1. Introduction

The relationship between expenditures and company performance has been previously studied by researchers (

Öztürk and Zeren 2015;

Huang et al. 2009;

Verma et al. 2022;

Kim 2001;

Peterson and Jeong 2010;

Lantz and Sahut 2005;

Tuhin 2014;

Sueyoshi and Goto 2009;

Rafiq et al. 2016;

Oware and Mallikarjunappa 2022;

Liao et al. 2016). Since these studies investigated this relationship generally, the current study sought to investigate the relationship between financial performance, accounting, and advertising expenditure. Furthermore, it investigated how liquidity influences the relationship between accounting expenditure, advertising expenditure, and financial performance, which is the main contribution addressed in this study, particularly during the COVID-19 pandemic, which can have an impact on this relationship during this critical era, as the ILO report

1 indicated that medium and small businesses in Jordan were among the most affected during the pandemic.

In a market, advertising is regarded as a major instrument for raising sales and enhancing the recognition of products and services (

Park and Jang 2012). Despite the significant effect of advertising on the performance of firms, there has been some disagreement among marketing and accounting/finance researchers (

Wang and Zhang 2008;

Park and Jang 2012;

Peterson and Jeong 2010). Expenditure on advertising assists in marketing the products and services of financial institutions, boosts bank cash flows, and is regarded as an investment for maximizing wealth (

Chen 2020). In order to reap future financial rewards possibly affecting a company’s success, advertising expenses may be compounded over a longer period of time (

Meyer and Ujah 2017). However, scant actual data are available regarding the financial performance of firms’ advertising expenditures (

Mulchandani et al. 2019).

In 2020, the Jordanian economy suddenly faced a stifling economic crisis as a result of the closure of trading in the Amman Stock Exchange for the first time (

AL-Zararee et al. 2022). On the seventh of March 2020, the Jordanian borders and airports were closed, and citizens were prohibited from leaving their homes due to the COVID-19 pandemic. This resulted in an economic disaster and increased the unemployment rate in Jordan. Therefore, companies felt at risk of continuity, especially SMEs (

Al-Sawalqa 2020). As a result of the COVID-19 pandemic, many SMEs stumbled and exited the market and failed to continue their economic activity. Despite the gradual opening of markets, companies are looking for other ways and solutions for enhancing their continuity to support their financial performance, provide cash, and improve investment in multiple economic activities (

Alduais 2022), especially in light of the severe competition in global markets and the Jordanian market. In order to measure the size of SMEs, the researchers relied on the study of

AL-Tamimi and Jaradat (

2019), which was based on measuring the number of employees, with small companies having 1–19 employees and medium companies having 20–99 employees. The current article focuses on the SME industry and aims to identify the effect of advertising and accounting concentration on the performance of SMEs in the environment of emerging markets such as Jordan.

Our study differs from previous studies in the following ways: Firstly, most previous studies were limited to examining the relationship between accounting and advertising expenditures and financial performance without addressing liquidity. Our study attempts to analyze the relationship above through the introduction of liquidity as a moderating variable. Secondly, most of the time horizon of the previous studies was in the course of normal conditions, whereas the current study analyzes the relationship in the course of unique conditions, including the COVID-19 pandemic, which is most appropriate to capture the effects of liquidity in exceptional circumstances. Medium and small businesses are improving circulars. Since medium and small businesses were the most affected during the pandemic and the most sensitive to the liquidity variable, our sample size is much larger than previous studies so that a more representative sample is obtained. It should also be noted that there is a gap in the current literature regarding the analysis of the relationship between liquidity and the impact of accounting and advertising expenditures on financial performance, which this study attempts to address especially with the given mixed results of the current literature. To the best of the authors’ knowledge, no previous study has investigated the moderating influence of liquidity on the relationship between the expenditures and financial performance of SMEs in Jordan. Thus, the present study is the first to carry out this investigation. The vast majority of empirical studies examined the connections between spending on advertising and financial measures, and spending on research and development and financial metrics (

Acar and Temiz 2017;

Sridhar et al. 2014).

The theoretical contribution in the current study is the moderating variable (liquidity) which is considered to a vital role in analyzing how it influences the relationship between IVS (accounting and advertising expenses) and DV (financial performance). Because the majority of studies that evaluate the independent and dependent variables are limited, the study will provide information on this relationship in the context of unnatural events and disasters. Furthermore, the researchers are not aware of any studies that investigate the association while also considering the moderating variable. In terms of practical consequences, this study presents incisive empirical evidence suggesting that considerable accounting and advertising expenditures will result in significant financial performance of SMEs based on a new moderator variable called liquidity.

In terms of practical implications, the current study assists policymakers in SMEs in maintaining ongoing concerns, as well as dealing with future financial difficulty and crisis management. The number of SMEs has risen to 95,000, with over 630,000 employees and workers. They contribute more than 55% of the state budget via taxes and fees. The practical contribution presented by ongoing-concern SMEs will help the Jordanian economy grow and reduce unemployment rates, especially given that these businesses account for more than 99.5% of all economic establishments operating in Jordan and contribute more than 35% of the GDP, according to Bulletin 2022 issued by the Amman Chamber of Industry.

2Moreover, the current study provides new insights into the relationship between liquidity as a moderator variable, its impact on financial performance, and its impact on accounting and marketing expenditures. The positive impact of liquidity on the financial performance of SMEs in this study is inconsistent with other empirical literature (

Abbas et al. 2019;

Adusei 2022;

Hassan et al. 2019;

Acharya and Naqvi 2012). The study also indicates the positive effect of liquidity on the relationship between accounting and advertising expenditures and financial performance, in addition to highlighting the importance of managing expenditures and enhancing financial performance. Liquidity is the capability of firms to finance asset growth and meet incurred obligations. From the perspective of growth and in the face of expanded competition, there will be a need to enhance operational efficiency through effective cash and liquidity management (

Bayer et al. 2020;

Wuave et al. 2020). The role of liquidity in SME performance has risen significantly recently. Liquidity risk is increasingly included among the key potential risks that affect the survival of the company (

Osoro and Muturi 2015).

According to

Jensen (

1986), the cash flow hypothesis which posits that increased free cash flows exacerbate agency costs does not support the direct positive impact of liquidity on financial performance. As SMEs’ self-serving tendencies increase, shareholder value is ultimately destroyed. The study illustrates that companies are likely to benefit from holding higher liquidity. Furthermore, this study proceeds from the theoretical argument of

Acharya and Naqvi (

2012) and

Adusei (

2022).

Acharya and Naqvi (

2012) contended that excess liquidity results in an improvement in financial performance. Our findings indicated that the accounting expenditures, moderated by liquidity, have a remarkable positive effect on the financial performance of small and medium enterprises. Furthermore, as SMEs increase their expenditures on accounting services to enhance their accounting quality, their earnings have increased. There is evidence that when advertising expenditures increase among small- and medium-sized companies in Jordan, financial performance suffers, regardless of liquidity levels. Moreover, contrary to popular belief, the study demonstrates that investing in high-quality accounting services is a better strategy in times of crisis than focusing on advertising expenditures.

The present study is organized as follows: The literature review and hypothesis development are presented in

Section 2. The methodology is discussed in

Section 3. Results and data analysis are given in

Section 4. The discussion is in

Section 5. Finally,

Section 6 presents the conclusion.

2. Literature Review and Hypothesis Development

Several relevant theories can be identified. Agency theory, which focuses on the relationship between principals and agents and their impact on organizational performance, may be useful in exploring how accounting and advertising expenditures can be utilized to align the interests of managers and owners and improve financial performance (

Jensen and Meckling 1976).

Resource-based theory suggests that a firm’s resources can be a source of sustained competitive advantage and superior performance. In the context of this paper, it may be relevant in exploring how accounting and advertising expenditures can be used to acquire and develop resources that can improve financial performance (

Barney 1991).

Signal theory suggests that advertising can be used as a signal to convey information about a firm’s quality or attributes to its stakeholders. In the context of this paper, it may be relevant in exploring how advertising expenditures can be used to signal the quality or attributes of a firm and influence its financial performance (

Spence 1978).

Liquidity theory examines the relationship between a firm’s ability to meet its short-term financial obligations and its financial performance (

Deloof 2003). In the context of this paper, it may be relevant in exploring how liquidity can moderate the relationship between accounting and advertising expenditures and the financial performance of SMEs in Jordan (

Opler and Titman 1994).

COVID-19 has negatively affected the financial performance of SMEs due to closures, reduced working hours, reduced workforce, and reduced wages and salaries.

Abu-Mater et al. (

2021) asserted that most expenditures of SMEs include operating costs, supply of materials, overhead costs, and staffing. This study considers other different expenditures, including accounting and advertising expenditures as the independent variables in order to examine the relationship with the dependent variable (financial performance) in this particular exceptional circumstance to explore this association.

This is the case in the Jordanian economy, as evidenced by the economic growth derived from industrial SMEs in Jordan (

Alawaqleh 2021). Due to their large number, small- and medium-sized businesses have been selected for this study.

Cicea et al. (

2019) demonstrated that various factors influence the financial performance of small and medium enterprises. Such factors include the availability and adequacy of quality accounting and advertisement services. However,

Yoshino (

2016) revealed that limited resources for investment in quality accounting services have continuously affected the financial performance of small and medium enterprises.

Yoshino (

2016) also indicated that most small and medium enterprises overlook the importance of accounting services in generating revenue for enterprises.

In this study, four hypotheses will be studied regarding the relationship of the dependent variable with the independent and the moderating role, which is liquidity.

2.1. Accounting Expenditures and Financial Performance

Abdul-Rahamon and Adejare (

2014) defined accounting as the process of generating, organizing, and keeping financial records of a business in order to ensure proper business management. Furthermore, the researchers stated that accounting plays a critical role in tracking expenditures and income, ensuring statutory compliance, and providing statistical data for the generation of business policies. Additionally, a smooth synchronization of all the above functions results in improved business performance.

Kamau (

2015) assessed the use of accounting services by small and medium enterprises in Kenya, a developing country. The researcher noted that accounting was the foundation upon which modern business society is based. The researcher also observed that accurate record-keeping provided background data upon which businesses planned, predicted outcomes, and made sound future plans to avoid business failure for sustainable growth. Moreover, the study indicated that it was difficult for businesses to foresee profitability and risks involved in various business ventures without quality accounting. Finally, the study found that expenditure on accounting services was greatly limited among small and medium enterprises, and consequently, financial performance was seriously affected.

Ackah and Vuvor (

2011) researched the challenges faced by small and medium enterprises in obtaining credit in Ghana. The researchers concluded that poor accounting significantly contributed to the challenges small and medium enterprises face in accessing financial assistance. In turn, poor financing led to poor business outcomes, evidenced by low sales. These findings were also supported by

Husin and Ibrahim (

2014), who analyzed the role of accounting services and their effect on small and medium enterprises.

Husin and Ibrahim (

2014) concluded that firms investing in quality accounting services have significantly fewer cases of business stagnation, lack of credit, failure, and illiquidity, in comparison with those that do not.

A report issued by the United Nations Conference on Trade and Development

3 also indicated that a large percentage of small- and medium-sized companies have a high disappearance rate in the early years. In this regard, McKinsey and the International Finance Corporation

4 highlighted the need for improved financial infrastructure such that the financial infrastructure comprises several accounting expenses, including credit reporting systems, guarantee and insolvency systems, and payment and settlement systems. The improvement of the financial infrastructure reduces the lack of transparency and legal uncertainties responsible for increasing the risks of lenders, in addition to higher access to finance, improved relations with microfinance institutions, and reduced exit of medium and small companies from the market.

Previous research on the relationship between accounting expenditure and business performance has generally highlighted the positive relationship between the two variables (

Kamau 2015;

Ackah and Vuvor 2011;

Husin and Ibrahim 2014). This means that higher levels of accounting expenditure are typically associated with better business performance. For instance, a study by

Kamau (

2015) illustrated the significant relationship between accounting expenditure and business performance in SMEs in Kenya. Similarly, a study by

Ackah and Vuvor (

2011) demonstrated that accounting expenditure was positively related to business performance in SMEs in Ghana. However, it is worth noting that these studies did not necessarily establish a causal relationship between accounting expenditure and business performance. There could be other factors contributing to both the level of accounting expenditure and the business performance of firms.

This analysis will focus on determining whether there is a significant relationship between accounting expenditure and the financial performance of SMEs, as evidenced by sales. Therefore, the first hypothesis is stated as follows:

Hypothesis 1 (H1). There is a significant relationship between accounting expenditures and the financial performance of SMEs in Jordan.

2.2. Advertising Expenditures and Financial Performance

According to

Murphy and Zimmerman (

1993), advertising is an expensed investment in which the benefits of the investment may not be fully realized during the year of expenditure.

Molla and Rahaman (

2022) defined advertising expenditures as the cost incurred by issuing a certain product promotion exercise in order to develop brand awareness and increase brand loyalty. Efficient advertising should incorporate effective media mix strategies so that messages concerning products are delivered to the end consumer efficiently.

Gupta and Steenburgh (

2008) stated that successful product promotion also depends on the optimal allocation of resources for advertisement. An adequate budget should be allocated for advertising services (

Rotfeld 2007).

Amin (

2021) asserted that small and medium enterprises that command only a small section of the market should increase their advertising expenditure in order to increase their competitive advantage and expand their market share. Several scorers have undertaken research to identify the nature of the relationship between advertising expenditure and business performance.

According to

Doraszelski and Markovich (

2008), market conditions and needs are frequently changing, and therefore, creativity in selling is required among small and medium enterprises. Adapting to the changing market dynamics calls for specialized production fitting customer needs and ensuring effective product promotion.

Frolova (

2014) noted that production followed by effective advertisement increases the response in consumption of a product, hence indicating a relationship between advertisement and sales performance.

Baack et al. (

2016) stated that organizations advertise to familiarize the market with their products, hence creating confidence in the product. Moreover, the study found that the more a firm spends on expenditure, the more the demand is for their products, and consequently, the more sales are made. However,

Preda and Furdui (

2009) observed that small and medium enterprises either spend too little on advertisement or spend relatively large percentages of their revenue on product promotion, thus affecting the profitability of their firms. Furthermore,

Kurt et al. (

2021) encouraged enterprises to employ advertising to mitigate the negative effects of warranty payment hikes and to aggressively communicate warranty payment reductions in the face of increased competition.

Lee et al. (

1996) analyzed the causal relationship between sales and advertising. The researchers found a two-way causal relationship between the two variables. The first notion was that advertising influences the purchase behavior of consumers, hence affecting sales. The second notion from the study claimed that sales and profits were key determinants of advertising budget, such that if profits were low, the budget for advertising would consequently be minimal. However, the second causality was criticized in the findings of

Leach and Reekie (

1996), who insisted that there exists a causal relationship between sales and advertising expenditure, such that the amounts spent on advertisement affect the number of sales generated. Furthermore, while advertising spending has a positive, long-term impact on a firm’s market capitalization, it may have a negative impact on the valuation of a competitor of comparable size (

Joshi and Hanssens 2010). Previous research has generally determined a positive relationship between advertising expenditure and business performance. For instance,

Sundarsan (

2007) indicated a positive causal relationship between sales and advertising expenditure in the context of different company sizes.

Acar and Temiz (

2017) also found a significant and positive association between advertising expenses and financial performance. Likewise,

Sharpe and Hanson (

2018) demonstrated that advertising spending, especially product-oriented advertising spending, significantly reduced the negative impact of negative corporate social performance on the performance of firms.

However, some studies have disputed the existence of a causal relationship between sales and advertisement in the long run.

Simester et al. (

2009) indicated that although advertising undoubtedly influences sales, the causal relationship between them was not always positive in the long run, which confirms the findings of

Molla and Rahaman (

2022). The findings reveal that the economic benefits of advertising expenditures completely end within the current period and should be treated as an expense as it does not bring any future return to Bangladeshi banks. Furthermore, a study by

Xu et al. (

2019) confirmed that research, development, and advertising expenditures negatively affect the financial performance of small businesses in Korea. The literature suggested that increased advertising expenditure results in an increased level of annual sales revenue in a business. This conclusion is based on the studies by

Sharpe and Hanson (

2018),

Baack et al. (

2016),

Sundarsan (

2007),

Acar and Temiz (

2017),

Simester et al. (

2009),

Molla and Rahaman (

2022), and

Xu et al. (

2019). Therefore, the second hypothesis for this study is stated as follows:

Hypothesis 2 (H2). Increased advertising expenditure increases the level of financial performance among SMEs in Jordan.

2.3. Liquidity and Financial Performance

According to

Bhunia (

2010), liquidity is the ability of a firm to finance its short-term obligations or to easily convert its assets into cash without suffering a loss. Liquidity is a critical aspect that SME managers should consider as one of their major duties.

Bhunia (

2010) argued that firms need to maintain a constant balance of liquidity since companies that maintain high liquidity are likely to be profitable up to a definite optimal point, after which any additional liquidity reduces financial performance. Therefore, it is noted that the management of SMEs is often faced with the dilemma of increasing profitability at the expense of liquidity.

Bhunia (

2010) recommended a balance between these two objectives of a financial entity.

Additionally, access to financial resources for obtaining adequate liquidity is the key impediment to the growth of small- and medium-sized businesses. Banks regarded SMEs as a source of risk and a threat to their stability in this regard. Because SMEs lack adequate collateral, no specialized financial services are available to them (

Kharabsheh and Gharaibeh 2022).

The Jordanian economy is facing failure among SMEs due to the COVID-19 pandemic. The closures in Jordan paralyzed the cash flows of companies, resulting in an increase in financial burdens and the exposure of numerous companies to failure (

Al-Ajlouni 2020). SMEs in Jordan faced financial liquidity problems during the pandemic, leading to the rise of contentious discussions by policymakers about SMEs’ financing. As a result of this crisis, the banks worked to schedule corporate loans until the end of 2020, and the Central Bank of Jordan worked to inject liquidity into banks with an amount of JOD 550 million. This resulted in a reduction in the mandatory cash reserve on bank deposits from 7% to 5% (

Central Bank of Jordan 2021), in addition to increasing loan tenors and volume limits, allowing banks to reschedule loans and postpone loan repayments due from SMEs, lowering the cost and expanding the coverage of Jordan Loan Guarantee Corporation guarantees on SME loans (these loans are 85% guaranteed), and requesting banks to postpone dividend payments (to retain earnings and strengthen their capital base). Some measures were extended in 2021: the CBJ expanded its subsidized lending schemes for SMEs, and the bank loan service suspension for negatively impacted borrowers was extended until the end of 2021. These policies significantly affected the availability of financing, especially for SMEs (

European Investment Bank 2022).

Antonios (

2015) emphasized that SMEs in all countries, if compared to large companies, are financially frustrated due to the lack of access to official financing.

Antonios (

2015) noted that SMEs mainly depend on internal financing from the owners’ retained earnings and loans, thus limiting their cash flows and consequently their financial performance. Therefore, liquidity is a key factor in creating cash flows for the success and continuity of these companies.

Hyz (

2011) illustrated that the Greek banks issued bureaucratic procedures such as asking for guarantees and implementing complicated sanctions related to financing. These complex procedures complicated the financing process, thus creating liquidity problems among SMEs.

Carbó-Valverde et al. (

2016) presented critical global evidence indicating the suffering of SMEs from high credit during the financial crises.

Our top priority is to ensure that SMEs can pay their bills without undue stress in the short term. In order to measure liquidity, the present study utilizes ratios focusing on current assets and current liabilities. In the short term, creditors are particularly interested in liquidity ratios. Current assets and liabilities have the advantage that their book and market values are likely to be similar. Current ratio will be utilized for measuring liquidity. This ratio is one of the best known and most widely utilized, and it is defined as follows:

In Jordan, uncertainty and capital controls resulted in a reduction in sales among SMEs, which negatively affected the financial performance of these companies in terms of profitability. The financial stability report published by the Central Bank of Jordan confirmed that the reduction in liquidity had a detrimental effect on medium and small businesses, especially in terms of profitability (

Central Bank of Jordan 2020).

Various theories have been advanced to analyze the impact of liquidity on financial performance. Although it is noted that high liquidity can be considered a characteristic of a well-performing firm,

Kontuš and Mihanović (

2019) outlined that high liquidity ratios can be as harmful to a firm as low ones. This is because, in some instances, high liquidity could mean that a firm is maintaining high liquidity at the expense of increased investments for improved financial performance. On the other hand,

Durrah et al. (

2016) encouraged high liquidity as it enables a firm to carry out its day-to-day activities such as paying for expenses more efficiently, hence ensuring effective service delivery, an ingredient of improved financial performance.

Antonios (

2015) observed that SMEs are among the most affected institutions when it comes to maintaining a healthy liquidity ratio.

Kharabsheh and Gharaibeh (

2022),

Al-Ajlouni (

2020),

Kontuš and Mihanović (

2019),

Durrah et al. (

2016),

Carbó-Valverde et al. (

2016), and

Central Bank of Jordan (

2020) demonstrated that liquidity is a crucial factor in the financial performance of SMEs and that reducing liquidity can negatively affect financial performance. These studies generally suggested that liquidity is a serious consideration for SMEs and that it is essential for businesses to maintain sufficient levels of liquidity in order to ensure their financial stability and performance.

Numerous studies in the literature have found a positive relationship between liquidity and financial performance. For instance, a study by

Fama et al. (

1995) illustrated that companies with higher liquidity ratios (e.g., the current ratio or quick ratio) tend to have higher returns on assets and higher market-to-book ratios in the United States. Similarly, a study by

Rajan and Zingales (

1995) demonstrated that companies with higher liquidity ratios have higher returns on assets and higher market valuations in a sample of manufacturing firms in several countries. These studies, as well as many others, suggested that companies with high levels of liquidity tend to be more financially stable and capable of generating better financial performance. However, it is worth noting that the relationship between liquidity and financial performance can be complex and may vary based on the specific circumstances of a company and the industry in which it operates.

Other studies in the literature found a negative relationship between liquidity and financial performance. For instance, a study by

Al-Mashari et al. (

2003) indicated that companies with higher levels of liquidity tend to have lower profitability and return on assets in the manufacturing sector in Saudi Arabia. Likewise, a study by

Chava and Jarrow (

2004) showed that companies with higher liquidity had lower returns on assets in the retail industry in the United States. However, it is worth noting that these studies are not necessarily representative of all industries or all countries, and the relationship between liquidity and financial performance can vary based on the specific circumstances of a company and the industry in which it operates. Other studies indicated a positive or no significant relationship between liquidity and financial performance, so it is crucial to consider the limitations and context of individual studies when evaluating this relationship.

Some studies in the literature also found no significant relationship between liquidity and financial performance. For instance, a study by

DeAngelo and DeAngelo (

2006) showed no significant relationship between liquidity measures (e.g., the current ratio and quick ratio) and financial performance measures (e.g., return on assets and return on equity) in a sample of publicly traded companies in the United States. Similarly, a study by

Sahyouni and Wang (

2019) found no significant correlation between liquidity creation and return on average assets (ROAA) for MENA banks. These studies suggested that there may not be a straightforward relationship between liquidity and financial performance and that other factors including operational efficiency, market demand, and the overall economic environment may also influence a company’s financial performance. It is worth noting that the relationship between liquidity and financial performance can be complex and may vary depending on the specific circumstances of a company and the industry in which it operates. Therefore, the third hypothesis for this study is formulated as follows:

Hypothesis 3 (H3). There is a positive significant relationship between liquidity and the financial performance of SMEs in Jordan.

2.4. Accounting and Advertising Expenditure with Liquidity

A mutually advantageous relationship exists between accounting and advertising expenditure and liquidity.

Thomas et al. (

2014) found a negative relationship between liquidity and capital structure. In addition,

Anderson (

2002), in their study of British companies, found a positive relationship between leverage and liquidity. According to

Sibilkov (

2009), liquid assets increase a company’s leverage and debt. With respect to this finding, it was suggested that organizations with more liquid and reversible assets are more leveraged (

Šarlija and Harc 2012).

Keynes (

1936), in the Keynesian theory of money, outlined the transaction motive as one of the key reasons for ensuring liquidity. The transaction motive refers to the need to maintain liquidity in order to easily settle a firm’s recurrent transactions. Firms need to have reliable liquidity ratios in order to efficiently spend on advertising and invest in quality accounting services. According to Keynes, the transaction motive is directly proportional to the level of income, indicating that companies with low and medium incomes, such as SMEs, have lower liquidity ratios. With reduced liquidity, SMEs face several challenges in executing their expenditure on key necessities including advertisement and accounting. Moreover, SMEs may face other challenges such as deferred market expansions and difficulty in wage payments.

According to

Deloof and Jegers (

1996), liquidity levels have an indirect impact on profitability and return on assets by influencing the expenditure levels within an organization. Many studies have examined the relationship between accounting and advertising expenditures and financial performance in isolation from liquidity (

Mulchandani et al. 2019). However, it is also essential to consider the moderating effect of liquidity on this relationship. Moreover, there is a scarcity of studies exploring the moderating role of liquidity as regards the relationship between accounting and advertising expenditures and financial performance. This could be an interesting area for further research, as understanding the role of liquidity in this relationship could provide firms with insights into how to allocate their resources in order to enhance their financial performance effectively.

It may be useful for future research to consider both the direct and indirect effects of accounting and advertising expenditures on financial performance and the moderating role of liquidity in this relationship. This could provide a more complete picture of the factors influencing financial performance and how they interact with one another. Therefore, the fourth hypothesis for this study is stated as follows:

Hypothesis 4a (H4a). Liquidity has a moderating effect on the relationship between accounting expenditures and the financial performance of SMEs in Jordan.

Hypothesis 4b (H4b). Liquidity has a moderating effect on the relationship between advertising expenditures and the financial performance of SMEs in Jordan.

3. Methodology

The aim of this study is to identify whether there is a significant relationship between the independent variables (IVs), namely accounting and advertising expenditures, and the dependent variable (DV), namely SMEs’ financial performance. Moreover, the study investigates the impact of the moderator variable (liquidity) on the relationship between the IVs and DV. This paper is based on descriptive statistics, regression, and correlation analysis in order to analyze the data, collecting secondary data from 200 SMEs.

3.1. Data Collection and Sample

The utilized data present annual sales revenue, liquidity, and accounting and advertising expenditures (all in JOD 1000s) for a sample of 200 small and medium enterprises in Jordan during the period from 3 March 2020 to 29 April 2021. According to the statistics of the Department of Statistics in Jordan, the number of small and medium enterprises reached 95,000 enterprises. The current study used just 200 enterprises due to the limitations of access to financial information for all SMEs. This analysis utilized a quantitative approach due to the nature of the publicly available cross-sectional data.

Cheng and Phillips (

2014) stated that secondary data is cost- and time-efficient and can be relied upon since it is collected, organized, and cleansed by experts.

3.2. Statistical Analysis Method

This analysis was conducted through the use of the Jamovi 2.2.5 software and Excel spreadsheet in order to determine the relationship between the dependent and independent variables, as well as the effect of the moderator variable on the relationship between the IVs and DV (

The Jamovi Project 2021;

Core Development Team 2021). An empirical study will be carried out through the use of panel data collected from SMEs in Jordan (Jordanian Ministry of Industry and Trade, 2022, and Amman Stock Exchange).

Albers (

2017) defined quantitative research as the process of collecting and analyzing numerical data through the use of mathematical and statistical computations in order to draw conclusions about a research hypothesis. The study will conduct a correlation analysis between each one of the independent variables (accounting and advertising expenditure) and the dependent variable, namely the financial performance of SMEs in Jordan.

Pandis (

2016) stated that regression and correlation analyses are the most straightforward methods for analyzing relationships between variables.

A regression analysis of the variables will also be conducted in order to establish the nature of the relationship between them and to identify the effect size of the moderator variable (liquidity) on the relationship between the IVs and DV.

Ali and Younas (

2021) demonstrated that regression models are useful for assessing the relationship between study variables, especially in cases with a significant correlation between the independent and the dependent variables. The main objective of conducting regression analysis is to predict changes in the dependent variable caused by changes in one or all the independent variables. Moderating variables are included in a regression for evaluating any significant links between the dependent and the independent variables.

Therefore, a researcher’s aim in constructing a reliable regression analysis is to ensure that the obtained coefficients for each independent variable are significantly different from zero. This ensures that changes in independent variables significantly affect the value of the dependent variable.

Ali and Younas (

2021) outlined that it is crucial to ensure that any apparent differences from zero in the coefficients are not randomly developed on a scale of probability. In constructing regression analysis, the null hypothesis is stated as follows: “There is no effect caused by the independent variable on the dependent variable”. The tests usually target rejecting the null hypothesis if the regression is to hold.

3.3. Measure

The current study targets establishing whether there is a significant relationship between accounting and advertising expenditures and business financial performance. The study also aims to identify the impact of the moderator variable on the relationship between the IVs and DV.

Table 1 presents the variables utilized in the study, in addition to their definition for the purposes of this study.

3.4. Model and Estimation Technique

In the first regression model where financial performance is the dependent variable and accounting expenditure and advertising expenditure are the independent variables, the goal is to understand the relationship between financial performance and these two variables. This type of model can be utilized for identifying the extent to which changes in accounting expenditure and advertising expenditure are associated with changes in financial performance. It can also be utilized for predicting financial performance based on the values of the independent variables.

In the second regression model where financial performance is the dependent variable and accounting expenditure and advertising expenditure moderated by liquidity are the independent variables, the goal is to understand the relationship between financial performance and these two variables, taking into consideration the moderating effect of liquidity. This type of model can be utilized for identifying the extent to which changes in accounting expenditure and advertising expenditure are associated with changes in financial performance and how this relationship is affected by the presence or absence of liquidity. It can also be utilized for predicting financial performance based on the values of the independent variables and the level of liquidity.

4. Results and Data Analysis

This data analysis section presents the computations aimed at establishing the relationship between financial performance as the dependent variable and accounting and advertising expenditure as the independent variables, in addition to the effect of the moderator variable (liquidity) on the relationship between the IVs and DV. The data utilized in this analysis were collected from a sample of 200 SMEs in Jordan.

4.1. Descriptive Statistics

Mishra et al. (

2019) outlined that the aim of using descriptive statistics in research is to present data in a summarized and meaningful way such that a researcher can analyze and observe any outstanding trend elements in the data. However, it is not possible to draw meaningful inferences about the research hypotheses from descriptive statistics. A researcher can only visualize ways of interpreting the data, given its most outstanding characteristics shown in descriptive statistics. Some of the most commonly used descriptive statistics include the median, standard deviation, mean, range, variance, maximum, skewness, minimum, ex. Kurtosis, interquartile range, and coefficient of variation.

Summary statistics for the data utilized in the current study are shown in

Table 2.

4.2. Correlation

This study conducted a correlational analysis to determine the nature of the relationship between financial performance, accounting expenditure, and advertising expenditure. It also examined the effect of liquidity as a moderator variable on the relationship between the IVs and DV. Correlation coefficient outputs normally range between negative one and positive one, with values near zero indicating a weak linear relationship. The sign of the obtained coefficient is a key element for a researcher to observe. Correlation coefficients are calculated for accounting expenditure relative to financial performance and for advertising expenditure relative to financial performance, and the results are illustrated in the correlation matrices below.

Table 3 presents the correlation coefficients observed for accounting expenditure, advertising expenditure, and liquidity in relation to the dependent variable, financial performance (FP), with values of 0.073, 0.049, and 0.008, respectively. All the coefficients are positive and not significant, indicating a direct relationship between the independent variables, the moderator variable, and the dependent variable. A weak positive correlation exists between the variables. That is why the present study suggests employing the moderation method. A weak positive correlation between two variables implies a relatively small relationship between the two variables. This means that as the value of one variable increases, the value of the other variable also tends to increase, but only to a small extent. In this case, it may be useful to consider using a moderating variable that helps illustrate or clarify the relationship between the two primary variables of interest. Moderating variables can assist in explaining why the relationship between two variables is stronger or weaker under certain conditions and can provide valuable insights into the complexity of the relationship between the two variables. It is vital to carefully consider the appropriateness of using a moderating variable in a particular study, as it can help in providing a more nuanced understanding of the relationship between the primary variables of interest.

The correlation coefficient observed between financial performance (annual sales revenue), accounting expenditure (ACC), and advertising expenditure (ADV) is positively not significant. However, it is worth noting that correlation does not necessarily imply causation (

Liang and Yang 2021). A correlation coefficient that is not significantly positive suggests no strong relationship between the two variables being studied. This means that changes in one variable do not tend to be accompanied by corresponding changes in the other variable. In this case, it may be difficult to draw conclusions about the relationship between financial performance and accounting expenditure based on these data. It is essential to carefully consider other factors that could potentially affect the relationship between these variables, including the liquidity of the firms being studied. In

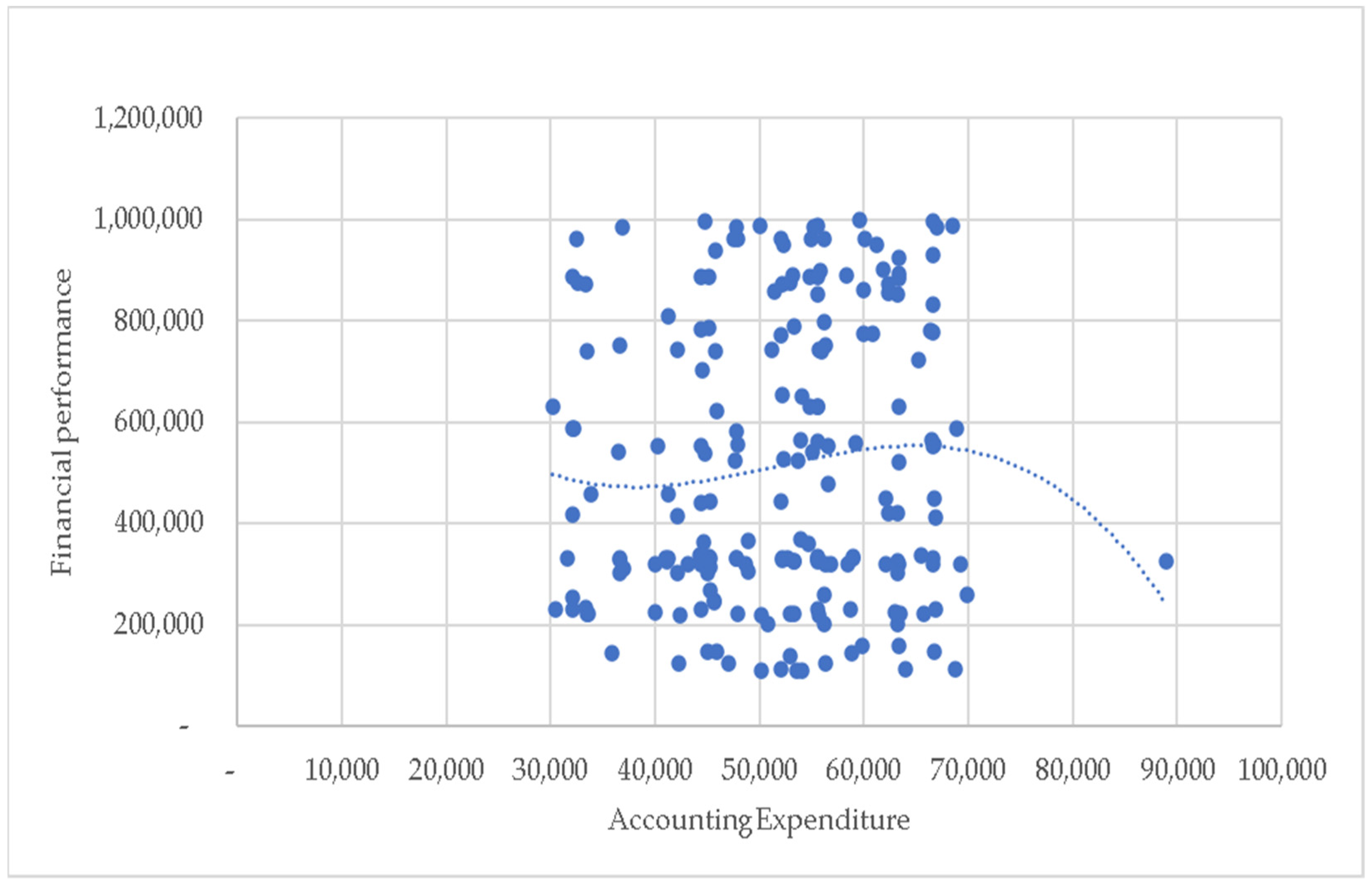

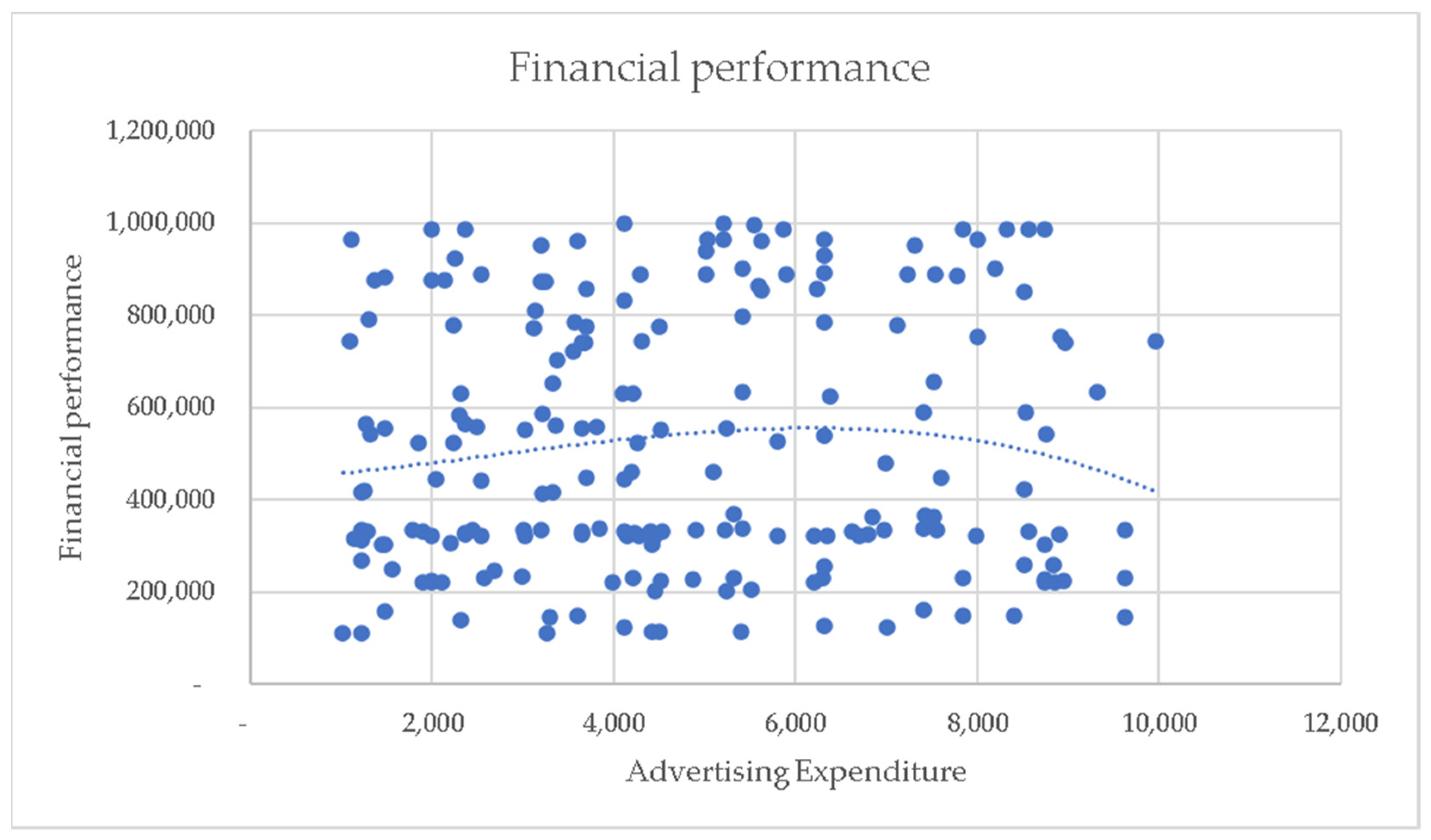

Figure 1 and

Figure 2, the scatter plot suggests a weak direct relationship between financial performance (annual sales revenue) and both accounting expenditure and advertising expenditure. It is important to note that the highest value in accounting expenditure appears to be close to 90,000, specifically 88,896, which is substantially higher than the other values. This outlier may indicate a divergence from the other values and can lead to a decline in the curve, indicating the instability of the direct relationship between sales and accounting expenses. It is possible that the relationship between financial performance, accounting expenditure, and advertising expenditure is not significantly positive in the context of the COVID-19 pandemic in Jordan due to the unique economic conditions and challenges that have arisen because of the pandemic. The pandemic has likely had a significant impact on businesses in Jordan, and this could potentially affect the relationship between these variables. The specific ways in which the pandemic has influenced the economy and businesses in Jordan should be carefully considered.

4.3. Regression Model

According to

Ali and Younas (

2021), researchers use regression analysis in order to describe or present the relationship between one or more independent variables and a dependent variable. Regression models present a way of predicting the effects on the dependent variable caused by variations in one or more independent variables in the regression. The current study analyzes the relationship between financial performance (annual sales revenue) and accounting and advertising expenditure through the use of regression analysis and assesses the effects of the moderator variable, liquidity, on the regression line. The coefficients of the variables and the comparisons of the obtained regression models are presented in

Table 4 and

Table 5.

In

Table 4, the coefficient of a variable in a regression analysis represents the expected change in the dependent variable (in this case, financial performance) that is associated with a one-unit change in the independent variable (in this case, accounting expenditure). A coefficient of ACC (β = 0.01323) for the accounting expenditure variable suggests a weak relationship (positive and not significant) between financial performance and accounting expenditure. This means that a JOD 1 change in accounting expenditure is not expected to be accompanied by a significant change in financial performance. This does not support our H1. The other coefficient, ADV (β = −0.17928 *), suggests a negative and significant relationship between financial performance and advertising expenditure. This is inversely proportional to our H2. This means that a one-unit change in advertising expenditure is expected to be accompanied by a small reduction in financial performance, and this relationship is statistically significant. It is crucial to consider the limitations of this analysis and to carefully interpret the results in the context of the specific study. Similar to

Sahyouni and Wang (

2019), we found no significant correlation between liquidity and firm performance. This does not support our H3. It is possible that the lack of a significant relationship between liquidity and firm performance in the regression analysis is attributed to the impact of the COVID-19 crisis on firms.

During times of economic uncertainty, such as during a pandemic, firms with high liquidity may be more capable of weathering the storm due to their access to a greater amount of cash or other assets that can be easily converted into cash. This can allow them to take advantage of opportunities as they arise, such as investing in new projects or making acquisitions. On the contrary, firms with low liquidity may struggle to meet their short-term financial obligations, which can result in financial distress and poor performance. For instance, they may have to sell assets at a discounted price in order to raise cash, which can erode their asset base and profitability.

In

Table 5, the coefficient for accounting expenditure moderated by liquidity given as ACC*LIQ (β = 0.11046 *) is significantly positive. These findings support our H4a. In a regression analysis, a moderated relationship is one in which the strength or direction of the relationship between two variables is affected by the presence or absence of a third variable. In this case, the coefficient for accounting expenditure moderated by liquidity (ACC*LIQ) implies a significantly positive relationship between accounting expenditure and financial performance when liquidity is considered. This means that as accounting expenditure increases, financial performance is expected to increase as well, but only when liquidity is present. Moreover, the strength or direction of the relationship between these two variables is influenced by the presence or absence of liquidity. When liquidity is present, an increase in accounting expenditure is expected to be accompanied by an increase in financial performance. However, if liquidity is not present, the relationship between these two variables may be different. It is essential to consider the specific ways by which liquidity may be affecting the relationship between accounting expenditure and financial performance and to carefully interpret the results in the context of the specific study.

In this case, the coefficient for advertising expenditure moderated by liquidity given as ADV*LIQ (β = −0.0815 **) suggests that there is a negative and significant relationship between advertising expenditure and financial performance when liquidity is considered. These findings do not support our H4b. This means that as advertising expenditure increases, financial performance is expected to decrease, but only when liquidity is present. The results of the analysis imply a negative relationship between advertising expenditure and financial performance both with and without the moderation of liquidity. This suggests that as advertising expenditure increases, financial performance tends to decrease. One possible explanation for this relationship is that companies may be unable to bear the costs of advertising expenses during times of crisis and may need to focus on expenses that are more critical for maintaining their performance, such as accounting expenses. This could potentially result in a reduction in sales value during times of crisis. These results imply that it may not be advisable for companies to increase their advertising expenditure during times of crisis, as it could potentially have a negative effect on their financial performance.

An R-squared change of 0.00789 (approximately 0.8%) is also observed in the regression output.

5. Discussion

Our findings indicate a significant positive relationship between accounting expenditure and the financial performance of SMEs in Jordan. Moreover, increased advertising expenditure results in improved financial performance among SMEs in Jordan. These results are inconsistent with the literature (

Joshi and Hanssens 2010;

Kurt et al. 2021;

Sueyoshi and Goto 2009;

Peterson and Jeong 2010). However, the results agree with the results from

Molla and Rahaman (

2022), who highlighted that these relationships were not always positive in the long run and should be treated as an expense as it does not bring any future return. The results of this study reveal that limited resources and low liquidity levels have often led to low expenditure among small- and medium-sized businesses. Furthermore, the liquidity level has not always been well suited to Jordan’s conditions, especially during the COVID-19 pandemic due to the closures in Jordan (

Al-Ajlouni 2020). When comparing this study and many previous studies, we have found that liquidity has a moderating significantly positive effect on the relationship between accounting expenditures and financial performance and a significantly negative effect on the relationship between advertising expenditures and the financial performance of SMEs in Jordan. The results of this study and previous studies have demonstrated that liquidity has a moderating effect on the relationship between accounting expenditure and financial performance, such that this relationship is significantly positive when liquidity is present. On the contrary, the relationship between advertising expenditure and financial performance is significantly negative when liquidity is present. This implies that the presence or absence of liquidity can influence the strength or direction of the relationship between these variables. It is important to consider the specific ways in which liquidity may be affecting these relationships and to carefully interpret the results in the context of the specific study.

By comparing the two regression models obtained in the previous section, it is evident that liquidity has a moderating effect on the relationship between advertising expenditure, accounting expenditure, and financial performance (annual sales revenue). This finding evidently displays the significant role of liquidity in defining the relationship between advertising expenditure, accounting expenditure, and financial performance.

The slight changes in coefficients of the predictor variables when the moderating variable is added to the model clearly indicate that liquidity has a moderating effect on the relationship of accounting and advertising expenditures with the financial performance of SMEs in Jordan. Even if the moderating variable effect of liquidity with advertising expenses on the financial performance of companies was significantly negative, it changed more from the first model to the second, when more liquidity was available. In addition, spending more on advertising resulted in a reduction in the financial performance of small and medium companies in Jordan.

Finally, the statistical results of this study dovetail with economic phenomena and Jordanian Government procedures that appeared during the COVID-19 pandemic.

Alawaqleh et al. (

2022) asserted that the Central Bank of Jordan’s policies and strategies regarding corporate governance always support the financial performance and profitability of companies, especially during the COVID-19 pandemic, as well as business risk management.

Due to the COVID-19 pandemic, the Jordanian economy is experiencing failure among SMEs. As a result of the closures in Jordan, many companies were exposed to failure, and their cash flow was paralyzed (

Al-Ajlouni 2020). In Jordan, small- and medium-sized enterprises faced financial liquidity problems during the pandemic, which sparked debate about the financing of SMEs. As a result of this crisis, the banks worked to schedule corporate loans until the end of 2020, and the Central Bank of Jordan worked to inject liquidity into banks with an amount of JOD 550 million. Consequently, a firm maintaining a high level of liquidity may be sacrificing increased investments in order to improve its financial performance. Due to this crisis, the Central Bank of Jordan injected liquidity into banks in an amount of JOD 550 million in order to avoid a default on corporate loans until 2020.

From this study, we gained a deeper understanding of how increasing advertising and accounting expenditures can increase total revenue, resulting in a boost in demand and an increase in annual sales. Furthermore, the liquidity of the Central Bank of Jordan influenced the performance of SMEs financially.

Corporate management resorts to borrowing from banks in order to acquire the necessary liquidity when needed in cases of seasonal distress and in times of emergency crises, by either rediscounting or direct borrowing. Therefore, borrowing from banks is crucial for small and medium companies. The financial decisions related to financing impact the possibility of fluctuation of the returns achieved by the establishment. Increasing the firm’s reliance on borrowing to finance its assets contributes to increasing the expected return. However, this increases the enterprise’s risk reflected in its inability to fulfill its financial obligations represented by loan interests. Risk is considered one of the major issues that small- and medium-sized companies must take into consideration when making financial decisions for supporting their financial performance.

The results of the current study suggest a variation in the confirmation of the four hypotheses. A significant positive relationship exists between accounting expenditures, moderate liquidity, and financial performance of small and medium enterprises in Jordan. Due to increased spending on accounting services by SMEs to achieve a higher level of accounting quality, income has remarkably increased. When advertising expenditures increase among small- and medium-sized companies in Jordan, financial performance suffers, regardless of liquidity levels. Furthermore, the study indicates that, contrary to popular belief, investment in quality accounting services is just as essential for a business as advertising. As a result of an increase in accounting expenses by JOD 1, sales increased, according to the regression analysis conducted. The sales of a company were reduced by JOD 1 when advertising expenses increased by JOD 1. Accounting services can help a business save time, money, and resources that would otherwise have been misappropriated, resulting in a considerable increase in the profits of the company.

6. Conclusions

The current study sought to ascertain the nature of the relationship between accounting expenditure, advertising expenditure, and financial performance among Jordanian SMEs. Furthermore, the study sought to assess liquidity’s significance as a moderator in defining the relationship between accounting expense, advertising expenditure, and financial performance. Annual sales revenue was used as a measure of financial performance in SMEs. The model’s independent variables were accounting expenditure and advertising expenditure, the dependent variable was annual sales revenue, and the moderator variable was liquidity. The study utilized a panel data research design using secondary data acquired from Jordanian SMEs. A regression study was undertaken to determine the relationship between annual sales revenue and accounting and advertising expenditures, as well as the role of liquidity as a moderator in this relationship. Correlation analysis was also used in the study to explain the rate of change in annual sales revenue that is justified by changes in each of the two independent variables and the moderator variable.

The study revealed an insignificantly positive relationship between accounting expenditure and liquidity, which is inconsistent with the findings of the studies of

Husin and Ibrahim (

2014) and

Frolova (

2014) who indicated a positive association between accounting expenses and advertising on sales. According to the study of

Ackah and Vuvor (

2011), the decline in sales was caused by a reduction in advertising, which, according to the study’s findings, may result in a reduction in sales and the departure of small and medium businesses. According to the report of the United Nations Conference on Trade and Development, which contradicts what was mentioned in the study of

Simester et al. (

2009) and what was additionally stated in the study of

Molla and Rahaman (

2022), accounting expenses and advertising expenses provide no future return. Contrary to what the study’s findings indicated, this study can advocate considering that accounting and advertising expenses can be capitalized in order to have a constructive role in raising revenues and sales.

The regression outputs gave variant findings for the coefficients indicating the relationship between the independent variables, the moderator variable, and the dependent variable. In addition, significant differences were observed between the two regression models of the study. Additionally, the two regression models used in the study differed significantly. The change in coefficients indicated that the addition of the moderator variable had a significant impact on the relationship between the dependent and independent variables. In addition, the moderator variable was found to have a direct positive correlation with the dependent variable, indicating that liquidity levels had a significant impact on SMEs in Jordan’s financial performance. When the moderator variable was incorporated into the regression, an increase in the model’s overall significance was also observed. In contrast to what was stated in the study by

Kontuš and Mihanović (

2019), the study by

Antonios (

2015) study asserted that liquidity plays a positive role in the performance and continuity of businesses.

The study’s findings have critical implications for researchers, regulators, and professionals because they provide a pragmatic perspective on the relevance of researching the impact of accounting and advertising expenditures on the financial performance of Jordanian SMEs. The findings, in particular, emphasize the significance and meaning of the impact of accounting and advertising expenses, as well as liquidity, on the financial performance of Jordanian SMEs. Furthermore, the findings of the study suggest that liquidity is required for defining and establishing the relationship between accounting expenses, advertising expenditures, and financial performance.

The study’s findings have several implications that could assist Jordanian SMEs in focusing their resources on ensuring that advertising effectively promotes products and brands. The outcomes of this study also provide insight and clarification into the impact of raising advertising costs in increasing total revenue, which in turn increases demand and annual sales. The study’s findings imply that small- and medium-sized enterprises should have optimal liquidity ratios in place to prevent underspending on important expenses such as accounting and advertising or keeping liquid assets instead of profitable investments. Several limitations need to be addressed in future research. Firstly, the sample only includes the financial reports issued by SMEs, not including interviews with policymakers in SMEs and not using questionnaires to know employees’ opinions in SMEs. Secondly, according to the statistics of the Department of Statistics in Jordan, the number of small and medium enterprises reached 95,000 enterprises. This study used just 200 enterprises due to the limitations of access to financial information for all SMEs. In order to improve future research and increase the generalizability of the results, larger sample sizes should be utilized. In light of the above findings, we recommend that small- and medium-sized businesses invest in the hiring of qualified accounting services. Jordanian small and medium businesses must maintain good liquidity levels in order to meet short-term expenses and pay obligations on time. Nevertheless, small- and medium-sized businesses should optimize the amount of liquidity available in order to ensure that they only spend on essential needs such as accounting and other major expenses or on liquid assets instead of investing in profitable ventures.

Author Contributions

Conceptualization, R.M.A., Q.A.A., N.A.A. and F.A.; data curation, R.M.A., Q.A.A. and S.Q.A.; formal analysis, R.M.A. and Q.A.A.; funding acquisition, R.M.A., Q.A.A., N.A.A. and F.A.; investigation, R.M.A., Q.A.A., N.A.A. and F.A.; methodology, R.M.A., Q.A.A., N.A.A. and F.A.; project administration, R.M.A.; resources, R.M.A., Q.A.A., N.A.A., F.A. and S.Q.A.; software, R.M.A., Q.A.A. and F.A.; supervision, R.M.A. and Q.A.A.; validation, R.M.A., Q.A.A., N.A.A. and F.A.; visualization, R.M.A., Q.A.A., N.A.A. and F.A.; writing—original draft, R.M.A. and Q.A.A.; writing—review and editing, R.M.A., Q.A.A., N.A.A., F.A. and S.Q.A. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Informed Consent Statement

Not applicable.

Data Availability Statement

The data presented in this study are available on request from the first author.

Acknowledgments

The publication of this research has been supported by the Deanship of Scientific Research and Graduate Studies at Philadelphia University, Jordan.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Abbas, Faisal, Shahid Iqbal, and Bilal Aziz. 2019. The Impact of Bank Capital, Bank Liquidity and Credit Risk on Profitability in Postcrisis Period: A Comparative Study of US and Asia. Edited by Zhaojun Yang. Cogent Economics and Finance 7: 1605683. [Google Scholar] [CrossRef]

- Abdul-Rahamon, Onaolapo Adekunle, and Adegbite Tajudeen Adejare. 2014. The Analysis of the Impact of Accounting Records Keeping on the Performance of the Small Scale Enterprises. International Journal of Academic Research in Business and Social Sciences 4: 1–17. [Google Scholar]

- Abu-Mater, Wesam, Malik Abu Afifa, and Mohammad Alghazzawi. 2021. The Impact of COVID-19 Pandemic on Small and Medium Enterprises in Jordan. Journal of Accounting, Finance & Management Strategy 16: 129–50. [Google Scholar]

- Acar, Merve, and Hüseyin Temiz. 2017. Advertising Effectiveness on Financial Performance of Banking Sector: Turkey Case. International Journal of Bank Marketing 35: 649–61. [Google Scholar] [CrossRef]

- Acharya, Viral, and Hassan Naqvi. 2012. The Seeds of a Crisis: A Theory of Bank Liquidity and Risk Taking over the Business Cycle. Journal of Financial Economics 106: 349–66. [Google Scholar] [CrossRef]

- Ackah, John, and Sylvester Vuvor. 2011. The Challenges Faced by Small and Medium Enterprises (SMEs) in Obtaining Credit in Ghana. Karlskrona: Blekinge Tekniska Hogskola School of Management, BTH University. Available online: https://www.diva-portal.org/smash/record.jsf?pid=diva2:829684 (accessed on 30 January 2023).

- Adusei, Michael. 2022. The Liquidity Risk–Financial Performance Nexus: Evidence from Hybrid Financial Institutions. Managerial and Decision Economics 43: 31–47. [Google Scholar] [CrossRef]

- Al-Ajlouni, Mohammed Iqbal. 2020. Can High-Performance Work Systems (HPWS) Promote Organisational Innovation? Employee Perspective-Taking, Engagement and Creativity in a Moderated Mediation Model. Employee Relations: The International Journal 43: 373–97. [Google Scholar] [CrossRef]

- Alawaqleh, Qasim A. 2021. The Effect of Internal Control on Employee Performance of Small and Medium-Sized Enterprises in Jordan: The Role of Accounting Information System. Journal of Asian Finance, Economics and Business 8: 855–63. [Google Scholar] [CrossRef]

- Alawaqleh, Qasim A., Mohammad Hamdan, Ahmed Al-Jayousi, and Rana Airout. 2022. The Moderating Role of IFRS in the Relationship between Risk Management and Financial Disclosure in Jordanian Banks. Banks and Bank Systems 17: 167–76. [Google Scholar] [CrossRef]

- Albers, Michael J. 2017. Quantitative Data Analysis—In the Graduate Curriculum. Journal of Technical Writing and Communication 47: 215–33. [Google Scholar] [CrossRef]

- Alduais, Fahd. 2022. Textual Analysis of the Annual Report and Corporate Performance: Evidence from China. Journal of Financial Reporting and Accounting. ahead-of-print. [Google Scholar] [CrossRef]

- Ali, Parveen, and Ahtisham Younas. 2021. Understanding and Interpreting Regression Analysis. Evidence-Based Nursing 24: 116–18. [Google Scholar] [CrossRef]

- Al-Mashari, Majed, Abdullah Al-Mudimigh, and Mohamed Zairi. 2003. Enterprise Resource Planning: A Taxonomy of Critical Factors. European Journal of Operational Research 146: 352–64. [Google Scholar] [CrossRef]

- Al-Sawalqa, Fawzi Ata. 2020. Risk Disclosure Patterns among Jordanian Companies: An Exploratory Study during Covid-19 Pandemic. Accounting and Finance Research 9: 69–84. [Google Scholar] [CrossRef]

- AL-Tamimi, Khaled Abdalla Moh’d, and Mohammad Sulieman Jaradat. 2019. The Role of Small Medium Enterprises in Reducing the Problem Of. International Journal of Development and Economic Sustainability 7: 28–36. Available online: www.eajournals.org (accessed on 20 January 2023).

- AL-Zararee, Abdulnafea, Nashat Ali Almasria, and Qasim Ahmad Alawaqleh. 2022. The Effect of Working Capital Management and Credit Management Policy on Jordanian Banks’ Financial Performance. Banks and Bank Systems 16: 229–39. [Google Scholar] [CrossRef]

- Amin, Hindu Jibril. 2021. Influence of Marketing Strategies on the Performance of SMEs: Evidence from Abuja SMEs. Journal of Economics and Business 4: 294–307. [Google Scholar] [CrossRef]

- Anderson, Ronald W. 2002. Capital Structure, Firm Liquidity and Growth. SSRN Electronic Journal 27: 1–19. [Google Scholar] [CrossRef]

- Antonios, Zairis G. 2015. The Effects of the Financial Crisis on the Performance of Greek SME’s. International Journal of Business 5: 29–37. Available online: www.ijbhtnet.com (accessed on 2 February 2023).

- Baack, Daniel W., Rick T. Wilson, Maria M. van Dessel, and Charles H. Patti. 2016. Advertising to Businesses: Does Creativity Matter? Industrial Marketing Management 55: 169–77. [Google Scholar] [CrossRef]

- Barney, Jay. 1991. Firm Resources and Sustained Competitive Advantage. Journal of Management 17: 99–120. [Google Scholar] [CrossRef]

- Bayer, Emanuel, Shuba Srinivasan, Edward J. Riedl, and Bernd Skiera. 2020. The Impact of Online Display Advertising and Paid Search Advertising Relative to Offline Advertising on Firm Performance and Firm Value. International Journal of Research in Marketing 37: 789–804. [Google Scholar] [CrossRef]

- Bhunia, Amalendu. 2010. A Study of Liquidity Trends on Private Sector Steel Companies in India. Asian Journal of Management Research 1: 618–28. [Google Scholar]

- Carbó-Valverde, Santiago, Francisco Rodríguez-Fernández, and Gregory F. Udell. 2016. Trade Credit, the Financial Crisis, and SME Access to Finance. Journal of Money, Credit and Banking 48: 113–43. [Google Scholar] [CrossRef]

- Central Bank of Jordan, Financial Stability Department. 2020. Financial Stability Report. Available online: https://www.cbj.gov.jo/EchoBusv3.0/SystemAssets/PDFs/EN/JFSR2020%20Final%2028-11-2021.pdf (accessed on 3 March 2023).

- Central Bank of Jordan. 2021. The Central Bank of Jordan Announces a Set of Procedures Aimed to Contain the Repercussions of the Emerging Corona Virus Impact on the National Economy. Available online: https://www.cbj.gov.jo/DetailsPage/CBJEn/NewsDetails.aspx?ID=279 (accessed on 14 March 2023).

- Chava, Sudheer, and Robert A. Jarrow. 2004. Bankruptcy Prediction with Industry Effects. Review of Finance 8: 537–69. [Google Scholar] [CrossRef]

- Chen, Kai. 2020. The Effects of Marketing on Commercial Banks’ Operating Businesses and Profitability: Evidence from US Bank Holding Companies. International Journal of Bank Marketing 38: 1059–79. [Google Scholar] [CrossRef]

- Cheng, Hui G., and Michael R. Phillips. 2014. Secondary Analysis of Existing Data: Opportunities and Implementation. Shanghai Archives of Psychiatry 26: 371–75. [Google Scholar] [CrossRef]

- Cicea, Claudiu, Ion Popa, Corina Marinescu, and Simona Cătălina Ștefan. 2019. Determinants of SMEs’ Performance: Evidence from European Countries. Economic Research-Ekonomska Istraživanja 32: 1602–20. [Google Scholar] [CrossRef]

- Core Development Team, R. 2021. A Language and Environment for Statistical Computing. In R Foundation for Statistical Computing. Vienna: R Core Team. Available online: http://www.r-project.org (accessed on 14 March 2023).

- DeAngelo, Harry, and Linda DeAngelo. 2006. The Irrelevance of the MM Dividend Irrelevance Theorem. Journal of Financial Economics 79: 293–315. [Google Scholar] [CrossRef]

- Deloof, Marc. 2003. Does Working Capital Management Affect Profitability of Belgian Firms? Journal of Business Finance and Accounting 30: 573–88. [Google Scholar] [CrossRef]

- Deloof, Marc, and Marc Jegers. 1996. Trade Credit, Product Quality, and Intragroup Trade: Some European Evidence. Financial Management 25: 33–43. [Google Scholar] [CrossRef]

- Doraszelski, Ulrich, and Sarit Markovich. 2008. Advertising Dynamics and Competitive Advantage. The RAND Journal of Economics 38: 557–92. [Google Scholar] [CrossRef]

- Durrah, Omar, Abdul Aziz Abdul Rahman, Syed Ahsan Jamil, and Nour Aldeen Ghafeer. 2016. Exploring the Relationship between Liquidity Ratios and Indicators of Financial Performance: An Analytical Study on Food Industrial Companies Listed in Amman Bursa. International Journal of Economics and Financial Issues 6: 435–41. [Google Scholar]

- Erdin, Ceren, and Gokhan Ozkaya. 2020. Contribution of Small and Medium Enterprises to Economic Development and Quality of Life in Turkey. Heliyon 6: e03215. [Google Scholar] [CrossRef]

- European Investment Bank. 2022. Banking in Jordan: Financing Corporates and SMEs in the Era of COVID-19: Evidence from the EIB Bank Lending Survey. Available online: https://library.oapen.org/bitstream/id/f3deae61-7396-4fc0-af4f-418bb924038d/banking_in_jordan_en.pdf (accessed on 20 January 2023).

- Fama, Eugene F., Kenneth R. French, Josef Lakonishok, Stephen Penman, Rex Sinquefield, and Rene Stulz. 1995. Size and Book-to-Market Factors in Earnings and Returns. The Journal of Finance 50: 131–55. [Google Scholar] [CrossRef]

- Frolova, Svetlana. 2014. The Role of Advertising in Promoting a Product. Centria University of Applied Sciences. Available online: https://www.theseus.fi/bitstream/handle/10024/80777/Frolova_Svetlana.pdf (accessed on 14 March 2023).

- Gupta, Sunil, and Thomas Steenburgh. 2008. Allocating Marketing Resources. In Marketing Mix Decisions: New Perspectives and Practices. Edited by Roger A. Kerin and Rob O’Regan. Chicago: American Marketing Association, pp. 90–105. Available online: https://www.hbs.edu/ris/Publication%20Files/08-069_17a7715d-c34b-4d9e-92fa-2ea2834a0cbe.pdf (accessed on 14 March 2023).

- Hassan, M. Kabir, Ashraf Khan, and Andrea Paltrinieri. 2019. Liquidity Risk, Credit Risk and Stability in Islamic and Conventional Banks. Research in International Business and Finance 48: 17–31. [Google Scholar] [CrossRef]

- Huang, Shaio Yan, Yu Chung Hung, Chi Chen Lin, and Ing Jung Tang. 2009. The Effects of Innovative Capacity and Capital Expenditures on Financial Performance. International Journal of Innovation and Learning 6: 323. [Google Scholar] [CrossRef]

- Husin, Mohd Azian, and Mohamed Dahlan Ibrahim. 2014. The Role of Accounting Services and Impact on Small Medium Enterprises (SMEs) Performance in Manufacturing Sector from East Coast Region of Malaysia: A Conceptual Paper. Procedia-Social and Behavioral Sciences 115: 54–67. [Google Scholar] [CrossRef]

- Hyz, Alina B. 2011. Small and Medium Enterprises (SMEs) in Greece-Barriers in Access to Banking Services. An Empirical Investigation. International Journal of Business and Social Science 2: 161–65. Available online: http://ec.europa.eu/enterprise/enterprise_policy/sme_definition/index_en.htm (accessed on 14 March 2023).

- Jensen, Michael C. 1986. Agency Costs of Free Cash Flow, Corporate Finance, and Takeovers. The American Economic Review 76: 323–29. Available online: http://www.jstor.org/stable/1818789 (accessed on 20 February 2023).

- Jensen, Michael C., and William H. Meckling. 1976. Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure. Journal of Financial Economics 3: 305–60. [Google Scholar] [CrossRef]

- Joshi, Amit, and Dominique M. Hanssens. 2010. The Direct and Indirect Effects of Advertising Spending on Firm Value. Journal of Marketing 74: 20–33. [Google Scholar] [CrossRef]

- Kamau, Robert Mwangi. 2015. The Influence of Accounting Records on the Financial Performance of Small and Medium Enterprises in Central Business District in Nairobi County. Ph.D. thesis, University of Nairobi, Nairobi, Kenya. Available online: http://41.204.161.209/handle/11295/93377 (accessed on 20 March 2023).

- Keynes, J. M. 1936. The Supply of Gold. The Economic Journal 46: 412–18. [Google Scholar] [CrossRef]

- Kharabsheh, Buthiena, and Omar Khlaif Gharaibeh. 2022. Determinants of Banks’ Stability in Jordan. Economies 10: 311. [Google Scholar] [CrossRef]

- Kim, Sungsoo. 2001. The Near-Term Financial Performance of Capital Expenditures: A Managerial Perspective. Managerial Finance 27: 48–62. [Google Scholar] [CrossRef]

- Kontuš, Eleonora, and Damir Mihanović. 2019. Management of Liquidity and Liquid Assets in Small and Medium-Sized Enterprises. Economic Research-Ekonomska Istrazivanja 32: 3247–65. [Google Scholar] [CrossRef]

- Kurt, Didem, Koen Pauwels, Ahmet C. Kurt, and Shuba Srinivasan. 2021. The Asymmetric Effect of Warranty Payments on Firm Value: The Moderating Role of Advertising, R&D, and Industry Concentration. International Journal of Research in Marketing 38: 817–37. [Google Scholar] [CrossRef]

- Lantz, Jean-sébastien, and Jean-michel Sahut. 2005. R&D Investment and the Financial Performance of Technological Firms. International Journal of Business 10: 252–70. Available online: https://ijb.cyut.edu.tw/var/file/10/1010/img/851/V103-4.pdf (accessed on 14 March 2023).

- Leach, Daniel F., and W. Duncan Reekie. 1996. A Natural Experiment of the Effect of Advertising on Sales: The SASOL Case. Applied Economics 28: 1081–91. [Google Scholar] [CrossRef]