1. Introduction

Economic growth is an indicator of the increase in the wealth of a country, and several factors are involved in this process, according to Batrancea [

1].Capital market dynamics is one of the factors that influence economic growth. Therefore, optimal asset allocation is essential in this market. It is not easy to make a compelling portfolio. This is why most experts are trying to find a model that is better than other models. Markowitz [

2] was the first researcher to develop a quantitative framework for portfolio selection. This model determined the combination of investment assets such that the risk was minimized and the desired return was achieved. This theory changed the course of thinking about portfolios and was accepted as a practical tool. After the introduction of this model, many researchers developed this model and offered other models, including Linsmeier and Pearson [

3], Rockafellar and Uryasev [

4], etc. The Markowitz model can be used when the number of assets and market constraints are small, but when the actual market conditions are considered, this model’s performance is not very favorable. In capital markets, the search space is vast. Therefore, If we can choose an efficient stock among several stocks and invest in it, we can say that we have made a successful investment. On the other hand, the basic mean-variance model only considers the variance of return as a measure of investment risk.Investors are interested in ascertainingtheir maximum loss on an investment, so that they can invest in the market with more confidence. Hence, relying on return variance as a measure of investment risk is insufficient. Therefore, unfavorable risk criteria, such as CVaR, have attracted attention from researchers. The CVaR model is a more developed mean-variance model, and the risk measure used in this model is the maximum amount of loss on an investment.

Using the DEA and CVaR models to optimize automotive companies’ portfolios in the Iranian stock market was the main objective of our research. Since the automotive price has a direct relationship with other industries, such as the steel, petrochemical, electronic industries, etc., automotive companies have played a decisive role in the Iranian stock market in recent years. They are known as the flagships of other large companies.

Since we are looking for an optimal mix of assets in the real market, we face restrictions such as the number of stocks, the weight of stock, the risk of a stock, etc., which lead to a complex optimization problem. Furthermore, increased taxes and limited resources means that the economic-financial system is complex and non-linear. The stock exchange is one of the subsystems of this system and it is exposed to external noise, including external events and political events. Therefore, optimization in such a context is difficult. For years, advanced mathematics and computers have been used to help researchers with such complex issues. Evolutionary methods are one of the advanced mathematical methods that are used for difficult optimization problems. Therefore, we utilized PSO and ICA algorithms in this study.

The first hypothesis presented in this paper is as follows: the return of the DEA-Mean-CVaR portfolio is higher than the return of the Mean-CVaR portfolio. The second hypothesis of the paper is that the use of the evolutionary methods PSO and ICA can reduce the risk in the Mean-CVaR portfolio.

The innovation of this article is that, as far as we know, it is the first study that deals with the optimization of automotive companies using the DEA-Mean-CVaR model and analyzes the efficiency of stock in relation to Iranian automotive companies.It is also the first study that solves the DEA-Mean-CVaR model with the PSO and ICA algorithms. In this paper, we also present the first study that compares the DEA-Mean-CVaR model with the Mean-CVaR model.

The paper is structured as follows:

Section 2, labeled the literature review, presents the recent studies conducted in portfolio optimization. The CVaR and DEA models are presented in

Section 3. PSO and ICA are explained in

Section 4. The suggested model’s usage in regard to the actual data is described in

Section 5. In

Section 6 we provide a discussion of the results; then, our conclusions are presented in

Section 7.

2. Literature Review

Financial pressures on countries’ economies affect their capital markets, according to Batrancea [

5]. Therefore, determining the optimal strategy in this market is necessary for small and large investors. One of those strategies entails the formation of an optimal portfolio. As mentioned earlier, the initial idea of basket formation was expressed by Markowitz [

2]. CVaR refers to the average of the worst losses at a given confidence level. With the introduction of CVaR and its benefits, such as convexity, many researchers have used this criterion to measure risk, and it quickly became the most popular risk criterion. Among the researchers that have optimized portfolios with Mean-CVaR include Krokhmal et al. [

6] and Bassett et al. [

7], who used discretization to turn the problem into a linear programming problem. Furthermore, Alexander and Baptista [

8], assuming that efficiency follows a multivariate normal distribution, introduced a new model, whereas Huang et al. [

9], Zhu and Fukushima [

10] and Zhu et al. [

11] suggested that robust optimization of the portfolio can be achieved through the use of the worst-case CVaR.Recently, continuous time balance policies were derived for optimization by means of the Mean-CVaR approach in the work of He and Jiang [

12], and Cui et al. [

13] also examined the discrete-time state. The Mean-CVaR portfolio optimization problem was solved based on Lagrangian relaxation of the problem in a discrete time and an imperfect state in a study by Strub et al. [

14]. They solved one of the old puzzles in financial economics, the premium puzzle, using a Mean-CVaR model. They indicated that a CVaR investor would have a balanced set of bills, bonds and stocks in the face of historical returns.

Benati and Conde [

15] put robust portfolio optimization on the agenda. They merged risk and regret criteria with expected returns to find a solution which would guarantee acceptable returns and protect the investor from market fluctuations. The objective function of their problem is the maximum regret of the average return, and the CVaR risk measure is considered as the constraint of the problem.

Aljinović et al. [

16] suggested the PROMETHEE II approach to the formation of a digital currency portfolio. They formed a portfolio considering capital market criteria, standard deviation, VaR, CVaR, and daily returns, then compared the proposed model with the Markowitz, Maximum Sharpe, VaR, and CVaR models. The results demonstrated the success of the PROMETHEE II approach.

Bodnar et al. [

17] investigated the optimal portfolio problem using the Bayesian perspective and VaR and CVaR criteria. In this study, the required values in VaR and CVaR calculations were extracted with the help of the posterior forecast distribution for future portfolio returns, and the optimal portfolio weights were obtained according to the observed data. Their results showed that the Bayesian approach worked better than other methods in VaR forecasting, and the optimal portfolios obtained by means of the Bayesian approach were efficient.

Gabrielli et al. [

18] presented an optimization of the purchase contract portfolio with the goal of maximizing the expected financial performance and minimizing the financial risk. They used CVaR as a measure of risk and showed that the risk of the purchase contract was reduced by forming a portfolio.

Some studies have used DEA, introduced by Charnes et al. [

19], to optimize portfolios. Morey and Morey [

20] presented the mean-variance model, supported by DEA. In this model, the input and output were the variance and the expected return of the portfolio. DEA is a mathematical programming method that assigns a relative efficiency to decision units that convert the same inputs into similar outputs. Based on the weighted sums of outputs in relation to the weighted sums of inputs, the relative efficiency assigned to each decision unit by DEA is calculated.

Briec et al. [

21] endeavored to predict the optimal points of the efficient frontier and to evaluate the efficiency of these desirable points. Joro and Na [

22] presented the mean-variance-skewness framework, relying on DEA. They examined the performance of mutual funds by considering the variance of returns as the input and the average return and deviation coefficient as the output. Chen and Lin [

23] examined the efficiency of investment funds by modeling VaR with DEA. They used VaR as the model’s input and showed that the combination of these two models could be used to evaluate the performance of different fund periods more scientifically. Lamb and Tee [

24], recognizing risk and return measures as valid, applied DEA to the analysis of mutual funds. They demonstrated how a diverse portfolio can be managed. Branda [

25] built upon conventional DEA models to offer a new performance evaluation method. He used standard deviation and return as the input and output, respectively.

Mashayekhi and Omrani [

26] solved a mean-variance-DEA model using the GA algorithm and found, considering the efficiency of the stock, that this model performed better than the mean-variance model.

Zhang and Chen [

27] used the DEA window analysis method and the DEA directional distance function to comprehensively evaluate the dynamic performance of energy portfolios. Using the study sample, they showed that investing in an energy portfolio has a higher average efficiency than investing in a form of energy.

Amin and Hajjam [

28] developed the DEA model for portfolio optimization and investigated the role of alternative optimal solutions in data envelopment analysis (DEA) models. They found that portfolio construction with lower risk and higher returns is possible when alternative optimal solutions are included in the model.

Xiao et al. [

29] built three variation-adaptive DEA models under the mean-variance framework. They considered the expectation and covariance of portfolio returns as the input and output in their DEA models. They investigated the impact of input data uncertainty on the performance and rankings of 30 portfolios from the American stock market.

Zhou et al. [

30] stated that the investment process consists of two parts: stock selection and stock weighting in the portfolio. They introduced a stock selection plan that integrated DEA with multiple data sources, then used a support vector machine (SVM) to select the stock.

Adding new constraints to the portfolio optimization problem makes it a nonlinear programming problem. Classical and meta-heuristic methods have been used to solve this type of problem. One of the evolutionary optimization techniques is PSO, initially developed as an optimization method by Kennedy and Eberhart [

31]. PSO is based on the social behavior of birds. The PSO method is based on the evolution of a group of particles that move in a search space to find an optimal global solution. Evolution occurs based on the velocity of the particles and their motion in the search space, according to Rehman et al. [

32]. Each particle has a memory and records the best position of itself and its neighbors, so the particle interacts with the whole group and has the ability to find the best path [

33]. Cura [

34] used the PSO method for a portfolio selection problem and compared this method with Tabu search approaches, genetic algorithms, and simulated annealing. He demonstrated that the PSO approach was successful in portfolio optimization. Zhu et al. [

35] presented a meta-heuristic perspective to portfolio optimization problems using the PSO method. They tested the model on different limited and unlimited risky investing portfolios and performed a comparison with genetic algorithms. They showed that the PSO model had the highest efficiency in the construction of optimal portfolios.

Najafi and Mushakhian [

36] used the mean-semivariance-CVaR model with PSO and a genetic algorithm (GA) and showed that the PSO algorithm performed better than the GA. Furthermore, the combination of two algorithms can provide better answers. Liu and Yin [

37] found that the PSO algorithm was successful in solving the CVaR model and provided better solutions.

Burney et al. [

38] applied particle-size computationand PSO to perform fuzzy bunching stock set exchange portfolio optimization. They examined the use of the proposed model on Hong Kong stocks. The results showed that fuzzy PSO was appropriate for portfolio optimization. Kaucic [

39] expanded a superseded portfolio plan that merged the risk equality approach with cardinality-constrained portfolio optimization, then for the complex integer programming problem, an ameliorated multi-objective PSO algorithm was used.Konstantinou et al. [

40] optimized the cardinality of the S&P 500 index portfolio using GA and Sonar algorithms. Zhang [

41] developed an improved typical transaction cost function based on CVaR, and managed the market risk by solving it with PSO. He demonstrated that the PSO algorithm effectively ameliorated the precocious phenomenon and showed higher convergence, velocity, and precision.

Another evolutionary optimization technique is ICA, which was introduced by Atashpaz and Lucas [

42]. This algorithm, like other algorithms, is formed with an initial population. These populations are divided into colonial and imperialist groups, and together they form an empire. Most researchers use this algorithm in the field of operations research problems, including Yin and Gao [

43], Saadatjoo and Babamir [

44], andLi et al. [

45]. In this study, we intended to use this algorithm in the optimization of a portfolio.

5. Instance Scrutiny: Iran Stock Exchange

In this section, DEA is used in two ways as follows. In the first method, efficient assets are first identified using DEA, then we optimize automotive industry portfolio with efficient assets using two algorithms, PSO and ICA. In the second method, the automotive industry portfolio is optimized with two algorithms, PSO and ICA, then we check the efficiency of the portfolio generated by the mentioned algorithms.Then, these methods were compared with the classic Mean-CVaR model. Here, the source of data was selected as the Iranian Stock Exchange. We considered the actual data of 23 automotive companies which had been active during the period from 2017 to 2020. We also applied the price index from 2017 to 2020 to determine the trends of the automotive market.

Figure 3 shows a Q-Q graph of the price index of the automotive group. The Q-Q graph was applied to test normality. In these graphs, if the data were located on the mean line, it was said that the data distribution was normal. If the data were scattered around the mean line, then the data were not normal. As expected, most of the data were scattered around the mean line, so the price index did not have a normal distribution. We plotted a histogram of the return matching (

Figure 4) to understand how the data were distributed.

Figure 4 presents a histogram of the automotive price index. The histogram demonstrates that the automotive index was skewed to the right. That is, there was a possibility of a price increase in the index in the future. In this way, investing in the automotive market would bring returns. Therefore, investors who were looking for short-term investments could benefit from this increase.

Matlab software was used to calculate the logarithmic returns of each asset and the CVaR, with three levels of confidence. This software was also used to implement PSO, ICA, and DEA. The logarithmic return of each asset is shown in

Figure 5.

Table 1 shows the input and output of the first method, including CVaR, with three levels of confidence, and the expected return. Futhermore, Tables 10 and 11 display the input and output for the second method.

According to

Table 1, asset #10 had the highest expected return, and CVaR increased with an increasing confidence level. Furthermore, asset #11 had the lowest CVaR in 90% and 95% confidence levels, and asset #3 had the lowest CVaR, with a confidence level of 99.

Table 2 presents the efficiency of each asset. According to these results, asset #10, which had the highest expected return, was efficient in the three confidence levels. Asset #11, which had the lowest CVaR at the 90% and 95% confidence levels, was efficient in three levels. Asset #3 had the lowest CVaR at a confidence level of 99, so it was efficient at this level.

Table 3 and

Table 4 illustrate the input parameters of two algorithms.

We formed an automotive industry portfolio with efficient assets and the Mean-CVaR model. The results are presented in

Table 5,

Table 6 and

Table 7 and

Figure 6 and

Figure 7. We found that:

Both algorithms preferred to invest in asset #10, which has the highest expected return and was efficient with three levels of confidence.

The risk and return of the portfolios in both algorithms were equal in three levels of confidence.

The frontiers in both algorithms overlapped in three levels of confidence.

According to

Table 7, the highest weight was related to asset #3 in the Mean-CVaR model.

The return and risk of the Mean-CVaR model were low.

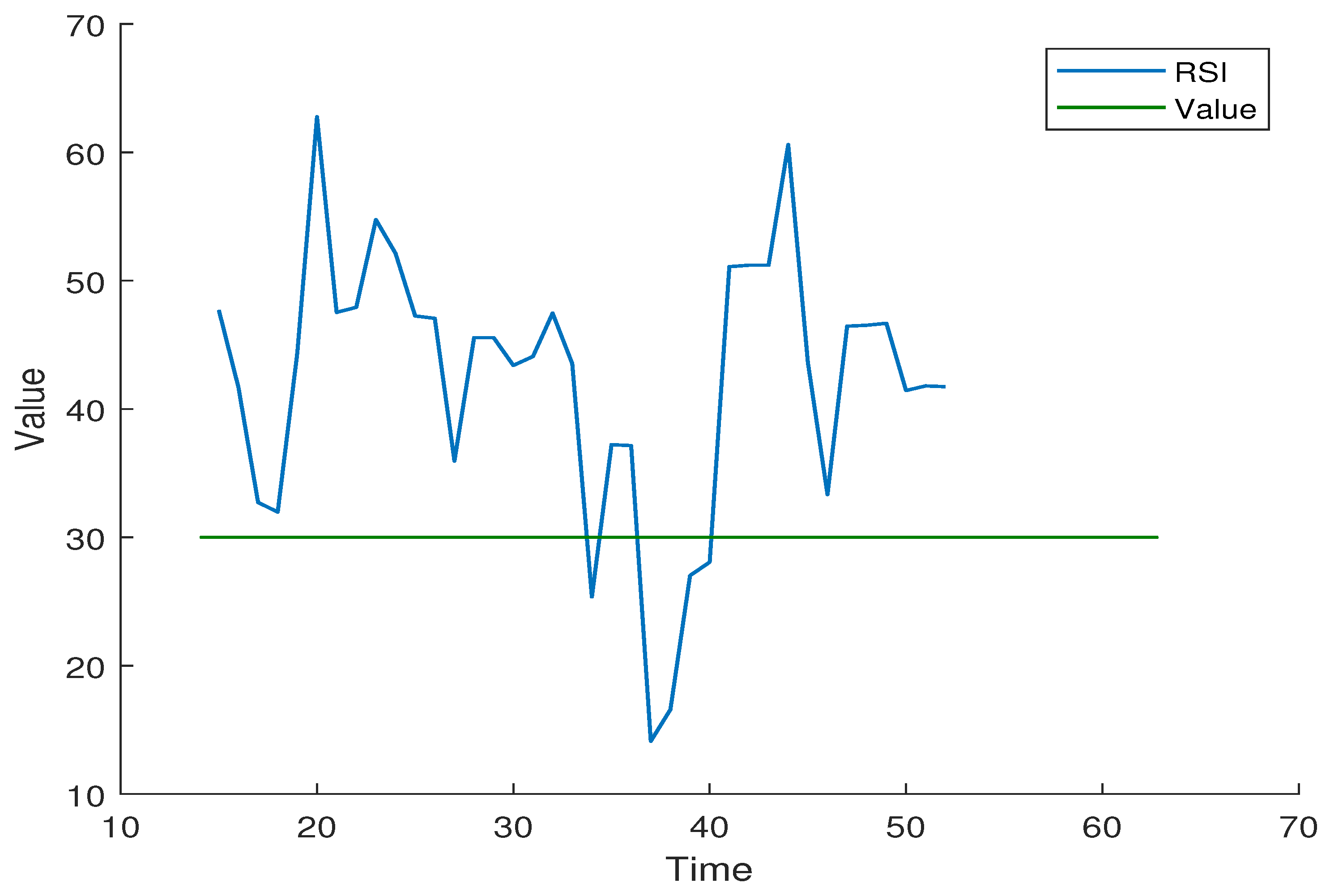

Figure 8 and

Figure 9 present the daily return distribution of asset #10 and the relative strength index, respectively.

Figure 9 displays the relative strength index. The stock has little risk if this index is below 30and should be bought. The stock has a lot of risk if this index reaches 70 and should be sold. After obtaining the optimal solution with the DEA-Mean-CVaR model, we found that the DEA-Mean-CVaR model suggested investing only in asset #10. By constructed the logarithmic return diagram of the proposed stock, we realized that the proposed stock was skewed to the right, which meant that there was a possibility of an increase in the return. Furthermore, by analyzing the relative strength index, we discovered that this asset had reached the number 30 and should be bought. Therefore, it can be concluded that in the first method, the model suggested an asset that should be bought according to the index and also, according to the histogram, there was a probability of a return from this stock.

The histogram of asset #3 return is shown in

Figure 10. This asset received the most weight according to the Mean-CVaR model. The histogram illustrates that the return distribution of asset #3 exhibited kurtosis. Thus, there were extreme points (a sudden price increase) in this asset. Therefore, it can be inferred that the weights were assigned based on the momentary return in the Mean-CVaR model, whereas

Figure 11 shows that the index has reached 70, so the stock risk is high and should be sold.

Table 8, shows that both algorithms in levels 90 and 95 assigned the most weight to asset #10, with the highest expected return, and in level 99 they assigned the most weight to asset #5. Furthermore, according to

Table 9, the PSO algorithm under constant return showed more risk than the ICA algorithm.

Figure 12 shows that the frontier of the PSO algorithm was higher than that of the ICA algorithm, so the PSO portfolio under certain return conditions showed more returns than the ICA portfolio.

Table 10 and

Table 11 show the inputs and outputs of the second method, including the CVaR of the portfolios in three levels of confidence, along with their returns. It was found that CVaR increased with increasing confidence levels.

As shown in

Table 12, portfolios 1, 4, 12, and 14 were efficient in three levels for both algorithms. The number of efficient portfolios in three levels was higher in the PSO algorithm than in the ICA algorithm.Portfolio #15, which was considered as the output of the algorithms, was efficient in the PSO algorithm in three levels. After obtaining the numerical results, we tested our hypotheses using the Wilcoxon test.

According to

Table 13, the probability was less than 0.05, so the hypothesis of return equality was rejected. In other words, there was a difference between the efficiencies. Furthermore, the hypothesis of risk equality was rejected because the probability was less than 0.05.

7. Conclusions

In this research, we optimized an automotive industry portfolio for the Iranian stock market in two ways. These companies play an essential role in the Iranian stock market. At the beginning of the research, we proposed two hypotheses as follows: 1. The returns obtained in the DEA-Mean-CVaR portfolio were higher than the returns of the Mean-CVaR portfolio. 2. The use of the evolutionary methods PSO and ICA reduced the risk of the Mean-CVaR portfolio.

Then, we checked the price index of the automotive industry. Our focus on the the automotive group index showed that the distribution of the price index was skewed to the right, so it could be said that investing in the automotive market would bring returns. Therefore, with the help of 23 automotive companies, we formed a portfolio using two methods. In the first method, CVaR was formulated using DEA, and then this model was solved using the PSO algorithm and the ICA algorithm. Based on the results shown in

Table 5, it was found that both algorithms led to the proposal to invest in assets that had the highest expected return and that were found to be efficient at three levels of confidenceand that should have been purchased according to the RSI index. Furthermore, considering

Table 9, the risk and return of both algorithms were equal with three levels of confidence, so according to

Figure 6, the frontiers of the two algorithms coincided. In the second method, was solved the CVaR model using the PSO and ICA algorithms, then evaluated the performance of the obtained securities. We found that out of 40 portfolios generated using the algorithms, only 15 portfolios were located at the border, and according to

Table 12 of these 15 portfolios, only four portfolios in both algorithms were considered efficient at three levels.

The results of the testing of the hypotheses indicated that the development of the Mean-CVaR model increased returns, and the use of innovative methods in its solution reduced risk.

Similarly to [

26], and as shown in

Table 5 and

Figure 6, we found that the development of portfolio selection models with the DEA model obtained better results.Furthermore, as shown in

Table 12 and

Figure 12, similarly to the research of [

36,

37], our results indicated that the PSO algorithm performed better in the task of portfolio optimization.

Finally, we conclude that when the Mean-CVaR model is developed using the DEA model and when evolutionary algorithms are used to the solution of these problems, we can invest more confidently in the proposed stocks. Overall, it can be stated that if investors have a low degree of risk aversion, they can take advantage of the combination of DEA and Mean-CVaR models. For future research, we suggested modeling other risk measures by means of DEA and then calculating solutions with the PSO algorithm to compare results with those the strength Pareto evolutionary algorithm.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}