The Impact of Financial Statement Comparability on Earnings Management: Evidence from Frontier Markets

Abstract

:1. Introduction

2. Related Research and Hypothesis Development

2.1. Frontier Market Countries

2.2. Comparability

2.3. Earnings Management

2.3.1. Accruals Earnings Management

2.3.2. Real Earnings Management

2.4. Institutional Factors

External Audit Quality

2.5. AEM and REM Trade-Off Decisions

3. Research Design

3.1. Comparability Measures

3.2. Accruals Manipulation

3.3. Real Activities Manipulation

3.4. Regression Specification

4. Results

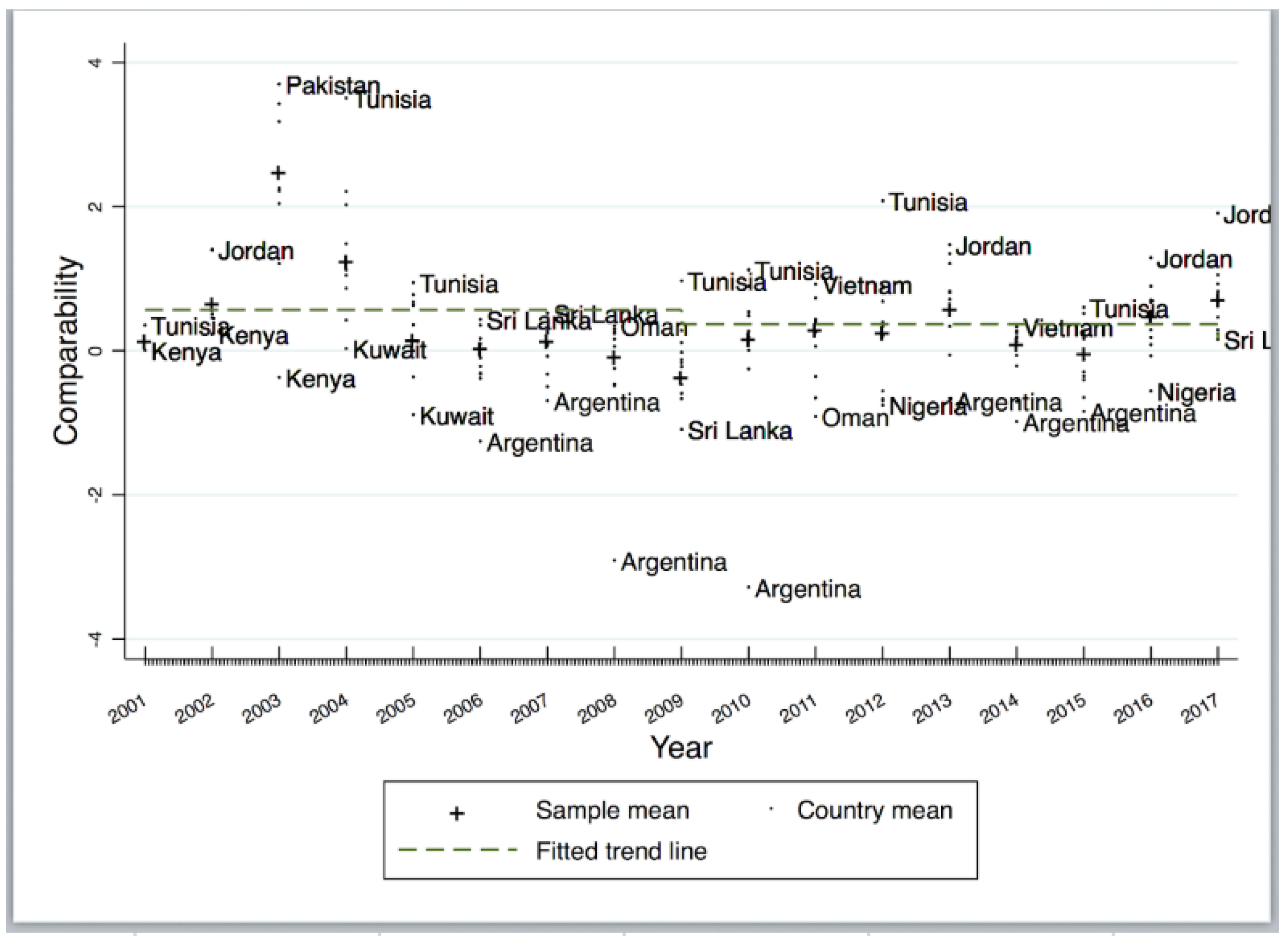

4.1. Study Sample, Data Sources, Descriptive Statistics, and Descriptive Statistics

4.2. Discussion of the Results

4.3. The Endogeneity Issue

5. Sensitivity Tests

5.1. Individual REM Measures

5.2. Earnings Management to Avoid Reported Diminished Earnings and Losses

5.3. IFRS Adoption in Europe

5.4. Legal System

5.5. IFRS Adhering Countries

5.6. External Audit Quality

6. Conclusions

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

| Industry Code | Industry | Mean | St | p25 | Median | p75 |

|---|---|---|---|---|---|---|

| 13 | Oil & Gas | 0.675688 | 1.168768 | −0.066618 | 0.482174 | 1.590968 |

| 20 | Food Products | 0.605875 | 1.110439 | −0.19555 | 0.31896 | 1.63655 |

| 24 | Paper and paper products | 0.501877 | 0.942295 | −0.143579 | 0.271035 | 1.148677 |

| 28 | Chemical Products | 0.579586 | 0.975116 | −0.072821 | 0.305981 | 1.352917 |

| 30 | Manufacturing | 0.686949 | 1.040302 | −0.074995 | 0.408874 | 1.63655 |

| 37 | Transportation | 0.535878 | 1.201013 | −0.281128 | 0.403475 | 1.610309 |

| 46 | Scientific instruments | 0.541757 | 1.008466 | −0.101431 | 0.227001 | 1.485157 |

| 48 | Communications | 0.94091 | 1.038662 | 0.103156 | 0.800769 | 1.945861 |

| 50 | Durable goods | 0.423259 | 0.944788 | −0.194386 | 0.211982 | 0.904411 |

| 58 | Eating and drinking establishments | 0.747424 | 1.00025 | −0.032264 | 0.437514 | 1.63655 |

| 80 | Health | 1.003957 | 1.182698 | 0.031 | 1.448939 | 1.94591 |

| Variable | Definition | |

|---|---|---|

| A | Total assets, sum of current and non-current assets. Source: Datastream. | |

| AEM | Accruals earnings management score, calculated using the Leuz et al. (2003) model. | |

| Analy | Analyst following, calculated by taking the natural log of one plus the number of analysts following a stock. Data source: Datastream. | |

| BM | Book to market, calculated by dividing book value of by equity market value. | |

| BigN | Big 4 or 5 auditor, dummy variable, set to 1 if yes. No otherwise. Source: Datastream. | |

| CA | Total current assets, as stated on the balance sheet. Source: Datastream. | |

| CapitalIntensity | Capital intensity, calculated by dividing net PPE by total assets. | |

| Cash | Cash as stated on the balance sheet. Source: Datastream. | |

| CFOA | Cash flow from operations divided by total assets at the start of the year. | |

| |CFOA| | Absolute value of CFOA. | |

| CL | Current liability. Source: Datastream. | |

| COGS | Cost of goods sold as stated on the balance sheet. Source: Datastream. | |

| CompScore | Firm-year level accounting comparability for the combination for firm i and other firms in the same two-digit SIC in a given year calculated as per Conaway (2017). | |

| DEP | Depreciation and amortisation. Source: Datastream. | |

| DISX | Abnormal discretionary expenses, estimated by discretionary expenses divided by lagged assets. Source: Datastream. | |

| EXP | Sales and General Admin expenses. Source: Datastream. | |

| Intangible | Intangible intensity, calculated as the sum of advertising and R&D expenses divided by sales. | |

| INV | Inventory. Source: Datastream. | |

| NI | Net income before extraordinary items. Source: Datastream. | |

| P | Price, annual share price at year end. Source: Datastream. | |

| LEV | Leverage, calculated by dividing total assets by total liabilities. | |

| LOSS | Loss, a dummy variable of 1 if dummy if loss generated (Net Income before extraordinary items < 0) as per Barth et al. (2012). | |

| OperCycle | Operating cycle, measured by natural logarithm of the sum of days receivables (365/(sales/accounts receivable)) and days inventory (365/(ales/ INV)). | |

| PAY | Payable, net accounts payable. Source: Datastream. | |

| PEN | Pension and retirement Expenses. Source: Datastream. | |

| PPE | Property, plant and equipment. Source: Datastream. | |

| REC | Receivables, total receivables. Source: Datastream. | |

| REM | Real earnings management score, calculated using the Roychowdhury (2006) model. | |

| RET | Return, 12 month buy and hold stock return; nine months before and three months after year-end. | |

| ROA | Net income before extraordinary items divided by divided by total assets at the start of the year. | |

| |ROA| | Absolute value of cash flow from operations divided by total assets at the start of the year. | |

| REV | Revenue, net sales. Source: Datastream. | |

| SD_ROA | Standard deviation of ROA for the previous five years at maximum. | |

| SD_Sales | Standard deviation of sales, calculated on the previous 5 years of revenue divided by total assets a the start of the year. | |

| Size | Firm size as calculated using the natural logarithm of the market value of equity. | |

| STD | Short term debt. Source: Datastream. |

References

- Abarbanell, Jeffery, and Reuven Lehavy. 2003. Biased forecasts or biased earnings? The role of reported earnings in explaining apparent bias and over/underreaction in analysts’ earnings forecasts. Journal of Accounting and Economics 36: 105–46. [Google Scholar] [CrossRef]

- Abernathy, John L., Brooke Beyer, and Eric T. Rapley. 2014. Earnings management constraints and classification shifting. Journal of Business Finance & Accounting 41: 600–26. [Google Scholar]

- Abid, Ammar, Muhammad Shaique, and Muhammad Anwar ul Haq. 2018. Do big four auditors always provide higher audit quality? Evidence from Pakistan. International Journal of Financial Studies 6: 58. [Google Scholar] [CrossRef] [Green Version]

- Ali, Sajid, Elie Bouri, Robert Lukas Czudaj, and Syed Jawad Hussain Shahzad. 2020. Revisiting the valuable roles of commodities for international stock markets. Resources Policy 66: 101603. [Google Scholar] [CrossRef]

- Alzoubi, Ebraheem Saleem Salem. 2016. Audit quality and earnings management: Evidence from jordan. Journal of Applied Accounting Research 17: 170–89. [Google Scholar] [CrossRef]

- Asgari, Mohammad Reza, Ali Asghar Shaban Pour, Reza Ataei Zadeh, and Samaneh Pahlavan. 2015. The relationship between firm’s growth opportunities and firm size on changes ratio in retained earnings of listed companies in tehran stock exchange. International Journal of Innovation and Applied Studies 10: 923. [Google Scholar]

- Ashbaugh, Hollis, Ryan LaFond, and Brian W Mayhew. 2003. Do nonaudit services compromise auditor independence? Further evidence. The Accounting Review 78: 611–39. [Google Scholar] [CrossRef]

- Bao, Shuji Rosey, and Krista B. Lewellyn. 2017. Ownership structure and earnings management in emerging markets—An institutionalized agency perspective. International Business Review 26: 828–38. [Google Scholar] [CrossRef]

- Barnes, Michelle L., and Anthony Tony W. Hughes. 2002. A quantile regression analysis of the cross section of stock market returns. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Barth, Mary E. 2008. Global financial reporting: Implications for us academics. The Accounting Review 83: 1159–79. [Google Scholar] [CrossRef]

- Barth, Mary E., Wayne R. Landsman, Mark Lang, and Christopher Williams. 2012. Are ifrs-based and us gaap-based accounting amounts comparable? Journal of Accounting and Economics 54: 68–93. [Google Scholar] [CrossRef]

- Bartov, Eli, Dan Givoly, and Carla Hayn. 2002. The rewards to meeting or beating earnings expectations. Journal of Accounting and Economics 33: 173–204. [Google Scholar] [CrossRef] [Green Version]

- Beatty, Anne, and Joseph Weber. 2003. The effects of debt contracting on voluntary accounting method changes. The Accounting Review 78: 119–42. [Google Scholar] [CrossRef]

- Beatty, Anne L., Bin Ke, and Kathy R. Petroni. 2002. Earnings management to avoid earnings declines across publicly and privately held banks. The Accounting Review 77: 547–70. [Google Scholar] [CrossRef]

- Becker, Connie L., Mark L. DeFond, James Jiambalvo, and K. R. Subramanyam. 1998. The effect of audit quality on earnings management. Contemporary Accounting Research 15: 1–24. [Google Scholar] [CrossRef]

- Blackburn, Douglas W., and Nusret Cakici. 2017. Overreaction and the cross-section of returns: International evidence. Journal of Empirical Finance 42: 1–14. [Google Scholar] [CrossRef]

- Braam, Geert, Monomita Nandy, Utz Weitzel, and Suman Lodh. 2015. Accrual-based and real earnings management and political connections. The International Journal of Accounting 50: 11–141. [Google Scholar] [CrossRef] [Green Version]

- Bradshaw, Mark T., Gregory S. Miller, and George Serafeim. 2009. Accounting Method Heterogeneity and Analysts’ Forecasts. Chicago: University of Chicago, Ann Arbor: University of Michigan, Cambridge: Harvard University. [Google Scholar]

- Burgstahler, David, and Ilia Dichev. 1997. Earnings management to avoid earnings decreases and losses. Journal of Accounting and Economics 24: 99–126. [Google Scholar] [CrossRef]

- Cai, Francis, and Hannah Wong. 2010. The effect of ifrs adoption on global market integration. International Business and Economics Research Journal 9: 25–34. [Google Scholar] [CrossRef]

- Cassell, Cory A., Linda A. Myers, and Timothy A. Seidel. 2015. Disclosure transparency about activity in valuation allowance and reserve accounts and accruals-based earnings management. Accounting, Organizations and Society 46: 23–38. [Google Scholar] [CrossRef]

- Chauhan, Yogesh, and Surya B. Kumar. 2019. Does accounting comparability alleviate the informational disadvantage of foreign investors? International Review of Economics & Finance 60: 114–29. [Google Scholar]

- Chen, Anthony. 2016. Does Comparability Restrict Opportunistic Accounting? Tallahassee: Florida State University, vol. 205. [Google Scholar]

- Chen, Ciao-Wei, Daniel W. Collins, Todd D. Kravet, and Richard D. Mergenthaler. 2018. Financial statement comparability and the efficiency of acquisition decisions. Contemporary Accounting Research 35: 164–202. [Google Scholar] [CrossRef]

- Chen, Jeff Zeyun, Lynn L. Rees, and Shiva Sivaramakrishnan. 2010. On the use of accounting vs. real earnings management to meet earnings expectations-a market analysis. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Chi, Ching-Wen, Ken Hung, and Shinhua Liu. 2020. Corporate governance and earnings management in taiwan: A quantile regression approach. Journal of Accounting and Finance 20. [Google Scholar] [CrossRef]

- Chin, Chen-Lung, Yu-Ju Chen, and Tsun-Jui Hsieh. 2009. International diversification, ownership structure, legal origin, and earnings management: Evidence from Taiwan. Journal of Accounting, Auditing & Finance 24: 233–62. [Google Scholar]

- Chircop, Justin, Daniel W. Collins, Lars Helge Hass, and Nhat (Nate) Q. Nguyen. 2020. Accounting comparability and corporate innovative efficiency. The Accounting Review 95: 127–51. [Google Scholar] [CrossRef]

- Clemons, Eric K. 2019. Resources, platforms, and sustainable competitive advantage: How to win and keep on winning. In New Patterns of Power and Profit. Berlin: Springer, pp. 93–104. [Google Scholar]

- Cohen, Daniel A., Aiyesha Dey, and Thomas Z. Lys. 2008. Real and accrual-based earnings management in the pre-and post-sarbanes-oxley periods. The Accounting Review 83: 757–87. [Google Scholar] [CrossRef] [Green Version]

- Cohen, Daniel A., and Paul Zarowin. 2010. Accrual-based and real earnings management activities around seasoned equity offerings. Journal of Accounting and Economics 50: 2–19. [Google Scholar] [CrossRef] [Green Version]

- Conaway, Jenelle. 2017. Has Global Financial Reporting Comparability Improved? Ph.D. Thesis, Boston University, Boston, MA, USA. [Google Scholar]

- Cuervo Valledor, Álvaro, Adolfo Pérez Mena, Miguel Vicente López, and Rosalía Calvo Clúa. 2016. Estudio de las Posibilidades de Inversión en los Mercados Frontera. Munich: Ludwig Maximilian University of Munich. [Google Scholar]

- Darmadi, Salim. 2016. Ownership concentration, family control, and auditor choice. Asian Review of Accounting 24: 19–42. [Google Scholar] [CrossRef]

- Dayanandan, Ajit, Han Donker, Mike Ivanof, and Gökhan Karahan. 2016. Ifrs and accounting quality: Legal origin, regional, and disclosure impacts. International Journal of Accounting and Information Management 24: 296–316. [Google Scholar] [CrossRef]

- De Franco, Gus, Ole-Kristian Hope, and Stephannie Larocque. 2015. Analysts’ choice of peer companies. Review of Accounting Studies 20: 82–109. [Google Scholar] [CrossRef]

- De Franco, Gus, Sagar P. Kothari, and Rodrigo S. Verdi. 2011. The benefits of financial statement comparability. Journal of Accounting Research 49: 895–931. [Google Scholar] [CrossRef] [Green Version]

- Dechow, Patricia, Weili Ge, and Catherine Schrand. 2010. Understanding earnings quality: A review of the proxies, their determinants and their consequences. Journal of Accounting and Economics 50: 344–401. [Google Scholar] [CrossRef] [Green Version]

- Dechow, Patricia M., Richard G. Sloan, and Amy P. Sweeney. 1995. Detecting earnings management. Accounting Review 70: 193–225. [Google Scholar]

- DeFond, Mark, Xuesong Hu, Mingyi Hung, and Siqi Li. 2011. The impact of mandatory ifrs adoption on foreign mutual fund ownership: The role of comparability. Journal of Accounting and Economics 51: 240–58. [Google Scholar] [CrossRef]

- Durnev, Artem, Tiemei Li, and Michel Magnan. 2017. Beyond tax avoidance: Offshore firms’ institutional environment and financial reporting quality. Journal of Business Finance & Accounting 44: 646–96. [Google Scholar]

- Ebraheem Saleem, Salem A. 2019. Audit committee, internal audit function and earnings management: Evidence from jordan. Meditari Accountancy Research 28: 72–90. [Google Scholar]

- Enomoto, Masahiro, Fumihiko Kimura, and Tomoyasu Yamaguchi. 2015. Accrual-based and real earnings management: An international comparison for investor protection. Journal of Contemporary Accounting & Economics 11: 183–98. [Google Scholar]

- Ewert, Ralf, and Alfred Wagenhofer. 2005. Economic effects of tightening accounting standards to restrict earnings management. The Accounting Review 80: 1101–24. [Google Scholar] [CrossRef]

- FASB. 2010. Conceptual Framework for Financial Reporting: Concepts Statement No. 8. Available online: https://www.fasb.org/resources/ccurl/515/412/Concepts (accessed on 13 September 2020).

- Framework, Conceptual. 2018. Conceptual Framework for Financial Reporting. London: IFRS Foundation. [Google Scholar]

- Francis, Jere R., Matthew L. Pinnuck, and Olena Watanabe. 2014. Auditor style and financial statement comparability. The Accounting Review 89: 605–33. [Google Scholar] [CrossRef]

- Francis, Jere R., and Dechun Wang. 2008. The joint effect of investor protection and big 4 audits on earnings quality around the world. Contemporary Accounting Review 25: 157–91. [Google Scholar] [CrossRef]

- Frankel, Richard M., Marilyn F. Johnson, and Karen K. Nelson. 2002. The relation between auditors’ fees for nonaudit services and earnings management. The Accounting Review 77: 71–105. [Google Scholar] [CrossRef] [Green Version]

- Ge, Wenxia, and Jeong-Bon Kim. 2014. Real earnings management and the cost of new corporate bonds. Journal of Business Research 67: 641–47. [Google Scholar] [CrossRef]

- Gerged, Ali Meftah, Lara Mohammad Al-Haddad, and Meshari O. Al-Hajri. 2020. Is earnings management associated with corporate environmental disclosure? Accounting Research Journal 33: 167–85. [Google Scholar] [CrossRef]

- Ghosh, Aloke, and Doocheol Moon. 2005. Auditor tenure and perceptions of audit quality. The Accounting Review 80: 585–612. [Google Scholar] [CrossRef]

- Ghosh, Saibal. 2007. Loan loss provisions, earnings, capital management and signalling: Evidence from indian banks. Global Economic Review 36: 121–36. [Google Scholar] [CrossRef]

- Giner, Begoña, and Bill Rees. 2005. The introduction of international financial reporting standards in the european union. European Accounting Review 14: 35–52. [Google Scholar]

- Glass, Christy, Alison Cook, and Alicia R. Ingersoll. 2016. Do women leaders promote sustainability? Analyzing the effect of corporate governance composition on environmental performance. Business Strategy and the Environment 25: 495–511. [Google Scholar] [CrossRef]

- Gramling, Audrey A., and Patricia M. Myers. 2003. Internal auditors’ assessment of fraud warning signs: Implications for external auditors. The CPA Journal 73: 20. [Google Scholar]

- Gregoriou, G. N., and M. Wu. 2016. An application of style analysis to middle east and north african (mena) hedge funds. In Handbook of Frontier Markets. Amsterdam: Elsevier, pp. 19–31. [Google Scholar]

- Gross, Christian, and Pietro Perotti. 2017. Output-based measurement of accounting comparability: A survey of empirical proxies. Journal of Accounting Literature 39: 1–22. [Google Scholar] [CrossRef] [Green Version]

- Gujarati, Damodar N. 2009. Basic Econometrics. New York: McGraw-Hill Education. [Google Scholar]

- Gul, Ferdinand A, Simon Yu Kit Fung, and Bikki Jaggi. 2009. Earnings quality: Some evidence on the role of auditor tenure and auditors’ industry expertise. Journal of Accounting and Economics 47: 265–87. [Google Scholar] [CrossRef]

- Gunny, Katherine A. 2010. The relation between earnings management using real activities manipulation and future performance: Evidence from meeting earnings benchmarks. Contemporary Accounting Research 27: 855–88. [Google Scholar] [CrossRef]

- Hail, Luzi, Christian Leuz, and Peter Wysocki. 2010. Global accounting convergence and the potential adoption of ifrs by the us. Part I: Conceptual underpinnings and economic analysis. Accounting Horizons 24: 355–94. [Google Scholar] [CrossRef]

- Hasan, Mostafa Monzur, and Grantley Taylor. 2020. Financial statement comparability and bank risk-taking. Journal of Contemporary Accounting & Economics 16: 100206. [Google Scholar]

- Haw, In-Mu, Bingbing Hu, Lee-Seok Hwang, and Woody Wu. 2004. Ultimate ownership, income management, and legal and extra-legal institutions. Journal of Accounting Review 42: 423–62. [Google Scholar] [CrossRef]

- Healy, Paul M., and Krishna G. Palepu. 2001. Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. Journal of Accounting and Economics 31: 405–40. [Google Scholar] [CrossRef]

- Healy, Paul M., and James M. Wahlen. 1999. A review of the earnings management literature and its implications for standard setting. Accounting Horizons 13: 365–83. [Google Scholar] [CrossRef]

- Hölmstrom, Bengt. 1979. Moral hazard and observability. The Bell Journal of Economics 10: 74–91. [Google Scholar] [CrossRef] [Green Version]

- Houqe, Muhammad Nurul, Kamran Ahmed, and Tony van Zijl. 2017. Audit quality, earnings management, and cost of equity capital: Evidence from india. International Journal of Auditing 21: 177–89. [Google Scholar] [CrossRef]

- Howard, Michael, Maroun Warren, and Robert Garnett. 2019. Misuse of non-mandatory earnings reporting by companies. Meditari Accountancy Research 28: 125–46. [Google Scholar] [CrossRef]

- Hughes, Susan, and Sander G. Xiques Larson Robert. 2017. Difficulties converging us gaap and ifrs through joint projects: The case of business combinations. Advances in Accounting 39: 1–20. [Google Scholar] [CrossRef]

- Hung, Mingyi. 2000. Accounting standards and value relevance of financial statements: An international analysis. Journal of Accounting and Economics 30: 401–20. [Google Scholar] [CrossRef]

- Hutchison, Michael M. 2002. European banking distress and emu: Institutional and macroeconomic risks. Scandinavian Journal of Economics 104: 365–89. [Google Scholar] [CrossRef] [Green Version]

- Ipino, Elisabetta, and Antonio Parbonetti. 2017. Mandatory ifrs adoption: The trade-off between accrual-based and real earnings management. Accounting and Business Research 47: 91–121. [Google Scholar] [CrossRef]

- Jelinek, Kate. 2007. The effect of leverage increases on earnings management. The Journal of Business and Economic Studies 13: 24. [Google Scholar]

- Jones, Jennifer J. 1991. Earnings management during import relief investigations. Journal of Accounting Review 29: 193–228. [Google Scholar] [CrossRef]

- Joosten, Carmen. 2012. Real Earnings Management and Accrual-Based Earnings Management as Substitutes. Tilburg: Tilburg University, vol. 52. [Google Scholar]

- Kaawaase, Twaha K., Mussa Juma Assad, Ernest G. Kitindi, and Stephen Korutaro Nkundabanyanga. 2016. Audit quality differences amongst audit firms in a developing economy. Journal of Accounting in Emerging Economies 6: 1–26. [Google Scholar] [CrossRef] [Green Version]

- Kawada, Brett. 2014. Auditor Offices and the Comparability and Quality of Clients’ Earnings. San Diego: San Diego State University. [Google Scholar]

- Khanh, Hoang Thi Mai, and Vinh Khuong Nguyen. 2018. Audit quality, firm characteristics and real earnings management: The case of listed Vietnamese firms. International Journal of Economics and Financial Issues 8: 243. [Google Scholar]

- Kim, Jeong-Bon, Richard Chung, and Michael Firth. 2003. Auditor conservatism, asymmetric monitoring, and earnings management. Contemporary Accounting Research 20: 323–59. [Google Scholar] [CrossRef]

- Kim, Jeong-Bon, Leye Li, Louise Yi Lu, and Yangxin Yu. 2016. Financial statement comparability and expected crash risk. Journal of Accounting and Economics 61: 294–312. [Google Scholar] [CrossRef]

- Kim, Seil, Pepa Kraft, and Stephen G. Ryan. 2013. Financial statement comparability and credit risk. Review of Accounting Studies 18: 783–823. [Google Scholar] [CrossRef]

- Kiya, Ali, and Safari G. 2017. Financial statement comparability, accruals-based earnings management, real earnings management. an empirical test of tehran stock exchange. Journal of Financial Accounting Knowledge 26: 115–137. [Google Scholar]

- Klein, April. 2002. Audit committee, board of director characteristics, and earnings management. Journal of Accounting and Economics 33: 375–400. [Google Scholar] [CrossRef] [Green Version]

- Knapp, Michael C. 1991. Factors that audit committee members use as surrogates for audit quality. Auditing: A Journal of Practice & Theory 10: 35–52. [Google Scholar]

- Kothari, Sagar P., Andrew J. Leone, and Charles E. Wasley. 2005. Performance matched discretionary accrual measures. Journal of Accounting and Economics 39: 163–97. [Google Scholar] [CrossRef]

- Krishnan, Gopal V. 2003. Does big 6 auditor industry expertise constrain earnings management? Accounting Horizons 17: 1–16. [Google Scholar] [CrossRef] [Green Version]

- La Porta, Rafael, Florencio Lopez-de Silanes, Andrei Shleifer, and Robert W. Vishny. 1997. Legal determinants of external finance. The Journal of Finance 52: 1131–50. [Google Scholar] [CrossRef]

- Lang, Mark H., Mark G. Maffett, and Edward Owens. 2010. Earnings comovement and accounting comparability: The effects of mandatory ifrs adoption. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Lee, Myung-Gun, Minjung Kang, Ho-Young Lee, and Jong Chool Park. 2016. Related-party transactions and financial statement comparability: Evidence from south korea. Asia-Pacific Journal of Accounting & Economics 23: 224–52. [Google Scholar]

- Lemma, Tesfaye Taddese, Ayalew Lulseged, Mthokozisi Mlilo, and Minga Negash. 2019. Political stability, political rights and earnings management: some international evidence. Accounting Research Journal 33: 57–74. [Google Scholar] [CrossRef]

- Lemma, Tesfaye T., Minga Negash, Mthokozisi Mlilo, and Ayalew Lulseged. 2018. Institutional ownership, product market competition, and earnings management: Some evidence from international data. Journal of Business Research 90: 151–63. [Google Scholar] [CrossRef]

- Leuz, Christian, Dhananjay Nanda, and Peter D. Wysocki. 2003. Earnings management and investor protection: an international comparison. Journal of Financial Economics 69: 505–27. [Google Scholar] [CrossRef]

- Li, Leon, and Chii-Shyan Kuo. 2017. Ceo equity compensation and earnings management: The role of growth opportunities. Finance Research Letters 20: 289–95. [Google Scholar] [CrossRef]

- Li, Shaomin, Seung Ho Park, and Rosey Shuji Bao. 2014. How much can we trust the financial report? Earnings management in emerging economies. International Journal of Emerging Markets 9: 33–53. [Google Scholar] [CrossRef]

- Li, Shaomin, David D. Selover, and Michael Stein. 2011. “Keep silent and make money”: Institutional patterns of earnings management in china. Journal of Asian Economics 22: 369–82. [Google Scholar] [CrossRef]

- Lin, Hsiou-Wei William, Huai-Chun Lo, and Ruei-Shian Wu. 2016. Modeling default prediction with earnings management. Pacific-Basin Finance Journal 40: 306–22. [Google Scholar] [CrossRef]

- Lin, Steve, William N. Riccardi, Changjiang Wang, Patrick E. Hopkins, and Gary Kabureck. 2019. Relative effects of ifrs adoption and ifrs convergence on financial statement comparability. Contemporary Accounting Research 36: 588–628. [Google Scholar] [CrossRef] [Green Version]

- MSCI. 2020. Msci Market Classification Framework. Available online: https://www.msci.com/documents/1296102/1330218/MSCI_Global_Market_Framework_2019.pdf/57f021bc-a41b-f6a6-c482-8d4881b759bf (accessed on 28 April 2020).

- Nouy, Daniele. 2014. Regulatory and Financial Reporting Essential for Effective Banking Supervision and Financial Stability. Available online: https://www.bankingsupervision.europa.eu/press/speeches/date/2014/html/se140603.en.html (accessed on 13 September 2020).

- Piot, Charles, and Rémi Janin. 2007. External auditors, audit committees and earnings management in France. European Accounting Review 16: 429–54. [Google Scholar] [CrossRef]

- Rodriguez-Ariza, Lázaro, Jennifer Martínez-Ferrero, and Manuel Bermejo-Sánchez. 2016. Consequences of earnings management for corporate reputation: Evidence from family firms. Accounting Research Journal 29: 457–74. [Google Scholar] [CrossRef]

- Roychowdhury, Sugata. 2006. Earnings management through real activities manipulation. Journal of Accounting and Economics 42: 335–70. [Google Scholar] [CrossRef]

- Ruddock, Caitlin, Sarah J. Taylor, and Stephen L. Taylor. 2006. Nonaudit services and earnings conservatism: Is auditor independence impaired? Contemporary Accounting Research 23: 701–46. [Google Scholar] [CrossRef]

- Rusmin, Rusmin. 2010. Auditor quality and earnings management: Singaporean evidence. Managerial Auditing Journal 25: 1–24. [Google Scholar] [CrossRef]

- Salehi, Mahdi, Hossein Tarighi, and Samaneh Safdari. 2018. The relation between corporate governance mechanisms, executive compensation and audit fees: Evidence from iran. Management Research Review 41: 939–67. [Google Scholar] [CrossRef]

- Shane, Philip, David Smith, and Suning Zhang. 2014. Financial statement comparability and valuation of seasoned equity offerings. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Shen, Chung-Hua, and Hsiang-Lin Chih. 2005. Investor protection, prospect theory, and earnings management: An international comparison of the banking industry. Journal of Banking & Finance 29: 2675–97. [Google Scholar]

- Sohn, Byungcherl Charlie. 2016. The effect of accounting comparability on the accrual-based and real earnings management. Journal of Accounting and Public Policy 35: 513–39. [Google Scholar] [CrossRef]

- Stereńczak, Szymon, Adam Zaremba, and Zaghum Umar. 2020. Is there an illiquidity premium in frontier markets? Emerging Markets Review 42: 100673. [Google Scholar] [CrossRef]

- Tabassum, Naila, Ahmad Kaleem, and Mian Sajid Nazir. 2015. Real earnings management and future performance. Global Business Review 16: 21–34. [Google Scholar] [CrossRef]

- Thomas, Nisha Mary, Smita Kashiramka, and Surendra S. Yadav. 2017. Dynamic linkages among developed, emerging and frontier capital markets of asia-pacific region. Journal of Advances in Management Research 14: 332–51. [Google Scholar] [CrossRef]

- Tran, Nam Hoai, and Chi Dat Le. 2020. Ownership concentration, corporate risk-taking and performance: Evidence from vietnamese listed firms. Cogent Economics & Finance 8: 219–38. [Google Scholar]

- Tversky, Amos, and Daniel Kahneman. 1992. Advances in prospect theory: Cumulative representation of uncertainty. Journal of Risk & Uncertainty 5: 297–323. [Google Scholar]

- Wang, Sean, and Julia D’Souza. 2006. Earnings management: The effect of accounting flexibility on R&D investment choices. SSRN Electronic Journal. [Google Scholar] [CrossRef]

- Young, Steven, and Yachang Zeng. 2015. Accounting comparability and the accuracy of peer-based valuation models. The Accounting Review 90: 2571–601. [Google Scholar] [CrossRef] [Green Version]

- Yu, Gwen, and Aida Sijamic Wahid. 2014. Accounting standards and international portfolio holdings. The Accounting Review 89: 1895–930. [Google Scholar] [CrossRef] [Green Version]

- Zang, Amy Y. 2011. Evidence on the trade-off between real activities manipulation and accrual-based earnings management. The Accounting Review 87: 675–703. [Google Scholar] [CrossRef]

- Zaremba, Adam, and Alina Maydybura. 2019. The cross-section of returns in frontier equity markets: Integrated or segmented pricing? Emerging Markets Review 38: 219–38. [Google Scholar] [CrossRef]

- Zhang, Joseph H. 2018. Accounting comparability, audit effort, and audit outcomes. Contemporary Accounting Research 35: 245–76. [Google Scholar] [CrossRef] [Green Version]

- Zhou, Zejiang, Jing Ma, and Yue Geng. 2017. Does tenure location impact governance role of independent directors? Empirical evidence from the earnings management perspective. Journal of Accounting and Economics 5: 275. [Google Scholar]

| 1. | Goodwill impairment or deferred tax assets and liabilities recognition are areas where interpretation may be applied. |

| 2. | Prospect theory suggests that individuals derive value from gains from a reference point, rather than absolute levels (Tversky and Kahneman 1992). |

| 3. | Based on the MSCI Frontier Market Index companies. |

| 4. | Based on weekly data of MSCI Frontier Market and MSCI Developed market index from 2015 to 2020. Source Thomson Datastream. |

| 5. | As evidenced by the EU members requirement to adopt IFRS, and the United States, Japan, and China, the choice to converge with IFRS (Lin et al. 2019). |

| 6. | Financial Accounting and Standards Board (FASB), and the International Accounting Standards Board (IASB). |

| 7. | Advantages may be market share dominance and or profitability above the industry average. |

| 8. | As opposed to earnings composed of cash. |

| 9. | Whether it is local accounting standards, International Financial Reporting Standards (IFRS), or Generally Accepted Accounting Principles GAAP). |

| 10. | A minimum of two countries with sufficient firms in each industry-year is required. |

| 11. | The Hausman test for fixed vs. random-effects models returns a chi-squared value of 51.87, which is significant at the 0.01% level, indicating that the fixed-effects model is appropriate. |

| 12. | Wooldridge test for autocorrelation in panel data finds an F-statistic of 1786.826, which is significant at the 0.01% level for the lag comparable score value. |

| 13. | Breusch–Pagan/Cook–Weisberg test for heteroskedasticity score is 96.46, which is significant at the 0.01% level. |

| 14. | Prior to 2005, EU listed companies followed a variety of country-specific accounting principles. |

| Panel A | Panel B | Panel C | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Sample by Calendar Year | Sample by Country of Listing | Sample by Industry | ||||||||

| Year | n | % | Country | n | Freq. | % | SIC | Industry | Freq. | % |

| 2001 | 568.0 | 23.0 | Argentina | 92.0 | 692.0 | 2 | 13 | Oil & Gas | 1297 | 4.7 |

| 2002 | 90.0 | 3.6 | Bangladesh | 25.0 | 1286.0 | 7 | 20 | Food Products | 1825 | 6.6 |

| 2003 | 122.0 | 4.9 | Bulgaria | 235.0 | 2488.0 | 8.7 | 24 | Paper and paper products | 2926 | 10.6 |

| 2004 | 48.0 | 1.9 | Croatia | 305.0 | 1033.0 | 3.9 | 28 | Chemical Products | 1280 | 4.7 |

| 2005 | 67.0 | 2.7 | Jordan | 134.0 | 1489.0 | 4.4 | 30 | Manufacturing | 13,413 | 48.7 |

| 2006 | 124.0 | 5.0 | Kazakhstan | 15.0 | 174.0 | 1.5 | 37 | Transportation | 314 | 1.1 |

| 2007 | 290.0 | 11.7 | Kenya | 150.0 | 166.0 | 0.4 | 46 | Scientific instruments | 181 | 0.7 |

| 2008 | 395.0 | 16.0 | Kuwait | 91.0 | 1229.0 | 3.9 | 48 | Communications | 1080 | 3.9 |

| 2009 | 180.0 | 7.3 | Mauritius | 38.0 | 387.0 | 1.5 | 50 | Durable goods | 1248 | 4.5 |

| 2010 | 101.0 | 4.1 | Morocco | 143.0 | 281.0 | 0.9 | 58 | Eating and drinking establishments | 3883 | 14.1 |

| 2011 | 135.0 | 5.5 | Nigeria | 5.0 | 1221.0 | 3.7 | 80 | Health | 102 | 0.4 |

| 2012 | 76.0 | 3.1 | Oman | 18.0 | 940.0 | 2.6 | ||||

| 2013 | 54.0 | 2.2 | Pakistan | 82.0 | 3510.0 | 9.2 | ||||

| 2014 | 40.0 | 1.6 | Romania | 57.0 | 3241.0 | 11.9 | ||||

| 2015 | 53.0 | 2.1 | Serbia | 158.0 | 4221.0 | 18.7 | ||||

| 2016 | 81.0 | 3.3 | Slovenia | 92.0 | 115.0 | 0.4 | ||||

| 2017 | 51.0 | 2.1 | Sri Lanka | 271.0 | 2840.0 | 7.9 | ||||

| Tunisia | 370.0 | 78.0 | 0.4 | |||||||

| Vietnam | 608.0 | 2158.0 | 11.1 | |||||||

| Total | 2475 | 100 | Total | 2475 | 27,549 | 100 | Total | 27,549 | 100 | |

| AEM | REM | CompScore | Size | BM | ROA | |ROA| | LEV | OpCycle | CFOA | |CFOA| | RET | Analyst | BigN | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Mean | 0.089 | 0.247 | 0.632 | 16.762 | 2.452 | 0.045 | 0.085 | 0.482 | 58,834 | 0.046 | 0.105 | −98.89 | 1.777 | 0.328 |

| Std. Dev | 0.110 | 0.341 | 1.116 | 2.145 | 24.259 | 0.262 | 0.252 | 0.428 | 1,416,160 | 0.527 | 0.519 | 21784 | 1.086 | 0.506 |

| Q1 | 0.023 | 0.057 | 0.142 | 15.478 | 0.520 | 0.000 | 0.018 | 0.246 | 2649 | −0.005 | 0.020 | −9.068 | 0.941 | 0.000 |

| Median | 0.055 | 0.145 | 0.394 | 16.748 | 1.005 | 0.029 | 0.049 | 0.455 | 4895 | 0.033 | 0.061 | 0.000 | 1.279 | 0.000 |

| Q3 | 0.115 | 0.306 | 1.637 | 18.193 | 1.849 | 0.082 | 0.103 | 0.661 | 10,281 | 0.106 | 0.129 | 8.991 | 2.660 | 1.000 |

| 0 AEM | 0REM | 0CompScore | 0SIZE | 0BM | 0ROA | 0LEV | 0OpCycle | 0SD_Sales | 0CFOA | 0RET | 0Analyst | 0Loss | 0BigN | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| AEM | 1 | 0.292 | 0.041 | 0.053 | 0.029 | 0.324 | −0.115 | −0.085 | −0.015 | −0.556 | 0.035 | −0.025 | −0.205 | −0.011 |

| REM | 0.222 | 1 | −0.019 | −0.095 | 0.072 | −0.110 | 0.213 | −0.070 | 0.111 | −0.423 | −0.045 | −0.023 | 0.046 | −0.027 |

| CompScore | 0.015 | −0.011 | 1 | −0.066 | 0.002 | 0.038 | −0.091 | −0.033 | −0.098 | −0.005 | −0.023 | 0.367 | −0.172 | −0.254 |

| SIZE | 0.061 | −0.041 | −0.069 | 1 | −0.406 | 0.383 | 0.012 | 0.129 | 0.606 | 0.297 | 0.145 | −0.325 | −0.207 | 0.164 |

| BM | 0.005 | −0.002 | −0.00214 | −0.143 | 1 | −0.261 | −0.224 | −0.131 | −0.148 | −0.200 | −0.236 | 0.196 | 0.053 | −0.065 |

| ROA | 0.259 | 0.015 | 0.005 | 0.131 | −0.003 | 1 | −0.191 | 0.177 | 0.203 | 0.437 | 0.225 | −0.246 | −0.518 | 0.087 |

| LEV | −0.111 | 0.109 | −0.073 | −0.043 | −0.043 | −0.097 | 1 | −0.0207 | 0.342 | −0.057 | -0.010 | −0.207 | 0.082 | 0.032 |

| OperCycle | 0.008 | 0.002 | −0.0109 | 0.006 | 0.000 | 0.006 | 0.000 | 1 | 0.108 | 0.244 | 0.075 | −0.122 | −0.055 | 0.075 |

| SD_Sales | −0.022 | 0.0112 | −0.092 | 0.284 | −0.018 | 0.030 | 0.073 | −0.00378 | 1 | 0.161 | 0.086 | −0.323 | −0.125 | 0.127 |

| CFOA | −0.234 | −0.145 | −0.003 | 0.069 | −0.004 | −0.124 | −0.0146 | 0.002 | 0.0153 | 1 | 0.128 | −0.169 | −0.201 | 0.093 |

| RET | −0.004 | 0.008 | −0.0102 | 0.028 | −0.002 | 0.001 | −0.002 | −0.001 | 0.0015 | 0.0018 | 1 | −0.061 | −0.074 | 0.014 |

| Analyst | −0.018 | −0.003 | 0.475 | −0.257 | 0.037 | −0.047 | −0.022 | −0.0124 | −0.067 | −0.036 | −0.0028 | 1 | −0.003 | −0.199 |

| Loss | −0.250 | 0.004 | −0.275 | −0.301 | −0.008 | −0.273 | 0.151 | −0.00838 | −0.062 | −0.047 | 0.0009 | −0.113 | 1 | 0.061 |

| BigN | −0.004 | −0.022 | −0.310 | 0.168 | −0.018 | 0.013 | 0.017 | −0.00840 | 0.066 | 0.020 | 0.00133 | −0.271 | 0.121 | 1 |

| Pooled OLS | Fixed Effects | Between Effects | Quantile | |||||

|---|---|---|---|---|---|---|---|---|

| AEM | REM | AEM | REM | AEM | REM | AEM | REM | |

| CompScore | −0.002 *** | 0.002 | −0.002 * | 0.002 | −0.002 * | 0.007 | −0.002 * | 0.003 |

| (−3.99) | (0.79) | (−2.45) | (0.73) | (−2.11) | (1.36) | (−2.39) | (1.75) | |

| Size | −0.003 *** | −0.010 *** | 0.006 ** | 0.013 * | −0.004 *** | −0.018 ** | −0.001 | −0.001 |

| (−4.12) | (−3.64) | (2.62) | (2.00) | (−3.75) | (−3.20) | (−1.13) | (−0.51) | |

| BM | 0.000 | −0.001 | 0.001 ** | 0.002 * | −0.000 | −0.007 * | 0.000 | −0.001 |

| (0.54) | (−0.97) | (2.91) | (2.42) | (−0.15) | (−2.32) | (0.80) | (−1.03) | |

| ROA | −0.253 *** | −0.071 | −0.222 *** | −0.048 | −0.329 *** | −0.085 | −0.292 *** | 0.041 |

| (−16.36) | (−1.23) | (−13.05) | (−0.95) | (−10.65) | (−0.57) | (−17.42) | (1.08) | |

| |ROA| | 0.288 *** | 0.172 ** | 0.257 *** | 0.157 ** | 0.367 *** | 0.110 | 0.334 *** | 0.046 |

| (18.65) | (2.97) | (15.00) | (3.06) | (12.19) | (0.74) | (19.91) | (1.21) | |

| LEV | 0.019 *** | 0.130 *** | 0.018 * | 0.085 *** | 0.010 | 0.085 * | 0.015 ** | 0.074 *** |

| (4.14) | (7.62) | (2.16) | (3.44) | (1.35) | (2.47) | (3.00) | (6.62) | |

| BigN | −0.028 *** | −0.120 *** | 0.000 | 0.000 | −0.023 *** | −0.074 * | −0.015 ** | −0.046 *** |

| (−5.90) | (−7.04) | (0.00) | (0.00) | (−3.50) | (−2.34) | (−2.87) | (−4.10) | |

| CFOA | 0.054 *** | 0.137 *** | 0.055 *** | 0.054 ** | 0.032 * | 0.194 ** | −0.233 *** | 0.009 |

| (9.29) | (6.53) | (8.29) | (2.86) | (2.33) | (3.05) | (−36.84) | (0.62) | |

| |CFOA| | 0.086 *** | 0.192 *** | 0.082 *** | 0.100 *** | 0.129 *** | 0.332 *** | 0.444 *** | 0.595 *** |

| (13.81) | (8.53) | (11.66) | (4.96) | (8.36) | (4.64) | (65.72) | (40.28) | |

| Loss | −0.026 *** | −0.052 *** | −0.021 *** | −0.012 | −0.046 *** | −0.101 ** | −0.016 *** | −0.020 * |

| (−6.37) | (−3.42) | (−4.46) | (−0.85) | (−5.75) | (−2.66) | (−3.55) | (−2.01) | |

| RET | 0.002 ** | 0.000 | 0.002 * | 0.004 | 0.000 | −0.003 | 0.001 | 0.002 |

| (2.94) | (0.24) | (2.30) | (1.19) | (0.21) | (−0.56) | (1.46) | (1.10) | |

| Intercept | 3.232 | −11.688 | −18.989 | −9.706 | 14.687 | −44.985 | −12.823 | −17.299 |

| (1.34) | (−1.01) | (−1.52) | (−0.28) | (0.96) | (−0.51) | (−0.95) | (−0.59) | |

| Industry | Included | Included | Included | Included | Included | Included | Included | Included |

| Year | Included | Included | Included | Included | Included | Included | Included | Included |

| Observations | 12026 | 11600 | 12026 | 11600 | 12026 | 11600 | 12026 | 11600 |

| Adj R-sq | 0.188 | 0.090 | 0.065 | 0.198 | 0.268 | 0.095 | 0.359 | 0.136 |

| Stage 1 | Stage 2 | |||

|---|---|---|---|---|

| Variable | CompScore | Variable | AEM | REM |

| EM | 0.158 ** | 0.838 *** | ||

| (19.54) | (29.63) | |||

| Std_ROA | −0.189 | Std_ROA | −0.032 * | −0.073 |

| (−1.89) | (−2.25) | (−1.48) | ||

| Size | −0.021 *** | Size | 0.003 *** | −0.005 * |

| (−4.74) | (4.47) | (−2.47) | ||

| BM | −0.001 | BM | 0.000 | 0.000 |

| (−1.57) | (0.02) | (0.27) | ||

| OperCycle | 0.008 | OperCycle | −0.006 *** | −0.015 *** |

| (1.13) | (−5.74) | (−4.61) | ||

| LEV | −0.324 *** | LEV | 0.139 *** | 0.639 *** |

| (−10.84) | (−9.88) | (12.03) | ||

| Intangible | −0.051 | Intangible | −0.010 | −0.028 |

| (−0.97) | (−1.34) | (−0.87) | ||

| CapitalIntensity | −0.265 *** | |||

| (−6.90) | ||||

| Intercept | 2.085 *** | Intercept | 0.080 | 0.916 *** |

| (10.05) | (1.77) | (6.18) | ||

| Industry Dummies | Included | Industry Dummies | Included | Included |

| N | 10511 | N | 10847 | 10343 |

| adj. R-sq | 0.084 | adj. R-sq | 0.073 | 0.126 |

| Pooled OLS | Fixed Effects | Between Effects | ||||

|---|---|---|---|---|---|---|

| AEM | REM | AEM | REM | AEM | REM | |

| L.CompScore | −0.001 * | 0.002 | −0.000 | 0.002 | −0.002 | −0.002 |

| (−2.22) | (0.81) | (−0.62) | (1.15) | (−1.95) | (−0.36) | |

| Size | −0.003 *** | −0.011 *** | 0.005 * | 0.011 | −0.004 ** | −0.019 *** |

| (−3.76) | (−3.70) | (2.11) | (1.61) | (−3.15) | (−3.31) | |

| BM | 0.000 | −0.001 | 0.001 * | 0.002 * | 0.000 | −0.007 * |

| (0.18) | (−1.00) | (2.05) | (2.17) | (0.08) | (−2.39) | |

| ROA | −0.262 *** | −0.069 | −0.223 *** | −0.041 | −0.347 *** | −0.099 |

| (−16.57) | (−1.17) | (−12.55) | (−0.79) | (−11.70) | (−0.68) | |

| |ROA| | 0.294 *** | 0.171 ** | 0.254 *** | 0.150 ** | 0.373 *** | 0.129 |

| (18.55) | (2.89) | (14.24) | (2.86) | (12.90) | (0.91) | |

| LEV | 0.019 *** | 0.123 *** | 0.015 | 0.077 ** | 0.012 | 0.081 * |

| (4.07) | (6.94) | (1.75) | (3.01) | (1.68) | (2.34) | |

| BigN | −0.024 *** | −0.122 *** | 0.000 | 0.000 | −0.024 *** | −0.071 * |

| (−5.06) | (−6.83) | (0.00) | (0.00) | (−3.61) | (−2.17) | |

| CFOA | 0.052 *** | 0.139 *** | 0.050 *** | 0.050 * | 0.043 ** | 0.188 ** |

| (8.55) | (6.20) | (7.11) | (2.43) | (3.18) | (2.94) | |

| |CFOA| | 0.083 *** | 0.188 *** | 0.076 *** | 0.091 *** | 0.134 *** | 0.308 *** |

| (12.66) | (7.87) | (10.17) | (4.20) | (8.88) | (4.34) | |

| Loss | −0.025 *** | −0.051 ** | −0.021 *** | −0.009 | −0.041 *** | −0.109 ** |

| (−6.11) | (−3.22) | (−4.41) | (−0.64) | (−5.27) | (−2.88) | |

| RET | 0.002 ** | −0.001 | 0.003 ** | 0.004 | 0.000 | −0.004 |

| (2.95) | (−0.25) | (2.94) | (1.40) | (0.13) | (−0.92) | |

| Intercept | 21.991 ** | 4.645 | −20.732 | −16.935 | 1.979 | 198.921 |

| (3.06) | (0.14) | (−1.70) | (−0.48) | (0.04) | (0.62) | |

| Industry | Included | Included | Included | Included | Included | Included |

| Year | Included | Included | Included | Included | Included | Included |

| N | 10960 | 10718 | 10960 | 10718 | 10960 | 10718 |

| Adj R-sq | 0.179 | 0.338 | 0.103 | 0.237 | 0.276 | 0.292 |

| Panel A | Panel B | Panel C | Panel D | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Individual REM Proxies | Small Profit | Small Increase | 2005–2006 | 2007–2009 | Civil | Common | |||||||||

| CFO | DISC | ProdCosts | AEM | REM | AEM | REM | AEM | REM | AEM | REM | AEM | REM | AEM | REM | |

| CompScore | −0.000 | 0.001 * | 0.002 | 0.004 * | −0.007 | 0.003 | 0.006 | −0.001 | 0.003 | −0.007 ** | −0.003 | −0.001 | 0.004 | −0.007 ** | −0.005 |

| (−0.65) | (2.47) | (0.90) | (1.98) | (−0.83) | (1.01) | (0.50) | (−0.87) | (0.85) | (−2.75) | (−0.34) | (−0.89) | (1.10) | (−2.88) | (−0.55) | |

| Size | 0.006 *** | −0.002 * | 0.013 * | 0.007 | 0.007 | −0.017 ** | −0.007 | −0.003 | −0.015 | −0.005 ** | −0.010 | −0.004 *** | −0.013 *** | −0.005 ** | −0.012 * |

| (3.39) | (−2.29) | (2.06) | (1.44) | (0.34) | (−3.13) | (−0.30) | (−0.85) | (−1.16) | (−2.68) | (−1.56) | (−4.28) | (−3.65) | (−2.76) | (−1.97) | |

| BM | 0.001 *** | 0.000 | 0.003 ** | 0.001 | −0.000 | −0.001 | −0.004 | −0.001 * | −0.001 | −0.001 | −0.009 | 0.000 | −0.001 | −0.001 | −0.011 * |

| (3.51) | (0.19) | (3.20) | (1.67) | (−0.18) | (−1.73) | (−0.81) | (−2.04) | (−0.70) | (−0.47) | (−1.76) | (0.84) | (−0.89) | (−0.45) | (−2.08) | |

| ROA | −0.020 | −0.016 * | −0.016 | 1.073 | 6.512 | 0.522 | −2.841 *** | −0.095 | −0.086 | −0.212 *** | 0.086 | −0.245 *** | 0.038 | −0.207 *** | 0.031 |

| (−1.43) | (−1.97) | (−0.33) | (1.24) | (1.96) | (1.75) | (−4.77) | (−1.50) | (−0.64) | (−6.59) | (0.86) | (−14.26) | (0.56) | (−6.48) | (0.28) | |

| |ROA| | 0.018 | 0.028 *** | 0.140 ** | 0.000 | 0.000 | −0.037 | 3.382 *** | 0.325 *** | −0.035 | 0.319 *** | 0.135 | 0.273 *** | 0.070 | 0.315 *** | 0.173 |

| (1.27) | (3.37) | (2.86) | (0.00) | (0.00) | (−0.13) | (6.79) | (5.46) | (−0.28) | (9.91) | (1.33) | (15.89) | (1.04) | (9.84) | (1.56) | |

| LEV | 0.016* | 0.002 | 0.062 ** | 0.025 | 0.161 | 0.098 *** | 0.073 | 0.022 | 0.077 | −0.004 | 0.156 *** | 0.019 *** | 0.135 *** | −0.004 | 0.161 *** |

| (2.27) | (0.60) | (2.62) | (1.06) | (1.56) | (3.34) | (0.63) | (0.91) | (1.00) | (−0.42) | (4.28) | (3.49) | (6.38) | (−0.35) | (4.54) | |

| BigN | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | 0.000 | −0.032 | −0.003 | −0.026 * | −0.135 ** | −0.060 *** | −0.170 *** | −0.026 * | −0.118 ** |

| (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | (0.00) | (−1.59) | (−0.04) | (−2.18) | (−3.11) | (−7.76) | (−5.88) | (−2.25) | (−3.00) | |

| CFOA | 0.213 *** | 0.014 *** | −0.019 | −0.077 * | −0.381 ** | −0.243 *** | −0.477 *** | −0.157 ** | −0.336 * | −0.082 *** | −0.086 | 0.056 *** | 0.103 *** | −0.083 *** | −0.101 |

| (39.13) | (8.29) | (−1.07) | (−2.60) | (−3.13) | (−9.50) | (−4.62) | (−2.73) | (−2.00) | (−5.15) | (−1.71) | (7.96) | (3.95) | (−5.23) | (−1.87) | |

| |CFOA| | 0.251 *** | 0.019 *** | −0.018 | 0.854 *** | 0.937 *** | 0.623 *** | 0.479 *** | 0.303 *** | 0.892 *** | 0.283 *** | 0.562 *** | 0.084 *** | 0.143 *** | 0.287 *** | 0.626 *** |

| (43.58) | (10.43) | (−0.92) | (21.90) | (5.76) | (19.90) | (3.77) | (3.91) | (4.98) | (14.55) | (9.13) | (11.18) | (5.15) | (14.89) | (9.39) | |

| Loss | −0.002 | −0.006 * | −0.008 | 0.004 | −0.174 | 0.012 | −0.125 | −0.026 * | −0.115 ** | −0.020 * | −0.004 | −0.022 *** | −0.054 ** | −0.020 * | −0.027 |

| (−0.47) | (−2.57) | (−0.56) | (0.12) | (−1.19) | (0.66) | (−1.80) | (−1.97) | (−2.80) | (−2.12) | (−0.12) | (−4.70) | (−3.05) | (−2.08) | (−0.82) | |

| RET | 0.001 | 0.001 * | 0.003 | −0.002 | 0.001 | 0.000 | −0.011 | −0.000 | −0.002 | 0.003 * | 0.002 | 0.003 *** | 0.005 | 0.003 * | 0.004 |

| (0.90) | (2.48) | (0.91) | (−0.87) | (0.13) | (0.15) | (−1.34) | (−0.30) | (−0.25) | (2.34) | (0.51) | (3.77) | (1.75) | (2.47) | (0.84) | |

| Intercept | −7.463 | −1.062 | 8.205 | 24.728 | −130.239 | −46.596 | 17.482 | 29.927 | 0.568 * | 48.719 * | 13.789 | 7.650 | −22.001 | 45.211 * | 2.418 |

| (−0.73) | (−0.18) | (0.25) | (1.18) | (−1.54) | (−1.90) | (0.18) | (1.58) | (2.42) | (2.36) | (0.22) | (1.59) | (−1.15) | (2.18) | (0.03) | |

| Industry | Included | Included | Included | Included | Included | Included | Included | Included | Included | Included | Included | Included | Included | Included | Included |

| Year | Included | Included | Included | Included | Included | Included | Included | Included | Included | Included | Included | Included | Included | Included | Included |

| N | 10960 | 10960 | 10960 | 1333 | 1308 | 1785 | 1760 | 1382 | 1238 | 2368 | 2322 | 2764 | 2476 | 2862 | 2757 |

| Adj R-sq | 0.141 | 0.183 | 0.204 | 0.026 | 0.097 | 0.073 | 0.132 | 0.392 | 0.104 | 0.103 | 0.34 | 0.179 | 0.086 | 0.454 | 0.153 |

| IFRS Only | No IFRS | |||

|---|---|---|---|---|

| Variable | AEM | REM | AEM | REM |

| CompScore | −0.005 ** | 0.004 | −0.004 | 0.006 |

| (−3.13) | (0.96) | (−1.22) | (0.52) | |

| Size | −0.000 | 0.006 | −0.003 | 0.004 |

| (−0.00) | (0.72) | (−0.65) | (0.24) | |

| BM | 0.001 | 0.003 * | −0.003 | 0.002 |

| (1.81) | (2.48) | (−1.36) | (0.17) | |

| |ROA| | 0.304 *** | 0.093 | 0.054 | 0.600 *** |

| (13.98) | (1.46) | (1.07) | (3.31) | |

| ROA | −0.275 *** | 0.018 | −0.021 | −0.362 * |

| (−12.65) | (0.29) | (-0.45) | (−2.15) | |

| LEV | 0.009 | 0.059 | −0.017 | 0.176 ** |

| (0.76) | (1.75) | (−1.04) | (2.87) | |

| BigN | 0.000 | 0.000 | 0.000 | 0.000 |

| (0.00) | (0.00) | (0.00) | (0.00) | |

| |CFOA| | 0.019 *** | 0.033 *** | 0.380 *** | 0.391 *** |

| (6.54) | (3.83) | (18.06) | (5.06) | |

| Loss | −0.027 *** | 0.011 | 0.007 | −0.079 |

| (−4.83) | (0.68) | (0.64) | (−1.91) | |

| RET | 0.002 | 0.007 | 0.003 | −0.002 |

| (1.91) | (1.84) | (1.25) | (−0.27) | |

| Intercept | −22.914 | 3.998 | −23.432 | −27.772 |

| (−1.48) | (0.09) | (−1.32) | (−0.44) | |

| Industry | Included | Included | Included | Included |

| Year | Included | Included | Included | Included |

| N | 2957 | 2921 | 1812 | 1828 |

| adj. R-sq | −0.085 | −0.208 | −0.054 | −0.293 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2020 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Martens, W.; Yapa, P.W.S.; Safari, M. The Impact of Financial Statement Comparability on Earnings Management: Evidence from Frontier Markets. Int. J. Financial Stud. 2020, 8, 73. https://doi.org/10.3390/ijfs8040073

Martens W, Yapa PWS, Safari M. The Impact of Financial Statement Comparability on Earnings Management: Evidence from Frontier Markets. International Journal of Financial Studies. 2020; 8(4):73. https://doi.org/10.3390/ijfs8040073

Chicago/Turabian StyleMartens, Wil, Prem W. S. Yapa, and Maryam Safari. 2020. "The Impact of Financial Statement Comparability on Earnings Management: Evidence from Frontier Markets" International Journal of Financial Studies 8, no. 4: 73. https://doi.org/10.3390/ijfs8040073