Google Scholar] [CrossRef]

- Chen, F.; Lu, J.; Li, J.; Wang, W.; Bissielou, H. Sustainable Financial Education and Consumer Life Satisfaction. Sustainability 2020, 12, 1150. [Google Scholar] [CrossRef] [Green Version]

- Sarkar, S.; Chauhan, S.; Khare, A. A meta-analysis of antecedents and consequences of trust in mobile commerce. Int. J. Inform. Manag. 2020, 50, 286–301. [Google Scholar] [CrossRef]

- Hu, Z.; Ding, S.; Li, S.; Chen, L.; Yang, S. Adoption intention of fintech services for bank users: An empirical examination with an extended technology acceptance model. Symmetry 2019, 11, 340. [Google Scholar] [CrossRef]

- Tahir, M.S.; Shahid, A.U.; Richards, D.W. The role of impulsivity and financial satisfaction in a moderated mediation model of consumer financial resilience and life satisfaction. Int. J. Bank Mark. 2022, 40, 773–790. [Google Scholar] [CrossRef]

- Ye, Y.; Chen, S.; Li, C. Financial technology as a driver of poverty alleviation in China: Evidence from an innovative regression approach. J. Innov. Knowl. 2022, 7, 100164. [Google Scholar] [CrossRef]

- Arner, D.W.; Buckley, R.P.; Zetzsche, D.A.; Veidt, R. Sustainability, FinTech and financial inclusion. Eur. Bus. Organ. Law Re. 2020, 21, 7–35. [Google Scholar] [CrossRef]

- Gnan, E.; Silgoner, M.A.; Weber, B. Economic and financial education: Concepts, goals and measurement. Monet. Policy Econ. 2007, 3, 28–49. [Google Scholar]

- Diener, E.; Biswas-Diener, R. Will money increase subjective wellbeing? Soc. Indic. Res. 2002, 57, 119–169. [Google Scholar] [CrossRef]

- Veblen, T. The limitations of marginal utility. J. Polit. Econ. 1909, 17, 620–636. [Google Scholar] [CrossRef] [Green Version]

- Vera-Toscano, E.; Ateca-Amestoy, V.; Serrano-Del-Rosal, R. Building financial satisfaction. Soc. Indic. Res. 2006, 77, 211–243. [Google Scholar] [CrossRef] [Green Version]

- Lim, S.H.; Kim, D.J.; Hur, Y.; Park, K. An empirical study of the impacts of perceived security and knowledge on continuous intention to use mobile fintech payment services. Int. J. Hum. Comput. Int. 2019, 35, 886–898. [Google Scholar] [CrossRef]

- Xiao, J.J.; Porto, N. Financial education and financial satisfaction: Financial literacy, behavior, and capability as mediators. Int. J. Bank Mark. 2017, 35, 805–817. [Google Scholar] [CrossRef]

- Kim, K.T.; Lee, J.M.; Lee, J. Student loans and financial satisfaction: The moderating role of financial education. J. Financ. Couns. Plan. 2021, 32, 266–279. [Google Scholar] [CrossRef]

- Allen, F.; Gu, X.; Jagtiani, J. A survey of fintech research and policy discussion. Rev. Corp. Financ. 2021, 1, 259–339. [Google Scholar] [CrossRef]

- Farag, H.; Johan, S. How alternative finance informs central themes in corporate finance. J. Corp. Financ. 2021, 67, 101879. [Google Scholar] [CrossRef]

- Mainardes, E.W.; Costa, P.M.F.; Nossa, S.N. Customers’ satisfaction with fintech services: Evidence from Brazil. J. Financ. Serv. Mark. 2022, 1–18. [Google Scholar] [CrossRef]

- Gerrans, P.; Heaney, R. The impact of undergraduate personal finance education on individual financial literacy, attitudes and intentions. Account. Financ. 2019, 59, 177–217. [Google Scholar] [CrossRef]

- Fox, J.; Bartholomae, S.; Lee, J. Building the case for financial education. J. Consum. Aff. 2005, 39, 195–214. [Google Scholar] [CrossRef]

- Bernheim, B.D.; Garrett, D.M. The effects of financial education in the workplace: Evidence from a survey of households. J. Public Econ. 2003, 87, 1487–1519. [Google Scholar] [CrossRef]

- Chen, F.; Lu, X.; Wang, W. Informal financial education and consumer financial capability: The mediating role of financial knowledge. Front. Psychol. 2022, 13, 1042085. [Google Scholar] [CrossRef]

- Atkinson, A.; McKay, S.; Collard, S.; Kempson, E. Levels of financial capability in the UK. Public Money Manag. 2007, 27, 29–36. [Google Scholar] [CrossRef]

- Baron, R.M.; Kenny, D.A. The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. J. Pers. Soc. Psychol. 1986, 51, 1173. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

| Type | Variables | Attribute |

|---|---|---|

| Dependent variable | Consumer financial satisfaction | “How satisfied are you with your current personal financial condition?” From 1 (Not at all satisfied) to 10 (Extremely satisfied) |

| Independent variable | Mobile payments | “How often do you pay with your cell phone code at retail stores?” 1—Never, 2—Sometimes, and 3—Frequently |

| Mediating variables | Financial education | “Have you received financial education in high school/college/from workplace/military?” 1—Yes, and 0—No |

| Financial capability | A sum of Z-scores of objective and subjective financial capabilities | |

| Control variables | Risk attitude | “When it comes to financial investments, what is your desire to take risks?” Increasing preference for risk from 1 to 10. |

| Participating in financial markets | “Are there any stocks, bonds, or mutual funds in your account that you own shares of?” 1—Yes, and 0—No | |

| Credit record rating | “What do you consider your credit situation to be?” From 1 (Very bad) to 5 (extremely good) | |

| Annual income | 1 = 0 to 15,000 dollars, 2 = 15,000 to 25,000 dollars, 3 = 25,000 to 35,000 dollars, 4 = 35,000 to 50,000 dollars, 5 = 50,000 to 75,000 dollars, 6 = 75,000 to 100,000 dollars, 7 = 10,000 to 150,000 dollars, 8 = greater than 150,000 dollars | |

| Subjective math capability | “Evaluate this statement: I have a good grasp of mathematics.” From 1 (Strongly disagree) to 7 (Strongly agree) | |

| Male | 1 = Male, and 0 = Female | |

| Age 18 to 24 | 1 if the respondent’s age was between 18 and 24 years, and 0 otherwise. | |

| Age 25 to 34 | 1 if the respondent’s age was between 25 and 34 years, and 0 otherwise. | |

| Age 35 to 44 | 1 if the respondent’s age was between 35 and 44 years, and 0 otherwise. | |

| Age 45 to 54 | 1 if the respondent’s age was between 45 and 54 years, and 0 otherwise. | |

| Age 55 to 64 | 1 if the respondent’s age was between 55 and 64 years, and 0 otherwise. | |

| Age 65 or older | 1 if the respondent’s age was 65 years or older, and 0 otherwise. | |

| Some college to bachelor’s degree | 1—Yes, and 0—No | |

| Postgraduate degree or higher | 1—Yes, and 0—No | |

| Marital status | 1 = Being married, and 0 otherwise | |

| Number of financially dependent children | “What is the number of children who are economically dependent?” 0 to 4 or more. | |

| Ethnicity | 1 = White, and 0 = Non-white |

| Variable | Obs. | Mean | Std. Dev. | Min. | Max. |

|---|---|---|---|---|---|

| Financial satisfaction | 53,038 | 5.75 | 2.81 | 1 | 10 |

| Mobile payments | 53,038 | 1.35 | 0.62 | 1 | 3 |

| Financial education | 53,038 | 0.21 | 0.41 | 0 | 1 |

| Financial capability | 53,038 | 0.00 | 1.62 | −5.56 | 2.87 |

| Risk attitude | 53,038 | 4.95 | 2.73 | 0 | 10 |

| Participating in the financial markets | 53,038 | 0.33 | 0.47 | 0 | 1 |

| Credit record rating | 53,038 | 3.01 | 1.28 | 0 | 5 |

| Annual income | 53,038 | 4.47 | 2.05 | 1 | 8 |

| Subjective math capability | 53,038 | 5.63 | 1.62 | 0 | 7 |

| Male | 53,038 | 0.44 | 0.5 | 0 | 1 |

| Age 18 to 24 | 53,038 | 0.11 | 0.31 | 0 | 1 |

| Age 25 to 34 | 53,038 | 0.18 | 0.38 | 0 | 1 |

| Age 35 to 44 | 53,038 | 0.17 | 0.37 | 0 | 1 |

| Age 45 to 54 | 53,038 | 0.18 | 0.38 | 0 | 1 |

| Age 55 to 64 | 53,038 | 0.18 | 0.38 | 0 | 1 |

| Age 65 or older | 53,038 | 0.2 | 0.4 | 0 | 1 |

| High school or lower | 53,038 | 0.26 | 0.44 | 0 | 1 |

| Some college to Bachelor’s degree | 53,038 | 0.61 | 0.49 | 0 | 1 |

| Postgraduate degree or higher | 53,038 | 0.14 | 0.34 | 0 | 1 |

| Being married | 53,038 | 0.54 | 0.5 | 0 | 1 |

| White | 53,038 | 0.73 | 0.44 | 0 | 1 |

| Number of financially dependent children | 53,038 | 0.67 | 1.06 | 0 | 4 |

| Financial Satisfaction | Mobile Payment | Financial Education | Financial Capability | Risk Attitude | Participating in the Financial Markets | Credit Record Rating | Annual Income | |

|---|---|---|---|---|---|---|---|---|

| Mobile payments | 0.11 *** | |||||||

| Financial education | 0.07 *** | 0.08 *** | ||||||

| Financial capability | 0.53 *** | 0.01 * | 0.11 *** | |||||

| Risk attitude | 0.36 *** | 0.25 *** | 0.12 *** | 0.26 *** | ||||

| Participating in the financial markets | 0.37 *** | 0.07 *** | 0.11 *** | 0.38 *** | 0.31 *** | |||

| Credit record rating | 0.42 *** | −0.08 *** | 0.04 *** | 0.41 *** | 0.12 *** | 0.27 *** | ||

| Annual income | 0.38 *** | 0.06 *** | 0.07 *** | 0.43 *** | 0.28 *** | 0.37 *** | 0.29 *** | |

| Subjective math capability | 0.20 *** | −0.02 *** | 0.10 *** | 0.44 *** | 0.14 *** | 0.15 *** | 0.16 *** | 0.19 *** |

| Variables | (1) | (2) | (3) |

|---|---|---|---|

| Mobile payments | 0.21 *** | ||

| (0.01) | |||

| Risk attitude | 0.27 *** | 0.13 *** | 0.12 *** |

| (0.01) | 0.00 | 0.00 | |

| Participating in the financial markets | 0.73 *** | 0.34 *** | 0.32 *** |

| (0.02) | (0.01) | (0.01) | |

| Credit record rating | 0.57 *** | 0.25 *** | 0.26 *** |

| (0.01) | (0.01) | (0.01) | |

| Annual income | 0.25 *** | 0.11 *** | 0.10 *** |

| (0.01) | 0.00 | 0.00 | |

| Subjective math capability | 0.09 *** | 0.04 *** | 0.05 *** |

| (0.01) | 0.00 | 0.00 | |

| Male | 0.11 *** | 0.05 *** | 0.04 *** |

| (0.03) | (0.01) | (0.01) | |

| Age 25 to 34 | 0.07 | 0.04 * | 0.05 ** |

| (0.04) | (0.02) | (0.02) | |

| Age 35 to 44 | −0.26 *** | −0.13 *** | −0.10 *** |

| (0.04) | (0.02) | (0.02) | |

| Age 45 to 54 | −0.36 *** | −0.18 *** | −0.12 *** |

| (0.04) | (0.02) | (0.02) | |

| Age 55 to 64 | 0.16 *** | 0.07 *** | 0.14 *** |

| (0.05) | (0.02) | (0.02) | |

| Age 65 or older | 0.90 *** | 0.42 *** | 0.50 *** |

| (0.05) | (0.03) | (0.02) | |

| Some college to Bachelor’s degree | −0.29 *** | −0.15 *** | −0.15 *** |

| (0.02) | (0.01) | (0.01) | |

| Postgraduate degree or higher | −0.35 *** | −0.18 *** | −0.17 *** |

| (0.04) | (0.02) | (0.02) | |

| Being married | 0.21 *** | 0.09 *** | 0.09 *** |

| (0.03) | (0.01) | (0.01) | |

| White | −0.12 *** | −0.06 *** | −0.03 ** |

| (0.03) | (0.01) | (0.01) | |

| Number of financially dependent children | −0.04 *** | −0.01 * | −0.02 *** |

| (0.01) | (0.01) | (0.01) | |

| Constant | 0.87 *** | ||

| (0.06) | |||

| State fixed effect | Yes | Yes | Yes |

| Observations | 53,038 | 53,038 | 53,038 |

| Adjusted R2 | 0.36 | ||

| Pseudo R2 | 0.10 | 0.10 |

| Variables | (1) | (2) | (3) | (4) | (5) | (6) |

|---|---|---|---|---|---|---|

| Mobile payments | 0.36 *** | 0.22 *** | 0.17 *** | 0.21 *** | 0.24 *** | 0.21 *** |

| (0.02) | (0.01) | (0.03) | (0.02) | (0.02) | (0.02) | |

| Risk attitude | 0.21 *** | 0.12 *** | 0.14 *** | 0.12 *** | 0.12 *** | 0.10 *** |

| (0.01) | 0.00 | (0.01) | (0.01) | 0.00 | (0.01) | |

| Participating in the financial markets | 0.54 *** | 0.32 *** | 0.31 *** | 0.34 *** | 0.30 *** | 0.33 *** |

| (0.02) | (0.01) | (0.02) | (0.02) | (0.02) | (0.02) | |

| Credit record rating | 0.46 *** | 0.29 *** | 0.26 *** | 0.26 *** | 0.24 *** | 0.27 *** |

| (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | (0.01) | |

| Annual income | 0.18 *** | 0.10 *** | 0.10 *** | 0.10 *** | 0.11 *** | 0.11 *** |

| (0.01) | 0.00 | (0.01) | (0.01) | (0.01) | (0.01) | |

| Subjective math capability | 0.08 *** | 0.05 *** | 0.04 *** | 0.05 *** | 0.04 *** | 0.05 *** |

| (0.01) | 0.00 | (0.01) | (0.01) | (0.01) | (0.01) | |

| Male | 0.06 *** | 0.05 *** | (0.01) | 0.01 | 0.08 *** | 0.06 *** |

| (0.02) | (0.01) | (0.03) | (0.03) | (0.02) | (0.02) | |

| Age 25 to 34 | 0.08 *** | 0.02 | 0.05 ** | 0.02 | 0.10 ** | 0.00 |

| (0.03) | (0.02) | (0.02) | (0.03) | (0.04) | (0.04) | |

| Age 35 to 44 | −0.17 *** | −0.12 *** | −0.12 ** | −0.10 *** | −0.07 ** | −0.11 *** |

| (0.03) | (0.02) | (0.05) | (0.04) | (0.03) | (0.03) | |

| Age 45 to 54 | −0.22 *** | −0.16 *** | −0.10 ** | −0.12 *** | −0.08 ** | −0.19 *** |

| (0.03) | (0.02) | (0.05) | (0.03) | (0.04) | (0.03) | |

| Age 55 to 64 | 0.25 *** | 0.12 *** | 0.10 ** | 0.13 *** | 0.16 *** | 0.14 *** |

| (0.04) | (0.02) | (0.05) | (0.04) | (0.04) | (0.04) | |

| Age 65 or older | 0.88 *** | 0.48 *** | 0.54 *** | 0.47 *** | 0.56 *** | 0.44 *** |

| (0.04) | (0.03) | (0.05) | (0.04) | (0.05) | (0.04) | |

| Some college to bachelor’s degree | −0.24 *** | −0.15 *** | −0.14 *** | −0.15 *** | −0.15 *** | −0.14 *** |

| (0.02) | (0.01) | (0.03) | (0.02) | (0.02) | (0.02) | |

| Postgraduate degree or higher | −0.29 *** | −0.16 *** | −0.19 *** | −0.11 *** | −0.24 *** | −0.11 *** |

| (0.03) | (0.02) | (0.06) | (0.03) | (0.02) | (0.02) | |

| Being married | 0.16 *** | 0.08 *** | 0.12 *** | 0.10 *** | 0.07 *** | 0.11 *** |

| (0.02) | (0.01) | (0.02) | (0.03) | (0.02) | (0.02) | |

| White | −0.05 ** | −0.05 *** | (0.08) | (0.02) | −0.05 *** | 0.01 |

| (0.02) | (0.02) | (0.05) | (0.03) | (0.02) | (0.02) | |

| Number of financially dependent children | −0.04 *** | −0.01 ** | (0.02) | −0.05 *** | 0.00 | −0.02 ** |

| (0.01) | (0.01) | (0.02) | (0.01) | (0.01) | (0.01) | |

| State fixed effect | Yes | Yes | Yes | Yes | Yes | Yes |

| Observations | 53,038 | 43,803 | 9227 | 12,177 | 17,025 | 14,609 |

| Pseudo R2 | 0.10 | 0.09 | 0.10 | 0.10 | 0.10 | 0.10 |

| Variables | (1) | (2) | (3) | (4) |

|---|---|---|---|---|

| Financial Education | Financial Satisfaction | Financial Capability | Financial Satisfaction | |

| Financial education | 0.03 *** | |||

| (0.01) | ||||

| Financial capability | 0.27 *** | |||

| 0.00 | ||||

| Mobile payments | 0.07 *** | 0.21 *** | 0.04 *** | 0.21 *** |

| (0.01) | (0.01) | (0.01) | (0.01) | |

| Risk attitude | 0.02 *** | 0.12 *** | 0.05 *** | 0.11 *** |

| 0.00 | 0.00 | 0.00 | 0.00 | |

| Participating in the financial markets | 0.21 *** | 0.32 *** | 0.50 *** | 0.20 *** |

| (0.02) | (0.01) | (0.02) | (0.01) | |

| Credit record rating | 0.00 | 0.26 *** | 0.32 *** | 0.19 *** |

| (0.01) | (0.01) | (0.01) | (0.01) | |

| Annual income | 0.01 *** | 0.10 *** | 0.15 *** | 0.07 *** |

| 0.00 | 0.00 | 0.00 | 0.00 | |

| Subjective math capability | 0.08 *** | 0.05 *** | 0.32 *** | −0.04 *** |

| 0.00 | 0.00 | 0.00 | 0.00 | |

| Male | 0.09 *** | 0.04 *** | −0.10 *** | 0.07 *** |

| (0.01) | (0.01) | (0.01) | (0.01) | |

| Age 25 to 34 | −0.36 *** | 0.05 ** | 0.32 *** | −0.04* |

| (0.03) | (0.02) | (0.03) | (0.02) | |

| Age 35 to 44 | −0.48 *** | −0.09 *** | 0.37 *** | −0.20 *** |

| (0.03) | (0.02) | (0.03) | (0.02) | |

| Age 45 to 54 | −0.44 *** | −0.12 *** | 0.44 *** | −0.25 *** |

| (0.04) | (0.02) | (0.03) | (0.02) | |

| Age 55 to 64 | −0.51 *** | 0.15 *** | 0.57 *** | 0.00 |

| (0.04) | (0.02) | (0.03) | (0.02) | |

| Age 65 or older | −0.55 *** | 0.51 *** | 0.52 *** | 0.39 *** |

| (0.04) | (0.03) | (0.03) | (0.02) | |

| Some college to Bachelor’s degree | 0.45 *** | −0.15*** | 0.10 *** | −0.18 *** |

| (0.02) | (0.01) | (0.01) | (0.01) | |

| Postgraduate degree or higher | 0.48 *** | −0.17 *** | 0.11 *** | −0.21 *** |

| (0.03) | (0.02) | (0.02) | (0.02) | |

| Being married | −0.03 * | 0.09 *** | 0.03 ** | 0.09 *** |

| (0.02) | (0.01) | (0.01) | (0.01) | |

| White | −0.11 *** | −0.03 ** | 0.02 | −0.04 *** |

| (0.02) | (0.01) | (0.01) | (0.01) | |

| Number of financially dependent children | 0.03 *** | −0.02 *** | 0.03 *** | −0.03 *** |

| (0.01) | (0.01) | (0.01) | (0.01) | |

| Constant | −1.40 *** | −4.42 *** | ||

| (0.05) | (0.04) | |||

| State fixed effect | Yes | Yes | Yes | Yes |

| Observations | 53,038 | 53,038 | 53,038 | 53,038 |

| Adjusted R2 | 0.43 | |||

| Pseudo R2 | 0.06 | 0.10 | 0.12 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chen, F.; Du, X.; Wang, W. Can FinTech Applied to Payments Improve Consumer Financial Satisfaction? Evidence from the USA. Mathematics 2023, 11, 363. https://doi.org/10.3390/math11020363

Chen F, Du X, Wang W. Can FinTech Applied to Payments Improve Consumer Financial Satisfaction? Evidence from the USA. Mathematics. 2023; 11(2):363. https://doi.org/10.3390/math11020363

Chicago/Turabian StyleChen, Fuzhong, Xin Du, and Wenting Wang. 2023. "Can FinTech Applied to Payments Improve Consumer Financial Satisfaction? Evidence from the USA" Mathematics 11, no. 2: 363. https://doi.org/10.3390/math11020363