1. Introduction

The word entrepreneur originates from the root words entre refers to “enter”, pre refers to “before” and neur stands for “nerve-center”. Briefly, one enters a business at a certain time to form meaningful change such as nerve or decision center (

McKay 2001). Similarly,

Cooke and Xiao (

2021) highlighted that entrepreneurship refers to the level of motivation and capability that enables to commence, organize, and develop a business with a certain level of risk. Moreover, entrepreneurship does not only refer to beginning a new enterprise, rather it requires a core mindset with creative and strategic thinking and vision even in uncertain conditions. Thus, it cannot be denied that entrepreneurial activities contribute a major portion to grow economically in a country, through implementing several policies regarding entrepreneurs.

Zeb and Ihsan (

2020) argued that Pakistan being a developing state comprises an estimated population of 207 million includes approximately 49.2% women but women’s participation in an economic expansion is less compared to men, which might be because of gender discrimination. Global Gender Report circulated in 2021 disclosed “The World Economic Forum” that among 156 nations, Pakistan is in 153rd position based on gender parity and it demonstrates the lowermost rate of woman entrepreneurs globally owing to several social and cultural factors. The Pakistani government is striving to empower the youth and bolster the entrepreneurial ecosystem in our motherland. Similarly, according to the state-owned associated press of Pakistan program “PM’s Start-up Pakistan” is also launched to boost entrepreneurs. Hence, women globally make a majority of purchasing decisions moreover, their economic empowerment is considered the biggest occurring change in our social lives (

Lakshmi 2015).

Scholars have discussed comprehensively on behavioral finance and they have analyzed investors’ behavior to make us aware of how investors manage to invest locally and internationally. Recent studies have witnessed individuals’ personal qualities and traits influence their behavior, risk perception, and willingness to make different decisions. Thus, these personal attributes that influence investment attitude and performance still need to be explored on a wider scale (

Akhtar et al. 2018).

Eysenck (

1991) studied that personal attributes comprise five principles facsimile, inclusiveness, external-correlates, source traits, and multiple levels. These principles were renamed as Five-Factor Model. On contrary, an investor is also affected by societal factors while performing investing activities such as media, social networks with friends and kinsfolks, electronic media i.e., the internet that has become an essential source to exchange information. Several studies also explain that behavioral finance discusses investors’ decision that is affected due to emotional and psychological factors and several other factors that drive the investor’s decisions (

Davis 2006;

Shiller 2000). Social interactions with friends and family greatly affect investment decisions as well as returns. Moreover, interaction with one another helps in seeking rational information to make final investment decisions (

Shiller and Pound 1989).

Baporikar and Akino (

2020) explored that collateral security, imperfect business services, asymmetry flow of information, and loans with high interest are a few issues that make financing and its accessibility difficult. This indicates a knowledge gap in entrepreneurs who are unaware of the potential information that banks need. Today knowledge is considered a critical resource, for any organization’s growth, progress, and sustainability. Financial literacy or learning widens access to relevant information, provides better knowledge to make long-term decisions and survive successfully.

Hence, women entrepreneurs require proper training with adequate knowledge and relevant information that enable them to access finance easily from distinct financial institutions. Besides,

Baum and Ingram (

1998) suggested that gaining external knowledge makes competent, enhances the base of knowledge, improves technological proficiencies, and helps generate profit for the ventures. The reason behind equipping them with sound knowledge is to make better financial decisions that are highly affected and influenced by emotional outcomes. Investors’ behavior changes or alters according to different markets and conditions therefore, it is necessary to inculcate psychological factors in finance too. Thus, keeping in view behavioral finance principles would mount a substantial amount of profits for the entrepreneurs as investors. The reason behind focusing on women in this study is to highlight issues that educate the future generation of the nation, which means to provide them with potential knowledge and such entrepreneurial expertise so that they can overcome the upcoming challenges. Moreover, to enable them to generate such ideas that can equip themselves with innovations and transfer the same to make a better place to live in (

Baporikar and Akino 2020). Several developing and developed countries in the past as well as in the present are still facing financial crises, and their markets have been witnessing and observing volatility for years. This vulnerability has led to increased uncertainty. Previous studies have comprehensively discussed numerous factors regarding women entrepreneur startups considering the incubators who facilitate them to accelerate their business successfully in the market.

In contrast,

Kappal and Rastogi (

2020) explored the personal financial decisions of women entrepreneurs. Whereas, this study proposes those underlying factors that highly influence women’s attitude towards financial investment decisions in the context of Pakistan. Women entrepreneurs in Pakistan tend to grow substantially, simultaneously; they are also highly affected by social, personal, and behavioral factors. Therefore, the research aims to discuss and highlight the issue that women entrepreneur suffers while making their capital investment decisions. These decisions to maximize their returns require sufficient financial knowledge, training, and societal encouragement and motivation so that they are capable enough to overcome uncertain events in the prevailing market and sustain to contribute to the well-being of the society, community, and nation as a whole. The research gap of the current study underlies the understanding of the crucial aspects of identifying decisions concerning women business owners while making capital investments, pertaining to running a successful business in two large and cosmopolitan cities Lahore and Karachi of Pakistan. Furthermore, analyzes the importance of influencing factors towards various long-term investments that still need attention because female business is a rising segment in the capital investor’s population that needs attention in Pakistan.

Pakistan is a nation where women entrepreneurs can play an integral role in economic development. Women entrepreneurs through this study will be encouraged and motivated to accelerate the economic status for future sustainability. Moreover, the female population running their business to form capital will invest their surplus in different productive investment projects to lead to rapid growth in the country. Resources like wealth and national income in the form of goods and services help to increase entrepreneurial activities and contribute to society as a whole. Therefore, if women actively maintain, sustain, and diversify their investment strategies so this will ultimately contribute to the economy. Furthermore, creating a trade-off between risk and return would generate more commercial activities in the foreign market. This in return will also generate revenue for the country so that the economy can utilize the funds in the capital expenditure projects and somehow produce more potential business leaders within their skills and capacities.

Hence, after reviewing the past literature. These are the following core objectives of the study; 1. to explore the investment attitude mediates with social factors and investment decisions. 2. To explore the investment attitude mediates with personal factors and investment decisions. 3. To explore the investment attitude mediates with behavioral factors and investment decisions. Moreover, the fourth objective of the study is to explore the uncertainty moderates with investment attitude and investment decisions. Likewise, this study has included women entrepreneurs who are running their business in distinct sectors of the economy, for instance, education services, event management, app services, beauty salons, food catering, tailoring business, women-owned clinics, women IT business, etc. This facilitates policymakers and government officials to understand women’s entrepreneurial empowerment for individual and family well-being in the light of cultural, economic, and institutional obstacles. The theoretical contribution derived from this study in the emerging world demonstrates women’s pervasive contributions to their families, households, and overall economic development through well-being.

2. Literature Review

Investment Decisions highly influences others’ personality, opposite or same gender, social and economic attitudes, faith, beliefs, and demographics. This helps us to understand their significant investment interest, psychology, and the influential decision-making factors. Several studies regarding behavioral finance have developed interest among various scholars and industries.

Kahneman and Tversky (

1988) criticized the theory of utility and they constructed an alternate model of prospect theory, which proved successful in the behavioral finance sphere. This success helped scholars to understand the deviation of human decisions at times of uncertainty because during unexpected and uncertain times an individual changes his/her decisions from the expected estimated outcomes employing Standard Economic Theory.

Investment Attitude comprehensively discusses the determinants of individual decisions, taken for investment purposes because investment behavior is mainly determined by the level of their financial knowledge or literacy and mathematical expertise. Several studies have pointed out numerous factors exceedingly affecting the financial decision of the investors because it is common in human nature that they don’t make rational decisions every time (

Nigam et al. 2018;

Kumar et al. 2018). The decisions which an individual takes are biased to an extent that depends on their respective personality, sex, intuitions about earning money (

Baker et al. 2018;

Chavali and Mohanraj 2016). Thus, it is a natural phenomenon that market sentiments and human personality affect long-term financial judgments. Thus, it is essential to explore what causes investors to behave in such a manner.

Behavioral Factors in Investment Decisions refers to investors being biased when they engage in investment (

Fisher and Statman 2000;

Kumar and Goyal 2015;

Godoi et al. 2005). Similarly,

Godoi et al. (

2005) discussed imperfect cognitive reasoning, emotions, or sentiments that heavily affect personal investment decisions and enforce them to make irrational financial decisions because cognitive biases are derived from flawed reasoning, time constraint, heavy responsibilities, and lack of attention. Similarly, overconfidence bias germinates when the investor overestimates their abilities of judgment and pays less attention to negative information (

Barber and Odean 1998;

Fisher and Statman 2000).

Mishra and Metilda (

2015) stressed the self-attribution bias takes place when merchants receive credit for assisting investors to reap profit, and at times of losses, they blame external factors.

Fisher and Statman (

2000);

Pompian (

2006) have also pointed out additional cognitive biases such as ambiguity-aversion, representativeness, mental-accounting, the illusion of control, authentication, framing bias, and hindsight. Hence,

Godoi et al. (

2005) emphasized emotional and loss-aversion biases that differ from expected financial conduct that is attributed to emotions based on judgments.

Kahneman and Lovallo (

1993) discussed other emotional biases such as endowment bias. Whereas,

Pompian (

2006) discussed optimism bias.

Barber and Odean (

1998) pointed out regret aversion bias.

Similarly,

Kappal and Rastogi (

2020) emphasized in their studies and confirmed that well-informed, educated, and more financially skilled people can cope up with their finances, which as a result helps to make better decisions for investment. Therefore, it becomes necessary for women entrepreneurs to be financially literate and well-equip themselves. Financial knowledge is a life skill that will raise growth in the economy and overall well-being. Scholars also assert that refined people in terms of education are more concerned about their sustainability and they carry out their capital expenses more cautiously as compared to those who are less literate or unqualified.

Social Factors in Investment Decisions observe that investment behavior is affected by a positive approach to the social environment (

Grohmann et al. 2015).

Hibbert et al. (

2004) pointed out that financial prudence demonstrated by family and parents significantly influences the financial wit of a young adult.

Kappal and Rastogi (

2020) also highlighted that financial socialization developed by parents increased investment habits in their adulthood. Besides this guidance of family, social factors such as friends, relatives, and print or digital media drive the financial decision (

Akhtar et al. 2018). Similarly, women after experiencing several years of investment differ in their attitudes and they exhibit different biases while taking investment decisions because it is observed that experienced entrepreneurs make sound capital investments and are more overconfident than those having less experience (

Mishra and Metilda 2015). Moreover, many other psychographic attributes, for instance, attitude, standards, and different lifestyles also influence financial decisions.

Tang and Baker (

2016) pointed out that individuals possessing high self-esteem will expose healthier financial behavior. Thus, it is presumed that the natives of an economy are responsible to make an adequate investment for their respective countries (

Imtiaz et al. 2019;

Lassoued et al. 2020;

Van Truong et al. 2020). Moreover,

Salim and Khan (

2020) revealed that people are more concerned about the anecdotes that affect the industry’s investment activity rather than the amendments of government rules and regulations.

According to

Salim and Khan (

2020), women make countless efforts in any activity collectively performed by them in their respective regions. Thus, scholars rightly proclaim that investment decisions are highly influenced by several psychological, social, and emotional factors of an individual investor. Thus, the key purpose that an investor possesses is to embrace a thoughtful investment activity that offers a high return on low-risk investments.

Sarkar and Sahu (

2018) investigated that people are risk-averse and they take investment decisions very cautiously that reaps sufficient return in the long term. Consistent with the above arguments women are contributing a lot in the long-term for the prosperity of the society this will ultimately help in uplifting the country’s development schemes.

Uncertainty while Investment is well defined in financial economics that an optimistic attitude of an entrepreneur is one in which he/she overestimates the possibility of worthy consequences and undervalues the possibility of undesirable consequences. Thus, this leads to a more risk-taking personal trait in financial decisions (

Kahneman and Lovallo 1993;

Heaton 2002). Owners of different businesses participate in capital expenditure and diversify their funds but they consistently make inappropriate valuations of probabilities. Sometimes individuals tend to overestimate the possibility of worthy outcomes in financial decisions (

Heaton 2002;

Camerer and Lovallo 1999;

Lee et al. 1991). Thus, this study investigates women entrepreneurs’ attitudes at the time of uncertain conditions. On contrary,

Son and Rojas (

2011) indicated that when owners fail to detect issues giving birth to faulty decisions so they do not own enough financial learning and experience. Whereas, some risk factors are relatively easier to identify, such as poor weather, delayed material delivery, scarcity of labor, inexpert labor, errors in design, change in orders, distinct site conditions whereas, factors such as organizational dynamics are difficult to detect. Thus, through the above discussion, the study examines that although women are risk-averse and possess a conservative attitude towards investment decisions, they often fail to plan the future adequately due to scarce financial knowledge, lack of training to maintain diversified funds.

The literature displays research on the underlying factors that influence women’s investment decision direct and through investment attitude considering uncertainty to find out the strengthening relationship of the conceptual framework. However, (

Arafat et al. 2020;

Marín et al. 2019;

Stefan et al. 2021;

Muhammad et al. 2021) explored that women’s businesses offer the chance to save by generating wealth and investment opportunities that contribute to their economic well-being. Furthermore, to attain business sustainability, women entrepreneurs save and invest to generate sufficient income for the future. The role of women’s businesses goes beyond their well-being to affect their families and communities. It is assumed that income generated by women’s businesses plays a crucial role in the family, economic, and societal well-being. Therefore, women must have sound knowledge to sustain themselves in the long run. Thus, The Path-Goal Theory and Prospect Theory enables an entrepreneur to become a successful leader and influence others by their actions to attain their path goals in the field of entrepreneurship whereas, Prospect Theory guides the entrepreneur especially women to frame such situations regarding profits and losses that ultimately assist her attitude towards risk. Since it is a common phenomenon that business and investing funds involve risk. The higher the risk will generate higher the profits although it requires sound financial knowledge that every entrepreneur possesses to sustain and grow substantially. Thus, motivating entrepreneurs to achieve a competitive advantage. Few studies have cogitated on how women entrepreneurs invest under these underlying factors such as social, personal, and behavioral factors together with investment attitude as a mediating variable and moderation of uncertainty between investment attitude and women investment decisions. Therefore, this study has focused in detail to the best of the investigators’ erudition. The study after reviewing the past literature proposes the following hypotheses:

Hypotheses 1 (H1). Investment Attitude mediates with Social Factors and Investment Decisions.

Hypotheses 2 (H2). Investment Attitude mediates with Personal Factors and Investment Decisions.

Hypotheses 3 (H3). Investment Attitude mediates with Behavioral Factors and Investment Decisions.

Hypotheses 4 (H4). Uncertainty moderates with Investment Attitude and Investment Decisions.

3. Methodology

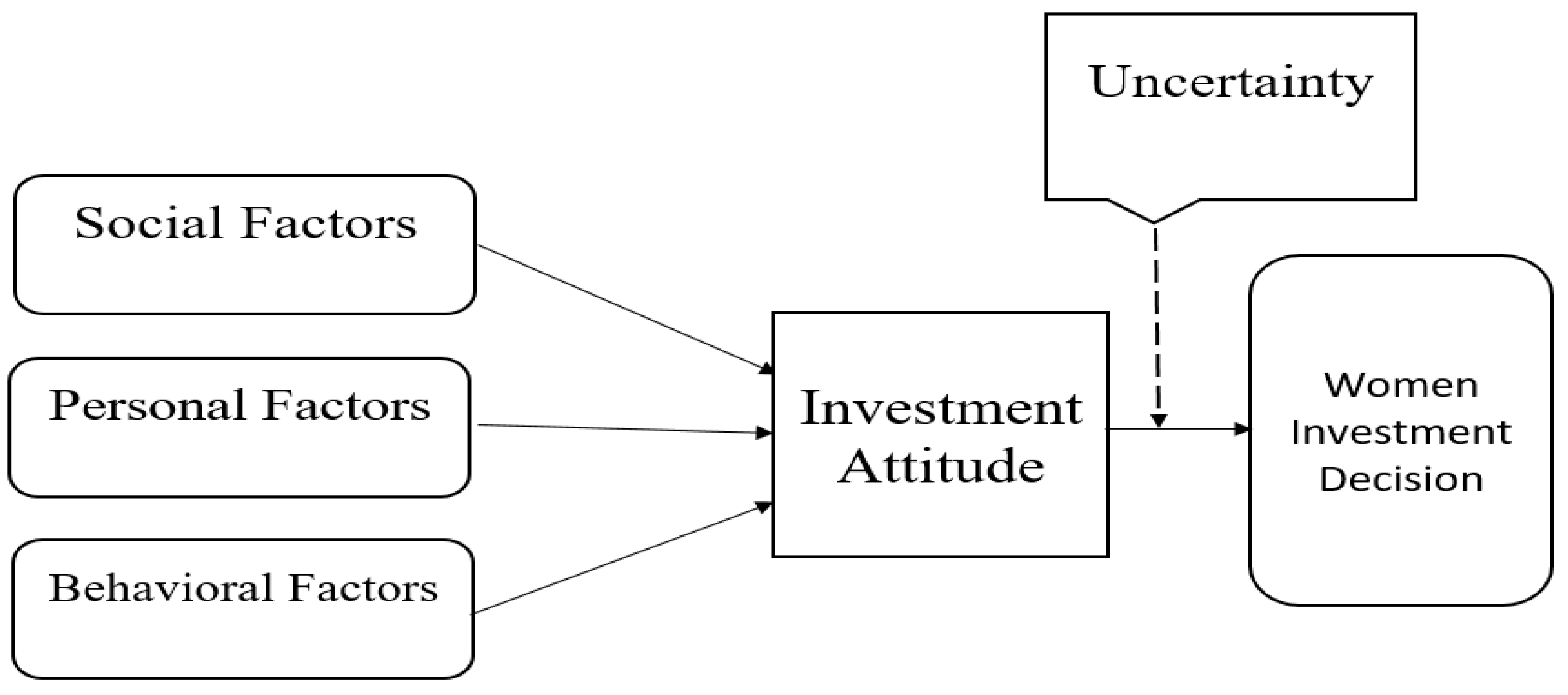

This study has adopted a deductive approach to survey potential respondents. Magazines, newspapers, articles, and journals of Web of Science were considered and read to better comprehend the current practices of Pakistani women entrepreneurs. This study collected primary data to survey the potential respondents, structural equation modeling (SEM) tabulated and critically analyzed the upcoming outcomes. The core objective of this study is to ascertain influencing factors that affect the investment attitude and final decisions of women entrepreneurs. A close-ended structured questionnaire was designed and developed, based on the literature of women entrepreneurs. The questionnaire entails two main parts where Part A covers general demographic information and Part B includes the selected items of the conceptual framework which is presented in

Figure 1 of the study. The Following proposed model is based on several sources shown in

Table 1 to support the construct and its items. The constructs of the prevailing study are measured on a Likert scale of Seven points delineated as “1 (Strongly Disagree) 2 (Disagree) 3 (Somewhat Disagree) 4 (Neither agree nor disagree) 5 (Somewhat Agree) 6 (Agree) 7 (Strongly Agree)”.

This study has incorporated women entrepreneurs executing their business in different sectors of the economy, for instance, small businesses like education services, event management, app services, beauty salons, food catering, tailoring business, women-owned clinics, women IT business. Therefore, the relevant data is accumulated from the two big cities Lahore and Karachi that lie in the region of Punjab and Sindh from the period Jan 2020–Jan 2021. The study has used a Snowball sampling technique to gather the data. This is a non-probability technique which is also called “chain-referral sampling”. It is used when the samples consist of certain traits that are rare to find. It helped us by providing referrals to enlist samples needed for our research.

A total of 800 questionnaires were circulated online, by email, and Google Form to our potential respondents out of which we just received 200 responses from Karachi and 225 from Lahore. These responses were further shortlisted. The shortlisting of the survey questionnaire helped to separate the most relevant responses as we found some responses were unengaged and most of them had missing values. Thus, in all 330 responses were incorporated and filled adequately i.e., 178 from Karachi which is 54 percent of the total selected sample, and 152 from Lahore which is 46 percent of the total sample selected in the study.

Table 2 illustrates the demographic distribution of the ultimate respondents.

5. Discussions

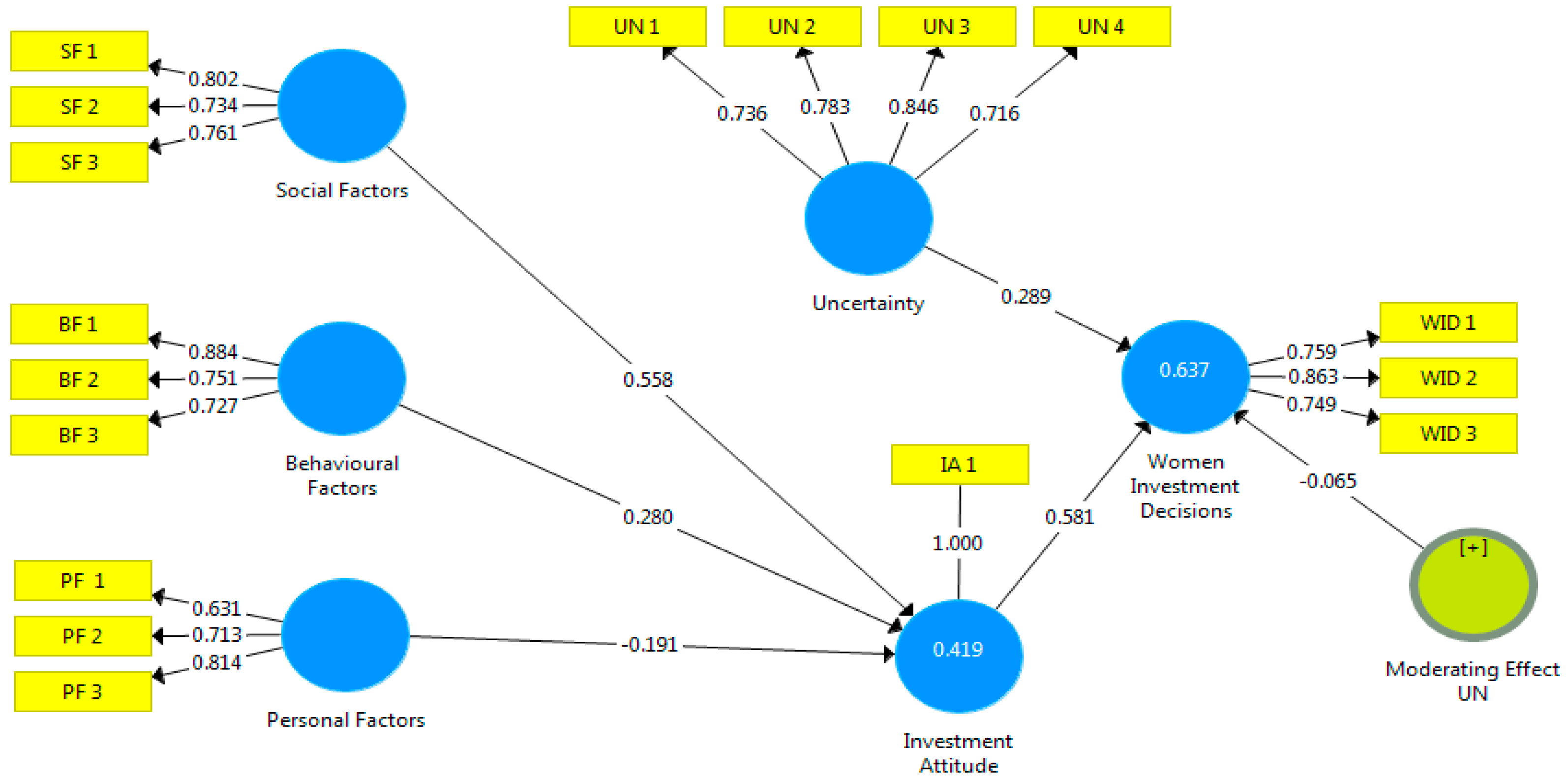

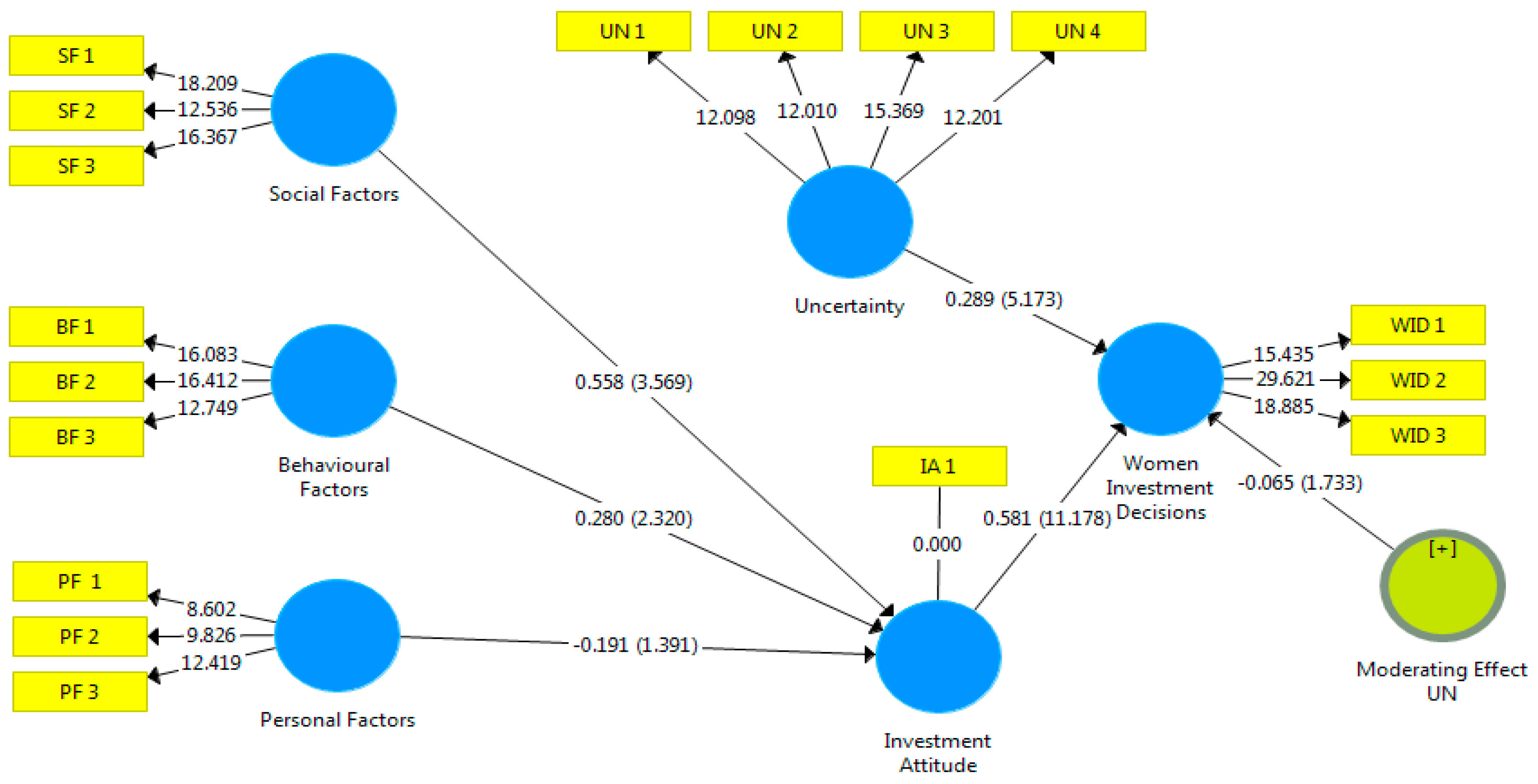

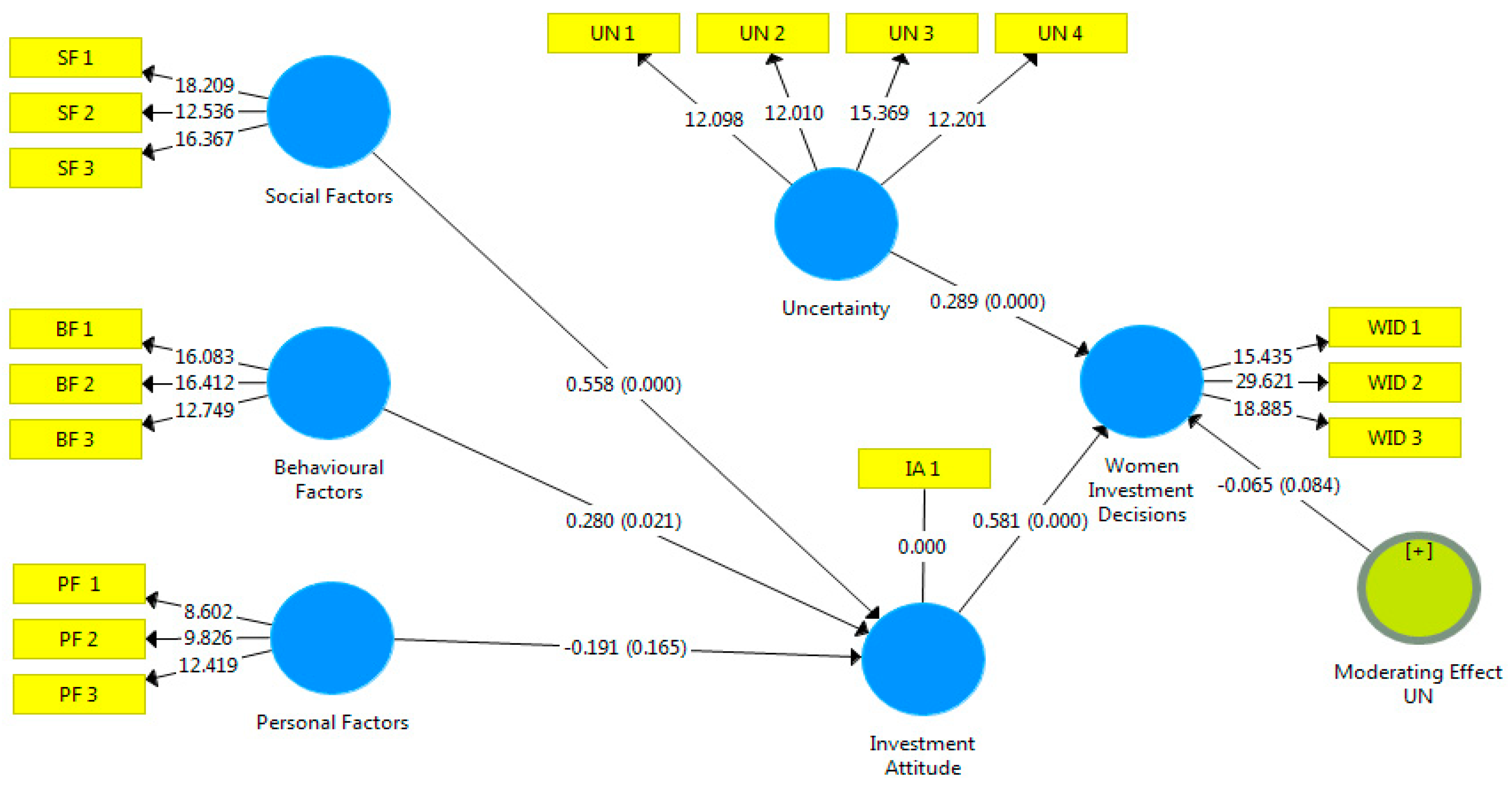

The above results significantly support H1, which implies that investment attitude, mediates with social factors and investment decisions while making long-term capital decisions. They feel more secure with those decisions, which are preferred by their parents and social network around while performing investing activities. It is contended by different scholars that family, society, or community affects the financial literacy of adults. Thus, the findings of the study reveal that women entrepreneurs select among alternatives by keeping in view the investment choices of their surroundings (

Grohmann et al. 2015). It is observed that young ones impersonate the investment behavior from their parents and the experiences of the community they belong (

Webley and Nyhus 2006) which ultimately is reinforced when they reach their maturity level. Thus, in Pakistan social norms built up their attitude and then help them to make final investment decisions in different investment projects. Similarly, Women business owners are also persuaded by the negative experiences of people around them therefore, they engage an investment advisor or consultant who assists them to best utilize their funds for the investment purpose. Thus, this helps them to diversify their long-term investment. On contrary, those who do not consult financial advisors only make traditional investments.

Correspondingly, the results of the study do not support the second hypothesis H2 as mentioned in a section of literature that inconsistency in selecting capital investment and the type of the investor’s personality will detrimentally affect its wealth. Therefore, it is essential to hire consultants who better grasp the personality and offer sound investment proposals to their potential investors (

Akhtar et al. 2018;

Brown and Taylor 2014;

Bucciol and Zarri 2017;

Mayfield et al. 2008;

Filbeck et al. 2005;

Parsaeemehr et al. 2013;

Kannadhasan et al. 2016). Since it was observed that women hold a risk-averse attitude towards investments, therefore; it becomes difficult for them to delve into risky investments because most of the owners hold a bundle of responsibility to run their families. Personality traits however vary even if they are optimistic their attitude relies on the type of circumstances. It does not matter what personal attitude she possesses the only thing matters is to earn and become independent for their survival. As far as investment decisions are concerned, they lack financial knowledge and time to spend on understanding various investment projects. Very few of them allocate their funds for capital expenditure for instance opening a new outlet or franchise but this again requires sound knowledge and consultancy. Thus, the concept of personality relies on a particular consistency of performance of an individual relating to its present and past behavior. Disparate behaviors demonstrate correspondence over time. As it is witnessed, being an entrepreneur the motivational structure of a person is rigid and constant to an extent that does not affect their leadership style otherwise they can’t carry on their business as entrepreneurs.

In contrast, the results supported the third hypothesis H3 as it was observed that women entrepreneurs are long-term investors therefore, they consider behavioral biases such as risk aversion and mental accounting. Although, they keep an optimistic approach and take risks in their business, but they avoid risks while making investment decisions. They prefer to invest in comfortable and secured projects. In Pakistan, they perceive themselves as long-term investors moreover, they utilize their surplus when they budget their expenditures. When they incur losses so they like better to wait until the next profitable investment. They do not believe to liquidate an investment in losses. It is observed that they daily re-assess their budgets. The current study witnessed three strong behavior all biases in women entrepreneurs of Karachi and Lahore city of Pakistan that greatly influence their financial investment decisions such as risk aversion, mental accounting, and optimistic approach. The respondents agreed that this will not adequately benefit them at the time of their retirement because their ultimate objective is capital appreciation (

Baig et al. 2021). Hence, it can be concluded that they are not satisfied financially by their management and planning of investment due to imperfect financial literacy. Moreover, scarce time restricts them to study and understanding various investment projects. Thus, the behavioral factors inducing the investment attitude are affected by the investment acquaintanceship and time availability for investments that eventually cause financial gratification and long-term sustainability.

Finally, the outcomes of the study do not support the fourth hypothesis H4 as the study witnessed that uncertainty varies in different situations. For instance, according to

Hsu et al. (

2017), entrepreneurs’ readiness to learn from failure changes as a function of the rate of failure so they mostly support approach-oriented appraisals by framing uncertainty or unexpected conditions as a learning opportunity. As it is observed that women are optimistic and also execute their business with more responsibility therefore, uncertain conditions also do not moderately affect their attitude and final investment decisions. They are well aware of unexpected events before their start-ups therefore, they are inclined to invest in secured investment projects and opportunities to sustain. Most of them are responsible to look after their families therefore, they hesitate to expand. Expansion in business and exploiting resources again require sound knowledge which is, unfortunately, less among women entrepreneurs. Our country, norms, culture, and traditions make them reluctant at small-scale businesses.

Griffin and Grote (

2020) also determined that uncertainty requires acquiring new and innovative information and knowledge about the changing world. This means that an entrepreneur sustains if it accepts challenges and innovations in the present to achieve reward in the future.

Thus, this study predicted that uncertainty would change the investment behavior therefore, to know the strength of the relationship among the variables the study attempted to empirically test the moderating effect. Eventually, the outcomes of the study did not depict a significant moderating effect of uncertainty between investment attitude and women’s investment decisions. In Pakistan where individuals, especially women, are habitual of several political instabilities, economic instability, and market volatility therefore, uncertain circumstances do not affect small businesses like beauty salons, food catering, tailoring business, schools, women-owned clinics, women IT business. These sectors after a survey revealed that they in case of instability especially at a time of COVID 19 were not affected by the uncertain conditions rather their businesses were running well as before.

7. Implications

The investment supervisor or manager will procure a sound insight regarding the psychology of female entrepreneurs in the field of investment. Moreover, will also enable them to progress personalized and pertinent proposals. As a result, this will also aid service facilitators to establish training institutions and different modules for women’s investment consultants to meet the needs and wants of women entrepreneurs. The policymakers and research scholars can benefit from this study as it provides a deep understanding of the factors that indirectly affect the process of women entrepreneurs’ decisions, through their investment attitude. Finally, women entrepreneurs would gain comprehensive knowledge about mitigating their prejudices, whilst corporate investments. Similarly, they will be able to draw wiser inferences, thereby lowering the risk and capitalizing on opportunities to sustain and expand their business globally.

This study will offer several opportunities to enhance gender equality among the pool of investors in society. Thus, it can be achieved if women in Pakistan are encouraged and are able to easily access proper training and education from field experts such as investment counselors or consultants. The study highly recommends well-organized workshops on investment awareness based on the outcomes of this research. Women entrepreneurs are triggering factors to start up and execute a prosperous business activity. Like men, women also possess the quality of self-actualization, hardworking, commitment, and continuous learning. They know how to exploit and employ resources productively and effectively. Thus, this study will also foster and raise different modes of qualifications by facilitating a promotion in the status of women in social activities.

{kind=link}

{kind=link}

{kind=link}

{kind=link}