Self-Expansion or Internalization as the Two Processes of Vertical Integration: What Informs the Decision?

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

2. Self-Expansion as a Blind Spot in Vertical Integration Literature

2.1. Production Efficiency Approach

2.2. Market Power Approach

2.3. Transaction Cost Economics Approach

2.4. Capability Approach

2.5. Self-Expansion as a Blind Spot in Vertical Integration Literature

3. Methodology

4. Building an Analytical Model

4.1. Vertical Integration Model Based on the TCE Approach

4.2. Integration of the Capability Approach into the TCE Approach

4.3. Building a Model

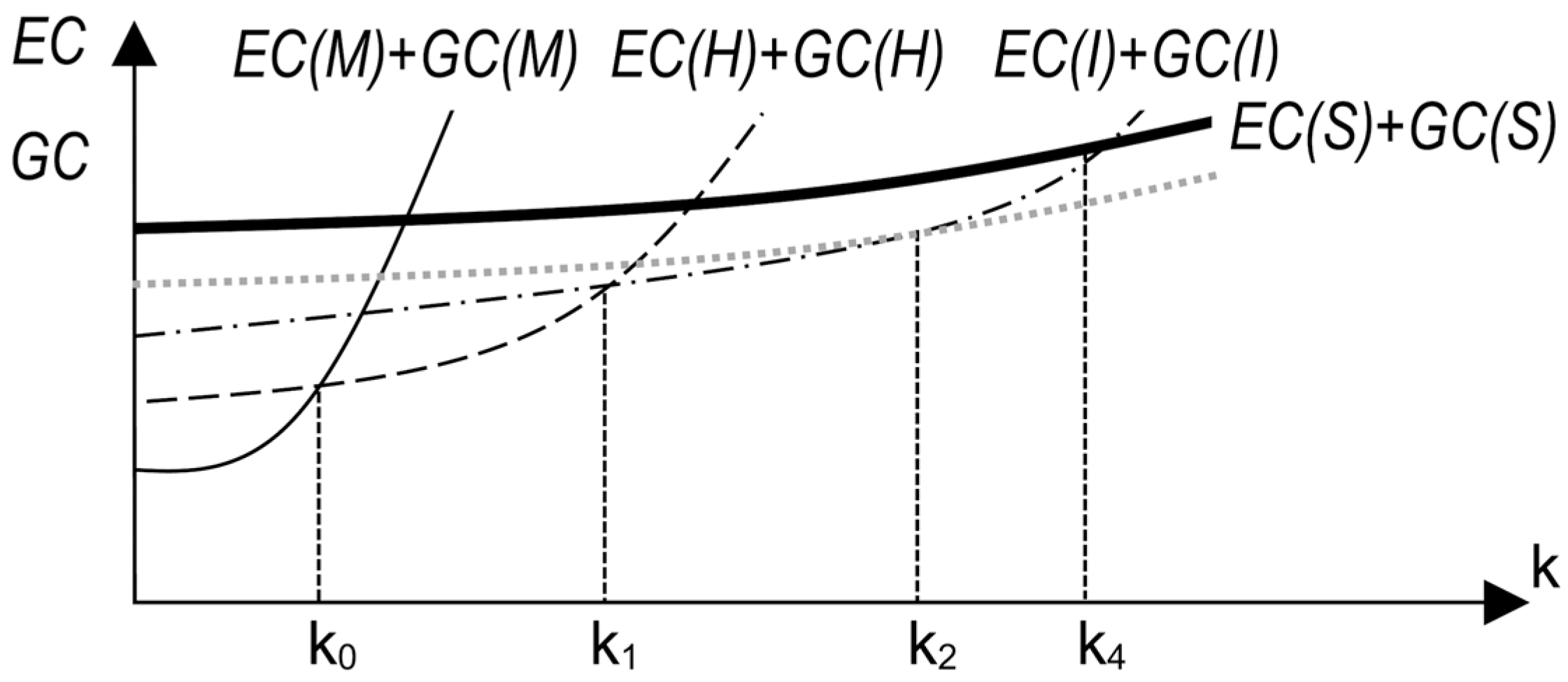

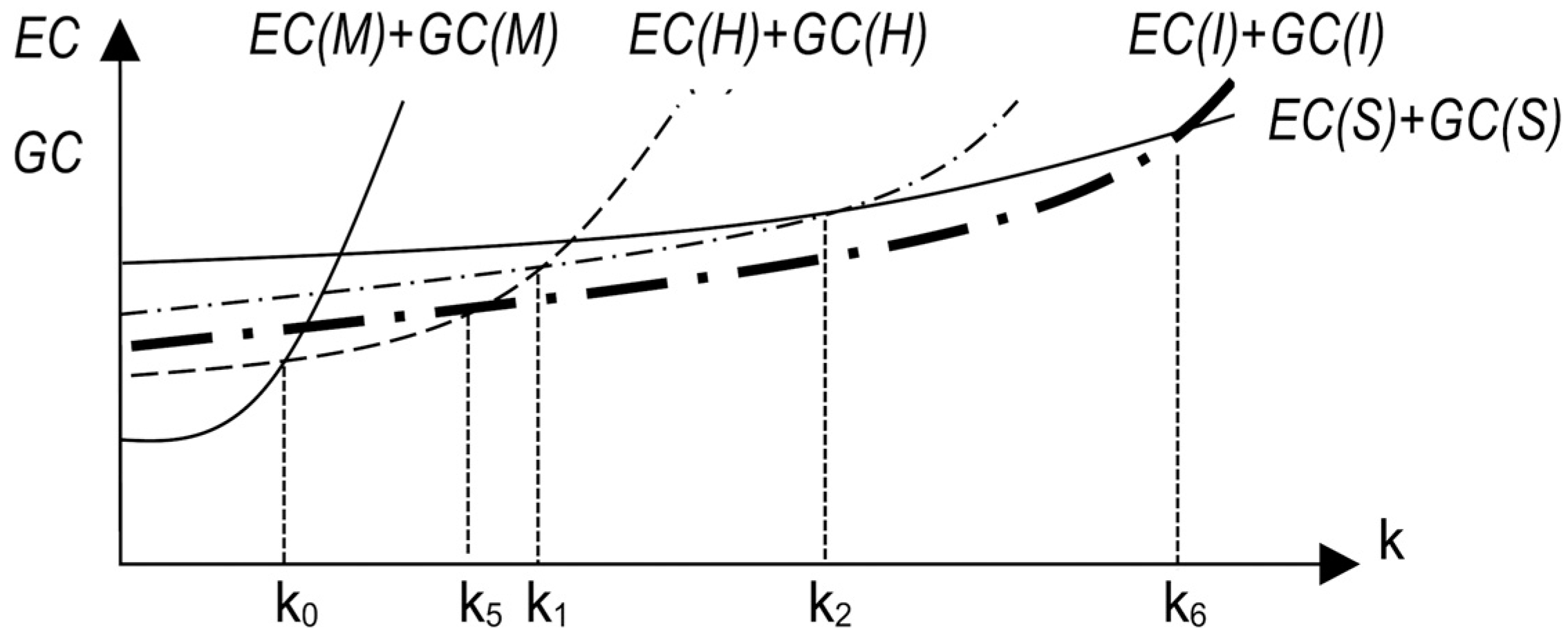

5. Hypotheses from the Model

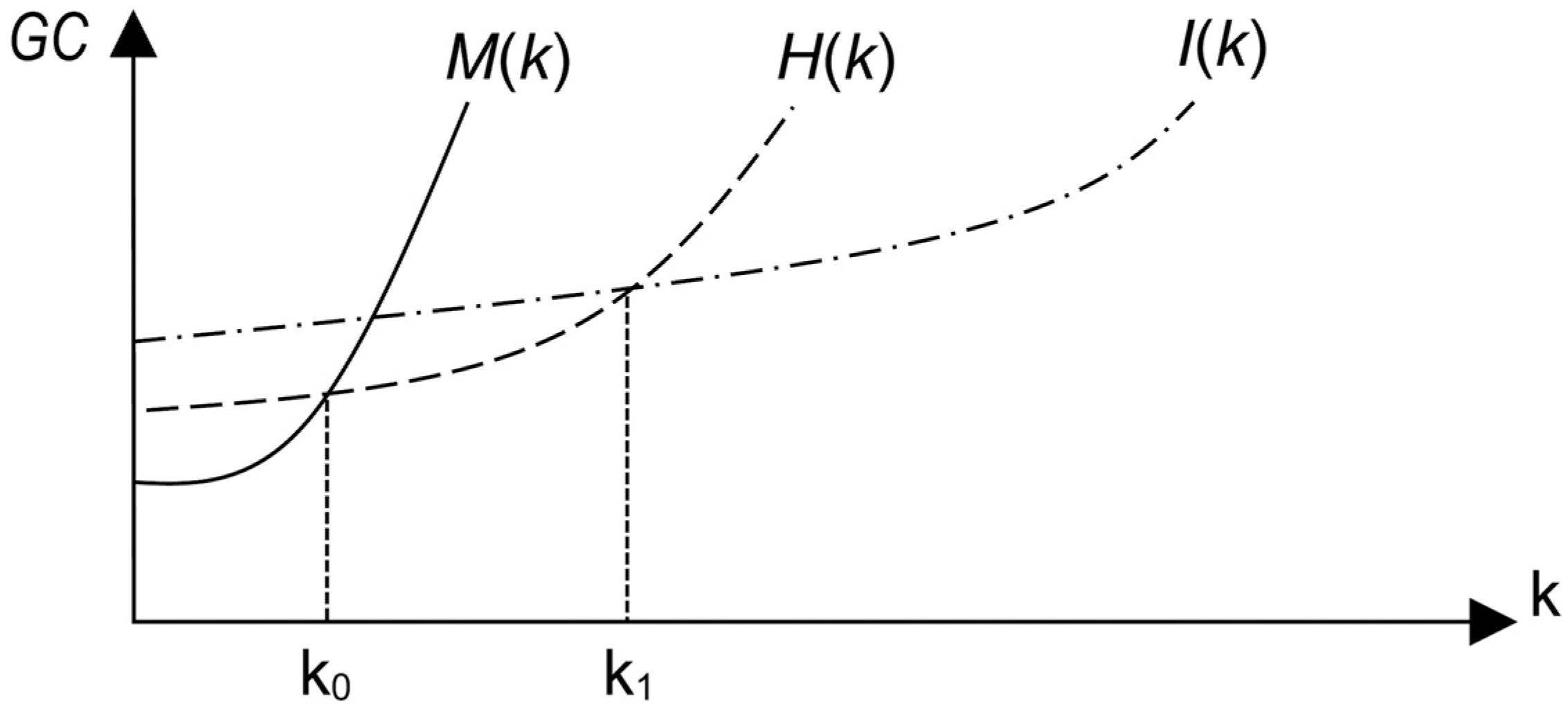

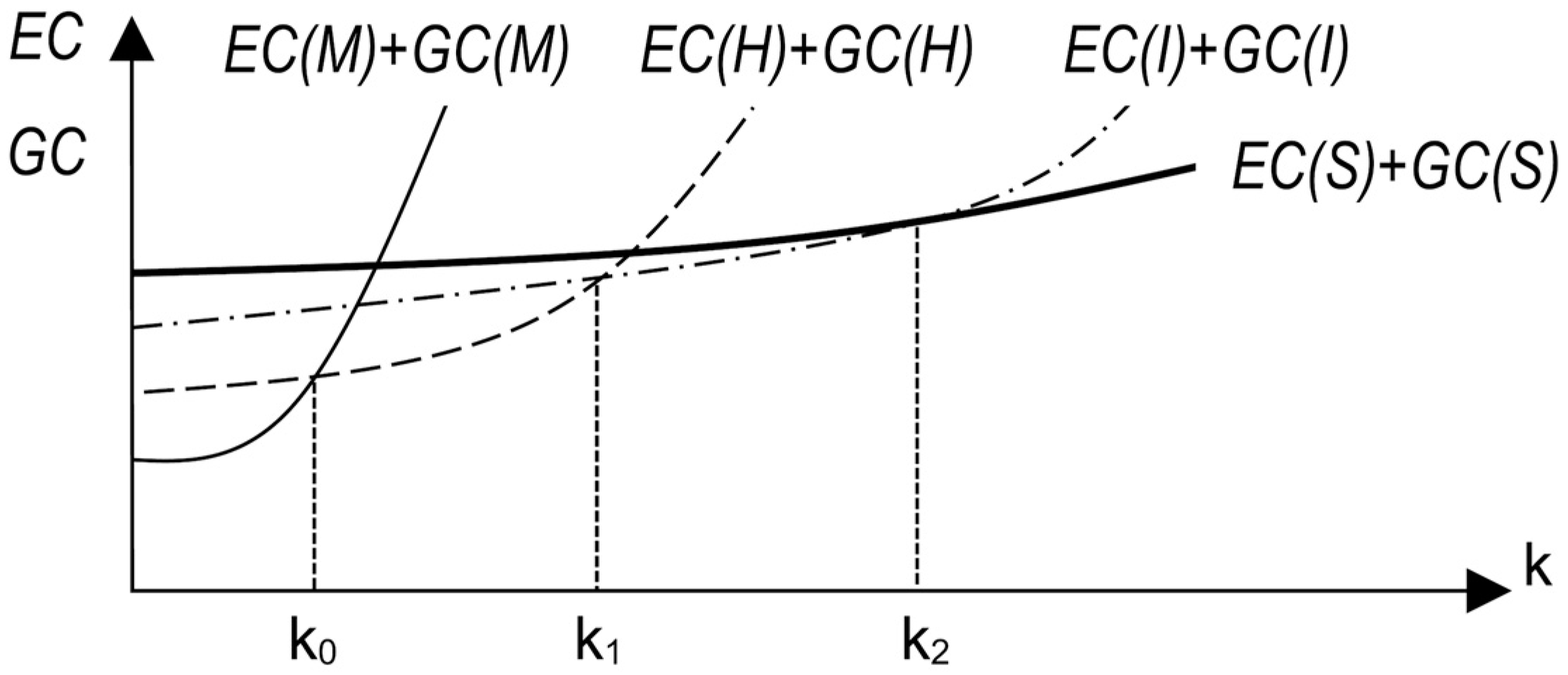

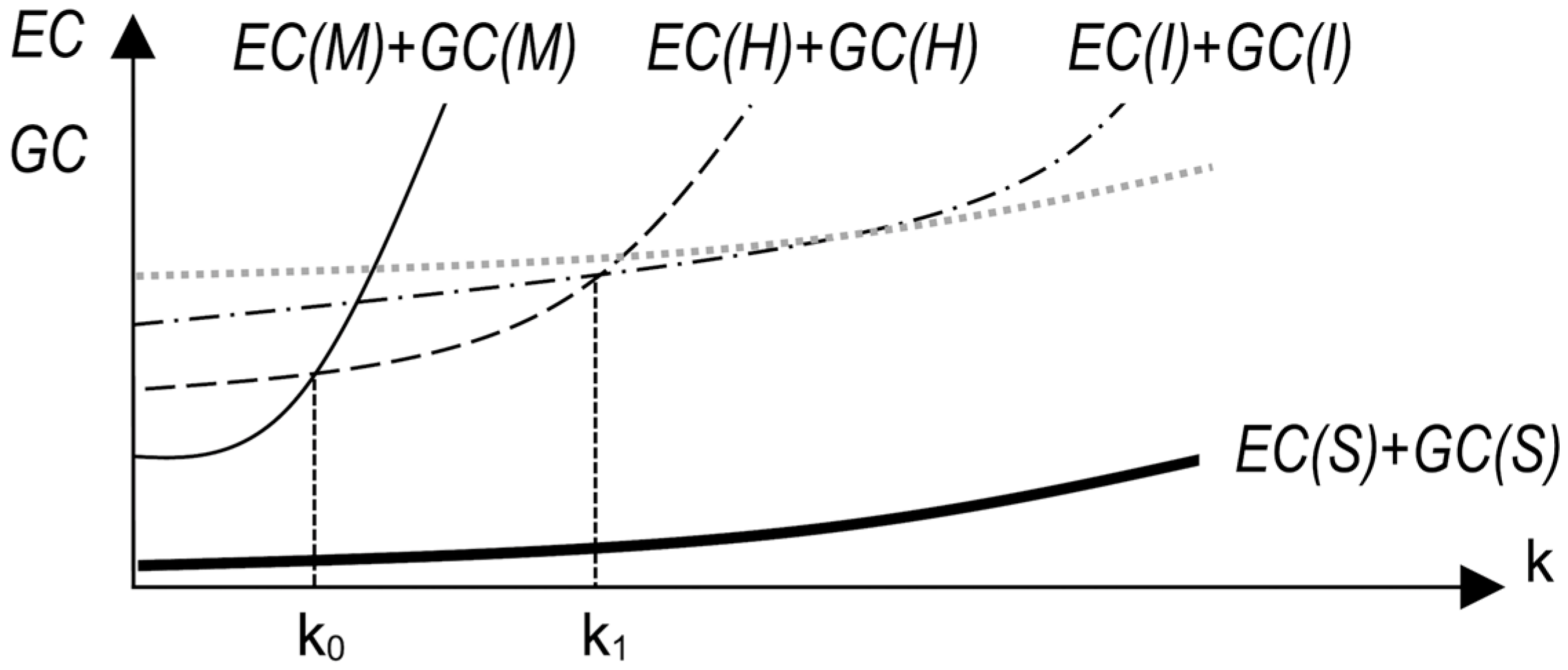

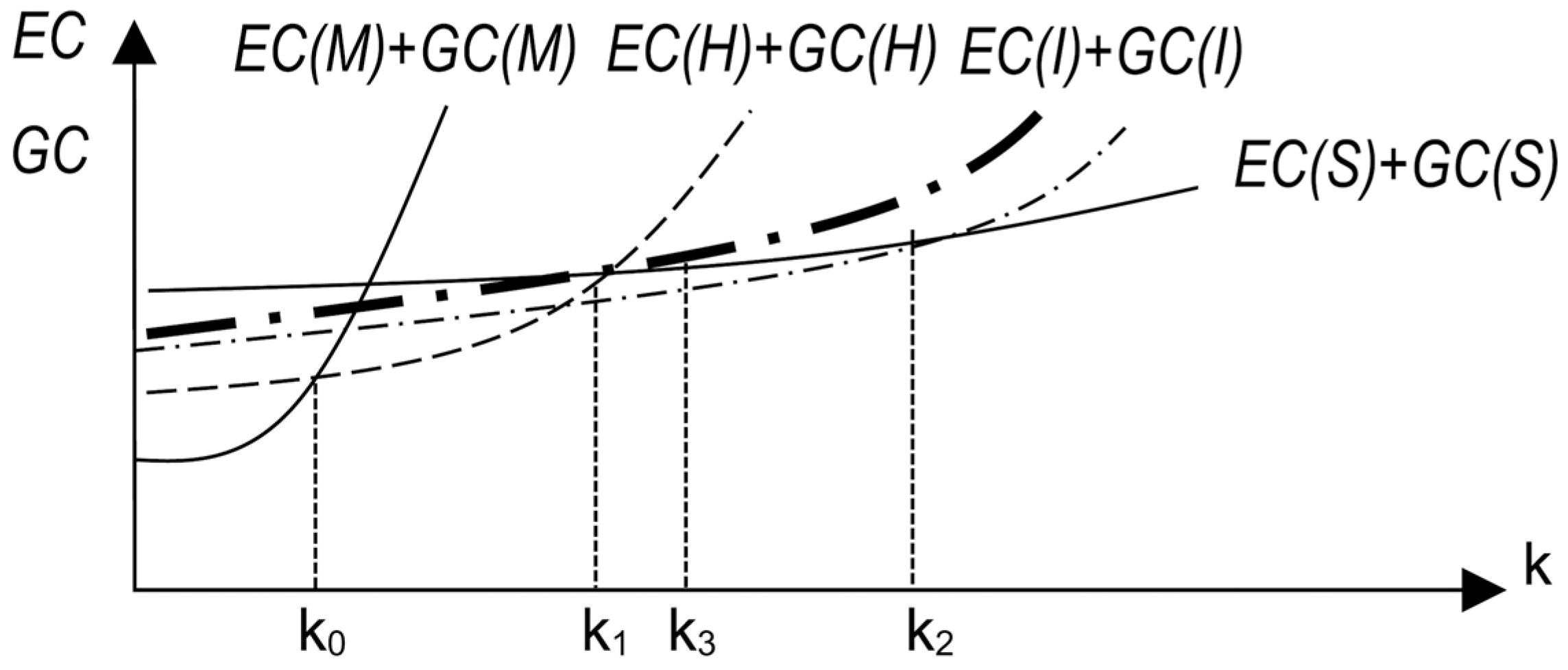

5.1. Why Self-Expand the Scope of Activities: Low EC and GC of Self-Expansion

5.2. Why Self-Expand the Scope of Activities: High EC and GC of Internalization

5.3. Why Choose Internalization of outside Activities: High EC and GC of Self-Expansion

5.4. Why Choose Internalization of outside Activities: Low EC and GC of Internalization

6. Discussion

7. Conclusions

Funding

Data Availability Statement

Conflicts of Interest

References

- Acemoglu, Daron, Simon Johnson, and Todd Mitton. 2009. Determinants of Vertical Integration: Financial Development and Contracting Costs. The Journal of Finance 64: 1251–90. [Google Scholar] [CrossRef]

- Anderson, Erin. 1985. The Salesperson as Outside Agent or Employee: A Transaction Cost Analysis. Marketing Science 4: 234–54. [Google Scholar] [CrossRef]

- Bain, Joe. 1968. Industrial Organization. New York: Wiley. [Google Scholar]

- Barney, Jay B. 1999. How a Firm’s Capabilities Affect Boundary Decisions. Sloan Management Review 40: 137–45. [Google Scholar]

- Cadot, Julien. 2015. Agency Costs of Vertical Integration-The Case of Family Firms, Investor-Owned Firms and Cooperatives in the French Wine Industry. Agricultural Economics 46: 187–94. [Google Scholar] [CrossRef]

- Cuypers, Ilya R. P., Jean-François Hennart, Brian S. Silverman, and Gokhan Ertug. 2021. Transaction cost theory: Past progress, current challenges, and suggestions for the future. Academy of Management Annals 15: 111–50. [Google Scholar] [CrossRef]

- David, Robert J., and Shin-K. Han. 2004. Systematic Assessment of the Empirical Support for Transaction Cost Economics. Strategic Management Journal 25: 39–58. [Google Scholar] [CrossRef]

- Díez-Vial, Isabel. 2007. Explaining Vertical Integration Strategies: Market Power, Transactional Attributes and Capabilities. Journal of Management Studies 44: 1017–40. [Google Scholar] [CrossRef]

- Fan, Joseph P. H., Jun Huang, Randall Morck, and Bernard Yeung. 2017. Institutional Determinants of Vertical Integration in China. Journal of Coporate Finance 44: 524–39. [Google Scholar] [CrossRef]

- Fan, Joseph P. H., and Larry H. P. Lang. 2000. The Measurement of Relatedness: An Application to Corporate Diversification. The Journal of Business 73: 629–60. [Google Scholar] [CrossRef]

- Fernández-Olmos, Marta, Natalia Dejo-Oricain, and Jorge Rosell-Martínez. 2016. Product Differentiation Strategy and Vertical Integration: An Application to the Doc Rioja Wine Industry. Journal of Business Economics and Management 17: 796–809. [Google Scholar] [CrossRef] [Green Version]

- Gould, Jay R. 1977. Price Discrimination and Vertical Control: A Note. Journal of Political Economy 85: 1063–71. [Google Scholar] [CrossRef]

- Greenhut, Melvin L., and Hiroshi Ohta. 1979. Vertical Integration of Successive Oligopolists. American Economic Review 69: 137–41. [Google Scholar]

- Grossman, Sanford J., and Oliver D. Hart. 1986. The Costs and Benefits of Ownership: A Theory of Vertical and Lateral Integration. Journal of Political Economy 94: 691–719. [Google Scholar] [CrossRef] [Green Version]

- Hart, Oliver, and John Moore. 1990. Property Rights and the Nature of the Firm. Jounral of Political Economy 98: 1119–58. [Google Scholar] [CrossRef] [Green Version]

- Krattenmaker, Thomas G., and Steven C. Salop. 1986. Anticompetitive Exclusion: Raising Rivals’ Costs to Achieve Power over Price. The Yale Law Journal 96: 209–93. [Google Scholar] [CrossRef]

- Lafontaine, Francine, and Margaret Slade. 2007. Vertical Integration and Firm Boundaries: The Evidence. Journal of Economic Literature 45: 629–85. [Google Scholar] [CrossRef] [Green Version]

- Leiblein, Michael J., Jeffrey J. Reuer, and Frédéric Dalsace. 2002. Do Make or Buy Decisions Matter? The Influence of Organizational Governance on Technological Performance. Strategic Management Journal 23: 817–33. [Google Scholar] [CrossRef]

- Loertscher, Simon, and Michael H. Riordan. 2019. Make and Buy: Outsourcing, Vertical Integration, and Cost Reduction. American Economic Journal Microecnomics 11: 105–23. [Google Scholar] [CrossRef]

- Mahoney, Joseph T. 1992. The Choice of Organizational Form: Vertical Financial Ownership Versus Other Methods of Vertical Integration. Strategic Management Journal 13: 559–84. [Google Scholar] [CrossRef] [Green Version]

- Masten, Scott E. 1984. The Organization of Production: Evidence from the Aerospace Industry. The Journal of Law and Economics 27: 403–17. [Google Scholar] [CrossRef]

- Moeen, Mahka, and Will Mitchell. 2020. How do pre-entrants to the industry incubation stage choose between alliances and acquisitions for technical capabilities and specialized complementary assets? Strategic Management Journal 41: 1450–89. [Google Scholar] [CrossRef]

- Monteverde, Kirk, and David J. Teece. 1982. Supplier Switching Costs and Vertical Integration in the Automobile Industry. The Bell Journal of Economics 13: 206–13. [Google Scholar] [CrossRef]

- Perry, Martin K. 1989. Vertical integration: Determinants and effects. Handbook of Industrial Organization 1: 183–255. [Google Scholar]

- Riordan, Michael H., and Oliver E. Williamson. 1985. Asset Specificity and Economic Organization. International Journal of Industrial Organization 3: 365–78. [Google Scholar] [CrossRef]

- Salinger, Michael A. 1988. Vertical Mergers and Market Foreclosure. The Quarterly Journal of Economics 103: 345–56. [Google Scholar] [CrossRef]

- Salop, Steven C., and David T. Scheffman. 1987. Cost-Raising Strategies. The Journal of Industrial Economics 36: 19–34. [Google Scholar] [CrossRef]

- Spengler, Joseph J. 1950. Vertical Integration and Antitrust Policy. The Journal of Political Economy 58: 347–52. [Google Scholar] [CrossRef]

- Stigler, George J. 1951. The Division of Labor is Limited by the Extent of the Market. The Journal of Political Economy 59: 185–93. [Google Scholar] [CrossRef]

- Teece, David J. 2007. Explicating Dynamic Capabilities: The Nature and Microfoundations of (Sustainable) Enterprise Performance. Strategic Management Journal 28: 1319–50. [Google Scholar] [CrossRef] [Green Version]

- Teece, David J. 2010. Forward Integration and Innovation: Transaction Costs and Beyond. Journal of Retailing 86: 277–83. [Google Scholar] [CrossRef]

- Teece, David J. 2014. A Dynamic Capabilities-Based Entrepreneurial Theory of the Multinational Enterprise. Journal of International Business Studies 45: 8–37. [Google Scholar] [CrossRef] [Green Version]

- Teece, David J., Gary Pisano, and Amy Shuen. 1997. Dynamic Capabilities and Strategic Management. Strategic Management Journal 18: 509–33. [Google Scholar] [CrossRef]

- Williamson, Oliver E. 1971. The Vertical Integration of Production: Market Failure Considerations. American Economic Review 61: 112–23. [Google Scholar]

- Williamson, Oliver E. 1975. Markets and Hierarchies: Analysis and Antitrust Implications. New York: Free Press. [Google Scholar]

- Williamson, Oliver E. 1983. Credible Commitments: Using Hostages to Support Exchange. American Economic Review 73: 519–40. [Google Scholar]

- Williamson, Oliver E. 1985. The Economic Institution of Capitalism: Firms, Markets, Relational Contracting. New York: Free Press. [Google Scholar]

- Williamson, Oliver E. 1991. Comparative Economic Organization: The Analysis of Discrete Structural Alternatives. Administrative Science Quarterly 36: 269–96. [Google Scholar] [CrossRef] [Green Version]

- Williamson, Oliver E. 1996. The Mechanisms of Governance. New York: Oxford University Press. [Google Scholar]

- Zhou, Yue M., and Xiang Wan. 2017. Product Variety and Vertical Integration. Strategic Management Journal 38: 1134–50. [Google Scholar] [CrossRef]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Hashimoto, N. Self-Expansion or Internalization as the Two Processes of Vertical Integration: What Informs the Decision? Economies 2021, 9, 197. https://doi.org/10.3390/economies9040197

Hashimoto N. Self-Expansion or Internalization as the Two Processes of Vertical Integration: What Informs the Decision? Economies. 2021; 9(4):197. https://doi.org/10.3390/economies9040197

Chicago/Turabian StyleHashimoto, Noriaki. 2021. "Self-Expansion or Internalization as the Two Processes of Vertical Integration: What Informs the Decision?" Economies 9, no. 4: 197. https://doi.org/10.3390/economies9040197