Testing the Validity of the Quantity Theory of Money on Sectoral Data: Non-Linear Evidence from South Africa

Abstract

:1. Introduction

2. Literature Review

- = Money supply;

- = Velocity (number of transactions that take place with a given amounts of money);

- = Average price level (inflation);

- = The quantity of goods and services sold.

3. Data and Methodology

3.1. Data Description

3.2. Theoretical Model

3.3. Empirical Model and Estimation Techniques

3.4. The Fishers’ Equation Specified in the NARDL Framework

3.5. Pre-Estimation Techniques

4. Results and Discussion

4.1. Unit Root Test

4.2. Non-Linear Cointegration Bound Test

4.3. Non-Linear ARDL Short-Term Results

4.4. Long-Term Relations Results

4.5. Granger Causality Results

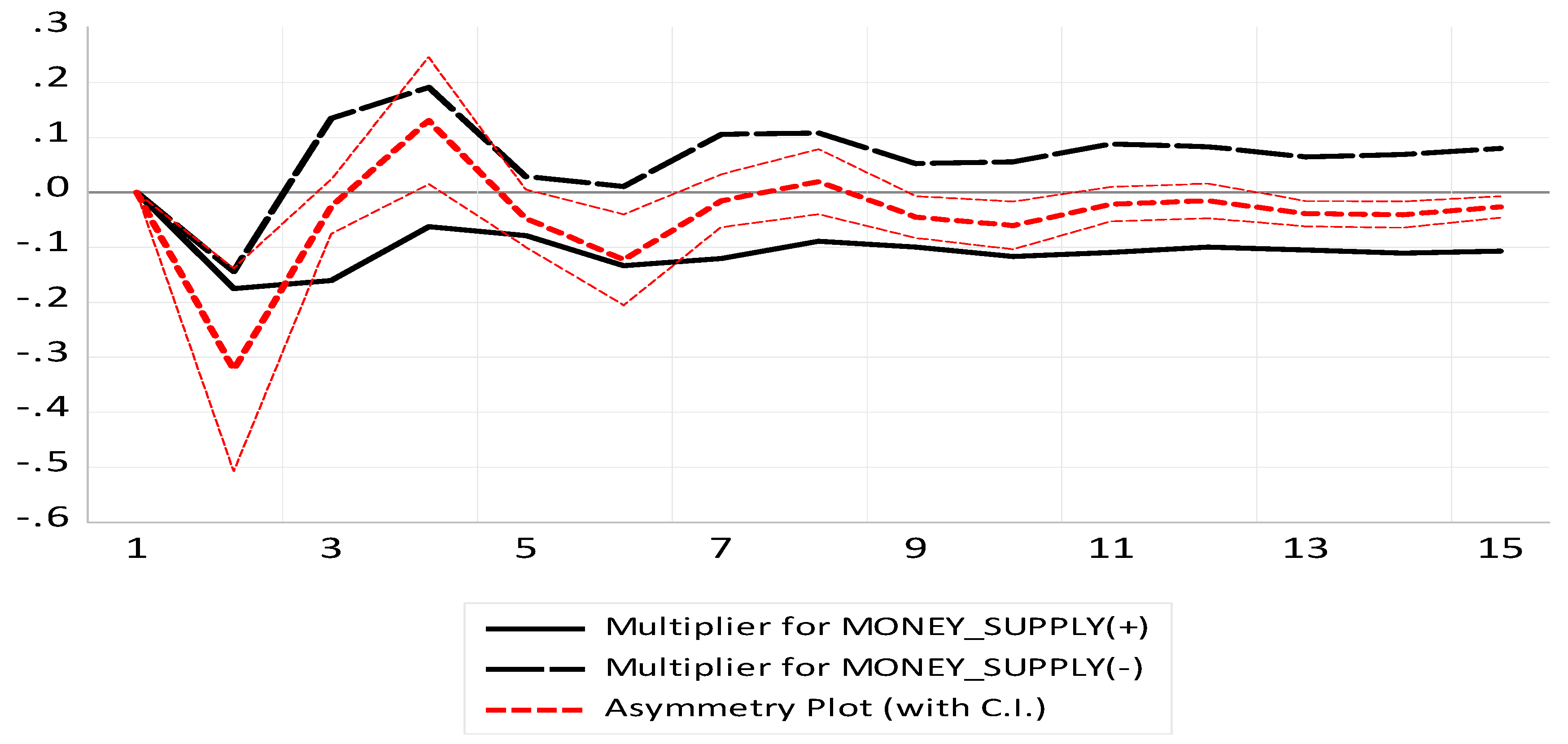

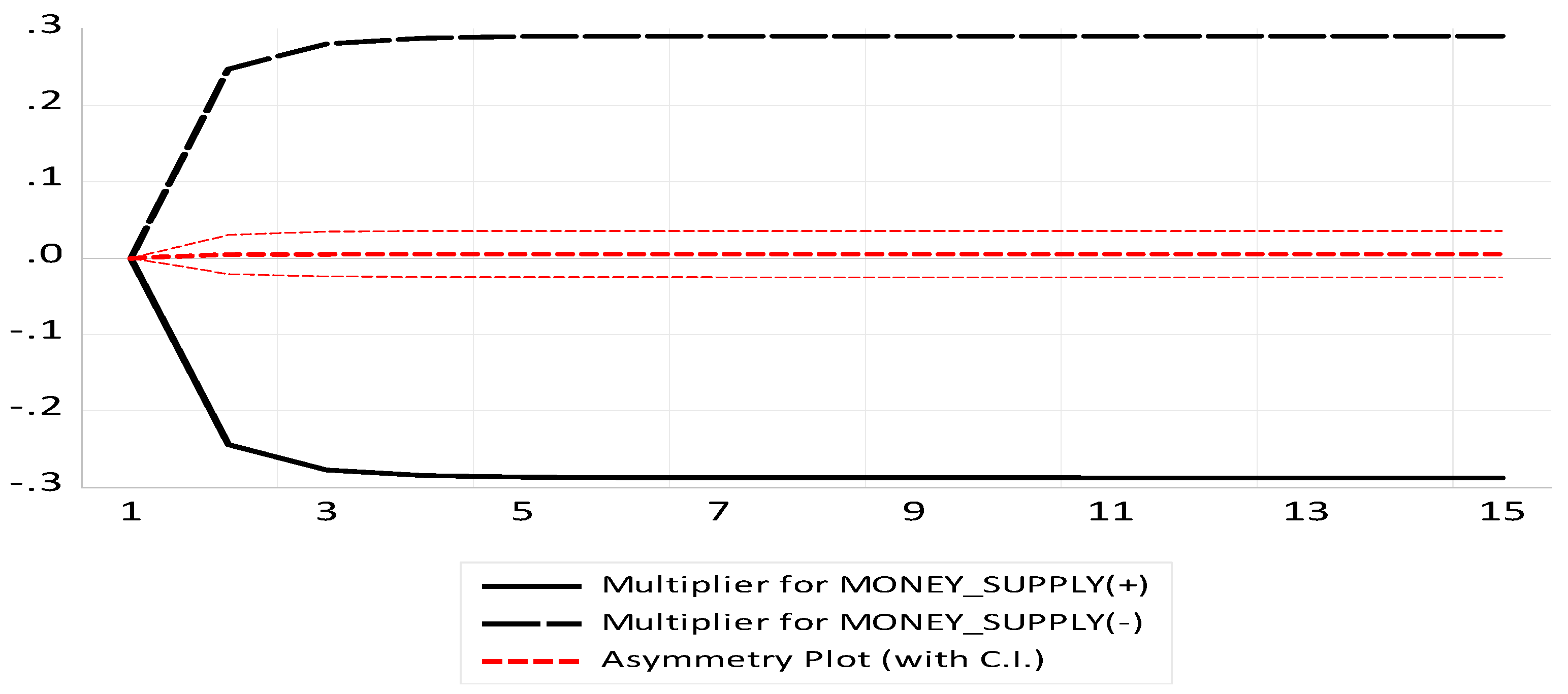

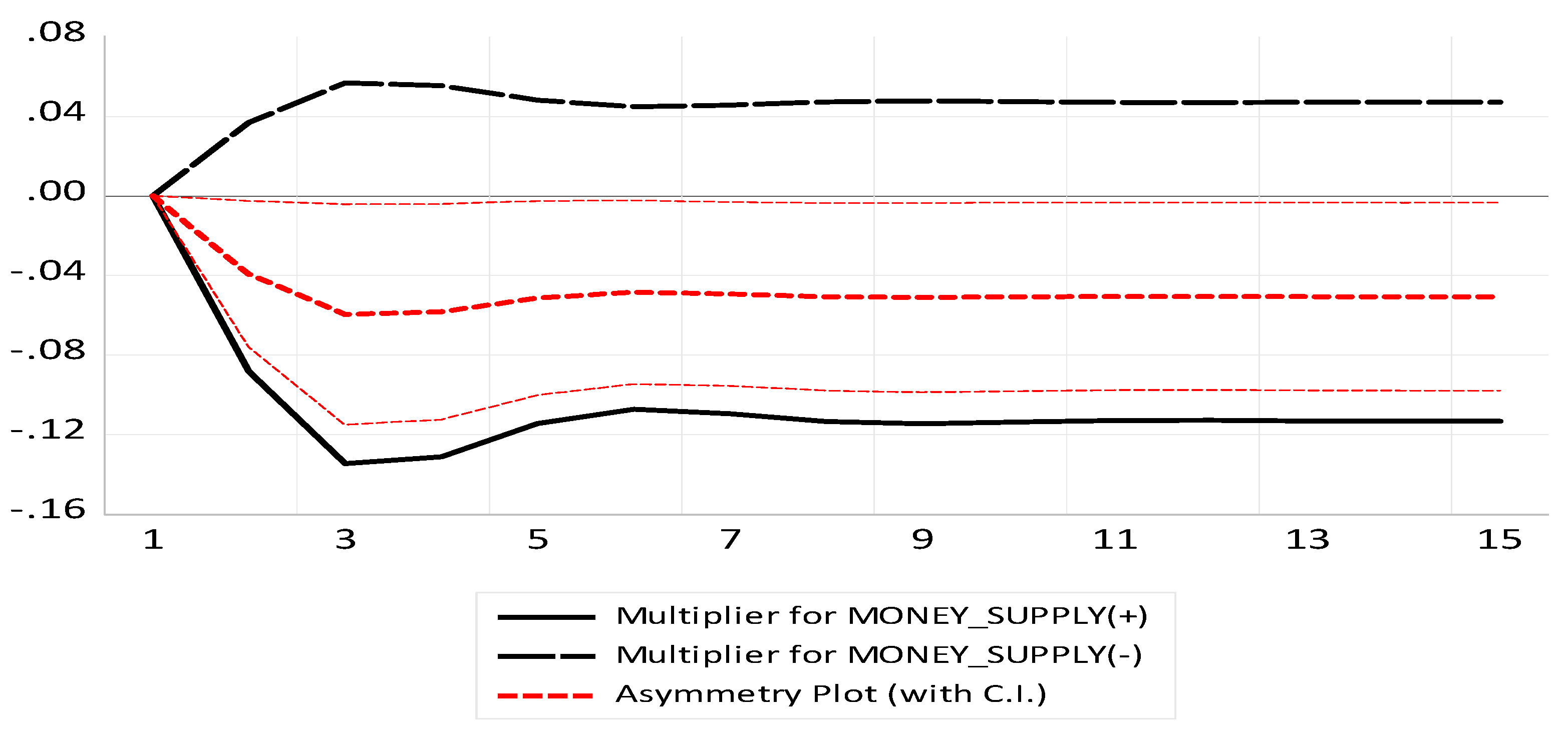

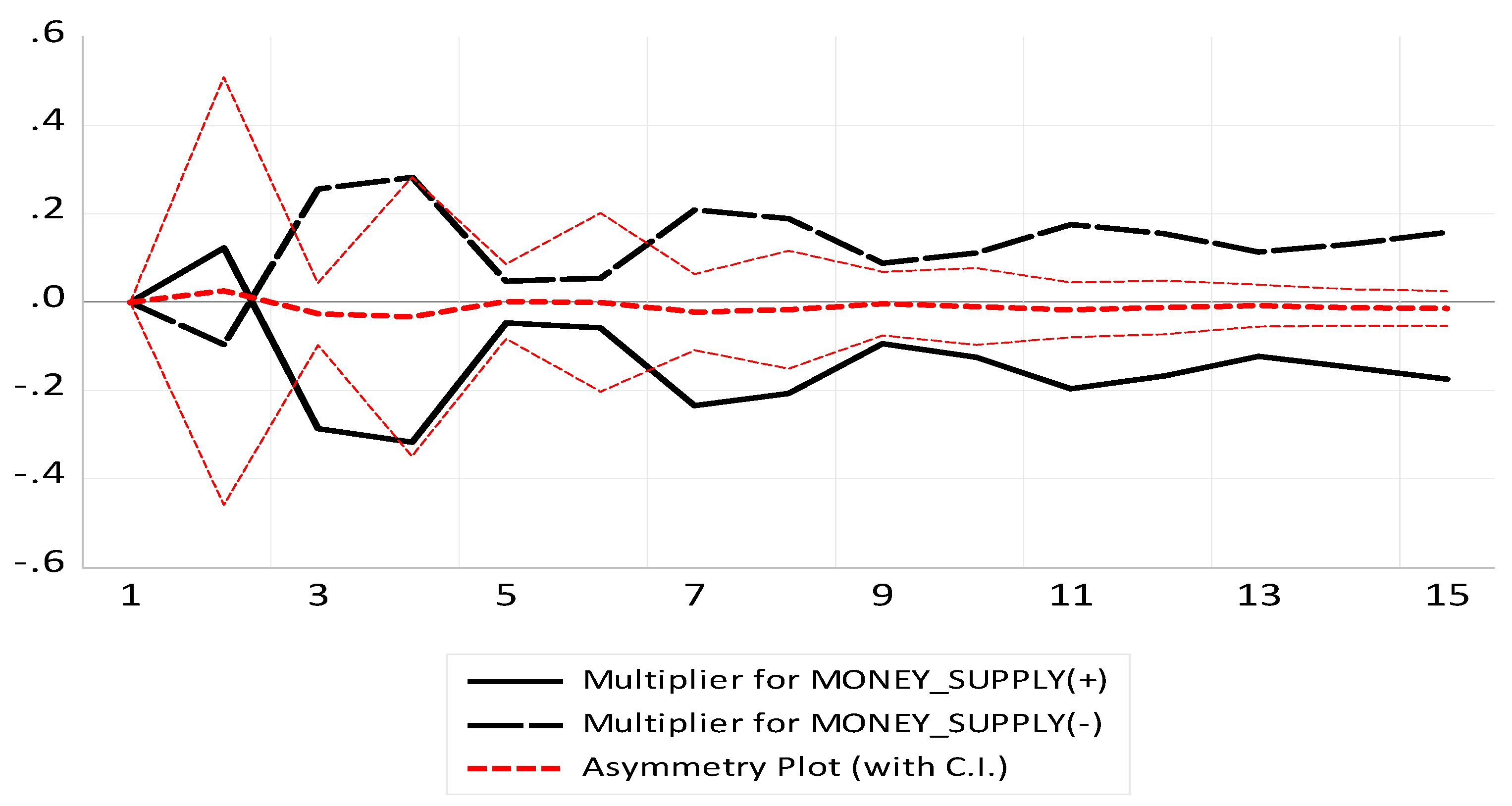

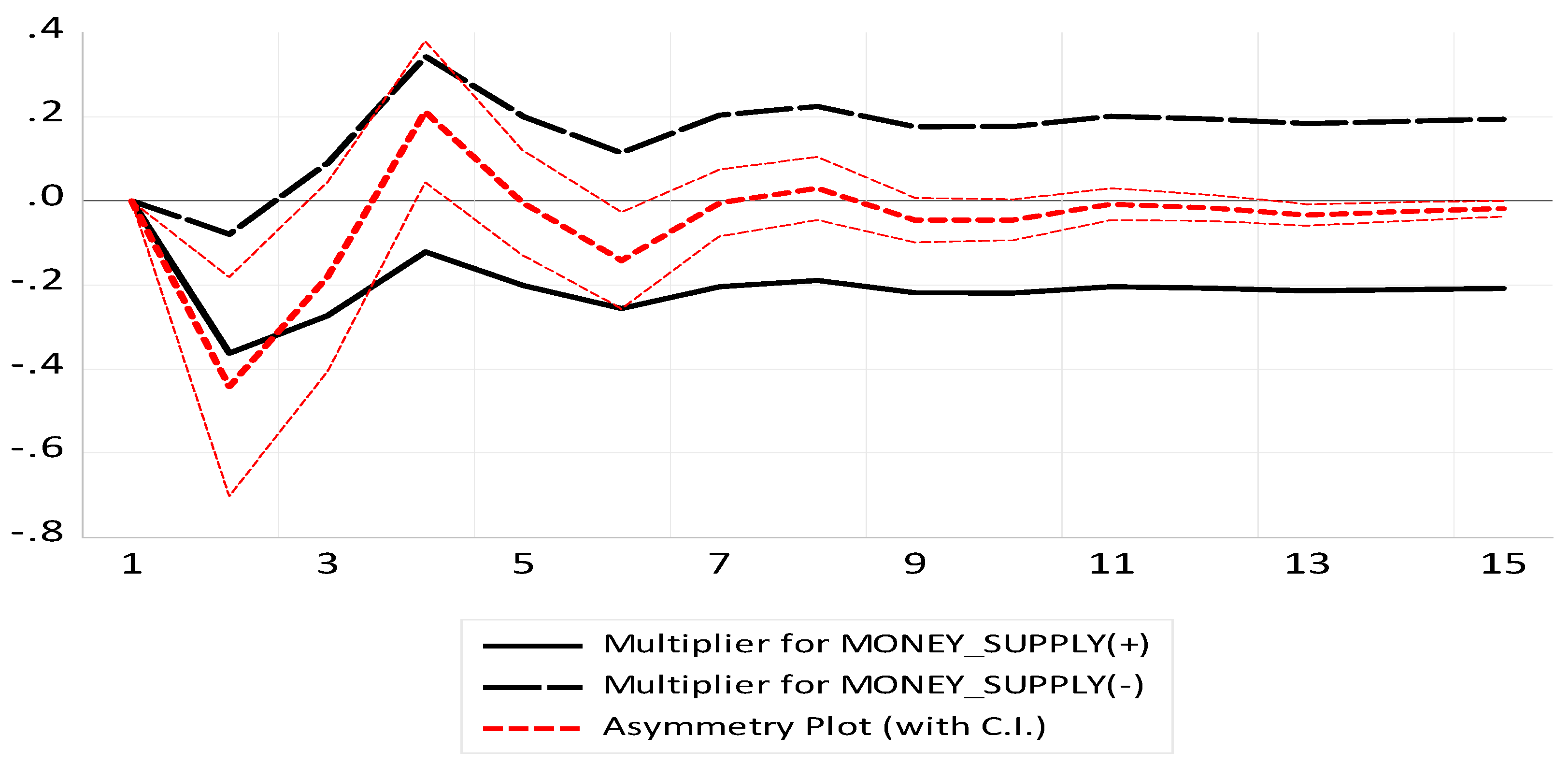

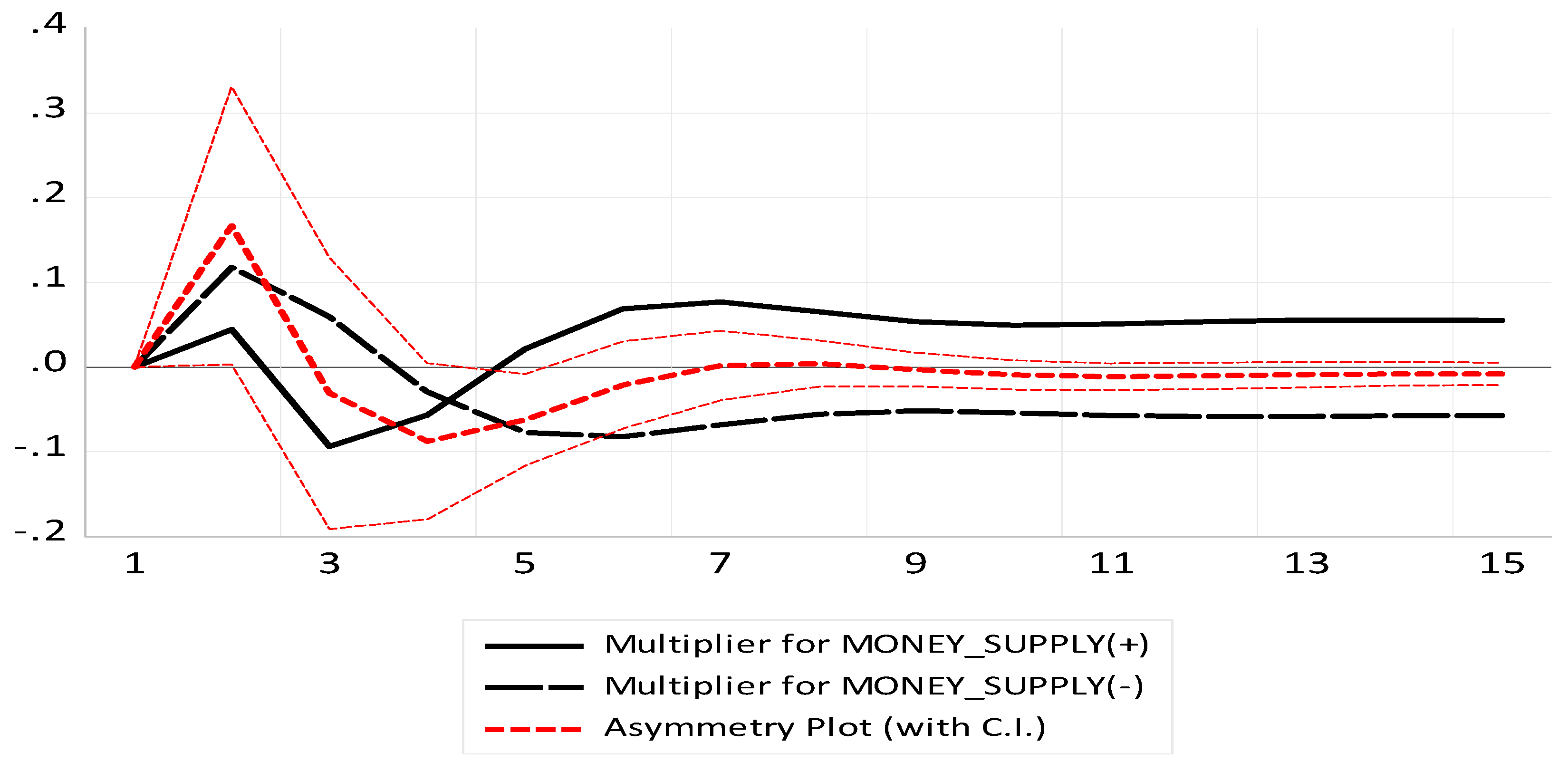

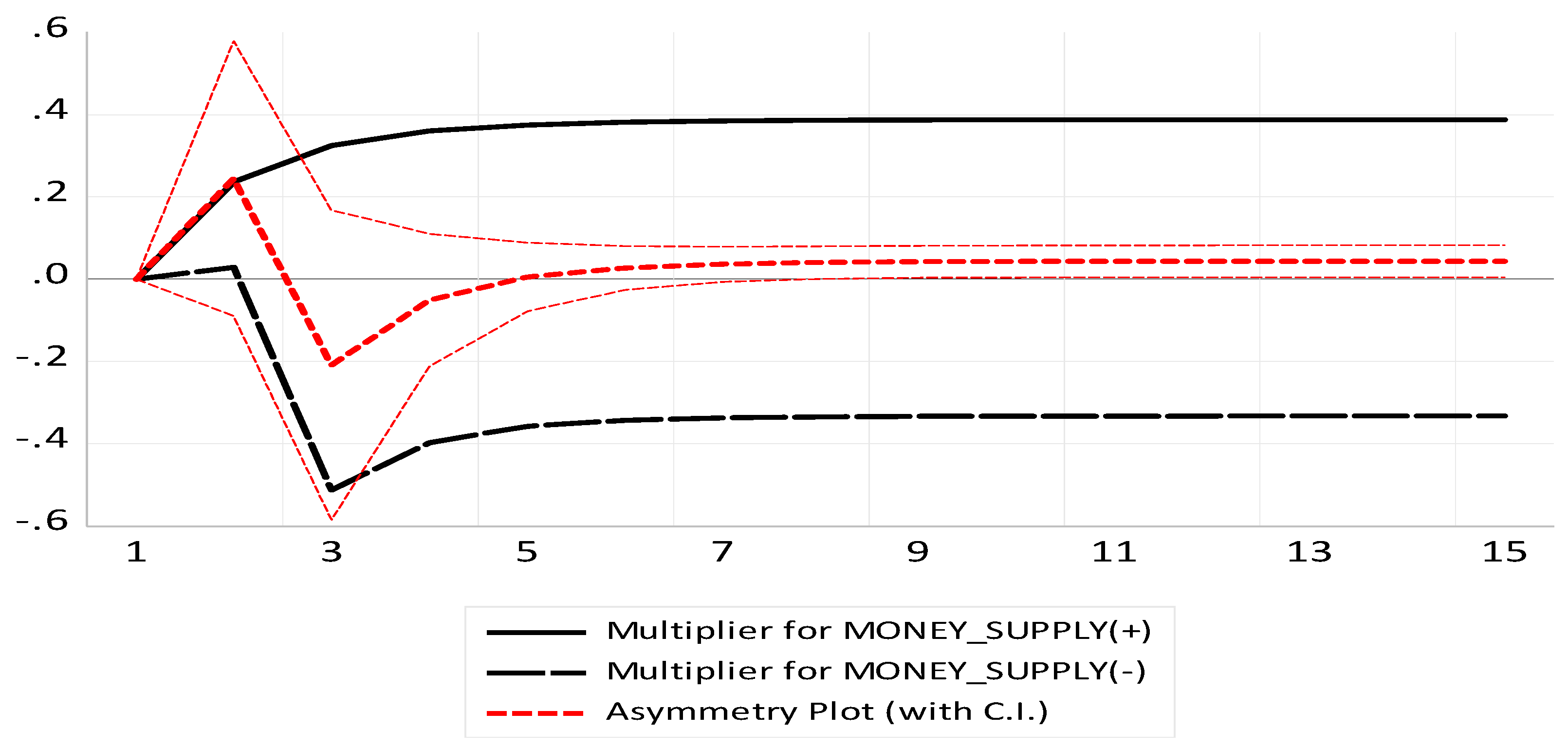

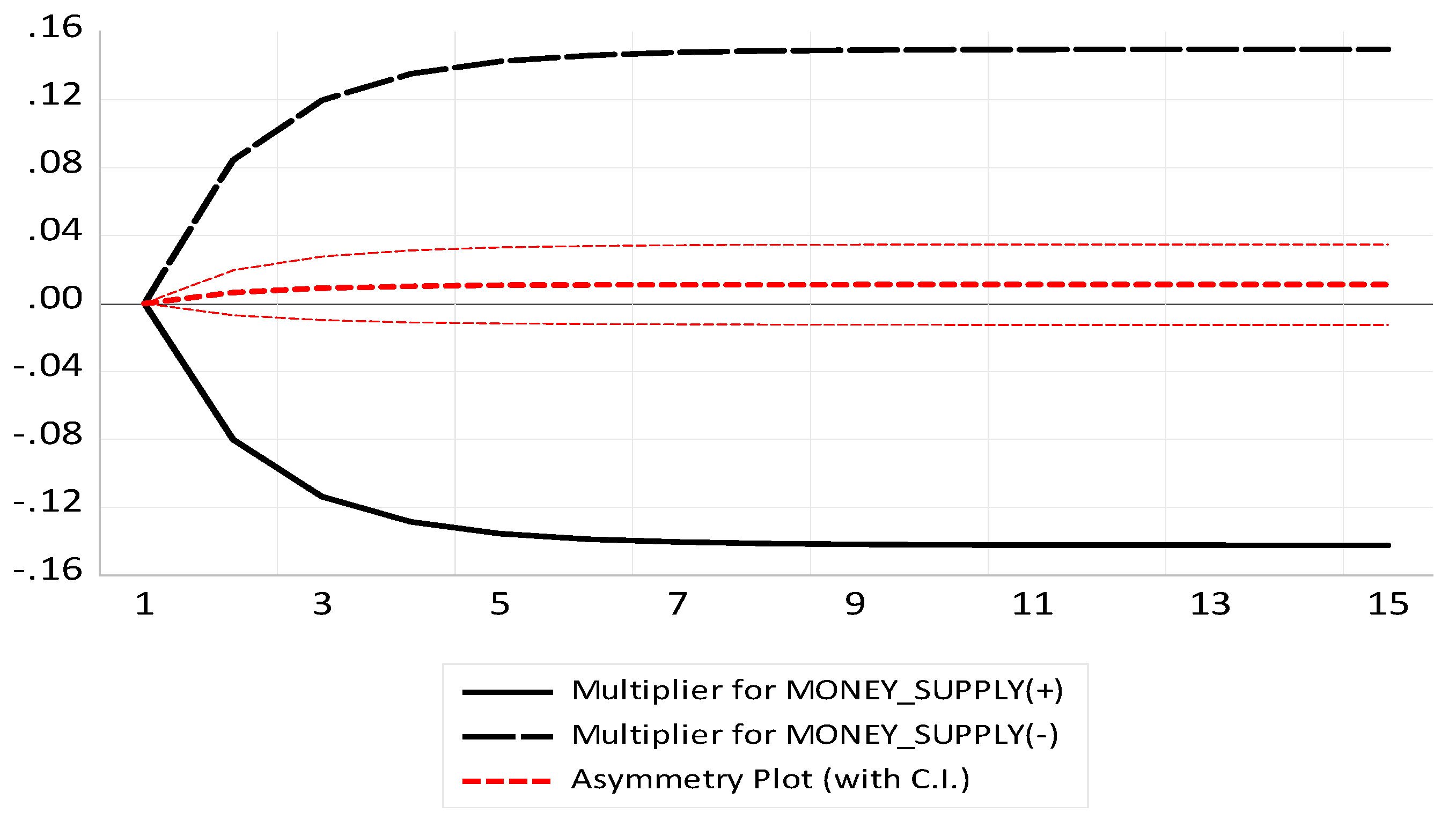

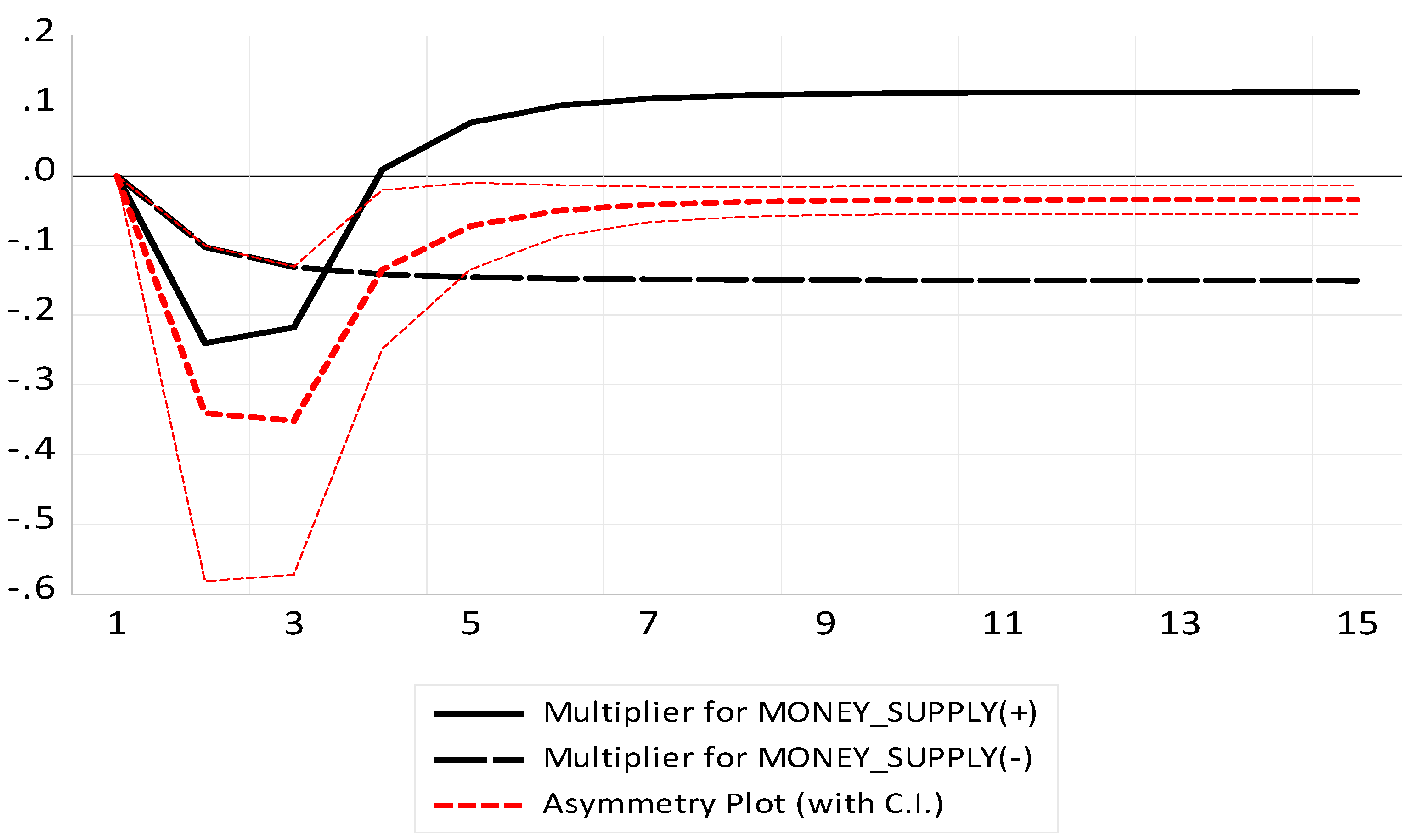

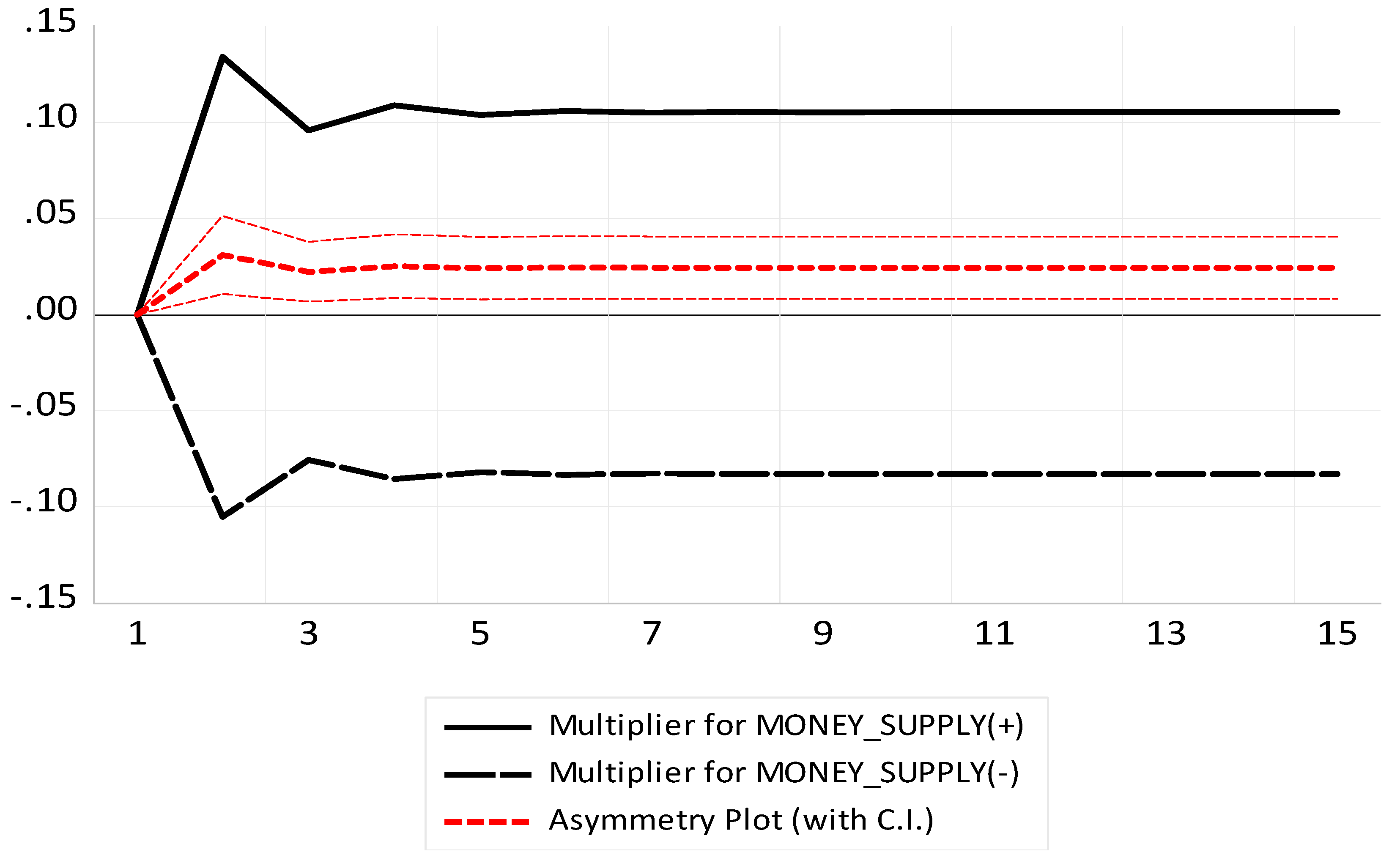

4.6. Dynamic Multiplier Graphs

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

Appendix A. CUSUM Test Graphs for Each Model

- 1.

- Clothing and footwear sector

- 2.

- Communication sector

- 3.

- Education sector

- 4.

- Food and non-alcoholic beverages sector

- 5.

- Health sector

- 6.

- Households’ contents and equipment sector

- 7.

- Housing and utilities sector

- 8.

- Recreation and culture sector

- 9.

- Restaurants and Hotels

- 10.

- Transport sector

Appendix B. Summary of Diagnostic Tests

| Tests | Results |

| Alcoholic beverages and tobacco sector | |

| Heteroskedasticity Test: Breusch–Pagan–Godfrey | Prob. 0.0515 > 0.05 |

| Serial Correlation LM Test: Breusch–Godfrey | Prob. 0.5973 > 0.05 |

| Normality test: Jarque–Bera | Prob. 0.5538 > 0.05 |

| Model specification: Ramsey RESET Test | Prob. 0.1696 > 0.05 |

| Stability: CUSUM test | Significant at 5% |

| Clothing and footwear sector | |

| Heteroskedasticity Test: Breusch–Pagan–Godfrey | Prob. 0.6138 > 0.05 |

| Serial Correlation LM Test: Breusch–Godfrey | Prob. 0.8313 > 0.05 |

| Normality test: Jarque–Bera | Prob. 0.4287 > 0.05 |

| Model specification: Ramsey RESET Test | Prob. 0.1299 > 0.05 |

| Stability: CUSUM test | Significant at 5%, but not for CUCUM SQ |

| Communication sector | |

| Heteroskedasticity Test: Breusch–Pagan–Godfrey | Prob. 0.7166 > 0.05 |

| Serial Correlation LM Test: Breusch–Godfrey | Prob. 0.3826 > 0.05 |

| Normality test: Jarque–Bera | Prob. 0.6249 > 0.05 |

| Model specification: Ramsey RESET Test | Prob. 0.2436 > 0.05 |

| Stability: CUSUM test | Significant at 5% |

| Education sector | |

| Heteroskedasticity Test: Breusch–Pagan–Godfrey | Prob. 0.3268 > 0.05 |

| Serial Correlation LM Test: Breusch–Godfrey | Prob. 0.1302 > 0.05 |

| Normality test: Jarque–Bera | Prob. 0.5666 > 0.05 |

| Model specification: Ramsey RESET Test | Prob. 0.6320 > 0.05 |

| Stability: CUSUM test | Significant at 5% |

| Health sector | |

| Heteroskedasticity Test: Breusch–Pagan–Godfrey | Prob. 0.2266 > 0.05 |

| Serial Correlation LM Test: Breusch–Godfrey | Prob. 0.1258 > 0.05 |

| Normality test: Jarque–Bera | Prob. 0.1301 > 0.05 |

| Model specification: Ramsey RESET Test | Prob. 0.1688 > 0.05 |

| Stability: CUSUM test | Significant at 5% |

| Households’ contents and equipment sector | |

| Heteroskedasticity Test: Breusch–Pagan–Godfrey | Prob. 0.0853 > 0.05 |

| Serial Correlation LM Test: Breusch–Godfrey | Prob. 0.0946 > 0.05 |

| Normality test: Jarque–Bera | Prob. 0.0966 > 0.05 |

| Model specification: Ramsey RESET Test | Prob. 0.4399 > 0.05 |

| Stability: CUSUM test | Significant at 5%, but not for CUCUM SQ |

| Housing and utilities sector | |

| Heteroskedasticity Test: Breusch–Pagan–Godfrey | Prob. 0.1451 > 0.05 |

| Serial Correlation LM Test: Breusch–Godfrey | Prob. 0.2266 > 0.05 |

| Normality test: Jarque–Bera | Prob. 0.1491 > 0.05 |

| Model specification: Ramsey RESET Test | Prob. 0.1496 > 0.05 |

| Stability: CUSUM test | Significant at 5% |

| Recreation and culture sector | |

| Heteroskedasticity Test: Breusch–Pagan–Godfrey | Prob. 0.4303 > 0.05 |

| Serial Correlation LM Test: Breusch–Godfrey | Prob. 0.3315 > 0.05 |

| Normality test: Jarque–Bera | Prob. 0.1473 > 0.05 |

| Model specification: Ramsey RESET Test | Prob. 0.1637 > 0.05 |

| Stability: CUSUM test | Significant at 5% |

| Restaurants and hotels sector | |

| Heteroskedasticity Test: Breusch–Pagan–Godfrey | Prob. 0.2758 > 0.05 |

| Serial Correlation LM Test: Breusch–Godfrey | Prob. 0.6136 > 0.05 |

| Normality test: Jarque–Bera | Prob. 0.2893 > 0.05 |

| Model specification: Ramsey RESET Test | Prob. 0.5468 > 0.05 |

| Stability: CUSUM test | Significant at 5%, but not for CUCUM SQ |

| Transport sector | |

| Heteroskedasticity Test: Breusch–Pagan–Godfrey | Prob. 0.0946 > 0.05 |

| Serial Correlation LM Test: Breusch–Godfrey | Prob. 0.7490 > 0.05 |

| Normality test: Jarque–Bera | Prob. 0.9291 > 0.05 |

| Model specification: Ramsey RESET Test | Prob. 0.8915 > 0.05 |

| Stability: CUSUM test | Significant at 5% |

| Source: compiled by the authors from the estimation results. | |

References

- Abate, Tadesse Wudu. 2020. Macro-economic Determinants of Recent Inflation in Ethiopia. Journal of World Economic Research 9: 136–42. [Google Scholar] [CrossRef]

- Abdelsalam, Mamdouh Abdelmoula M. 2018. Asymmetric Effect of Monetary Policy in Emerging Countries: The Case of Egypt. Applied Economics and Finance 5: 1–11. [Google Scholar] [CrossRef] [Green Version]

- Adusei, Micheael. 2013. Is Inflation in South Africa a Structural or Monetary Phenomenon? British Journal of Economics, Management and Trade 3: 60–72. [Google Scholar] [CrossRef]

- Agenor, Pierre Richard. 2001. Asymmetric Effect of Monetary Policy Shocks. Washington, DC: World Bank Working Paper 20433. [Google Scholar]

- Akinboade, Oludele Akiloye, Franz Krige Siebrits, and Elizabeth Wambach Niedermeier. 2004. The Determinants of Inflation in South Africa: An Econometric Analysis. Nairobi: AERC. [Google Scholar]

- Alehegn, Mebtu Melaku. 2021. Determinants of inflationin Sub-Saharan Africa: A systematic Review. Horn of Africa Journal of Business and Economics (HAJBE) 4: 17–23. [Google Scholar]

- Alemu, Minyahil, Wondaferahu Mulugeta, and Yikal Wassie. 2016. Monetary Policy and Inflation Dynamics in Ethiopia: An Empirical Analysis. Global Journal of Human Social Science: Economics 16: 44–60. [Google Scholar]

- Amassoma, Ditimi, Krey Sunday, and Emma Ebere Onyedikachi. 2018. The influence of money supply on inflation in Nigeria. Journao of Economics ana Management 31: 5–23. [Google Scholar] [CrossRef]

- Atil, Assia, and Mourad Saouli. 2020. Determinants of Inflation in Algeria: Analysis with a Vector Error Correction Model from 2001 to 2016. ASJP 7: 429–44. [Google Scholar]

- Atkin, Tim, and G. La Cava. 2017. The Transmission of Monetary Policy: How Does It Work? RBA Bulletin-September 2017. Available online: https://www.rba.gov.au/publications/bulletin/2017/sep/1.html (accessed on 12 October 2022).

- Badokhon, Sultana, and Faisal Rana. 2021. Macroeconomic determinants of inflation in middle east and north african countries. Palarch’s Journal of Archaeology of Egypt/Egoptology 18: 151–67. [Google Scholar]

- Bellemare, Charles, Rolande Kpekou Tossou, and Kevin Moran. 2020. The Determinents of Consumer Expectation: Evidence from US and Canada. No. 2020-52. Ottawa: Bank of Canada Staff Working Paper. [Google Scholar]

- Caglayan, Ebru, and Melek Asta. 2012. Interest Reaction Function of the Central Bank: The Case of Czech Republic. International Journal of Business and Social Sciences 3: 225–32. [Google Scholar]

- Cao, Tang. 2015. Paradox of Inflation: The Study on Correlation between Money Supply and Inflation in New Era. Ann Arbor: Arizona State University. [Google Scholar]

- Chaudhary, Sunil Kumar, and Li Xiumin. 2018. Analysis of the Determinants of Inflation in Nepal. American Journal of Economics 8: 209–12. [Google Scholar]

- Cooray, Arusha, and Naceur Khraief. 2018. Money growth and inflation: New evidence from a nonlinear and asymetric analysis. The Manchester School 87: 543–77. [Google Scholar] [CrossRef]

- Cukierman, Alex, and Antol Muscatell. 2008. Nonlinear Taylor Rules and Asymmetric Preferences in Central Banking: Evidence from the United Kingdom and the United. The B.E Journal of Macroeconomics 8. [Google Scholar] [CrossRef]

- Dajcman, Silvo. 2020. Nonlinear effects of monetary policy on the consumer loans market. Enomic Computationand Economic Cybernetics Studies and Research 54. [Google Scholar] [CrossRef]

- De Grauwe, Paul, and Magdalena Polan. 2005. Is Inflation Always and Everywhere a Monetary Phenomenon? Scandinaviana Journal of Economics 107: 239–59. [Google Scholar] [CrossRef]

- De Sá, Rodrigo, and Marcelo S. Portugal. 2015. Central bank and asymmetric preferences: An application of sieve estimators to the U.S. and Brazil. Economic Modelling 51: 72–83. [Google Scholar] [CrossRef] [Green Version]

- Debortoli, Davide, Ario Forni, Luca Gambetti, and Luca Sala. 2017. Asymmetric Effects of Monetary Policy Easing and Tightening. CEPR Discussion Paper No. DP15005. Available online: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3650120 (accessed on 14 November 2022).

- Ditimi, Amasoma, Keji Sunday, and Emma Ebere Onyedikachi. 2017. The Upshot of Money Supply and Inflation in Nigeria. Valahian Journal of Economic Studies 8: 75–90. [Google Scholar] [CrossRef] [Green Version]

- Dolado, Juan J., Maria Dolores, and Ruge Murcia. 2004. Are Central Banks Reaction Functions Asymmetric?: Evidence from Some Central Banks. Madrid: Department of Economics, Universidad Carlos lll de Madrid. [Google Scholar]

- Dua, Pami, and Deepika Goel. 2021. Determinants of Inflation in India. The Journal of Developing Areas 55: 205–21. [Google Scholar] [CrossRef]

- Espinosa-Vega, Marco A. 1997. How Powerful Is Monetary Policy in the Long Run? Economic Review-Federal reserve bank of Atlanta 83: 12. [Google Scholar]

- Esumanba, Sampon Vivian, Nanaa Danaa, and Eria Akyaa Konadu. 2019. The I mpact of Money Supply on Inflation Rate in Ghana. Research Journal of Finance and Accounting 10: 156–70. [Google Scholar]

- Friedman, Milton. 1989. Quantity theory of money. In Money. London: Palgrave Macmillian, pp. 1–40. [Google Scholar]

- Imbs, Jean, Eric Jondeau, and Florian Pelgrin. 2011. Sectoral Phillips Curves and the Aggregate Phillips curve. Journal of Monetary Economics 58: 328–44. [Google Scholar] [CrossRef]

- Jawadi, Reji, Shushanta K. Mallick, and Ricardo M. Sousa. 2013. Nonlinear Monetary Policy Reaction Functions in Large Emerging Economies: The Case of Brazil and China. Applied Economics 46: 973–84. [Google Scholar] [CrossRef]

- Katria, Sagar, Niaz Ahmed Bhutto, Flahhuddin Butt, Azhar Ali Domki, and Hyder Ali Khawaja. 2011. Is There Any Tradeoff Between Inflation And Unemployment? The Case of SAARC Countries. Pakistan Journal of ccommerce and Social science 8: 867–86. [Google Scholar]

- Kemal, Ali M. 2006. Is Inflation In Pakistan Monetary Phenomenon? The Pakista Development Review 45: 213–20. [Google Scholar]

- Kiganda, Evans. 2014. Relationship between money supply and inflation in Kenya. Journal of Social Economics 2: 63–83. [Google Scholar]

- Kisswani, Khalid, and Mohammad I. Elian. 2017. Exploring the nexus between oil prices and sectoral stock prices: Nonlinear evidence from Kuwait stock exchange. Cngent Economics and Finance 5: 1286061. [Google Scholar] [CrossRef]

- Komijani, Akbar, Mostafa Sargolzaei, Razieh Ahmad, and Marzieh Ahmadi. 2012. Asymmetric Effects of Monetary Shocks on Growth and Inflation: Case study in Iran. International Journal of Business and Social Science 3: 224–30. [Google Scholar]

- Kumar, Ankit, and Pradyumna Dash. 2020. Changing transmission of monetary policy on disaggregate inflation in India. Economic Modelling 92: 109–25. [Google Scholar] [CrossRef]

- Loayza, Norman, and Raimundo Soto. 2002. Inflation Targeting: An Overview. Series on Central Banking, Analysis, and Economic Policies, No. 5. Washington, DC: World Bank. [Google Scholar]

- Loungani, Prakash, and Phillip Swagel. 2001. Sources of Inflation in Developing Countries. (December 2001). IMF Working Paper No.01/198. Available online: https://ssrn.com/abstract=880326 (accessed on 14 September 2022).

- Mahyar, Hami. 2017. The Effect of Inflation on Financial Development Indicators in Iran (2000–2015). Studies in Business and Economics 12: 53–62. [Google Scholar]

- Murayama, Haruhiko. 2017. Why Does Money Supply Growth Not Push Up Prices? Chuo City: Tokyo Research Institute Economic Report, Summer. Available online: https://www.kyotobank.co.jp/houjin/report/pdf/201708_02_e.pdf (accessed on 14 September 2022).

- Narayan, Paresh Kumar, and Ruipeng Liu. 2015. A unit root model for trending time series energy variables. Energy Economies 50: 391–402. [Google Scholar] [CrossRef]

- Nelson, Edward. 2008. Why Money Growth Determines Inflation in the Long Run: Answering the Woodford Critique. Journal of Money, Credit and Banking 40: 1791–814. [Google Scholar] [CrossRef]

- Nobay, Robert A., and David A. Peel. 2003. Optimal Monetary Policy in a Model of Asymmetric Bank Preferences. The Economic Journal 113: 657–65. [Google Scholar] [CrossRef]

- Ofori, Collins Frimpong, Benjamin Adjei Danquah, and Xuegong Zhang. 2017. The Impact of Money Supply on Inflation, A Case of Ghana. Imperial Journal of Interdisciplinary Research 3: 2312–18. [Google Scholar]

- Perasan, M. Hashem, Yongcheol Shin, and Richard J. Smith. 2001. Bounds testing approaches to the analysis of level relationship. Journal of Applied Econometrics 16: 289–326. [Google Scholar]

- Perevalov, Nikita, and Philip Maier. 2010. On the Advantages of Disaggregated Data: Insights from Forecasting the U.S. Economy in a Data-Rich Enviromnent. No. 2010-10. Ottawa: Bank of Canada. [Google Scholar]

- Rasool, Horoon, and Md. Tarique. 2017. Determinants of Inflation: Evidence from India using Autoregressive Distributed Lagged Approach. Asian Journal of Research in Banking and Finance 8: 1–17. [Google Scholar] [CrossRef]

- Roshan, Sedigheh Atrkar. 2014. Inflation and Money supply growth in Iran: Empirical Evidences from Cointegration and Causality. Iranian Economic Review 18: 131–52. [Google Scholar]

- Shin, Yongcheol, Byungvhul Yu, and Matthew Greenwood Nimmo. 2014. Modelling Asymmetric Cointegration and Dynamic Multipliers in a Nonlinear ARDL Framework. New York: Festschrift in Honor of Peter Schmidt Springer, pp. 281–314. [Google Scholar]

- Statistics South Africa. 2021. The Annual Reweighted and Industry Based Consumer Price Index of December; Pretoria: Statistics South Africa.

- Sultana, Nair, Rabiunnesa Koli, and Mahamuda Firoj. 2019. Causal relationship of money supply and inflation: A study of bangladesh. Asian Economic and Financial Review 9: 42–51. [Google Scholar] [CrossRef] [Green Version]

- Taslim, Mohammad Ali. 1982. Inflation in Bangladesh: A Reexamination of the Structuralist, and Monetarist Controversy. The Bangladesh Development Studies, 23–52. Available online: https://www.jstor.org/stable/4094338 (accessed on 14 September 2022).

- Tolulope, Olumuyiwa. 2016. Asymmetry Effects of Monetary Policy Shocks on Output in Nigeria: A Non-Linear Autoregressive Distributed Lag (ARDL) Approach. Available online: https://www.researchgate.net/publication/320907736 (accessed on 14 September 2022).

- Uddin, Ijaz. 2020. What determine inflation in Pakistan: An investigation through structural Equation modeling by using time series data for a period from 1975 to 2017. Economic Consultant 4: 54–72. [Google Scholar] [CrossRef]

- Ullah, Sana, Iihan Ozturk, and Sidra Sohail. 2021. The asymmetric effects of fiscal and monetary policy instruments on Pakistan’s envirinmental Pollution. Enviromnental Science and Pollution Research 28: 7450–61. [Google Scholar] [CrossRef] [PubMed]

- Wang, X. 2017. The Quantity Theory of Money: An Empirical and Quantitative Rassessment. Available online: htttps://sites.wustl.edu/xiwang/files/2017/09/QTMmainCIA-v206pt.pdf (accessed on 14 September 2022).

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Consumer Price Index (CPI) Components | Component’s Percentage Weights in the Basket |

|---|---|

| 1. Housing | 42.36% |

| 2. Transportation | 18.18% |

| 3. Food and Beverages | 14.26% |

| 4. Medical Care | 8.49% |

| 5. Education and Communication | 6.41% |

| 6. Recreation | 5.11% |

| 7. Other Goods and services | 2.74% |

| 8. Apparel | 2.46% |

| Independent Variables and Description | Units | Source | Expected Sign |

|---|---|---|---|

| 1. Money supply | % | Easy Data | + |

| 2. Oil price | % | Easy Data | + |

| Dependent Variables (Sectoral inflation) | |||

| 1. Food and non-alcoholic beverages | % | Easy Data | + |

| 2. Alcoholic beverages and tobacco | % | Easy Data | + |

| 3. Clothing and Footwear | % | Easy Data | + |

| 4. Housing and utilities | % | Easy Data | + |

| 5. Households’ contents and equipment | % | Easy Data | + |

| 6. Health | % | Easy Data | + |

| 7. Transport | % | Easy Data | + |

| 8. Communication | % | Easy Data | + |

| 9. Recreation and culture | % | Easy Data | + |

| 10. Education | % | Easy Data | + |

| 11. Restaurants and hotels | % | Easy Data | + |

| 12. Miscellaneous goods and services | % | Easy Data | + |

| Critical Values | |||||

|---|---|---|---|---|---|

| Variables | Tau Stat | 1% | 5% | 10% | Order |

| Money supply | −9.79484 | −4.08887 | −3.47255 | −3.16345 | I (1) |

| Oil price | −7.89026 | −2.59574 | −1.94513 | −1.61398 | I (0) |

| Sectoral inflation | |||||

| Alcoholic beverages and tobacco | −19.0511 | −4.88713 | −3.47255 | −3.16345 | I (1) |

| Clothing and Footwear | −6.91878 | −2.59574 | −1.94513 | −1.61398 | I (0) |

| Communication | −5.54312 | −4.08335 | −3.47003 | −3.16198 | I (0) |

| Education | −7.56257 | −3.52423 | −2.90235 | −2.58858 | I (1) |

| Food and non-alcoholic beverages | −4.93840 | −3.51905 | −2.90013 | −2.58740 | I (0) |

| Health | −6.80065 | −3.52423 | −2.90235 | −2.58858 | I (1) |

| Households’ contents and equipment | −4.83999 | −4.08335 | −3.47003 | −3.16198 | I (0) |

| Housing and utilities | −3.96782 | −3.53320 | −2.90621 | −2.59062 | I (0) |

| Miscellaneous goods and services | −4.97819 | −3.52423 | −2.90235 | −2.58858 | I (1) |

| Recreation and culture | −5.23732 | −4.08335 | −3.47003 | −3.16198 | I (0) |

| Restaurants and hotels | −5.21867 | −4.14458 | −3.49869 | −3.17857 | I (0) |

| Transport | −8.64064 | −2.59574 | −1.94513 | −1.61398 | I (0) |

| Lower Bound I (0) | Upper Bound I (0) | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Dependent Variables | F Stat | 1% | 2.5% | 5% | 10% | 1% | 2.5% | 5% | 10% |

| Alcoholic beverages and tobacco | 11.78601 | 2.72 | 3.23 | 3.69 | 4.29 | 3.77 | 4.35 | 4.89 | 5.61 |

| Clothing and Footwear | 8.410977 | 2.72 | 3.23 | 3.69 | 4.29 | 3.77 | 4.35 | 4.89 | 5.61 |

| Communication | 7.813047 | 2.72 | 3.23 | 3.69 | 4.29 | 3.77 | 4.35 | 4.89 | 5.61 |

| Education | 5.983043 | 2.72 | 3.23 | 3.69 | 4.29 | 3.77 | 4.35 | 4.89 | 5.61 |

| Food and non-alcoholic beverages | 2.60083 | 2.72 | 3.23 | 3.69 | 4.29 | 3.77 | 4.35 | 4.89 | 5.61 |

| Health | 8.119789 | 2.72 | 3.23 | 3.69 | 4.29 | 3.77 | 4.35 | 4.89 | 5.61 |

| Households’ contents and equipment | 7.187314 | 2.72 | 3.23 | 3.69 | 4.29 | 3.77 | 4.35 | 4.89 | 5.61 |

| Housing and utilities | 5.135456 | 2.72 | 3.23 | 3.69 | 4.29 | 3.77 | 4.35 | 4.89 | 5.61 |

| Miscellaneous goods and services | 1.828820 | 2.72 | 3.23 | 3.69 | 4.29 | 3.77 | 4.35 | 4.89 | 5.61 |

| Recreation and culture | 96.33065 | 2.72 | 3.23 | 3.69 | 4.29 | 3.77 | 4.35 | 4.89 | 5.61 |

| Restaurants and hotels | 14.25950 | 2.72 | 3.23 | 3.69 | 4.29 | 3.77 | 4.35 | 4.89 | 5.61 |

| Transport | 63.87961 | 2.72 | 3.23 | 3.69 | 4.29 | 3.77 | 4.35 | 4.89 | 5.61 |

| INDEPENDENT VARIABLE | ALCOHOLIC BEVERAGES AND TOBACCO | CLOTHING AND FOOTWEAR | COMMUNICATION | EDUCATION | HEALTH | HOUSEHOLDS CONTENTS AND EQUIPMENTS | HOUSING AND UTILITIES | RECREATION AND CULTURE | RESTAURANTS AND HOTELS | TRANSPORT |

|---|---|---|---|---|---|---|---|---|---|---|

| constant | 6.27 [0.0000] | −0.04 [0.9293] | −0.20 [0.1848] | 1.14 [0.0190] | 3.03 [0.0000] | 0.62 [0.0009] | 0.24 [0.5472] | −0.12 [0.5957] | 1.64 [0.0079] | 0.15 [0.6892] |

| (S (−1)) | 0.77 [0.00205] | −0.04 [0.3529] | −0.31 [0.0247] | 0.06 [0.3100] | 0.36 [0.0020] | 0.04 [0.1274] | ||||

| −0.01 [0.817] | 0.04 [0.4820] | |||||||||

| −0.02 [0.7644] | −0.11 [0.0872] | |||||||||

| 0.005 [0.3081] | −0.00 [0.1952] | 0.00 [0.8639] | ||||||||

| −0.15 [0.0122] | ||||||||||

| 0.18 [0.0379] | ||||||||||

| 0.01 [0.0083] | −0.00 [0.6230] | |||||||||

| ECM (−1) | −2.35 [0.0000] | −0.86 [0.0000] | −1.01 [0.0000] | −0.50 [0.0074] | −1.40 [0.0000] | −0.58 [0.0000] | −0.31 [0.0016] | −0.53 [0.0000] | −0.67 [0.0000] | −1.01 [0.0000] |

| Sectors | Coefficients | Coefficients | Coefficients |

|---|---|---|---|

| Alcoholic beverages and tobacco | −0.11 [0.0000] | −0.08 [0.0005] | −0.01 [0.0064] |

| Clothing and Footwear | −0.28 [0.0914] | −0.29 [0.0701] | −0.00 [0.6074] |

| Communication | −0.00 [0.9009] | −0.00 [0.9578] | 0.00 [0.7045] |

| Education | −0.13 [0.1308] | −0.12 [0.1626] | −0.02 [0.1106] |

| Health | −0.20 [0.0000] | −0.17 [0.0000] | −0.02 [0.0066] |

| Households’ contents and equipment | 0.05 [0.5351] | 0.06 [0.4423] | −0.00 [0.2323] |

| Housing and utilities | 0.44 [0.2874] | 0.41 [0.2961] | 0.06 [0.4856] |

| Recreation and culture | −0.10 [0.4417] | −0.12 [0.3510] | −0.02 [0.1361] |

| Restaurants and hotels | −0.25 [0.0360] | −0.21 [0.0785] | −0.00 [0.7263] |

| Transport | 0.09 [0.3918] | 0.07 [0.4870] | 0.09 [0.0000] |

(Long Run Asymmetry) | (Short Run Asymmetry) | Conclusion | |

|---|---|---|---|

| Sectors | F Statistic | F Statistic | |

| Alcoholic beverages and tobacco | 5.72 [0.0196] | -- | Long run asymmetry |

| Clothing and Footwear | 3.15 [0.0798] | -- | Long run asymmetry |

| Communication | 0.00 [0.9224] | -- | Long run symmetry |

| Education | 0.90 [0.3442] | -- | Long run symmetry |

| Health | 14.04 [0.0004] | -- | Long run asymmetry |

| Households’ contents and equipment | 3.33 [0.0724] | -- | Long run asymmetry |

| Housing and utilities | 1.14 [0.2883] | -- | Long run symmetry |

| Recreation and culture | 0.55 [0.4591] | -- | Long run symmetry |

| Restaurants and hotels | 4.25 [0.446] | -- | Long run symmetry |

| Transport | 0.04 [0.8307] | -- | Long run symmetry |

| Null Hypothesis | F-Statistic | Probability |

|---|---|---|

| Bi-directional causality | ||

| Education does not granger cause M3-pos | 5.16592 | 0.0081 |

| M3-pos does not granger cause Education | 2.59922 | 0.0816 |

| Health does not granger cause M3-pos | 3.41821 | 0.0384 |

| M3-pos does not granger cause Health | 2.54069 | 0.0862 |

| Uni-directional causality | ||

| Oil price does not granger cause Health | 2.67650 | 0.0758 |

| M3-pos does not granger cause Households’ contents and equipment | 3.20350 | 0.0467 |

| M3-neg does not granger cause Households’ contents and equipment | 3.33885 | 0.0413 |

| M3-pos does not granger cause Housing and utilities | 2.88424 | 0.0627 |

| M3-neg does not granger cause Housing and utilities | 3.00191 | 0.0562 |

| Oil price does not granger cause Recreation and culture | 3.98495 | 0.0230 |

| M3-pos does not granger cause Restaurants and hotels | 4.99151 | 0.0109 |

| M3-neg does not granger cause Restaurants and hotels | 5.13120 | 0.0097 |

| Oil price does not granger cause Transport | 6.54824 | 0.0025 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mndebele, S.; Tewari, D.D.; Ilesanmi, K.D. Testing the Validity of the Quantity Theory of Money on Sectoral Data: Non-Linear Evidence from South Africa. Economies 2023, 11, 71. https://doi.org/10.3390/economies11020071

Mndebele S, Tewari DD, Ilesanmi KD. Testing the Validity of the Quantity Theory of Money on Sectoral Data: Non-Linear Evidence from South Africa. Economies. 2023; 11(2):71. https://doi.org/10.3390/economies11020071

Chicago/Turabian StyleMndebele, Siyabonga, Devi Datt Tewari, and Kehinde Damilola Ilesanmi. 2023. "Testing the Validity of the Quantity Theory of Money on Sectoral Data: Non-Linear Evidence from South Africa" Economies 11, no. 2: 71. https://doi.org/10.3390/economies11020071