1. Introduction

The banking sectors in the Middle Eastern and North African (MENA henceforth) countries have gone through a fundamental transformation in the past 30 years. Foreign-owned banks have begun to increasingly dominate the MENA banking market. At the same time, financial systems in MENA countries have remained bank-dominated, and banks have become the main source of external financing for the private sector.

Bank profitability and bank stability are the most important targets of bankers and policymakers, particularly in some emerging economies where the stability of the whole economy is nearly dependent on the stability of the banking sector. A well-functioning banking sector is essential for sustainable growth and development in this political and economic part of the world (

Olson and Zoubi 2011). Currently, many banks can utilize social media to access and share information with stakeholders at a minimum cost to improve bank performance (

Ballouk et al. 2022). According to the financial intermediation theory, banking institutions play an intermediary role between savers and borrowers in the economy. Moreover,

Yüksel et al. (

2018) proved the vital role of banks as a catalyst for economic growth. According to

Boubaker et al. (

2022b), the global banking sector must maintain and improve its efficiency during difficult times.

Banks face multiple and complex risks. One of the most serious bank risks is credit risk. Non-performing loans (NPLs

henceforth) are considered financial pollution and exert harmful effects on the level of bank profitability and bank stability. Increasing the level of NPLs poses a great risk to banks, the financial system, and the economy as a whole. Additionally, an increase in loan loss provision is also considered a significant determinant of credit risk (

Kolapo et al. 2012). Moreover, the credit risk that might arise by increasing the level of NPLs on the bank’s balance sheet reveals the occurrence of the banking crisis (

Goswami 2022). The difficulties that borrowers might face due to the unwillingness to pay back their loans led to a progressive deterioration in credit quality and, thus, a significant increase in credit risk (

Orlando and Pelosi 2020).

To the best of our knowledge, banking literature on the NPLs–profitability relationship is abundant. Several empirical studies concluded that the high-level ratio of NPLs significantly affects the level of bank profitability (

Flamini et al. 2009;

Messai and Jouini 2013;

Ozurumba 2016;

Apergis 2014). A significant part of the literature supports the negative relationship between NPLs and bank profitability (

Manz 2019;

Kjosevski et al. 2019;

Panta 2018). NPLs represent a major challenge for the banking sector, as they reduce the profitability of banks and prevent them from lending to businesses and individuals. Nevertheless, less abundant studies support the negative association or the absence of a significant effect (

Lata 2014).

When reviewing the literature on this topic, we noted that most of the prior studies are based on linear approaches using OLS regression, fixed effect models, random effect models, and dynamic panel data models (

Vithessonthi 2016;

Tölö and Virén 2021;

Kumar et al. 2020). Only a few empirical studies are focused on the possible non-linear relationship (

Bolarinwa et al. 2021;

Merhbene 2021). Although the banking literature on the NPLs–profitability relationship (linear relationship) is well documented, most prior works supported the negative association. However, studies on the level at which the NPL ratio can affect bank profitability are less abundant. To date, no study has investigated both the linear and non-linear relationship between NPLs and bank profitability.

This paper aims to explore the effect of NPLs on bank profitability using a sample of MENA banks over the period from 2005 to 2020. The first step consists of checking the effect of NPLs on bank profitability using the system generalized method of moments (SGMM

henceforth) approach. The second step refers to defining an optimal threshold for NPLs using the panel smooth transition regression (PSTR

henceforth) model developed by

González et al. (

2005). The MENA region can be considered an appropriate case study for several reasons. The financial system of this region is a bank-centric financial system, despite the numerous reforms undertaken to establish a market-based financial system. Banks still play a dominant role in financing economic activities. They continue to collect their resources in the form of deposits and grant credit to their clients. However, these traditional activities carry risks that can destabilize banks. Consequently, the government budget deficit in the MENA region expanded to 10.1% of the region’s GDP in 2020, compared to 3.8% in 2009 (

IMF 2021).

North African banks operate in a highly concentrated banking sector market with a low level of profitability and a high level of NPLs, but they continue to show strong resilience. For example, in 2016, the level of NPLs in Algeria increased to 11.4% due to the fall in hydrocarbon prices, resulting in deterioration for public-sector enterprises. In Tunisia, the level of NPLs is still high, with around 50% of NPLs concerned with the industrial and tourism sectors. However, some North African countries made improvements in the provisioning of credit risk. For example, the loan loss provision rate in Egypt was close to 100% (

Azzabi et al. 2018). The banking sector in the MENA region comprises two categories of banks, conventional and Islamic banks. Islamic banks dominate in GCC countries, while most banks in North African countries are conventional. The banking sector in GCC countries is more stable and developed. Thus, the levels of NPLs in GCC countries are lower than in North African countries (

Hakimi et al. 2020).

Since there are a few studies that investigated the NPLs–profitability non-linear relationship, this paper comes to fill this gap. Firstly, it investigates the effect of NPLs on bank profitability. Secondly, it defines the optimal threshold of NPLs that affects bank profitability in the MENA region.

This paper contributes to the existing literature in several ways. First, to the best of our knowledge, this is the first paper that simultaneously investigates the linear and non-linear relationship between NPLs and bank profitability in the MENA region. Prior studies have focused on a linear relationship using either the OLS method or GMM regression. In the current study, we investigate both linear and non-linear relationships between NPLs and profitability. Furthermore, defining an optimal threshold of NPLs that affect bank profitability will be very useful for policymakers and bankers to develop appropriate strategies to hedge and manage credit risk. Second, it focuses on a region where banks still play a dominant role in financing economic activities. Additionally, the financial system of this region is a bank-centric financial system, and banks in some countries operate in a highly concentrated baking sector market with a low level of profitability and a high level of NPLs. Hence, defining the threshold of NPLs that might affect bank profitability could be of great importance for banks and policymakers to improve their decision-making and manage their credit risks.

The remainder of this paper is structured as follows: The literature review is given in

Section 2.

Section 3 describes the sample and the empirical strategy.

Section 4 discusses the empirical findings, while

Section 5 concludes and addresses some policy recommendations.

2. Literature Review and Hypotheses Development

There are some early investigations of the determinants of bank profitability (

Short 1979;

Bourke 1989;

Molyneux and Thornton 1992). The existing literature provides the key determinants of profitability, which can be categorized into internal and external determinants. The internal determinants comprise return on assets (ROA) and return on equity (ROE), depending on the bank specifics, such as bank size, liquidity risk, credit risk, capital adequacy, and non-interest income. However, the external determinants of profitability are macroeconomic factors, such as the inflation rate, GDP, and money supply, as well as the financial environment, such as the global financial crisis. Many scholars have established evidence from both developed and developing countries (

Onofrei et al. 2018;

Mirzaei et al. 2013). Firm-level, industry-level, and macroeconomic determinants have been considered in prior studies as the main determinants of bank performance (

Pasiouras and Kosmidou 2007;

Natsir et al. 2019;

Beck et al. 2015). Based on previous literature, bank size, capitalization, NPLs, growth of deposits, and efficiency are the major variables (

Bolarinwa et al. 2019;

Garcia and Guerreiro 2016;

Dietrich and Wanzenried 2011). One of the important factors in banking literature is NPL, which is widely used as one of the determinants of bank profitability. While most of the empirical studies on the NPLs–profitability relationship focused on linear approaches (

Akter and Roy 2017;

Serrano 2021;

Thornton and Di Tommaso 2021;

Ugoani 2016;

Rosenkranz and Lee 2019), a few studies investigated the possible non-linear relationship (

Alqahtani et al. 2022;

Neves et al. 2020;

Kusi et al. 2020).

Boubaker et al. (

2022a) examined the role of bank affiliation in bank efficiency using a fuzzy approach, including bank NPLs as one of the relevant control variables that might affect bank stability.

2.1. The Linear Relationship between NPLs and Bank Profitability

NPLs represent a standard measure for the quality of assets and can be used to mark the onset of a banking crisis (

Reinhart and Rogoff 2011). The higher level of NPLs adversely affects provisioning for doubtful debts and written-off loans that will distress bank profitability. Moreover, NPLs affect banks’ profitability by decreasing revenues and eroding retained earnings (

Kithinji 2010).

The extant literature found a negative effect of NPLs on bank profitability (

Altunbas et al. 2000;

Fan and Shaffer 2004;

Girardone et al. 2004). These findings support the hypothesis proposed by

Berger and DeYoung (

1997) that efficient banks are better at managing their credit risk. In European countries, there is extensive literature regarding NPLs and bank profitability. For example, in the Republic of North Macedonia,

Kjosevski et al. (

2019) found a negative relationship between NPLs and profitability and confirmed the empirical results of

Louzis et al. (

2012). Similarly,

Athanasoglou et al. (

2005) used a dynamic panel data model to examine the impact of credit risk on the profitability of Greek banks. The results revealed a negative and significant impact of credit risk on a bank’s profitability.

Çollaku and Aliu (

2021) studied the impact of NPLs on banks’ profitability in Kosovo over the period 2010–2019 by using multiple linear regression. The results showed that the effect of NPLs on profitability is significant and negative.

Godlewski (

2005) used ROA as a performance indicator to study the impact of NPLs on bank profitability in Spain and found that there is a negative relationship between ROA and NPLs.

Louzis et al. (

2012) formulated the bad management hypothesis, demonstrating the negative relation between a bank’s profitability and NPLs.

In the USA,

Ghosh (

2015) studied 50 banks over the period of 1984–2013 and confirmed the negative impact of NPLs on the level of banks’ profitability. In Asia,

Swandewi and Purnawati (

2021) examined the impact of NPLs on ROA and the capital adequacy ratios for 24 Indonesian banks. The authors found that both ROA and the capital adequacy ratio have a significant and negative relationship with NPLs. Moreover,

Kaaya and Pastory (

2013) investigated the relationship between credit risk and bank performance (measured by ROA) and found a negative relationship.

Banker et al. (

2010), by using a panel dataset for 14 Korean commercial banks, found that NPLs have a negative impact on bank profitability.

Vinh (

2017) examined the impact of NPLs on the profitability of 34 Vietnamese commercial banks; the results suggested that NPLs exert a negative effect on banks’ profitability. Recently,

Naili and Lahrichi (

2022) examined the determinants of NPLs for 53 banks in the MENA region over the period of 2000–2019 and found that bank performance is more sensitive to an increase in NPLs. The results confirm the bad management hypothesis, which suggests that low profitability indicates poor management skills concerning lending strategies. Thus, increasing their risk exposure which may be achieved, at the expense of higher future NPLs.

Foos et al. (

2010) described credit growth in their study as the most critical driver of bank profitability and found a negative correlation between credit growth and both interest income and risk-adjusted interest income. Concerning NPLs, the expectation is that higher NPLs are associated with lower bank profitability because, when loan losses materialize, banks will lose the interest income associated with the loan category. Based on the prior literature we propose the hypotheses as follows:

H1. A higher level of NPLs is associated with a lower level of bank profitability.

2.2. The Non-Linear Relationship between NPLs and Bank Profitability

While prior studies on the NPLs–profitability nexus were dedicated to the bank performance, many studies examined the relationship between NPLs and profitability in emerging markets based on a linear approach (

Albulescu 2015;

Laryea et al. 2016;

Kumar et al. 2018;

Kohlscheen et al. 2018;

Koju et al. 2018), but only a few examined the non-linear relationship. For instance,

Bolarinwa et al. (

2021) examined the threshold effect on NPLs–profitability within the Nigerian banking sector using a dynamic panel threshold adopted by

Seo et al. (

2019). Their findings showed that there is a threshold for NPLs of 3.5% and 5% for ROA and ROE, respectively.

Rahbar and Soufiani (

2021) used the PSTR model to test the impact of bank-specific factors on NPLs for 10 Iranian banks. The sample banks were categorized as bad banks if the interest spread was below 1% and good banks if the interest spread exceeded 1%.

Pop et al. (

2018) used a non-linear PSTR model to investigate the level of liquidity risk that affects the level of the NPL ratio in seven emerging European countries. They determined the threshold for liquidity of 94.98% for both low-liquid banks and high-liquid banks.

Ben Ali et al. (

2020) documented the effect of corruption on the occurrence of a banking crisis by using a threshold regression approach. The results reveal that corruption negatively affects the banks’ lending through excessive risk rather than through their profitability.

Elekdag et al. (

2020) explored the determinants of profitability across large Euro-area banks by using an approach based on conditional probability distributions. Interestingly, they found that the most reliable determinant of bank profitability is real GDP growth and NPLs. As explained by the scenario with higher growth and lower NPLs, the joint materialization of higher growth and lower NPLs reduces the probability of ROE falling below 8% more than these shocks reflecting nonlinear interaction. The theoretical framework of the non-linear relationship between NPLs and bank profitability is based on the study of

Seo et al. (

2019), which found that the relationship between NPLs and bank profitability is non-linear, and they defined an optimal threshold. Therefore, we propose hypothesis 2 as follows:

H2. There is a threshold effect in the NPLs–profitability relationship.

5. Concluding Remarks and Policy Recommendations

This study aims to investigate both linear and non-linear relationships between NPLs and bank profitability across the MENA region. The study uses a sample of 74 banks located in 11 MENA countries over the 2005–2020 period, with an empirical strategy based on the SGMM regression and PSTR model.

Overall, the empirical findings of SGMM regression reveal that the level of NPLs is significantly and negatively associated with bank profitability. Regarding the effect of bank size, we found a positive and significant relationship with bank profitability. Moreover, for industry specifications, we found that the effect of the bank concentration in the MENA countries is negative and significant. Regarding the effect of the macroeconomic and financial environment, we found that the effect of the global financial crisis is negative and significant. Not surprisingly, the relationship between GDP and bank profitability is positive and significant, while the inflation rate exerts a negative impact on bank profitability.

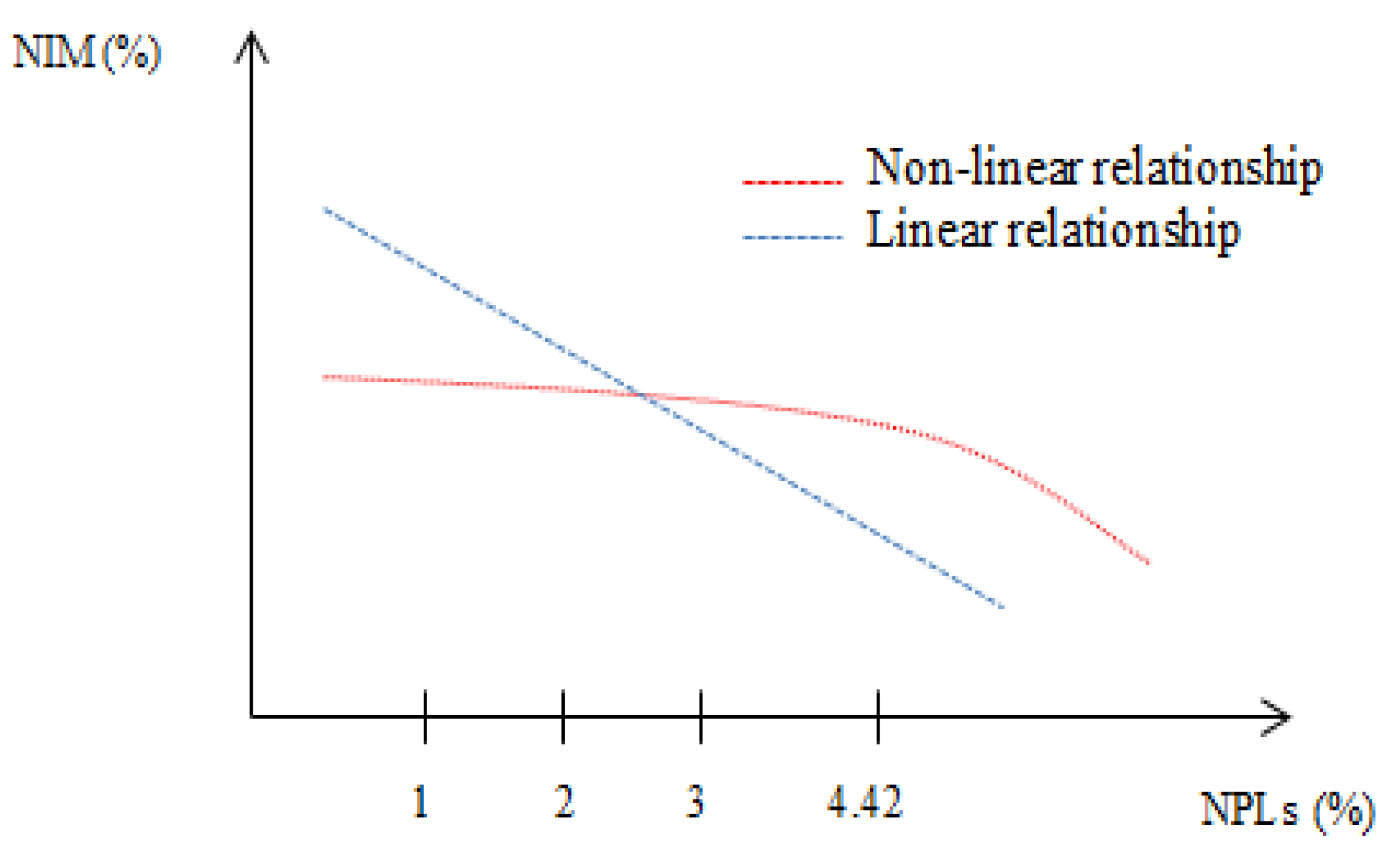

The empirical findings of a non-linear relationship based on the PSTR model confirm the existence of a threshold effect. We found that below the threshold of 4.42%, the effect of NPLs is negative but insignificant, while on surpassing this threshold, the effect becomes negative and significant. Like the SGMM results, we found that the effect of bank size is positive and significant, while bank concentration decreases bank profitability. For the effect of macroeconomic conditions, only GDP growth exerts a significant effect. The inflation rate was found to be without any significant impact.

The findings of this research have substantial implications. Firstly, by identifying these thresholds, policymakers and bankers will address appropriate interventions to adjust their credit policies. To improve their profitability, banks in this region are invited to maintain their ratios of NPLs below the defined threshold of 4.42%. Secondly, economic and fiscal policies should be directed toward creating an environment that will empower economic growth. Hence, the main factors that increase NPLs are liquidity risk and bank size as internal factors and GDP growth, inflation, and unemployment as external factors. Therefore, the regulators should pay more attention to stabilizing macroeconomic conditions. Finally, central banks are also invited to monitor banks in this region, especially large banks with high liquidity risk.

This study has some limitations regarding the regression of the whole sample, which includes banks from the Middle East and North Africa. There are several social, economic, and financial differences between the two groups of countries. In addition, to measure bank profitability, this study used the NIM. While NIM is a common measure of financial performance, especially for banks that make money from the spread between loans and deposits, it does not capture the impact on profitability from provisions to loan-loss reserves.

In future research, decomposing the whole sample into two sub-samples could improve the results of this paper. We check whether the threshold of NPLs affecting bank profitability differs across the two groups of countries or whether it remains equal to 4.42% for both banks in the Middle East and North Africa. Additionally, instead of the NIM, we will use broader measures of profitability such as ROE and ROA that seem more appropriate measures of profitability given the research questions.

{kind=link}