Optimal Purchasing Decisions with Supplier Default in Portfolio Procurement

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

2. Problem Context

3. Theoretical Model Construction

4. Optimal Decision in Portfolio Procurement under Supplier Default

4.1. Portfolio Procurement Decision without Considering Supplier Default

4.2. Portfolio Procurement Decision Considering Supplier Default

5. Numerical Simulation and Discussion

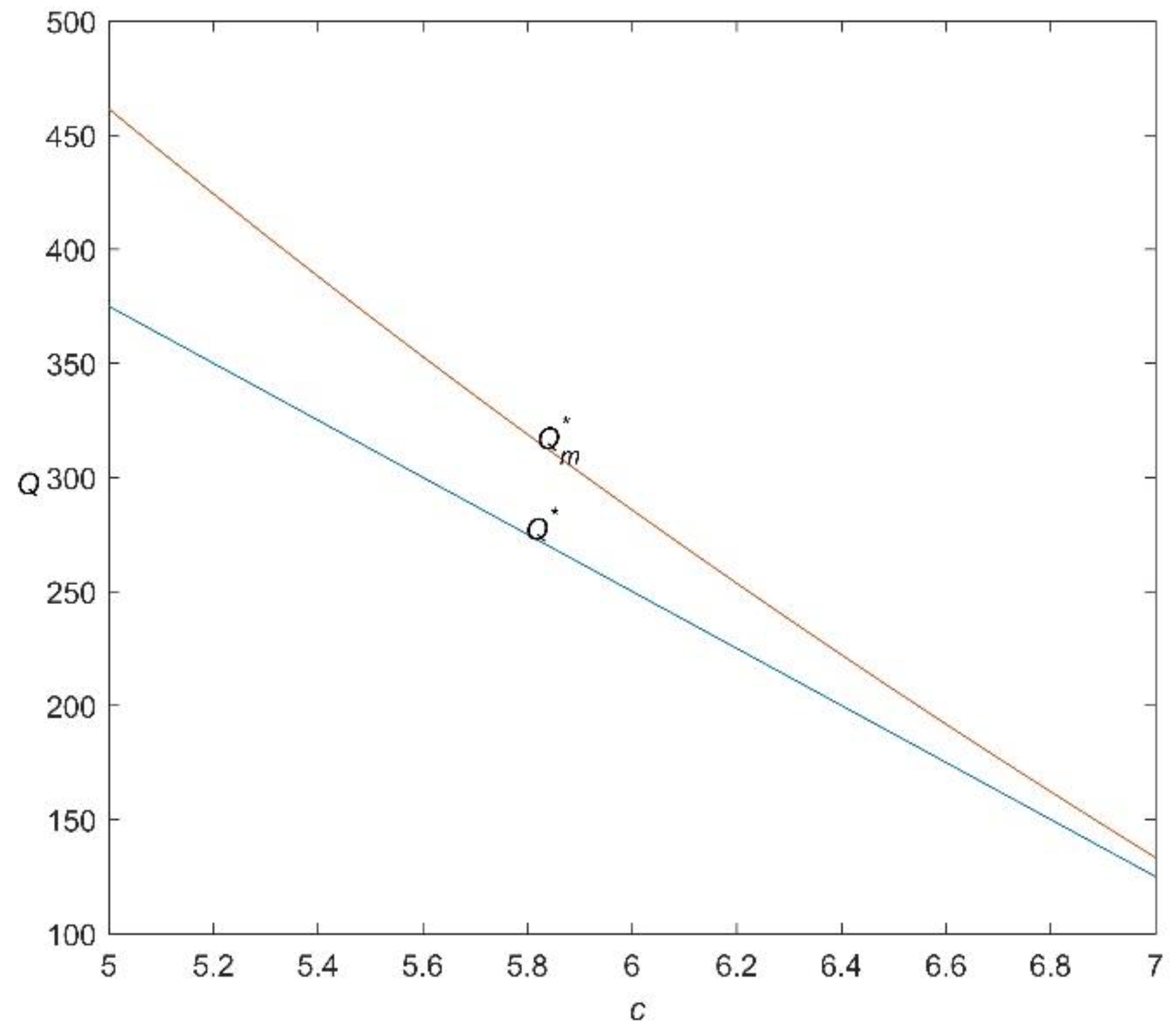

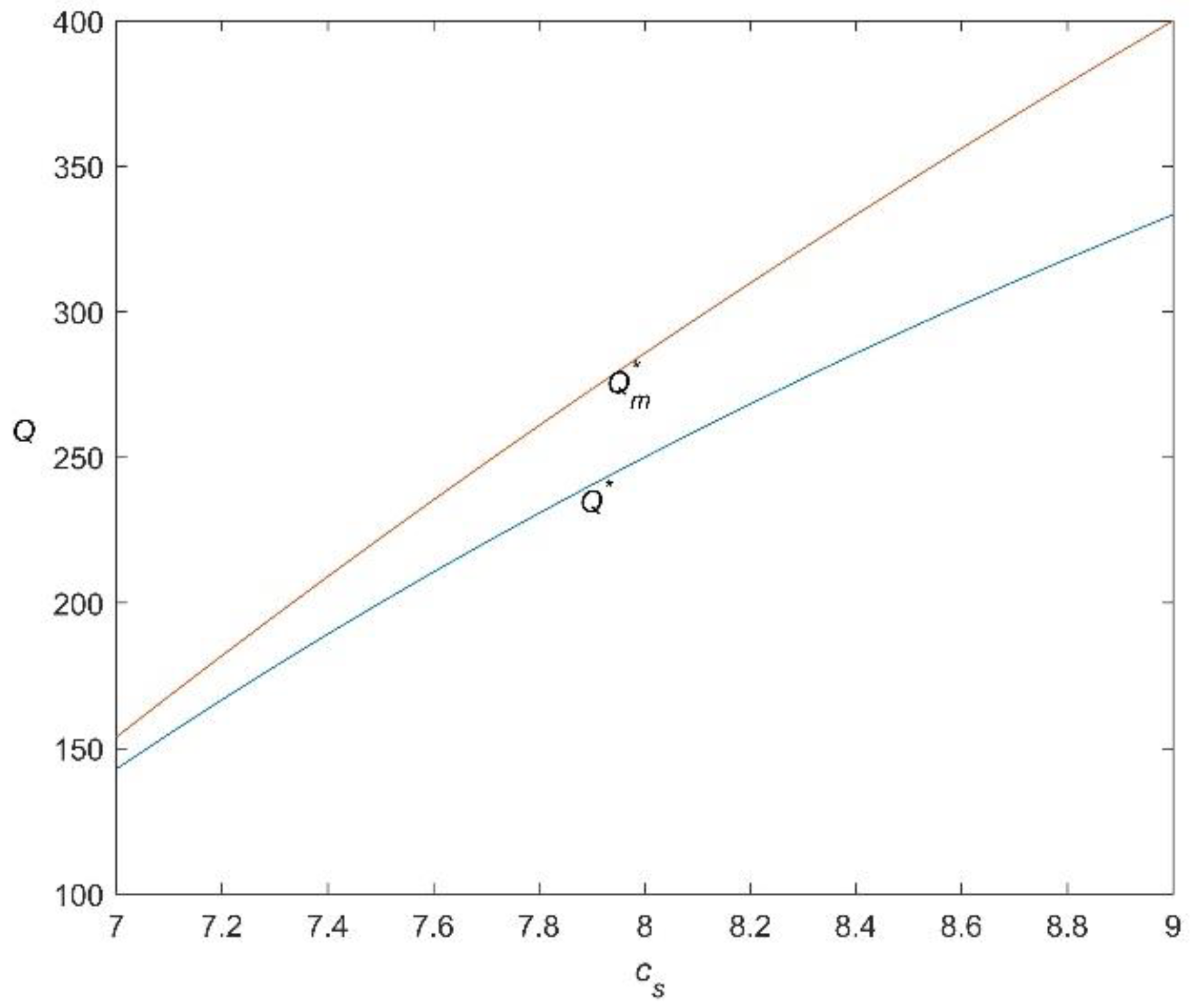

5.1. Impact of Changes in Wholesale Price and Spot Price on Optimal Procurement Decision

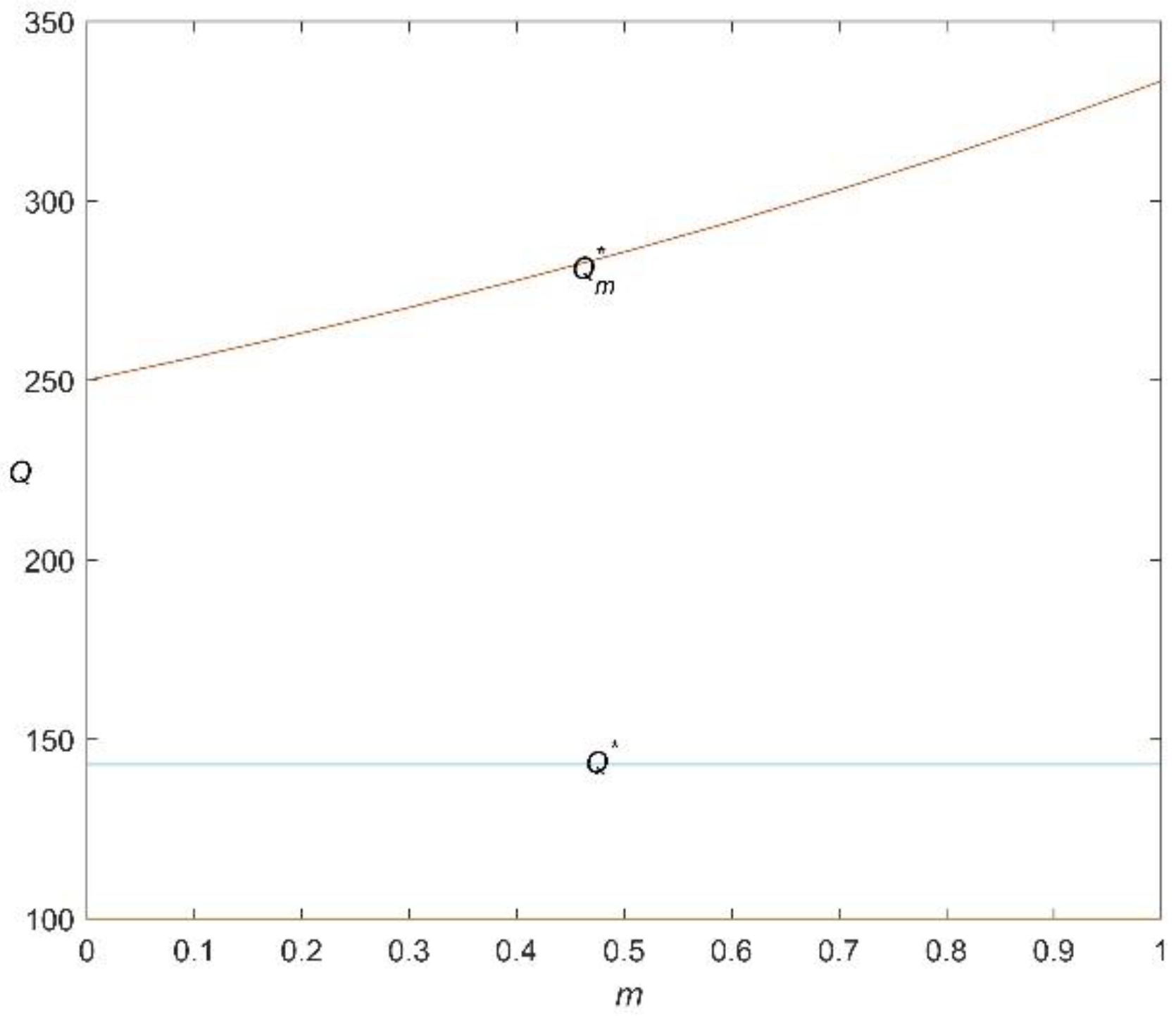

5.2. The Influence of Fixed-Term Contract Supplier Default on Optimal Purchasing Decision

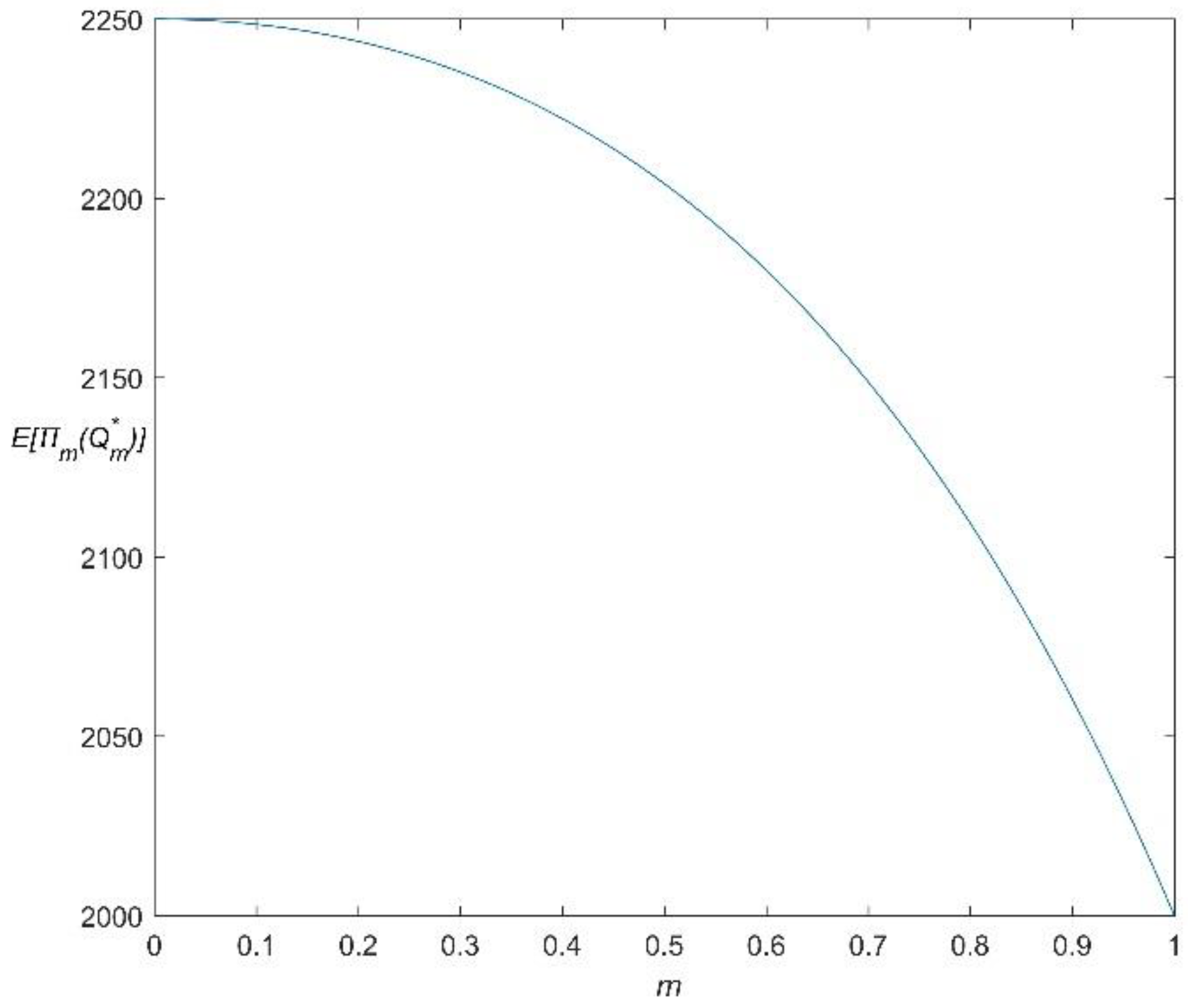

5.3. The Influence of Fixed-Term Contract Supplier’s Default on Buyer’s Expected Profits

6. Conclusions and Management Enlightenment

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Lee, H.; Whang, S. The Impact of the Secondary Market on the Supply Chain. Manag. Sci. 2002, 48, 719–731. [Google Scholar] [CrossRef]

- Chen, F.; Xue, W.; Yang, J. Optimal inventory policy in the presence of a long-term supplier and a spot market. Oper. Res. 2013, 61, 88–97. [Google Scholar] [CrossRef]

- Gao, Y.; Feng, Z.; Zhang, S.B. Managing supply chain resilience in the era of VUCA. Front. Eng. Manag. 2021, 8, 465–470. [Google Scholar] [CrossRef]

- Karl, I.; Peter, K. Capacity reservation under spot market price uncertainty. Int. J. Prod. Econ. 2011, 133, 272–279. [Google Scholar]

- Xu, X.S.; Wang, H.W.; Dang, C.Y.; Ji, P. The loss-averse newsvendor model with backordering. Int. J. Prod. Econ. 2017, 188, 1–10. [Google Scholar] [CrossRef]

- Huang, Z.C.; Zheng, Q.P. A multistage stochastic programming approach for preventive maintenance scheduling of GENCOs with natural gas contract. Eur. J. Oper. Res. 2020, 287, 1036–1051. [Google Scholar] [CrossRef]

- Nicola, S.; Sunder, K. Optimal energy procurement in spot and forward markets. Manuf. Serv. Oper. Manag. 2014, 16, 270–282. [Google Scholar]

- Anderson, E.; Chen, B.; Shao, L.S. Supplier competition with option contracts for discrete blocks of capacity. Oper. Res. 2017, 65, 952–967. [Google Scholar]

- Xu, X.S.; Chan, F.T.S. Optimal option purchasing decisions for the risk-averse retailer with shortage cost. Asia-Pac. J. Oper. Res. 2019, 36, 15. [Google Scholar] [CrossRef]

- Li, J.B.; Luo, X.M.; Wang, Q.F.; Zhou, W.H. Supply chain coordination through capacity reservation contract and quantity flexibility contract. Omega 2021, 99, 102195. [Google Scholar] [CrossRef]

- Zhang, J.H.; Xu, X.S.; Chan, F.T.S. Data-driven analysis on optimal purchasing decisions in combined procurement. Int. J. Prod. Res. 2022, 1–14. [Google Scholar] [CrossRef]

- Lee, C.Y.; Tang, C.S.; Yin, R.; An, J. Fractional price matching policies arising from the ocean freight service industry. Prod. Oper. Manag. 2015, 24, 1118–1134. [Google Scholar]

- Ai, Y.Q.; Xu, Y.F. Strategic sourcing in forward and spot markets with reliable and unreliable suppliers. Int. J. Prod. Res. 2021, 59, 926–941. [Google Scholar] [CrossRef]

- Hong, Z.; Lee, C.K.M. A decision support system for procurement risk management in the presence of spot market. Decis. Support Syst. 2013, 55, 67–78. [Google Scholar] [CrossRef]

- Xu, J.; Feng, G.Z.; Jiang, W.; Wang, S.Y. Optimal procurement of long-term contracts in the presence of imperfect spot market. Omega 2015, 52, 42–52. [Google Scholar] [CrossRef]

- Liu, X.Q.; Chan, F.T.S.; Xu, X.S. Hedging Risks in the Loss-Averse Newsvendor Problem with Backlogging. Mathematics 2019, 7, 429. [Google Scholar] [CrossRef]

- Feng, B.; Ye, Q.W. Operations management of smart logistics: A literature review and future research. Front. Eng. Manag. 2021, 8, 344–355. [Google Scholar] [CrossRef]

- Xu, X.S.; Chan, F.T.S.; Chan, C.K. Optimal option purchase decision of a loss-averse retailer under emergent replenishment. Int. J. Prod. Res. 2019, 57, 4594–4620. [Google Scholar] [CrossRef]

- Xu, X.S.; Ji, P.; Chan, F.T.S. On maximizing a loss-averse buyer’s expected utility in a multi-sourcing problem. Math. Comput. Simul. 2022, 202, 388–404. [Google Scholar] [CrossRef]

- Hendricks, K.B.; Jacobs, B.W.; Singhal, V.R. Stock market reaction to supply chain disruptions from the 2011 great east Japan earthquake. Manuf. Serv. Oper. Manag. 2020, 22, 683–699. [Google Scholar] [CrossRef]

- Yuan, X.; Bi, G.; Zhang, B.; Yu, Y. Option contract strategies with risk-aversion and emergencey purchase. Int. Trans. Oper. Res. 2020, 27, 3079–3103. [Google Scholar] [CrossRef]

- Dhingra, V.; Krishnan, H. Managing reputation risk in supply chains: The role of risk sharing under limited liability. Manag. Sci. 2021, 67, 4845–4862. [Google Scholar] [CrossRef]

- Lin, Q.; Zhao, Q.H.; Lev, B. Influenza vaccine supply chain coordination under uncertain supply and demand. Eur. J. Oper. Res. 2022, 297, 930–948. [Google Scholar] [CrossRef]

- Boute, R.N.; Disney, S.M.; Gijsbrechts, J.; Van, M.J.A. Dual sourcing and smoothing under nonstationary demand time series: Reshoring with speed factories. Manag. Sci. 2021, 68, 1039–1057. [Google Scholar] [CrossRef]

- Zhang, X.; Wang, Y.; Geng, G.; Yu, J. Delay-Optimized Multicast Tree Packing in Software-Defined Networks. In IEEE Transactions on Services Computing; IEEE: Los Alamos, NM, USA, 2021; pp. 1–14. [Google Scholar] [CrossRef]

- Zhang, X.; Wang, T. Elastic and Reliable Bandwidth Reservation Based on Distributed Traffic Monitoring and Control. In IEEE Transactions on Parallel and Distributed Systems; IEEE: Los Alamitos, CA, USA, 2022; pp. 1–18. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Liu, X.; Luo, G.; Xu, X. Optimal Purchasing Decisions with Supplier Default in Portfolio Procurement. Mathematics 2022, 10, 3155. https://doi.org/10.3390/math10173155

Liu X, Luo G, Xu X. Optimal Purchasing Decisions with Supplier Default in Portfolio Procurement. Mathematics. 2022; 10(17):3155. https://doi.org/10.3390/math10173155

Chicago/Turabian StyleLiu, Xiaoqing, Gongli Luo, and Xinsheng Xu. 2022. "Optimal Purchasing Decisions with Supplier Default in Portfolio Procurement" Mathematics 10, no. 17: 3155. https://doi.org/10.3390/math10173155