A Deep Network-Based Trade and Trend Analysis System to Observe Entry and Exit Points in the Forex Market

,

,  , , and

, , and

Abstract

:1. Introduction

- Five variants of LSTM, such as Vanilla-LSTM, Stacked-LSTM, Bidirectional-LSTM, Convolutional Neural Network-LSTM (CNN-LSTM), and Conv-LSTM, are used as trading strategies [16,17,18,19,20,21]. The performance of these five models is recorded with respect to explained variance score (EVS), maximum error (ME), mean squared error (MSE), and R-square (R2) [22];

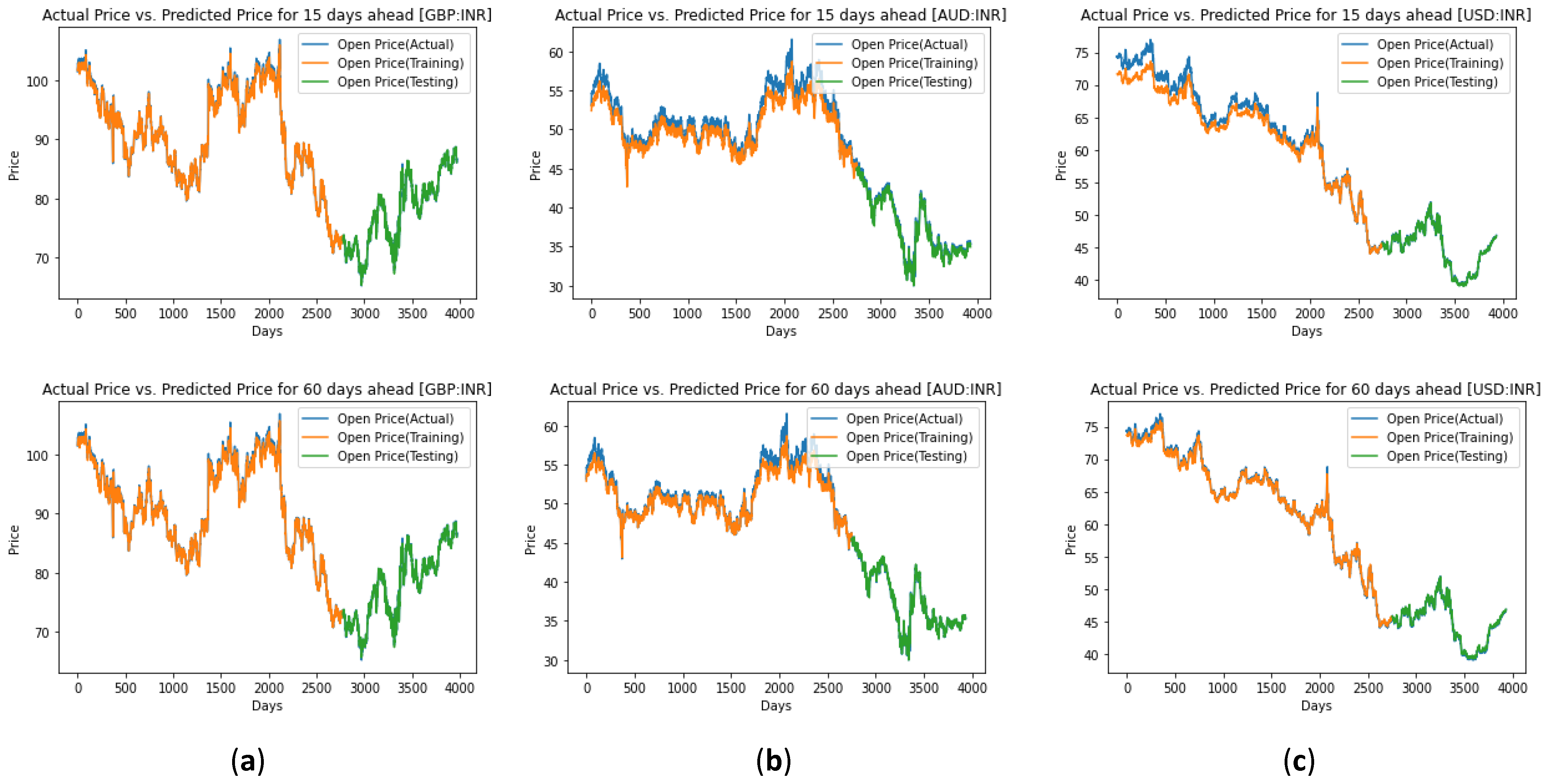

- Prediction curves are plotted to visualize the predictive performance. The best fit models are obtained with respect to the prediction period for all three currency pairs used for experimentation;

- A deep learning-based system for obtaining the trends of the currency pair is proposed based on the selling or buying of currencies, focusing on the previous day and the determinant day (a few days ahead as per user input) to observe the trends for a certain day (date) for both short-term and long-term forecasting horizons;

- A straightforward comparison is made between the proposed trend analysis strategy, actual trends observed on original datasets, and the trends observed based upon those tools;

- In order to handle risks in this financial market, an attempt is made to help investors and traders to identify not only the trends but also the strength of the trends with respect to the average, maximum, and minimum number of units, either up or down, observed during the up trends or down trends and put them in a position to understand the profitable entry and exit points and provide buying or selling opportunities. Finally, the average computational time for all the algorithms used for trading and trend analysis are presented.

2. Literature Survey

3. Preliminaries

3.1. Long-Short-Term-Memory (LSTM) Based Forecasting

3.2. Proposed Trend Analysis Strategy Overview

| Algorithm 1: Proposed Trend Analysis. |

| Input: Number of days = ; Current Day Price = ; Previous Day Price = ; and = Window Size |

| Output: Up trend: UP; Down trend: DOWN; Previous day Magnitude:; Determinant day Magnitude: |

| Process: |

| Let , Where is Day1, is Day2 and is Day ; |

| , Where = current price of Day2, = current price of Day3 and = the current price of day ; |

| , Where = previous day price of Day2, = previous day price of Day3 and = previous day price of ; |

| Where, from to from to from to ; |

| Where, , ; |

| , Where, ; |

| ; |

| ; |

| ; |

| Algorithm 2: Proposed strategy for buying and selling decisions. |

| If Open price of a of previous day |

| then, is observed and |

| else is observed and the asset |

| end if |

| If Open price of a of the determinant day |

| then, is observed and |

| else is observed and the asset |

| end if |

3.3. Trend Analysis Tools and Techniques for Evaluation

3.4. Performance Measures

4. Experimental Setup

4.1. System Configuration

4.2. Datasets Experimented

4.3. Parameters Selection

5. Experimentation, Model Evaluation and Result Analysis

5.1. Model Representation

5.2. LSTM Based Forex Market Prediction

- Step 1.

- Let us define the null () and alternate () hypothesis.

- Step 2.

- Level of significance .

- Step 3.

- Calculate the degrees of freedom (DF).; = number of blocks to be measured.Here, .

- Step 4.

- Obtain the critical chi-square value (critical chi-square value for and is observed from the chi-Square table.

- Step 5.

- State the decision rule, such as ; therefore, the null hypothesis is rejected.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Currency Pairs/Total Rank | Vanilla-LSTM | Stacked-LSTM | Bidirectional-LSTM | CNN-LSTM | Conv-LSTM |

|---|---|---|---|---|---|

| GBP:INR [Short Term] | 0.0001(2) | 0.0009(5) | 0.0001(2) | 0.0008(4) | 0.0001(2) |

| GBP:INR [Long Term] | 0.0001(2) | 0.0001(2) | 0.0001(2) | 0.0007(4) | 0.0009(5) |

| AUD:INR [Short Term] | 0.0001(1) | 0.0009(4.5) | 0.0002(2) | 0.0009(4.5) | 0.0003(3) |

| AUD:INR [Long Term] | 0.0001(1.5) | 0.0004(3) | 0.0007(4) | 0.0009(5) | 0.0001(1.5) |

| USD:INR [Short Term] | 0.0008(4) | 0.0007(3) | 0.0001(1) | 0.0009(5) | 0.0006(2) |

| USD:INR [Long Term] | 0.0008(5) | 0.0007(4) | 0.0001(1.5) | 0.0002(3) | 0.0001(1.5) |

| Total Rank(Tr) | 15.5 | 21.5 | 12.5 | 25.5 | 15 |

| Tr2 | 240.25 | 462.25 | 156.25 | 650.25 | 225 |

5.3. Trend Analysis Strategy and Evaluation

5.4. Average Computational Time

6. Conclusions and Future Scope

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Delgado-Bonal, A.; López, Á.G. Quantifying the randomness of the forex market. Phys. A Stat. Mech. Its Appl. 2021, 569, 125770. [Google Scholar] [CrossRef]

- Kočenda, E.; Moravcová, M. Exchange rate comovements, hedging and volatility spillovers on new EU forex markets. J. Int. Financ. Mark. Inst. Money 2019, 58, 42–64. [Google Scholar] [CrossRef] [Green Version]

- Abounoori, E.; Shahrazi, M.; Rasekhi, S. An investigation of Forex market efficiency based on detrended fluctuation analysis: A case study for Iran. Phys. A Stat. Mech. Its Appl. 2012, 391, 3170–3179. [Google Scholar] [CrossRef]

- Beckmann, J.; Boonman, T.M. Expectations, disagreement and exchange rate pressure. Econ. Lett. 2022, 212, 110205. [Google Scholar] [CrossRef]

- Sarangi, P.K.; Chawla, M.; Ghosh, P.; Singh, S.; Singh, P. FOREX trend analysis using machine learning techniques: INR vs USD currency exchange rate using ANN-GA hybrid approach. Mater. Today Proc. 2022, 49, 3170–3176. [Google Scholar] [CrossRef]

- Talebi, H.; Hoang, W.; Gavrilova, M.L. Multi-scale Foreign Exchange Rates Ensemble for Classification of Trends in Forex Market. Procedia Comput. Sci. 2014, 29, 2065–2075. [Google Scholar] [CrossRef] [Green Version]

- Kaltwasser, P.R. Uncertainty about fundamentals and herding behavior in the FOREX market. Phys. A Stat. Mech. Its Appl. 2010, 389, 1215–1222. [Google Scholar] [CrossRef]

- Wen, T.; Wang, G.-J. Volatility connectedness in global foreign exchange markets. J. Multinatl. Financ. Manag. 2020, 54, 100617. [Google Scholar] [CrossRef]

- Neely, C.; Weller, P.A. Lessons from the evolution of foreign exchange trading strategies. J. Bank. Financ. 2013, 37, 3783–3798. [Google Scholar] [CrossRef] [Green Version]

- Ni, L.; Li, Y.; Wang, X.; Zhang, J.; Yu, J.; Qi, C. Forecasting of Forex Time Series Data Based on Deep Learning. Procedia Comput. Sci. 2019, 147, 647–652. [Google Scholar] [CrossRef]

- Gonçalves, R.; Ribeiro, V.M.; Pereira, F.L.; Rocha, A.P. Deep learning in exchange markets. Inf. Econ. Policy 2019, 47, 38–51. [Google Scholar] [CrossRef]

- Sengupta, S.; Basak, S.; Saikia, P.; Paul, S.; Tsalavoutis, V.; Atiah, F.; Ravi, V.; Peters, A. A review of deep learning with special emphasis on architectures, applications and recent trends. Knowl.-Based Syst. 2020, 194, 105596. [Google Scholar] [CrossRef] [Green Version]

- Ozbayoglu, A.M.; Gudelek, M.U.; Sezer, O.B. Deep learning for financial applications: A survey. Appl. Soft Comput. 2020, 93, 106384. [Google Scholar] [CrossRef]

- Yang, S. A novel study on deep learning framework to predict and analyze the financial time series information. Future Gener. Comput. Syst. 2021, 125, 812–819. [Google Scholar] [CrossRef]

- Sezer, O.B.; Gudelek, M.U.; Ozbayoglu, A.M. Financial time series forecasting with deep learning: A systematic literature review: 2005–2019. Appl. Soft Comput. 2020, 90, 106181. [Google Scholar] [CrossRef] [Green Version]

- Ahmed, S.; Hassan, S.-U.; Aljohani, N.R.; Nawaz, R. FLF-LSTM: A novel prediction system using Forex Loss Function. Appl. Soft Comput. 2020, 97, 106780. [Google Scholar] [CrossRef]

- Shen, M.-L.; Lee, C.-F.; Liu, H.-H.; Chang, P.-Y.; Yang, C.-H. Effective multinational trade forecasting using LSTM recurrent neural network. Expert Syst. Appl. 2021, 182, 115199. [Google Scholar] [CrossRef]

- Park, S.; Yang, J.-S. Interpretable deep learning LSTM model for intelligent economic decision-making. Knowl.-Based Syst. 2022, 248, 108907. [Google Scholar] [CrossRef]

- U, J.; Lu, P.; Kim, C.; Ryu, U.; Pak, K. A new LSTM based reversal point prediction method using upward/downward reversal point feature sets. Chaos Solitons Fractals 2020, 132, 109559. [Google Scholar] [CrossRef]

- Ji, L.; Zou, Y.; He, K.; Zhu, B. Carbon futures price forecasting based with ARIMA-CNN-LSTM model. Procedia Comput. Sci. 2019, 162, 33–38. [Google Scholar] [CrossRef]

- Lee, S.W.; Kim, H.Y. Stock market forecasting with super-high dimensional time-series data using ConvLSTM, trend sampling, and specialized data augmentation. Expert Syst. Appl. 2020, 161, 113704. [Google Scholar] [CrossRef]

- Raghav, A. Know The Best Evaluation Metrics for Your Regression Model! Published on 19 May 2021 and Last Modified on 21 July 2022. 2021. Available online: https://www.analyticsvidhya.com/blog/2021/05/know-the-best-evaluation-metrics-for-your-regression-model/ (accessed on 16 August 2022).

- Friedman Test/Two-way Analysis of Variance by Ranks. Available online: https://www.statisticshowto.com/friedmans-test/ (accessed on 17 August 2022).

- Upper Critical Values for the Friedman Test. Available online: https://www.york.ac.uk/depts/maths/tables/friedman.pdf (accessed on 16 August 2022).

- Vajda, V. Could a Trader Using Only “Old” Technical Indicator be Successful at the Forex Market? Procedia Econ. Financ. 2014, 15, 318–325. [Google Scholar] [CrossRef] [Green Version]

- Ozturk, M.; Toroslu, I.H.; Fidan, G. Heuristic based trading system on Forex data using technical indicator rules. Appl. Soft Comput. 2016, 43, 170–186. [Google Scholar] [CrossRef]

- Alonso-Monsalve, S.; Suárez-Cetrulo, A.L.; Cervantes, A.; Quintana, D. Convolution on neural networks for high-frequency trend prediction of cryptocurrency exchange rates using technical indicators. Expert Syst. Appl. 2020, 149, 113250. [Google Scholar] [CrossRef]

- Sun, S.; Wang, S.; Wei, Y. A new ensemble deep learning approach for exchange rates forecasting and trading. Adv. Eng. Inform. 2020, 46, 101160. [Google Scholar] [CrossRef]

- Islam, M.S.; Hossain, E. Foreign exchange currency rate prediction using a GRU-LSTM hybrid network. Soft Comput. Lett. 2021, 3, 100009. [Google Scholar] [CrossRef]

- Wang, G.; Tao, T.; Ma, J.; Li, H.; Fu, H.; Chu, Y. An improved ensemble learning method for exchange rate forecasting based on complementary effect of shallow and deep features. Expert Syst. Appl. 2021, 184, 115569. [Google Scholar] [CrossRef]

- Lin, Y.; Wang, R.; Gong, X.; Jia, G. Cross-correlation and forecast impact of public attention on USD/CNY exchange rate: Evidence from Baidu Index. Phys. A Stat. Mech. Its Appl. 2022, 604, 127686. [Google Scholar] [CrossRef]

- Patel, M.M.; Tanwar, S.; Gupta, R.; Kumar, N. A Deep Learning-based Cryptocurrency Price Prediction Scheme for Financial Institutions. J. Inf. Secur. Appl. 2020, 55, 102583. [Google Scholar] [CrossRef]

- Tokár, T.; Horváth, D. Market inefficiency identified by both single and multiple currency trends. Phys. A Stat. Mech. Its Appl. 2012, 391, 5620–5627. [Google Scholar] [CrossRef]

- Lee, Y.; Ow, L.T.C.; Ling, D.N.C. Hidden Markov Models for Forex Trends Prediction. In Proceedings of the 2014 International Conference on Information Science & Applications (ICISA), Seoul, Korea, 6–9 May 2014; pp. 1–4. [Google Scholar]

- Lahmiri, S. Long memory in international financial markets trends and short movements during 2008 financial crisis based on variational mode decomposition and detrended fluctuation analysis. Phys. A Stat. Mech. Its Appl. 2015, 437, 130–138. [Google Scholar] [CrossRef]

- Sandoval, J.; Nino, J.; Hernandez, G.; Cruz, A. Detecting Informative Patterns in Financial Market Trends based on Visual Analysis. Procedia Comput. Sci. 2016, 80, 752–761. [Google Scholar] [CrossRef] [Green Version]

- Bartoš, E.; Pinčák, R. Identification of market trends with string and D2-brane maps. Phys. A Stat. Mech. Its Appl. 2017, 479, 57–70. [Google Scholar] [CrossRef] [Green Version]

- Adegboye, A.; Kampouridis, M.; Johnson, C.G. Regression genetic programming for estimating trend end in foreign exchange market. In Proceedings of the 2017 IEEE Symposium Series on Computational Intelligence (SSCI), Honolulu, HI, USA, 27 November–1 December 2017; pp. 1–8. [Google Scholar]

- Palsma, J.; Adegboye, A. Optimising Directional Changes trading strategies with different algorithms. In Proceedings of the 2019 IEEE Congress on Evolutionary Computation (CEC), Wellington, New Zealand, 10–13 June 2019; pp. 3333–3340. [Google Scholar]

- Adegboye, A.; Kampouridis, M. Machine learning classification and regression models for predicting directional changes trend reversal in FX markets. Expert Syst. Appl. 2021, 173, 114645. [Google Scholar] [CrossRef]

- Sadeghi, A.; Daneshvar, A.; Zaj, M.M. Combined ensemble multi-class SVM and fuzzy NSGA-II for trend forecasting and trading in Forex markets. Expert Syst. Appl. 2021, 185, 115566. [Google Scholar] [CrossRef]

- Fiorucci, J.A.; Silva, G.N.; Barboza, F. Reaction trend system with GARCH quantiles as action points. Expert Syst. Appl. 2022, 198, 116750. [Google Scholar] [CrossRef]

- Zhi, B.; Wang, X.; Xu, F. Managing inventory financing in a volatile market: A novel data-driven copula model. Transp. Res. Part E Logist. Transp. Rev. 2022, 165, 102854. [Google Scholar] [CrossRef]

- Zhuang, X.; Wei, D. Asymmetric multifractality, comparative efficiency analysis of green finance markets: A dynamic study by index-based model. Phys. A Stat. Mech. Its Appl. 2022, 604, 127949. [Google Scholar] [CrossRef]

- Xu, C.; Liu, Z.; Liao, M.; Yao, L. Theoretical analysis and computer simulations of a fractional order bank data model incorporating two unequal time delays. Expert Syst. Appl. 2022, 199, 116859. [Google Scholar] [CrossRef]

- Fuentes, R.; Cantillo, V.; López-Ospina, H. A road pricing model involving social costs and infrastructure financing policies. Appl. Math. Model. 2022, 105, 729–750. [Google Scholar] [CrossRef]

- Samanta, S.R.; Mallick, P.K.; Pattnaik, P.K.; Mohanty, J.R.; Polkowski, Z. (Eds.) Cognitive Computing for Risk Management; Springer: Berlin/Heidelberg, Germany, 2022. [Google Scholar]

- Mukherjee, A.; Singh, A.K.; Mallick, P.K.; Samanta, S.R. Portfolio Optimization for US-Based Equity Instruments Using Monte-Carlo Simulation. In Cognitive Informatics and Soft Computing; Lecture Notes in Networks and Systems; Mallick, P.K., Bhoi, A.K., Barsocchi, P., de Albuquerque, V.H.C., Eds.; Springer: Singapore, 2022; Volume 375. [Google Scholar] [CrossRef]

- GBP to INR-British Pound Rupee. Available online: https://in.investing.com/currencies/gbp-inr-historical-data (accessed on 10 January 2022).

- AUD to INR-British Pound Rupee. Available online: https://in.investing.com/currencies/aud-inr-historical-data (accessed on 10 January 2022).

- USD to INR-British Pound Rupee. Available online: https://in.investing.com/currencies/usd-inr-historical-data (accessed on 10 January 2022).

| Days (D) | Determinant Day Magnitude | Window Number and Trend Calculation | Analysis | |

|---|---|---|---|---|

| 0 | 0 | with respect to Previous Day = −45/4 = −10.25 with respect to Determinant day = Analysis cannot be carried out as there is no information about previous determinant days | Considering the previous day of the condition, the trend observed is DOWN with 10.25 units. | |

| −18 | 0 | |||

| −12 | 0 | |||

| −15 | 0 | |||

| −5 | −50 | with respect to Previous Day = +16/4 = +4 with respect to Determinant day = −74/4 = −18.5 | Considering previous day of the condition, the trend observed is UP with 4 units, and for the determinant day it is DOWN by 18.5 units. This signifies that it has a short-term rise of 3.5 units and a long-term fall of 18.5 units. | |

| 0 | −32 | |||

| +12 | −8 | |||

| +9 | +16 | |||

| 0 | −32 | with respect to Previous Day = +333/4 = +8 with respect to Determinant day = +8/4 = +2 | Considering the previous day of the condition, the trend observed is UP with 8 units, and for the determinant day, it is UP by 2 units. This signifies that it has a short-term rise of 7.5 units and a long-term rise of 2 units per step. | |

| +12 | −8 | |||

| +9 | +16 | |||

| +11 | +32 | |||

| +12 | −8 | with respect to Previous Day = +21/4 = +5.25 with respect to Determinant day = + 61/4 = +15.25 | Considering the previous day of the condition, the trend observed is UP with 5.25 units, and for the determinant day, it is UP by 15.25 units. This signifies that it has a short-term rise of 4.75 units and a long-term rise of 15.25 units per step. | |

| +9 | +16 | |||

| +11 | +32 | |||

| −11 | +21 | |||

| +9 | +16 | with respect to Previous Day = −2/4 = −0.05 with respect to Determinant day = + 67/4 = +17.25 | Considering the previous day of the condition, the trend observed is DOWN with 0.05 units, and for the determinant day, it is UP by 17.25 units. This signifies that it has a short-term fall of 0.05 units and a long-term rise of 17.25 units per step. | |

| +11 | +32 | |||

| −11 | +21 | |||

| −11 | −2 | |||

| +11 | +32 | with respect to Previous Day = −21/4 = −5.25 with respect to Determinant day = +30/4 = +7.5 | Considering the previous day of the condition, the trend observed is DOWN with −5.25 units, and for the determinant day, it is UP by 7.5 units. This signifies that it has a short-term fall of 5.25 units and a long-term rise of 7.5 units per step. | |

| −11 | +21 | |||

| −11 | −2 | |||

| −10 | −21 |

| Indicators | Formula | Range of Values | Discussion |

|---|---|---|---|

| ADX | where MA is the moving average, and DI is are the positive and negative directional movements representing the difference between today’s and yesterday’s highest price and the difference between today’s and yesterday’s lowest price, respectively. | 0 to 100 | It helps to identify the strongest trends and distinguishes between trending and non-trending situations. ADX > 25 signifies trend strength while ADX < 25 represents a weak trend. |

| ROC | where, is the price at the current time, and is the price at the previous time, proving a value as a percentage. | 0 to 100 | When ROC is above the zero line, it signifies the uptrend is accelerating, and when it is below the zero line, it represents the uptrend slowing down and trending towards a down trend. |

| Momentum | , where is the latest price and is closing price, and is the number of days ago. | + or − | This is computed by continually taking the price difference for a fixed timeframe. For example, to construct a 10-day momentum line, the closing price of 10 days ago is subtracted from the last closing price, and these positive and negative values are then plotted around a zero line to observe the trends. Above the zero line represents up trends, below the zero line represents down trends, and the value on the zero line represents a stable condition. |

| CCI | where TP is the typical price and is computed as 0.015 is a constant, and SMA is a simple moving average. The mean deviation is calculated by subtracting the 20-period average typical prices from each period’s typical price. | <−100 to >+100 | Generally, this CCI value fluctuates above and below 0. The CCI is relatively high when prices are far above their average and low when the prices are far below their average. CCI > +100 shows the buy signal, and CCI < −100 shows the sell signal. In another way, it represents up trends and down trends, respectively. |

| MACD | where EMA is an exponential moving average. | + or − | When MACD crosses above the zero line, the decision is taken to buy and when below the zero line, it signals to sell. Similar to CCI, it also represents up trends and down trends, respectively. |

| Currency | Training Set | Testing Set | Features |

|---|---|---|---|

| GBP:INR | 2775 | 1189 | Open, Low, High, and Close Price |

| AUD:INR | 2751 | 1179 | |

| USD:INR | 2751 | 1178 |

| Networks/Models | Parameters and Values |

|---|---|

| CNN-LSTM | Conv1D = filters = 64; kernel_size = 1; activation = ‘relu’ |

| MaxPooling1D = pool_size = 2 | |

| Conv-LSTM | Filters = 64; kernel_size = (1,2); activation = ‘relu’ |

| Currency Pairs/Prediction Horizon | Performance Measures | Training Phase | Testing Phase | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Vanilla-LSTM | Stacked-LSTM | Bidirectional-LSTM | CNN-LSTM | Conv-LSTM | Vanilla-LSTM | Stacked-LSTM | Bidirectional-LSTM | CNN-LSTM | Conv-LSTM | ||

| GBP:INR/Short term | MSE | 0.0002 | 0.0001 | 0.0001 | 0.0005 | 0.0007 | 0.0001 | 0.0009 | 0.0001 | 0.0008 | 0.0001 |

| R2 | 0.9928 | 0.9950 | 0.9955 | 0.9986 | 0.9979 | 0.9994 | 0.9995 | 0.9994 | 0.9996 | 0.9993 | |

| EVS | 0.9958 | 0.9965 | 0.9977 | 0.9989 | 0.9993 | 0.9995 | 0.9995 | 0.9996 | 0.9996 | 0.9995 | |

| ME | 0.0585 | 0.0441 | 0.0434 | 0.0371 | 0.0416 | 0.0235 | 0.0213 | 0.0227 | 0.0210 | 0.0227 | |

| GBP:INR/Long term | MSE | 0.0004 | 0.0009 | 0.0002 | 0.0006 | 0.0001 | 0.0001 | 0.0001 | 0.0001 | 0.0007 | 0.0009 |

| R2 | 0.9892 | 0.9975 | 0.9924 | 0.9985 | 0.9959 | 0.9990 | 0.9992 | 0.9992 | 0.9996 | 0.9994 | |

| EVS | 0.9942 | 0.9994 | 0.9961 | 0.9992 | 0.9973 | 0.9990 | 0.9993 | 0.9994 | 0.9996 | 0.9995 | |

| ME | 0.0897 | 0.0256 | 0.0583 | 0.0333 | 0.0453 | 0.0377 | 0.0223 | 0.0245 | 0.0223 | 0.0217 | |

| AUD:INR/Short term | MSE | 0.0007 | 0.0005 | 0.0007 | 0.0017 | 0.0001 | 0.0001 | 0.0009 | 0.0002 | 0.0009 | 0.0003 |

| R2 | 0.9340 | 0.9506 | 0.9411 | 0.8571 | 0.9897 | 0.9987 | 0.9993 | 0.9984 | 0.9935 | 0.9978 | |

| EVS | 0.9769 | 0.9818 | 0.9828 | 0.9753 | 0.9992 | 0.9990 | 0.9993 | 0.9993 | 0.9992 | 0.9988 | |

| ME | 0.0918 | 0.0810 | 0.0778 | 0.0999 | 0.0347 | 0.0490 | 0.0422 | 0.0390 | 0.0347 | 0.0485 | |

| AUD:INR/Long term | MSE | 0.0010 | 0.0032 | 0.0009 | 0.0007 | 0.0003 | 0.0001 | 0.0004 | 0.0007 | 0.0009 | 0.0001 |

| R2 | 0.9142 | 0.7251 | 0.9179 | 0.9381 | 0.9699 | 0.9989 | 0.9974 | 0.9949 | 0.9993 | 0.9992 | |

| EVS | 0.9594 | 0.9219 | 0.9886 | 0.9727 | 0.9898 | 0.9989 | 0.9984 | 0.9986 | 0.9994 | 0.9993 | |

| ME | 0.1141 | 0.1709 | 0.0737 | 0.0916 | 0.0545 | 0.0394 | 0.0440 | 0.0370 | 0.0408 | 0.0429 | |

| USD:INR/Short term | MSE | 0.0001 | 0.0001 | 0.0001 | 0.0014 | 0.0002 | 0.0008 | 0.0007 | 0.0001 | 0.0009 | 0.0006 |

| R2 | 0.9970 | 0.9966 | 0.9958 | 0.9684 | 0.9953 | 0.9989 | 0.9990 | 0.9982 | 0.9987 | 0.9991 | |

| EVS | 0.9993 | 0.9985 | 0.9974 | 0.9883 | 0.9985 | 0.9989 | 0.9990 | 0.9990 | 0.9987 | 0.9991 | |

| ME | 0.0389 | 0.0578 | 0.0556 | 0.0973 | 0.0623 | 0.0157 | 0.0156 | 0.0180 | 0.0173 | 0.0183 | |

| USD:INR/Long term | MSE | 0.0050 | 0.0011 | 0.0003 | 0.0007 | 0.0017 | 0.0008 | 0.0007 | 0.0001 | 0.0002 | 0.0001 |

| R2 | 0.8902 | 0.9760 | 0.9992 | 0.9984 | 0.9624 | 0.9987 | 0.9990 | 0.9991 | 0.9973 | 0.9985 | |

| EVS | 0.9578 | 0.9930 | 0.9995 | 0.9988 | 0.9858 | 0.9991 | 0.9990 | 0.9991 | 0.9987 | 0.9987 | |

| ME | 0.1640 | 0.0869 | 0.0421 | 0.0527 | 0.1063 | 0.0170 | 0.0181 | 0.0169 | 0.0185 | 0.0167 | |

| Tools and Methods Compared with | No. of Trends | GBP:INR | AUD:INR | USD:INR |

|---|---|---|---|---|

| Actual Trends Observed on original datasets | Up Trends | 1440 | 1425 | 1504 |

| Down Trends | 1485 | 1500 | 1421 | |

| Proposed Trend Analysis Approach [Previous day] | Up Trends [Short-term] | 1376 | 1429 | 1387 |

| Up Trends [Long-term] | 1445 | 1432 | 1510 | |

| Down Trends [Short-term] | 1549 | 1496 | 1538 | |

| Down Trends [Long-term] | 1480 | 1493 | 1415 | |

| Proposed Trend Analysis Approach [Determinant day] | Up Trends [Short-term] | 1364 | 1400 | 1350 |

| Up Trends [Long-term] | 1560 | 1522 | 1562 | |

| Down Trends [Short-term] | 1561 | 1525 | 1575 | |

| Down Trends [Long-term] | 1365 | 1403 | 1363 | |

| ADX | Up Trends | 2451 | 2018 | 1789 |

| Down Trends | 474 | 907 | 1136 | |

| ROC | Up Trends | 1563 | 1521 | 1576 |

| Down Trends | 1362 | 1404 | 1349 | |

| Momentum | Up Trends | 1512 | 1441 | 1589 |

| Down Trends | 1413 | 1484 | 1336 | |

| CCI | Up Trends | 1550 | 1508 | 1544 |

| Down Trends | 1375 | 1417 | 1381 | |

| MACD | Up Trends | 827 | 1760 | 761 |

| Down Trends | 2098 | 1165 | 2164 |

| Tools and Methods Compared with | Prediction Timeframe | GBP:INR | AUD:INR | USD:INR |

|---|---|---|---|---|

| Proposed Trend Analysis Approach [Previous day] | Short-term | 95.624 | 99.7265 | 92.00 |

| Long-term | 99.6582 | 99.5214 | 99.5898 | |

| Proposed Trend Analysis Approach [Determinant day] | Short-term | 94.8035 | 98.2906 | 89.4701 |

| Long-term | 91.7849 | 93.3676 | 96.0342 | |

| ADX | 30.8718 | 59.453 | 80.5729 | |

| ROC | 91.5898 | 93.4359 | 95.0770 | |

| Momentum | 95.077 | 98.7693 | 94.1881 | |

| CCI | 92.4787 | 94.3282 | 97.2650 | |

| MACD | 58.0855 | 77.0941 | 49.1966 | |

| Tools and Methods Compared with | Prediction Timeframe | Trends | GBP:INR | AUD:INR | USD:INR |

|---|---|---|---|---|---|

| Proposed Trend Analysis Approach [Previous day] | Short-term | Ups | 0.1014 | 0.0555 | 0.0440 |

| Downs | 0.1105 | 0.0645 | 0.0587 | ||

| Long-term | Ups | 0.1992 | 0.1228 | 0.0898 | |

| Downs | 0.4152 | 0.2486 | 0.2068 | ||

| Proposed Trend Analysis Approach [Determinant day] | Short-term | Ups | 0.8385 | 0.4796 | 0.3816 |

| Downs | 0.8878 | 0.5043 | 0.4513 | ||

| Long-term | Ups | 1.5859 | 0.9155 | 0.8222 | |

| Downs | 1.4881 | 0.8239 | 0.6552 | ||

| ADX | Ups | 4.3620 | 5.3328 | 0.6627 | |

| Downs | 18.7422 | 11.9767 | 0.3795 | ||

| ROC | Ups | 1.5664 | 1.6097 | 1.1352 | |

| Downs | 1.4541 | 1.4365 | 0.9228 | ||

| Momentum | Ups | 1.3764 | 0.7981 | 0.6813 | |

| Downs | 1.3237 | 0.7432 | 0.5702 | ||

| CCI | Ups | 94.2892 | 24.4864 | 94.1963 | |

| Downs | 92.0334 | 25.5105 | 87.6374 | ||

| MACD | Ups | 2.1568 | 1.3842 | 1.2850 | |

| Downs | 1.6636 | 1.1362 | 0.9951 | ||

| Tools and Methods Compared with | Prediction Timeframe | Trends | GBP:INR | AUD:INR | USD:INR |

|---|---|---|---|---|---|

| Proposed Trend Analysis Approach [Previous day] | Short-term | Ups | 0.8578 | 0.3569 | 0.3613 |

| Downs | 0.6667 | 0.1333 | 6.6667 | ||

| Long-term | Ups | 7.2380 | 2.0790 | 2.2500 | |

| Downs | 0.001 | 0.001 | 0.001 | ||

| Proposed Trend Analysis Approach [Determinant day] | Short-term | Ups | 10.108 | 3.4542 | 3.577 |

| Downs | 0.4 | 0.4666 | 3.5487 | ||

| Long-term | Ups | 12.47 | 6.222 | 8.074 | |

| Downs | 0.001 | 0.002 | 0.003 | ||

| ADX | Ups | 72.8872 | 40.9258 | 2.8636 | |

| Downs | 0.0086 | 0.0086 | 0.0005 | ||

| ROC | Ups | 10.4259 | 10.7953 | 9.8713 | |

| Downs | 0.0019 | 0.0074 | 0.0016 | ||

| Momentum | Ups | 8.9080 | 4.4320 | 6.0110 | |

| Downs | 0.002 | 0.004 | 0.001 | ||

| CCI | Ups | 314.0978 | 127.3759 | 327.078 | |

| Downs | 0.1324 | 0.0397 | 0.0647 | ||

| MACD | Ups | 4.0845 | 3.3507 | 4.4197 | |

| Downs | 0.0001 | 0.0008 | 0.0016 | ||

| Tools and Methods Compared with | Prediction Timeframe | Trends | GBP:INR | AUD:INR | USD:INR |

|---|---|---|---|---|---|

| Proposed Trend Analysis Approach [Previous day] | Short-term | Ups | 0.6667 | 0 | 0 |

| Downs | 0.8021 | 0.4284 | 0.5063 | ||

| Long-term | Ups | 0 | 0 | 0 | |

| Downs | 0 | 0 | 0 | ||

| Proposed Trend Analysis Approach [Determinant day] | Short-term | Ups | 0.0004 | 0.0002 | 0.3333 |

| Downs | 5.9571 | 2.7547 | 2.4950 | ||

| Long-term | Ups | 0 | 0 | 0 | |

| Downs | 13.176 | 5.006 | 5.43 | ||

| ADX | Ups | 0.0407 | 0.0007 | 0.0002 | |

| Downs | 6.1925 | 2.9710 | 1.9347 | ||

| ROC | Ups | 0 | 0.0018 | 0 | |

| Downs | 12.8535 | 14.5346 | 7.7303 | ||

| Momentum | Ups | 0 | 0.001 | 0 | |

| Downs | 12.741 | 6.982 | 5.165 | ||

| CCI | Ups | 0.3048 | 0 | 0.2554 | |

| Downs | 310.2466 | 178.3489 | 349.7084 | ||

| MACD | Ups | 0.0096 | 0.0004 | 0.003 | |

| Downs | 3.3272 | 4.3739 | 1.9886 | ||

| Forecasting Models/Execution Time | Vanilla-LSTM | Stacked-LSTM | Bidirectional-LSTM | CNN-LSTM | Covn-LSTM |

|---|---|---|---|---|---|

| 125.06812 | 161.3049 | 161.9708 | 171.1201 | 169.0091 |

| Trend Analysis | Proposed Trend Analysis Approach | ADX | ROC | Momentum | CCI | MACD |

|---|---|---|---|---|---|---|

| 0.272612 | 0.15505 | 0.0037 | 0.0018 | 0.00174 | 0.0017 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Das, A.K.; Mishra, D.; Das, K.; Mohanty, A.K.; Mohammed, M.A.; Al-Waisy, A.S.; Kadry, S.; Kim, J. A Deep Network-Based Trade and Trend Analysis System to Observe Entry and Exit Points in the Forex Market. Mathematics 2022, 10, 3632. https://doi.org/10.3390/math10193632

Das AK, Mishra D, Das K, Mohanty AK, Mohammed MA, Al-Waisy AS, Kadry S, Kim J. A Deep Network-Based Trade and Trend Analysis System to Observe Entry and Exit Points in the Forex Market. Mathematics. 2022; 10(19):3632. https://doi.org/10.3390/math10193632

Chicago/Turabian StyleDas, Asit Kumar, Debahuti Mishra, Kaberi Das, Arup Kumar Mohanty, Mazin Abed Mohammed, Alaa S. Al-Waisy, Seifedine Kadry, and Jungeun Kim. 2022. "A Deep Network-Based Trade and Trend Analysis System to Observe Entry and Exit Points in the Forex Market" Mathematics 10, no. 19: 3632. https://doi.org/10.3390/math10193632