Macroeconomic Factors of Consumer Loan Credit Risk in Central and Eastern European Countries

, , ,

, , ,

Abstract

:1. Introduction

- (1)

- to improve the classifications of factors influencing both systematic and unsystematic banking credit risk; to advance the classification of macroeconomic factors influencing consumer loan credit risk by analysing not only the group of general macroeconomic condition factors but also other groups;

- (2)

- to assess the overall (aggregate) impact of the general macroeconomic condition factors on the consumer loan credit risk;

- (3)

- to assess the impact of the macroeconomic condition factors (i.e., factors of (i) the direction of the economy, (ii) financial market conditions, and (iii) institutional environment) on the consumer loan credit risk;

- (4)

- to assess the overall (aggregate) impact of the macroeconomic factors on the consumer loan credit risk.

- (i)

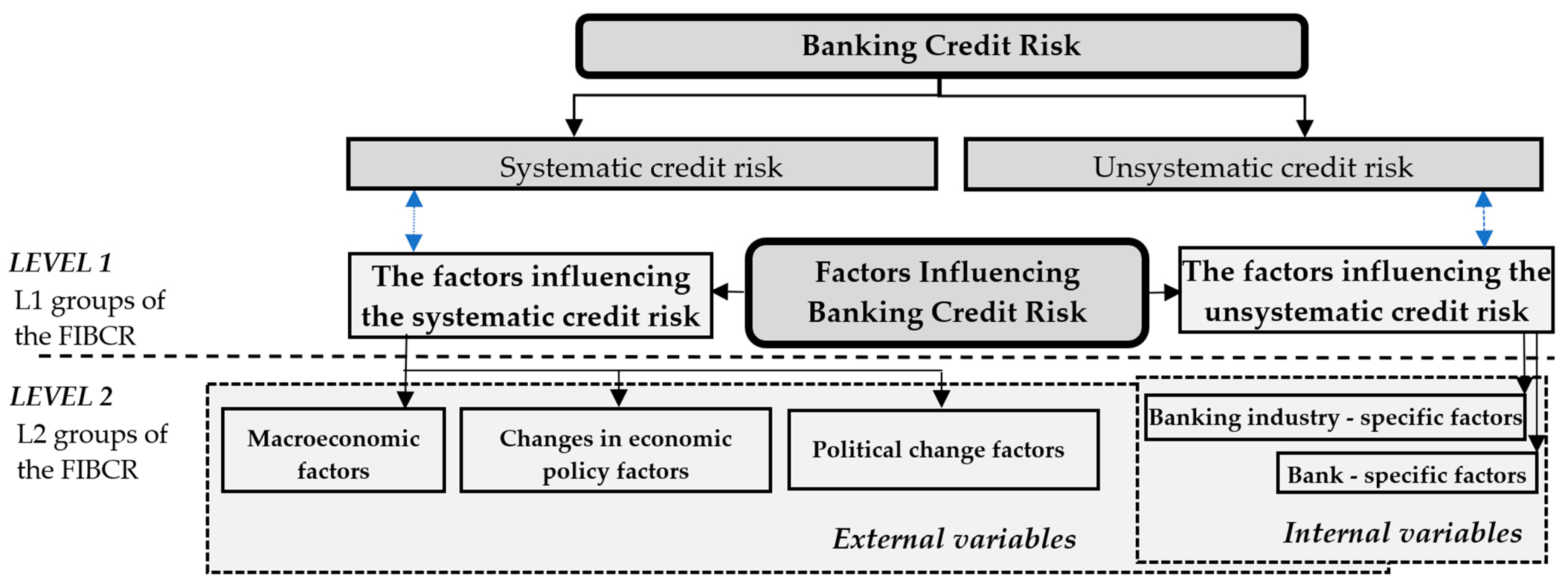

- To investigate the systematic and unsystematic factors influencing banking credit risk, it is necessary to classify them at different levels. An analysis of the scientific literature on credit risk factors has concluded that no single approach exists, i.e., different trends can be identified. This study proposes an improved and detailed (at five different levels) classification of factors influencing banking credit risk. This classification can be beneficial for more enhanced analysis of the factors influencing banking credit risk for the whole loan portfolio and for different types of loans, e.g., consumer loans.

- (ii)

- Previous studies have analysed only a few of the most commonly identified macroeconomic determinants of banking credit risk, while other potential determinants have remained outside the scope of the study. This study focuses on a more detailed classification of the macroeconomic determinants of banking credit risk.

2. Classifications of Factors Influencing Systematic Banking Credit Risk

- (1)

- only macroeconomic factors such as the FICR (e.g., Castro (2013); Mileris (2013); Washington (2014); Beck et al. (2015); Koju et al. (2020)).

- (2)

- only bank-specific factors such as the FICR (e.g., Boyd and De Nicoló (2005); Podpiera and Weill (2008); Rossi et al. (2009); Haq and Heaney (2012); Zhang et al. (2016)).

- (3)

- both macroeconomic and bank-specific variables such as the FICR (e.g., Salas and Saurina (2002); Espinoza and Prasad (2010); Louzis et al. (2012); Abusharbeh (2020)). For instance, Abusharbeh (2020) examines the influence of macroeconomic and bank-specific factors on credit quality (in Palestine, 2007–2018). The analysis uses five macroeconomic factors and three bank-specific factors. In the analysis of the nine largest Greek banks from 2003 to 2009, Louzis et al. (2012) examine the effect of macroeconomic and bank-specific variables on loan quality. As macroeconomic variables that are exogenous to the banking industry, the authors use (i) the real GDP growth rate, (ii) the unemployment rate, and (iii) the lending rates. Louzis et al. (2012) emphasise that bank-specific variables possess additional explanatory power, and in their research, the authors use the following variables: return on equity, solvency ratio, inefficiency, non-interest income, leverage ratio, size, and ownership concentration.Several different models in one research are presented by Dimitrios et al. (2016), i.e., the models use (i) only macroeconomic variables, (ii) only bank-specific variables, and (iii) both macroeconomic and bank-specific variables.

- (4)

- both macroeconomic and banking-industry-specific variables such as the FICR (e.g., Ghosh (2015); Zheng et al. (2020)). More specifically, after empirical research, Nikolaidou and Vogiazas (2017) conclude that the analysis of the determinants of NPLs “primarily points to the importance of macroeconomic factors and to lesser-extent industry factors” (in the five Sub-Saharan Africa (SSA) countries). Zheng et al. (2020) have discovered the impact of these determinants of NPLs across the entire banking system of Bangladesh for the period 1979–2018, and the results of the research show that both macroeconomic and industry-specific factors influence NPLs significantly. Ghosh (2015) examines macroeconomic (i.e., state-level banking-industry-specific as well as region economic) and banking-industry-specific determinants of NPLs in both commercial banks and savings institutions in the US for 1984–2013.

- (5)

- three groups of the FICR, i.e., (i) macroeconomic, (ii) banking-industry-specific, and (iii) bank-specific variables. For instance, Naili and Lahrichi (2022a) provide a structured review of the literature on the determinants of NPLs and discuss three groups of NPL determinants: macroeconomic, industry-related, and bank-specific determinants. Additionally, the analysis of the data of 53 banks listed in five Middle Eastern and North African emerging markets between 2000 and 2019 and the empirical study by these authors indicate that NPLs can be explained “mainly by macroeconomic variables and bank-specific factors”, whereas industry-specific factors, specifically interbank competition, have an insignificant impact on NPLs.

- (1)

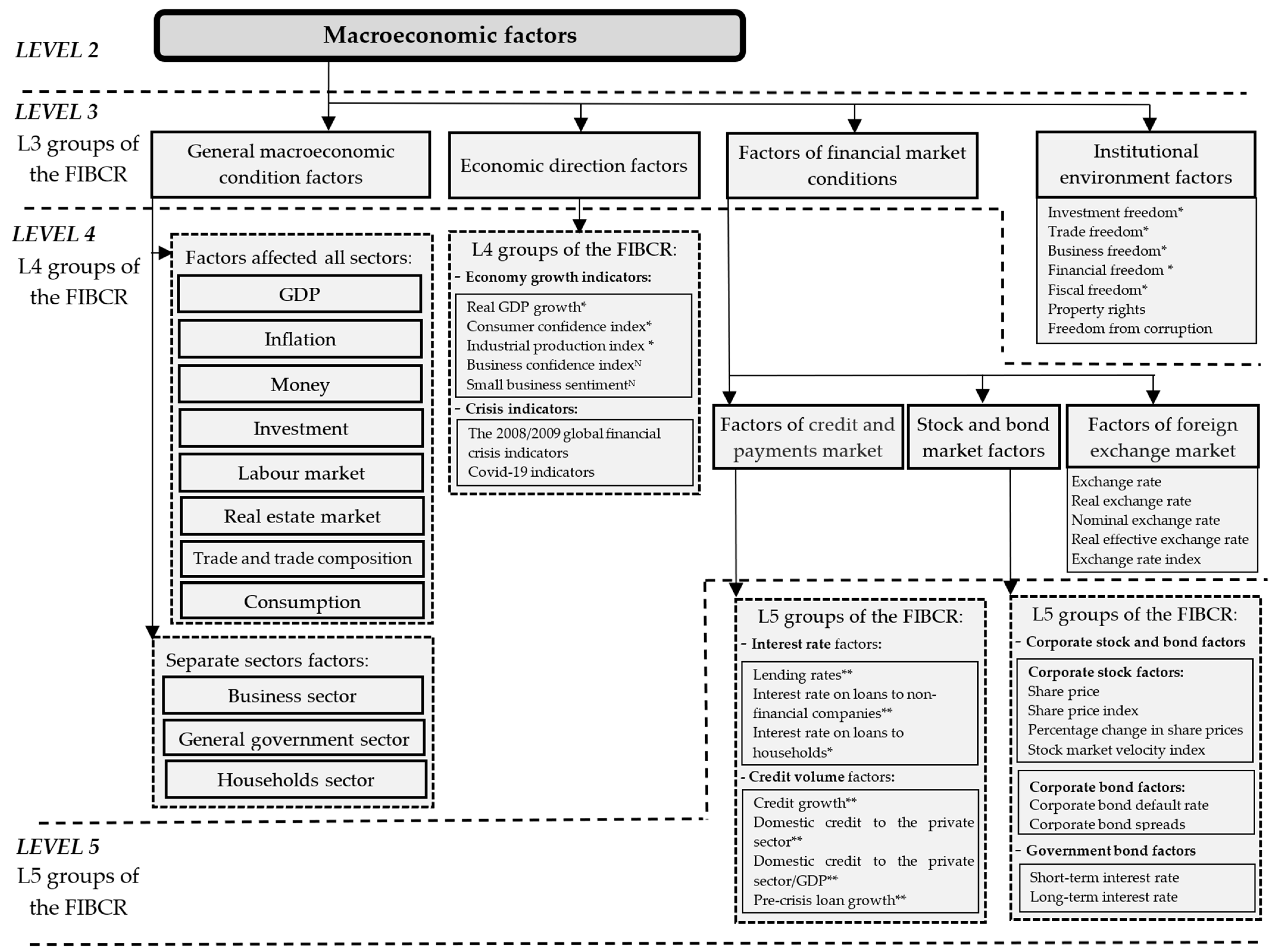

- Liao and Chang (2005) combine economic and financial variables and identify three factors: (i) the real economy, (ii) inflation, and (iii) housing. According to the authors, the real economic factor includes the following variables: GDP deflator, industrial production, personal income, and unemployment. The inflation factor includes (i) the consumer price index (CPI) and (ii) the producer price index (PPI). The housing factor includes the following five variables: (i) house price index (HPI), (ii) delinquency of all US real estate mortgage loans, (iii) delinquency of US real estate subprime mortgage loans, (iv) foreclosure of all US real estate mortgage loans, and (v) foreclosure of US real estate subprime mortgage loans.

- (2)

- Figlewski et al. (2012) and Mileris (2013) distinguish macroeconomic factors into three groups: (i) general macroeconomic condition factors (e.g., unemployment rate, inflation, etc.), (ii) economic direction factors (this group includes the real GDP growth, the growth of industrial production, and the change in consumer sentiment), and (iii) factors of the financial market conditions (this group includes interest rates (such as a 3-month T-Bill rate, a long-term interest rate (10-year Treasury), stock market returns (such as S&P 500 returns, Russell 2000 index returns, etc.), and the corporate bond default rate).

- (3)

- In addition to the studies discussed above, in the context of classification, it is worth discussing the study by Feldkircher (2014). To explain the distinct response of the real economy of the countries to the 2008 global financial crisis, the researcher uses 43 macroeconomic determinants that measure macroeconomic risks and divides them into six groups, i.e., not only the (i) “GDP and investment”, (ii) “money and inflation”, (iii) “monetary regime”, (iv) “trade and trade composition”, and (v) “business environment and labour market” groups but also the group of “institutional quality” are distinguished.

3. Research Hypotheses

3.1. The Dependent Variables

3.2. The Independent Variables and Development of Hypotheses

3.2.1. Variables of General Macroeconomic Conditions

3.2.2. Variables of the Direction of the Economy

3.2.3. Variables of the Financial Market Conditions: (i) Factors of the Credit and Payment Market

3.2.4. Variables of the Financial Market Conditions: (ii) Factors of the Stock and Bond Market

3.2.5. Variables of the Financial Market Conditions: (iii) Factors of the Foreign Exchange Market

3.2.6. Variables of the Institutional Environment

4. Data and Methodology

4.1. Data Selection

4.2. Model Specification

- i = 1, 2, …, N and t = 1, 2, …, T;

- N—number of cross-sections;

- T—number of periods;

- —dependent variable;

- —intercept;

- —coefficient;

- —independent variable;

- —error.

- —intercept;

- —error.

- At first, analysing the group of general macroeconomic condition factors, the “best-performing” variable representing each L4 group of the FIBCR is selected. Based on the previously mentioned criteria and according to the results obtained by Kanapickienė et al. (2022), the following variables are selected: GDP gap (output GAP), GDP deflator, money supply (M2) growth rate, long-term unemployment rate, capital investment, current account balance, house price index, industry value to GDP, budget balance to GDP, and wages and salaries per employee. The multiple regression models of the overall (aggregate) impact of the general macroeconomic condition factors on the consumer loan credit risk are constructed.

- Secondly, the “best-performing” variables representing the groups of factors of the direction of the economy, financial market conditions (credit and payment market, stock and bond market, foreign exchange market), and institutional environment are selected (these are consumer confidence index, cases of COVID-19, domestic credit to private sector to GDP, share price index, exchange rate, and investment freedom). Then, multiple regression models of the overall (aggregate) impact of the macroeconomic factors on the consumer loan credit risk are constructed.

5. Results

5.1. Variables of the General Macroeconomic Condition

5.2. Variables of the Direction of the Economy

5.3. Variables of the Financial Market Conditions: (i) Factors of the Credit and Payment Market

5.4. Variables of the Financial Market Conditions: (ii) Factors of the Stock and Bond Market

5.5. Variables of the Financial Market Conditions: (iii) Factors of the Foreign Exchange Market

5.6. Variables of the Institutional Environment

5.7. Overall Assessment of the Impact of Macroeconomic Factors

6. Discussion

7. Conclusions

- (i)

- economy growth indicators proved to have a risk-decreasing effect in CEE countries; the effect of crisis indicators (COVID-19-related variables) appeared to have an impact (risk-decreasing) on NPDs.

- (ii)

- it was confirmed that, in the case of CEE countries, credit market indicators have statically significant positive (risk-increasing) or statistically insignificant effects on NPLs.

- (iii)

- most of the analysed stock and bond market variables appeared to have a statistically significant impact on consumer loan credit risk in the group of CEE countries: bond market indicators proved to have a positive impact on NPLs, while stock market indicators had a negative impact.

- (iv)

- one of the foreign exchange market indicators (exchange rate) appeared to have a statistically significant negative effect on NPLs in CEE countries.

- (v)

- property rights and investment freedom variables appeared to have a statistically significant negative impact on consumer loan credit risk in CEE countries, while the effect of the rest of the institutional environment variables was proven to be insignificant.

Author Contributions

Funding

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Credit Risk Proxies | Authors |

|---|---|

| (1) expected default frequency | (Sommar and Shahnazarian 2009; Beck et al. 2015; Mpofu and Nikolaidou 2018) |

| (2) probability of default (PD) | (Jiménez and Saurina 2004; Bonfim 2009; Buncic and Melecky 2013; Johnson et al. 2017; Carvalho et al. 2020) |

| (3) loan loss provisions | (Quagliariello 2007; Buncic and Melecky 2013; Karoglou et al. 2018) |

| (4) loss given default | (Beck et al. 2015; Mpofu and Nikolaidou 2018) |

| (5) new bad debts | (Quagliariello 2007) |

| (6) loan loss reserves | (Love and Turk Ariss 2014) |

| (7) non-performing loans (NPLs) | (Buncic and Melecky 2013; Beck et al. 2015; Gila-Gourgoura and Nikolaidou 2018; Karoglou et al. 2018; Mpofu and Nikolaidou 2018; Koju et al. 2020; Foglia 2022; Naili and Lahrichi 2022a) |

| (7a) NPLs ratio | (De Bock and Demyanets 2012; Buncic and Melecky 2013; Kjosevski and Petkovski 2017; Zheng et al. 2020) |

| (7b) The logit transformation | (Espinoza and Prasad 2010) |

| The Impact of GDP Growth Variables on Credit Risk | Authors |

|---|---|

| (a) The impact of GDP growth variables on credit risk | |

| (i) significantly positive | (Beck et al. 2015) |

| (ii) negative | (Gila-Gourgoura and Nikolaidou 2018) (cite Messai and Jouini’s (2013) findings); (Washington 2014) |

| (iii) significantly negative | (Espinoza and Prasad 2010; Nkusu 2011; De Bock and Demyanets 2012; Castro 2013; Washington 2014; Beck et al. 2015; Mpofu and Nikolaidou 2018) |

| (iv) insignificant | (Aver 2008; Haniifah 2015) |

| (b) The impact of interest rates on credit risk | |

| (i) positive | (Espinoza and Prasad 2010; Castro 2013; Messai and Jouini 2013; Abusharbeh 2020) |

| (ii) negative | (Sulganova 2016; Karoglou et al. 2018) |

| (iii) insignificant | (Maltritz and Molchanov 2014); (Ghosh 2015) |

| (c) The impact of lending interest rate on credit risk | |

| (i) positive | (Louzis et al. 2012; Washington 2014; Beck et al. 2015; Zheng et al. 2020) |

| (ii) insignificant | (De Bock and Demyanets 2012) |

| (d) The impact of credit growth on credit risk | |

| (i) positive | (Castro 2013; Karoglou et al. 2018; Bayar 2019; Tatarici et al. 2020) |

| (ii) negative | (Washington 2014; Agic and Gacic 2021) |

| (iii) insignificant | (De Bock and Demyanets 2012) |

| (e) The impact of the variables of corporate stock on credit risk | |

| (i) positive | corporate stock (Aver 2008), spread of corporate over government bond yields (Lehmann and Manz 2006) |

| (ii) negative | corporate stock (Castro 2013; Yurdakul 2014 (as cited by Gila-Gourgoura and Nikolaidou (2018))) |

| (iii) insignificant | stock market index (Abusharbeh 2020) |

| (f) The impact of government bond factors on credit risk | |

| (i) positive | government bond yield (Bonfim 2009) the spread between the yield on the 10-year Italian government bond and the corresponding German one (Gila-Gourgoura and Nikolaidou 2018) |

| (ii) significantly positive | the 90-day Treasury bill rate (in the banking systems of Uganda and Namibia) (Nikolaidou and Vogiazas 2017) |

| (iii) negative | government bond interest rate (Maltritz and Molchanov 2014) the 90-day Treasury bill rate (in the banking systems of of South Africa) (Nikolaidou and Vogiazas 2017) |

| (iv) significantly negative | the average interest rate on a 1-year T-bill (in the banking system of Zambia) (Nikolaidou and Vogiazas 2017) |

| (v) insignificant | the US 10-year Treasury yield (Duffie et al. 2007) |

| (g) The impact of exchange rate on credit risk | |

| (i) significantly positive | (Nkusu 2011; Castro 2013; Kjosevski et al. 2019) |

| (ii) significantly negative | (Washington 2014; Nikolaidou and Vogiazas 2017) |

| (iii) insignificant | (Aver 2008; Wong et al. 2010; Nkusu 2011; Nikolaidou and Vogiazas 2017; Abusharbeh 2020) |

| (h) The impact of the institutional environment factors on credit risk | |

| (i) significantly positive | trade freedom (in developed countries) (Maltritz and Molchanov 2014) |

| (ii) insignificantly positive | business freedom (in developed countries) (Maltritz and Molchanov 2014) trade freedom (in emerging economies) (Maltritz and Molchanov 2014) |

| (iii) insignificantly negative | business freedom (in emerging economies) (Maltritz and Molchanov 2014) fiscal freedom (in developed countries and in emerging economies) (Maltritz and Molchanov 2014) freedom from corruption, property rights, financial freedom, investment freedom (both in developed countries and in emerging economies) (Maltritz and Molchanov (2014) |

Appendix B

| Symbol | Variable | Measurement Unit | Data Source |

|---|---|---|---|

| Dependent variables | |||

| Y1 | Non-performing loans for consumption-to-total loans | Percent | Deloitte |

| Y2 | Total loans for consumption | Mln. Eur. | ECB Statistical Data Warehouse |

| Factors of direction of economy | |||

| Economy growth indicators | |||

| X1 | Real GDP growth rate | Percent | FRED Economic Data; own calculations |

| X2 | Consumer confidence index (CCI) | Index (points) | Eurostat |

| X3 | Industrial production index | Percent | OECD Statistics |

| Crisis indicators | |||

| X4 | Cases of COVID-19 | Total number of cases per mln. | Matheu et al. (2020) |

| X5 | Deaths from COVID-19 | Total number of deaths per mln. | Matheu et al. (2020) |

| X6 | Stringency index | Index (points) | Matheu et al. (2020) |

| X7 | COVID-19 pandemic | Dummy variable (0 = no pandemic; 1 = pandemic) | - |

| X8 | The 2008–2009 global financial crisis | Dummy variable (0 = no crisis; 1 = crisis) | - |

| Factors of financial market conditions | |||

| Factors of credit and payment market | |||

| X9 | Credit growth | Percentage change | CEIC Data Global Database |

| X10 | Domestic credit to the private sector | Mln. Eur. | ECB Statistical Data Warehouse |

| X11 | Domestic credit to private sector-to-GDP | Percent | Worldbank Data |

| X12 | Interest rates on loans to non-financial companies | Percent | OECD Statistics |

| X13 | Interest rates on loans to households | Percent | OECD Statistics |

| Factors of stock and bond market | |||

| X14 | Share price index | CEIC Data Global Database | |

| X15 | Percentage change in stock market prices | CEIC Data Global Database | |

| X16 | Short-term interest rate | OECD Statistics | |

| X17 | Long-term interest rate | OECD Statistics | |

| Factors of foreign exchange market | |||

| X18 | Exchange rate | Eurostat | |

| X19 | Real exchange rate | FRED Economic Data | |

| Institutional environment factors | |||

| X20 | Freedom from corruption | Index (points) | The Heritage Foundation |

| X21 | Property rights | Index (points) | The Heritage Foundation |

| X22 | Investment freedom | Index (points) | The Heritage Foundation |

| X23 | Trade freedom | Index (points) | The Heritage Foundation |

| X24 | Business Freedom | Index (points) | The Heritage Foundation |

| Factors of general macroeconomic condition | |||

| X1 mcee | GDP gap (Output gap) | Per cent | OECD Statistics |

| X2 mcee | GDP deflator | Per cent | CEIC Data Global Database |

| X3 mcee | Money supply (M2) growth rate | Per cent | CEIC Data Global Database |

| X4 mcee | Long-term unemployment rate | Per cent | Eurostat |

| X5 mcee | Capital investment | Per cent of GDP | The Global Economy |

| X6 mcee | Current account balance | Per cent | Worldbank Data |

| X7 mcee | House price index | Index (points, annual average) | Eurostat |

| X8 mcee | Industry-value-to-GDP | Per cent | Worldbank Data |

| X9 mcee | Budget-balance-to-GDP | Per cent | Eurostat |

| X10 mcee | Wages and salaries per employee | Eur. | OECD Statistics |

| Dependent Variables | ||||

|---|---|---|---|---|

| Levin, Lin and Chu t * Probability | ||||

| Y1 | Non-performing loans for consumption-to-total loans | −9.672 | <0.0001 ** | |

| Y2 | Total loans for consumption | −4.698 | <0.0001 ** | |

| Factors of direction of economy | ||||

| Economy growth indicators | ||||

| X1 | Real GDP growth rate | - | - | - |

| X2 | Consumer confidence index (CCI) | −5.418 | <0.0001 ** | |

| X3 | Industrial production index | - | - | -. |

| Crisis indicators | ||||

| X4 | Cases of COVID-19 | <0.0001 ** | ||

| X5 | Deaths from COVID-19 | - | - | - |

| X6 | Stringency index | - | - | - |

| X7 | COVID-19 pandemic | - | - | - |

| X8 | The 2008–2009 global financial crisis | - | - | - |

| Factors of financial market conditions | ||||

| Factors of credit and payment market | ||||

| X9 | Credit growth | −2.960 | <0.0001 ** | 1st diff. |

| X10 | Domestic credit to the private sector | - | - | - |

| X11 | Domestic credit to private sector-to-GDP | −3.429 | <0.0001 ** | |

| X12 | Interest rates on loans to non-financial companies | - | - | - |

| X13 | Interest rates on loans to households | - | - | - |

| Factors of stock and bond market | ||||

| X14 | Share price index | −4.885 | <0.0001 ** | |

| X15 | Percentage change in stock market prices | −16.042 | <0.0001 ** | |

| X16 | Short-term interest rate | −38.344 | <0.0001 ** | |

| X17 | Long-term interest rate | −7.181 | <0.0001 ** | |

| Factors of foreign exchange market | ||||

| X18 | Exchange rate | −2.051 | 0.020 * | |

| X19 | Real exchange rate | −8.793 | <0.0001 ** | |

| Institutional environment factors | ||||

| X20 | Freedom from corruption | −3.553 | <0.0001 ** | |

| X21 | Property rights | −3.445 | <0.0001 ** | 1st diff. |

| X22 | Investment freedom | −5.361 | <0.0001 ** | |

| X23 | Trade freedom | - | - | - |

| X24 | Business Freedom | −6.531 | <0.0001 ** | |

| Factors of general macroeconomic condition | ||||

| X1 mcee | GDP gap (Output gap) | −7.018 | <0.0001 ** | |

| X2 mcee | GDP deflator | −3.874 | <0.0001 ** | 1st diff. |

| X3 mcee | Money supply (M2) growth rate | −2.384 | 0.009 ** | |

| X4 mcee | Long-term unemployment rate | −7.243 | <0.0001 ** | 1st diff. |

| X5 mcee | Capital investment | −14.219 | <0.0001 ** | |

| X6 mcee | Current account balance | −5.773 | <0.0001 ** | |

| X7 mcee | House price index | −6.276 | <0.0001 ** | 1st diff. |

| X8 mcee | Industry-value-to-GDP | −3.154 | <0.0001 ** | |

| X9 mcee | Budget-balance-to-GDP | −9.339 | <0.0001 ** | 1st diff. |

| X10 mcee | Wages and salaries per employee | −8.679 | <0.0001 ** | 1st diff. |

| Primary Model | Final Model I | Final Model II | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Symbol | Variable | Coefficient | t-Statistic | Prob. | Coefficient | t-Statistic | Prob. | Coefficient | t-Statistic | Prob. |

| C | 2.207 | 0.254 | 0.799 | 8.397 | 21.878 | <0.0001 ** | 1.726 | 0.696 | 0.487 | |

| X1 mcee | GDP gap (Output gap) | 0.078 | 0.486 | 0.629 | ||||||

| X2 mcee | GDP deflator | −0.396 | −2.195 | 0.032 * | −0.598 | −4.322 | <0.0001 ** | |||

| X3 mcee | Money supply (M2) growth rate | −0.089 | −1.515 | 0.134 | ||||||

| X4 mcee | Long-term unemployment rate | 0.044 | 0.810 | 0.421 | ||||||

| X5 mcee | Capital investment | −0.339 | −1.472 | 0.146 | ||||||

| X6 mcee | Current account balance | 0.025 | 0.132 | 0.896 | 0.238 | 2.005 | 0.048 * | |||

| X7 mcee | House price index | −0.149 | −2.321 | 0.023 * | −0.165 | −4.232 | <0.0001 ** | −0.242 | −6.014 | <0.0001 ** |

| X8 mcee | Industry-value-to-GDP | 0.532 | 1.543 | 0.128 | 0.219 | 2.297 | 0.024 * | |||

| X9 mcee | Budget-balance-to-GDP | 0.121 | 1.122 | 0.266 | 0.201 | 2.553 | 0.012 * | 0.212 | 2.545 | 0.012 * |

| X10 mcee | Wages and salaries per employee | −0.121 | −0.689 | 0.493 | ||||||

| R-squared | 0.353 | 0.329 | 0.354 | |||||||

| F test | <0.0001 | <0.0001 | <0.0001 | |||||||

| Hausman test | <0.0001 | <0.0001 | 0.182 | |||||||

| Model | Fixed effects | Fixed effects | Random effects | |||||||

| Observations | 87 | 106 | 106 | |||||||

| Symbol | Variable | Coefficient | t-Statistic | Prob. | R sq. | Observ. | F Test | Hausman Test | Model |

|---|---|---|---|---|---|---|---|---|---|

| General macroeconomic condition factors | |||||||||

| Factors of direction of economy | |||||||||

| Economy growth indicators | |||||||||

| X2 | Consumer confidence index (CCI) | −0.094 | −3.599 | 0.001 ** | 0.107 | 110 | 0.000 | 0.177 | Random effects |

| Crisis indicators | |||||||||

| X4 | Cases of COVID-19 | −7.37 × 10−5 | −3.794 | <0.0001 ** | 0.117 | 111 | 0.000 | 0.519 | Random effects |

| X7 | COVID-19 pandemic | −3.015 | −3.518 | 0.001 ** | 0.102 | 111 | 0.000 | 0.299 | Random effects |

| X8 | The 2008–2009 global financial crisis | −0.768 | −0.663 | 0.509 | 0.004 | 111 | 0.000 | 0.829 | Random effects |

| Factors of financial market conditions | |||||||||

| Factors of credit and payment market | |||||||||

| X9 | Credit growth | −0.023 | −0.661 | 0.510 | 0.004 | 108 | 0.000 | 0.267 | Random effects |

| X11 | Domestic credit to private sector-to-GDP | 0.191 | 5.391 | <0.0001 ** | 0.003 | 111 | 0.000 | 0.011 | Fixed effects |

| Factors of stock and bond market | |||||||||

| X14 | Share price index | −0.018 | −3.714 | <0.0001 ** | 0.609 | 111 | 0.000 | 0.057 | Fixed effects |

| X15 | Percentage change in stock market prices | 0.008 | 0.422 | 0.674 | 0.002 | 111 | 0.000 | 0.805 | Random effects |

| X16 | Short-term interest rate | 0.675 | 3.728 | 0.003 ** | 0.118 | 104 | 0.000 | 0.158 | Random effects |

| X17 | Long-term interest rate | 0.839 | 5.758 | <0.0001 ** | 0.243 | 105 | 0.000 | 0.174 | Random effects |

| Factors of foreign exchange market | |||||||||

| X18 | Exchange rate | −0.101 | −3.031 | 0.003 ** | 0.592 | 111 | 0.000 | 0.001 | Fixed effects |

| X19 | Real exchange rate | 0.018 | 0.257 | 0.798 | 0.001 | 111 | 0.000 | 0.798 | Random effects |

| Institutional environment factors | |||||||||

| X20 | Freedom from corruption | −0.005 | −0.300 | 0.765 | 0.005 | 111 | 0.000 | 0.032 | Fixed effects |

| X21 | Property rights | −0.082 | −2.233 | 0.028 * | 0.045 | 108 | 0.000 | 0.667 | Random effects |

| X22 | Trade freedom | −0.162 | −2.939 | 0.004 ** | 0.074 | 111 | 0.000 | 0.521 | Random effects |

| X24 | Business Freedom | 0.139 | 1.424 | 0.157 | 0.019 | 108 | 0.000 | 0.144 | Random effects |

| Symbol | Variable | Coefficient | t-Statistic | Prob. | R sq. | Observ. | F Test | Hausman Test | Model |

|---|---|---|---|---|---|---|---|---|---|

| General macroeconomic condition factors | |||||||||

| Factors of direction of economy | |||||||||

| Economy growth indicators | |||||||||

| X2 | Consumer confidence index (CCI) | −7.698 | −0.382 | 0.702 | 0.001 | 138 | 0.000 | 0.456 | Random effects |

| Crisis indicators | |||||||||

| X4 | Cases of COVID-19 | 0.020 | 1.138 | 0.257 | 0.009 | 139 | 0.000 | 0.632 | Random effects |

| X7 | COVID-19 pandemic | 1183.849 | 1.519 | 0.131 | 0.017 | 139 | 0.000 | 0.329 | Random effects |

| X8 | The 2008–2009 global financial crisis | −504.121 | −0.788 | 0.432 | 0.004 | 139 | 0.000 | 0.326 | Random effects |

| Factors of financial market conditions | |||||||||

| Factors of credit and payment market | |||||||||

| X9 | Credit growth | −1.719 | −0.074 | 0.942 | 0.007 | 130 | 0.000 | 0.016 | Fixed effects |

| X11 | Domestic credit to private sector-to-GDP | 32.683 | 1.493 | 0.137 | 0.016 | 137 | 0.000 | 0.214 | Random effects |

| Factors of stock and bond market | |||||||||

| X14 | Share price index | 7.804 | 2.241 | 0.027 * | 0.036 | 139 | 0.000 | 0.710 | Random effects |

| X15 | Percentage change in stock market prices | −3.659 | −0.321 | 0.748 | 0.001 | 139 | 0.000 | 0.428 | Random effects |

| X16 | Short-term interest rate | 44.007 | 0.394 | 0.694 | 0.006 | 132 | 0.000 | 0.028 | Fixed effects |

| X17 | Long-term interest rate | 57.422 | −0.559 | 0.577 | 0.003 | 127 | 0.000 | 0.168 | Random effects |

| Factors of foreign exchange market | |||||||||

| X18 | Exchange rate | −31.869 | −1.461 | 0.146 | 0.015 | 139 | 0.000 | 0.151 | Random effects |

| X19 | Real exchange rate | −3.366 | −0.071 | 0.943 | 0.001 | 139 | 0.000 | 0.307 | Random effects |

| Institutional environment factors | |||||||||

| X20 | Freedom from corruption | 10.489 | 1.114 | 0.267 | 0.009 | 139 | 0.000 | 0.668 | Random effects |

| X21 | Property rights | −16.007 | −0.550 | 0.583 | 0.002 | 130 | 0.000 | 0.759 | Random effects |

| X22 | Trade freedom | 156.236 | 3.715 | <0.0001 ** | 0.091 | 139 | 0.000 | 0.144 | Random effects |

| X24 | Business Freedom | −62.287 | −0.946 | 0.346 | 0.007 | 130 | 0.000 | 0.251 | Random effects |

| Primary Model | Final Model | ||||||

|---|---|---|---|---|---|---|---|

| Symbol | Variable | Coefficient | t-Statistic | Prob. | Coefficient | t-Statistic | Prob. |

| C | −13.435 | −1.403 | 0.165 | −10.786 | −1.989 | 0.049 * | |

| X1 mcee | GDP gap (Output gap) | −0.181 | −1.105 | 0.273 | |||

| X2 mcee | GDP deflator | −0.029 | −0.176 | 0.860 | −0.334 | −2.510 | 0.014 * |

| X3 mcee | Money supply (M2) growth rate | 0.009 | 0.165 | 0.869 | |||

| X4 mcee | Long-term unemployment rate | 0.053 | 1.070 | 0.288 | |||

| X5 mcee | Capital investment | 0.061 | 0.277 | 0.782 | |||

| X6 mcee | Current account balance | 0.195 | 1.126 | 0.264 | 0.258 | 2.396 | 0.019 * |

| X7 mcee | House price index | −0.164 | −2.617 | 0.011 * | −0.164 | −4.333 | <0.0001 ** |

| X8 mcee | Industry-value-to-GDP | 0.841 | 2.640 | 0.011 * | 0.429 | 2.206 | 0.030 * |

| X9 mcee | Budget-balance-to-GDP | 0.035 | 0.355 | 0.723 | 0.143 | 1.933 | 0.046 * |

| X10 mcee | Wages and salaries per employee | −0.001 | −0.135 | 0.892 | |||

| X2 | Consumer confidence index (CCI) | 0.025 | 0.690 | 0.492 | |||

| X4 | Cases of COVID-19 | −1.81 × 10−5 | −0.573 | 0.568 | |||

| X11 | Domestic credit to private sector-to-GDP | 0.138 | 3.793 | <0.0001 ** | 0.154 | 5.059 | <0.0001 * |

| X14 | Share price index | - | - | - | |||

| X18 | Exchange rate | −0.130 | −2.596 | 0.012 * | |||

| X22 | Investment freedom | −0.066 | −1.016 | 0.313 | |||

| R-squared | 0.542 | 0.158 | |||||

| F test | 0.000 | 0.000 | |||||

| Hausman test | 0.000 | 0.000 | |||||

| Model | Fixed effects | Fixed effects | |||||

| Observations | 86 | 106 | |||||

References

- Abusharbeh, Mohammed T. 2020. Determinants of Credit Risk in Palestine: Panel Data Estimation. International Journal of Finance and Economics 27: 3434–43. [Google Scholar] [CrossRef]

- Agic, Zorana, and Svetlana Dusanic Gacic. 2021. Specific Banking Determinants of Non-Performing Loans: The Case of Bosnia and Herzegovina. Economy and Market Communication Review 11: 546–59. [Google Scholar]

- Agnello, Luca, and Ricardo M. Sousa. 2014. The Determinants of the Volatility of Fiscal Policy Discretion. Fiscal Studies 35: 91–115. [Google Scholar] [CrossRef]

- Agnello, Luca, Davide Furceri, and Ricardo M. Sousa. 2011. Fiscal Policy Discretion, Private Spending, and Crisis Episodes. NIPE Working Papers. Available online: www.banque-france.fr (accessed on 1 April 2022).

- Anita, Saom Shawleen, Nishat Tasnova, and Nousheen Nawar. 2022. Are Non-Performing Loans Sensitive to Macroeconomic Determinants? An Empirical Evidence from Banking Sector of SAARC Countries. Future Business Journal 8: 1–16. [Google Scholar] [CrossRef]

- Aver, Boštjan. 2008. An Empirical Analysis of Credit Risk Factors of the Slovenian Banking System. Managing Global Transitions 6: 317–34. [Google Scholar]

- Bayar, Yilmaz. 2019. Macroeconomic, Institutional and Bank-Specific Determinants of Non-Performing Loans in Emerging Market Economies: A Dynamic Panel Regression Analysis. Journal of Central Banking Theory and Practice 8: 95–110. [Google Scholar] [CrossRef] [Green Version]

- Beck, Roland, Petr Jakubik, and Anamaria Piloiu. 2015. Key Determinants of Non-Performing Loans: New Evidence from a Global Sample. Open Economies Review 26: 525–50. [Google Scholar] [CrossRef]

- Berkmen, S. Pelin, Gaston Gelos, Robert Rennhack, and James P. Walsh. 2012. The Global Financial Crisis: Explaining Cross-Country Differences in the Output Impact. Journal of International Money and Finance 31: 42–59. [Google Scholar] [CrossRef]

- Blanco, Roberto, and Ricardo Gimeno. 2012. Determinants of Default Ratios in the Segment of Loans to Households in Spain. Banco de Espana Working Paper 1210: 40. [Google Scholar] [CrossRef] [Green Version]

- Bonfim, Diana. 2009. Credit Risk Drivers: Evaluating the Contribution of Firm Level Information and of Macroeconomic Dynamics. Journal of Banking and Finance 33: 281–99. [Google Scholar] [CrossRef] [Green Version]

- Boudriga, Abdelkader, Neila Boulia Taktak, and Sana Jellouli. 2010. Bank Specific, Business and Institutional Environment Determinants of Banks Nonperforming Loans: Evidence from MENA Countries. Journal of Chemical Information and Modeling 53: 1689–99. [Google Scholar]

- Boyd, John H., and Gianni De Nicoló. 2005. The Theory of Bank Risk Taking and Competition Revisited. Journal of Finance 60: 1329–43. [Google Scholar] [CrossRef]

- Buncic, Daniel, and Martin Melecky. 2013. Macroprudential Stress Testing of Credit Risk: A Practical Approach for Policy Makers. Journal of Financial Stability 9: 347–70. [Google Scholar] [CrossRef] [Green Version]

- Carvalho, Paulo V., José D. Curto, and Rodrigo Primor. 2020. Macroeconomic Determinants of Credit Risk: Evidence from the Eurozone. International Journal of Finance and Economics 27: 2054–72. [Google Scholar] [CrossRef]

- Castro, Vítor. 2013. Macroeconomic Determinants of the Credit Risk in the Banking System: The Case of the GIPSI. Economic Modelling 31: 672–83. [Google Scholar] [CrossRef] [Green Version]

- De Bock, Reinout, and Alexander Demyanets. 2012. Bank Asset Quality in Emerging Markets: Determinants and Spillovers. IMF Working Papers 12: 27. [Google Scholar] [CrossRef]

- Dimitrios, Anastasiou, Louri Helen, and Tsionas Mike. 2016. Determinants of Non-Performing Loans: Evidence from Euro-Area Countries. Finance Research Letters 18: 116–19. [Google Scholar] [CrossRef]

- Doshi, Hitesh, Kris Jacobs, and Virgilio Zurita. 2017. Economic and Financial Determinants of Credit Risk Premiums in the Sovereign CDS Market. Review of Asset Pricing Studies 7: 43–80. [Google Scholar] [CrossRef] [Green Version]

- Duffie, Darrell, Leandro Saita, and Ke Wang. 2007. Multi-Period Corporate Default Prediction with Stochastic Covariates. Journal of Financial Economics 83: 635–65. [Google Scholar] [CrossRef] [Green Version]

- Džidić, Ante, Igor Živko, and Anela Čolak. 2022. Macroeconomic Factors of Non-Performing Loans: The Case of Bosnia and Herzegovina. Ekonomska Misao i Praksa 31: 421–38. [Google Scholar] [CrossRef]

- Espinoza, Raphael, and Ananthakrishnan Prasad. 2010. Nonperforming Loans in the GCC Banking System and Their Macroeconomic Effects. IMF Working Papers 10: 25. [Google Scholar] [CrossRef]

- European Parliament. 2013. Directive 2013/36/EU of the European Parliament and of the Council of 26 June 2013 on Access to the Activity of Credit Institutions and the Prudential Supervision of Credit Institutions and Investment Firms, Amending Directive 2002/87/EC and Repealing Dir. Official Journal of the European Union 176: 338–436. Available online: http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2013:176:0338:0436:En:PDF (accessed on 19 May 2022).

- Feldkircher, Martin. 2014. The Determinants of Vulnerability to the Global Financial Crisis 2008 to 2009: Credit Growth and Other Sources of Risk. Journal of International Money and Finance 43: 19–49. [Google Scholar] [CrossRef] [Green Version]

- Figlewski, Stephen, Halina Frydman, and Weijian Liang. 2012. Modeling the Effect of Macroeconomic Factors on Corporate Default and Credit Rating Transitions. International Review of Economics and Finance 21: 87–105. [Google Scholar] [CrossRef]

- Foglia, Antonella. 2009. Stress Testing Credit Risk: A Survey of Authorities’ Approaches. The International Journal of Central Banking 5: 9–45. [Google Scholar] [CrossRef] [Green Version]

- Foglia, Matteo. 2022. Non-Performing Loans and Macroeconomics Factors: The Italian Case. Risks 10: 21. [Google Scholar] [CrossRef]

- Gashi, Adelina, Saranda Tafa, and Roberta Bajrami. 2022. The Impact of Macroeconomic Factors on Non-Performing Loans in the Western Balkans. Emerging Science Journal 6: 1032–45. [Google Scholar] [CrossRef]

- Ghosh, Amit. 2015. Banking-Industry Specific and Regional Economic Determinants of Non-Performing Loans: Evidence from US States. Journal of Financial Stability 20: 93–104. [Google Scholar] [CrossRef]

- Gila-Gourgoura, Esida, and Eftychia Nikolaidou. 2018. Credit Risk Determinants in the Vulnerable Economies of Europe: Evidence From the Italian Banking System. Paper presented at 10th Economics & Finance Conference, Rome, Italy, September 10–13; pp. 119–37. [Google Scholar] [CrossRef]

- González, Francisco. 2005. Bank Regulation and Risk-Taking Incentives: An International Comparison of Bank Risk. Journal of Banking and Finance 29: 1153–84. [Google Scholar] [CrossRef]

- Haniifah, Nanteza. 2015. Economic Determinants of Non-Performing Loans (NPLs) in Ugandan Commercial Banks. Taylor’s Business Review 5: 137–53. Available online: http://university2.taylors.edu.my/tbr/uploaded/2015_vol5_issue2_p3.pdf (accessed on 29 June 2022).

- Haq, Mamiza, and Richard Heaney. 2012. Factors Determining European Bank Risk. Journal of International Financial Markets, Institutions and Money 22: 696–718. [Google Scholar] [CrossRef]

- Jiménez, Gabriel, and Jesús Saurina. 2004. Collateral, Type of Lender and Relationship Banking as Determinants of Credit Risk. Journal of Banking and Finance 28: 2191–212. [Google Scholar] [CrossRef] [Green Version]

- Johnson, Andrew M., Michael D. Boehlje, and Michael A. Gunderson. 2017. Agricultural Credit Risk and the Macroeconomy: Determinants of Farm Credit Mid-America PD Migrations. Agricultural Finance Review 77: 164–80. [Google Scholar] [CrossRef]

- Kaminskyi, Andrii, and Maryna Nehrey. 2021. Information Technology Model for Customer Relationship Management of Nonbank Lenders: Coupling Profitability and Risk. Paper presented at 2021 11th International Conference on Advanced Computer Information Technologies, Deggendorf, Germany, September 15–17; pp. 234–37. [Google Scholar] [CrossRef]

- Kanapickienė, Rasa, Greta Keliuotytė-Staniulėnienė, Deimantė Teresienė, Renatas Špicas, and Airidas Neifaltas. 2022. Macroeconomic Determinants of Credit Risk: Evidence on the Impact on Consumer Credit in Central and Eastern European Countries. Sustainability 14: 13219. [Google Scholar] [CrossRef]

- Karoglou, Michail, Konstantinos Mouratidis, and Sofoklis Vogiazas. 2018. Estimating the Impact of Credit Risk Determinants in Two Southeast European Countries: A Non-Linear Structural VAR Approach. Review of Economic Analysis 10: 55–74. [Google Scholar] [CrossRef]

- Kjosevski, Jordan, and Mihail Petkovski. 2017. Non-Performing Loans in Baltic States: Determinants and Macroeconomic Effects. Baltic Journal of Economics 17: 25–44. [Google Scholar] [CrossRef] [Green Version]

- Kjosevski, Jordan, Mihail Petkovski, and Elena Naumovska. 2019. Bank-Specific and Macroeconomic Determinants of Non-Performing Loans in the Republic of Macedonia: Comparative Analysis of Enterprise and Household NPLs. Economic Research-Ekonomska Istrazivanja 32: 1185–203. [Google Scholar] [CrossRef] [Green Version]

- Koju, Laxmi, Ram Koju, and Shouyang Wang. 2020. Macroeconomic Determinants of Credit Risks: Evidence from High-Income Countries. European Journal of Management and Business Economics 29: 41–53. [Google Scholar] [CrossRef] [Green Version]

- Lehmann, Hansjörg, and Michael Manz. 2006. The Exposure of Swiss Banks to Macroeconomic Shocks—An Empirical Investigation. Swiss National Bank Working Paper 4: 28. [Google Scholar]

- Liao, Szu-Lang, and Jui-Jane Chang. 2005. Economic Determinants of Default Risks and Their Impacts on Credit Derivative Pricing. Journal of Futures Markets 30: 67–68. [Google Scholar] [CrossRef]

- Louzis, Dimitrios P., Angelos T. Vouldis, and Vasilios L. Metaxas. 2012. Macroeconomic and Bank-Specific Determinants of Non-Performing Loans in Greece: A Comparative Study of Mortgage, Business and Consumer Loan Portfolios. Journal of Banking and Finance 36: 1012–27. [Google Scholar] [CrossRef]

- Love, Inessa, and Rima Turk Ariss. 2014. Macro-Financial Linkages in Egypt: A Panel Analysis of Economic Shocks and Loan Portfolio Quality. Journal of International Financial Markets, Institutions and Money 28: 158–81. [Google Scholar] [CrossRef] [Green Version]

- Maltritz, Dominik, and Alexander Molchanov. 2014. Country Credit Risk Determinants with Model Uncertainty. International Review of Economics and Finance 29: 224–34. [Google Scholar] [CrossRef]

- Melecky, Ales, and Monika Sulganova. 2013. The Influence of the Monetary Policy Rate on the Non-Performing Loans and Their Determinants. Paper presented at 11th International Conference: Economic Policy in the European Union Member Countries, Selected Papers, Velke Karlovice, Czech Republic, September 18–20; pp. 217–26. [Google Scholar]

- Melecky, Ales, and Monika Sulganova. 2015. The Quantitative Survey on Macroeconomic Determinants of Aggregate Credit Risk. Paper presented at 2nd International Conference on Education and Social Sciences (INTCESS’15) (Proceedings Paper), Istanbul, Turkey, February 2–4; p. 64453. [Google Scholar]

- Messai, Ahlem Selma, and Fathi Jouini. 2013. Micro and Macro Determinants of Refugee Economic Status. International Journal of Economics and Financial Issues 3: 852–60. [Google Scholar] [CrossRef]

- Messai, Ahlem Selma, and Mohamed Imen Gallali. 2019. Macroeconomic Determinants of Credit Risk: A P-VAR Approach Evidence from Europe. International Journal of Monetary Economics and Finance 12: 15–24. [Google Scholar] [CrossRef]

- Mileris, Ričardas. 2013. Macroeconomic Determinants of Loan Portfolio Credit Risk in Banks. Engineering Economics 23: 496–504. [Google Scholar] [CrossRef] [Green Version]

- Mpofu, Trust R., and Eftychia Nikolaidou. 2018. Determinants of Credit Risk in the Banking System in Sub-Saharan Africa. Review of Development Finance 8: 141–53. [Google Scholar] [CrossRef]

- Naceur, Sami Ben, and Mohammed Omran. 2011. The Effects of Bank Regulations, Competition, and Financial Reforms on Banks’ Performance. Emerging Markets Review 12: 1–20. [Google Scholar] [CrossRef]

- Naili, Maryem, and Younes Lahrichi. 2022a. The Determinants of Banks’ Credit Risk: Review of the Literature and Future Research Agenda. International Journal of Finance and Economics 27: 334–60. [Google Scholar] [CrossRef]

- Naili, Maryem, and Younès Lahrichi. 2022b. Banks’ Credit Risk, Systematic Determinants and Specific Factors: Recent Evidence from Emerging Markets. Heliyon 8: e08960. [Google Scholar] [CrossRef]

- Nikolaidou, Eftychia, and Sofoklis Vogiazas. 2017. Credit Risk Determinants in Sub-Saharan Banking Systems: Evidence from Five Countries and Lessons Learnt from Central East and South East European Countries. Review of Development Finance 7: 52–63. [Google Scholar] [CrossRef]

- Nkusu, Mwanza. 2011. Nonperforming Loans and Macrofinancial Vulnerabilities in Advanced Economies. IMF Working Papers 11: 28. [Google Scholar] [CrossRef] [Green Version]

- Pluskota, Anna. 2021. Macroeconomic Determinants Affecting Credit Risk in Central and Eastern Europe. Folia Oeconomica Stetinensia 21: 92–104. [Google Scholar] [CrossRef]

- Podpiera, Jiří, and Laurent Weill. 2008. Bad Luck or Bad Management? Emerging Banking Market Experience. Journal of Financial Stability 4: 135–48. [Google Scholar] [CrossRef] [Green Version]

- Priyadi, Unggul, Kurnia Dwi Sari Utami, Rifqi Muhammad, and Peni Nugraheni. 2021. Determinants of Credit Risk of Indonesian Sharīʿah Rural Banks. ISRA International Journal of Islamic Finance 13: 284–301. [Google Scholar] [CrossRef]

- Quagliariello, Mario. 2007. Banks’ Riskiness over the Business Cycle: A Panel Analysis on Italian Intermediaries. Applied Financial Economics 17: 119–38. [Google Scholar] [CrossRef]

- Radivojević, Nikola, Drago Cvijanović, Dejan Sekulic, Dejana Pavlovic, Srdjan Jovic, and Goran Maksimović. 2019. Econometric Model of Non-Performing Loans Determinants. Physica A: Statistical Mechanics and Its Applications 520: 481–88. [Google Scholar] [CrossRef]

- Rashid, Abdul, and Maurizio Intartaglia. 2017. Financial Development—Does It Lessen Poverty? Journal of Economic Studies 44: 69–86. [Google Scholar] [CrossRef]

- Rossi, Stefania P. S., Markus S. Schwaiger, and Gerhard Winkler. 2009. How Loan Portfolio Diversification Affects Risk, Efficiency and Capitalization: A Managerial Behavior Model for Austrian Banks. Journal of Banking and Finance 33: 2218–26. [Google Scholar] [CrossRef]

- Salas, Vicente, and Jesús Saurina. 2002. Credit Risk in Two Institutional Regimes: Spanish Commercial and Savings Banks. Journal of Financial Services Research 22: 203–24. [Google Scholar] [CrossRef]

- Sommar, Pe Asberg, and Hovick Shahnazarian. 2009. Interdependencies between Expected Default Frequency and the Macro Economy. International Journal of Central Banking 5: 84–110. Available online: http://www.ijcb.org/journal/ijcb09q3a3.pdf (accessed on 12 April 2022).

- Stolbov, Mikhail. 2017. Determinants of Sovereign Credit Risk: The Case of Russia. Post-Communist Economies 29: 51–70. [Google Scholar] [CrossRef]

- Sulganova, Monika. 2016. The Lag Length Structure of Banking Determinants of Non-Performing Loans in the Czech Republic. In Proceedings of the 15th International Conference on Finance and Banking. Prague: School of Business Administration Silesian University in Opava, pp. 400–10. [Google Scholar]

- Tatarici, Luminita Roxana, Matei Nicolae Kubinschi, and Dinu Barnea. 2020. Determinants of Non-Performing Loans for the EEC Region. A Financial Stability Perspective. Management & Marketing-Challenges for the Knowledge Society 15: 621–42. [Google Scholar] [CrossRef]

- Umar, Muhammad, and Gang Sun. 2018. Determinants of Non-Performing Loans in Chinese Banks. Journal of Asia Business Studies 12: 273–89. [Google Scholar] [CrossRef]

- Washington, Gitonga Kariuki. 2014. Effects of Macroeconomic Variables on Credit Risk in the Kenyan Banking System. International Journal of Business and Commerce 3: 26. [Google Scholar]

- Wong, Jim, Tak Chuen Wong, and Phyllis Leung. 2010. Predicting Banking Distress in the EMEAP Economies. Journal of Financial Stability 6: 169–79. [Google Scholar] [CrossRef]

- Yüksel, Serhat, Shahriyar Mukhtarov, Elvin Mammadov, and Mustafa Özsarı. 2018. Determinants of Profitability in the Banking Sector: An Analysis of Post-Soviet Countries. Economies 6: 41. [Google Scholar] [CrossRef] [Green Version]

- Yurdakul, Funda. 2014. Macroeconomic Modelling of Credit Risk for Banks. Procedia—Social and Behavioral Sciences 109: 784–93. [Google Scholar] [CrossRef] [Green Version]

- Zhang, Dayong, Jing Cai, David G. Dickinson, and Ali M. Kutan. 2016. Non-Performing Loans, Moral Hazard and Regulation of the Chinese Commercial Banking System. Journal of Banking and Finance 63: 48–60. [Google Scholar] [CrossRef]

- Zheng, Changjun, Probir Kumar Bhowmik, and Niluthpaul Sarker. 2020. Industry-Specific and Macroeconomic Determinants of Non-Performing Loans: A Comparative Analysis of ARDL and VECM. Sustainability 12: 325. [Google Scholar] [CrossRef] [Green Version]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kanapickienė, R.; Keliuotytė-Staniulėnienė, G.; Vasiliauskaitė, D.; Špicas, R.; Neifaltas, A.; Valukonis, M. Macroeconomic Factors of Consumer Loan Credit Risk in Central and Eastern European Countries. Economies 2023, 11, 102. https://doi.org/10.3390/economies11040102

Kanapickienė R, Keliuotytė-Staniulėnienė G, Vasiliauskaitė D, Špicas R, Neifaltas A, Valukonis M. Macroeconomic Factors of Consumer Loan Credit Risk in Central and Eastern European Countries. Economies. 2023; 11(4):102. https://doi.org/10.3390/economies11040102

Chicago/Turabian StyleKanapickienė, Rasa, Greta Keliuotytė-Staniulėnienė, Deimantė Vasiliauskaitė, Renatas Špicas, Airidas Neifaltas, and Mantas Valukonis. 2023. "Macroeconomic Factors of Consumer Loan Credit Risk in Central and Eastern European Countries" Economies 11, no. 4: 102. https://doi.org/10.3390/economies11040102