Analysis of Maximization Strategy Intangible Assets through the Speed of Innovation on Knowledge-Driven Business Performance Improvement

Abstract

:1. Introduction

2. Methodology

2.1. Financial Performance

2.2. Human Capital

2.3. Structural Capital

2.4. Consumer Capital

2.5. Speed of Innovation

3. Results

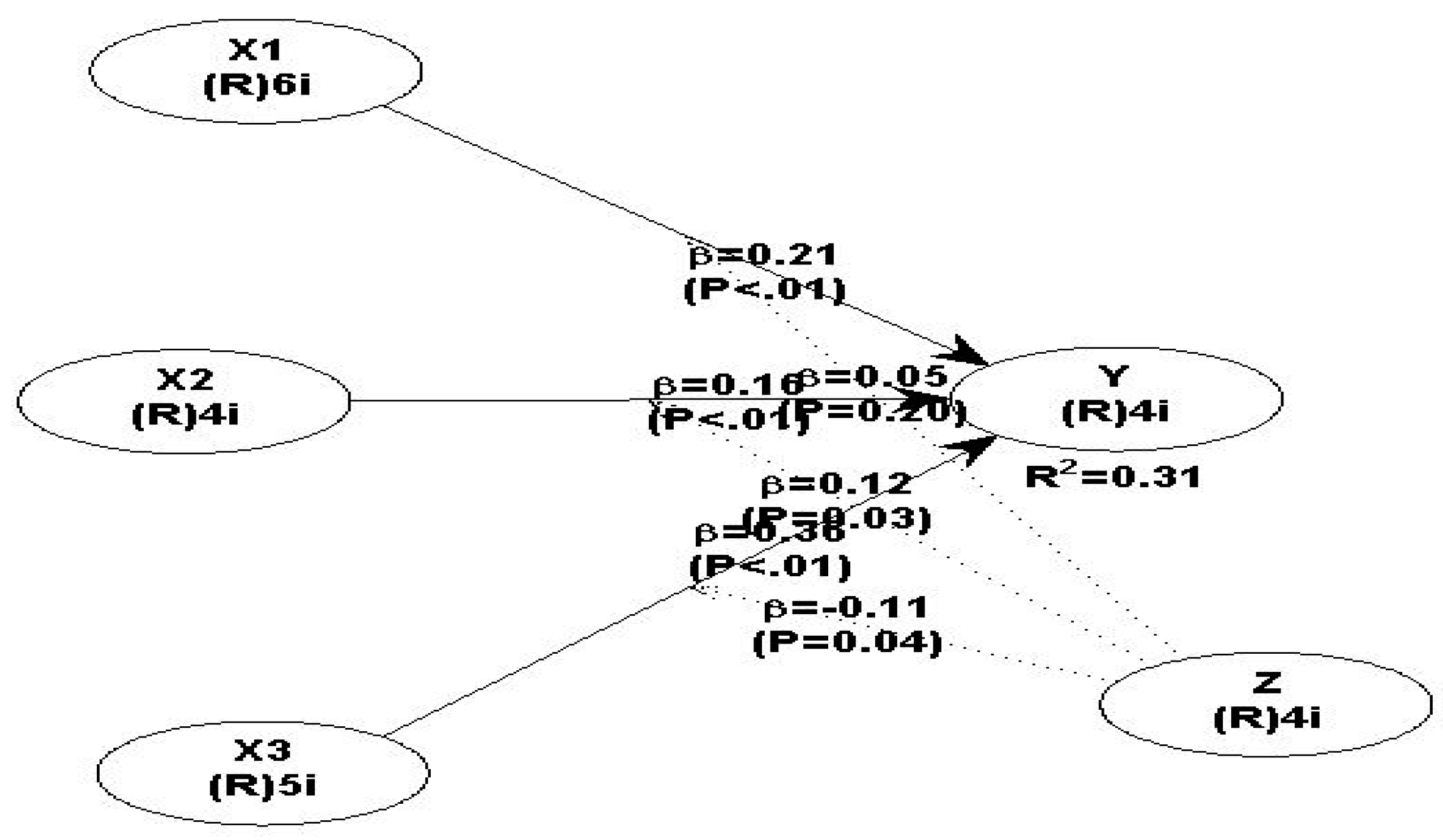

3.1. The Effect of Human Capital on Improving Financial Performance

3.2. The Effect of Structural Capital on Improving Financial Performance

3.3. The Effect of Consumer Capital on Improving Financial Performance

3.4. Speed of Innovation Moderates the Effect of Human Capital on Improving Financial Performance

3.5. Speed of Innovation Moderates the Effect of Structural Capital on Improving Financial Performance

3.6. Speed of Innovation Moderates the Effect of Consumer Capital on Improving Financial Performance

- Y = γ1X + γ2M + γ3XM + ε

- Description:

- Y: Endogenous variables;

- X: Exogenous variable;

- γ: The influence coefficient of the exogenous on the endogenous latent variable;

- M: Moderating variables;

4. Discussion

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Abuzayed, Bana. 2012. Working capital management and firms’ performance in emerging markets: The case of Jordan. International Journal of Managerial Finance 8: 155–79. [Google Scholar] [CrossRef]

- Adnan, Nur Syuhada, Amrizah Kamaluddi, and Nawal Kasim. 2013. Intellectual Capital in Religious Organisations: Malaysian Zakat Institutions Perspective. Middle-East Journal of Scientific Research 16: 368–77. [Google Scholar] [CrossRef]

- Affandi, Azhar, Akhmad Sobarna Sarwani, Heri Erlangga, Ade Onny Siagian, Agus Purwanto, Aidil Amin Effendy, and G. Juhaeri. 2020. Optimization of MSME empowerment in facing competition in the global market during the COVID-19 pandemic. Systematic Reviews in Pharmacy 11: 1506–15. [Google Scholar]

- Aghamirian, Bahman, Behrouz Dorri, and Babak Aghamirian. 2015. Customer knowledge management application in gaining organization’s competitive advantage in electronic commerce. Journal of Theoretical and Applied Electronic Commerce Research 10: 63–78. [Google Scholar] [CrossRef] [Green Version]

- Agostini, Lara, Anna Nosella, and Roberto Filippini. 2017. Does intellectual capital allow improving innovation performance? A quantitative analysis in the SME context. Journal of Intellectual Capital 18: 400–18. [Google Scholar] [CrossRef]

- Akman, Gülşen, and Cengiz Yilmaz. 2019. Innovative capability, innovation strategy and market orientation: An empirical analysis in Turkish software industry. In Managing Innovation: What Do We Know About Innovation Success Factors? Singapore: World Scientific Publishing, pp. 139–81. [Google Scholar]

- Aksoy, Hasan. 2017. How do innovation culture, marketing innovation and product innovation affect the market performance of small and medium-sized enterprises (SMEs). Technology in Society 51: 133–41. [Google Scholar] [CrossRef]

- Al-Ansari, Yahya, Marwan Altalib, and Muna Sardoh. 2013. Technology orientation, innovation and business performance: A study of Dubai SMEs. The International Technology Management Review 3: 1–11. [Google Scholar] [CrossRef] [Green Version]

- Alipour, Mohammad. 2012. The effect of intellectual capital on firm performance: An investigation of Iran insurance companies. Measuring Business Excellence 16: 53–66. [Google Scholar] [CrossRef]

- Alrowwad, Ala’aldin, and Shadi Habis Abualoush. 2020. Innovation and intellectual capital as intermediary variables among transformational leadership, transactional leadership, and organizational performance. Journal of Management Development 39: 196–222. [Google Scholar] [CrossRef]

- Aramburu, Nekane, Josune Sáenz, and Carlos Blanco. 2013. Structural capital, innovation capability, and company performance in technology-based colombian firms. Proceedings of the International Conference on Intellectual Capital, Knowledge Management & Organizational Learning 2: 20–29. [Google Scholar]

- Archer-Brown, Chris, and Jan Kietzmann. 2018. Strategic knowledge management and enterprise social media. Journal of Knowledge Management 22: 1288–309. [Google Scholar] [CrossRef]

- Aryanto, Riza, Avanti Fontana, and Adi Zakaria Afiff. 2015. Strategic human resource management, innovation capability and performance: An empirical study in Indonesia software industry. Procedia-Social and Behavioral Sciences 211: 874–79. [Google Scholar] [CrossRef] [Green Version]

- Babai, Fatemeh, Rogieh Niazy, Maryam Talebi, and Jamal Mohamade. 2016. Intellectual Capital Measuring and Reporting. Bull. Sociétét R. Des. Sci. Liege 85: 1063–69. [Google Scholar] [CrossRef]

- Bagher Taghieh, Mohammad, Sedigheh Taghieh, and Zahra Poorzamani. 2013. The effects of relational capital (customer) on the market value and financial performance. European Online Journal of Natural and Social Sciences 2: 207–11. [Google Scholar]

- Baporikar, Neeta, Geoffrey Nambira, and Geroldine Gomxos. 2016. Exploring factors hindering SMEs’ growth: Evidence from Nambia. Journal of Science and Technology Policy Management 7: 190–211. [Google Scholar] [CrossRef]

- Barney, Jay B., and Alison Mackey. 2016. Text and metatext in the resource-based view. Human Resource Management Journal 26: 369–78. [Google Scholar] [CrossRef]

- Bayraktaroglu, Ayse Elvan, Fethi Calisir, and Murat Baskak. 2019. Intellectual capital and firm performance: An extended VAIC model. Journal of Intellectual Capital 20: 406–25. [Google Scholar] [CrossRef]

- Bendickson, Joshua S., and Timothy D. Chandler. 2017. Operational performance: The mediator between human capital developmental programs and financial performance. Journal of Business Research 94: 162–71. [Google Scholar] [CrossRef]

- Beringer, Claus, Daniel Jonas, and Alexander Kock. 2013. Behavior of internal stakeholders in project portfolio management and its impact on success. International Journal of Project Management 31: 830–46. [Google Scholar] [CrossRef]

- Budi, Ichsan Setiyo. 2019. The Effect of Intellectual Capital and Islamic Corporate Governance on Islamic Social Reporting Disclosure with Financial Performance Mediation. The Winners 20: 95–110. [Google Scholar] [CrossRef] [Green Version]

- Callarisa, Luis, Javier Sánchez García, John Cardiff, and Alexandra Roshchina. 2012. Harnessing social media platforms to measure customer-based hotel brand equity. Tourism Management Perspectives 4: 73–79. [Google Scholar] [CrossRef]

- Campbell, Benjamin A., Russell Coff, and David Kryscynski. 2012. Rethinking sustained competitive advantage from human capital. The Academy of Management Review (AMR) 37: 376–95. [Google Scholar] [CrossRef] [Green Version]

- Campo, Sara, Ana M. Diaz, and María J. Yagüe. 2014. Hotel innovation and performance in times of crisis. International Journal of Contemporary Hospitality Management 26: 1292–311. [Google Scholar] [CrossRef]

- Casadesus-Masanell, Ramon, and Feng Zhu. 2013. Business model innovation and competitive imitation: The case of sponsor-based business models. Strategic Management Journal 34: 464–82. [Google Scholar] [CrossRef] [Green Version]

- Casalino, Nunzio, Stefan Ivanov, and Toshko Nenov. 2014. Innovation’s governance and investments for enhancing competitiveness of manufacturing SMEs. Law and Economics Yearly Review Journal 3: 72–97. [Google Scholar]

- Chahal, Hardeep, and Purnima Bakshi. 2015. Examining intellectual capital and competitive advantage relationship: Role of innovation and organizational learning. International Journal of Bank Marketing 33: 376–99. [Google Scholar] [CrossRef]

- Chatterjee, Joydeep. 2016. Strategy, human capital investments, business-domain capabilities, and performance: A study in the global software services industry. Strategic Management Journal 38: 588–608. [Google Scholar] [CrossRef]

- Cherkesova, Elvira Y., Evgeniya A. Breusova, Ekaterina P. Savchishkina, and Nataliya E. Demidova. 2016. Competitiveness of the human capital as strategic resource of innovational economy functioning. Journal of Advanced Research in Law and Economic 7: 1662–67. [Google Scholar]

- Churet, Cecile, and Robert G. Eccles. 2014. Integrated reporting, quality of management, and financial performance. Journal of Applied Corporate Finance 26: 56–64. [Google Scholar] [CrossRef]

- Costa, Ricardo V., Carlos Fernández-Jardon Fernández, and Pedro Figueroa Dorrego. 2014. Critical elements for product innovation at Portuguese innovative SMEs: An intellectual capital perspective. Knowledge Management Research and Practice 12: 322–38. [Google Scholar] [CrossRef]

- Crane, Lesley, and Nick Bontis. 2014. Trouble with tacit: Developing a new perspective and approach. Journal of Knowledge Management 18: 1127–40. [Google Scholar] [CrossRef]

- Davcik, Nebojsa S. 2014. The use and misuse of structural equation modeling in management research: A review and critique. Journal of Advances in Management Research 11: 47–81. [Google Scholar] [CrossRef]

- Dawkins, Cedric E. 2014. The principle of good faith: Toward substantive stakeholder engagement. Journal of Business Ethics 121: 283–95. [Google Scholar] [CrossRef]

- Deniswara, Kevin, Ratu Marwaah Firhatil Uyuun, Ang Swat Lin Lindawati, and Willnaldo Willnaldo. 2019. Intellectual Capital Effect, Financial Performance, and Firm Value: An Empirical Evidence from Real Estate Firm, in Indonesia. The Winners 20: 49–60. [Google Scholar] [CrossRef]

- Distanont, Anyanitha, and Orapan Khongmalai. 2020. The role of innovation in creating a competitive advantage. Kasetsart Journal of Social Sciences 41: 15–21. [Google Scholar] [CrossRef]

- Dumay, John, James Guthrie, and Jim Rooney. 2020. Being critical about intellectual capital accounting in 2020: An overview. Critical Perspectives on Accounting 70: 1–9. [Google Scholar] [CrossRef]

- Dženopoljac, Vladimir, Stevo Janoševic, and Nick Bontis. 2016. Intellectual capital and financial performance in the Serbian ICT industry. Journal of Intellectual Capital 17: 373–96. [Google Scholar] [CrossRef]

- Engel, Jerome S. 2015. Global clusters of innovation: Lessons from Silicon Valley. California Management Review 57: 36–65. [Google Scholar] [CrossRef] [Green Version]

- Fathi, Saeed, Shekoofeh Farahmand, and Mahnaz Khorasani. 2013. Impact of Intellectual Capital on Financial Performance. International Journal of Academic Research in Economics and Management Sciences 2: 6–17. [Google Scholar]

- Felício, Jose Augusto, Eduardo Couto, and Jorge Caiado. 2014. Human capital, social capital and organizational performance. Management Decision 52: 350–64. [Google Scholar] [CrossRef]

- Fisher, Greg. 2019. Online communities and firm advantages. Academy of Management Review 44: 279–98. [Google Scholar] [CrossRef]

- Frias-Aceituno, José V., Lázaro Rodríguez-Ariza, and Isabel M. Garcia-Sánchez. 2014. Explanatory factors of integrated sustainability and financial reporting. Business Strategy and the Environment 23: 56–72. [Google Scholar] [CrossRef]

- Gambardella, Alfonso, Claudio Panico, and Giovanni Valentini. 2013. Strategic incentives to human capital. Strategic Management Journal 36: 37–52. [Google Scholar] [CrossRef]

- Gogan, Luminita Maria, Dan Cristian Duran, and Anca Draghici. 2015. Structural capital-A proposed measurement model. Procedia Economics and Finance 23: 1139–46. [Google Scholar] [CrossRef] [Green Version]

- Hadiyati, Ernani. 2015. Marketing and government policy on MSMEs in Indonesian: A theoretical framework and empirical study. International Journal of Business and Management 10: 128–38. [Google Scholar] [CrossRef] [Green Version]

- Hair, Joe F., Jr., Marko Sarstedt, Lucas Hopkins, and Volker G. Kuppelwieser. 2014. Partial least squares structural equation modeling (PLS-SEM): An emerging tool in business research. European Business Review 26: 106–21. [Google Scholar] [CrossRef]

- Hamdani, Jahja, and Christina Wirawan. 2012. Open innovation implementation to sustain Indonesian SMEs. Procedia Economics and Finance 4: 223–33. [Google Scholar] [CrossRef] [Green Version]

- Han, Yuqian, and Dayuan Li. 2015. Effects of intellectual capital on innovative performance: The role of knowledge-based dynamic capability. Management Decision 53: 40–56. [Google Scholar] [CrossRef]

- Harmeling, Colleen M., Jordan W. Moffett, Mark J. Arnold, and Brad D. Carlson. 2017. Toward a theory of customer engagement marketing. Journal of the Academy of Marketing Science 45: 312–35. [Google Scholar] [CrossRef]

- Hartono, Hendry, and Erwin Halim. 2014. The impact of knowledge management and entrepreneur’s knowledge on innovation and firm performance. The Winners 15: 108–14. [Google Scholar] [CrossRef]

- Hashemnia, Shahram, Somayeh Naseri, and S. Mozdabadi. 2014. A strategic Review the Impact of Intellectual Capital Components on Organizational Performance in Sepah Bank Branches throughout Tehran Province. Journal of Educational and Management Studies 4: 46–56. [Google Scholar]

- Hashim, Maryam Jameelah, Idris Osman, and Syed Musa Alhabshi. 2015. Effect of Intellectual Capital on Organizational Performance. Procedia-Social and Behavioral Sciences 211: 207–14. [Google Scholar] [CrossRef] [Green Version]

- Hecker, Achim, and Alois Ganter. 2013. The influence of product market competition on technological and management innovation: Firm-level evidence from a large-scale survey. European Management Review 10: 17–33. [Google Scholar] [CrossRef]

- Hejazi, Rezvan, Mehrdad Ghanbari, and Mohammad Alipour. 2016. Intellectual, human and structural capital effects on firm performance as measured by Tobin’s Q. Knowledge and Process Management 23: 259–73. [Google Scholar] [CrossRef]

- Irjayanti, Maya, and Anton Mulyono Azis. 2012. Barrier factors and potential solutions for Indonesian SMEs. Procedia Economics and Finance 4: 3–12. [Google Scholar] [CrossRef] [Green Version]

- Isanzu, Janeth N. 2015. Impact of Intellectual Capital on Financial Performance of Banks in Tanzania. Journal of International Business Research and Marketing 1: 16–23. [Google Scholar] [CrossRef]

- Iwamoto, Hiroki, and Hideo Suzuki. 2019. An empirical study on the relationship of corporate financial performance and human capital concerning corporate social responsibility: Applying SEM and Bayesian SEM. Cogent Business & Management 6: 1–10. [Google Scholar] [CrossRef]

- Jalali, Alireza, Mastura Jaafar, and Thurasamy Ramayah. 2014. Entrepreneurial orientation and performance: The interaction effect of customer capital. World Journal of Entrepreneurship, Management and Sustainable Development 10: 48–68. [Google Scholar] [CrossRef]

- James, Marianne L. 2013. Sustainability and integrated reporting: Opportunities and strategies for small and midsize companies. The Entrepreneurial Executive 18: 17–27. [Google Scholar]

- Joshi, Mahesh, Daryll Cahill, Jasvinder Sidhu, and Monika Kansal. 2013. Intellectual capital and financial performance: An evaluation of the Australian financial sector. Journal of Intellectual Capital 14: 264–85. [Google Scholar] [CrossRef] [Green Version]

- Jovanovski, Bojan, Denitsa Seykova, Admira Boshnyaku, and Clemens Fischer. 2019. The impact of industry 4.0 on the competitiveness of SMEs. Industry 4.0 4: 250–55. [Google Scholar]

- Kianto, Aino, Josune Sáenz, and Nekane Aramburu. 2017. Knowledge-based human resource management practices, intellectual capital and innovation. Journal of Business Research 81: 11–20. [Google Scholar] [CrossRef]

- Kim, Kyoung Yong, Leanne Atwater, Pankaj C. Patel, and James W. Smither. 2016. Multisource feedback, human capital, and the financial performance of organizations. Journal of Applied Psychology 101: 1569–84. [Google Scholar] [CrossRef] [Green Version]

- Kim, Taegoo, Woo Gon Kim, Simon Si-Sa Park, Gyehee Lee, and Bonggu Jee. 2012. Intellectual Capital and Business Performance: What Structural Relationships Do They Have in Upper-Upscale Hotels? International Journal of Tourism Research 14: 391–408. [Google Scholar] [CrossRef]

- Kirmaci, Sevcan. 2012. Customer relationship management and customer loyalty; a survey in the sector of banking. International Journal of Business and Social Science 3: 1–10. [Google Scholar]

- Kock, Ned. 2015. WarpPLS 5.0 User Manual. Laredo: ScriptWarp Systems. [Google Scholar]

- Komnenic, Biserka, and Dragana Pokrajčić. 2012. Intellectual capital and corporate performance of MNCs in Serbia. Journal of Intellectual Capital 13: 106–19. [Google Scholar] [CrossRef]

- Kuncoro, Wuryanti, and Wa Ode Suriani. 2018. Achieving sustainable competitive advantage through product innovation and market driving. Asia Pacific Management Review 23: 186–92. [Google Scholar] [CrossRef]

- Leitner, Karl-Heinz. 2018. Intellectual capital, innovation, and performance: Empirical evidence from SMEs. In Exploiting Intellectual Property to Promote Innovation and Create Value. Singapore: World Scientific, pp. 255–82. [Google Scholar]

- Lendel, Viliam, and Michal Varmus. 2014. Evaluation of the innovative business performance. Procedia-Social and Behavioral Sciences 129: 504–11. [Google Scholar] [CrossRef] [Green Version]

- Lentjušenkova, Oksana, and Inga Lapina. 2016. The transformation of the organization’s intellectual capital: From resource to capital. Journal of Intellectual Capital 17: 610–31. [Google Scholar] [CrossRef]

- Leonidou, Leonidas C., Paul Christodoulides, Lida P. Kyrgidou, and Daydanda Palihawadana. 2017. Internal drivers and performance consequences of small firm green business strategy: The moderating role of external forces. Journal of Business Ethics 140: 585–606. [Google Scholar] [CrossRef] [Green Version]

- Lestari, Setyani Dwi, Farah Margaretha Leon, Sri Widyastuti, Nora Andira Brabo, and Aditya Halim Perdana Kusuma Putra. 2020. Antecedents and consequences of innovation and business strategy on performance and competitive advantage of SMEs. The Journal of Asian Finance, Economics and Business 7: 365–78. [Google Scholar] [CrossRef]

- Li, Yina. 2014. Environmental innovation practices and performance: Moderating effect of resource commitment. Journal of Cleaner Production 66: 450–58. [Google Scholar] [CrossRef]

- Ling, Ya-Hui. 2013. The influence of intellectual capital on organizational performance—Knowledge management as moderator. Asia Pacific Journal of Management 30: 937–64. [Google Scholar] [CrossRef]

- Maharani, Tia, and Khoirul Fuad. 2020. The effect of human capital, structural capital, customer capital, managerial ownership, and leverage toward profitability of company. Journal of Advanced Multidisciplinary Research 1: 46–62. [Google Scholar] [CrossRef]

- Malaolu, Victor, and Jonathan Emenike Ogbuabor. 2013. Training and Manpower Development, Employee Productivity and Organizational Performance in Nigeria: An Empirical Investigation. International Journal of Advances in Management and Economics 2: 163–77. [Google Scholar]

- Martin, Bruce C., Jeffrey J. McNally, and Michael J. Kay. 2013. Examining the formation of human capital in entrepreneurship: A meta-analysis of entrepreneurship education outcomes. Journal of Business Venturing 28: 211–24. [Google Scholar] [CrossRef] [Green Version]

- Matos, Florinda, Valter Martins Vairinhos, Renata Paola Dameri, and Susanne Durst. 2017. Increasing smart city competitiveness and sustainability through managing structural capital. Journal of Intellectual Capital 18: 693–707. [Google Scholar] [CrossRef]

- McGuirk, Helen, Helena Lenihan, and Mark Hart. 2015. Measuring the impact of innovative human capital on small firms’ propensity to innovate. Research Policy 44: 965–76. [Google Scholar] [CrossRef] [Green Version]

- Mehdivand, Mohsen, Mohammad Reza Zali, Merhdad Madhoshi, and Asadollah Kordnaeij. 2012. Intellectual capital and nano-businesses performance: The moderating role of entrepreneurial orientation. European Journal of Economics, Finance and Administrative Sciences 52: 147–62. [Google Scholar]

- Meihami, Bahram, and Hussein Meihami. 2014. Knowledge Management a way to gain a competitive advantage in firms (evidence of manufacturing companies). International Letters of Social and Humanistic Sciences 3: 80–91. [Google Scholar] [CrossRef] [Green Version]

- Miller, Kristel, Maura McAdam, and Rodney McAdam. 2014. The changing university business model: A stakeholder perspective. R&D Management 44: 265–87. [Google Scholar]

- Murray, Alan, Armando Papa, Benedetta Cuozzo, and Giuseppe Russo. 2016. Evaluating the innovation of the Internet of Things: Empirical evidence from the intellectual capital assessment. Business Process Management Journal 22: 341–56. [Google Scholar] [CrossRef] [Green Version]

- Musibah, Anwar Salem, and Wan Sulaiman Bin Wan Yusoff Alfattani. 2014. The mediating effect of financial performance on the relationship between Shariah supervisory board effectiveness, intellectual capital and corporate social responsibility, of Islamic banks in Gulf Cooperation Council countries. Asian Social Science 10: 139–64. [Google Scholar] [CrossRef] [Green Version]

- Ndubisi, Nelson Oly, Celine Marie Capel, and Gibson C. Ndubisi. 2015. Innovation strategy and performance of international technology services ventures: The moderating effect of structural autonomy. Journal of Service Management 26: 548–64. [Google Scholar] [CrossRef]

- Nejati, Ramin. 2016. Management of intangible assets a value enhancing strategy in knowledge economy. Research Journal of Humanities and Social Sciences 7: 54–60. [Google Scholar] [CrossRef]

- Ngari, James Mark Karimi, and James Kamau Muiruri. 2014. Effects of Financial Innovations on the Financial Performance of Commercial Banks in Kenya. International Journal of Humanities and Social Science 4: 51–57. [Google Scholar]

- Nikolaou, Ioannis. 2019. A framework to explicate the relationship between CSER and financial performance: An intellectual capital-based approach and knowledge-based view of firm. Journal of the Knowledge Economy 10: 1427–46. [Google Scholar] [CrossRef]

- Nimtrakoon, Sirinuch. 2015. The relationship between intellectual capital, firms’ market value and financial performance: Empirical evidence from the ASEAN. Journal of Intellectual Capital 16: 587–618. [Google Scholar] [CrossRef]

- Nuryani, Ni Nyoman Juli, Dewa Putu Rida Satrawan, Anak Agung Ngurah Oka Suryadinatha Gorda, and Luh Kadek Budi Martini. 2018. Influence of Human Capital, Social Capital, Economic Capital towards Financial Performance & Corporate Social Responsibility. International Journal of Social Sciences and Humanities 2: 65–76. [Google Scholar] [CrossRef] [Green Version]

- Ogunyomi, Paul, and Nealia S. Bruning. 2016. Human resource management and organizational performance of small and medium enterprises (SMEs) in Nigeria. The International Journal of Human Resource Management 27: 612–34. [Google Scholar] [CrossRef]

- Omotayo, Funmilola Olubunmi. 2015. Knowledge Management as an important tool in Organisational Management: A Review of Literature. Library Philosophy and Practice 1: 1–23. [Google Scholar]

- Osinski, Marilei, Paulo Mauricio Selig, Florinda Matos, and Darlan José Roman. 2017. Methods of evaluation of intangible assets and intellectual capital. Journal of Intellectual Capital 18: 470–85. [Google Scholar] [CrossRef]

- Pasban, Mohammad, and Sadegheh Hosseinzadeh Nojedeh. 2016. A Review of the Role of Human Capital in the Organization. Procedia-Social and Behavioral Sciences 230: 249–53. [Google Scholar] [CrossRef] [Green Version]

- Paunović, Mihailo. 2021. The impact of human capital on financial performance of entrepreneurial firms in Serbia. Management: Journal of Sustainable Business and Management Solutions in Emerging Economies 26: 29–46. [Google Scholar] [CrossRef]

- Ployhart, Robert E. 2012. Personnel selection and the competitive advantage of firms. International Review of Industrial and Organizational Psychology 27: 153–95. [Google Scholar]

- Ployhart, Robert E., Anthony J. Nyberg, Greg Reilly, and Mark A. Maltarich. 2014. Human capital is dead; long live human capital resources! Journal of Management 40: 371–98. [Google Scholar] [CrossRef] [Green Version]

- Post, Corinne, and Kris Byron. 2015. Women on boards and firm financial performance: A meta-analysis. Academy of Management Journal 58: 1546–71. [Google Scholar] [CrossRef]

- Przychodzen, Justyna, and Wojciech Przychodzen. 2015. Relationships between eco-innovation and financial performance–evidence from publicly traded companies in Poland and Hungary. Journal of Cleaner Production 90: 253–63. [Google Scholar] [CrossRef]

- Ranani, Hossein Sharifi, and Zivar Bijani. 2014. The Impact of Intellectual Capital on the Financial Performance of Listed Companies in Tehran Stock Exchange. International Journal of Academic Research in Accounting, Finance and Management Sciences 4: 119–27. [Google Scholar] [CrossRef] [Green Version]

- Ratnawati, Kusuma. 2020. The influence of financial inclusion on MSMEs’ performance through financial intermediation and access to capital. The Journal of Asian Finance, Economics, and Business 7: 205–18. [Google Scholar] [CrossRef]

- Reardon, Thomas, Ben Belton, Lenis Saweda O. Liverpool-Tasie, Liang Lu, Chandra S. R. Nuthalapati, Oyinkan Tasie, and David Zilberman. 2021. E-commerce’s fast-tracking diffusion and adaptation in developing countries. Applied Economic Perspectives and Policy 43: 1243–59. [Google Scholar] [CrossRef]

- Revelli, Christophe, and Jean-Laurent Viviani. 2015. Financial performance of socially responsible investing (SRI): What have we learned? A meta-analysis. Business Ethics: A European Review 24: 158–85. [Google Scholar] [CrossRef]

- Sardo, Filipe, Zélia Serrasqueiro, and Helena Alves. 2018. On the relationship between intellectual capital and financial performance: A panel data analysis on SME hotels. International Journal of Hospitality Management 75: 67–74. [Google Scholar] [CrossRef]

- Scafarto, Vincenzo, and Panagiotis Dimitropoulos. 2018. Human capital and financial performance in professional football: The role of governance mechanisms. Corporate Governance: The International Journal of Business in Society 18: 289–316. [Google Scholar] [CrossRef]

- Shaw, Jason D., Tae-Youn Park, and Eugene Kim. 2013. A resource-based perspective on human capital losses, HRM investments, and organizational performance. Strategic Management Journal 34: 572–89. [Google Scholar] [CrossRef]

- Silva, Vander Luiz, João Luiz Kovaleski, and Regina Negri Pagani. 2019. Technology transfer and human capital in the industrial 4.0 scenario: A theoretical study. Future Studies Research Journal: Trends and Strategies 11: 102–22. [Google Scholar] [CrossRef] [Green Version]

- Sima, Violeta, Ileana Georgiana Gheorghe, Jonel Subić, and Dumitru Nancu. 2020. Influences of the industry 4.0 revolution on the human capital development and consumer behavior: A systematic review. Sustainability 12: 4035. [Google Scholar] [CrossRef]

- Snyder, Hannah, Lars Witell, Anders Gustafsson, Paul Fombelle, and Per Kristensson. 2016. Identifying categories of service innovation: A review and synthesis of the literature. Journal of Business Research 69: 2401–8. [Google Scholar] [CrossRef] [Green Version]

- Soo, Christine, Amy Wei Tian, Stephen T. T. Teo, and John Cordery. 2017. Intellectual capital-enhancing HR, absorptive capacity, and innovation. Human Resource Management 56: 431–54. [Google Scholar] [CrossRef] [Green Version]

- Sumedrea, Silvia. 2013. Intellectual capital and firm performance: A dynamic relationship in crisis time. Procedia Economics and Finance 6: 137–44. [Google Scholar] [CrossRef] [Green Version]

- Surya, Batara, Firman Menne, Hernita Sabhan, Seri Suriani, Herminawaty Abubakar, and Muhammad Idris. 2021. Economic growth, increasing productivity of SMEs, and open innovation. Journal of Open Innovation: Technology, Market, and Complexity 7: 20. [Google Scholar] [CrossRef]

- Suseno, Yuliani, and Ashly H. Pinnington. 2017. The war for talent: Human capital challenges for professional service firms. Asia Pacific Business Review 23: 205–29. [Google Scholar] [CrossRef]

- Sydler, Renato, Stefan Haefliger, and Robert Pruksa. 2014. Measuring intellectual capital with financial figures: Can we predict firm profitability? European Management Journal 32: 244–59. [Google Scholar] [CrossRef]

- Teece, David J. 2018. Business models and dynamic capabilities. Long Range Planning 51: 40–49. [Google Scholar] [CrossRef]

- Teeratansirikool, Luliya, Sununta Siengthai, Yuosre Badir, and Chotchai Charoenngam. 2013. Competitive strategies and firm performance: The mediating role of performance measurement. International Journal of Productivity and Performance Management 62: 168–84. [Google Scholar] [CrossRef]

- Tehseen, Shehnaz, and Sulaiman Sajilan. 2016. Network competence based on resource-based view and resource dependence theory. International Journal of Trade and Global Markets 9: 60–82. [Google Scholar] [CrossRef]

- Thiagarajan, Anthony, and Utpal Baul. 2014. Holistic Intellectual Capital Conceptual Offering for Empirical Research and Business Application. International Journal of Management 3: 31–50. [Google Scholar]

- Tzabbar, Daniel, and Jaclyn Margolis. 2017. Beyond the startup stage: The founding team’s human capital, new venture’s stage of life, founder–CEO duality, and breakthrough innovation. Organization Science 28: 857–72. [Google Scholar] [CrossRef]

- Ungerman, Otakar, Jaroslava Dedkova, and Katerina Gurinova. 2018. The impact of marketing innovation on the competitiveness of enterprises in the context of industry 4.0. Journal of Competitiveness 10: 132–48. [Google Scholar] [CrossRef]

- Wang, Zhining, and Nianxin Wang. 2012. Knowledge sharing, innovation and firm performance. Expert Systems with Applications 39: 8899–908. [Google Scholar] [CrossRef]

- Wang, Zhining, Nianxin Wang, and Huigang Liang. 2014. Knowledge sharing, intellectual capital and firm performance. Management Decision 52: 230–58. [Google Scholar] [CrossRef] [Green Version]

- Wang, Zhining, Nianxin Wang, Jinwei Cao, and Xinfeng Ye. 2016. The impact of intellectual capital—Knowledge management strategy fit on firm performance. Management Decision 54: 1861–85. [Google Scholar] [CrossRef]

- Wang, Zhining, Shaohan Cai, Huigang Liang, Nianxin Wang, and Erwei Xiang. 2018. Intellectual capital and firm performance: The mediating role of innovation speed and quality. The International Journal of Human Resource Management 32: 1222–50. [Google Scholar] [CrossRef]

- Wataya, Eiko, and Rajib Shaw. 2019. Measuring the value and the role of soft assets in smart city development. Cities 94: 106–15. [Google Scholar] [CrossRef]

- Wijaya, Putu Yudy, and Ni Nyoman Reni Suasih. 2020. The effect of knowledge management on competitive advantage and business performance: A study of silver craft SMEs. Entrepreneurial Business and Economics Review 8: 105–21. [Google Scholar] [CrossRef]

- Wright, Patrick M., Russell Coff, and Thomas P. Moliterno. 2014. Strategic human capital: Crossing the great divide. Journal of Management 40: 353–70. [Google Scholar] [CrossRef] [Green Version]

- Wuttke, David A., Constantin Blome, and Michael Henke. 2013. Focusing the financial flow of supply chains: An empirical investigation of financial supply chain management. International Journal of Production Economics 145: 773–89. [Google Scholar] [CrossRef]

- Yong, Jing Yi, M.-Y. Yusliza, Charbel Jose Chiappetta Jabbour, and Noor Hazlina Ahmad. 2020. Exploratory cases on the interplay between green human resource management and advanced green manufacturing in light of the Ability-Motivation-Opportunity theory. Journal of Management Development 39: 31–49. [Google Scholar] [CrossRef]

- Yusuf, Ismaila. 2013. The Relationship between Human Capital Efficiency and Financial Performance: An Empirical Investigation of Quoted Nigerian Banks. Research Journal of Finance and Accounting 4: 148–54. [Google Scholar]

- Zambon, Stefano. 2017. Intangibles and intellectual capital: An overview of the reporting issues and some measurement models. In The Economic Importance of Intangible Assets. London: Routledge, Taylor & Francis Group, pp. 153–83. [Google Scholar]

- Zhou, Yu, Ying Hong, and Jun Liu. 2013. Internal commitment or external collaboration? The impact of human resource management systems on firm innovation and performance. Human Resource Management 52: 263–88. [Google Scholar] [CrossRef]

{kind=link}

| Sample Criteria | Number of Observations |

|---|---|

| Total questionnaires distributed | 401 |

| Complete questionnaires that were not returned | (9) |

| Total returned questionnaires | 392 |

| Complete questionnaires that cannot be processed | 0 |

| Total questionnaires that can be processed | 392 |

| Variable | Definition | Data Source |

|---|---|---|

| Improved Financial Performance | A company’s financial condition in a certain period regarding aspects of fundraising and its distribution is presented in the financial statements (Frias-Aceituno et al. 2014) | Questionnaire |

| Human Capital | Value is added in the form of knowledge, expertise, abilities and skills possessed by humans and then makes humans capital or assets of an organization to achieve strategic goals (Pasban and Nojedeh 2016) | Questionnaire |

| Structural Capital | Supporting infrastructure, organizational databases, and organizational design structures that enable human capital to carry out its functions for better performance (Sumedrea 2013) | Questionnaire |

| Consumer Capital | The knowledge possessed in aspects of marketing channels and relationships that occur with outside parties such as customers, suppliers, communities and governments that develop in the organization through operational activities (Kim et al. 2012). | Questionnaire |

| Speed of Innovation | The pace of progress manifests a bold appearance in innovating and commercializing new products, which means the company can accelerate its operational activities in developing new products (Engel 2015). | Questionnaire |

| Variable | Indicator | X1 | X2 | X3 | Z | Y | p-Value | Description |

|---|---|---|---|---|---|---|---|---|

| Human Capital (X1) | X1.1 | 0.631 * | > | <0.001 | Valid | |||

| X1.2 | 0.663 * | <0.001 | Valid | |||||

| X1.3 | 0.677 * | <0.001 | Valid | |||||

| X1.4 | 0.709 * | <0.001 | Valid | |||||

| X1.5 | 0.741 * | <0.001 | Valid | |||||

| X1.6 | <0.001 | Valid | ||||||

| Structural Capital (X2) | X2.1 | 0.973 * | <0.001 | Valid | ||||

| X2.2 | 0.992 * | <0.001 | Valid | |||||

| X2.3 | 0.978 * | <0.001 | Valid | |||||

| X2.4 | 0.981 * | <0.001 | Valid | |||||

| Consumer Capital (X3) | X3.1 | 0.638 * | <0.001 | Valid | ||||

| X3.2 | 0.768 * | <0.001 | Valid | |||||

| X3.3 | 0.745 * | <0.001 | Valid | |||||

| X3.4 | 0.718 * | <0.001 | Valid | |||||

| X3.5 | 0.823 * | <0.001 | Valid | |||||

| Speed of Innovation (Z) | >Z1 | >0.832 * | ><0.001 | >Valid | ||||

| Z2 | 0.776 * | <0.001 | Valid | |||||

| Z3 | 0.807 * | <0.001 | Valid | |||||

| Z4 | 0.797 * | <0.001 | Valid | |||||

| Improvement of financial performance (Y) | Y1 | 0.646 * | <0.001 | Valid | ||||

| Y2 | 0.786 * | <0.001 | Valid | |||||

| Y3 | 0.844 * | <0.001 | Valid | |||||

| Y4 | 0.913 * | <0.001 | Valid | |||||

| Z × X1 | Z × X2 | Z × X3 | p-Value | Description | |||

|---|---|---|---|---|---|---|---|

| Z1 × X1.1 | 0.596 | Z1 × X2.1 | 0.977 | Z1 × X3.1 | 0.867 | <0.001 | Valid |

| Z1 × X1.2 | 0.876 | Z1 × X2.2 | 0.997 | Z1 × X3.2 | 0.852 | <0.001 | Valid |

| Z1 × X1.3 | 0.831 | Z1 × X2.3 | 0.977 | Z1 × X3.3 | 0.688 | <0.001 | Valid |

| Z1 × X1.4 | 0.829 | Z1 × X2.4 | 0.985 | Z1 × X3.4 | 0.716 | <0.001 | Valid |

| Z1 × X1.5 | 0.934 | Z2 × X2.1 | 0.978 | Z1 × X3.5 | 0.852 | <0.001 | Valid |

| Z1 × X1.6 | 0.792 | Z2 × X2.2 | 0.988 | Z2 × X3.1 | 0.838 | <0.001 | Valid |

| Z2 × X1.1 | 0.892 | Z2 × X2.3 | 0.972 | Z2 × X3.2 | 0.932 | <0.001 | Valid |

| Z2 × X1.2 | 0.704 | Z2 × X2.4 | 0.957 | Z2 × X3.3 | 0.760 | <0.001 | Valid |

| Z2 × X1.3 | 0.866 | Z3 × X2.1 | 0.984 | Z2 × X3.4 | 0.721 | <0.001 | Valid |

| Z2 × X1.4 | 0.823 | Z3 × X2.2 | 0.986 | Z2 × X3.5 | 0.827 | <0.001 | Valid |

| Z2 × X1.5 | 0.808 | Z3 × X2.3 | 0.991 | Z3 × X3.1 | 0.798 | <0.001 | Valid |

| Z2 × X1.6 | 0.780 | Z3 × X2.4 | 0.990 | Z3 × X3.2 | 0.943 | <0.001 | Valid |

| Z3 × X1.1 | 0.861 | Z4 × X2.1 | 0.962 | Z3 × X3.3 | 0.794 | <0.001 | Valid |

| Z3 × X1.2 | 0.932 | Z4 × X2.2 | 0.992 | Z3 × X3.4 | 0.728 | <0.001 | Valid |

| Z3 × X1.3 | 0.744 | Z4 × X2.3 | 0.953 | Z3 × X3.5 | 0.937 | <0.001 | Valid |

| Z3 × X1.4 | 0.897 | Z4 × X2.4 | 0.964 | Z4 × X3.1 | 0.868 | <0.001 | Valid |

| Z3 × X1.5 | 0.852 | Z4 × X3.2 | 0.837 | <0.001 | Valid | ||

| Z3 × X1.6 | 0.791 | Z4 × X3.3 | 0.730 | <0.001 | Valid | ||

| Z4 × X1.1 | 0.850 | Z4 × X3.4 | 0.779 | <0.001 | Valid | ||

| Z4 × X1.2 | 0.800 | Z4 × X3.5 | 0.953 | <0.001 | Valid | ||

| Z4 × X1.3 | 0.851 | <0.001 | Valid | ||||

| Z4 × X1.4 | 0.795 | <0.001 | Valid | ||||

| Z4 × X1.5 | 0.848 | <0.001 | Valid | ||||

| Z4 × X1.6 | 0.844 | <0.001 | |||||

| Correlations among l. vs. with sq. rts. of AVEs | ||||||||

|---|---|---|---|---|---|---|---|---|

| X1 | X2 | X3 | Z | Y | Z × X1 | Z × X2 | Z × X3 | |

| Human Capital (X1) | 0.634 * | |||||||

| Structural Capital (X2) | 0.902 * | |||||||

| Consumer Capital (X3) | 0.603 * | |||||||

| Innovation Speed (Z) | 0.739 * | |||||||

| Improvement of financial performance (Y) | 0.613 * | |||||||

| Z × X1 | 0.588 * | |||||||

| Z × X2 | 0.708 * | |||||||

| Z × X3 | 0.520 * | |||||||

| X1 | X2 | X3 | Z | Y | Z × X1 | Z × X2 | Z × X3 | |

|---|---|---|---|---|---|---|---|---|

| R-squared coefficients | 0.393 | |||||||

| Adjusted R-squared coefficients | 0.311 | |||||||

| Composite reliability coefficients | 0.798 | 0.946 | 0.732 | 0.828 | 0.693 | 0.876 | 0.941 | 0.806 |

| Cronbach’s alpha coefficients | 0.696 | 0.923 | 0.547 | 0.722 | 0.513 | 0.854 | 0.933 | 0.749 |

| Average variances extracted | 0.401 | 0.813 | 0.364 | 0.547 | 0.363 | 0.238 | 0.501 | 0.177 |

| Full collinearity VIFs | 2.893 | 1.035 | 1.732 | 2.181 | 1.448 | 1.506 | 1.013 | 1.264 |

| Q-squared coefficients | 0.335 |

| No. | Model Fit and Quality Indices | Fit Criteria | Indeks | Description |

|---|---|---|---|---|

| 1 | Average path coefficient (APC) | p < 0.05 | 0.169 | Fulfilled |

| 2 | Average R-squared (ARS) | p < 0.05 | 0.311 | Fulfilled |

| 3 | Average adjusted R-squared (AARS) | p < 0.05 | 0.293 | Fulfilled |

| 4 | Average block VIF (AVIF) | acceptable if ≤5, ideally ≤3.3 | 1.341 | Fulfilled |

| 5 | Average full collinearity VIF (AFVIF) | acceptable if ≤5, ideally ≤3.3 | 1.634 | Fulfilled |

| 6 | Tenenhaus GoF (GoF) | small ≥0.1, medium ≥0.25, large ≥0.36 | 0.364 | Fulfilled, Categori Large |

| 7 | Sympson’s paradox ratio (SPR) | acceptable if ≥0.7, ideally = 1 | 0.767 | Fulfilled |

| 8 | R-squared contribution ratio (RSCR) | acceptable if ≥0.9, ideally = 1 | 0.951 | Fulfilled |

| 9 | Statistical suppression ratio (SSR) | acceptable if ≥0.7 | 0.833 | Fulfilled |

| 10 | Nonlinear bivariate causality direction ratio (NLBCDR) | acceptable if ≥0.7 | 0.833 | Fulfilled |

| Variable | Criteria | Description | |

|---|---|---|---|

| Path Coefficients | p Values | ||

| Human Capital (X1) | 0.205 | <0.001 *** | Highly Significant |

| Structural Capital (X2) | 0.157 | 0.007 *** | Highly Significant |

| Consumer Capital (X3) | 0.362 | <0.001 *** | Highly Significant |

| Innovation Speed× Human Capital (Z × X1) | 0.054 | 0.202 | Not significant |

| Innovation Speed× Structural Capital (Z × X2) | 0.119 | 0.031 ** | Significant |

| Innovation Speed× Consumer Capital (Z × X3) | −0.113 | 0.038 ** | Significant |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Purnamawati, I.G.A.; Jie, F.; Hong, P.C.; Yuniarta, G.A. Analysis of Maximization Strategy Intangible Assets through the Speed of Innovation on Knowledge-Driven Business Performance Improvement. Economies 2022, 10, 149. https://doi.org/10.3390/economies10060149

Purnamawati IGA, Jie F, Hong PC, Yuniarta GA. Analysis of Maximization Strategy Intangible Assets through the Speed of Innovation on Knowledge-Driven Business Performance Improvement. Economies. 2022; 10(6):149. https://doi.org/10.3390/economies10060149

Chicago/Turabian StylePurnamawati, I Gusti Ayu, Ferry Jie, Puah Chin Hong, and Gede Adi Yuniarta. 2022. "Analysis of Maximization Strategy Intangible Assets through the Speed of Innovation on Knowledge-Driven Business Performance Improvement" Economies 10, no. 6: 149. https://doi.org/10.3390/economies10060149