Revisiting the Impact of Corporate Carbon Management Strategies on Corporate Financial Performance: A Systematic Literature Review

Abstract

:1. Introduction

- RQ1.

- What are the prevailing theories utilized to support research on corporate carbon management strategies and their impact on corporate financial performance?

- RQ2.

- What do the findings from the literature reveal concerning the relationship between carbon management strategies and financial performance from 2016 to 2022 after the Paris Agreement 2015?

- RQ3.

- Which variables and indicators are employed in quantitative studies focusing on carbon management strategies in corporate settings?

- RQ4.

- What are the motivations, drivers, and barriers influencing the adoption and outcomes of corporate carbon strategies?

- RQ5.

- (a) What potential opportunities exist for future research that could contribute to advancing the academic discourse on corporate carbon management? (b) What are the limitations inherent in the existing literature?

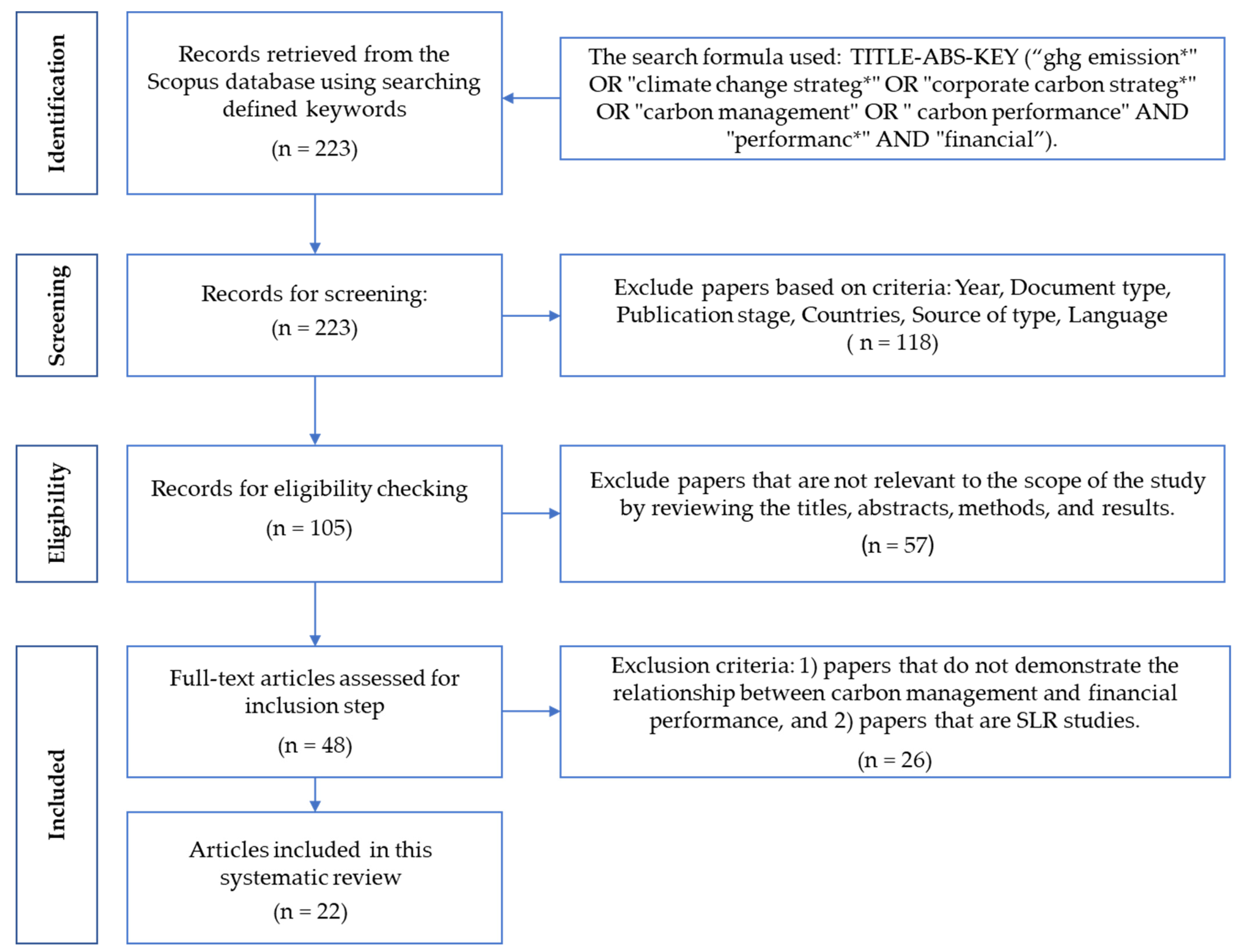

2. Methodology

- Identification: searching for all relevant articles from selected or various databases.

- Screening: selecting articles based on a defined set of criteria to include or exclude.

- Eligibility: ensure that all screened articles conform to the eligibility criteria.

- Inclusion and exclusion: making the final selection of the eligible articles for analysis.

2.1. Identification

2.2. Screening

2.3. Eligibility

2.4. Inclusion

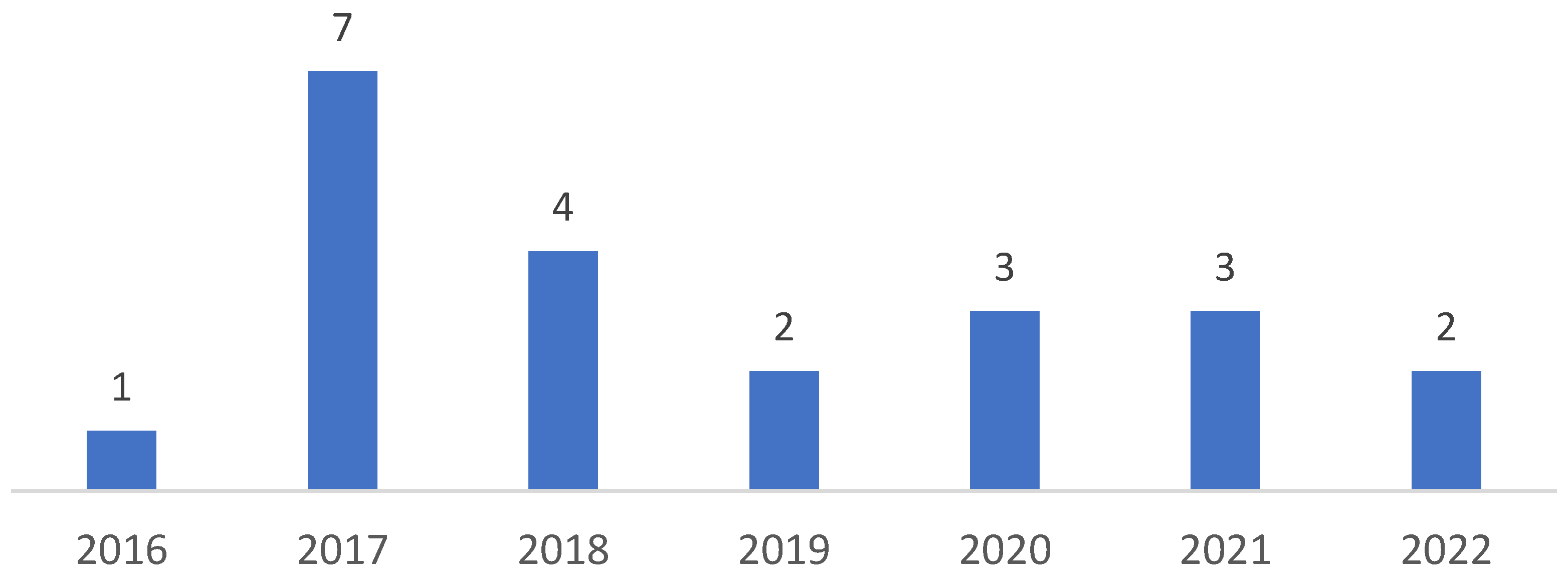

3. Results

4. Discussion

- The utilization of theories in all selected research articles.

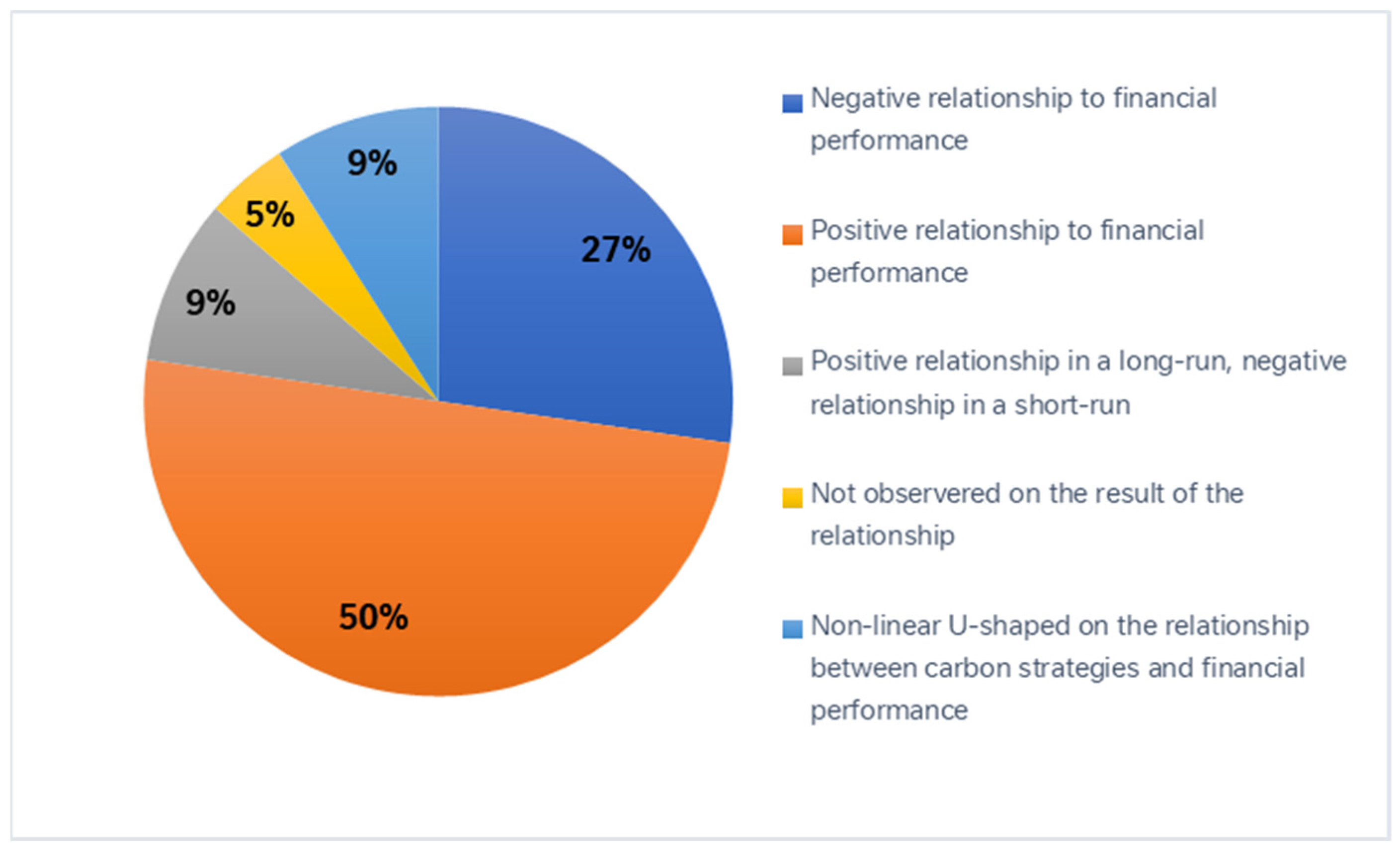

- The result obtained regarding the relationship between carbon management strategies and financial performance.

- The shared variables and indicators employed in the selected studies.

- The motivations, drivers, and barriers encountered by companies when implementing corporate carbon strategies.

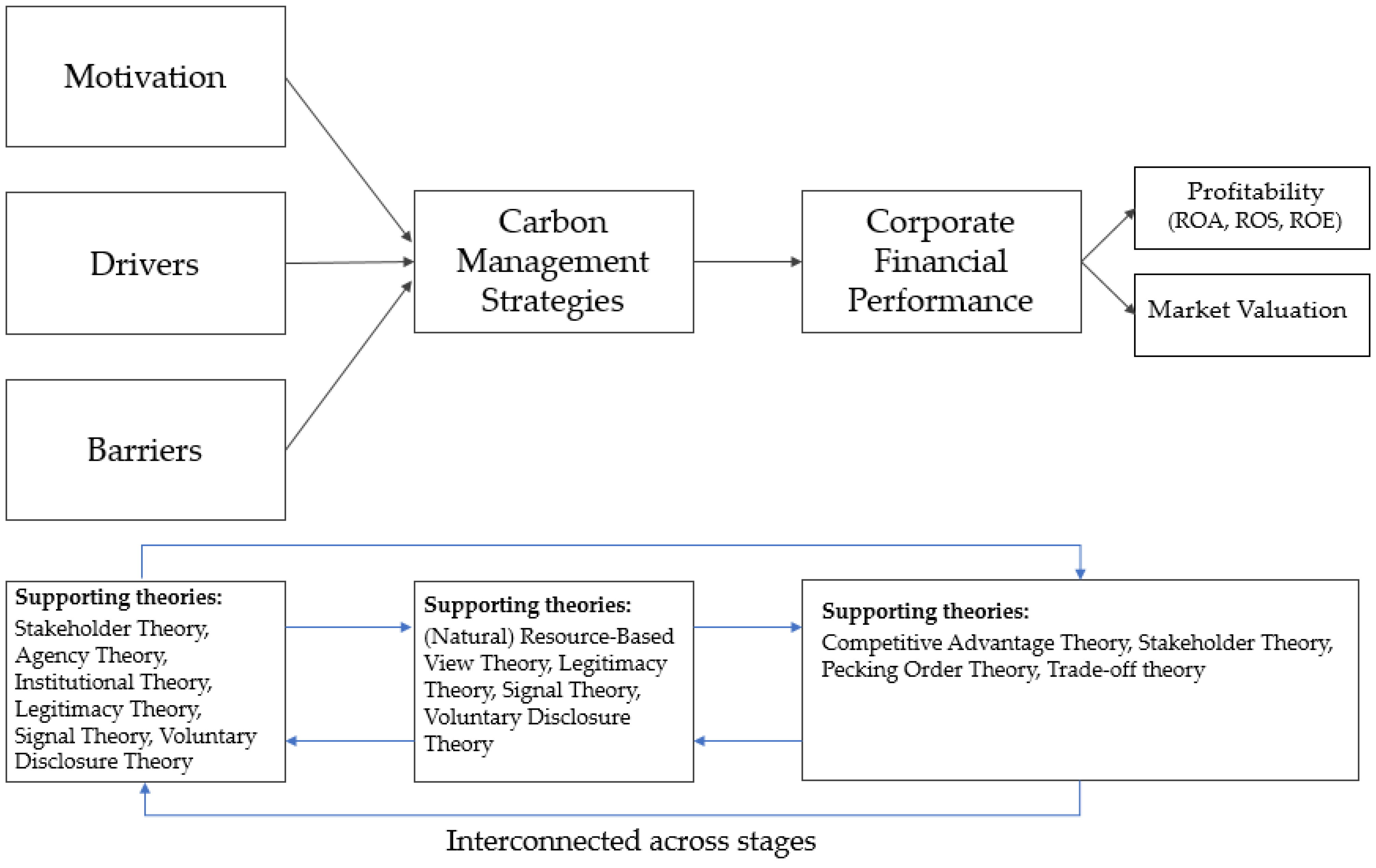

4.1. The Theories in the Literature on Carbon Management Strategy and Corporate Performance

4.2. The Relationship between Corporate Carbon Management and Financial Performance

4.3. The Variables and Indicators Used in Quantitative Research Literature Studied

4.4. The Motivations, Drivers, and Barriers to Corporate Carbon Strategies and their Outcome

5. Conclusions

5.1. The Various Brief Results and Conclusions of the Study

5.2. The Future Research Opportunities and Research Limitations

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Alsaifi, Khaled, Marwa Elnahass, and Aly Salama. 2019. Carbon disclosure and financial performance: UK environmental policy. Business Strategy and the Environment 29: 711–26. [Google Scholar] [CrossRef]

- Alves, Marcelo W. F. M., Ana Beatriz Lopes de Sousa Jabbour, Devika Kannan, and Charbel Jose Chiappetta Jabbour. 2017. Contingency theory, climate change, and low-carbon operations management. Supply Chain Management 22: 223–36. [Google Scholar] [CrossRef] [Green Version]

- Ambec, Stefan, and Paul Lanoie. 2008. Does It Pay to Be Green? A Systematic Overview. Academy of Management Perspectives 22: 45–62. [Google Scholar] [CrossRef] [Green Version]

- Backman, Charles A., Alain Verbeke, and Robert A. Schulz. 2017. The Drivers of Corporate Climate Change Strategies and Public Policy: A New Resource-Based View Perspective. Business & Society 56: 545–75. [Google Scholar] [CrossRef]

- Borghei, Zahra, Philomena Leung, and James Guthrie. 2018. Voluntary greenhouse gas emission disclosure impacts on accounting-based performance: Australian evidence. Australasian Journal of Environmental Management 25: 321–38. [Google Scholar] [CrossRef]

- Böttcher, Christian F., and Martin Müller. 2015. Drivers, practices and outcomes of low-carbon operations: Approaches of German automotive suppliers to cutting carbon emissions. Business Strategy and the Environment 24: 477–98. [Google Scholar] [CrossRef]

- Brouwers, Roel, Frederiek Schoubben, Cynthia Van Hulle, and Steve Van Uytbergen. 2016. The initial impact of EU ETS verification events on stock prices. Energy Policy 94: 138–49. [Google Scholar] [CrossRef]

- Busch, Timo, Alexander Bassen, Stefan Lewandowski, and Franziska Sump. 2022. Corporate Carbon and Financial Performance Revisited. Organization and Environment 35: 154–71. [Google Scholar] [CrossRef]

- Buysse, Kristel, and Alain Verbeke. 2003. Proactive environmental strategies: A stakeholder management perspective. Strategic Management Journal 24: 453–70. [Google Scholar] [CrossRef]

- Cadez, Simon, Albert Czerny, and Peter Letmathe. 2018. Stakeholder pressures and corporate climate change mitigation strategies. Business Strategy and the Environment 28: 1–14. [Google Scholar] [CrossRef]

- Capece, Guendalina, Francesca Di Pillo, Massimo Gastaldi, Nathan Levialdi, and Michela Miliacca. 2017. Examining the effect of managing GHG emissions on business performance. Business Strategy and the Environment 26: 1041–60. [Google Scholar] [CrossRef]

- CDP (Carbon Disclosure Project). 2017. The Carbon Majors Database: CDP Carbon Majors Report 2017. Available online: https://cdn.cdp.net/cdpproduction/cms/reports/documents/000/002/327/original/Carbon-MajorsReport-2017.pdf?1501833772 (accessed on 10 May 2023).

- Climate Impact Partners. 2023. If Not Now, When? How are Companies Stepping Up with the Urgency Required to Deliver Climate Impact. Available online: https://info.climateimpact.com/hubfs/IfNotNowWhen_FortuneGlobal500_ClimateImpactPartners_2022.pdf (accessed on 2 June 2023).

- Damert, Matthias, and Rupert J. Baumgartner. 2018. Intra-Sectoral Differences in Climate Change Strategies: Evidence from the Global Automotive Industry. Business Strategy and the Environment 27: 265–81. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Damert, Matthias, Arijit Paul, and Rupert J. Baumgartner. 2017. Exploring the determinants and long-term performance outcomes of corporate carbon strategies. Journal of Cleaner Production 160: 123–38. [Google Scholar] [CrossRef]

- de Sousa Jabbour, Ana B. L., Charbel J. C. Jabbour, Joseph Sarkis, Angappa Gunasekaran, Marcelo W. F. M. Alves, and Daniela A. Ribeiro. 2018. Decarbonisation of operations management—Looking back, moving forward: A review and implications for the production research community. International Journal of Production Research 57: 4743–65. [Google Scholar] [CrossRef]

- Derwall, Jeroen, Nadja Guenster, Rob Bauer, and Kees Koedijk. 2005. The eco-efficiency premium puzzle. Financial Analysts Journal 61: 51–63. [Google Scholar] [CrossRef] [Green Version]

- Dhanda, Kanwalroop K., and Mahfuja Malik. 2020. Carbon management strategy and carbon disclosures: An exploratory study. Business and Society Review 125: 225–39. [Google Scholar] [CrossRef]

- Fernández-Cuesta, Carmen, Paula Castro, María T. Tascón, and Francisco J. Castaño. 2019. The effect of environmental performance on financial debt. European evidence. Journal of Cleaner Production 207: 379–90. [Google Scholar] [CrossRef]

- Ganda, Fortune. 2018. The effect of carbon performance on corporate financial performance in a growing economy. Social Responsibility Journal 14: 895–16. [Google Scholar] [CrossRef]

- Ganda, Fortune. 2022. Carbon performance, company financial performance, financial value, and transmission channel: An analysis of South African listed companies. Environmental Science and Pollution Research 29: 28166–79. [Google Scholar] [CrossRef]

- Gao, Shang, Fanchen Meng, Zhouyang Gu, Zhiyuan Liu, and Muhammad Farrukh. 2021. Mapping and Clustering Analysis on Environmental, Social and Governance Field a Bibliometric Analysis Using Scopus. Sustainability 13: 7304. [Google Scholar] [CrossRef]

- Gerged, Ali M., Lane Matthews, and Mohamed Elheddad. 2020. Mandatory disclosure, greenhouse gas emissions and the cost of equity capital: UK evidence of a U-shaped relationship. Business Strategy and the Environment 30: 908–30. [Google Scholar] [CrossRef]

- Gramkow, Camila, and Annela Anger-Kraavi. 2019. Developing Green: A Case for the Brazilian Manufacturing Industry. Sustainability 11: 6783. [Google Scholar] [CrossRef] [Green Version]

- Hang, Markus, Jerome Geyer-Klingeberg, and Andreas W. Rathgeber. 2019. It is merely a matter of time: A meta- analysis of the causality between environmental performance and financial performance. Business Strategy and the Environment 28: 257–73. [Google Scholar] [CrossRef]

- He, Yu, Qingliang Tang, and Kaitian Wang. 2016. Carbon performance versus financial performance. China Journal of Accounting Studies 4: 357–78. [Google Scholar] [CrossRef]

- Herrera-Franco, Gricelda, Néstor Montalván-Burbano, Paúl Carrión-Mero, Boris Apolo-Masache, and María Jaya-Montalvo. 2020. Research Trends in Geotourism: A Bibliometric Analysis Using the Scopus Database. Geosciences 10: 379. [Google Scholar] [CrossRef]

- Hoffman, Andrew J. 2005. Climate Change Strategy: The Business Logics Behind Voluntary Greenhouse Gas Reductions. California Management Review 47: 21–46. [Google Scholar] [CrossRef]

- ICAP (International Carbon Action Partnership). 2023. Indonesia Launches Emissions Trading System for Power Generation Sector. Available online: https://icapcarbonaction.com/en/news/indonesia-launches-emissions-trading-system-power-generation-sector (accessed on 2 June 2023).

- IMF (International Monetary Fund, Asia and Pacific Dept). 2022. Indonesia: Selected Issues. Indonesia’s Transition Toward a Greener Economy—Carbon Pricing and Green Financing. International Monetary Fund 2022: 62. [Google Scholar] [CrossRef]

- IPCC (Intergovernmental Panel on Climate Change). 2021. Climate Change 2021, Summary for Policymaker. Intergovernmental Panel on Climate Change. Available online: https://www.ipcc.ch/report/ar6/wg1/downloads/report/IPCC_AR6_WGI_SPM.pdf (accessed on 15 November 2022).

- IPCC (Intergovernmental Panel on Climate Change). 2023. Climate Change 2023, Summary for Policymaker. A Report of the Intergovernmental Panel on Climate Change. Available online: https://www.ipcc.ch/report/ar6/syr/downloads/report/IPCC_AR6_SYR_SPM.pdf (accessed on 15 November 2022).

- Ismail, Siti N., Azizan Ramli, and Hanida A. Aziz. 2021. Research trends in mining accidents study: A systematic literature review. Safety Science 143: 105438. [Google Scholar] [CrossRef]

- Jayasundara, Susantha, David Worden, Alfons Weersink, Tom Wright, Andrew VanderZaag, Robert Gordon, and Claudia Wagner-Riddle. 2019. Improving farm profitability also reduces the carbon footprint of milk production in intensive dairy production systems. Journal of Cleaner Production 229: 1018–28. [Google Scholar] [CrossRef]

- Kayan-Fadlelmula, Abdellatif Sellami, Nada Abdelkader, and Salman Umer. 2022. A systematic review of STEM education research in the GCC countries: Trends, gaps and barriers. International Journal of STEM Education 9: 1–24. [Google Scholar] [CrossRef]

- Kolk, Ans, and Jonatan Pinkse. 2007. Towards strategic stakeholder management? Integrating perspectives on sustainability challenges such as corporate responses to climate change. Corporate Governance 7: 370–78. [Google Scholar] [CrossRef]

- Kumar, Anupam. 2018. Environmental Reputation: Attribution from Distinct Environmental Strategies. Corporate Reputation Review 21: 115–26. [Google Scholar] [CrossRef]

- Lee, Su-Yol. 2012. Corporate carbon strategies in responding to climate change. Business Strategy and the Environment 21: 33–48. [Google Scholar] [CrossRef]

- Lewandowski, Stefan. 2017. Corporate carbon and financial performance: The role of emission reductions. Business Strategy and the Environment 26: 1196–211. [Google Scholar] [CrossRef]

- Liberati, Alessandro, Douglas G. Altman, Jennifer Tetzlaff, Cynthia Mulrow, Peter C. Gøtzsche, John P. A. Ioannidis, Mike Clarke, P. J. Devereaux, Jos Kleijnen, and David Moher. 2009. The PRISMA statement for reporting systematic reviews and meta-analyses of studies that evaluate healthcare interventions: Explanation and elaboration. Annals of Internal Medicine 151: 65–94. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Michalisin, Michael D., and Bryan T. Stinchfield. 2010. Climate Change Strategies and Firm Performance: An Empirical Investigation of The Natural Resource-Based View of The Firm. Journal of Business Strategies 27: 123–49. [Google Scholar] [CrossRef]

- Mishra, Deepa, Angappa Gunasekaran, Thanos Papadopoulos, and Benjamin Hazen. 2017. Green Supply Chain Performance Measures: A Review and Bibliometric Analysis. Sustainable Production and Consumption 10: 85–99. [Google Scholar] [CrossRef]

- Moher, David, Alessandro Liberati, Jennifer Tetzlaff, and Douglas G. Altman. 2009. Preferred Reporting Items for Systematic Reviews and Meta-Analyses: The PRISMA Statement. Annals of Internal Medicine 151: 264–70. [Google Scholar] [CrossRef] [Green Version]

- Nishitani, Kimitaka, Nurul Jannah, Shinji Kaneko, and Hardinsyah. 2017. Does corporate environmental performance enhance financial performance? An empirical study of indonesian firms. Environmental Development 23: 10–21. [Google Scholar] [CrossRef]

- Okereke, Chukwumerije. 2007. An Exploration of Motivations, Drivers and Barriers to Carbon Management: The UK FTSE 100. European Management Journal 25: 475–86. [Google Scholar] [CrossRef]

- Orsato, Renato J. 2006. Competitive Environmental Strategies: When does it pay to be green? California Management Review 48: 127–43. [Google Scholar] [CrossRef] [Green Version]

- Qian, Wei, Ani Suryani, and Ke Xing. 2020. Does carbon performance matter to market returns during climate policy changes? Evidence from Australia. Journal of Cleaner Production 259: 121040. [Google Scholar] [CrossRef]

- Rokhmawati, Andewi, and Ardi Gunardi. 2017. Is Going Green Good for Profit? Empirical Evidence from Listed Manufacturing Firms in Indonesia. International Journal of Energy Economics and Policy 7: 181–92. Available online: https://www.proquest.com/openview/d96bf2fadb0bcc8ec55c5e9cba9ed6cc/1?pq-origsite=gscholar&cbl=816340&casa_token=vj25AEE4ceMAAAAA:E5JM6nnc8Ug-btlstLku0nkIwuS1pvdUKTtMnbLyRB_-FySMb7G455NI-vr0aFlEElmhdXw66sT8 (accessed on 20 November 2022).

- Rokhmawati, Andewi, Ardi Gunardi, and Matteo Rossi. 2017. How Powerful is Your Customers’ Reaction to Carbon Performance? Linking Carbon and Firm Financial Performance. International Journal of Energy Economics and Policy 7: 85–95. Available online: https://www.researchgate.net/profile/Andewi-Rokhmawati/publication/321824734_How_Powerful_is_Your_Customers’_Reaction_to_Carbon_Performance_Linking_Carbon_and_Firm_Financial_Performance/links/5a336679458515afb691692d/How-Powerful-is-Your-Customers-Reaction-to-Carbon-Performance-Linking-Carbon-and-Firm-Financial-Performance.pdf (accessed on 20 November 2022).

- Schultz, Karl, and Peter Williamson. 2005. Gaining Competitive Advantage in a Carbon-constrained World: Strategies for European Business. European Management Journal 3: 383–91. [Google Scholar] [CrossRef]

- Siddique, Md A., Md Akhtaruzzaman, Afzalur Rashid, and Helmi Hammami. 2021. Carbon disclosure, carbon performance and financial performance: International evidence. International Review of Financial Analysis 75: 101734. [Google Scholar] [CrossRef]

- Slawinski, Natalie, Jonatan Pinkse, Timo Busch, and Subhabrata B. Banerjee. 2017. The Role of ShortTermism and Uncertainty Avoidance in Organizational Inaction on Climate Change: A Multi-Level Framework. Business & Society 56: 253–82. [Google Scholar] [CrossRef]

- Tahat, Yasean A., and Ghassan H. Mardini. 2021. Corporate carbon disclosure, carbon performance and corporate firm performance. International Journal of Sustainable Economy 13: 219–35. [Google Scholar] [CrossRef]

- Trumpp, Christoph, and Thomas Guenther. 2017. Too Little or too much? Exploring U-shaped Relationships between Corporate Environmental Performance and Corporate Financial Performance. Business Strategy and the Environment 26: 49–68. [Google Scholar] [CrossRef]

- Tuesta, Yenny N., Cristina C. Soler, and Vicente R. Feliu. 2020. The Influence of Carbon Management on the Financial Performance of European Companies. Sustainability 12: 4951. [Google Scholar] [CrossRef]

- Tuesta, Yenny N., Cristina C. Soler, and Vicente R. Feliu. 2021. Carbon management accounting and financial performance: Evidence from the European Union emission trading system. Business Strategy and the Environment 30: 1270–82. [Google Scholar] [CrossRef]

- UNFCCC (United Nations Framework Convention for Climate Change). 2015. Paris Agreement. United Nations Framework Convention for Climate Change. Available online: https://unfccc.int/sites/default/files/english_paris_agreement.pdf (accessed on 15 November 2022).

- Wahyudi, Indra, Arif I. Suroso, Bustanul Arifin, Rizal Syarief, and Meika S. Rusli. 2021. Multidimensional Aspect of Corporate Entrepreneurship in Family Business and SMEs: A Systematic Literature Review. Economies 9: 156. [Google Scholar] [CrossRef]

- Weinhofer, Georg, and Volker H. Hoffmann. 2010. Mitigating climate change: How do corporate strategies differ? Business Strategy and the Environment 19: 77–89. [Google Scholar] [CrossRef]

- Wójcik-Jurkiewicz, Magdalena, Marzena Czarnecka, Grzegorz Kinelski, Beata Sadowska, and Katarzyna Bilińska-Reformat. 2021. Determinants of Decarbonisation in the Transformation of the Energy Sector: The Case of Poland. Energies 14: 1217. [Google Scholar] [CrossRef]

- Yagi, Michiyuki, and Shunsuke Managi. 2018. Decomposition analysis of corporate carbon dioxide and greenhouse gas emissions in Japan: Integrating corporate environmental and financial performances. Business Strategy and the Environment 27: 1476–92. [Google Scholar] [CrossRef]

- Yunus, Somaiya, Evangeline O. Elijido-Ten, and Subhash Abhayawansa. 2020. Impact of stakeholder pressure on the adoption of carbon management strategies: Evidence from Australia. Sustainability Accounting, Management and Policy Journal 11: 1189–212. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Criteria | Inclusion | Exclusion |

|---|---|---|

| Year published | From 2016 to 2022 | Outside of 2016–2022 |

| Document type | Article | Book Chapter, Conference Paper, Abstract Report, Review, Letter, Conference Review. |

| Publication stage | Final | Article in Press |

| Country/territory | All countries | |

| Source type | Journal | Proceeding of Conference, Book, Trade Journal, Book Series. |

| Language | English | Non-English |

| Source of Journal | Number of Articles | Quartiles | SJR 2021 |

|---|---|---|---|

| Business Strategy and the Environment | 7 | Q1 | 2.24 |

| Journal of Cleaner Production | 4 | Q1 | 1.92 |

| Environmental Development | 1 | Q1 | 0.91 |

| Environmental Science and Pollution Research | 1 | Q1 | 0.83 |

| International Review of Financial Analysis | 1 | Q1 | 0.83 |

| Organization and Environment | 1 | Q1 | 1.62 |

| Social Responsibility Journal | 1 | Q1 | 0.63 |

| Sustainability (Switzerland) | 1 | Q1 | 0.66 |

| International Journal of Energy Economics and Policy | 2 | Q2 | 0.38 |

| Australasian Journal of Environmental Management | 1 | Q2 | 0.44 |

| China Journal of Accounting Studies | 1 | Q3 | 0.28 |

| Grand Total | 22 |

| Countries Studied | Frequency |

|---|---|

| Multi-countries | 5 |

| European Union countries | 4 |

| Indonesia | 3 |

| Australia | 2 |

| South Africa | 2 |

| United Kingdom | 2 |

| Canada | 1 |

| Italy | 1 |

| Japan | 1 |

| USA | 1 |

| Industry Sector | Frequency | Percentage |

|---|---|---|

| Automotive | 1 | 4.5% |

| Dairy farming | 1 | 4.5% |

| Manufacturing | 4 | 18% |

| Multi-industries | 16 | 73% |

| Grand Theories | Authors |

|---|---|

| Agency theory | Fernández-Cuesta et al. (2019); Tuesta et al. (2021) |

| Pecking order theory | Fernández-Cuesta et al. (2019) |

| Trade-off theory | Fernández-Cuesta et al. (2019) |

| Institutional theory | Damert et al. (2017); Damert and Baumgartner (2018); Ganda (2018); Tuesta et al. (2021) |

| Stakeholder theory | Damert et al. (2017); Rokhmawati and Gunardi (2017); Lewandowski (2017); Trumpp and Guenther (2017); Ganda (2018); Siddique et al. (2021); Tuesta et al. (2021) |

| Natural resource-based view theory | He et al. (2016); Lewandowski (2017); Trumpp and Guenther (2017); Tuesta et al. (2021) |

| Resource-based view theory | Borghei et al. (2018); Alsaifi et al. (2019) |

| Legitimacy theory | He et al. (2016); Ganda (2018); Tuesta et al. (2021); Siddique et al. (2021) |

| Signal theory | He et al. (2016); Siddique et al. (2021); Damert et al. (2017) |

| Voluntary disclosure theory | Siddique et al. (2021); Tahat and Mardini (2021) |

| Competitive advantage theory | Rokhmawati and Gunardi (2017) |

| Authors | Independent | Dependent | Controls | Correlations | Year Sample | Number of Samples | ||

|---|---|---|---|---|---|---|---|---|

| Variables | Indicators | Variables | Indicators | |||||

| (Busch et al. 2022) | Corporate carbon performance | Total GHG Emissions for direct and indirect scopes | Financial performance | ROA | Growth, size, leverage, capital insensitive. | Negative | 2005–2014 | 27,986 firm-year, 4873 companies |

| (Ganda 2022) | Carbon performance | Carbon performance | Financial performance | Return on assets, firm values, Tobin’s Q | Debt-to-equity ratio, interest cover, price-to-cash flow, and current ratio | Positive in a long run, negative in a short run | 2014–2018 | 107 firms |

| (Siddique et al. 2021) | Carbon performance | Carbon disclosure scores; Carbon performance | Financial performance | ROA, Tobin’s Q | Firm age, firm size, capital intensity, leverage, earnings quality, Stock liquidity and carbon intensity | Positive in a long run, negative in a short-run | 2011–2015 | 187 firms |

| (Tuesta et al. 2021) | Total emissions, the ratio of emissions, direct emissions, indirect emissions, environmental certificate | Tons of CO2 reported, emission/sales, tons of direct emissions, tons of indirect emissions | Tobin’s Q | (Market value + liquidation value share + current liabilities + long-term debt)/total assets | Growth, size, leverage, capital intensities, age | Negative | 2007–2018 | 350 firms |

| (Tahat and Mardini 2021) | Carbon performance | Corporate carbon disclosure score, carbon emissions (Scope 1, 2, 3) | Financial performance | ROA, ROE | Size, liquidity, leverage, growth, and dividends per share | Positive | 2015–2018 | 116 firms |

| (Alsaifi et al. 2019) | Carbon disclosure | Financial Performance | ROA, ROE, asset turnover, debt to equity ratio, interest coverage, return volatility, cost of equity, price earnings ratio, market to book ratio. | Firm size, leverage, market competition, foreign market activities, board size | Positive | 2007–2015 | 977 firm years | |

| (Qian et al. 2020) | Environmental performance | Carbon Performance, Industry Sensitivity (IndSen), Environment Sensitivity (NGER) | Financial performance | Cumulative Abnormal Stock Returns (CARs) | Market capitalization, market to book value, growth rate, | Positive | 2009–2010 2011 2013–2014 | 1475 firms for the ETS event 1672 firms for carbon tax events 1842 firms for repeal of carbon tax events |

| (Tuesta et al. 2020) | Carbon management measures | Score emissions, emissions, variation of emissions, carbon performance | Financial performance | ROA, ROE, ROS | Global Reporting Initiative, variation in property, plant, and equipment, growth, market share, leverage, size, operational expenses, type of legislation. | Negative | 2006–2017 | 497 firms |

| (Fernández-Cuesta et al. 2019) | Environmental performance | Carbon performance | Financial debt | Sales, profitability, investment intensity | Profitable, size, tangible assets, non-debt tax shields, R&D expenses, firm age, liquidity, and the corporate tax rate in each country | Negative | 2005–2012 | 4223 firm year, 428 firms |

| (Jayasundara et al. 2019) | Carbon footprint | GHG emissions | Financial performance | Profit | None | Negative | 2010–2012 | 182 farms |

| (Damert and Baumgartner 2018) | Emissions reduction | Governance, innovation, compensation, legitimation | Financial performance | ROA, ROE | Firm size, financial performance | Not observed | 2013–2014 | 117 firms |

| (Yagi and Managi 2018) | Corporate Environmental Performance (CEP) | Carbon intensity, energy intensity | Corporate Financial Performance (CFP) | ROA | TATR, leverage, firm size | Positive | 2011–2015 | 225 firms |

| (Borghei et al. 2018) | GHG Disclosure | GHG Disclosure Score | Financial performance | ROA, ROE, ROS | Age, firm size, leverage, enterprise value, and capital intensity. | Positive | 2009–2011 | 290 firms |

| (Ganda 2018) | Carbon performance | CP Rating | Financial Performance | ROE, ROI and ROS, Market Valuation | Firm size, capital intensity, leverage, growth | Positive | 2014–2015 | 63 firms |

| (Trumpp and Guenther 2017) | CEP | Carbon performance, waste intensity | CFP | TSR, ROA | R&D intensity, capital intensity, leverage, growth, cash flow, company size, legal origin | Non-linear U-shaped relationship | 2008–2012 | 1179 firm years |

| (Lewandowski 2017) | Carbon performance | Carbon performance (CO2 intensity) | Financial performance | Profitability (ROA, ROE, ROS, ROIC), market performance (Tobin’s Q) | Firm size, risk or leverage, sales growth, capital intensity, cash flow | Non-linear U-shaped relationship | 2003–2015 | 7625 firm-years (1640 firms) |

| (Damert et al. 2017) | Carbon performance | Carbon intensity, Carbon exposure | Financial performance | ROA, ROE | Company size | Negative | 2008–2013 | 45 firms |

| (Nishitani et al. 2017) | Environmental performance | GHG emissions reduction, pollution emissions reduction | Financial performance | Profit growth, sales increase, productivity improvement. | Firm size, type of firm, market orientation, supply chain area, type of industry | Positive | 2009 | 100 firms |

| (Rokhmawati et al. 2017) | GHG emissions | Intensity of CO2 | Financial performance | Return on Sales (ROS) | Firm size, leverage, capital intensity | Positive | 2010–2011 | 134 firms |

| (Capece et al. 2017) | Environmental performance | CO2 emissions | Economic performance | ROI | Positive | 2008–2013 | 237 firms, 1422 firm-years | |

| (Rokhmawati and Gunardi 2017) | GHG emissions | Carbon intensity | Financial performance | ROE, ROI, ROS, Tobin’s Q | Firm size, leverage, capital intensity, industry type | Positive | 2011 | 102 firms |

| (He et al. 2016) | Carbon performance | Carbon emissions/sales value, carbon disclosure index | Financial performance | Tobin’s Q, ROA | Financing activities, leverage and firm size, capital intensity, sales growth, age of equipment, industry indicators, and year indicators. | Positive | 2007–2010 | 620 firms |

| Determinant Aspects | Detailed Practices |

|---|---|

| Motivation | Gain profitability Reduce operational costs Reduce business risks Enhance reputation and brand image Responsibility to mitigate the risk of climate change Credibility to leverage in climate policy development Ethical consideration Developing market opportunities Achieving competitive advantage |

| Drivers | Energy prices and costs Market shifts Regulation and government directions. Investors’ pressure Financial institutions’ pressures Customer/consumers expectations Technological shift and innovation Business competition Carbon Tax and financial penalties |

| Barriers | Lack of strong policy framework Uncertainty about the government’s action and regulation Lack of law enforcement on compliance Uncertainty about the marketplace Short-term profit maximization Lack of leadership commitment |

| Strategies | Corporate carbon policy and measurement Product innovation Process innovation Logistics improvement Energy efficiency initiatives Switching to renewable energy Planting trees and conservation New market and product development Participation in emissions trading scheme Carbon compensation through carbon credits |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Sitompul, M.; Suroso, A.I.; Sumarwan, U.; Zulbainarni, N. Revisiting the Impact of Corporate Carbon Management Strategies on Corporate Financial Performance: A Systematic Literature Review. Economies 2023, 11, 171. https://doi.org/10.3390/economies11060171

Sitompul M, Suroso AI, Sumarwan U, Zulbainarni N. Revisiting the Impact of Corporate Carbon Management Strategies on Corporate Financial Performance: A Systematic Literature Review. Economies. 2023; 11(6):171. https://doi.org/10.3390/economies11060171

Chicago/Turabian StyleSitompul, Maruli, Arif Imam Suroso, Ujang Sumarwan, and Nimmi Zulbainarni. 2023. "Revisiting the Impact of Corporate Carbon Management Strategies on Corporate Financial Performance: A Systematic Literature Review" Economies 11, no. 6: 171. https://doi.org/10.3390/economies11060171