1. Background

There is growing interest among scholars in investigating the impact of macroeconomic uncertainty on economic growth, which includes the following investigations:

Mandeya and Ho (

2021), and

Balcilar et al. (

2022), among others. However, no consensus has been reached as to the impact of macroeconomic uncertainty on economic growth, as both positive and negative results are found (

Mumtaz and Theodoridis (

2018),

Gupta and Jooste (

2018),

Redl (

2018),

Olanipekun et al. (

2019),

Mandeya and Ho (

2021), and

Balcilar et al. (

2022). Macroeconomic uncertainty refers to a lack of knowledge about the set of possible effects and their related probabilities because the final results are highly particular or complex, which makes forecasting difficult (

Bloom 2014). One of the broad measures of macroeconomic uncertainty is the world uncertainty for the South Africa index (WUI). Less attention has been given directly to the investigation of macroeconomic uncertainty in different regimes of economic growth in the presence of fiscal consolidation in South Africa. The main contribution of this paper to fill that gap. The thinking around fiscal consolidation is that government expenditure cuts and tax increases will result in a fall in debt because present, forwards-looking economic agents will anticipate a reduction in tax and interest rates. This will increase permeant income as well crowed-in investment; as such, there will be an increase in economic activities, leading to higher economic growth and higher tax collection that can be used to reduce government debt (

Alesina and Ardagna 2010;

Mankiw 2019). One of the broad measures of discretionary government intervention to reduce the government debt that defines fiscal consolidation episodes is the cyclically adjusted primary balance (CAPB). The measure is concerned with the identification of discretionary fiscal policy changes in tax and government expenditure by filtering out changes that are due to economic fluctuations in tax as well as government expenditure (

Alesina et al. 2019). The investigation of aggregate effects of global uncertainty with evidence from an emerging economy including South Africa was undertaken by

Ahiadorme (

2022) using vector autoregressions (VARs). It was discovered that shocks related to global unpredictability are a significant cause of economic fluctuations. Additionally, the predicted macroeconomic uncertainty harms the financial and stock markets and significantly explains the cyclical downturn in economic growth.

In 2014, the Financial and Fiscal Commission (FFC) in South Africa recommended more fiscal consolidation stances to restore the fiscal position to increase economic growth and reduce government debt (

BR 2014). The FFC recommendation outlined that “

Fiscal consolidation can no longer be postponed. Ensuring continued progress towards a better life obliges the government to safeguard public finances by acting within fiscal limits that can be sustained over the long term. To do otherwise would risk exposing the country to a debt trap, with damaging consequences for development for many years to come” (

MTBPS 2014). The Fiscal Responsibility Bill (FRB) was tabled for discussion in the parliament of SA in 2018. The bill seeks to introduce government expenditure cuts, limit new government borrowing, maintain an expenditure ceiling, and eliminate wasteful expenditure (

FRB 2018). In 2019, the International Monterey Fund (IMF), Standard and Poor’s, Moody’s, and Fitch stressed that SA needs to implement a credible fiscal strategy and fiscal consolidation to contain the rise in government debt. This recommendation came with concern that the country is faced with high government debt and that there is policy uncertainty (

IMF 2020).

Despite this effort, the economic growth is at the mean rate of 2.43%, which is below the 5% stipulated in the South African macroeconomic policy of the National Development Plan in 2013 (

National Planning Commission 2013). It is against this background that it is critical to investigate the dynamics of macroeconomic uncertainty in different regimes of economic growth in the presence of fiscal consolidation in South Africa. The key questions of this paper are as follows: What is the impact of macroeconomic uncertainty in different regimes of economic growth in the presence of fiscal consolidation in South Africa? How long will economic growth be at a higher rate and a lower rate? What is the probability of transitioning to different regimes of economic growth in the presence of fiscal consolidation and macroeconomic uncertainty? What is the impact of macroeconomic uncertainty and fiscal consolidation shocks? Given the questions of this paper, the hypotheses are as follows:

| Null: | Macroeconomic uncertainty has no impact on different regimes of economic growth in the presence of fiscal consolidation. |

| Alt: | Macroeconomic uncertainty has an impact on different regimes of economic growth in the presence of fiscal consolidation. |

| Null: | There is no probability of transition to different regimes of economic growth rate. |

| Alt: | There is the probability of transition to different regimes of economic growth rate. |

| Null: | Macroeconomic uncertainty shock has no impact on economic growth. |

| Alt: | Macroeconomic uncertainty shock has an impact on economic growth. |

Three states are found for economic growth, with a negative mean rate of 2.349% and positive means of 1.129% and 3.679%, respectively. Macroeconomic uncertainty was found to have a negative impact of 6.729%, 4.385% and 3.080% in states 1 to 3, respectively. Fiscal consolidation provided an accommodative policy, as it reduced the negative impact of macroeconomic uncertainty by 3.57%, 1.996% and 0.92% in states 1 to 3, respectively. However, fiscal consolidation does not completely reduce the negative impact of macroeconomic uncertainty. The result reflected that the economy is expected to stay for 1 year, 2 years, and 3 years in the respective state. The transition probabilities of economic growth moving and returning to the same states are 29.46%, 34.07% 58.02%, respectively. The time-varying impulse response functions showed that macroeconomic uncertainty harms economic growth. Nevertheless, the multiplier effect is not large; however, the economy operates below equilibrium and does not restore equilibrium after the impact of macroeconomic uncertainty. This reflects that it takes time for macroeconomic uncertainty to filter out of the South African economy. It is recommended that fiscal consolidation be used in accommodative fiscal policy to reduce macroeconomic uncertainty.

The paper structure is as follows:

Section 2 outlines the literature review.

Section 3 discusses the methodology.

Section 4 discusses empirical results. Finally,

Section 5 outlines the conclusion and recommendations of this paper.

4. Result

Table 2 shows the descriptive statistics of economic variables from 1994 to 2022. The

is found to have a mean of 2.43%. The level of

is found to have an average of 1.07% between 1979 and 2022. The

is found to have a mean of 0.30%. The

is found to have a rate of 0.39% over the period reflecting the mean. Finally, the

is found to be 0.30% between 1994 and 2022 on average. There is an indication of the skewness used to test for normal distribution. The Pr(Skewness) reflect that all economic variables except

and

fail to reject the null; therefore, it can be concluded that the economic variables are normally distributed.

Table 3 shows the correlations among the economic variables. Correlation is a statistic that measures the degree to which two variables move in relation to each other. In the important because it can reflect the direction of the relationship, the form (shape) of the relationship, and the degree (strength) of the relationship between two variables. All of the economic variables of interest considered in the paper are found to have a positive correlation with

except

. In the variables of interest,

has a correlation value of −0.34 with

, this reflects that as the macroeconomic uncertainty increase this will have detrimental effect on economic growth. On the other hand, fiscal consolidation proxied by

has a correlation value of 0.60 with

, which is the highest among all of the economic variables. The reflect there are fiscal consolidation can be an accommodative economic policy in the effort to stimulate economic growth. This is similar to the result of

Alesina and Ardagna (

2010) and

Bi et al. (

2013) among others that concluded that fiscal consolidation economic variables have a positive correlation with economic growth.

Moreover, the economic variables that will proxy the macroeconomic uncertainty, which include

,

,

,

, and

, are found to have a negative correlation with gross domestic product. This correlation reflects that it may be expected that macroeconomic uncertainty may have a negative impact on economic growth. The result has been found in research which is reflected in the work of

Jordà and Taylor (

2016),

Burger and Jimmy (

2006),

Heimberger (

2017), and

Brady and Magazzino (

2018), among others. Nevertheless, the correlation result in

Table 2 is not the cause result, and the result to focus on casual effect among economic varies. An important limitation of the correlation coefficient is that it assumes a linear association. Finally, the variable of

, or political stability, is found to have a positive correlation with economic growth.

Table 4 shows the Dickey-Fuller test and structural break, the unit root for the economic variables of interest in the paper. Most of the economic variables are stationary at level

, including the economic variables of

,

,

,

, and

. On the other hand, the economic variables of

,

,

,

,

and

are stationary at the first difference

or first-order condition.

In

Table 4, the unit-root tests with structural shifts both indicate a cointegration relationship between the gross domestic product, labour, capital, macroeconomic uncertainty, and fiscal consolidation in the period between 1994 and 2022. For the economic variable that is not integrated at order one

. Given theses results in this paper there will be an estimation that include both the level and the first differences economic variables in the empirical model. The break points for each economic variable from 1994 to 2022 are reflected in the column for the estimated break date, which is yearly. The structural breaks for the economic variables of interest

and

in 2009 can be attributed to the financial crisis period beginning in 2008.

Table 5 reflects the Markov chain, a dynamic regression model for macroeconomic uncertainty. In the first state model’s estimation 1,

is found to have a mean of negative 6.299%, which is statistically significant at a 1% p-value. On the other hand, under the economic operating in states 2 and 3,

is found to have positive means of 3.910% and 1.476%, respectively, with a statistically significant 1% p-value. These results are similar to that of

Burger and Jimmy (

2006); however, they are slightly different given the different time spent used in this paper. Nevertheless, across all states, no rate of 5% economic growth is found. This reflects that the South African economy is lagging behind in the effort to meet its target as stipulated in the National Development Plan of 2013 for the South Africa

National Planning Commission (

2013). This reflects that there will be a need for a huge economic policy intervention in South Africa to achieve the 5% rate.

Moreover, the rate of 5% was believed to be effective in resolving some of the macroeconomic challenges. Given that, these results reflect that South Africa is still far behind in achieving its objectives of reducing employment and inequality and increasing economic growth. In the first state, model estimation 2 reflects the impact of fiscal consolidation proxied by a cyclical adjusted primary balance. The consideration of fiscal consolidation in estimation 2 shows it to have a positive impact of the policy on economic growth. This is because there are 2.127%, 0.930% and 0.919% increases in economic growth for a 1% increase in

in the three respective states, which is statistically significant at a 1%

p-value. These results are contrary to those of

Jordà and Taylor (

2016),

Burger and Jimmy (

2006),

Heimberger (

2017), and

Brady and Magazzino (

2018), among others, who found that fiscal consolidation has a negative impact on the economy. Moreover, the results suggest that there is more evidence of the rationale of the classical school of thought than of the Keynesian, which is mostly advocated in South African economic environment. Therefore, there is evidence that fiscal consolidation may be able to provide an accommodative policy, especially in the presence of macroeconomic uncertainty in the effort to stimulate economic growth.

In estimation 5, it is found that a 1% increase in

reduces

by the negative rates of 6.729%, 4.385%, and 3.080% in states 1 to 3, respectively. There is a higher detrimental effect of economic growth when it is operating in state one with a negative mean of 6.299%. However, if the economy is operating in economic state of 3.910% and 1.476% which is state 1 and 2, the effect of

is negative but not with a high magnitude. This result suggests that the South African economy is very vulnerable to macroeconomic uncertainty. These results are similar to those of

Olanipekun et al. (

2019),

Mandeya and Ho (

2021),

Balcilar et al. (

2022), and

Ahiadorme (

2022), among others, who have found a negative impact of macroeconomic uncertainty proxy indexes on economic growth. However, they are contrary to that of

Bredin et al. (

2009), who found that sometimes uncertainty may stimulate competition and increase economic growth in an economy. When

macroeconomic uncertainty is estimated in the presence of

fiscal consolidation in estimation 5, it is found that

macroeconomic uncertainty harms economic growth, as it results in a 1.209% and 1.2759% decrease in states 2 and 3, while in state 1 the result was found to be insignificant. This result show more insight of what its magnitude impact of

and

. This is more insightful to then the correlation result in that

Table 3 which reflected correlation value of −0.34 between

and

. The result reflects the venerability of the South Africa economic growth on macroeconomic uncertainty. At an imperial level the result provides the support of

Balcilar et al. (

2022) and

Ahiadorme (

2022), among others. Nevertheless, these rates in estimation 5 are less than those in estimation 4. This reflects that a fiscal consolidation policy provides an accommodative policy for macroeconomic uncertainty that keeps it from being drastically detrimental to economic growth.

However, fiscal consolidation does not provide a positive effect that revises the impact of macroeconomic uncertainty, but only reduces the negative impact. Fiscal consolidation reduces the negative impact of macroeconomic uncertainty by 3.176% and 1.805% from 1 to 2, respectively. The state 3 magnitudes were not calculated because of the insignificance of the result in estimation 5. Nevertheless, this provides evidence that fiscal consolidation provides an accommodative policy that reduces the impact of macroeconomic uncertainty. However, there are tradeoffs, given that, if fiscal consolidation is used, it may harm economic growth. The dummy variable reflecting the structural break of the fiscal consolidation, is found to have a positive impact on economic growth. This reflects that, in the case of a quick change or adoption of fiscal consolidation, there is a 1.962% chance that there will be an increase in economic growth. On the other hand, the structural break for macroeconomic uncertainty is found to result in a 3.765% chance of a fall in the gross domestic product. This reflects that unexpected change over time on macroeconomic uncertainty harms economic growth. South Africa fiscal author need to put in place economic model that can forecast unexpected change that can affect economic growth.

Table 6 reflects a Markov-switching dynamic regression that has four proxies of macroeconomic uncertainty, as a ground for comparison with the based result in

Table 5. The first proxy,

reflecting the volatility of the stock price index for South Africa, is found to have a negative rate that reduces the gross domestic product by 0.211%, 0.150%, and 0.119% from states 1 to 3, respectively. This result is similar to those of

Wu and Wang (

2021),

Chen et al. (

2022), and

Long and Zhang (

2022). The second proxy of macroeconomic uncertainty in estimation 2, which is

is found to have a negative impact only in state 1, with the rate of 0.271%, and its effects states 2 and 3 are insignificant. This is when GDP is at the mean rate of negative 6.299%; however, fiscal consolidation is found to provide support in the effort in the present of

which reflects a rate of 2.326%. The economic policy uncertainty in estimation 3 is found to result in a negative impact of 0.0344% and 0.0422% in states 1 and 3, while its effect in state 2 is insignificant. These results are similar to those of

Olanipekun et al. (

2019),

Mandeya and Ho (

2021),

Balcilar et al. (

2022), and

Ahiadorme (

2022), among others, who have found a negative impact for the macroeconomic uncertainty proxy indexes on economic growth. The smoothed world uncertainty index for South Africa in estimation 4 is found to have a negative impact on economic growth at rates of 0.456% and 0.216% in states 1 and 2, while its effect in state 3 is insignificant. The political instability in South Africa,

is found to result in a negative impact on economic growth of rates of 0.630% and 2.051% in the first and the second state, while in state three it has a positive impact of 3.346%. The government effectiveness,

is shown to result in an increase of 1.903% in state 1, while in states 2 and 3 it is found to be insignificant.

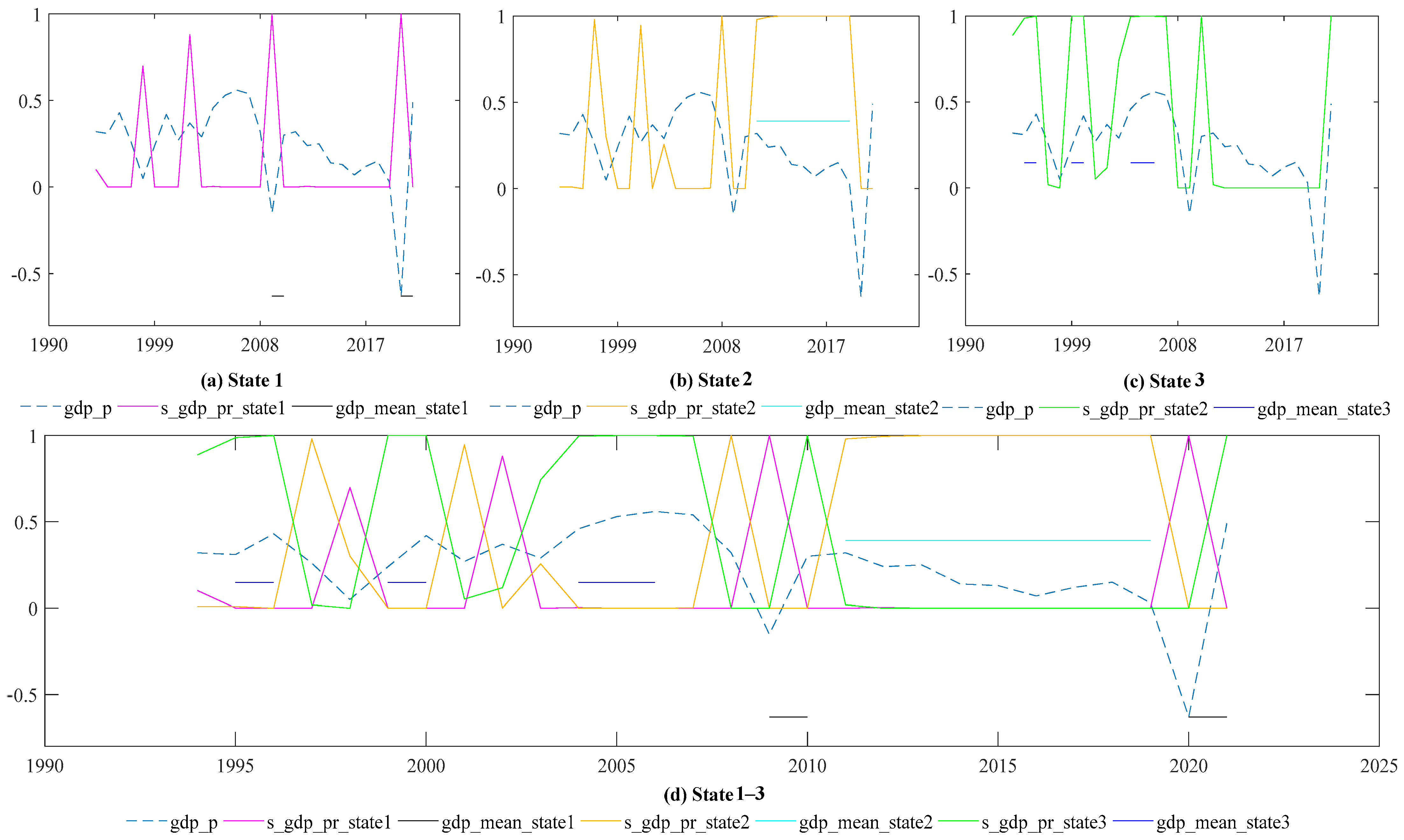

Figure 1 shows the filter transition probability from state 1 to state 3 as well as

.

Figure 1, graph a, shows the state 1 filter transition probability for

. There is a weak transition probability for moving to state 2 in 1998 and 2002. The

moved to state 1 briefly in 2009 and 2021.

Figure 1, graph b, shows the state 2 filter transition probability for

. The economy moved to state 2 four times, and the one possible fifth transition to the state was not successful. The times that the economy operated in state 2 were in 1997, 2001, and 2008, and from 2011 to 2019. The one time that the economy failed to be in state 2 was in 2003. Graph c in

Figure 1 shows the state 3 filter transition probability for

. The economy moved to state 3 five times in 1995 to 1996, 1999 to 2000, 2004 to 2006, 2010, and 2021.

Figure 1, graph d, shows all the different regimes combined with the repetitive mean for the GDP.

Table 7 shows the expected duration of each state. When the economy is in state 1, it is found to run for 1 year. State 2 is found to run for 2 years, and state 3 is found to run for 3 years.

Table 8 reflects the matrix of transition probabilities for economic growth in different states. The first state is characterized by a negative mean of 2.349%. In this state, the economy is found to have a transition probability of 0.2946238. This reflects that there is a 29.46% chance that the economy will move from state 1 and return to state 1. On the other hand, the second state is characterized by a mean of 1.129%. In this state, the economy is found to have a transition probability of 0.3407753. This reflects that there is a 34.07% chance that the economy will move from state 2 and return to state 2. The third state has a mean of 3.679%. In this state, the economy is found to have a transition probability of 0.5802805. This reflects that there is a 58.02% chance that the economy will move from state 3 and return to state 3. The highest rate is a 58.02% chance of staying in a state that has a positive economic growth rate of 3.67%. However, this rate is still not sufficient to solve the South African macroeconomic challenges. Therefore, even if the economy is operating in this state, fiscal authorities need to find ways to stimulate economic growth.

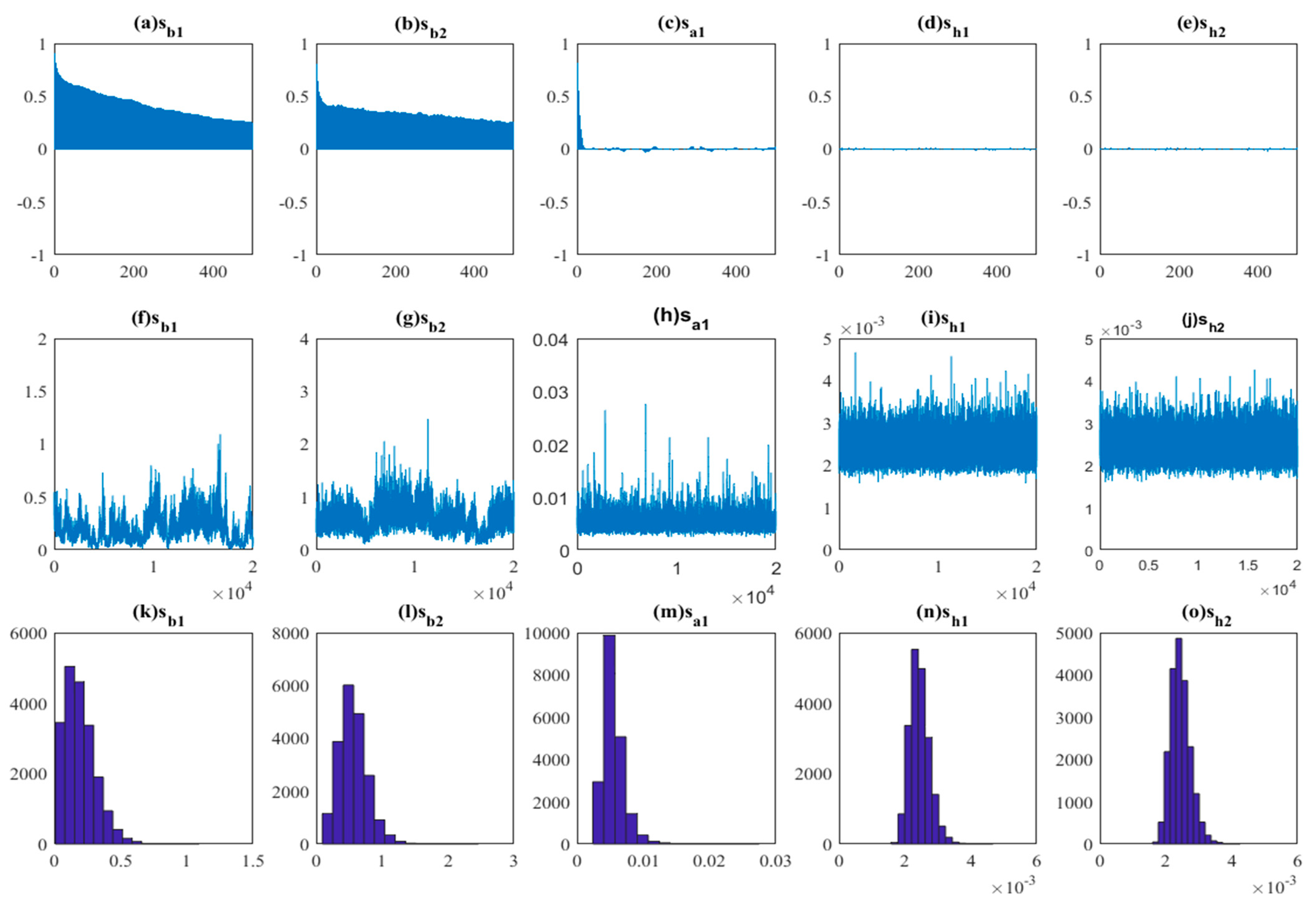

The TVP-VAR results are shown in

Table 9, which shows the parameters, 95% confidence intervals, convergence diagnostics (CD) of

Geweke (

1992), and inefficiency factors computed using the MCMC sample. In the estimated result, the null hypothesis of convergence to the posterior distribution is not rejected for the parameters at the 5% significance level based on the CD statistics, and the inefficiency factors are quite low, except for sh2, which indicates efficient sampling for the parameters and the state variables. In the simulation in this paper, the priors are summed to follow the TVP regression model with stochastic volatility discussed above in Equation (21).

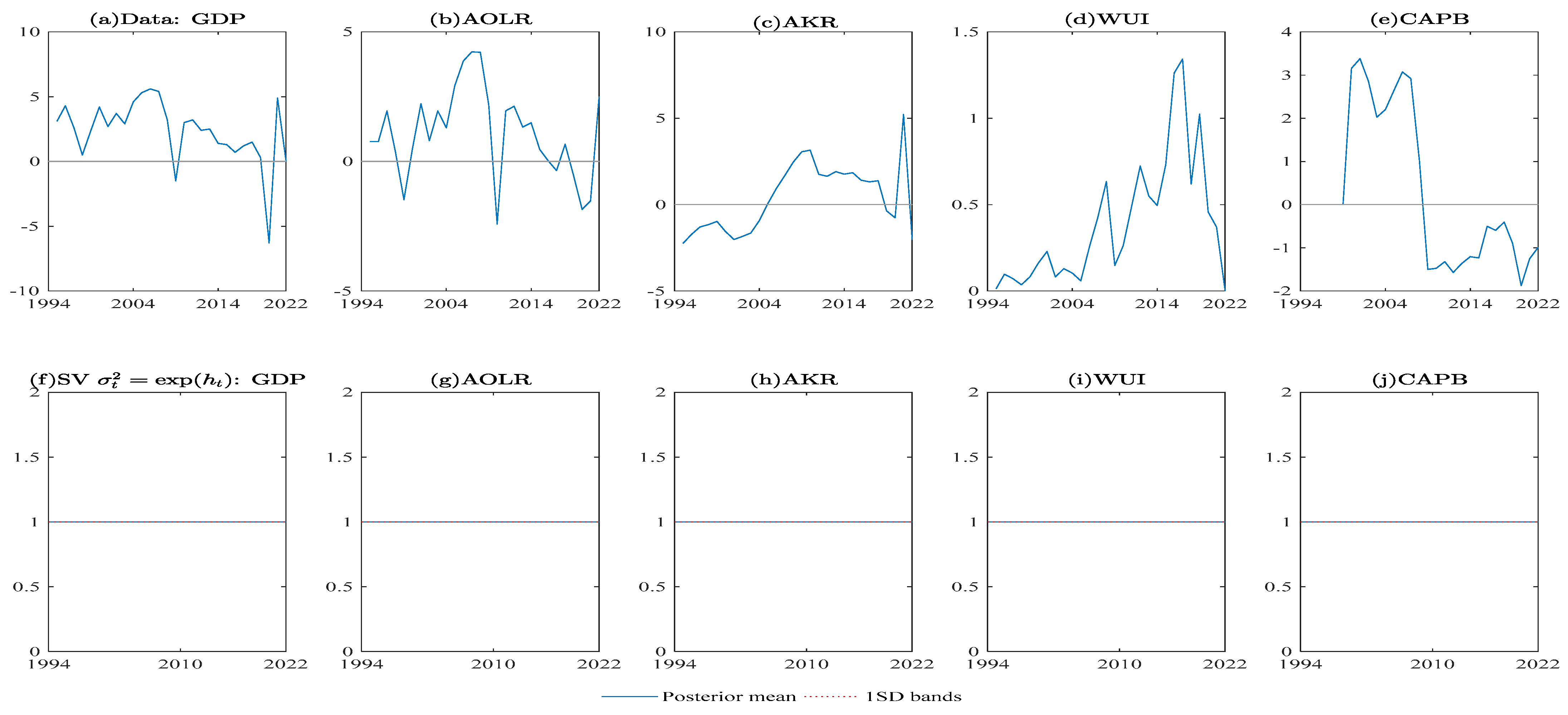

Table 9 reports the estimation results for the TVP regression model. The standard deviation is wider than the stochastic volatility model, and the posterior means are slightly apart from the true value.

Figure A2 reflect that the posterior means trace the movement of the true values, and the 95% credible intervals tend to be narrower overall than the constant volatility model, and almost include the true values.

Figure 2 shows the sample autocorrelation function, the sample paths, and the posterior densities for the selected parameters. After discarding the initial 5000 samples in the burn-in period, the sample paths look stable, and the sample autocorrelations drop smoothly.

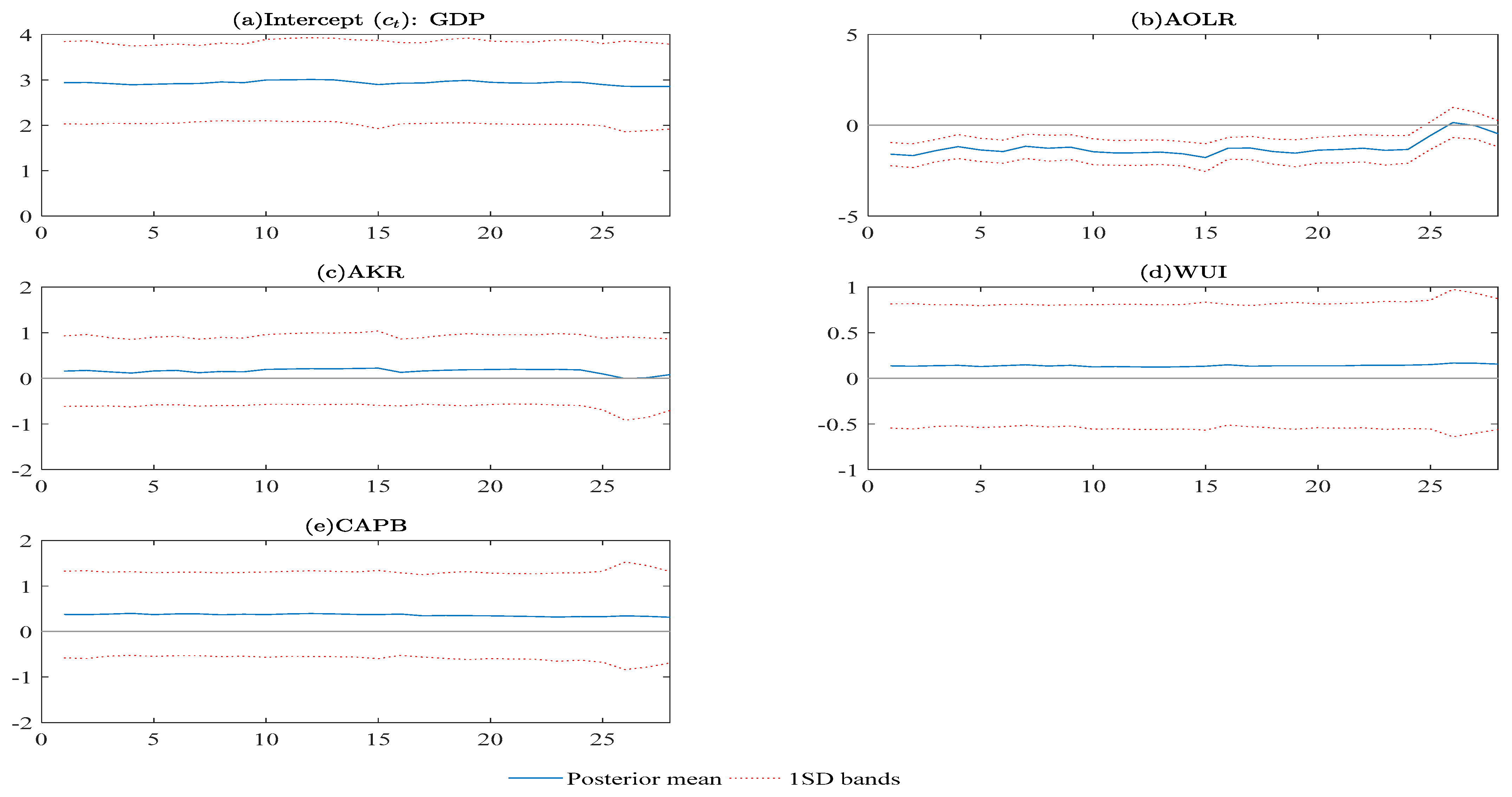

The properties of the state space model are reflected by the time-varying intercept in

Figure A3. The lag-order selection criteria of (LR, FPE, AIC, HQIC, and SBIC) are presented in

Table A1. The criteria LR, AIC, HQIC, and SBIC recommend the use of the optimal 4 lag. The paper concludes with an optimal 4. The results of the Johansen cointegration tests, in

Table A2, show that the null hypothesis for the zero cointegrating equation is rejected at a 0.05 significance level. All of the trace statistics are greater than the critical value, therefore there is no long-run relationship. Therefore, the VAR in the TAP-VAR is valid to be used.

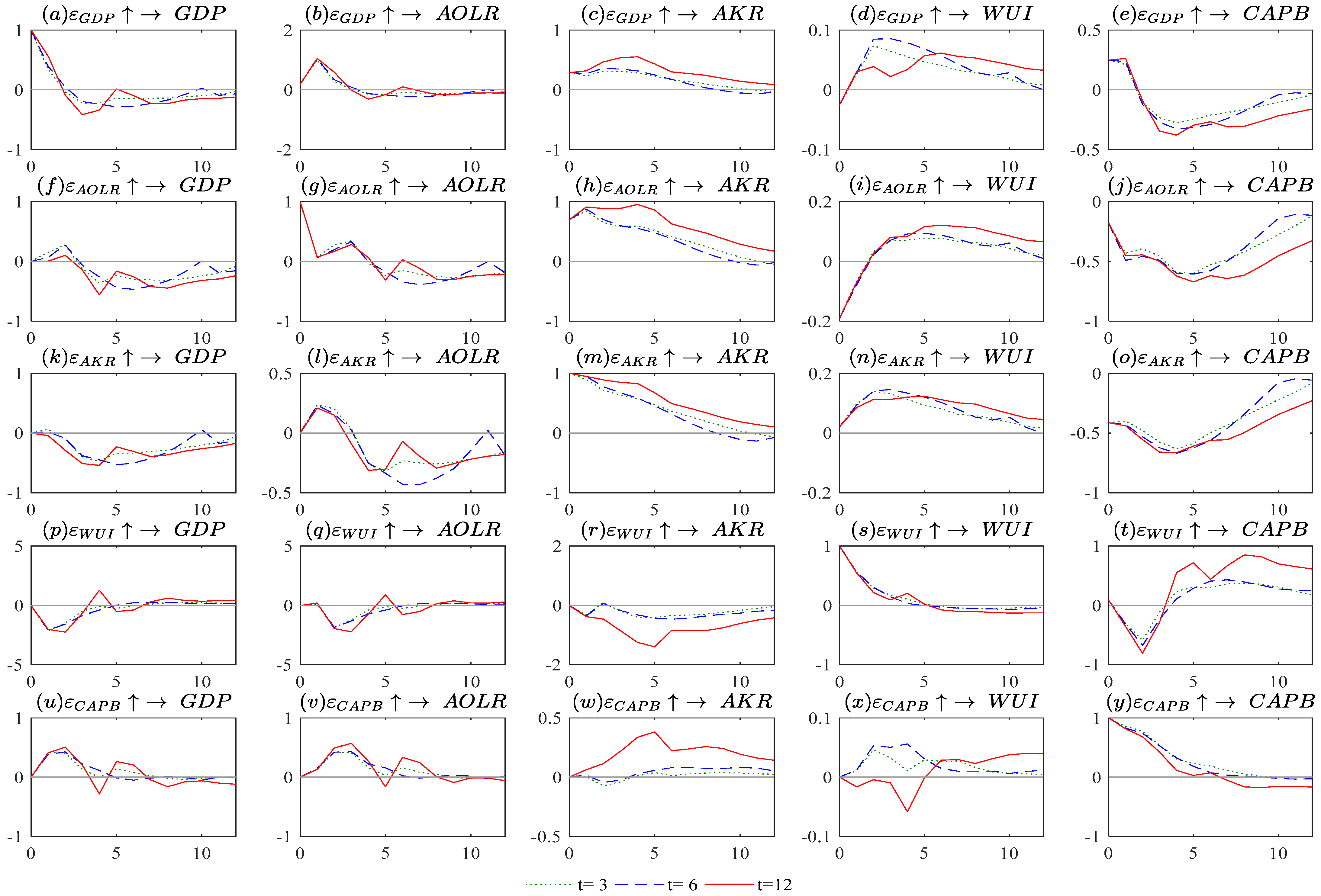

Figure 3 reflects the time-varying coefficient from 1994 to 2022. In graph p, there is a reflection of world uncertainty for South Africa. It is noted that, if uncertainty is expected in the next one- and three-year periods, it results in the economic growth operating below equilibrium. However, when uncertainty is expected in 6 years, the economic growth performs better. This may be because fiscal consolidation provides an accommodative policy and because there is an opportunity to implement better planning to account for the uncertainty when it is expected to occur far in the future. On the other hand, graph u reflects the impact of fiscal consolidation on economic growth. It is noted that, in the presence of fiscal consolidation, the economic growth operates above equilibrium. However, in the 1990 and 2000s, there is a reflection of volatility in economic growth. On the other hand, in recent times, economic growth is above the equilibrium in the presence of fiscal consolidation.

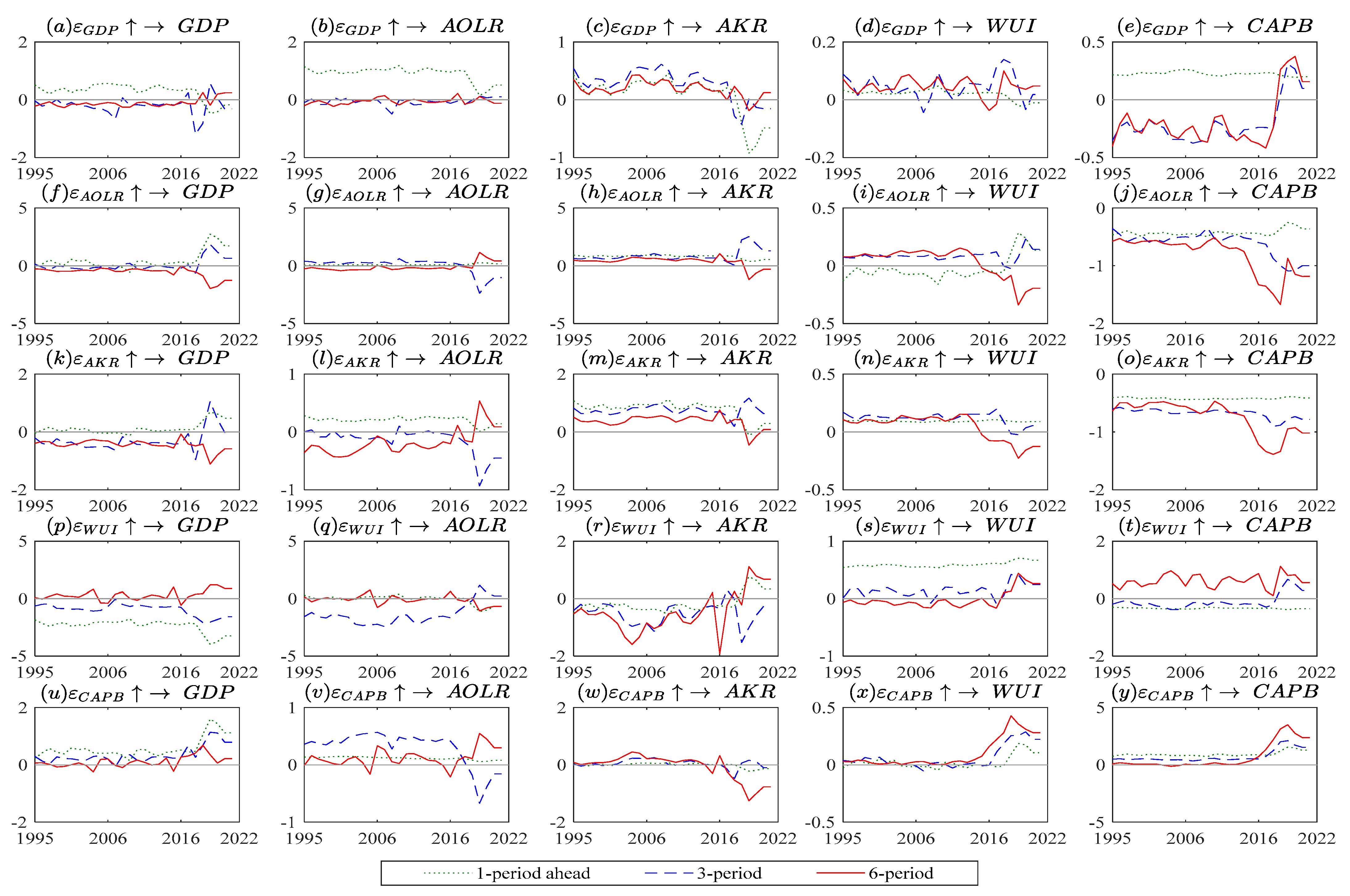

Figure 4 shows the time-varying impulse response functions.

Figure 4, graph p provides evidence that the shock of macroeconomic uncertainty harms

. There is evidence that

results in a negative impact of 1.5% to 2.5% on

in years 1 and 2, respectively. This result is similar to those of

Redl (

2018),

Bournakis and Ramirez-Rondan (

2022), and

Tunc et al. (

2022), who found a negative impact for macroeconomic uncertainty on economic growth. The

is in the negative values until year 5, when

records a 1% increase; thereafter,

normalizes around the equilibrium. The time reach equilibrium is better by year 4, which is similar to the result obtained by

Binge and Boshoff (

2020).

Figure 3, graph u provides evidence that the shock of fiscal consolidation,

has a positive effect on

from year 1 to year 2 as

increases by 0.3 to 0.5%. However, after year 2, there is a drastic decrease in

to 0%, and then a further decrease of 0.2%. This are similar to the findings of

Bardaka et al. (

2021) and

Caselli and Reynaud (

2020), who note that fiscal consolidation has a negative impact on the gross domestic product. This may have critical implications and put the economy in recession. There is a possibility of a further negative effect on the economy if the recession occurred as a result of the adoption of fiscal consolidation. Nevertheless,

shows resilience, as it rebounds in year 5 with a positive rate of 0.1%. After that,

falls and does not return to equilibrium; it operates below the equilibrium level. This result suggests that fiscal consolidation cannot be used in the effort to stimulate economic growth.

5. Conclusions

There has been growing interest in the effort to investigate the impact of macroeconomic uncertainty on economic growth. However, there is no agreement in the findings of scholars as to what the impact of macroeconomic uncertainty on economic growth is. South Africa has been lagging in its efforts to achieve an economic growth rate of 5%, which is stipulated in the National Development Plan of 2013. On the other hand, fiscal authorities have been showing commitment to adopting fiscal consolidation. The issues with South Africa’s economy cannot be isolated to macroeconomic uncertainty. However, less attention has been given to the investigation of macroeconomic uncertainty in different regimes of economic growth in South Africa. The key contribution of this paper is to fill this gap in the effort to understand the impact of macroeconomic uncertainty in the presence of fiscal consolidation.

In this regard, it is important to investigate the impact of macroeconomic uncertainty on different regimes of economic growth in the presence of fiscal consolidation in South Africa. Markov-switching dynamic regression and time-varying vector autoregression (TA-VAR) were performed using time series data from 1994 to 2022. Three states are found for economic growth, with mean rates of negative 6.72%, 4.38% and 3.08% in the respective states. It is recommended that fiscal authorities revise the policy of the NDP with the key tangible target. The formulation of policy is critical in accounting for the state of the economy, as outlined above.

Macroeconomic uncertainty was found to have negative impacts of 6.729%, 4.385% and 3.080% in states 1 to 3, respectively. Fiscal consolidation provided an accommodative policy, as it reduced the negative impact of macroeconomic uncertainty by 3.57%, 1.996% and 0.92% in states 1 to 3, respectively. Investment and consumer expenditure may decline as a result of policy uncertainty, which might have a detrimental effect on economic growth. In the meantime, fiscal consolidation, which is the process of cutting government expenditure while raising income, can hinder economic development in the near term, since it decreases demand. On the other hand, fiscal consolidation has the potential to lower government debt over the long run, boost economic confidence, and produce a more stable political climate. These factors can drive spending and investment, which will ultimately result in better rates of economic growth. It is in this context that South African fiscal authorities and policymakers may face tradeoffs when trying to counter macroeconomic uncertainty. Therefore, further studies may be needed to ascertain the magnitude of the tradeoffs in order to make informed decisions.

Nevertheless, in this paper, it was found that fiscal consolidation does not completely reduce the negative impact of macroeconomic uncertainty. The transition probabilities of economic growth moving and returning to the same states are 29.46%, 34.07%, and 58.02% in each state, respectively. The time-varying impulse response functions showed that the shock of macroeconomic uncertainty harms economic growth. Nevertheless, the multiplier effect is not large; however, the economy operates below equilibrium and does not return to equilibrium after the effects of macroeconomic uncertainty. This reflects that it takes time for macroeconomic uncertainty to filter out of the South African economy. It is recommended that fiscal consolidation be considered as an accommodative fiscal policy to reduce macroeconomic uncertainty but not as a main policy for economic growth. The dummy variable reflecting the structural break of the fiscal consolidation, is found to have a positive impact on economic growth. This reflects that, in the case of a quick change or adoption of fiscal consolidation, there is a 1.962% chance that there will be an increase in economic growth. On the other hand, the structural break for macroeconomic uncertainty is found to result in a 3.765% chance of a fall in the gross domestic product. This reflects that unexpected change over time on macroeconomic uncertainty harms economic growth. South Africa fiscal author need to put in place economic model that can forecast unexpected change that can affect economic growth.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}