Regression Analysis of Macroeconomic Conditions and Capital Structures of Publicly Listed British Firms

Abstract

:1. Introduction

- Is the effect of and (industrial production) on (capital structure) pro-cyclical or counter-cyclical?

- Do , , and (credit supply, credit market risk and stock market performance) have significant effects on ?

- Is the impact of macroeconomic variables on consistent with the prediction of POT, TOT and MTT?

2. Hypotheses

3. Data Descriptions

3.1. Data Collection

3.2. Variables

Dependant Variable: Leverage Ratio ()

4. Methodology

4.1. Static Panel Data Regression Model

4.1.1. Fixed Effect Model

4.1.2. Random Effect Model

4.1.3. Tobit Model

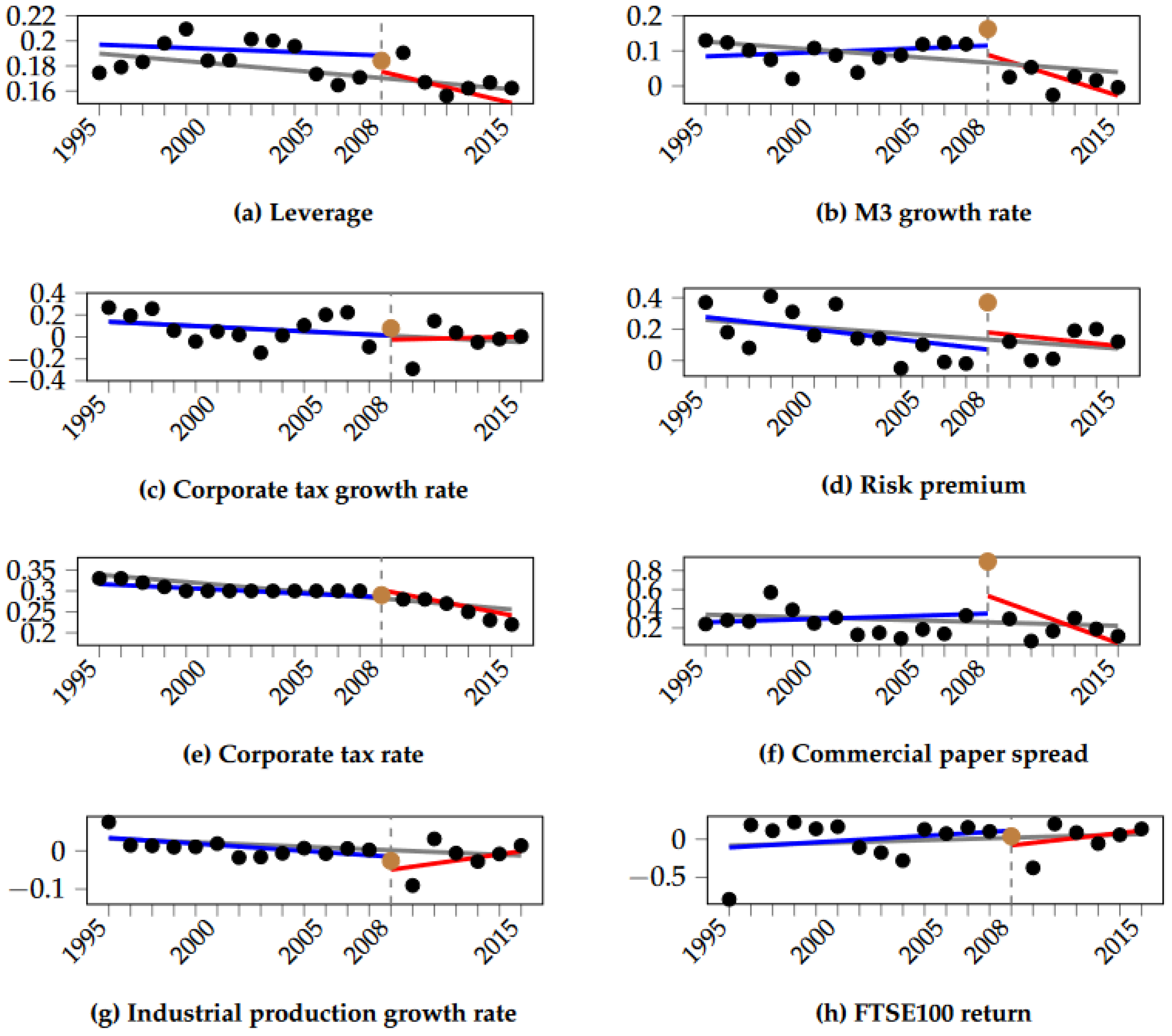

5. Results and Discussion

5.1. Descriptive Statistics

5.2. Empirical Results from Static Model

5.2.1. The Empirical Results from FEM

- and are statistically significant and negative, thus showing a deleterious effect on non-financial firms in the UK (this supports H1 and is consistent with the prediction of POT);

- has a significantly positive effect on on the non-financial firm in the UK (this agrees with H2 and with the prediction of the POT and TOT);

- The negative coefficients for and imply that financial market risk has a negative effect on for the period after the crisis;

- has a highly positive effect on , which indicates that a high stock market performance leads firms to issue more debt (in line with H4 and with the prediction of TOT).

5.2.2. The Empirical Results from REM

- There is a negative effect of the business cycle on , which is in line with POT (H1);

- There is a positive effect of credit supply on , which is in line with both POT and TOT (H2);

- There is a negative effect of financial market risk on , which is in line with TOT (H3);

- There is a positive effect of stock market performance on , which is in line with TOT (H4);

- Our results are highly robust, as they are not sensitive using REM models.

5.2.3. The Empirical Results from Tobit Model

- Capital structure is negatively associated with the business cycle, and this is in line with POT’s prediction (H1);

- Capital structure is positively associated with credit supply, and this is in line with the prediction of both TOT and POT theories (H2);

- For the period after the crisis, capital structure is negatively associated with financial market risks, and this is in line with TOT’s predictions (H3);

- The positive impact of stock market performance on capital structure is in line with TOT’s prediction (H4);

- The results are in line with those obtained with FEM and REM, and hence they are robust.

5.3. Robustness Check Results

6. Discussion and Conclusions

- As the data were not available for the financial market risk variable over the period 1980–2014, this study was limited to a shorter period of time, although we aim to collect missing data in order to be able to strengthen our analysis in future work;

- More proxies can also be used to measure macroeconomic variables, such as aggregated commercial paper and bank-loan supply, which can be used for the business cycle—as carried out in [53];

- The use of other dynamic models, such as the nested logit model, might also help us strengthen our future analyses;

- Lastly, instead of limiting our attention to the ‘great recession’ that occurred in 2008, we plan on including the so-called 2011 ‘Euro area sovereign debt crisis’ in future investigations.

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Modigliani, F.; Miller, M. The cost of capital, corporation finance and the theory of investment. Am. Econ. Rev. 1958, 48, 261–297. [Google Scholar]

- Rajan, R.; Zingales, L. What Do We Know about Capital Structure? Some Evidence from International Data. J. Financ. 1995, 50, 1421–1460. [Google Scholar] [CrossRef]

- Myers, S. Determinants of corporate borrowing 1. J. Financ. Econ. 1977, 5, 147–175. [Google Scholar] [CrossRef] [Green Version]

- Myers, S.C.; Majluf, N.S. Corporate financing and investment decisions when firms have information that investors do not have. J. Financ. Econ. 1984, 13, 187–221. [Google Scholar] [CrossRef] [Green Version]

- Myers, S. The Capital Structure Puzzle. J. Financ. 1984, 39, 574–592. [Google Scholar] [CrossRef]

- Baker, M.; Wurgler, J. Market Timing and Capital Structure. J. Financ. 2002, 57, 1–32. [Google Scholar] [CrossRef]

- Loughran, T.; Ritter, J.R. The new issues puzzle. J. Financ. 1995, 50, 23–51. [Google Scholar] [CrossRef]

- Hertzel, M.; Lemmon, M.; Linck, J.S.; Rees, L. Long-run performance following private placements of equity. J. Financ. 2002, 57, 2595–2617. [Google Scholar] [CrossRef]

- Korajczyk, R.A.; Levy, A. Capital structure choice: Macroeconomic conditions and financial constraints. J. Financ. Econ. 2003, 68, 75–109. [Google Scholar] [CrossRef]

- Hackbarth, D.; Miao, J.; Morellec, E. Capital structure, credit risk, and macroeconomic conditions. J. Financ. Econ. 2006, 82, 519–550. [Google Scholar] [CrossRef] [Green Version]

- Cook, D.O.; Tang, T. Macroeconomic conditions and capital structure adjustment speed. J. Corp. Financ. 2010, 16, 73–87. [Google Scholar] [CrossRef]

- Lynch, M. Bond Index Rules & Definitions; Global Securities Research & Economics Group, Fixed Income Analytics: New York, NY, USA, 2000. [Google Scholar]

- Gujarati, D.N. Econometrics by Example; Palgrave Macmillan: New York, NY, USA, 2011. [Google Scholar]

- Tobin, J. Estimation of relationships for limited dependent variables. Econom. J. Econom. Soc. 1958, 26, 24–36. [Google Scholar] [CrossRef] [Green Version]

- Jensen, M.C. Agency costs of free cash flow, corporate finance, and takeovers. Am. Econ. Rev. 1986, 76, 323–329. [Google Scholar]

- Graham, J.R.; Harvey, C.R. The theory and practice of corporate finance: Evidence from the field. J. Financ. Econ. 2001, 60, 187–243. [Google Scholar] [CrossRef]

- Levy, A.; Hennessy, C. Why does capital structure choice vary with macroeconomic conditions? J. Monet. Econ. 2007, 54, 1545–1564. [Google Scholar] [CrossRef] [Green Version]

- Voutsinas, K.; Werner, R.A. Credit supply and corporate capital structure: Evidence from Japan. Int. Rev. Financ. Anal. 2011, 20, 320–334. [Google Scholar] [CrossRef]

- Morellec, E.; Nikolov, B.; Schürhoff, N. Corporate governance and capital structure dynamics. J. Financ. 2012, 67, 803–848. [Google Scholar] [CrossRef]

- Chen, H. Macroeconomic conditions and the puzzles of credit spreads and capital structure. J. Financ. 2010, 65, 2171–2212. [Google Scholar] [CrossRef]

- Welch, I. Capital structure and stock returns. J. Political Econ. 2004, 112, 106–131. [Google Scholar] [CrossRef] [Green Version]

- Barclay, M.J.; Smith, C.W., Jr.; Morellec, E. On the debt capacity of growth options. J. Bus. 2006, 79, 37–60. [Google Scholar] [CrossRef] [Green Version]

- Hovakimian, A.; Opler, T.; Titman, S. The debt-equity choice. J. Financ. Quant. Anal. 2001, 36, 1–24. [Google Scholar] [CrossRef]

- Marsh, P. The Choice between Equity and Debt: An Empirical Study. J. Financ. 1982, 37, 121–144. [Google Scholar] [CrossRef]

- Bennett, M.; Donnelly, R. The determinants of capital structure: Some UK evidence. Br. Account. Rev. 1993, 25, 43–59. [Google Scholar] [CrossRef]

- Ozkan, A. An empirical analysis of corporate debt maturity structure. Eur. Financ. Manag. 2000, 6, 197–212. [Google Scholar] [CrossRef]

- Ozkan, A. Determinants of capital structure and adjustment to long run target: Evidence from UK company panel data. J. Bus. Financ. Account. 2001, 28, 175–198. [Google Scholar] [CrossRef]

- Benito, A. The Capital Structure Decisions of Firms: Is There a Pecking Order? Working Papers 0310, Working Papers Homepage; Banco de España: Madrid, Spain, 2003. [Google Scholar]

- Panno, A. An empirical investigation on the determinants of capital structure: The UK and Italian experience. Appl. Financ. Econ. 2003, 13, 97–112. [Google Scholar] [CrossRef]

- Bevan, A.; Danbolt, J. Testing for inconsistencies in the estimation of UK capital structure determinants. Appl. Financ. Econ. 2004, 14, 55–66. [Google Scholar] [CrossRef] [Green Version]

- Hugonnier, J.; Morellec, E. Bank capital, liquid reserves, and insolvency risk. J. Financ. Econ. 2017, 125, 266–285. [Google Scholar] [CrossRef]

- Ross, S.A. The determination of financial structure: The incentive-signalling approach. Bell J. Econ. 1977, 8, 23–40. [Google Scholar] [CrossRef]

- Tzeremes, P. Productivity, efficiency and firm’s market value: Microeconomic evidence from multinational corporations. Bull. Appl. Econ. 2020, 7, 95. [Google Scholar]

- Cannaday, R.E.; Yang, T.T. Optimal leverage strategy: Capital structure in real estate investments. J. Real Estate Financ. Econ. 1996, 13, 263–271. [Google Scholar] [CrossRef]

- Lord, R.A. The impact of operating and financial risk on equity risk. J. Econ. Financ. 1996, 20, 27. [Google Scholar] [CrossRef]

- Baum, C. XTTEST3: Stata Module to Compute Modified Wald Statistic for Groupwise Heteroskedasticity. 2001. Available online: https://EconPapers.repec.org/RePEc:boc:bocode:s414801 (accessed on 11 March 2017).

- Hausman, J.A.; Taylor, W.E. Panel Data and Unobservable Individual Effects. Econometrica 1981, 49, 1377–1398. [Google Scholar] [CrossRef] [Green Version]

- Gujarati, D.; Porter, D. Basic Econometrics; Economics Series; McGraw-Hill Irwin: New York, NY, USA, 2009. [Google Scholar]

- Frank, M.Z.; Goyal, V.K. Chapter 12—Trade-Off and Pecking Order Theories of Debt. In Handbook of Empirical Corporate Finance; Eckbo, B.E., Ed.; Handbooks in Finance; Elsevier: San Diego, CA, USA, 2008; pp. 135–202. [Google Scholar] [CrossRef]

- Gujarati, D. Basic Econometrics; Economic Series; McGraw Hill: New York, NY, USA, 2003. [Google Scholar]

- Goldberger, A.S. Econometric Theory; John Willey & Sons: New York, NY, USA, 1964. [Google Scholar]

- Tobin, J. Liquidity Preference as Behavior Towards Risk. Rev. Econ. Stud. 1958, 25, 65–86. [Google Scholar] [CrossRef]

- Kayhan, A.; Titman, S. Firms’ Histories and Their Capital Structures; Working Paper 10526; National Bureau of Economic Research: Cambridge, MA, USA, 2004. [Google Scholar]

- Harford, J.; Klasa, S.; Walcott, N. Do firms have leverage targets? Evidence from acquisitions. J. Financ. Econ. 2009, 93, 1–14. [Google Scholar] [CrossRef]

- Cong, R. Marginal effects of the tobit model. Stata Tech. Bull. 2001, 10, 56. [Google Scholar]

- Bevan, A.A.; Danbolt, J. Capital structure and its determinants in the UK—A decompositional analysis. Appl. Financ. Econ. 2002, 12, 159–170. [Google Scholar] [CrossRef] [Green Version]

- Homapour, E.; Su, L.; Caraffini, F.; Chiclana, F. Extended results for ‘Statistical Analysis of Macroeconomic Conditions and Capital Structures of Publicly Listed British Firms’. 2021. Available online: https://doi.org/10.21253/DMU.13139438 (accessed on 26 March 2022).

- Huang, Z. Evidence of a bank lending channel in the UK. J. Bank. Financ. 2003, 27, 491–510. [Google Scholar] [CrossRef]

- Balsari, C.K.; Kirkulak, B. Effect of financial crises on the capital structure choice: Evidence from Istanbul Stock Exchange (ISE). In Proceedings of the 5th Conference of the Portuguese Finance Network, Coimbra, Portugal, 10–12 July 2008; p. 16. [Google Scholar]

- Morellec, E. Credit Supply and Corporate Policies. 2010. Available online: https://ssrn.com/abstract=1599409 (accessed on 11 March 2017).

- Bhamra, H.S.; Kuehn, L.A.; Strebulaev, I.A. The aggregate dynamics of capital structure and macroeconomic risk. Rev. Financ. Stud. 2010, 23, 4187–4241. [Google Scholar] [CrossRef]

- Bhamra, H.S.; Kuehn, L.A.; Strebulaev, I.A. The levered equity risk premium and credit spreads: A unified framework. Rev. Financ. Stud. 2009, 23, 645–703. [Google Scholar] [CrossRef]

- Kashyap, A.K.; Stein, J.C.; Wilcox, D.W. Monetary Policy and Credit Conditions: Evidence from the Composition of External Finance; Technical Report; National Bureau of Economic Research: Cambridge, MA, USA, 1992. [Google Scholar]

{kind=link}

{kind=link}

| UK | US | |

|---|---|---|

| Power of the banking sector | Market-oriented | Market-oriented |

| Bankruptcy laws | Receivership | Reorganisation and liquidation (chapters 11 and 7) |

| Bond Markets Average Duration (years) | 8.5 | 4.5 |

| Index Weight | 0.049 | 0.437 |

| Macroeconomic Variable | TOT | POT | MTT |

|---|---|---|---|

| Business cycle | H1 (+) | H1 (−) | (∼) |

| Credit supply | H2 (+) | H2 (+) | (∼) |

| Financial market risk | H3 (−) | H3 (+) | (∼) |

| Stock market performance | H4 (+) | H4 (−) | H4 (−) |

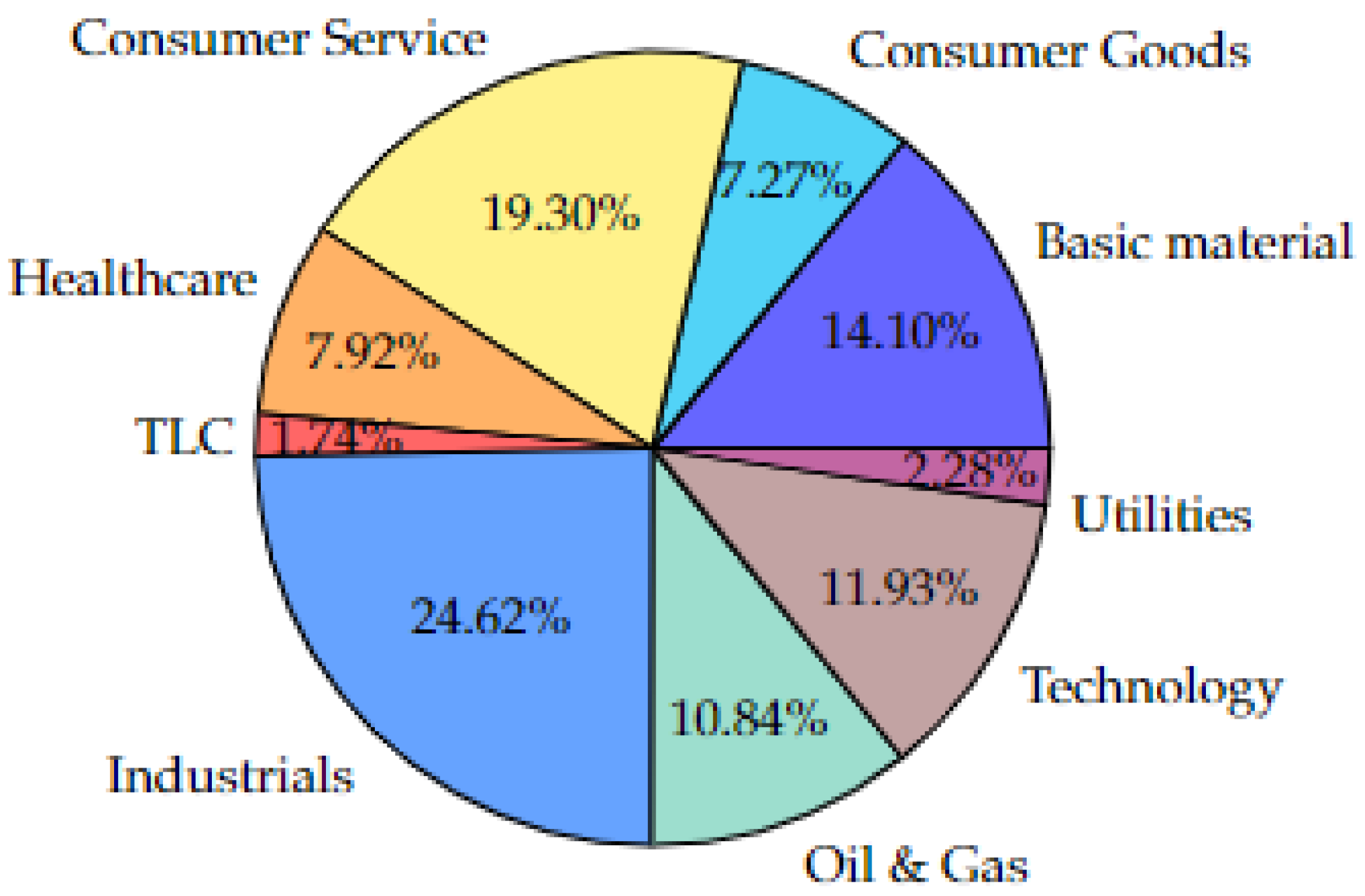

| Industry Name | Oil and Gas | Basic Materials | Industrials | Consumer Goods | Healthcare | Consumer Services | TLC | Utilities | Technology |

|---|---|---|---|---|---|---|---|---|---|

| 0.193 | 0.183 | 0.164 | 0.182 | 0.169 | 0.194 | 0.111 | 0.174 | 0.174 | |

| 0.006 | 0.011 | 0.008 | 0.007 | 0.005 | 0.011 | 0.003 | 0.008 | 0.015 | |

| Liquidity | 3.241 | 3.305 | 3.458 | 5.888 | 2.787 | 3.010 | 3.962 | 2.623 | 3.980 |

| 0.145 | 0.085 | 0.133 | 0.141 | 0.125 | 0.133 | 0.146 | 0.131 | 0.101 | |

| −0.257 | −0.320 | −0.026 | −0.097 | −0.088 | −0.108 | −0.002 | −0.123 | −0.210 | |

| 11.108 | 11.011 | 11.457 | 11.600 | 10.823 | 11.185 | 10.012 | 11.021 | 11.342 |

| Year | Oil and Gas | Basic Materials | Industrials | Consumer Goods | Healthcare | Consumer Services | TLC | Utilities | Technology |

|---|---|---|---|---|---|---|---|---|---|

| 1995 | 0.1869 | 0.1573 | 0.1591 | 0.1478 | 0.1548 | 0.2032 | 0.1951 | 0.2853 | 0.1893 |

| 1996 | 0.1979 | 0.1719 | 0.1598 | 0.1559 | 0.1560 | 0.1935 | 0.1050 | 0.3291 | 0.2054 |

| 1997 | 0.2101 | 0.1731 | 0.1497 | 0.1541 | 0.1911 | 0.2118 | 0.1101 | 0.2834 | 0.2048 |

| 1998 | 0.2288 | 0.1789 | 0.1637 | 0.1671 | 0.2153 | 0.2248 | 0.1736 | 0.2826 | 0.2236 |

| 1999 | 0.2208 | 0.2294 | 0.1809 | 0.1574 | 0.2129 | 0.2340 | 0.2673 | 0.2824 | 0.2110 |

| 2000 | 0.2183 | 0.1879 | 0.1777 | 0.1510 | 0.1589 | 0.1925 | 0.1496 | 0.2744 | 0.1637 |

| 2001 | 0.2208 | 0.1882 | 0.1739 | 0.1922 | 0.1811 | 0.1899 | 0.1852 | 0.1754 | 0.1562 |

| 2002 | 0.2810 | 0.2001 | 0.1845 | 0.2047 | 0.1859 | 0.1972 | 0.1882 | 0.1952 | 0.1912 |

| 2003 | 0.2761 | 0.2343 | 0.1534 | 0.2112 | 0.1881 | 0.1923 | 0.2223 | 0.1407 | 0.2208 |

| 2004 | 0.2297 | 0.2319 | 0.1665 | 0.2082 | 0.1994 | 0.1959 | 0.1350 | 0.1614 | 0.1980 |

| 2005 | 0.2222 | 0.1730 | 0.1642 | 0.1709 | 0.1903 | 0.1763 | 0.0911 | 0.1681 | 0.1559 |

| 2006 | 0.1656 | 0.1745 | 0.1637 | 0.1544 | 0.1878 | 0.1833 | 0.0813 | 0.1728 | 0.1285 |

| 2007 | 0.1578 | 0.1742 | 0.1637 | 0.1512 | 0.1792 | 0.2025 | 0.1098 | 0.1575 | 0.1600 |

| 2008 | 0.1712 | 0.2112 | 0.1844 | 0.1733 | 0.1889 | 0.2075 | 0.1007 | 0.1211 | 0.1531 |

| 2009 | 0.1881 | 0.2088 | 0.1829 | 0.2042 | 0.1687 | 0.2145 | 0.0875 | 0.1273 | 0.1815 |

| 2010 | 0.1814 | 0.1700 | 0.1571 | 0.1828 | 0.1466 | 0.1872 | 0.0542 | 0.1209 | 0.1672 |

| 2011 | 0.1632 | 0.1561 | 0.1468 | 0.1835 | 0.1241 | 0.1745 | 0.0778 | 0.1269 | 0.1590 |

| 2012 | 0.1563 | 0.1654 | 0.1530 | 0.1929 | 0.1390 | 0.1793 | 0.1041 | 0.1442 | 0.1621 |

| 2013 | 0.1713 | 0.1547 | 0.1569 | 0.1981 | 0.1388 | 0.1889 | 0.0862 | 0.1467 | 0.1765 |

| 2014 | 0.1691 | 0.1386 | 0.1471 | 0.2046 | 0.1331 | 0.1855 | 0.0828 | 0.1786 | 0.1807 |

| Study | Period | Firms | Model |

|---|---|---|---|

| [24] | 1959–1970 | 748 | Logit and Probit |

| [25] | 1977–1988 | 433 | Variance, ANOVA |

| [2] | 1987–1991 | 608 | Maximum likelihood and Tobit |

| [26] | 1983–1996 | 429 | GMM |

| [27] | 1984–1996 | 390 | GMM |

| [28] | 1973–2000 | 1784 | GMM-system |

| [29] | 1992–1996 | 87 | Logit and Probit |

| [30] | 1991–1997 | 1054 | Fixed effects panel estimation |

| Variable | Proxy | Symbol |

|---|---|---|

| Leverage | Book Leverage | |

| Business Cycle | Industrial Production Growth | IPGrate |

| Corporate Tax Growth Rate | TAXGrate | |

| Financial risk premium | RiskP | |

| ComPaperSp | ||

| Credit Supply | M3Grate | |

| Stock Market Performance | FTSE100Re | |

| Tangibility | Tangible assets divided by total assets | Tang |

| Profitability | Earnings (pre-interests and taxes) over the total assets | Prof |

| Firm Size | logarithm of total assets: | FSize |

| Growth Opportunity | Growth rate of net sales | Growthopp |

| Current Ratio | Current assets divided by current liabilities | CRatio |

| Variable | Mean | Median | Std | Min | Max | Conf. Int. (95%) | N |

|---|---|---|---|---|---|---|---|

| 0.1778 | 0.1151 | 0.2072 | 0 | 0.9505 | [0.1744, 0.1813] | 13,765 | |

| TAXGrate | 0.0514 | 0.0447 | 0.1375 | −0.2904 | 0.2674 | [0.0494, 0.0533] | 20 |

| IPGrate | −0.00000409 | 0.0027 | 0.0303 | −0.0906 | 0.0756 | [−0.0004, 0.0004] | 20 |

| M3Grate | 0.0735 | 0.0842 | 0.0503 | −0.0259 | 0.1624 | [0.0728, 0.0743] | 20 |

| 0.159 | 0.14 | 0.1421 | −0.05 | 0.41 | [0.1570, 0.1610] | 20 | |

| ComPaperSp | 0.2677 | 0.2449 | 0.1888 | 0.0629 | 0.8933 | [0.2650, 0.2703] | 20 |

| FTSE100Re | 0.0007 | 0.0945 | 0.2464 | −0.7878 | 0.2213 | [−0.0028, 0.0041] | 20 |

| Tang | 0.0093 | 0 | 0.0545 | −0.0034 | 1 | [0.0084, 0.0103] | 13,195 |

| CRatio | 3.5 | 1.472 | 23.4324 | 0 | 2273.13 | [3.0807, 3.9193] | 12,000 |

| Growthopp | 0.1235 | 0.0741 | 0.8365 | −11.0191 | 11.6272 | [0.1085, 0.1386] | 11,900 |

| Prof | −0.1413 | 0.052 | 4.1144 | −396.4 | 5.3351 | [−0.2108, −0.0718] | 13,463 |

| Size | 11.2109 | 11.0116 | 2.7172 | 0.6931 | 24.5519 | [11.1655, 11.2563] | 13,778 |

| (a) Corporate Tax Growth Rate | ||||||

| Variables | FEM | REM | Tobit | |||

| 1 | 2 | 1 | 2 | 1 | 2 | |

| ComPaperSp | −0.0078 | −0.00849 | −0.0115 | −0.0108 | −0.00749 | −0.00636 |

| (−0.95) | (−1.03) | (−1.39) | (−1.31) | (−1.48) | (−1.25) | |

| TAXGrate | −0.162 *** | −0.157 *** | −0.0791 *** | −0.0811 *** | −0.0436 *** | −0.0481 *** |

| (−5.61) | (−5.20) | (−5.79) | (−5.90) | (−5.23) | (−5.68) | |

| M3Grate | 0.165 *** | 0.186 *** | 0.206 *** | 0.189 *** | 0.142 *** | 0.108 *** |

| (−4.49) | (−4.76) | (−5.65) | (−4.83) | (−6.27) | (−4.5) | |

| FTSE100Re | 0.0199 *** | 0.0176 ** | 0.0144 * | 0.0164 ** | 0.00734 | 0.0113 ** |

| (−2.65) | (−2.29) | (−1.91) | (−2.13) | (−1.62) | (−2.44) | |

| Tang | −0.0508 | −0.0507 | −0.02 | −0.0198 | −0.0221 | −0.022 |

| (−0.88) | (−0.88) | (−0.35) | (−0.35) | (−0.64) | (−0.64) | |

| CRatio | −0.008 *** | −0.008 *** | −0.0084 *** | −0.0084 *** | −0.0114 *** | −0.0115 *** |

| (−18.14) | (−18.07) | (−19.42) | (−19.44) | (−22.77) | (−22.85) | |

| Growthopp | −0.00114 | −0.000919 | −0.00177 | −0.0019 | −0.000599 | −0.000892 |

| (−0.68) | (−0.54) | (−1.05) | (−1.13) | (−0.57) | (−0.84) | |

| Prof | −0.0013 *** | −0.0013 *** | −0.0018 *** | −0.0018 *** | −0.0009 *** | −0.0009 *** |

| (−4.12) | (−4.08) | (−5.42) | (−5.43) | (−4.94) | (−4.99) | |

| FSize | −0.0155 *** | −0.0170 *** | −0.00368 ** | −0.00299 * | −0.000011 | 0.00144 |

| (−8.11) | (−7.97) | (−2.49) | (−1.92) | (−0.01) | (−1.42) | |

| Year | yes | yes | yes | |||

| Adjusted R2 | 0.09% | 0.02% | 3.68% | 4.05% | 0.0547 | 0.0592 |

| Wald chi2 | 0.000 | 0.000 | ||||

| N | 9952 | 9952 | 9952 | 9952 | 9951 | 9951 |

| (b) Industrial Production Growth Rate | ||||||

| Variables | FEM | REM | Tobit | |||

| 1 | 2 | 1 | 2 | 1 | 2 | |

| ComPaperSp | −0.0085 | −0.00838 | −0.0107 | −0.0109 | −0.00566 | −0.00616 |

| (−1.02) | (−1.00) | (−1.28) | (−1.30) | (−1.11) | (−1.19) | |

| IPGrate | −0.332 *** | −0.321 *** | −0.285 *** | −0.317 *** | −0.137 *** | −0.185 *** |

| (−5.89) | (−5.50) | (−5.06) | (−5.42) | (−4.01) | (−5.16) | |

| M3Grate | 0.0940 ** | 0.104 ** | 0.137 *** | 0.109 *** | 0.0991 *** | 0.0602 *** |

| (2.96) | (3.02) | (−4.36) | (3.17) | (−5.11) | (2.85) | |

| FTSE100Re | 0.0171 * | 0.0156 * | 0.0103 | 0.0147 * | 0.00397 | 0.0100 ** |

| (2.31) | (2.03) | (−1.4) | (1.9) | (−0.9) | (2.16) | |

| Tang | −0.0538 | −0.0537 | −0.0227 | −0.0222 | −0.0239 | −0.0238 |

| (−0.93) | (−0.93) | (−0.40) | (−0.39) | (−0.70) | (−0.69) | |

| CRatio | −0.008 *** | −0.008 *** | −0.008 *** | −0.0084 *** | −0.0114 *** | −0.0115 *** |

| (−18.06) | (−18.02) | (−19.35) | (−19.38) | (−22.73) | (−22.82) | |

| Growthopp | −0.001 | −0.0009 | −0.0017 | −0.0018 | −0.0005 | −0.0008 |

| (−0.60) | (−0.55) | (−1.02) | (−1.12) | (−0.55) | (−0.81) | |

| Prof | −0.0014 *** | −0.0014 *** | −0.0018 *** | −0.0018 *** | −0.0009 *** | −0.001 *** |

| (−4.16) | (−4.14) | (−5.47) | (−5.50) | (−4.98) | (−5.04) | |

| FSize | −0.0161 *** | −0.0168 *** | −0.0039 *** | −0.00281 * | −0.0001 | 0.0015 |

| (−8.37) | (−7.86) | (−2.65) | (−1.81) | (−0.12) | (1.49) | |

| Year | yes | yes | yes | |||

| Adjusted R2 | 0.05% | 0.03% | 3.52% | 4.13% | ||

| Wald chi2 | 0.000 | 0.000 | ||||

| N | 9952 | 9952 | 9952 | 9952 | 9951 | 9951 |

| (a) Corporate Tax Growth Rate | ||||||

| Variables | FEM | REM | Tobit | |||

| 1 | 2 | 1 | 2 | 1 | 2 | |

| RiskP | −0.00829 | −0.0054 | −0.00454 | −0.00756 | 0.00322 | −0.00254 |

| (−0.78) | (−0.50) | (−0.42) | (−0.69) | (−0.49) | (−0.38) | |

| TAXGrate | −0.0809 *** | −0.0781 *** | −0.0717 *** | −0.0749 *** | −0.0383 *** | −0.0442 *** |

| (−6.47) | (−6.17) | (−5.74) | (−5.90) | (−5.02) | (−5.66) | |

| M3Grate | 0.149 *** | 0.164 *** | 0.179 *** | 0.162 *** | 0.121 *** | 0.0921 *** |

| (4.93) | (5.11) | (−5.95) | (5.02) | (−6.47) | (4.62) | |

| FTSE100Re | 0.0177 ** | 0.0159 ** | 0.0122 | 0.0142 * | 0.0069 | 0.0103 ** |

| (2.31) | (2.05) | (−1.59) | (1.82) | (−1.5) | (2.19) | |

| Tang | −0.0512 | −0.0511 | −0.0206 | −0.0203 | −0.0224 | −0.0223 |

| (−0.89) | (−0.89) | (−0.36) | (−0.36) | (−0.65) | (−0.65) | |

| CRatio | −0.0080 *** | −0.008 *** | −0.0084 *** | −0.0084 *** | −0.0114 *** | −0.0115 *** |

| (−18.12) | (−18.05) | (−19.39) | (−19.42) | (−22.75) | (−22.84) | |

| Growthopp | −0.0011 | −0.0009 | −0.0017 | −0.0019 | −0.0005 | −0.0008 |

| (−0.67) | (−0.55) | (−1.04) | (−1.13) | (−0.57) | (−0.84) | |

| Prof | −0.0013 *** | −0.0013 *** | −0.0018 *** | −0.0018 *** | −0.0009 *** | −0.0009 *** |

| (−4.11) | (−4.07) | (−5.40) | (−5.43) | (−4.91) | (−4.97) | |

| FSize | −0.0157 *** | −0.0170 *** | −0.0038 *** | −0.00302 * | −0.00007 | 0.0014 |

| (−8.24) | (−8.00) | (−2.60) | (−1.94) | (−0.08) | (1.38) | |

| Year | yes | yes | yes | |||

| Adjusted R2 | 0.08% | 0.02% | 3.60% | 4.03% | ||

| Wald chi2 | 0.000 | 0.000 | ||||

| N | 9952 | 9952 | 9952 | 9952 | 9951 | 9951 |

| (b) Industrial Production Growth Rate | ||||||

| Variables | FEM | REM | Tobit | |||

| 1 | 2 | 1 | 2 | 1 | 2 | |

| RiskP | −0.0079 | −0.0065 | −0.00376 | −0.0086 | 0.00407 | −0.00289 |

| (−0.74) | (−0.60) | (−0.35) | (−0.79) | (−0.63) | (−0.43) | |

| IPGrate | −0.310 *** | −0.300 *** | −0.254 *** | −0.290 *** | −0.119 *** | −0.169 *** |

| (−6.10) | (−5.64) | (−5.02) | (−5.43) | (−3.87) | (−5.15) | |

| M3Grate | 0.0798 ** | 0.0878 ** | 0.117 *** | 0.0884 *** | 0.0857 *** | 0.0482 *** |

| (2.96) | (2.95) | (−4.37) | (2.96) | (−5.18) | (2.62) | |

| FTSE100Re | 0.0148 | 0.0137 | 0.00839 | 0.0122 | 0.00397 | 0.0088 * |

| (−1.96) | (1.78) | (−1.11) | (1.58) | (−0.88) | (1.91) | |

| Tang | −0.0541 | −0.054 | −0.023 | −0.0226 | −0.024 | −0.024 |

| (−0.94) | (−0.94) | (−0.41) | (−0.40) | (−0.70) | (−0.69) | |

| CRatio | −0.008 *** | −0.008 *** | −0.0084 *** | −0.0084 *** | −0.0114 *** | −0.0115 *** |

| (−18.03) | (−18.00) | (−19.33) | (−19.36) | (−22.71) | (−22.81) | |

| Growthopp | −0.00101 | −0.00093 | −0.00172 | −0.00191 | −0.000595 | −0.0008 |

| (−0.60) | (−0.55) | (−1.02) | (−1.13) | (−0.57) | (−0.82) | |

| Prof | −0.0014 *** | −0.0014 *** | −0.0018 *** | −0.0018 *** | −0.0009 *** | −0.001 *** |

| (−4.15) | (−4.13) | (−5.45) | (−5.49) | (−4.95) | (−5.03) | |

| FSize | −0.0162 *** | −0.0168 *** | −0.004 *** | −0.00285 * | −0.0001 | 0.00147 |

| (−8.46) | (−7.90) | (−2.72) | (−1.84) | (−0.14) | (1.45) | |

| Year | yes | yes | yes | |||

| Adjusted R | 0.04% | 0.02% | 3.47% | 4.1% | ||

| Wald chi2 | 0.000 | 0.000 | ||||

| N | 9952 | 9952 | 9952 | 9952 | 9951 | 9951 |

| Variables | FEM | REM | Tobit | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 3 | 4 | 5 | 6 | 3 | 4 | 5 | 6 | 3 | 4 | 5 | 6 | |

| ComPaperSp | −0.00599 | −0.00635 | −0.00596 | −0.00177 | −0.0072 | −0.0053 | −0.0046 | 0.00007 | −0.0036 | −0.0017 | −0.0011 | 0.0017 |

| (−0.72) | (−0.72) | (−0.67) | (−0.19) | (−0.88) | (−0.60) | (−0.52) | (−0.01) | (−0.70) | (−0.32) | (−0.21) | (0.31) | |

| TAXGrate | −0.167*** | −0.163 *** | −0.203 *** | −0.193 *** | −0.0726 *** | −0.0696 *** | −0.0540 *** | −0.0499 *** | −0.0373 *** | −0.0345 *** | −0.0193 * | −0.0169 |

| (−5.76) | (−5.52) | (−6.33) | (−5.03) | (−5.29) | (−4.82) | (−2.99) | (−2.75) | (−4.42) | (−3.89) | (−1.74) | (−1.51) | |

| M3Grate | 0.0925 * | 0.0973 | 0.0798 | 0.0611 | 0.0533 | 0.0279 | −0.00347 | −0.0241 | −0.00541 | −0.0293 | −0.0598 | −0.0720 * |

| (1.78) | (1.48) | (1.15) | (0.87) | (1.03) | (0.43) | (−0.05) | (−0.35) | (−0.17) | (−0.74) | (−1.43) | (−1.71) | |

| FTSE100Re | 0.0184 ** | 0.0184 ** | 0.0210 ** | 0.0193 ** | 0.0119 | 0.0115 | 0.0164 ** | 0.0147 * | 0.0047 | 0.0044 | 0.0091 * | 0.0079 |

| (2.43) | (2.43) | (2.54) | (2.29) | (1.58) | (1.52) | (1.98) | (1.74) | (1.05) | (0.97) | (1.82) | (1.56) | |

| Tang | −0.0493 | −0.0493 | −0.0502 | −0.0486 | −0.0166 | −0.0162 | −0.0178 | −0.0161 | −0.0192 | −0.019 | −0.0207 | −0.0196 |

| (−0.86) | (−0.86) | (−0.87) | (−0.84) | (−0.29) | (−0.28) | (−0.31) | (−0.28) | (−0.56) | (−0.55) | (−0.60) | (−0.57) | |

| CRatio | −0.0081 *** | −0.0081 *** | −0.0081 *** | −0.0081 *** | −0.0084 *** | −0.0085 *** | −0.0084 *** | −0.0084 *** | −0.0116 *** | −0.0116 *** | −0.0116 *** | −0.0116 *** |

| (−18.23) | (−18.23) | (−18.22) | (−18.22) | (−19.56) | (−19.56) | (−19.55) | (−19.53) | (−22.96) | (−22.96) | (−22.97) | (−22.96) | |

| Growthopp | −0.00142 | −0.00142 | −0.00142 | −0.00141 | −0.00222 | −0.0022 | −0.0022 | −0.0021 | −0.001 | −0.001 | −0.001 | −0.001 |

| (−0.84) | (−0.84) | (−0.84) | (−0.84) | (−1.32) | (−1.31) | (−1.30) | (−1.30) | (−1.02) | (−1.01) | (−0.99) | (−0.99) | |

| Prof | −0.0014 *** | −0.0014 *** | −0.0014 *** | −0.0014 *** | −0.0018 *** | −0.0018 *** | −0.0018 *** | −0.0018 *** | −0.0009 *** | −0.0009 *** | −0.0009 *** | −0.0009 *** |

| (−4.14) | (−4.14) | (−4.15) | (−4.15) | (−5.40) | (−5.41) | (−5.42) | (−5.42) | (−4.94) | (−4.93) | (−4.94) | (−4.94) | |

| FSize | −0.0140 *** | −0.0140 *** | −0.0138 *** | −0.0137 *** | −0.0019 | −0.0017 | −0.0015 | −0.0015 | 0.0018 * | 0.0019 * | 0.0021 ** | 0.0021 ** |

| (−6.81) | (−6.75) | (−6.62) | (−6.55) | (−1.28) | (−1.14) | (−1.02) | (−0.97) | (1.86) | (1.96) | (2.15) | (2.17) | |

| −0.0100 ** | −0.00947 | −0.0111 | 0.00177 | −0.0204 *** | −0.0233 *** | −0.0261 *** | −0.01 | −0.0200 *** | −0.0227 *** | −0.0254 *** | −0.0165 ** | |

| (−1.96) | (−1.38) | (−1.54) | (0.15) | (−4.15) | (−3.53) | (−3.79) | (−0.83) | (−6.51) | (−5.57) | (−5.97) | (−2.19) | |

| −0.0126 | 0.0082 | 0.0306 | 0.067 | 0.105 | 0.118 | 0.0665 | 0.103 | 0.119 | ||||

| (−0.12) | (0.08) | (0.25) | (0.64) | (0.97) | (0.98) | (1.02) | (1.52) | (1.59) | ||||

| −0.0193 | −0.0679 | −0.0362 | −0.075 | −0.0357 ** | −0.0722 | |||||||

| (−0.77) | (−0.84) | (−1.44) | (−0.92) | (−2.29) | (−1.43) | |||||||

| 0.00445 | −0.00846 | 0.00504 | ||||||||||

| (0.07) | (−0.13) | (0.13) | ||||||||||

| −0.0814 * | −0.0961 ** | −0.0571 * | ||||||||||

| (−1.75) | (−2.06) | (−1.95) | ||||||||||

| Adjusted R2 | 0.22% | 0.22% | 0.24% | 0.26% | 4.63% | 4.74% | 4.84% | 4.91% | ||||

| Wald chi2 | 0.000 | 0.000 | 0.000 | 0.000 | ||||||||

| N | 9952 | 9952 | 9952 | 9952 | 9952 | 9952 | 9952 | 9952 | 9951 | 9951 | 9951 | 9951 |

| Variables | FEM | REM | Tobit | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 3 | 4 | 5 | 6 | 3 | 4 | 5 | 6 | 3 | 4 | 5 | 6 | |

| ComPaperSp | −0.0081 | −0.0053 | −0.0093 | −0.006 | −0.00977 | −0.00588 | −0.0087 | −0.00489 | −0.005 | −0.0026 | −0.0032 | −0.0009 |

| (−0.97) | (−0.62) | (−1.07) | (−0.68) | (−1.17) | (−0.68) | (−0.99) | (−0.55) | (−0.99) | (−0.50) | (−0.60) | (−0.18) | |

| IPGrate | −0.351*** | −0.345 *** | −0.599 *** | −0.581 *** | −0.322 *** | −0.315 *** | −0.492 *** | −0.472 *** | −0.170 *** | −0.165 *** | −0.204 *** | −0.193 *** |

| (−6.20) | (−6.08) | (−5.89) | (−5.69) | (−5.69) | (−5.54) | (−4.87) | (−4.66) | (−4.90) | (−4.74) | (−3.34) | (−3.14) | |

| M3Grate | −0.0171 | −0.0573 | −0.0424 | −0.0531 | −0.0426 | −0.0983 * | −0.0896 | −0.101 * | −0.0550 ** | −0.0902 *** | −0.0882 *** | −0.0949 *** |

| (−0.37) | (−1.05) | (−0.77) | (−0.96) | (−0.93) | (−1.80) | (−1.64) | (−1.85) | (−1.97) | (−2.72) | (−2.65) | (−2.84) | |

| FTSE100Re | 0.0170 * | 0.0174 * | 0.00466 | 0.00568 | 0.0113 | 0.012 | 0.00276 | 0.0038 | 0.0045 | 0.0049 | 0.0028 | 0.0035 |

| (2.3) | (2.36) | (0.55) | (0.67) | (1.53) | (1.62) | (0.32) | (0.45) | (1.01) | (1.1) | (0.55) | (0.68) | |

| Tang | −0.0507 | −0.0502 | −0.0448 | −0.0427 | −0.0176 | −0.0166 | −0.0128 | −0.0106 | −0.0198 | −0.0192 | −0.0184 | −0.0169 |

| (−0.88) | (−0.87) | (−0.78) | (−0.74) | (−0.31) | (−0.29) | (−0.23) | (−0.19) | (−0.57) | (−0.56) | (−0.53) | (−0.49) | |

| CRatio | −0.0081 *** | −0.0081 *** | −0.0081 *** | −0.0081 *** | −0.0084 *** | -0.0084 *** | −0.0085 *** | −0.0085 *** | −0.0116 *** | −0.0116 *** | −0.0116 *** | −0.0116 *** |

| (−18.22) | (−18.23) | (−18.28) | (−18.28) | (−19.55) | (−19.55) | (−19.60) | (−19.60) | (−22.95) | (−22.95) | (−22.95) | (−22.96) | |

| Growthopp | −0.0014 | −0.0013 | −0.0011 | −0.0011 | −0.0021 | −0.0021 | −0.002 | −0.0019 | −0.001 | −0.0009 | −0.0009 | −0.0009 |

| (−0.83) | (−0.81) | (−0.70) | (−0.68) | (−1.29) | (−1.25) | (−1.19) | (−1.17) | (−0.96) | (−0.91) | (−0.89) | (−0.87) | |

| Prof | −0.0014 *** | −0.0014 *** | −0.0014 *** | −0.0014 *** | −0.0018 *** | −0.0018 *** | −0.0018 *** | −0.0018 *** | −0.0009 *** | −0.0009 *** | −0.0009 *** | −0.0009 *** |

| (−4.20) | (−4.19) | (−4.15) | (−4.14) | (−5.45) | (−5.44) | (−5.43) | (−5.43) | (−4.97) | (−4.95) | (−4.95) | (−4.94) | |

| FSize | −0.0136 *** | −0.0133 *** | −0.0143 *** | −0.0142 *** | −0.0018 | −0.0014 | −0.0017 | −0.0017 | 0.0019 * | 0.002 ** | 0.0019 ** | 0.002 ** |

| (−6.66) | (−6.47) | (−6.87) | (−6.80) | (−1.18) | (−0.96) | (−1.17) | (−1.12) | (1.93) | (2.09) | (1.98) | (2.02) | |

| −0.0172 *** | −0.0226 *** | −0.0191 ** | 0.0149 | −0.0268 *** | −0.0343 *** | −0.0323 *** | 0.005 | −0.0234 *** | −0.0282 *** | −0.0277 *** | −0.0042 | |

| (−3.38) | (−3.47) | (−2.89) | (0.97) | (−5.44) | (−5.41) | (−5.04) | (−0.33) | (−7.59) | (−7.17) | (−6.97) | (−0.44) | |

| 0.133 | 0.108 | −0.0863 | 0.186 * | 0.171 * | −0.0344 | 0.123 ** | 0.120 * | −0.0125 | ||||

| (1.33) | (1.07) | (−0.54) | (1.86) | (1.7) | (−0.21) | (1.98) | (1.92) | (−0.12) | ||||

| 0.378 ** | 1.648 | 0.266 ** | 1.595 * | 0.0595 | 0.925 | |||||||

| (3.00) | (1.76) | (2.12) | (1.7) | (0.78) | (1.58) | |||||||

| −0.29 | −0.307 * | −0.198 * | ||||||||||

| (−1.60) | (−1.69) | (−1.75) | ||||||||||

| Commercial paper spread*Crisis | −0.0567 | −0.0674 | −0.0397 | |||||||||

| (−1.02) | (−1.21) | (−1.14) | ||||||||||

| Adjusted R2 | 0.27% | 0.31% | 0.21% | 0.23% | 4.74% | 4.91% | 4.77% | 4.85% | ||||

| Wald chi2 | 0.000 | 0.000 | 0.000 | 0.000 | ||||||||

| N | 9952 | 9952 | 9952 | 9952 | 9952 | 9952 | 9952 | 9952 | 9951 | 9951 | 9951 | 9951 |

| Variables | FEM | REM | Tobit | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 3 | 4 | 5 | 6 | 3 | 4 | 5 | 6 | 3 | 4 | 5 | 6 | |

| RiskP | −0.0097 | −0.0097 | −0.0093 | −0.0067 | −0.008 | −0.0078 | −0.0072 | −0.0029 | −0.0004 | −0.0003 | 0.0002 | 0.0028 |

| (−0.91) | (−0.91) | (−0.88) | (−0.59) | (−0.75) | (−0.73) | (−0.67) | (−0.25) | (−0.07) | (−0.06) | (0.04) | (0.4) | |

| TAXGrate | −0.0784*** | −0.0782*** | −0.0700 *** | −0.0695 *** | −0.0682 *** | −0.0661 *** | −0.0510 *** | −0.0503 *** | −0.0349 *** | −0.0332 *** | −0.0183 * | −0.0180 * |

| (−6.25) | (−6.11) | (−4.20) | (−4.17) | (−5.45) | (−5.20) | (−3.09) | (−3.05) | (−4.54) | (−4.24) | (−1.81) | (−1.77) | |

| M3Grate | 0.0770 * | 0.0736 | 0.0577 | 0.0566 | 0.0329 | 0.00781 | −0.0207 | −0.0226 | −0.0164 | −0.0365 | −0.0647 * | −0.0656 * |

| (1.69) | (1.37) | (1) | (0.98) | (0.73) | (0.15) | (−0.37) | (−0.40) | (−0.59) | (−1.12) | (−1.86) | (−1.88) | |

| FTSE100Re | 0.0160 ** | 0.0160 ** | 0.0187 ** | 0.0176 ** | 0.0095 | 0.0094 | 0.0146 * | 0.0141 | 0.0042 | 0.0041 | 0.009 * | 0.0087 * |

| (2.08) | (2.08) | (2.21) | (2.04) | (1.25) | (1.23) | (1.72) | (1.63) | (0.91) | (0.89) | (1.77) | (1.67) | |

| Tang | −0.0495 | −0.0495 | −0.0504 | −0.0485 | −0.0169 | −0.0163 | −0.0179 | −0.0159 | −0.0193 | −0.019 | −0.0207 | −0.0194 |

| (−0.86) | (−0.86) | (−0.87) | (−0.84) | (−0.30) | (−0.29) | (−0.32) | (−0.28) | (−0.56) | (−0.55) | (−0.60) | (−0.56) | |

| CRatio | −0.008 *** | −0.008 *** | −0.008 *** | −0.008 *** | −0.0084 *** | −0.0084 *** | −0.0084 *** | −0.0084 *** | −0.0116 *** | −0.0116 *** | −0.0116 *** | −0.0116 *** |

| (−18.21) | (−18.21) | (−18.21) | (−18.21) | (−19.55) | (−19.55) | (−19.54) | (−19.54) | (−22.95) | (−22.96) | (−22.96) | (−22.97) | |

| Growthopp | −0.0014 | −0.0014 | −0.0014 | −0.0014 | −0.0022 | −0.0022 | −0.0022 | −0.0022 | −0.001 | −0.001 | −0.001 | −0.001 |

| (−0.84) | (−0.84) | (−0.84) | (−0.83) | (−1.32) | (−1.31) | (−1.30) | (−1.30) | (−1.02) | (−1.01) | (−0.99) | (−0.99) | |

| Prof | −0.0014 *** | −0.0014 *** | −0.0014 *** | −0.0014 *** | −0.0018 *** | −0.0018 *** | −0.0018 *** | −0.0018 *** | −0.0009 *** | −0.0009 *** | −0.0009 *** | −0.0009 *** |

| (−4.14) | (−4.14) | (−4.15) | (−4.15) | (−5.40) | (−5.41) | (−5.42) | (−5.42) | (−4.92) | (−4.92) | (−4.94) | (−4.94) | |

| FSize | −0.0141 *** | −0.0140 *** | −0.0139 *** | −0.0138 *** | −0.002 | −0.0017 | −0.0015 | −0.0015 | 0.0018 * | 0.0019 ** | 0.0021 ** | 0.0021 ** |

| (−6.86) | (−6.76) | (−6.62) | (−6.57) | (−1.32) | (−1.14) | (−1.03) | (−0.98) | (1.84) | (1.96) | (2.15) | (2.18) | |

| −0.0107 ** | −0.0112 * | −0.0127 * | −0.0142 * | −0.0212 *** | −0.0248 *** | −0.0274 *** | −0.0277 *** | −0.0203 *** | −0.0232 *** | −0.0257 *** | −0.0260 *** | |

| (−2.11) | (−1.72) | (−1.86) | (−1.85) | (−4.34) | (−3.95) | (−4.20) | (−3.72) | (−6.62) | (−5.93) | (−6.32) | (−5.58) | |

| 0.0117 | 0.031 | 0.155 | 0.0878 | 0.122 | 0.256 ** | 0.0735 | 0.107 * | 0.193 *** | ||||

| (0.12) | (0.3) | (1.3) | (0.89) | (1.2) | (2.16) | (1.19) | (1.69) | (2.6) | ||||

| −0.0193 | −0.207 ** | −0.0363 | −0.235 ** | −0.0359 ** | −0.164 *** | |||||||

| (−0.77) | (−2.12) | (−1.44) | (−2.40) | (−2.30) | (−2.68) | |||||||

| 0.125 * | 0.129 ** | 0.0833 ** | ||||||||||

| (1.91) | (1.98) | (2.04) | ||||||||||

| −0.062 | −0.0768 ** | −0.0489 ** | ||||||||||

| (−1.63) | (−2.01) | (−2.05) | ||||||||||

| Adjusted R2 | 0.21% | 0.22% | 0.24% | 0.26% | 4.61% | 4.74% | 4.84% | 4.90% | ||||

| Wald chi2 | 0.000 | 0.000 | 0.000 | 0.000 | ||||||||

| N | 9952 | 9952 | 9952 | 9952 | 9952 | 9952 | 9952 | 9952 | 9951 | 9951 | 9951 | 9951 |

| Variables | FEM | REM | Tobit | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 3 | 4 | 5 | 6 | 3 | 4 | 5 | 6 | 3 | 4 | 5 | 6 | |

| RiskP | −0.011 | −0.0109 | −0.0176 | −0.0189 | −0.0092 | −0.0091 | −0.0137 | −0.0128 | −0.001 | −0.00101 | −0.0019 | −0.00103 |

| (−1.03) | (−1.02) | (−1.61) | (−1.60) | (−0.86) | (−0.85) | (−1.26) | (−1.08) | (−0.15) | (−0.15) | (−0.28) | (−0.14) | |

| IPGrate | −0.332 *** | −0.335 *** | −0.592 *** | −0.592 *** | −0.297 *** | −0.301 *** | −0.479 *** | −0.475 *** | −0.156 *** | −0.158 *** | −0.194 *** | −0.191 *** |

| (−6.48) | (−6.53) | (−6.12) | (−6.09) | (−5.81) | (−5.88) | (−5.00) | (−4.93) | (−4.96) | (−5.02) | (−3.34) | (−3.27) | |

| M3Grate | −0.0324 | −0.0704 | −0.0654 | −0.0652 | −0.0621 | −0.114 ** | −0.112 ** | −0.113 ** | −0.0656 ** | −0.0974 *** | −0.0969 *** | −0.0972 *** |

| (−0.77) | (−1.44) | (−1.34) | (−1.33) | (−1.48) | (−2.33) | (−2.30) | (−2.32) | (−2.54) | (−3.27) | (−3.26) | (−3.27) | |

| FTSE100Re | 0.0143 | 0.0151* | 0.00012 | 0.000896 | 0.0086 | 0.00983 | −0.000826 | 0.000604 | 0.00375 | 0.00449 | 0.00232 | 0.00326 |

| (1.89) | (2) | (0.01) | (0.1) | (1.14) | (1.3) | (−0.09) | (0.07) | (0.82) | (0.98) | (0.43) | (0.6) | |

| Tang | −0.0509 | −0.0503 | −0.0447 | −0.0436 | −0.0178 | −0.0166 | −0.0127 | −0.0114 | −0.0199 | −0.0193 | −0.0185 | −0.0175 |

| (−0.88) | (−0.87) | (−0.78) | (−0.76) | (−0.31) | (−0.29) | (−0.22) | (−0.20) | (−0.58) | (−0.56) | (−0.53) | (−0.51) | |

| CRatio | −0.0081 *** | −0.0081 *** | −0.0081 *** | −0.0081 *** | −0.0084 *** | −0.0084 *** | −0.0085 *** | −0.0085 *** | −0.0116 *** | −0.0116 *** | −0.0116 *** | −0.0116 *** |

| (−18.20) | (−18.22) | (−18.26) | (−18.29) | (−19.54) | (−19.54) | (−19.59) | (−19.62) | (−22.94) | (−22.95) | (−22.95) | (−22.97) | |

| Growthopp | −0.0014 | −0.0013 | −0.0011 | −0.001 | −0.0021 | −0.0021 | −0.002 | −0.0019 | −0.001 | −0.0009 | −0.0009 | −0.0009 |

| (−0.83) | (−0.80) | (−0.68) | (−0.62) | (−1.30) | (−1.25) | (−1.19) | (−1.14) | (−0.97) | (−0.91) | (−0.89) | (−0.85) | |

| Prof | −0.0014 *** | −0.0014 *** | −0.0014 *** | −0.0014 *** | −0.002 *** | −0.002 *** | −0.002 *** | −0.002 *** | −0.001 *** | −0.001 *** | −0.001 *** | −0.001 *** |

| (−4.19) | (−4.19) | (−4.15) | (−4.13) | (−5.44) | (−5.44) | (−5.43) | (−5.42) | (−4.96) | (−4.95) | (−4.94) | (−4.93) | |

| FSize | −0.0138 *** | −0.0134 *** | −0.0145 *** | −0.0147 *** | −0.0018 | −0.0014 | −0.0018 | −0.00185 | 0.0018 * | 0.002 ** | 0.0019 ** | 0.0019 * |

| (−6.74) | (−6.50) | (−6.94) | (−6.98) | (−1.23) | (−0.98) | (−1.20) | (−1.20) | (1.9) | (2.08) | (1.97) | (1.94) | |

| −0.0177 *** | −0.0237 *** | −0.0208 ** | 0.0123 | −0.0273 *** | −0.0354 *** | −0.0338 *** | 0.00246 | −0.0235 *** | −0.0285 *** | −0.0282 *** | −0.0046 | |

| (−3.47) | (−3.67) | (−3.19) | (0.8) | (−5.53) | (−5.65) | (−5.37) | (0.16) | (−7.58) | (−7.33) | (−7.18) | (−0.49) | |

| 0.148 | 0.132 | −0.16 | 0.202 ** | 0.194 ** | −0.109 | 0.131 ** | 0.129 ** | −0.0646 | ||||

| (1.52) | (1.36) | (−1.06) | (2.08) | (2) | (−0.72) | (2.16) | (2.13) | (−0.69) | ||||

| 0.397 ** | 2.375 ** | 0.277 ** | 2.347 *** | 0.0571 | 1.382 *** | |||||||

| (3.13) | (2.98) | (2.2) | (2.94) | (0.74) | (2.78) | |||||||

| −0.406 * | −0.428 *** | −0.275 *** | ||||||||||

| (−2.49) | (−2.63) | (−2.70) | ||||||||||

| 0.0322 | 0.0177 | 0.00905 | ||||||||||

| (0.98) | (0.54) | (0.44) | ||||||||||

| Adjusted R2 | 0.25% | 0.30% | 0.19% | 0.19% | 4.70% | 4.90% | 4.75% | 4.79% | ||||

| Wald chi2 | 0.000 | 0.000 | 0.000 | 0.000 | ||||||||

| N | 9952 | 9952 | 9952 | 9952 | 9952 | 9952 | 9952 | 9952 | 9951 | 9951 | 9951 | 9951 |

| Model Sign | ||||||

|---|---|---|---|---|---|---|

| Variable, Theory, Hypothesis and Sign | FE | RE | Tobit | |||

| Business Cycle | TOT | H1 | + | |||

| POT | H1 | − | − | − | − | |

| MTT | N/A | N/A | ||||

| Credit Supply | TOT | H2 | + | + | + | + |

| POT | H2 | + | + | + | + | |

| MTT | N/A | N/A | ||||

| Final Market Risk | TOT | H3 | − | |||

| POT | H3 | + | ||||

| MTT | N/A | N/A | ||||

| Stock Market Performance | TOT | H4 | + | + | + | + |

| POT | H4 | − | ||||

| MTT | H4 | − | ||||

| Pre-Crisis Sign | Post-Crisis Sign | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Variable, Theory, Hypothesis and Sign | FE | RE | Tobit | FE | RE | Tobit | |||

| Business Cycle | TOT | H1 | + | ||||||

| POT | H1 | − | − | − | − | − | − | − | |

| MTT | N/A | N/A | |||||||

| Credit Supply | TOT | H2 | + | + | + | + | + | ||

| POT | H2 | + | + | + | + | + | |||

| MTT | N/A | N/A | − | − | |||||

| Final Market Risk | TOT | H3 | − | − | − | − | |||

| POT | H3 | + | |||||||

| MTT | N/A | N/A | |||||||

| Stock Market Performance | TOT | H4 | + | + | + | + | + | + | + |

| POT | H4 | − | |||||||

| MTT | H4 | − | |||||||

| Variable | FEM | REM | Tobit | GLS | SGMM | DGMM |

|---|---|---|---|---|---|---|

| ComPaperSp | −0.0078 | −0.0115 | −0.00749 | −0.0169 ** | 0.0496 *** | 0.0310 ** |

| (−0.95) | (−1.39) | (−1.48) | (−2.46) | (−3.52) | (−2.18) | |

| TAXGrate | −0.162 *** | −0.0791 *** | −0.0436 *** | −0.0876 *** | −0.0253 | −0.033 |

| (−5.61) | (−5.79) | (−5.23) | (−8.32) | (−1.09) | (−1.23) | |

| M3Grate | 0.165 *** | 0.206 *** | 0.142 *** | 0.297 *** | −0.135 ** | −0.059 |

| (−4.49) | (−5.65) | (−6.27) | (−10.6) | (−1.98) | (−0.79) | |

| FTSE100Re | 0.0199 *** | 0.0144 * | 0.00734 | 0.00852 | 0.0224 | 0.0103 |

| (−2.65) | (−1.91) | (−1.62) | (−1.44) | (−1.08) | (−0.4) | |

| Tang | −0.0508 | −0.02 | −0.0221 | 0.0760 * | 0.0354 | −0.0295 |

| (−0.88) | (−0.35) | (−0.64) | (−1.83) | (−0.37) | (−0.21) | |

| CRatio | −0.00808 *** | −0.00843 *** | −0.0114 *** | −0.00900 *** | −0.00940 *** | −0.00748 *** |

| (−18.14) | (−19.42) | (−22.77) | (−33.70) | (−6.10) | (−5.57) | |

| Growthopp | −0.00114 | −0.00177 | −0.000599 | 0.0000676 | −0.00489 | −0.00101 |

| (−0.68) | (−1.05) | (−0.57) | (−0.05) | (−1.57) | (−0.36) | |

| −0.00139 *** | −0.00182 *** | −0.000981 *** | −0.00473 *** | −0.00219 *** | −0.00961 ** | |

| (−4.12) | (−5.42) | (−4.94) | (−3.94) | (−3.90) | (−2.32) | |

| FSize | −0.0155 *** | −0.00368 ** | −0.000011 | 0.0174 *** | −0.0142 ** | −0.00716 |

| (−8.11) | (−2.49) | (−0.01) | (−37.82) | (−2.05) | (−0.57) | |

| 0.690 *** | 0.615 *** | |||||

| (−24.76) | (17.98) | |||||

| Adjusted R2, overall | 0.09% | 3.68% | ||||

| Wald chi2 (Prob > chi2) | 0.000 | 0.000 | 0.000 | 0.000 | ||

| Sargan test (Prob > chi2) | 0.000 | 0.000 | ||||

| Hansen test (Prob > chi2) | 0.000 | 0.074 | ||||

| N | 9952 | 9952 | 9951 | 9952 | 9495 | 8605 |

| Methods | FEM | REM | Tobit | GLS | SGMM | DGMM |

|---|---|---|---|---|---|---|

| ComPaperSp | −0.0085 | −0.0107 | −0.00566 | −0.00893 | 0.0441 *** | 0.0428 *** |

| (−1.02) | (−1.28) | (−1.11) | (−1.27) | (−2.67) | (−2.91) | |

| IPGrate | −0.332 *** | −0.285 *** | −0.137 *** | −0.215 *** | 0.00144 | 0.103 |

| (−5.89) | (−5.06) | (−4.01) | (−4.75) | (−0.01) | (−0.43) | |

| M3Grate | 0.0940 ** | 0.137 *** | 0.0991 *** | 0.183 *** | −0.0865 * | −0.0839 |

| (−2.96) | (−4.36) | (−5.11) | (−7.13) | (−1.67) | (−1.52) | |

| FTSE100Re | 0.0171 * | 0.0103 | 0.00397 | −0.00213 | −0.0128 | −0.0348 |

| (−2.31) | (−1.4) | (−0.9) | (−0.36) | (−0.23) | (−0.75) | |

| Tang | −0.0538 | −0.0227 | −0.0239 | 0.0235 | 0.0275 | −0.0409 |

| (−0.93) | (−0.40) | (−0.70) | (−0.55) | (−0.29) | (−0.29) | |

| CRatio | −0.00805 *** | −0.00841 *** | −0.0114 *** | −0.00994 *** | −0.00941 *** | −0.00749 *** |

| (−18.06) | (−19.35) | (−22.73) | (−27.09) | (−6.11) | (−5.61) | |

| Growthopp | −0.00102 | −0.00171 | −0.000581 | −0.000177 | −0.00528 * | −0.000701 |

| (−0.60) | (−1.02) | (−0.55) | (−0.12) | (−1.68) | (−0.25) | |

| Prof | −0.00141 *** | −0.00184 *** | −0.000989 *** | −0.00486 *** | −0.00229 *** | −0.00977 ** |

| (−4.16) | (−5.47) | (−4.98) | (−4.05) | (−4.12) | (−2.34) | |

| FSize | −0.0161 *** | −0.00393 *** | −0.000116 | 0.0170 *** | −0.0112 * | −0.00284 |

| (−8.37) | (−2.65) | (−0.12) | (−36.36) | (−1.86) | (−0.32) | |

| 0.690 *** | 0.618 *** | |||||

| −24.87 | −18.12 | |||||

| Adjusted R2, overall | 0.05% | 3.52% | ||||

| Wald chi2 (Prob > chi2) | 0.000 | 0.000 | 0.000 | 0.000 | ||

| Sargan test (Prob > chi2) | 0.000 | 0.000 | ||||

| Hansen test (Prob > chi2) | 0.000 | 0.102 | ||||

| N | 9952 | 9952 | 9951 | 9952 | 9495 | 8605 |

| Methods | FEM | REM | Tobit | GLS | SGMM | DGMM |

|---|---|---|---|---|---|---|

| RiskP | −0.00829 | −0.00454 | 0.00322 | −0.0134 | 0.0367 *** | 0.0268 |

| (−0.78) | (−0.42) | (−0.49) | (−1.56) | (−2.6) | (−1.1) | |

| TAXGrate | −0.0809 *** | −0.0717 *** | −0.0383 *** | −0.0792 *** | −0.0398 * | −0.0313 |

| (−6.47) | (−5.74) | (−5.02) | (−8.17) | (−1.65) | (−1.10) | |

| M3Grate | 0.149 *** | 0.179 *** | 0.121 *** | 0.265 *** | −0.0165 | −0.00682 |

| (−4.93) | (−5.95) | (−6.47) | (−11.45) | (−0.37) | (−0.09) | |

| FTSE100Re | 0.0177 ** | 0.0122 | 0.0069 | 0.00454 | 0.0138 | 0.00387 |

| (−2.31) | (−1.59) | (−1.5) | (−0.74) | (−0.63) | (−0.13) | |

| Tang | −0.0512 | −0.0206 | −0.0224 | 0.0802 * | 0.0358 | −0.0331 |

| (−0.89) | (−0.36) | (−0.65) | (−1.96) | (−0.37) | (−0.23) | |

| CRatio | −0.00807 *** | −0.00842 *** | −0.0114 *** | −0.00891 *** | −0.00949 *** | −0.00752 *** |

| (−18.12) | (−19.39) | (−22.75) | (−34.02) | (−6.14) | (−5.60) | |

| Growthopp | −0.00112 | −0.00175 | −0.000597 | 0.0000515 | −0.00497 | −0.000825 |

| (−0.67) | (−1.04) | (−0.57) | (−0.04) | (−1.59) | (−0.29) | |

| Prof | −0.00139 *** | −0.00182 *** | −0.000974 *** | −0.00471 *** | −0.00226 *** | −0.00956 ** |

| (−4.11) | (−5.40) | (−4.91) | (−3.92) | (−4.00) | (−2.36) | |

| FSize | −0.0157 *** | −0.00383 *** | −0.0000785 | 0.0174 *** | −0.0122 * | −0.00557 |

| (−8.24) | (−2.60) | (−0.08) | (−37.86) | (−1.74) | (−0.38) | |

| 0.687 *** | 0.613 *** | |||||

| −24.78 | −18.1 | |||||

| Adjusted R2, overall | 0.08% | 3.60% | ||||

| Wald chi2 (Prob > chi2) | 0.000 | 0.000 | 0.000 | 0.000 | ||

| Sargan test (Prob > chi2) | 0.000 | 0.000 | ||||

| Hansen test (Prob > chi2) | 0.000 | 0.047 | ||||

| N | 9952 | 9952 | 9951 | 9952 | 9495 | 8605 |

| Methods | FEM | REM | Tobit | GLS | SGMM | DGMM |

|---|---|---|---|---|---|---|

| RiskP | −0.0079 | −0.00376 | 0.00407 | −0.00429 | 0.0352 ** | 0.00377 |

| (−0.74) | (−0.35) | (−0.63) | (−0.49) | (−2.01) | (−0.16) | |

| IPGrate | −0.310 *** | −0.254 *** | −0.119 *** | −0.194 *** | −0.08 | −0.244 |

| (−6.10) | (−5.02) | (−3.87) | (−4.77) | (−0.54) | (−1.15) | |

| M3Grate | 0.0798 ** | 0.117 *** | 0.0857 *** | 0.168 *** | −0.0339 | 0.0203 |

| (−2.96) | (−4.37) | (−5.18) | (−7.67) | (−0.89) | (−0.29) | |

| FTSE100Re | 0.0148 | 0.00839 | 0.00397 | −0.0037 | −0.0195 | 0.0173 |

| (−1.96) | (−1.11) | (−0.88) | (−0.61) | (−0.65) | (−0.46) | |

| Tang | −0.0541 | −0.023 | −0.024 | 0.0269 | 0.0221 | −0.0505 |

| (−0.94) | (−0.41) | (−0.70) | (−0.64) | (−0.23) | (−0.35) | |

| CRatio | −0.00804 *** | −0.00840 *** | −0.0114 *** | −0.00990 *** | −0.00948 *** | −0.00756 *** |

| (−18.03) | (−19.33) | (−22.71) | (−27.13) | (−6.15) | (−5.54) | |

| Growthopp | −0.00101 | −0.00172 | −0.000595 | −0.000196 | −0.00474 | −0.000818 |

| (−0.60) | (−1.02) | (−0.57) | (−0.14) | (−1.53) | (−0.30) | |

| Prof | −0.00140 *** | −0.00183 *** | −0.000982 *** | −0.00486 *** | −0.00228 *** | −0.00990 ** |

| (−4.15) | (−5.45) | (−4.95) | (−4.05) | (−4.08) | (−2.30) | |

| FSize | −0.0162 *** | −0.00403 *** | −0.000132 | 0.0170 *** | −0.0123 * | −0.00228 |

| (−8.46) | (−2.72) | (−0.14) | (−36.32) | (−1.89) | (−0.25) | |

| 0.690 *** | 0.617 *** | |||||

| (−24.95) | (−18.08) | |||||

| Adjusted R2, overall | 0.04% | 3.47% | ||||

| Wald chi2 (Prob > chi2) | 0.000 | 0.000 | 0.000 | 0.000 | ||

| Sargan test (Prob > chi2) | 0.000 | 0.000 | ||||

| Hansen test (Prob > chi2) | 0.000 | 0.031 | ||||

| N | 9952 | 9952 | 9951 | 9952 | 9495 | 8605 |

| Model Sign | ||||||

|---|---|---|---|---|---|---|

| Variable, Theory, Hypothesis and Sign | GLS | SGMM | DGMM | |||

| Business Cycle | TOT | H1 | + | |||

| POT | H1 | − | − | − | − | |

| MTT | N/A | N/A | ||||

| Credit supply | TOT | H2 | + | + | ||

| POT | H2 | + | + | |||

| MTT | N/A | N/A | ||||

| Final Market Risk | TOT | H3 | − | − | ||

| POT | H3 | + | + | + | ||

| MTT | N/A | N/A | ||||

| Stock Market Performance | TOT | H4 | + | + | ||

| POT | H4 | − | ||||

| MTT | H4 | − | ||||

| Pre-Crisis Sign | Post-Crisis Sign | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Variable, Theory, Hypothesis and Sign | FE | RE | Tobit | GLS | FE | RE | Tobit | GLS | |||

| Business Cycle | TOT | H1 | + | ||||||||

| POT | H1 | − | − | − | − | − | − | − | − | − | |

| MTT | N/A | N/A | |||||||||

| Credit supply | TOT | H2 | + | + | + | + | + | + | + | ||

| POT | H2 | + | + | + | + | + | + | + | |||

| MTT | N/A | N/A | − | − | |||||||

| Final Market Risk | TOT | H3 | − | − | − | − | − | − | |||

| POT | H3 | + | |||||||||

| MTT | N/A | N/A | |||||||||

| Stock Market Performance | TOT | H4 | + | + | + | + | + | + | + | + | + |

| POT | H4 | − | |||||||||

| MTT | H4 | − | |||||||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Homapour, E.; Su, L.; Caraffini, F.; Chiclana, F. Regression Analysis of Macroeconomic Conditions and Capital Structures of Publicly Listed British Firms. Mathematics 2022, 10, 1119. https://doi.org/10.3390/math10071119

Homapour E, Su L, Caraffini F, Chiclana F. Regression Analysis of Macroeconomic Conditions and Capital Structures of Publicly Listed British Firms. Mathematics. 2022; 10(7):1119. https://doi.org/10.3390/math10071119

Chicago/Turabian StyleHomapour, Elmina, Larry Su, Fabio Caraffini, and Francisco Chiclana. 2022. "Regression Analysis of Macroeconomic Conditions and Capital Structures of Publicly Listed British Firms" Mathematics 10, no. 7: 1119. https://doi.org/10.3390/math10071119