1. Introduction

The flexibility of generally accepted accounting principles makes it easier for managers to have some discretion in estimating reported earnings that may not accurately reflect the underlying economic conditions of the company (

Prior et al. 2008). This opportunistic behavior of using managerial discretion is known as Earnings Management (EM) (

Habbash and Alghamdi 2017) and is defined as the process of taking deliberate steps within the constraints of generally accepted accounting principles to achieve the desired level of reported earnings (

Davidson et al. 1987). EM is thus broadly interpreted as a latent and unwanted threat (

Mohsen Al-Absy et al. 2018), which could result in devastating long-term effects if the relevant suspicions, highlighted and inflamed by various sources and events, become public (

Dechow and Skinner 2000). It is therefore considered unethical and irresponsible behavior (

Scholtens and Kang 2013).

Researchers have attempted to analyze the relationship between corporate EM practices and commitment to Corporate Social Responsibility (CSR) (

Bozzolan et al. 2015;

Choi et al. 2018;

Maglio et al. 2020). Thus, socially committed companies are presumed to have less manipulation of profits as they are intrinsically more committed to creating value for their shareholders and transparent disclosure policies (

Mercedes Palacios-Manzano et al. 2019). However, although the importance and influence of EM practices on CSR is an area of significant value today, it requires further research (

Kim et al. 2012).

Thus, an essential component of any research is to relate it to existing knowledge. In this situation, the literature review takes on great relevance, as it can promote knowledge, facilitate theory development, provide an overview of existing research areas and synthesize research findings to uncover areas in need of further research (

Snyder 2019). This study aims to analyze current research trends on the influence of CSR on EM. To this end, a bibliometric study was carried out, starting with a group of more than 300 published articles selected from scientific journals in the Web of Science database, published in the period between 2002 and 2020, and filtering this group to find specialized works on the proposed topic. In recent years, a large number of articles have been published on the relationship between CSR and EM. These studies have identified a number of current issues that have been analyzed in the research published to date. Despite its current scope, the literature published to date has not assessed the performance of the scientific activity of this relationship. Thus, the main attraction of this work lies in the lack of similar previous studies on this important topic and in the fact that the sample used to conduct the research consists of articles published anywhere in the world. In short, we aim to answer the following research questions.

- What are the volume, growth trajectory and geographic distribution of papers on this topic?

- Which scholars have emerged as influential in the literature on this topic?

- How can researchers expand their knowledge in this stream of research?

- What gaps can be found in the literature on the topic addressed that could give rise to future lines of research?

Finally, this paper makes important contributions to the existing literature, broadening and strengthening knowledge about the impact of CSR on earnings management. Firstly, this article presents an analysis of various bibliometric indicators, including the number of publications, total citations, citations per article, top journals, most relevant universities and most influential countries on the subject, which will be of great relevance to researchers who want to broaden their knowledge about the origin, evolution and current state of the relationship studied. Secondly, this study uses an inductive approach through bibliometric analysis of scientific production to observe the evolution of the field of empirical knowledge analyzed in this research. Specifically, we used the bibliometric tool VOSviewer, which allowed us to analyze co-occurrence of terms and co-authorship networks and map density based on researcher networks. These analyses have provided us with an insight into current research trends on the topic under study.

Consequently, this study contributes to the theoretical development of research on the impact of CSR on EM because it helps researchers identify the main research topics, applicable techniques and the possibility of investigating underutilized problems. In short, the main contribution of this article is the identification of a number of gaps in the literature. The results demonstrate how certain aspects such as gender diversity on boards of directors, the family or non-family character of companies, the voluntary issuance of CSR reports or the presence of an audit committee in companies and the influence of these on the relationship between CSR and EM have not been sufficiently addressed, thus opening up important possibilities for future research.

The rest of the article is organized as follows: We review the conceptual framework of the relationship between EM and CSR in

Section 2. In

Section 3, we describe the research methodology. In

Section 4, we conduct a bibliometric review and a network analysis. Finally, in

Section 5, we report the empirical findings and present the conclusions drawn from our analyses.

2. Conceptual Framework

Earnings management is one of the most challenging, debated and controversial topics in finance and financial management. This method is performed by the company’s management in the process of preparing the financial statements and can affect the level of earnings shown (

Mahdaleta et al. 2016). Thus, EM occurs when managers use their financial reporting decisions and prepare transactions to alter financial statements to either create a false picture for stakeholders about the company’s economic performance or to influence contractual results that depend on accounting figures reported (

Muda et al. 2018). Moreover, it has been demonstrated that the existence of CSR-contingent executive compensation contracts can serve, if the contingent remuneration is high, to persuade managers to manipulate performance (

Li and Thibodeau 2019).

In this context, earnings management is seen as the use of accounting techniques to produce financial statements that present an overly positive view of corporate business activities and financial position (

Ye 2007) and aims to achieve stable and predictable financial results (

Healy 1985). Additionally, EM helps to achieve specific targets involving the manipulation of accruals through the discretionary choices of accrual accounting (

McNichols and Wilson 1988).

CSR activity by companies is based on the agency theory. This theory claims that it is necessary to limit the opportunistic behavior of the administration (

Jensen and Meckling 1976;

Mahrani and Soewarno 2018). In addition, this theory is complemented by the theory of legitimacy and stakeholder theory. The first argues that a company’s survival depends on the support of stakeholders (

Gray et al. 1995), as they will be affected and influenced by the company’s activities (

Freeman 1984;

Mahrani and Soewarno 2018). Furthermore, the theory of legitimacy adds that the company must operate according to the prevailing norms of the society or environment in which it is situated. The company seeks to ensure that its operational activities are accepted as “legitimate” (

Mahrani and Soewarno 2018).

From a managerial point of view, this research can be used to raise managers’ awareness of the inappropriateness of engaging in practices aimed at manipulating the outcome, which has been demonstrated by the worldwide interest in analyzing this malpractice. From a company owner’s point of view, this research can serve to enhance the implementation of CSR practices as mechanisms to reduce managers’ opportunistic behavior in relation to EM. Finally, it could be helpful for auditors as well. Auditors have to evaluate the quality of the EM and if the audited company has a developed CSR system, it could be considered by auditors as a positive factor to reduce the irregular audit risk.

Research on EM is an important constant concern within CSR. In this context, EM is perceived as an act that is irresponsible according to CSR principles (

Choi et al. 2018), as CSR-oriented companies are more likely to act responsibly when reporting their financial statements (

Wang and Choi 2013). This is because business organizations with strong social responsibility commitments are less likely to manage their profits, and do not hide unfavorable profit-making, and therefore do not engage in EM. In this context, EM is broadly interpreted as a latent threat and an unwanted practice, which could potentially result in devastating long-term effects if relevant suspicions, as signaled by various sources and events, are made public (

Dechow and Skinner 2000).

Thus, it is widely accepted that EM and CSR are linked through two perspectives. The first of these corresponds to the long-term perspective hypothesis, which suggests that socially responsible companies generally focus on fostering future stakeholder relationships (

Mercedes Palacios-Manzano et al. 2019). Hence, business organizations committed to CSR tend to encourage long-term relationships with stakeholders rather than maximizing their profits in the short term (

Choi et al. 2018). This results in companies’ commitment to CSR being largely driven by the long-term perspective (

Ehsan et al. 2021). Thus, companies use CSR practices to manage or manipulate the information needs of various powerful stakeholder groups in society (such as employees, shareholders, non-governmental agencies and the general public) in order to gain their support, which is necessary for the survival of the company and its stakeholders (

Gray et al. 1995). As a result, business organizations committed to CSR tend to encourage long-term relationships with stakeholders rather than maximizing short-term profits (

Wang and Choi 2013).

On the other hand, the second perspective is related to the managerial opportunism hypothesis, which suggests that managers who manage for profit can strategically use CSR information to disguise their opportunistic behavior (

Mercedes Palacios-Manzano et al. 2019). It is important to note that economic cycles and financial performance play important roles in the relation between CSR and EM (

Gonçalves et al. 2021). Thus, previous research has demonstrated the efforts made by managers to demonstrate better measures of profitability through EM practices in order to secure their personal financial incentives (

Walker 2013). As a result, managers pursue their own self-interest by reporting earnings in financial statements that do not show an accurate picture of the true economic situation of the company (

Scholtens and Kang 2013) because some of them are likely to take discretionary actions with respect to reported revenues in order to maximize their own profit (

Sun et al. 2010). Therefore, EM activities are conceptualized as opportunistic practices through which managers inflate earnings to meet budget targets in order to increase their own compensation (

Grougiou et al. 2014). In this way, managers can use CSR to reduce the likelihood of being scrutinized by unsatisfied stakeholders in the first place (

Prior et al. 2008) and maximize their own private benefits (

Choi et al. 2018). A similar conclusion was achieved by Lui et al. (

Liu et al. 2017), who determined that companies with a deep CSR system show a more aggressive EM behavior. However, there is controversy about whether only the mandatory CSR impacts on the EM or the voluntary CSR affects EM (

Gong and Ho 2021).

In conclusion, EM is perceived as irresponsible according to CSR principles, as CSR-oriented companies are more likely to act responsibly because they report on their financial statements (

Wang and Choi 2013). Therefore, they are less likely to manage their profits, and they do not hide unfavorable profit-taking, so they do not engage in EM (

Mercedes Palacios-Manzano et al. 2019). Additionally, CSR can be used as a mechanism to distort earnings information to become a tool to achieve managers’ self-interested objectives (

Prior et al. 2008).

4. Bibliometric Review and Network Analysis

In order to analyze the investigation carried out on CSR and EM, this study was inspired by the methodology used previously on bibliometrics (

Llanos-Herrera and Merigo 2019;

Shah et al. 2019;

Vošner et al. 2016). This methodology has been used to perform bibliometric reviews on the economy (

Camón Luis and Celma 2020;

Kraus et al. 2020), environment (

Milfont et al. 2019;

Nita 2019) or specific journals (

Byington et al. 2019;

Tang et al. 2018), for instance. Therefore, a systematic quantitative and qualitative evaluation of the literature of 329 WoS publications related to the analysis of the influence of CSR on EM was carried out. In this research, in line with León- Gómez et al. (

León-gómez et al. 2021), we determine the interconnections between articles by analyzing the frequency with which other articles cite another given article related to a specific study domain. Later, VOSviewer was used to import the file created in Web of Science with information about authors, articles, citations, journals, research papers, institutions and countries. Furthermore, a mapping of citations related to CSR and EM was carried out. These results allowed us to explore the research streams in this topic. Moreover, VOSviewer completed network analysis and graphical investigation of the selected sample. In this stage, we produced a map based on the co-occurrence of keywords, map density based on network data connected by co-authorship items and a map of co-citations.

4.1. Author Influence and Affiliation Statistics

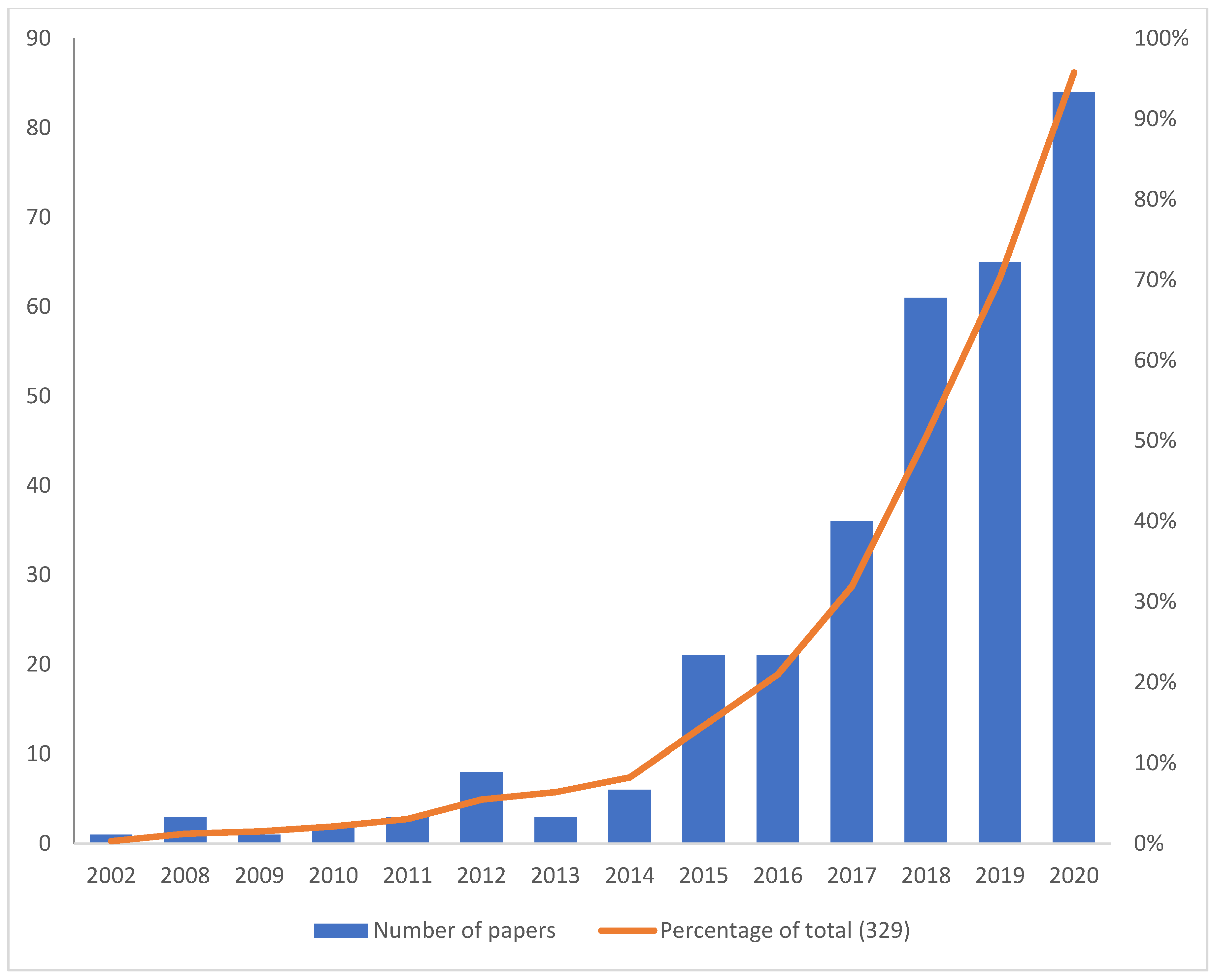

From 2002 to February 2021, 786 authors made fundamental contributions to the development of the investigation of the relationship between CSR and EM. The results show that the two authors with the most contributions have each published a total of 14 articles, and the third has published seven articles.

Although all the authors have research experience in business and economics, there are two major subdivisions in terms of themes: Social sciences and environmental sciences and ecology. Overall, the breadth of methodologies and disciplines, even among the most prolific scholars, exemplifies the interdisciplinary nature of research on the influence of sustainable tourism development on economic growth.

As far as the geographical contribution is concerned, the authors of the papers represent 58 countries.

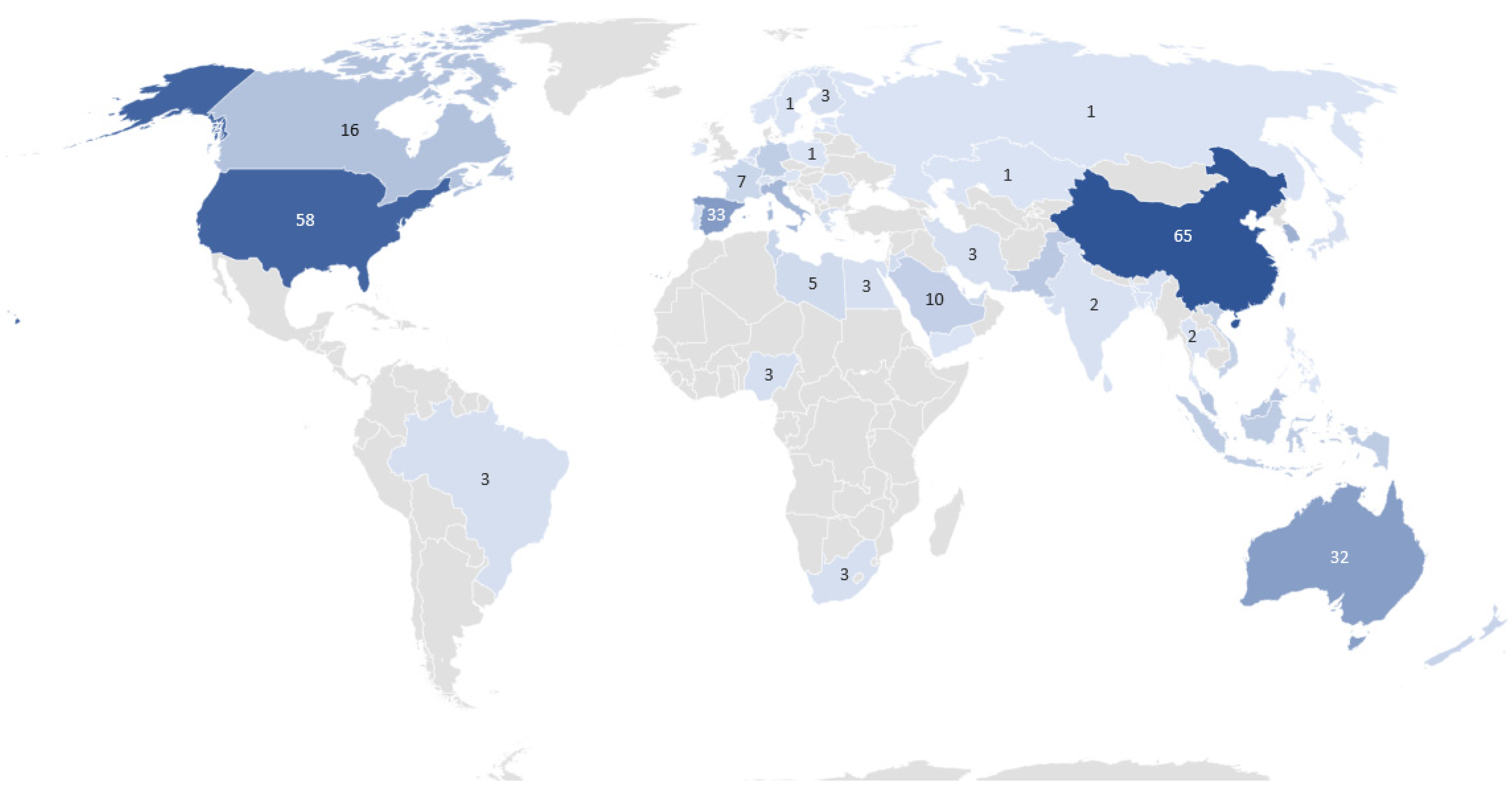

Figure 2 shows the geographic locations of the organizations which have published articles in the field of this study. The intensity of the color is proportional to the degree of participation of each organization. Greater density of contributing organizations can be found in China with 65 articles (19.75%), followed by the USA (17.62%), United Kingdom (12.46%), Spain (10.03%), Australia (9.72%), South Korea (7.2%), Italy (6.38%) and Taiwan (6.38%). Note the case of Spain and the UK, because they are smaller countries than the others. Overall, the geographical dispersion indicates that the effect of CSR on EM has attracted organizations and research centers from all over the world.

A greater breakdown of these contributions can be carried out for different geographical regions.

Table 5 shows the contribution of each region to the literature on the influence of CSR on EM (note that articles with authors from different organizations may have been assigned to multiple regions). Meridian Asia is the most productive region, followed by the European Union and North America. Developing regions do not publish much in this field.

Next, let us examine the productivity of the organizations. The top-performing organizations (based on the number of papers contributed), their geographical location, the number of papers and the percentage of contribution are shown in

Table 6. It is observed that Salamanca University in Spain is the most prolific organization in the field studied, followed by the Chinese University of Hong Kong, the University of Korea and Santa Carla University.

Table 7 shows the list of the 10 most influential authors’ organizations. It is observed that the University of Salamanca, the University of Islamabad, the University of Pisa, De Montfort University and Monash University are represented by the most prolific authors. Therefore, it may only take the work of one researcher for an organization to be classified as high performing.

4.2. Keywords Statistics and Analysis

The most popular keywords used in the papers are summarized in

Table 8. This is from a pool of 1292 keywords drawn from 329 papers, once the terms used to compose the sample of this research were excluded from this search. It is observed how the most popular keywords are related to companies’ performance or governance through a technique similar to that used by Ortiz-Martínez and Marín-Hernández (

Ortiz-Martínez and Marín-Hernández 2021).

The keywords in the article refer to and reflect the research topic in question (

Juhmani 2017). This part involved a graphical investigation of the most used keywords to obtain information on the most studied topics and concepts (

Gümüş et al. 2020). The most used keywords have been linked to describe the conceptual framework of the topic under investigation (

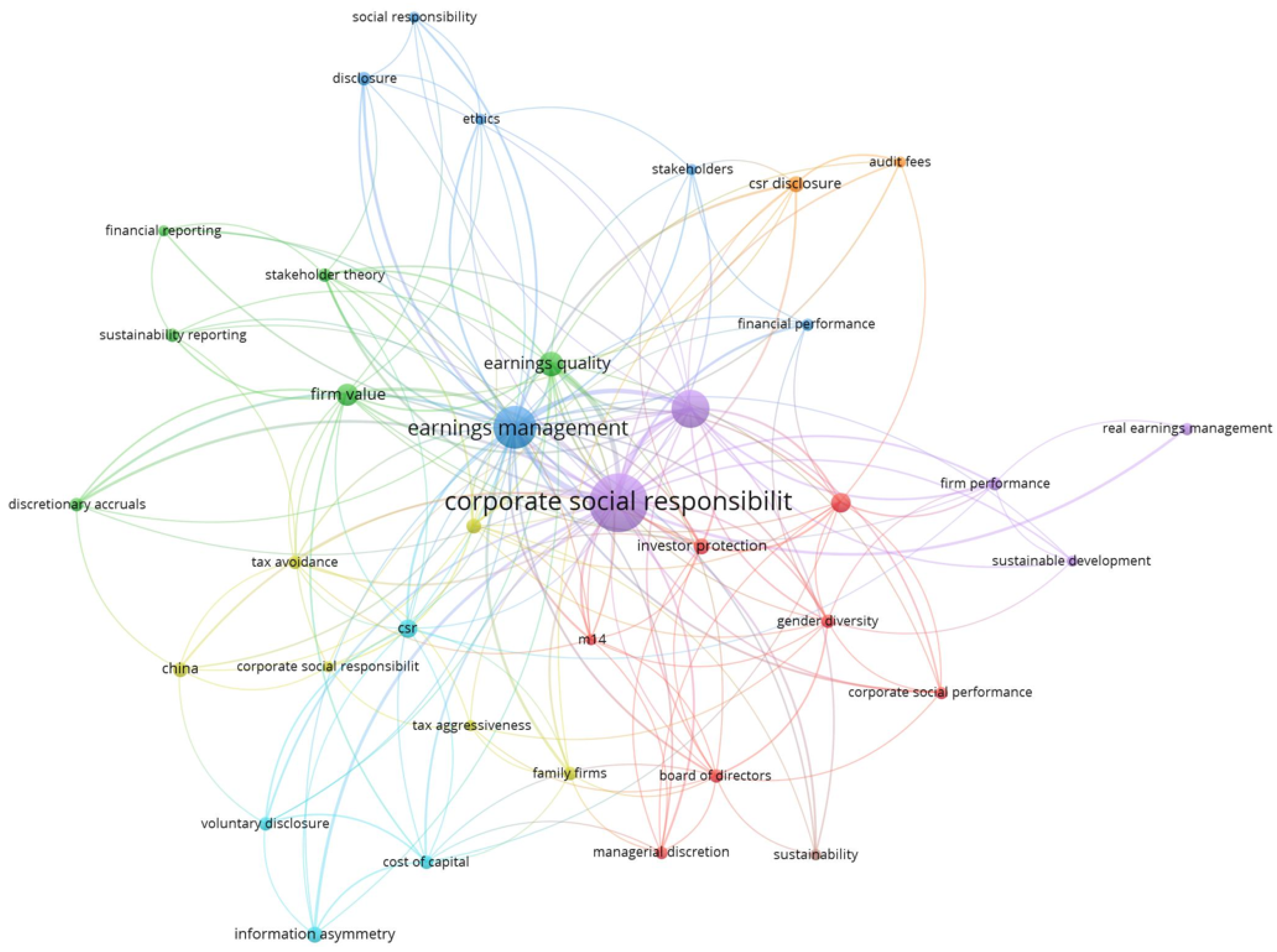

Mas-Tur et al. 2020). For this purpose, a co-occurrence map of author keywords in the analysis of the influence of CSR on EM (minimum threshold of five keyword occurrences) has been created. As a result of this, 37 keywords were obtained.

Figure 3 allows the identification and visualization of eight thematic clusters based on the relatedness between the published papers (details in

Table 9), which help to identify the streams in the field. The nodes represent the keywords, and the links represent how close a keyword is to others. Therefore, the figure displays how each keyword is connected to the other ones and the size of the circles is proportional to the number of papers published with specific keywords. The grouping of a keyword into a cluster indicates that these keywords are more likely to be in combination with other keywords grouped into this cluster than with keywords grouped into other clusters (

Kovacs et al. 2015). The keywords “corporate social responsibility” and “earnings management” are the largest nodes.

This is evidence that the relationship mentioned above has been analyzed from a broad perspective. The red cluster is the largest and includes several keywords related to the characteristics of the board of directors, such as “gender diversity” and “board of directors”. The blue cluster includes several keywords related to disclosure of information, such as “financial reporting” and “sustainability reporting”. The rest of the clusters are smaller and present a variety of concepts. The size of the circles indicates how there are no predominant concepts in the published papers, with the exception of “corporate social responsibility” and “earnings management” which are the source concepts of this research.

Based on the size of the circles, we can detect certain topics that can be the subject of further scientific production, thus becoming interesting gaps in the current literature on CSR and EM. These are the following topics: Voluntary CSR disclosure and EM, real earnings management, firm performance, non-family firm and gender diversity.

4.3. Citation Analysis

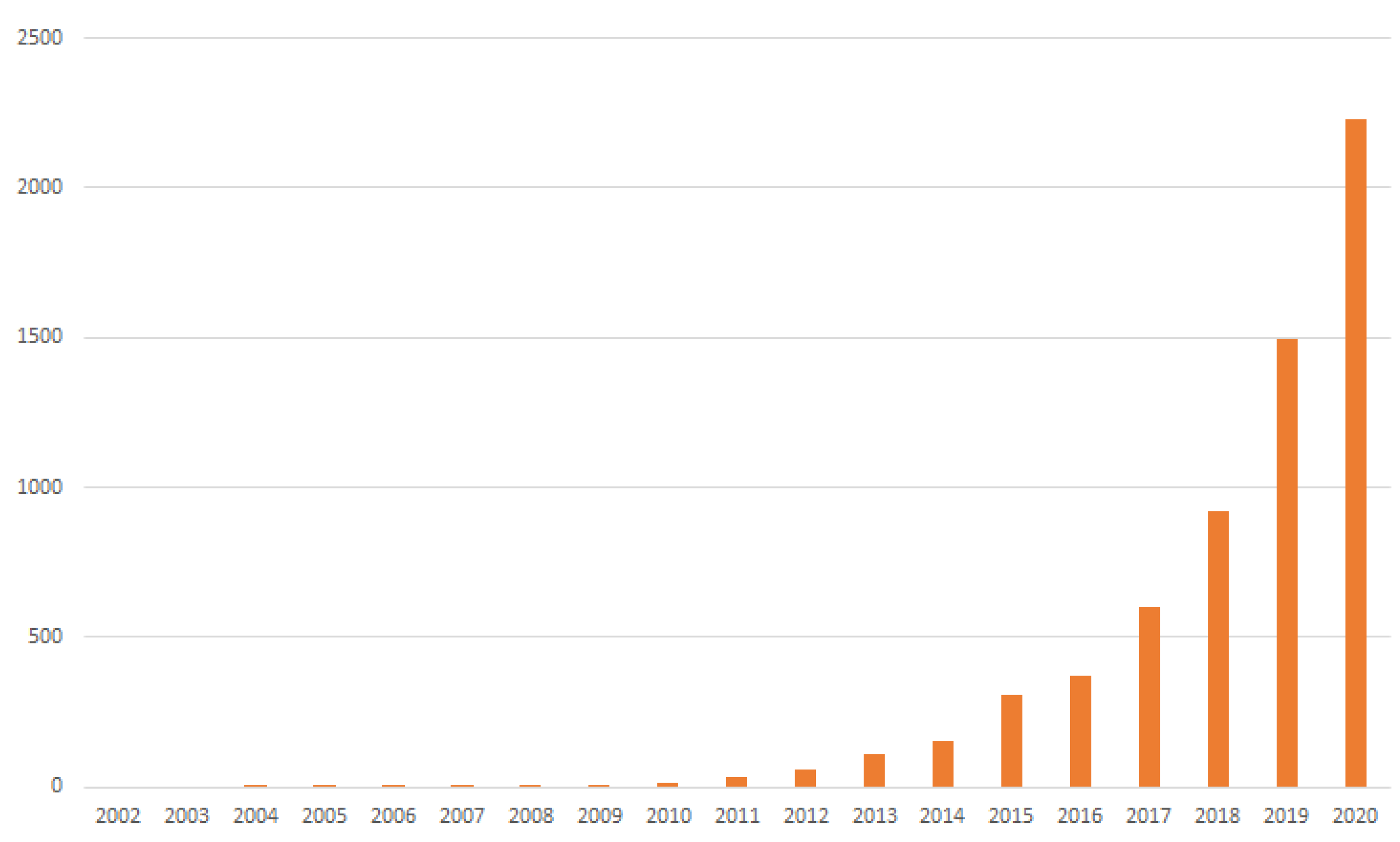

From 2004 to February 2021, the total number of citations was 6506.

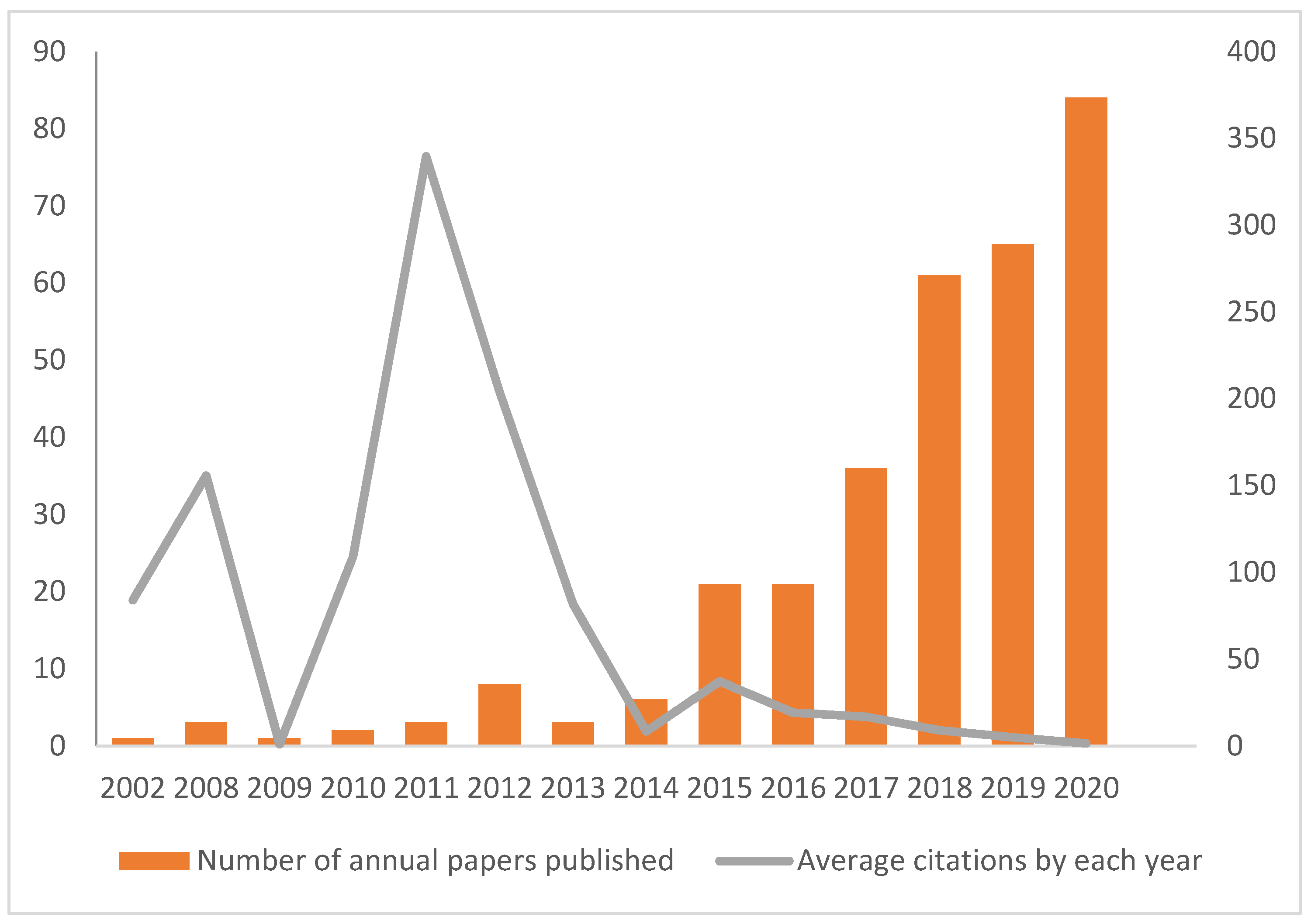

Figure 4 shows how the citations received each year increase over time, demonstrating the growing interest of researchers in this area. As is seen, the number of citations has grown very significantly, especially since 2015.

Figure 5 shows that the articles published between 2010 and 2013 are the most cited articles. Currently, 2011 is the year when the papers published reached the highest impact, with more than 300 citations. Likewise, the average numbers of citations for each article are fewer in recent years because these articles are new in the literature and have not had time to obtain a significant citation rate. Obviously, these data are dynamic and once these articles reach maturity, they will receive more citations.

Another interesting issue concerning citations is to analyze the most cited articles published in the journals. The 10 main articles with the highest number of citations are shown in

Table 10. Dhaliwai, Li, Tsang and Yang have the most cited article with 918 since 2011. The results also show that these authors also have the third most cited article, with 496 citations. However, it is important to note that both the first- and third-ranked articles do not aim to analyze the effects of CSR on EM. In both studies, EM is only a control variable, being neither the dependent variable nor the variable of interest. It can also be seen that another group of authors, Chih, Shen and Kang, have co-authored two of the highly cited papers, the sixth and the seventh. Another interesting issue is that the top four articles, in terms of the number of citations, are also the ones that receive the most citations on average per year. Finally, it can also be seen that the top five most cited articles have not been published by any of the 10 most prolific journals.

Another interesting issue to consider is the work of the most influential authors.

Table 11 presents the 10 most influential authors. Based on his published papers, Tsang has the highest influence, and Dhaliwal appears in the second position. This table also shows that only one of the 10 most prolific authors (Tsang, A.) is among the 10 most influential authors. However, other authors with few articles have received many citations. This evidences that being prolific in the field under study does not imply being influential. The most obvious case is Ionnou, I., who, with only one article, has received 349 citations. The total link strength can also be observed. This index measures collaboration among researchers. This collaboration pursues a mutual interest in a specific research area. Therefore, it could foster more beneficial research outcomes.

Next, let us examine the influence of countries.

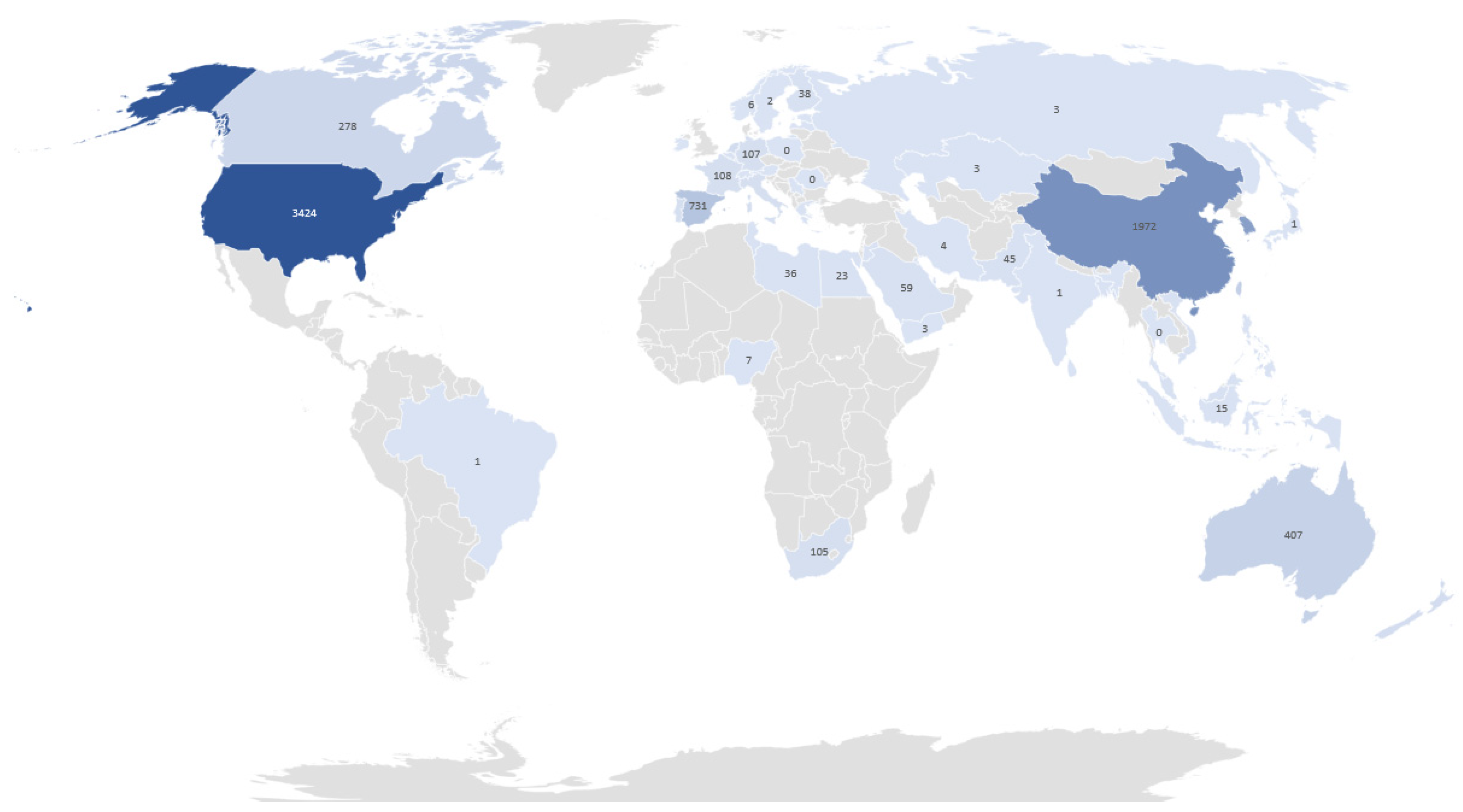

Figure 6 shows the geographical locations of the citations received by the articles in the field of this study. The intensity of the color is proportional to the number of citations received in each country. The results show how the two most prolific countries are also the two most influential, although with changed positions in the rankings. Thus, the greatest number of citations is found in the USA (3424), followed by China (1972), South Korea (1642), England (910) and Spain (731).

4.4. Co-Author Analysis

In this stage, in line with van Eck and Waltman (

van Eck and Waltman 2020), we present a map based on researcher networks. This allows us to identify the main authors who are doing scholarly work in this field so that potential researchers can know them (

Alshater et al. 2020). The elements of these networks are connected through co-authorship links (

León-gómez et al. 2021). We have used articles published jointly and, with them, we show map density based on network data connected by co-authorship items, which is shown in

Figure 5. Each link has a strength in this map, indicating the number of papers published between a pair of authors (

van Eck and Waltman 2020). Moreover, standard weight attributes are used to indicate the strength of each link with others (

Al-Ashmori et al. 2020). As is seen in

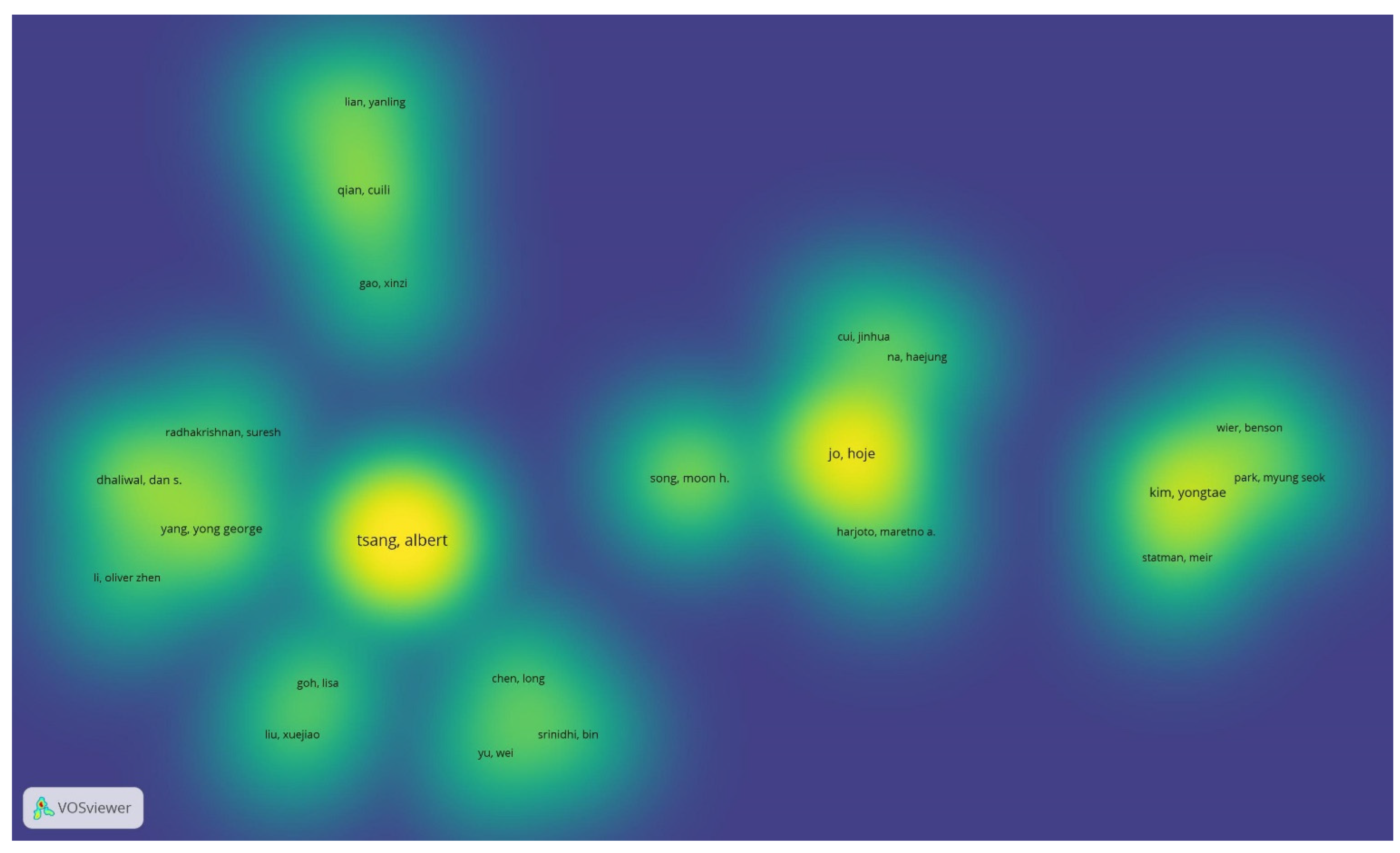

Figure 7, this map is composed of six different clusters, where the largest sets consist of five elements. Tsang has the highest total bond strength, followed by Jo, Kim, Dhaliwal and Qian. In turn, Dhaliwal and Kim are considered influential authors in the field studied. Likewise, Tsang and Jo are two of the most prolific authors.

4.5. Co-Citation Analysis

Co-citation analysis seeks to examine how many times two documents are cited together by other documents and can thus be considered as a proximity measure of publications (

Zhao et al. 2019). For this reason, in this analysis, it is interesting to consider the most cited papers and how they are connected with other papers. In this bibliometric review, an author co-citation analysis was performed, which examines how research communities evolve. For this purpose, we have used a co-citation map. The co-citation map visualization is a method of Exploratory Data Analysis (EDA) based on graph theory to explore the data structure (

Lewis-Beck et al. 2004). This method is able to provide the best cluster labels representing the authors who quote each other.

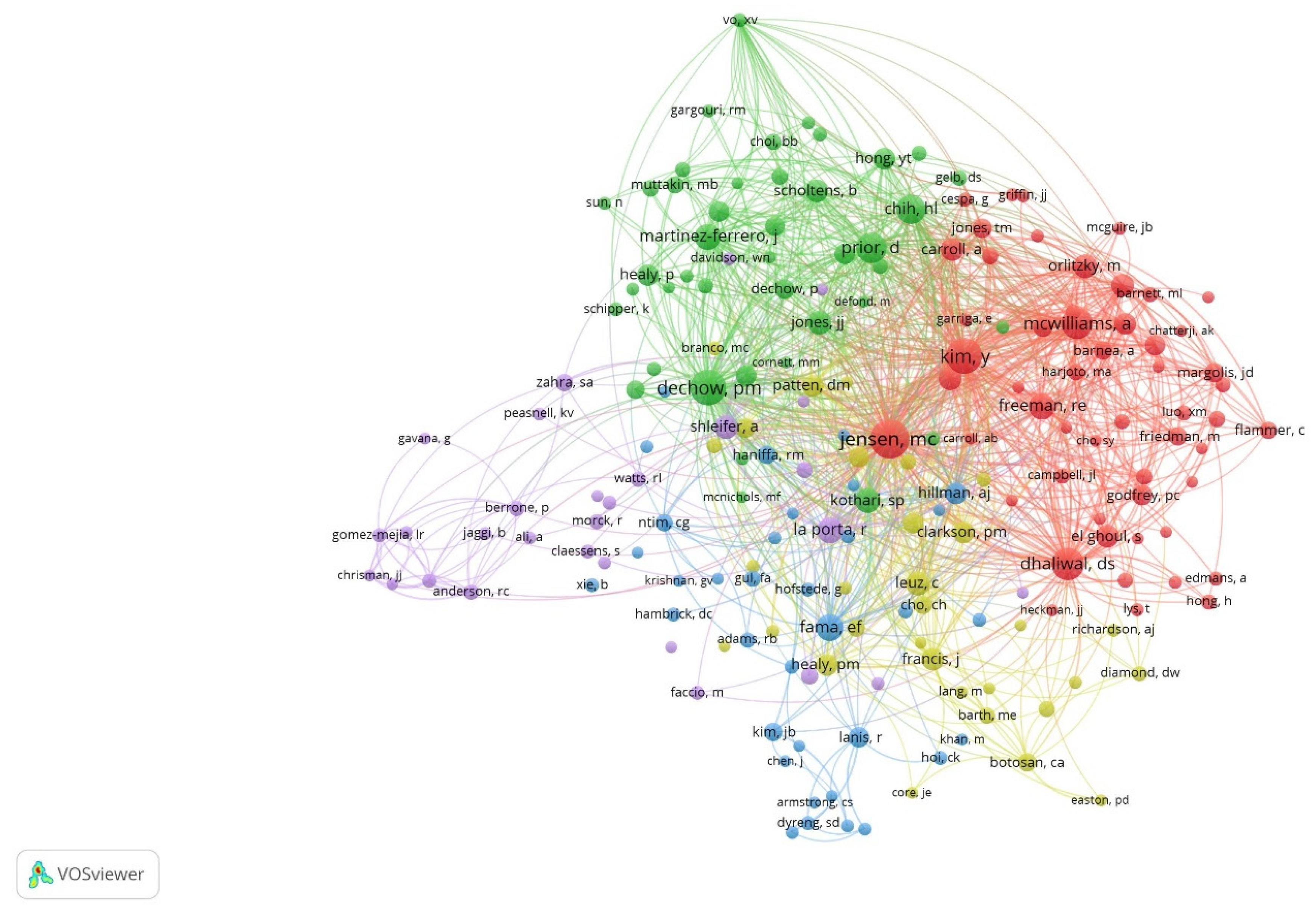

With a total of 9974 citations among authors in the field analyzed in this paper,

Figure 8 shows the existence of five clusters. It should be borne in mind that a single paper may result in several citations among authors. The color represents the collaboration clusters, the size denotes the number of co-citations and the line between two authors represents their cooperation through co-citations. The sizes of the five clusters ranged from 51 to 29. It can also be noted that there are three clusters that are particularly isolated and detached from the rest (red, green and purple). This is evidence of the existence of groups of authors who quote each other, so forming research communities. Moreover, the figure shows how the red and green clusters include the most influential authors.

5. Discussion and Conclusions

This research presents a structured review of the literature studying the influence of CSR on EM. Bibliometric studies on EM and the impact of CSR on EM are found in previous literature (

Velte 2020;

Parvin et al. 2020;

Benlemlih 2017). However, a bibliometric review linking CSR and EM that analytically and objectively identifies emerging works, authors and research groups has not been completed previously.

From the results of this study, it is possible to identify some of the most productive and influential research on the influence of CSR in EM in terms of journals, articles and authors. The results reveal that there are many journals (148) in which articles have been published in this field, with a total of 329 articles. This result differs from the bibliometric study published by

Velte (

2020), in which he claims that only 33 highly influential studies have been published on the topic analyzed. This difference is due to the fact that our article analyzes a longer period and also considers regions all over the world. Thus, our results show the publication of articles in this field by a large number of authors in more than 50 countries around the world. However, our analysis of geographical dispersion coincides with the previous study by

Parvin et al. (

2020), as it indicates that the most prolific current research is concentrated in a number of countries, such as China and the US, followed by the UK and Spain. In addition, this bibliometric review differs from others published to date, analyzing the productivity of organizations. Thus, our conclusions show that the University of Salamanca in Spain is the most prolific organization in this field, but its level of publications (0.005%) does not allow it to be considered as the leading organization in this field. The lack of a leading organization is another indication of the attention from researchers and organizations around the world.

However, our study differs from previous studies by

Velte (

2020) and

Parvin et al. (

2020), indicating that, in 2015, there was a growing interest in the study of CSR’s influence on EM. It has thus been confirmed that there has been a recent and successful period of related academic literature, specifically from 2015 to date.

On the other hand, the results of our bibliometric review on CSR and EM indicate that there is a relative concentration of the most influential papers among a certain number of researchers. Authors Garcia-Sanchez M., Martinez-Ferrero J. and Tsang A. have the highest number of publications. Other authors also have a high number of publications, such as Sial M.S., Ferramosca S., Garcia-Meca E. and Gerged A.M. However, the results reveal that, in this field, being a prolific author does not imply being an influential author because Tsang and Dhaliwal are the authors who have the most influence based on their published articles. Thus, as the field continues to mature, numerous authors are joining this line of research, expanding the work in a variety of areas (e.g., entrepreneurial finance, business and management) (

Benlemlih 2017). As a consequence, the number of citations is progressing upwards, reaching a total of 300 citations in the last five years, which shows the current significance of the analyzed relationship.

On the basis of the results obtained from the analysis of the keywords co-occurrence network, we have been able to identify a number of gaps in the literature on CSR and EM. These are issues that have already been addressed but have not been addressed with sufficient intensity. First, it is very interesting to study the effect of voluntary CSR disclosure on EM.

Gong and Ho (

2018) concluded that CSR has a moderate effect on managerial short-termism. However, they did not find evidence of voluntary disclosure and a reduction in EM, but there was the limitation that the study was only focused on China and the variables used to measure the managerial short-termism were limited. Second, the literature has dealt extensively with the effects of CSR on firm performance by providing firms with the opportunity to gain a number of competitive advantages that set them apart from their competitors (

Palacios-Manzano et al. 2021;

Santos-Jaén et al. 2021). However, it has not been extensively studied how reducing EM by implementing CSR practices can help improve firm performance. Third, it could also be very interesting to study the effects of CSR on EM in family businesses. Many authors have shown how family businesses have a greater awareness of sustainability and a greater commitment to the society around them (

Ruiz-Palomo et al. 2019). This leads them to implement CSR practices to a greater extent, which is supposed to reduce the opportunistic behavior of managers and shareholders and thus EM. Fourth, the literature could also elaborate further on how the presence of an audit committee influences the CSR practices developed by companies and their effect on EM. Fifth, there is scarce literature about the influences of CSR and real EM, taking into account that real EM has a high level of real manipulation (

Oskouei and Sureshjani 2021). A deep CSR should prevent and avoid all kinds of frauds and irregularities, and one of the main differences between EM and real EM is the intentionality, so CSR’s mitigation effect should be different in both cases. Finally, the possible effect of gender diversity on boards on the relationship between CSR and EM is not to be overlooked. The composition of the board of directors is recognized as an important factor in defining the strategy of companies (

Reguera-Alvarado et al. 2017). In recent years, there has been a growing interest among researchers to analyze the effect of the role played by women on boards (

Hossain et al. 2017). As the gender socialization theory states, women’s experience caring for children gives them a high degree of concern for others and makes them more sensitive to ethical and environmental issues than men. This leads women to be more reluctant to engage in result manipulation practices (

Ibrahim et al. 2009). For this reason, it is very interesting to address the influence of gender diversity on the effects of CSR on EM.

In accordance with the citation statistics from the WoS database, the findings demonstrate that there is a relative dispersion of keywords. A great number of clusters have been found and, from their analysis, it cannot be concluded that thematic clusters exist. Nevertheless, through co-citation analysis, the existence of clusters by authors who quote each other, forming research communities, is noted.

This research offers implications for the theory and research on CSR and its effect on EM through the growing global concern about the pernicious effects of manipulation of corporate performance. The results obtained in this topic suggest future lines of research, which will be of interest to researchers interested in developing their own studies on the influence of CSR on EM. We have found that research on the topic under analysis has mainly focused on the areas of corporate finance, business and management. Therefore, it would be interesting to approach new areas of studies that extend the results obtained. In this context, as indicated by our findings of the keywords co-occurrence network, there is a lack of research that seeks to determine the influence of the audit committee or the board of directors in this field, the influence of gender diversity or the family character of a company, etc., previously identified as gaps in the current literature. It would therefore be interesting to study further the influence of the characteristics of the audit committee or the board of directors, such as independence, gender or professionalization, on the direct or indirect impact of CSR on EM. Furthermore, given that the published studies focus on analyzing a number of countries, it would be necessary to extend the research to a wide range of regions in order to achieve a multicultural and globally relevant viewpoint.

Nevertheless, this study suffers from several limitations. First, the findings are only confined to the WoS database, retrieved on 28 February 2021. Although the WoS is the most important database, some articles are inevitably not stored in this database. Thus, we recommend conducting bibliometric analyses in the future by incorporating other databases such as Scopus or Google Scholar. Second, because the influence is a construct that depends on the passing of time, the age of the articles affects their influence, but only temporarily (

Ramos-Rodríguez and Ruíz-Navarro 2004). It would be interesting for future bibliometric reviews to establish a minimum threshold of citations for the time elapsed since the publication of the article. Finally, this study has provided the context and justification for the research published to date. In this context, there is a need to use bibliometric tools that apply mathematical and statistical methods to contrast and extend the conclusions obtained in this study.

In conclusion, this review offers an in-depth understanding of the status quo, gaps and future agenda of the influence of CSR on EM research for researchers. As it evidences the need to promote research on responsible business practices in order to formulate policies that enable the implementation of CSR practices that favor EM, therefore, researchers should follow the recommended directions and fill the existing knowledge gaps, thus extending the body in this field, developing better and more precise hypotheses and research questions, and, therefore, increasing the quality of research on the influence of CSR on EM.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}