A Credibility Theory-Based Robust Optimization Model to Hedge Price Uncertainty of DSO with Multiple Transactions

Abstract

:1. Introduction

1.1. Literature Review

1.2. Our Contributions

- •

- Based on credibility theory, a risk aversion-based fuzzy chance constraint model is proposed. In the model, the uncertain spot price is designed as a fuzzy variable and its credibility distribution is derived to assess the uncertain risk. The proposed model optimizes the credibility that the expected objective is met, from which decision makers can assess the risk of transaction strategy.

- •

- Multiple transactions, including the spot market, option contract and bilateral contract, are considered to hedge the risk caused by uncertain price, and the impact of different electricity transaction combinations on DSO cost is analyzed while considering power flow constraints.

- •

- A clear equivalence class method with fuzzy chance constraint is used to transform the proposed model into a deterministic robust optimization model. The effectiveness of the model is verified with a modified 15-node network.

1.3. Organization of the Research

2. Problem Formulation

- Axiom 1. for a non-empty set , .

- Axiom 2. whenever .

- Axiom 3. for any event .

- Axiom 4. for any collection of events with .

Credibility Distribution Function Associated with Forecast Error Percentage of Spot Price

3. Multiple Electricity Transaction Model under the Deterministic Spot Price

3.1. Objective Function

3.2. Constraints

4. Robust Optimization Model for DSO Based on Credibility Theory

| Algorithm 1 Solution process |

|

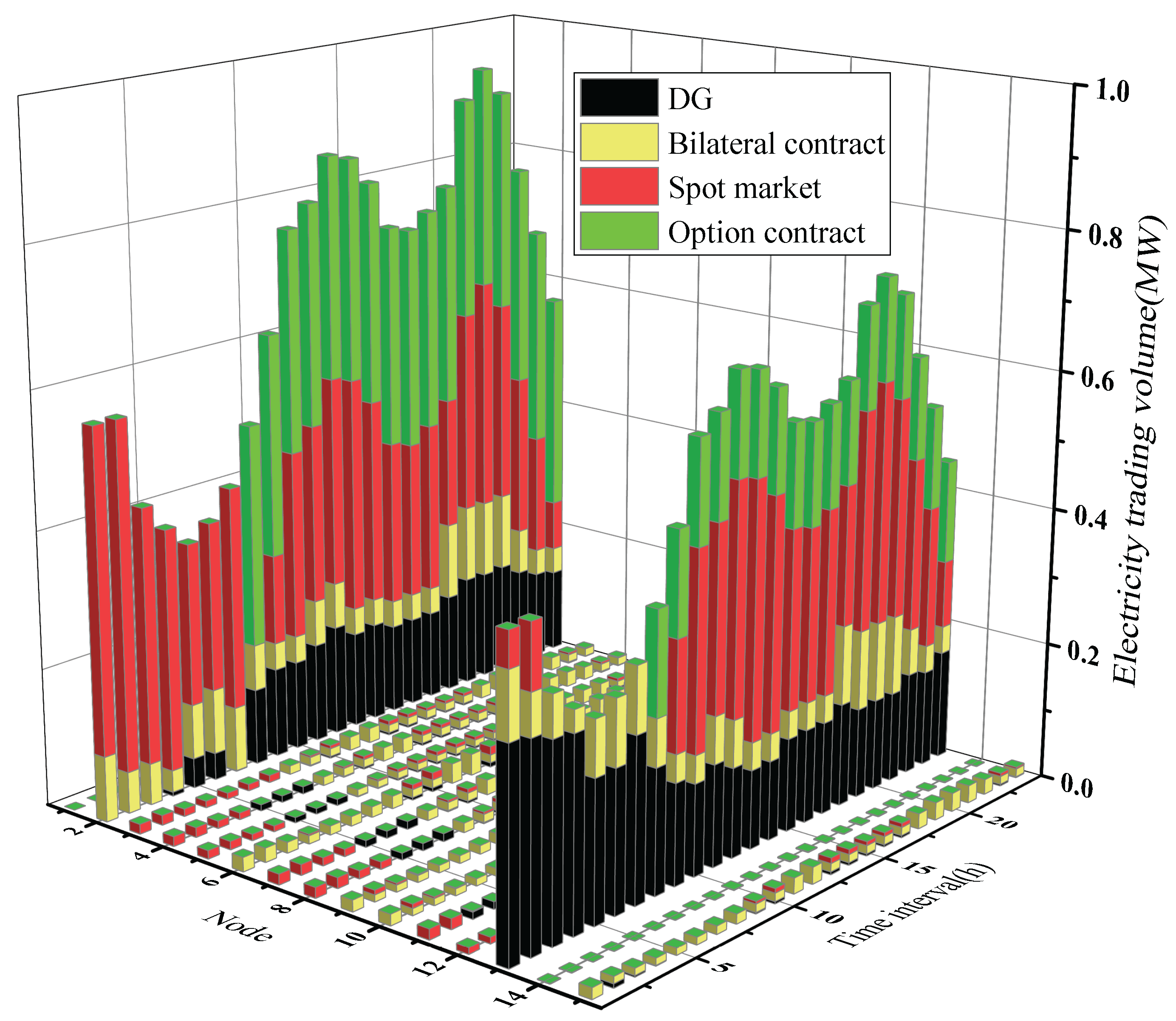

5. Case Analysis

5.1. Comparison of Transaction Cost under Deterministic Spot Electricity Price

5.2. Robust Optimization Model to Hedge Price Uncertainty of DSO with Multiple Transactions

5.3. The Influence of Different Risk Aversion Coefficients of DSO on Electricity Transaction

6. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Nomenclature

| forecast error percentage of spot price | |

| credibility index | |

| actual spot price, USD/MWh | |

| spot market power purchase cost, USD | |

| bilateral contract power purchase cost, USD | |

| option contract power purchase cost, USD | |

| power generation cost, USD | |

| trading volume in the spot market, MW | |

| trading volume of nth bilateral contract, MW | |

| call option contract trading volume, MW | |

| active power output of DG, MW | |

| binary variable | |

| range of network node | |

| range of network line | |

| range of time | |

| forecast spot price, USD/MWh | |

| weighting factor | |

| statistical average of positive and negative error percentages | |

| electricity price with respect to bilateral contract, USD/MWh | |

| strike price and premium of the call option, USD/MWh | |

| power generation cost price of DG, USD/MWh | |

| maximum active power output of DG, MW | |

| active power injected from the power grid, MW | |

| reactive power injected from the power grid, MW | |

| square of the current of line l | |

| upper limit of the apparent power of line l | |

| power outflow end of line l | |

| power inflow end of line l | |

| risk aversion factor | |

| expected cost of DSO, USD | |

| , | resistance and reactance of distribution network |

| , | admittance and conductance of distribution network |

| minimum contract volume of bilateral contract, MW | |

| maximum contract volume of bilateral contract, MW | |

| , | active and reactive power flow |

| active load and reactive load, MW | |

| maximum and minimum values of node voltage |

Appendix A

References

- Johansson, P.; Vendel, M.; Nuur, C. Integrating distributed energy resources in electricity distribution systems: An explorative study of challenges facing DSOs in Sweden. Util. Policy 2020, 67, 101117. [Google Scholar] [CrossRef]

- Tsaousoglou, G.; Giraldo, J.S.; Pinson, P.; Paterakis, N.G. Mechanism design for fair and efficient dso flexibility markets. IEEE Trans. Smart Grid 2021, 12, 2249–2260. [Google Scholar] [CrossRef]

- Villanueva-Rosario, J.A.; Santos-García, F.; Aybar-Mejía, M.E.; Mendoza-Araya, P.; Molina-García, A. Coordinated ancillary services, market participation and communication of multi-microgrids: A review. Appl. Energy 2022, 308, 118332. [Google Scholar] [CrossRef]

- Su, H.; Peng, X.; Liu, H.; Quan, H.; Wu, K.; Chen, Z. Multi-Step-Ahead Electricity Price Forecasting Based on Temporal Graph Convolutional Network. Mathematics 2022, 10, 2366. [Google Scholar] [CrossRef]

- Xiang, D.; Wei, E. A general sensitivity analysis approach for demand response optimizations. IEEE Trans. Netw. Sci. Eng. 2020, 8, 40–52. [Google Scholar] [CrossRef]

- Yang, S.; Tan, Z.; Liu, Z.; Lin, H.; Ju, L.; Zhou, F.; Li, J. A multi-objective stochastic optimization model for electricity retailers with energy storage system considering uncertainty and demand response. J. Clean. Prod. 2020, 277, 124017. [Google Scholar] [CrossRef]

- Zhao, H.; Guo, S. Uncertain interval forecasting for combined electricity-heat-cooling-gas loads in the integrated energy system based on multi-task learning and multi-kernel extreme learning machine. Mathematics 2021, 9, 1645. [Google Scholar] [CrossRef]

- Li, Y.; Ding, Y.; Liu, Y.; Yang, T.; Wang, P.; Wang, J.; Yao, W. Dense Skip Attention based Deep Learning for Day-Ahead Electricity Price Forecasting. IEEE Trans. Power Syst. 2022. [Google Scholar] [CrossRef]

- Shafiee, S.; Zareipour, H.; Knight, A.M. Developing bidding and offering curves of a price-maker energy storage facility based on robust optimization. IEEE Trans. Smart Grid 2017, 10, 650–660. [Google Scholar] [CrossRef]

- Rodriguez, D.E.; Trespalacios, A.; Galeano, D. Risk transfer in an electricity market. Mathematics 2021, 9, 2661. [Google Scholar] [CrossRef]

- Nazari-Heris, M.; Mohammadi-Ivatloo, B.; Gharehpetian, G.B.; Shahidehpour, M. Robust short-term scheduling of integrated heat and power microgrids. IEEE Syst. J. 2018, 13, 3295–3303. [Google Scholar] [CrossRef]

- Gholami, A.; Shekari, T.; Grijalva, S. Proactive management of microgrids for resiliency enhancement: An adaptive robust approach. IEEE Trans. Sustain. Energy 2017, 10, 470–480. [Google Scholar] [CrossRef]

- Najafi, A.; Pourakbari-Kasmaei, M.; Jasinski, M.; Lehtonen, M.; Leonowicz, Z. A max–min–max robust optimization model for multi-carrier energy systems integrated with power to gas storage system. J. Energy Storage 2022, 48, 103933. [Google Scholar] [CrossRef]

- Nojavan, S.; Nourollahi, R.; Pashaei-Didani, H.; Zare, K. Uncertainty-based electricity procurement by retailer using robust optimization approach in the presence of demand response exchange. Int. J. Electr. Power Energy Syst. 2019, 105, 237–248. [Google Scholar] [CrossRef]

- Nojavan, S.; Najafi-Ghalelou, A.; Majidi, M.; Zare, K. Optimal bidding and offering strategies of merchant compressed air energy storage in deregulated electricity market using robust optimization approach. Energy 2018, 142, 250–257. [Google Scholar] [CrossRef]

- Yu, D.; Ebadi, A.G.; Jermsittiparsert, K.; Jabarullah, N.H.; Vasiljeva, M.V.; Nojavan, S. Risk-constrained stochastic optimization of a concentrating solar power plant. IEEE Trans. Sustain. Energy 2019, 11, 1464–1472. [Google Scholar] [CrossRef]

- Shuai, H.; Fang, J.; Ai, X.; Tang, Y.; Wen, J.; He, H. Stochastic optimization of economic dispatch for microgrid based on approximate dynamic programming. IEEE Trans. Smart Grid 2018, 10, 2440–2452. [Google Scholar] [CrossRef] [Green Version]

- Wozabal, D.; Rameseder, G. Optimal bidding of a virtual power plant on the Spanish day-ahead and intraday market for electricity. Eur. J. Oper. Res. 2020, 280, 639–655. [Google Scholar] [CrossRef]

- Charwand, M.; Gitizadeh, M.; Siano, P. A new active portfolio risk management for an electricity retailer based on a drawdown risk preference. Energy 2017, 118, 387–398. [Google Scholar] [CrossRef]

- Wang, K.; Zhu, Z.; Guo, Z. Optimal Day-Ahead Decision-Making Scheduling of Multiple Interruptible Load Schemes for Retailer With Price Uncertainties. IEEE Access 2021, 9, 102251–102263. [Google Scholar] [CrossRef]

- Yu, B.; Guo, L.; Li, Q. A characterization of novel rough fuzzy sets of information systems and their application in decision making. Expert Syst. Appl. 2019, 122, 253–261. [Google Scholar] [CrossRef]

- Si, A.; Das, S.; Kar, S. An approach to rank picture fuzzy numbers for decision making problems. Decis. Making Appl. Manag. Eng. 2019, 2, 54–64. [Google Scholar] [CrossRef]

- Solis, A.R.; Panoutsos, G. Granular computing neural-fuzzy modelling: A neutrosophic approach. Appl. Soft Comput. 2013, 13, 4010–4021. [Google Scholar] [CrossRef] [Green Version]

- Yan, H.; Luh, P.B. A fuzzy optimization-based method for integrated power system scheduling and inter-utility power transaction with uncertainties. IEEE Trans. Power Syst. 1997, 12, 756–763. [Google Scholar]

- Moradi, M.H.; Eskandari, M. A hybrid method for simultaneous optimization of DG capacity and operational strategy in microgrids considering uncertainty in electricity price forecasting. Renew. Energy 2014, 68, 697–714. [Google Scholar] [CrossRef]

- Chen, J.; Qi, B.; Rong, Z.; Peng, K.; Zhao, Y.; Zhang, X. Multi-energy coordinated microgrid scheduling with integrated demand response for flexibility improvement. Energy 2021, 217, 119387. [Google Scholar] [CrossRef]

- Zhao, P.; Gu, C.; Huo, D.; Shen, Y.; Hernando-Gil, I. Two-stage distributionally robust optimization for energy hub systems. IEEE Trans. Ind. Inform. 2019, 16, 3460–3469. [Google Scholar] [CrossRef]

- Zare, A.; Chung, C.; Zhan, J.; Faried, S.O. A distributionally robust chance-constrained MILP model for multistage distribution system planning with uncertain renewables and loads. IEEE Trans. Power Syst. 2018, 33, 5248–5262. [Google Scholar] [CrossRef]

- Lacagnina, V.; Pecorella, A. A stochastic soft constraints fuzzy model for a portfolio selection problem. Fuzzy Sets Syst. 2006, 157, 1317–1327. [Google Scholar] [CrossRef]

- Peng, X.; Tao, X. Cooperative game of electricity retailers in China’s spot electricity market. Energy 2018, 145, 152–170. [Google Scholar] [CrossRef]

- Ghazvini, M.A.F.; Soares, J.; Horta, N.; Neves, R.; Castro, R.; Vale, Z. A multi-objective model for scheduling of short-term incentive-based demand response programs offered by electricity retailers. Appl. Energy 2015, 151, 102–118. [Google Scholar] [CrossRef]

- Li, R.; Wei, W.; Mei, S.; Hu, Q.; Wu, Q. Participation of an energy hub in electricity and heat distribution markets: An MPEC approach. IEEE Trans. Smart Grid 2018, 10, 3641–3653. [Google Scholar] [CrossRef]

- Sun, B.; Wang, F.; Xie, J.; Sun, X. Electricity Retailer trading portfolio optimization considering risk assessment in Chinese electricity market. Electr. Power Syst. Res. 2021, 190, 106833. [Google Scholar] [CrossRef]

- Soroudi, A.; Ehsan, M. IGDT based robust decision making tool for DNOs in load procurement under severe uncertainty. IEEE Trans. Smart Grid 2012, 4, 886–895. [Google Scholar] [CrossRef] [Green Version]

- Golmohamadi, H.; Keypour, R. Stochastic optimization for retailers with distributed wind generation considering demand response. J. Mod. Power Syst. Clean Energy 2018, 6, 733–748. [Google Scholar] [CrossRef] [Green Version]

- Yu, X.; Sun, Y. Trading risk control model of electricity retailers in multi-level power market of China. Energy Sci. Eng. 2019, 7, 2756–2767. [Google Scholar] [CrossRef]

- Zhou, J.; Li, X.; Pedrycz, W. Mean-semi-entropy models of fuzzy portfolio selection. IEEE Trans. Fuzzy Syst. 2016, 24, 1627–1636. [Google Scholar] [CrossRef]

- Gao, J.; Chen, J.; Qi, B.; Zhao, Y.; Peng, K.; Zhang, X. A cost-effective two-stage optimization model for microgrid planning and scheduling with compressed air energy storage and preventive maintenance. Int. J. Electr. Power Energy Syst. 2021, 125, 106547. [Google Scholar] [CrossRef]

- Liu, B. A survey of credibility theory. Fuzzy Optim. Decis. Mak. 2006, 5, 387–408. [Google Scholar] [CrossRef]

- Pinhão, M.; Fonseca, M.; Covas, R. Electricity Spot Price Forecast by Modelling Supply and Demand Curve. Mathematics 2022, 10, 2012. [Google Scholar] [CrossRef]

- Farivar, M.; Low, S.H. Branch flow model: Relaxations and convexification—Part I. IEEE Trans. Power Syst. 2013, 28, 2554–2564. [Google Scholar] [CrossRef]

- Low, S.H. Convex relaxation of optimal power flow—Part II: Exactness. IEEE Trans. Control. Netw. Syst. 2014, 1, 177–189. [Google Scholar] [CrossRef] [Green Version]

- Jahangir, H.; Tayarani, H.; Baghali, S.; Ahmadian, A.; Elkamel, A.; Golkar, M.A.; Castilla, M. A novel electricity price forecasting approach based on dimension reduction strategy and rough artificial neural networks. IEEE Trans. Ind. Inform. 2019, 16, 2369–2381. [Google Scholar] [CrossRef]

- Lu, M. On crisp equivalents and solutions of fuzzy programming with different chance measures. Information-Yamaguchi 2003, 6, 125–134. [Google Scholar]

- Kim, J.; Dvorkin, Y. A P2P-dominant distribution system architecture. IEEE Trans. Power Syst. 2019, 35, 2716–2725. [Google Scholar] [CrossRef] [Green Version]

- Baringo, L.; Conejo, A.J. Offering strategy via robust optimization. IEEE Trans. Power Syst. 2010, 26, 1418–1425. [Google Scholar] [CrossRef]

- Mei, F.; Zhang, J.; Lu, J.; Lu, J.; Jiang, Y.; Gu, J.; Yu, K.; Gan, L. Stochastic optimal operation model for a distributed integrated energy system based on multiple-scenario simulations. Energy 2021, 219, 119629. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Literature | Network Topology Constraint | Deterministic Optimization Model | Risk Asessment Model | Robust Optimization | Stochastic Optimization | Fuzzy Optimization |

|---|---|---|---|---|---|---|

| 11–15 | ✗ | ✗ | ✓ | ✓ | ✗ | ✗ |

| 16–20 | ✗ | ✗ | ✓ | ✗ | ✓ | ✗ |

| 21–26 | ✗ | ✗ | ✓ | ✗ | ✗ | ✓ |

| 30–32 | ✓ | ✓ | ✗ | ✗ | ✗ | ✗ |

| 33–36 | ✗ | ✗ | ✓ | ✗ | ✓ | ✗ |

| The proposed method | ✓ | ✓ | ✓ | ✓ | ✗ | ✓ |

| Contract Number | Period (h) | Min (MW) | Max (MW) | Contract Price (USD/MWh) |

|---|---|---|---|---|

| 1 | Non-peak period | 0.006 | 0.015 | 43.0 |

| 2 | Non-peak period | 0.008 | 0.020 | 42.0 |

| 3 | Non-peak period | 0.010 | 0.025 | 38.0 |

| 4 | Non-peak period | 0.010 | 0.030 | 35.5 |

| 5 | Non-peak period | 0.012 | 0.040 | 33.0 |

| 6 | Peak period | 0.006 | 0.015 | 63.5 |

| 7 | Peak period | 0.008 | 0.020 | 62.0 |

| 8 | Peak period | 0.010 | 0.025 | 59.5 |

| 9 | Peak period | 0.010 | 0.030 | 58.5 |

| 10 | Peak period | 0.012 | 0.040 | 56.0 |

| Nodes | Contract Number | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | |

| 1 | - | - | - | - | - | - | - | - | - | - |

| 2 | 0 | 0 | 0.115 | 0.150 | 0.252 | 0 | 0.184 | 0.230 | 0.250 | 0.428 |

| 3 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0.273 |

| 4 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0.273 |

| 5 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0.207 | 0 |

| 6 | 0 | 0 | 0 | 0 | 0.112 | 0 | 0 | 0 | 0 | 0.347 |

| 7 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0.288 |

| 8 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0.288 |

| 9 | 0 | 0 | 0 | 0.081 | 0 | 0 | 0 | 0 | 0 | 0.301 |

| 10 | 0 | 0 | 0 | 0.080 | 0 | 0 | 0 | 0 | 0 | 0.296 |

| 11 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0.286 |

| 12 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| 13 | 0 | 0 | 0.115 | 0.150 | 0.252 | 0 | 0.184 | 0.230 | 0.250 | 0.428 |

| 14 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| 15 | 0 | 0 | 0 | 0.079 | 0 | 0 | 0 | 0 | 0 | 0.292 |

| Nodes | Contract Number | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | |

| 1 | - | - | - | - | - | - | - | - | - | - |

| 2 | 0.078 | 0.128 | 0.175 | 0.210 | 0.280 | 0.192 | 0.265 | 0.363 | 0.430 | 0.596 |

| 3 | 0 | 0.077 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0.324 |

| 4 | 0 | 0.077 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0.324 |

| 5 | 0.056 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0.273 | 0 |

| 6 | 0 | 0 | 0 | 0 | 0.115 | 0 | 0 | 0 | 0 | 0.440 |

| 7 | 0 | 0.083 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0.349 |

| 8 | 0 | 0.083 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0.343 |

| 9 | 0 | 0 | 0 | 0.093 | 0 | 0 | 0 | 0 | 0 | 0.372 |

| 10 | 0 | 0 | 0 | 0.090 | 0 | 0 | 0 | 0 | 0 | 0.356 |

| 11 | 0 | 0.083 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0.347 |

| 12 | 0.047 | 0 | 0 | 0 | 0 | 0 | 0.197 | 0 | 0 | 0 |

| 13 | 0.078 | 0.128 | 0.175 | 0.210 | 0.280 | 0.192 | 0.268 | 0.350 | 0.430 | 0.596 |

| 14 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 | 0 |

| 15 | 0 | 0 | 0 | 0.088 | 0 | 0 | 0 | 0 | 0 | 0.349 |

| Scenario 1 | Scenario 2 | Scenario 3 | ||||

|---|---|---|---|---|---|---|

| Credibility | Credibility | Credibility | ||||

| 0 | 0 | 0.50 | 0 | 0.50 | 0 | 0.50 |

| 0.05 | 6% | 0.55 | 7% | 0.57 | 10% | 0.61 |

| 0.1 | 11% | 0.65 | 14% | 0.70 | 25% | 0.83 |

| RO | SO | The Proposed Model | |||

|---|---|---|---|---|---|

| - | - | = 0.04 | = 0.05, | = 0.06 | |

| Operation cost | USD 1933.58 | USD 1735.7 | USD 1721.8 | USD 1738.4 | USD 1754.9 |

| Optimization time | 303.3 s | 2310.8 s | 527.5 s | 461.1 s | 694.3 s |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Shao, L.-P.; Chen, J.-J.; Pan, L.-W.; Yang, Z.-J. A Credibility Theory-Based Robust Optimization Model to Hedge Price Uncertainty of DSO with Multiple Transactions. Mathematics 2022, 10, 4420. https://doi.org/10.3390/math10234420

Shao L-P, Chen J-J, Pan L-W, Yang Z-J. A Credibility Theory-Based Robust Optimization Model to Hedge Price Uncertainty of DSO with Multiple Transactions. Mathematics. 2022; 10(23):4420. https://doi.org/10.3390/math10234420

Chicago/Turabian StyleShao, Li-Peng, Jia-Jia Chen, Lu-Wen Pan, and Zi-Juan Yang. 2022. "A Credibility Theory-Based Robust Optimization Model to Hedge Price Uncertainty of DSO with Multiple Transactions" Mathematics 10, no. 23: 4420. https://doi.org/10.3390/math10234420