1. Introduction

Sustainability reporting practices have increased significantly in the last two decades. This phenomenon has been caused by the number of companies publishing social and environmental responsibility information in annual reports, sustainability reports, and integrated reports on their websites. Sustainability reporting is a development of the Triple Bottom Line (TBL) concept. Previously, business was only oriented to one P (Profit); now, it has developed into the Triple P model (Profit, Planet, People). The corporate sustainability concept describes the companies’ abilities to create value and the ability to stand in the long term.

Mahmood (

2018) argues that sustainability activities and governance practices are essential in company operations because the governance practices are designed for all interests within the organizational context.

Green governance is a concept that bridges conflicts between humans and nature through a set of institutional rules. In other words, the green governance action ensures that decision-making maintains sustainable operations in terms of their economic, social, and environmental aspects (

Mahmood and Orazalin 2017;

Post et al. 2011). The sustainability performance succeeds when it is supported by the company’s commitment to energy-saving, reducing environmental impacts, using natural resources effectively and efficiently, developing human resources, as well as invest in the community, so that the company is sustainable. Green governance, which is supported by a sustainability commitment, is expected to have a positive impact by improving sustainability performance and disclosure quality (

Aznar et al. 2016). Several studies explain that green governance has an important role in the quality sustainability report and sustainability performance (

García-Sánchez et al. 2019;

Mahmood and Orazalin 2017;

Amran et al. 2014;

Post et al. 2011). Sustainability report quality (SRQ) faces challenges in terms of reliability and transparency.

Hussain and Rigoni (

2018) argue that company management has control over the reporting process so that information is only disseminated if it has a positive impact on the company rather than providing transparent and accountable information to stakeholders. However, stakeholders’ demands for ethical or socially responsible investments are increasing. As a result, the need for quality sustainability reports is also increasing. According to agency theory there is a relationship between corporate governance practices and corporate disclosure practices. Good governance practices will strengthen the company’s internal control in terms of environmental protection, reduce opportunistic management behavior and information asymmetry, and improve reporting quality. Meanwhile, the resource-based view (RBV) theory explains that companies must use resources effectively to achieve strategic goals. The board is a strategic resource responsible for confirming the management interests, the shareholders, and other stakeholders. The values and attitudes of boards, managers, and committees regarding sustainability are very important for the company’s success or failure (

Jo and Harjoto 2011;

Naciti 2019).

Previous research has examined the board size and the proportion independent board members on the effect of sustainability reports (

Naciti 2019;

Mason 2019;

Liu et al. 2020). However,

Amran et al. (

2014) do not find a significant relationship between the existence of a board and the voluntary disclosure since the governance practices have a deficiency, such as the lack of disclosure caused by the low level of the effectiveness and reliability of internal control mechanisms. The board diversity affects the quality of sustainability reports (

Post et al. 2011;

Hussain and Rigoni 2018;

García-Sánchez et al. 2019;

Arayssi et al. 2020). In contrast,

Adams (

2015) argues that female directors have the same impact as male directors. Furthermore, a chief sustainability officer (CSO) is an executive manager who is responsible to the program design, and has the duty of implementing and reporting the sustainability activities (

Peters and Romi 2012;

Fu et al. 2019). However,

Menz and Scheef (

2014) find no evidence that the existence of a CSO improved the company’s performance. In order to ensure that the CSO has carried out his or her duties and functions, a sustainability committee is needed. A special committee that deals with sustainability or CSR, is expected to play an important role in ensuring that the CSR perspective is serving as a part of the organization’s strategic direction and to apply it into a real action (

Amran et al. 2014;

Hussain and Rigoni 2018;

Arayssi et al. 2020). However, according to

Berrone and Gomez-Mejia (

2009), the committee’s role does not run optimally.

Rodrigue et al. (

2013) state that the presence of the sustainability committee provides only symbolic legitimacy the eyes to the public, rather than having substantive effects.

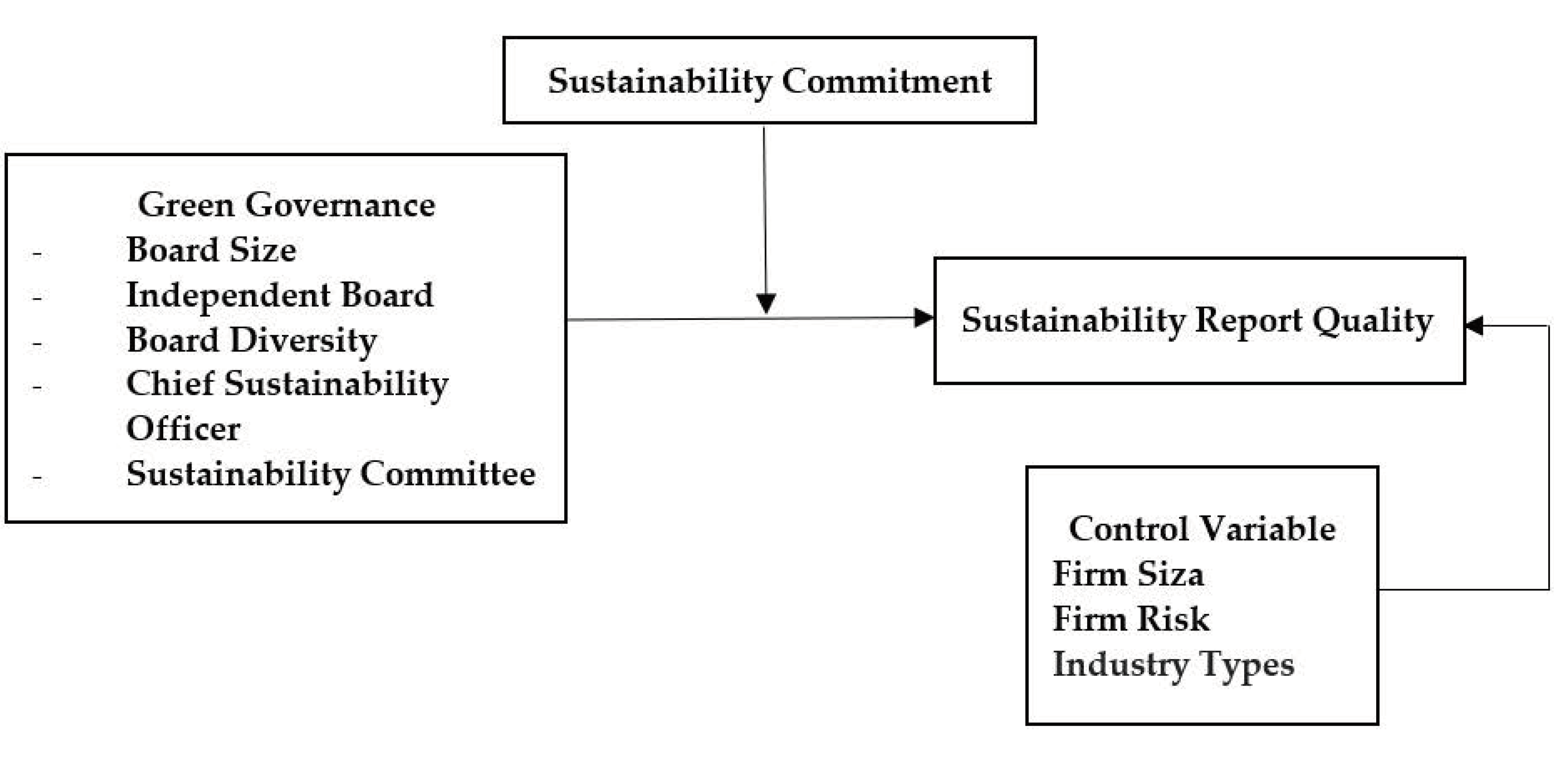

The findings of this study still yield inconsistent results. Therefore, this study propose a moderating variable that potentially strengthens the relationship between green governance and the quality of sustainability reports, namely sustainability commitment, this is because (1) the company’s success in the future is not only influenced by green governance practices but also needs to be supported by a strong commitment to sustainability activities (

Aznar et al. 2016); and (2) commitment is an intangible resource that helps organizations gain a competitive advantage. However, the relationship between commitment to sustainability and performance has not been widely studied. This is because sustainability commitments must be initiated effectively in the company to lead to performance improvement (

Luzzini et al. 2015). In this study, the sustainability commitments are measured by social costs (

Rhou et al. 2016). The uniqueness of this research is (1) measuring the quality of sustainability report is placed on conciseness, clarity, and reliability (

García-Sánchez et al. 2019); (2) the use of sustainability commitment measured by social costs as a moderating variable; and (3) the research focuses on the phenomenon of the quality of sustainability reports in ASEAN countries.

The trend of sustainability reports in ASEAN countries has also increased in line with the formation of the ASEAN CSR Network (ACN) community through the ASEAN Foundation. ASEAN countries have a unique geographical location; therefore, it is not easy to bridge the environmental sustainability issues to the economic development of other regions. The high growth of the economic sector that improves prosperity is not well-balanced by attention to environment and social investment. As a result, it can be a problem for the company’s sustainability in the future (

Loh et al. 2018). Therefore, the ASEAN CSR Network has a responsibility to promote the social responsibility (CSR) agenda in all ASEAN into the visions and missions of companies. Furthermore, it is expected that the investment will contribute to the sustainable social and economic development; therefore, it will make ASEAN countries a better place to live (

Loh et al. 2018;

Husni Syam et al. 2020).

This study examines the effect of green governance on the quality of sustainability reports. Then, we examine the moderating role of sustainability commitment to the relationship between green governance and the quality of sustainability reports. The study is based on a sample comprising 409 observations from 154 companies in six ASEAN countries: Indonesia, Malaysia, Singapore, Thailand, the Philippines, and Vietnam. These six countries have developing capital markets and since 2012, they have started a securities transaction connectivity program to encourage the growth of the ASEAN capital market and to expand all investment opportunities. The findings of this study are expected to encourage the business organizations in ASEAN to improve sustainability practices based on good governance and high commitment in the future. Ultimely, this will help to improve the sustainability reports’ quality.

This paper is organized into five sections including the introduction section.

Section 2 reviews the literature and develops the hypotheses.

Section 3 describes the method or approach used in this research. The results and analysis are presented and discussed in

Section 4 and

Section 5, the authors provide conclusions, implications, and suggestions for future research.

5. Conclusions

This study examines the effects of green governance on the quality of sustainability reports and the role of sustainability commitment in ASEAN countries. A sustainability report is a good medium to communicate the relevant information about sustainability and monitor management behavior. The results of the research show that green governance plays an important role in sustainability reporting and in ensuring the quality of the reports. Other results such as the proportion of independent board members, female directors, and the commitment to sustainability have great influences on the quality of sustainability reports. The board size has little effect on the reliability of the quality. Likewise, effect of the chief sustainability officer on the conciseness of the sustainability reports is small. Meanwhile, the existence of sustainability committee is not proven to be correlated to the quality of reports.

In particular, the commitment to sustainability affects the quality of sustainability reports. In contrast, the commitment to social responsibility is applied through the social costs. Companies have an interest in widely disclosing and publishing their social responsibility activities. The social costs also moderate the proportion of female directors and the quality of sustainability reports. However, the role of sustainability commitment does not moderate the effect of the board size, the independent board, the CSOs, and the sustainability committees on the quality of sustainability reports.

The empirical evidence shows that quality of sustainability reports in ASEAN countries needs to be improved. This result can also be seen in terms of the sustainability report which is only observed at 27.87%. It has an assurance assessment from an independent party. One possible explanation is the existence of mandatory regulations and an external environment that is weak in encouraging it. There are regulations to require quality assurance. The most important finding is the low presence of female directors in the composition of the boards of directors. Even though their role has a significant effect on the quality of sustainability reports because their narrative ability and sensitivity, further research is required on the role of boards, management, committees, and sustainability commitments in the reporting process. The practice of green governance throughout the company is an important step that cannot be ignored in designing an effective sustainability report. The company must establish strategy and commitment in its organization to produce quality sustainability practices and for this to be reflected in the report. Other findings are obtained from the company’s characteristics where company size and type of industry are positively correlated with the quality of sustainability reports.

This research findings contribute to the following scopes: Firstly, the empirical results show that green governance helps to improve corporate reporting quality. Therefore, the government and the regulators must have initiatives to implement green governance and commitment to sustainability. Secondly, investors should invest in companies with good green governance practices and a commitment to sustainability. In particular, the proportion of independent members on boards, gender diversity, and CSO are essential factors. Thirdly, companies with strong commitments to sustainability and green corporate governance are competitive resources that support businesses in growing, attracting more investment, and earning stakeholders’ trust. Lastly, this research also contributes to the agency theory and the resource-based theory related to the green governance practices as effective corporate resources in improving the quality of sustainability reports in terms of clarity, conciseness, and reliability of reporting in the context of ASEAN countries.

Furthermore, this study has several limitations, which may also serve to provide opportunities for future research. Firstly, the sample companies sample only provides information on obtained social costs. Some of the companies under observation spent money on social costs, but the amount was unclear. Therefore, it is necessary to consider using another measurement to represent each company’s sustainability commitment. Lastly, while this study only focuses on three aspects of quality, namely, clarity, conciseness, and reliability, looking at other aspects such as tone, accuracy, completeness, comparability, and legibility may also be necessary to further investigate the comprehensive SRQ. This offers many opportunities for future research in expanding the scope of SRQ.

{kind=link}