Short-Selling and Financial Performance of SMEs in China: The Mediating Role of CSR Performance

Abstract

:1. Introduction

2. Literature Review

2.1. Short-Selling and the SME Board in China

2.2. Short-Selling and Firm Financial Performance

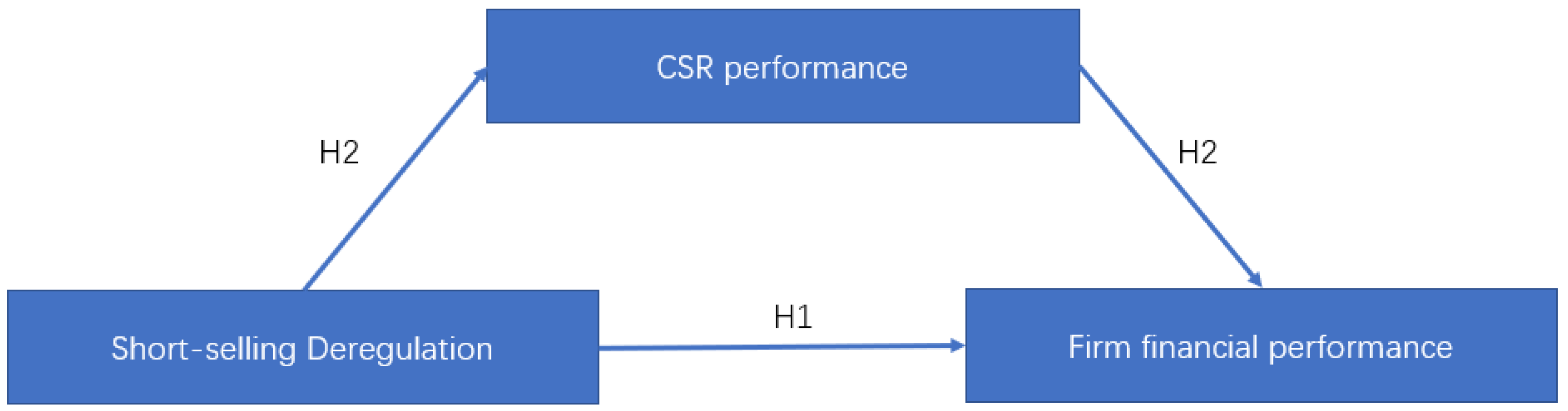

2.3. Short-Selling, CSR Performance, and Firm Financial Performance

3. Methodology

3.1. Measurements of Variables

3.2. Empirical Models

3.3. The Propensity Score Matching (PSM) Method

3.4. Data and Sample Sources

4. Results and Discussion

4.1. Empirical Results

4.2. Further Analysis of Family Business Effect

4.3. Further Analysis of Real Short-Selling Threats

4.4. Robustness Test

5. Conclusions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Ali, Waris, Jedrzej George Frynas, and Zeeshan Mahmood. 2017. Determinants of Corporate Social Responsibility (CSR) Disclosure in Developed and Developing Countries: A Literature Review. Corporate Social Responsibility and Environmental Management 24: 273–94. [Google Scholar] [CrossRef]

- Alshehhi, Ali, Haitham Nobanee, and Nilesh Khare. 2018. The impact of sustainability practices on corporate financial performance: Literature trends and future research potential. Sustainability 10: 494. [Google Scholar] [CrossRef] [Green Version]

- Baron, Reuben M., and David A. Kenny. 1986. The moderator–mediator variable distinction in social psychological research: Conceptual, strategic, and statistical considerations. Journal of Personality and Social Psychology 51: 1173. [Google Scholar] [CrossRef] [PubMed]

- Birindelli, Giuliana, Paola Ferretti, Mariantonietta Intonti, and Antonia Patrizia Iannuzzi. 2015. On the drivers of corporate social responsibility in banks: Evidence from an ethical rating model. Journal of Management and Governance 19: 303–40. [Google Scholar] [CrossRef]

- Brockman, Paul, Juan Luo, and Limin Xu. 2020. The impact of short-selling pressure on corporate employee relations. Journal of Corporate Finance 64: 101677. [Google Scholar] [CrossRef]

- Caliendo, Marco, and Sabine Kopeinig. 2008. Some practical guidance for the implementation of propensity score matching. Journal of Economic Surveys 22: 31–72. [Google Scholar] [CrossRef] [Green Version]

- Chen, Huili, Ying Chen, Bin Lin, and Yanchao Wang. 2019. Can short selling improve internal control? An empirical study based on the difference-in-differences model. Accounting & Finance 58: 1233–59. [Google Scholar]

- Chen, Jun, Huimin Li, and Dazhi Zheng. 2020a. The Impact of Margin-Trading and Short-Selling on Stock Price Efficiency—Evidence from the Fifth-Round Ban Lift in the Chinese Stock Market. The Chinese Economy 53: 265–84. [Google Scholar] [CrossRef]

- Chen, Shenglan, Robin K. Chou, Xiaoling Liu, and Yuhui Wu. 2020b. Deregulation of short-selling constraints and cost of bank loans: Evidence from a quasi-natural experiment. Pacific Basin Finance Journal 64. [Google Scholar] [CrossRef]

- Cheng, Shijun, Robert Felix, and Yijiang Zhao. 2019. Board interlock networks and informed short sales. Journal of Banking & Finance 98: 198–211. [Google Scholar]

- Cicea, Claudiu, Ion Popa, Corina Marinescu, and Simona Cătălina Ștefan. 2019. Determinants of SMEs’ performance: Evidence from European countries. Economic Research-Ekonomska Istraživanja 32: 1602–20. [Google Scholar] [CrossRef] [Green Version]

- Deng, Xiang, and Xiang Cheng. 2019. Can ESG Indices Improve the Enterprises’ Stock Market Performance?—An Empirical Study from China. Sustainability 11: 4765. [Google Scholar]

- Deng, Xiaohu, and Lei Gao. 2018. The monitoring of short selling: Evidence from China. Research in International Business and Finance 43: 68–78. [Google Scholar] [CrossRef]

- Endrikat, Jan. 2016. Market Reactions to Corporate Environmental Performance Related Events: A Meta-analytic Consolidation of the Empirical Evidence. Journal of Business Ethics 138: 535–48. [Google Scholar] [CrossRef]

- Erhemjamts, Otgontsetseg, and Kershen Huang. 2019. Institutional ownership horizon, corporate social responsibility and shareholder value. Journal of Business Research 105: 61–79. [Google Scholar] [CrossRef]

- Fang, Vivian W., Allen H. Huang, and Jonathan M. Karpoff. 2016. Short selling and earnings management: A controlled experiment. The Journal of Finance 71: 1251–94. [Google Scholar] [CrossRef] [Green Version]

- Gao, Xinghua, and Scott D. Julian. 2018. The Use of CSR to Insure Against Short Selling Downside Risk. Paper presented at the Academy of Management Proceedings, Chicago, IL, USA, July 9. [Google Scholar]

- Gao, George, Qingzhong Ma, and David Ng. 2018. The informativeness of short sellers: An insider’s perspective. China Finance Review International 8: 354–86. [Google Scholar] [CrossRef]

- He, Jie, and Xuan Tian. 2016. Do Short Sellers Exacerbate or Mitigate Managerial Myopia? Evidence from Patenting Activities. Paper presented at the 2016 American Finance Association Meetings, San Francisco, September 15. [Google Scholar]

- Hou, Deshuai, Qingbin Meng, Kai Zhang, and Kam C. Chan. 2019. Motives for corporate philanthropy propensity: Does short selling matter? International Review of Economics & Finance 63: 24–36. [Google Scholar]

- Hu, Yuanyuan, Shouming Chen, Yuexin Shao, and Su Gao. 2018. CSR and firm value: Evidence from China. Sustainability 10: 4597. [Google Scholar] [CrossRef] [Green Version]

- Jiang, Haiyan, Ahsan Habib, and Mostafa Monzur Hasan. 2020. Short Selling: A Review of the Literature and Implications for Future Research. European Accounting Review. [Google Scholar] [CrossRef]

- Kiriu, Takuya, and Masatoshi Nozaki. 2020. A Text Mining Model to Evaluate Firms’ ESG Activities: An Application for Japanese Firms. Asia-Pacific Financial Markets 27: 621–32. [Google Scholar] [CrossRef]

- Lamb, Nai H., and Frank C. Butler. 2018. The influence of family firms and institutional owners on corporate social responsibility performance. Business & Society 57: 1374–406. [Google Scholar]

- Leitterstorf, Max P., and Sabine B. Rau. 2014. Socioemotional wealth and IPO underpricing of family firms. Strategic Management Journal 35: 751–60. [Google Scholar] [CrossRef]

- Li, Chuntao, Hongmei Xu, Liwei Wang, and Peng Zhou. 2019a. Short-selling and corporate innovation: Evidence from the Chinese market. China Journal of Accounting Studies 7: 293–316. [Google Scholar] [CrossRef]

- Li, Jialong, Zulfiquer Ali Haider, Xianzhe Jin, and Wenlong Yuan. 2019b. Corporate controversy, social responsibility and market performance: International evidence. Journal of International Financial Markets, Institutions and Money 60: 1–18. [Google Scholar] [CrossRef]

- Li, Rui, Jiahui Li, and Jinjian Yuan. 2017. Short-sale prohibitions, firm characteristics and stock returns: Evidence from Chinese market. China Finance Review International 7: 407–28. [Google Scholar] [CrossRef]

- Lu, Louise Yi, Yu Yangxin, and Liandong Zhang. 2016. Short selling pressure and corporate social responsibility performance. Paper presented at the Sakura Luojia Accounting Symposium 2016, Wuhan, China, December 15–16; Available online: https://ink.library.smu.edu.sg/soa_research/1673 (accessed on 8 April 2021).

- Luo, Jinbo, Xiaoran Ni, and Gary Gang Tian. 2020. Short selling and corporate tax avoidance: Insights from a financial constraint view. Pacific-Basin Finance Journal 61: 101323. [Google Scholar] [CrossRef]

- Mai, Wenzhen, and Nik Intan Norhan Binti Abdul Hamid. 2020. Understanding the Effect of Short Selling Mechanism on Market Value of Pharmaceutical Industry in China Under Covid-19. Paper presented at the Basic & Clinical Pharmacology& Toxicology, Toronto, ON, Canada, June 26. [Google Scholar]

- Massa, Massimo, Bohui Zhang, and Hong Zhang. 2015. The invisible hand of short selling: Does short selling discipline earnings management? The Review of Financial Studies 28: 1701–36. [Google Scholar] [CrossRef]

- Meng, Qingbin, Ying Li, Xuanyu Jiang, and Kam C. Chan. 2017. Informed or speculative trading? Evidence from short selling before star and non-star analysts’ downgrade announcements in an emerging market. Journal of Empirical Finance 42: 240–55. [Google Scholar] [CrossRef]

- Michna, Anna, and Roman Kmieciak. 2020. Open-Mindedness Culture, Knowledge-Sharing, Financial Performance, and Industry 4.0 in SMEs. Sustainability 12: 9041. [Google Scholar] [CrossRef]

- Miller, Edward M. 1977. Risk, uncertainty, and divergence of opinion. The Journal of Finance 32: 1151–68. [Google Scholar] [CrossRef]

- Ni, Xiaoran, and Sirui Yin. 2020. The unintended real effects of short selling in an emerging market. Journal of Corporate Finance 64. [Google Scholar] [CrossRef]

- Park, KoEunc. 2017. Earnings quality and short selling: Evidence from real earnings management in the United States. Journal of Business Finance & Accounting 44: 1214–40. [Google Scholar]

- Rahman, Anisur, Bakhtear Talukdar, and Rafiqul Bhuyan. 2020. Board independence and short selling. Finance Research Letters. [Google Scholar] [CrossRef]

- Rajesh, R., and Chandrasekharan Rajendran. 2020. Relating Environmental, Social, and Governance scores and sustainability performances of firms: An empirical analysis. Business Strategy and the Environment 29: 1247–67. [Google Scholar] [CrossRef]

- Rennekamp, Kristina, Kathy Rupar, and Nicholas Seybert. 2019. Short Selling Pressure, Reporting Transparency, and the Use of Real and Accruals Earnings Management to Meet Benchmarks. Journal of Behavioral Finance 21: 186–204. [Google Scholar] [CrossRef]

- Rusinova, Vanya, and Georg Wernicke. 2019. Short Selling and Performance on Corporate Social Responsibility: Evidence from a Natural Experiment. Paper presented at the Academy of Management Proceedings, Boston, MA, USA, August 1. [Google Scholar]

- Velte, Patrick. 2020. Institutional ownership, environmental, social, and governance performance and disclosure—A review on empirical quantitative research. Problems and Perspectives in Management 18: 282–306. [Google Scholar] [CrossRef]

- Wang, Shuxun, and Dongyang Zhang. 2020. Short-selling restrictions and firms’ environment responsibility. Research in International Business and Finance 54. [Google Scholar] [CrossRef]

- Xu, Jian, Feng Liu, and Yue Shang. 2020. R&D investment, ESG performance and green innovation performance: Evidence from China. Kybernetes 50: 737–56. [Google Scholar]

- Zulfiqar, Muhammad, Khalid Hussain, Muhammad Usman Yousaf, Nadeem Sohail, and Sadeen Ghafoor. 2020. Moderating role of CEO compensation in lean innovation strategies of Chinese listed family firms. Corporate Governance (Bingley) 20: 887–902. [Google Scholar] [CrossRef]

{kind=link}

| Variable | Measurement | Source |

|---|---|---|

| Independent variables | ||

| Deregulation of short-selling (SHORT) | A dummy variable (0,1) equals 1 if the firm is shortable and 0 otherwise | Shenzhen Stock Exchange |

| Time factor of short-selling (TREAT) | A dummy variable (0,1) equals 1 for the years after the firm is shortable and 0 otherwise. | Shenzhen Stock Exchange |

| SHORT * TREAT | Interactive item of SHORT and TREAT | Shenzhen Stock Exchange |

| Mediating variable | ||

| CSR performance (CSR) | The actual CSR scores of individual stocks | Hexun Net CSR rating data |

| Dependent variables | ||

| Tobin’s Q | Market value of total assets divided by asset value | CSMAR Database |

| ROA | Net income divided by total assets | CSMAR Database |

| Control Variables | ||

| Firm size (SIZE) | Natural logarithm of market capitalization | CSMAR Database |

| Firm growth (GROWTH) | Market-to-book ratio | CSMAR Database |

| Firm leverage (LEV) | Total liability divided by total assets | CSMAR Database |

| Year effect | ||

| Industry effect |

| Treatment Group (Shortable) | Control Group (Non-Shortable) | |||||||

|---|---|---|---|---|---|---|---|---|

| Variables | N | Mean | Std | Median | N | Mean | Std | Median |

| Tobin’s Q | 2519 | 2.1173 | 1.0901 | 1.7596 | 2519 | 2.1435 | 1.0057 | 1.8221 |

| ROA | 2519 | 0.0596 | 0.0455 | 0.0528 | 2519 | 0.0580 | 0.0461 | 0.0545 |

| CSR | 2519 | 24.6204 | 14.1353 | 22.0800 | 2519 | 25.9472 | 15.6520 | 22.8500 |

| SIZE | 2519 | 22.8171 | 0.8156 | 22.7828 | 2519 | 22.7885 | 0.7553 | 22.7858 |

| GROWTH | 2519 | 0.0501 | 0.0351 | 0.0392 | 2519 | 0.0449 | 0.0302 | 0.0361 |

| LEV | 2519 | 0.3717 | 0.1799 | 0.3572 | 2519 | 0.3837 | 0.1725 | 0.3795 |

| Industry | Total Firms | Shortable Firms | Non-Shortable Firms |

|---|---|---|---|

| Manufacturing | 640 | 235 | 405 |

| Leasing and commercial services | 14 | 5 | 9 |

| Civil engineering | 7 | 1 | 6 |

| Real estate | 9 | 4 | 5 |

| Wholesale and retail trade | 23 | 14 | 9 |

| Infrastructure | 8 | 1 | 7 |

| Transport and postal services | 13 | 2 | 11 |

| Animal husbandry | 11 | 4 | 7 |

| Healthcare | 3 | 1 | 2 |

| Construction | 30 | 10 | 20 |

| Software and information technology services | 53 | 30 | 23 |

| Internet and related services | 10 | 0 | 10 |

| Mining and washing of coal | 6 | 3 | 3 |

| Hospitality | 1 | 0 | 1 |

| Culture, sports and arts | 5 | 0 | 5 |

| Education | 3 | 1 | 2 |

| Total | 836 | 311 | 525 |

| Variables | Samples | Mean | Sd | Min | Max |

|---|---|---|---|---|---|

| Tobin’s Q | 5038 | 2.1304 | 1.0487 | 0.9905 | 6.8277 |

| ROA | 5038 | 0.059 | 0.046 | −0.102 | 0.191 |

| SHORT | 5038 | 0.509 | 0.500 | 0.000 | 1.000 |

| TREAT | 5038 | 0.326 | 0.463 | 0.000 | 1.000 |

| SHORT * TREAT | 5038 | 0.217 | 0.412 | 0.000 | 1.000 |

| CSR | 5038 | 25.284 | 14.926 | −16.720 | 89.010 |

| SIZE | 5038 | 22.803 | 0.786 | 20.959 | 24.781 |

| GROWTH | 5038 | 0.047 | 0.033 | 0.010 | 0.209 |

| LEV | 5038 | 0.3777 | 0.1763 | 0.0445 | 0.8017 |

| Tobin’s Q | ROA | SHORT | SHORT * TREAT | CSR | SIZE | GROWTH | LEV | |

|---|---|---|---|---|---|---|---|---|

| Tobin’s Q | 1.0000 | |||||||

| ROA | 0.2726 *** | 1.0000 | ||||||

| SHORT | 0.0125 ** | 0.0175 ** | 1.0000 | |||||

| SHORT * TREAT | 0.0688 *** | 0.0302 ** | 0.5264 *** | 1.0000 | ||||

| CSR | 0.0511 *** | 0.3546 *** | 0.0444 *** | 0.0383 *** | 1.0000 | |||

| SIZE | 0.2763 *** | 0.3256 *** | −0.0182 * | 0.2382 *** | 0.0943 *** | 1.0000 | ||

| GROWTH | 0.5678 *** | 0.3569 *** | −0.0789 *** | −0.1011 *** | 0.0323 ** | 0.4313 *** | 1.0000 | |

| LEV | −0.2934 *** | −0.3072 *** | 0.0342 ** | 0.0797 *** | −0.0853 *** | 0.0772 *** | −0.0344 ** | 1.0000 |

| Model 1 | Model 2 | Model 3 | |||

|---|---|---|---|---|---|

| Variables | Tobin’s Q | ROA | CSR | Tobin’s Q | ROA |

| Intercept | 1.0552 *** (0.0013) | −0.2591 *** (0.0000) | −16.4354 ** (0.0221) | 1.1684 *** (0.0016) | −0.2608 *** (0.0000) |

| SHORT | 0.0098 * | 0.0137 ** | 0.0305 *** | 0.0100 * | 0.0143 ** |

| (0.0648) | (0.0251) | (0.0064) | (0.0536) | (0.0261) | |

| TREAT | 0.0539 *** | 0.0237 ** | 0.2785 *** | 0.0549 *** | 0.0246 ** |

| (0.0055) | (0.0165) | (0.0026) | (0.0056) | (0.0171) | |

| SHORT * TREAT | 0.3804 *** (0.0000) | 0.0050 *** (0.0006) | 0.7572 ** (0.0365) | 0.1679 (0.1192) | 0.0048 (0.1105) |

| CSR | 0.0010 ** (0.0348) | 0.0009 *** (0.0000) | |||

| SIZE | 0.0260 * (0.0873) | 0.0145 *** (0.0000) | 2.0751 *** (0.0000) | 0.0277 * (0.0901) | 0.0133 *** (0.0000) |

| GROWTH | 18.9028 *** (0.0000) | 0.3708 *** (0.0000) | −5.5686 (0.4107) | 17.9795 *** (0.0000) | 0.3337 *** (0.0000) |

| LEV | −1.6685 *** (0.0000) | −0.0841 *** (0.0000) | −8.8203 *** (0.0000) | −1.6655 *** (0.0000) | −0.0726 *** (0.0000) |

| Ind-fixed | yes | yes | yes | yes | yes |

| Year-fixed | yes | yes | yes | yes | yes |

| R-squared | 0.4236 | 0.2676 | 0.0177 | 0.4185 | 0.3481 |

| Adj R-squared | 0.4291 | 0.2632 | 0.0171 | 0.4192 | 0.3513 |

| F-statistics | 903.3398 | 463.2897 | 23.3832 | 1031.3358 | 647.0402 |

| N | 5038 | 5038 | 5038 | 5038 | 5038 |

| Tobin’s Q | ROA | |||||||

|---|---|---|---|---|---|---|---|---|

| Family Owned | Non-Family Owned | Family Owned | Non-Family Owned | |||||

| Variables | Coefficient | Probability | Coefficient | Probability | Coefficient | Probability | Coefficient | Probability |

| Intercept | 4.0089 *** | 0.0000 | 3.4903 *** | 0.0026 | −0.5950 *** | 0.0000 | −0.4049 *** | 0.0001 |

| SHORT | 0.0097 * | 0.0608 | 0.0096 * | 0.0686 | 0.0142 ** | 0.0259 | 0.0143 ** | 0.0261 |

| TREAT | 0.0538 *** | 0.0055 | 0.0530 *** | 0.0054 | 0.0244 ** | 0.0170 | 0.0246 ** | 0.0171 |

| SHORT * TREAT | 0.3093 | 0.2337 | 0.1304 | 0.7012 | −0.0037 | 0.8335 | 0.0547 | 0.1296 |

| CSR | 0.0015 * | 0.0647 | 0.0008 * | 0.0535 | 0.0010 *** | 0.0000 | 0.0009 *** | 0.0000 |

| SIZE | −0.0755 * | 0.0601 | −0.0856 * | 0.0919 | 0.0225 *** | 0.0000 | 0.0130 *** | 0.0001 |

| GROWTH | 26.7907 *** | 0.0000 | 33.7172 *** | 0.0000 | 0.2311 *** | 0.0004 | 0.2838 *** | 0.0003 |

| LEV | −2.4589 *** | 0.0000 | −2.2797 *** | 0.0000 | −0.0929 *** | 0.0000 | −0.0846 *** | 0.0000 |

| Ind-fixed | yes | yes | yes | yes | ||||

| Year-fixed | yes | yes | yes | yes | ||||

| R-squared | 0.6953 | 0.7690 | 0.4388 | 0.2959 | ||||

| Adj R-squared | 0.6617 | 0.7582 | 0.4273 | 0.3002 | ||||

| F-statistics | 259.1580 | 0.0000 | 296.0042 | 0.0000 | 96.8428 | 0.0000 | 39.9757 | 0.0000 |

| N | 640 | 449 | 640 | 449 | ||||

| Tobin’s Q | ROA | |||||||

|---|---|---|---|---|---|---|---|---|

| High SIR | Low SIR | High SIR | Low SIR | |||||

| Variables | Coefficient | Probability | Coefficient | Probability | Coefficient | Probability | Coefficient | Probability |

| Intercept | 2.7812 *** | 0.0016 | 4.6826 *** | 0.0001 | −0.3971 *** | 0.0000 | −0.4058 *** | 0.0000 |

| SHORT | 0.0099 * | 0.0532 | 0.0097 * | 0.0721 | 0.0144 ** | 0.0263 | 0.0142 ** | 0.0260 |

| TREAT | 0.0547 *** | 0.0056 | 0.0543 *** | 0.0055 | 0.0248 ** | 0.0173 | 0.0245 ** | 0.0170 |

| SHORT * TREAT | 0.2749 | 0.3168 | 0.1647 | 0.5910 | 0.0145 | 0.4707 | 0.0188 | 0.3146 |

| CSR | 0.0012 ** | 0.0322 | 0.0007 * | 0.0620 | 0.0011 *** | 0.0000 | 0.0008 *** | 0.0000 |

| SIZE | −0.0542 | 0.1785 | −0.1139 ** | 0.0139 | 0.0204 *** | 0.0000 | 0.0219 *** | 0.0000 |

| GROWTH | 26.7180 *** | 0.0000 | 28.8178 *** | 0.0000 | 0.3377 *** | 0.0001 | 0.1828 *** | 0.0053 |

| LEV | −2.0198 *** | 0.0000 | −2.4332 *** | 0.0000 | −0.0830 *** | 0.0000 | −0.0891 *** | 0.0000 |

| Ind-fixed | yes | yes | yes | yes | ||||

| Year-fixed | yes | yes | yes | yes | ||||

| R-squared | 0.7425 | 0.6647 | 0.3923 | 0.3493 | ||||

| Adj R-squared | 0.7139 | 0.6982 | 0.3980 | 0.3436 | ||||

| F-statistics | 281.2179 | 0.0000 | 251.2186 | 0.0000 | 73.5539 | 0.0000 | 58.5682 | 0.0000 |

| N | 545 | 545 | 545 | 545 | ||||

| Model 4 | Model 5 | Model 6 | |||

|---|---|---|---|---|---|

| Variables | PB | ROE | CSRr | PB | ROE |

| Intercept | −2.6156 *** (0.0000) | −0.6108 *** (0.0000) | 0.7900 *** (0.0014) | −2.6585 *** (0.0000) | −0.5599 *** (0.0000) |

| SHORT | 0.0684 *** | 0.0148 ** | 0.0179 * | 0.0664 *** | 0.0144 ** |

| (0.0049) | (0.0160) | (0.0879) | (0.0047) | (0.0157) | |

| TREAT | 0.0607 *** | 0.0039 * | 0.1152 *** | 0.0588 *** | 0.0038 * |

| (0.0040) | (0.0561) | (0.0036) | (0.0039) | (0.0548) | |

| SHORT * TREAT | 0.0010 *** (0.0032) | 0.0095 *** (0.0001) | 0.2141 ** (0.0374) | 0.0004 (0.1949) | 0.0099 (0.2313) |

| CSRr | 0.0008 ** (0.0431) | 0.0015 *** (0.0000) | |||

| SIZE | 0.1606 *** (0.0000) | 0.0241 *** (0.0000) | 0.0135 (0.1923) | 0.1541 *** (0.0000) | 0.0249 *** (0.0000) |

| GROWTH | 65.3481 *** (0.0000) | 0.5901 *** (0.0000) | −0.0761 (0.7729) | 67.5807 *** (0.0000) | 0.5890 *** (0.0000) |

| LEV | −0.1185 (0.3133) | 0.0120 ** (0.0495) | −0.0021 (0.9562) | −0.0994 (0.3463) | 0.0247 *** (0.0000) |

| Ind-fixed | yes | yes | yes | yes | yes |

| Year-fixed | yes | yes | yes | yes | yes |

| R-squared | 0.7337 | 0.2028 | 0.0324 | 0.7556 | 0.3119 |

| Adj R-squared | 0.7712 | 0.2102 | 0.0313 | 0.7675 | 0.3108 |

| F-statistics | 3930.2706 | 334.6904 | 1.1477 | 3180.6216 | 452.3354 |

| N | 5038 | 5038 | 5038 | 5038 | 5038 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Mai, W.; Hamid, N.I.N.b.A. Short-Selling and Financial Performance of SMEs in China: The Mediating Role of CSR Performance. Int. J. Financial Stud. 2021, 9, 22. https://doi.org/10.3390/ijfs9020022

Mai W, Hamid NINbA. Short-Selling and Financial Performance of SMEs in China: The Mediating Role of CSR Performance. International Journal of Financial Studies. 2021; 9(2):22. https://doi.org/10.3390/ijfs9020022

Chicago/Turabian StyleMai, Wenzhen, and Nik Intan Norhan binti Abdul Hamid. 2021. "Short-Selling and Financial Performance of SMEs in China: The Mediating Role of CSR Performance" International Journal of Financial Studies 9, no. 2: 22. https://doi.org/10.3390/ijfs9020022