Optimal Timing Strategies in the Evolutionary Dynamics of Competitive Supply Chains

College of Business, Hankuk University of Foreign Studies, 107, Imun-ro, Dongdaemun-gu, Seoul 02450, Republic of Korea

Systems 2024, 12(4), 114; https://doi.org/10.3390/systems12040114

Submission received: 18 February 2024

/

Revised: 21 March 2024

/

Accepted: 25 March 2024

/

Published: 28 March 2024

(This article belongs to the Section Supply Chain Management)

Abstract

:This study investigates the dynamics of endogenous order placement timing among competing retailers within a single period, driven by the evolution of demand-forecast information. Despite the critical role of accurate market trends and demand forecasts in determining firm success during selling seasons, the existing literature lacks a comprehensive understanding of how firms strategically adjust their order timing with imperfect and evolving information landscapes. By leveraging resources such as predictive analytics systems operated by big data and social media, firms tend to enhance their market demand precision as the selling season approaches, aligning with market practices. With this background, we aim to address the strategic behaviors of competing retailers in timing their orders, filling the aforementioned research gap. We construct a non-cooperative game-theoretical model to analyze the strategic behaviors of competing retailers in timing their orders. The model incorporates factors such as imperfect and evolving information landscapes, considering how firms leverage resources to enhance their market demand precision as the selling season approaches. Our analysis shows two primary equilibria, each shedding light on distinct strategic choices and their implications. First, the better-informed firm decides to execute early orders, capitalizing on the first mover’s advantage, particularly when initial information imprecision exceeds a specific threshold. Conversely, a second equilibrium emerges when the better-informed firm delays its orders, yielding the first mover’s advantage to the less-informed competitor. These equilibria highlight the correlation between order timing strategies and the trajectory of information evolution within the competitive landscape. Additionally, our study extends beyond equilibrium analysis to investigate these strategic choices on supply-chain performance.

1. Introduction

Competing firms’ profitability is essentially dependent on the ability to determine the preferences of customers and satisfies customer demand in a timely manner such as in the fashion and apparel industries [1]. However, estimating accurate market demand information and matching supply and demand well in advance of the selling season in these industries is challenging due to unpredictable nature of customer preferences, short selling seasons, and long production and delivery lead times. The demand for clothing in the retail industry changes according to shifts in consumer preferences, which are influenced by fashion trends and seasonal changes [2]. So, companies may struggle to keep pace with trends and introduce products to the market as promptly as their rivals, leading to a negative impact on their sales [3]. Typically, companies encounter inaccurate initial market demand data long before the selling season begins, but this imprecision tends to diminish as the selling season approaches [4]. While some firms rely on secondary data sources like social media to predict market trends, they generally achieve greater accuracy in gauging market demand as the selling season approaches by gathering data from diverse sources. Consequently, companies aspiring to take the lead in the market allocate significant portions of their costs to market research, aiming to enhance the precision of demand forecasting. Many firms adopt a predictive analytics system based on big data and social media information collected inside and outside the company. By doing so, they promote future trends through demand analysis and establish new product development processes [5,6].

Competing firms could have different strategies about the order placement timing depending on the market demand information they receive in advance and the certainty of the demand when the selling season approaches. Various models consider the order placement with imperfect demand-forecast information and noise in early periods or order commitment decisions made after resolving information imprecision [7,8]. In a competitive market, an early order strategy enables the retailer to gain a first-mover advantage akin to a Stackelberg leader for improved profitability and market share compared to competitors [9], despite a certain degree of market noise. In spite of being a market follower, the delayed order strategy may provide different advantages in better matching market demand and supply. Building upon the aforementioned factors, this study explores the equilibrium of endogenously timed order placements within a single period, considering imperfect demand forecasting and the evolution of information with non-cooperative game-theoretic framework. We consider a supply chain comprising two distinct retailers characterized by information asymmetry, with different slopes of information evolution contingent upon the performance of predictive analytics systems. Within the context of a competitive market characterized by demand uncertainty, each retailer independently determines the timing of their order placements. We define this autonomy in decision making as endogeneity in order placements. Our analysis reveals that the timing and quantity of orders from each firm result in distinct equilibria, influenced by the degree of noise and the slope of information evolution. The uniqueness of our model lies in its consideration of order timing dynamics among competing retailers, each experiencing distinct rates of information evolution. Importantly, all retailers are presumed to retain full control over their order timing, regardless of the quality of information they have.

This paper explores the asymmetric imperfect information and information evolution model with two competing retailers. In the context of an asymmetric and imperfect information model, the better-informed firm holds a more comprehensive understanding compared to the less-informed competitor, although the better-informed firm is subject to degree of uncertainty. We extend this baseline model using the information evolution concept. The two firms have different information evolution slopes (information exploitation) when approaching the selling season. This assumption is reasonable because two competing retailers may experience a predictive analytics system with different performances. We discover the optimal timing decision in equilibrium within these scenarios. Therefore, the research aims to report the following research questions: (a) What are the order timing and quantity in equilibrium for two rival retailers in instances where the demand information of the better-informed firm contains a degree of noise, implying imperfect information? How does this equilibrium differ from the existing literature? (b) Given that the better-informed firm can enhance its understanding of demand by delaying its order, thereby experiencing information evolution, what represents the optimal timing and quantity of orders for the better-informed and the less-informed firms to achieve equilibrium? Additionally, how do the profit functions of firms alter with varying information evolution rates? We conduct a comprehensive analysis, considering all potential scenarios involving three risk-neutral participants in the supply chain: two rival retailers and a sole supplier.

Our findings show two primary equilibria having significant managerial implications. In the first scenario, the better-informed firm opts to place orders early, notwithstanding the presence of some noise in the market demand information. This decision capitalizes on the first mover’s advantage, which persists as long as the level of information imprecision surpasses a certain threshold. Despite potential access to superior information at a later stage, the inherent advantage of being the first mover prevails over other advantages that may arise from postponing order placement within the competitive environment. For the less-informed firm, observing the order placement of the better-informed firm and then utilizing more precise demand information to place an order at the later point is a strategy for profit maximization. Conversely, in the second case, the better-informed firm opts to delay its order placement, thereby ceding the first mover’s advantage to the less-informed counterpart. These contrasting equilibriums underscore the pivotal role of the information evolution slope in determining optimal order timing. When information evolution is sufficiently pronounced within a given period—characterized by initially low-quality information followed by significant enhancement—the better-informed firm delays orders until the point of precision, facilitated by the superior performance of predictive analytics systems. In certain instances, such a strategy of delayed ordering proves effective, particularly when high-performance predictive analytics systems substantially enhance the accuracy of market demand forecasts. However, when information quality faces gradual improvement or remains stagnant due to low performance of the predictive analytics system, the better-informed firm decides to place an order as early as feasible, despite the presence of noise.

Our results also suggest the following practical implications: when the firm receives an early low-quality market signal, the firm obtains the first mover’s advantage but may also wait for more precise market demand information. Hence, a trade-off emerges between seizing the first mover’s advantage upfront and awaiting a more refined demand signal later. While one firm capitalizes on the advantages afforded by possessing more accurate market information, the other firm enjoys the benefits associated with leading the market. However, a firm with low-quality demand information may have the first mover’s disadvantage, similar to the results of [10]. In some cases, the timing of the better-informed firm’s order is less important if a high-performance predictive analytics system exists. In reality, under the highly uncertain demand and competitive environments, firms often struggle to determine the ideal timing for placing orders. The uncertainty and imprecision surrounding initial market demand information make it challenging to have confidence in order timing. Furthermore, as the selling season approaches, firms may gain access to more accurate information. This study aims to provide guidance on the optimal timing of orders between competing companies by addressing these real-world challenges.

The rest of this paper is structured as follows: Section 2 provides a review of the relevant literature. Section 3 introduces the models incorporating imperfect information and information evolution. Section 4 explores a comprehensive examination of the imperfect information model and its equilibrium. Section 5 explores the information evolution model, its equilibriums, and compares the payoff functions of each player. Finally, Section 6 offers our concluding remarks.

2. Literature Review

This work is related to the substantial literature exploring the information considerations with information asymmetry, information updates, and timing of orders in the supply chain as illustrated in Table 1. We mainly focus on three streams of the literature that motivated our research: (i) demand information evolution and updates, (ii) asymmetric and imperfect demand information including horizontal competition, and (iii) endogenous timing of order for competing firms.

The first strand of the literature centers on updates regarding demand information within the supply chain. Ref. [11] investigates the timing of orders by a single manufacturer and supplier, comparing delayed and early commitments while taking into account demand-forecast updates. Their findings illustrate that the preference of each participant hinges upon the degree of resolved demand uncertainty. Ref. [12] explores the demand-forecasting updates model incorporating a periodic review inventory model based on the martingale model of forecast evolution (MMFE). The MMFE framework has been widely employed in forecasting update models [7,8,13]. For instance, ref. [7] analyzes a newsvendor model with forecast evolution utilizing the MMFE concept, delineating the optimal ordering policy in a model featuring a single supplier and retailer. Ref. [8] extends this model to incorporate the evolution of demand forecasts, exploring both multiplicative and additive versions of the MMFE. Ref. [14] shows that preordering in a supply chain significantly impacts sales dynamics by facilitating information updates for retailers and suppliers, allowing for strategic adjustments in pricing and inventory management. Additionally, ref. [15] analyzes the timing of orders by two symmetric retailers relative to the realization of demand uncertainty. An important yet understudied factor in analyzing demand-forecast updates is horizontal competition, especially considering asymmetric firms’ dynamic strategy of order timing for evolutionary demand.

The second stream of the literature is asymmetric and imperfect demand information, including horizontal competition. Asymmetric demand information has been a significant area of research in the supply-chain literature. Ref. [16] examines how information asymmetry between manufacturers and retailers, as well as a manufacturer’s timing decisions regarding sales in light of retailer sales efforts, impact sales timing preferences. He illustrates that both sales efforts and information asymmetry influence the manufacturer’s preference for sales timing. Ref. [17] examines the value of investing in-demand forecasting in a competitive environment with multiple retailers. Their findings suggest that downstream firms, engaged in Cournot competition, tend to overinvest in demand forecasting, leading to inefficiencies and substantial losses. Ref. [18] assesses the implications of demand information asymmetry within a supply chain with a single manufacturer and supplier. They propose a collaborative forecasting scheme where the supplier possesses forecast information ahead of the manufacturer at two distinct time points. Additionally, refs. [19,20] analyze the impacts of asymmetric demand information between manufacturers and retailers, along with manufacturers’ decisions regarding encroachment and quality, and information acquisition. In alignment with the existing literature, our study examines a scenario involving two rival retailers and a shared supplier, incorporating information asymmetry and distinct information evolution slopes. We specifically investigate the strategic order timing of asymmetric retailers in equilibrium, considering variations in demand and the extent of information evolution. For a broader understanding of information update dynamics, including demand and supply information updates and information asymmetry, readers may refer to [21,22].

The academic literature has proposed diverse strategies to better align supply with demand and enhance channel performance. Numerous studies explored the endogenous timing of orders and firms’ strategic conduct. For example, ref. [23] examines the timing of commitments in demand uncertainty, suggesting that a seller may benefit from a contract necessitating early commitment. He illustrates that the selection of commitment timing is contingent upon the extent to which demand uncertainty is resolved. Ref. [24] explores the timing impact of a retailer’s sales efforts on firms’ pricing decisions and investment in equilibrium within a manufacturer–retailer relationship. Scenarios involving both early and delayed commitments are explored, depending on whether the retailer’s sales effort precedes or follows improvements in the quality level of the manufacturer. Ref. [25] analyzes competition between two retailers concerning pricing and service levels, explaining the characterization of both aspects and the timing of service investment decisions. Their findings suggest that investment in services before the realization of demand could be advantageous for competition. Recently, the firm’s innovation capability and timing to the market has been explored. Ref. [26] shows the premium firm’s choice of innovation in launching fashion products affects market position and competition between firms, leading to varied optimal timing decisions based on customer characteristics. Ref. [27] examines how different types of competition (specifically, quantity-based versus price-based) influence a manufacturer’s timing preference when establishing a direct distribution channel. Numerous studies in the literature on operations [15,28,29] and economics [10,30,31,32] have addressed endogenous timing commitments encompassing demand updates, vertical and horizontal competition, outsourcing, and quality efforts, applying a plethora of approaches to enhance supply-chain dynamics.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Table 1.

Summary of research on information considerations.

| Paper | Modeling Technique | No. of Players | Period | Applied Industry | |

|---|---|---|---|---|---|

| Information update and evolution | [11] | Newsvendor model | One manufacturer and one supplier | Two | General |

| [12] | MMFE | One manufacturer and one supplier | Multiple | General | |

| [7] | Newsvendor model with MMFE | One manufacturer and one supplier | Multiple | Toy and fashion | |

| [15] | Nash Game | Two retailers and one supplier | Multiple | General | |

| Asymmetric and imperfect information | [16] | Nash Game | One manufacturer and one supplier | Two | Toy |

| [17] | Cournot Game | One supplier and multiple retailers | 4 periods | General | |

| [18] | Dynamic programming | One manufacturer and one supplier | Multiple | General | |

| [19] | Signaling game | One manufacturer and one supplier | Single | Electronics | |

| Endogenous timing of orders | [23] | Stackelberg game | One manufacturer and one buyer | Two | General |

| [28] | Stackelberg game | One manufacturer and one buyer | Single | General | |

| [24] | Stackelberg and Cournot game | One manufacturer and one retailer | Two | Movie | |

| [25] | Nash Game | Two retailers | Two | Retailing | |

| [29] | Stackelberg and Cournot game | Two retailers and one supplier | Single | Fashion and apparel | |

| [26] | Bertrand game | Two retailers | Single | Fashion |

The effect of demand information is an influential area in current supply-chain research, as it may exert a significant impact on firm profitability. Most previous works have adopted a single manufacturer–retailer setting, fixed sequence of events, symmetric firms’ competition, and perfect information endowment without considering the horizontally competing firms’ differing information endowments and evolution structure. Expanding upon existing research, our study extends the analysis from fixed to endogenous events. We comprehensively examine all potential endogenous actions taken by two rival retailers, one better-informed and the other less-informed. Furthermore, we explore deeper into the strategic retailer’s optimal order timing within the equilibrium by integrating imperfect and evolutionary information.

3. The Model

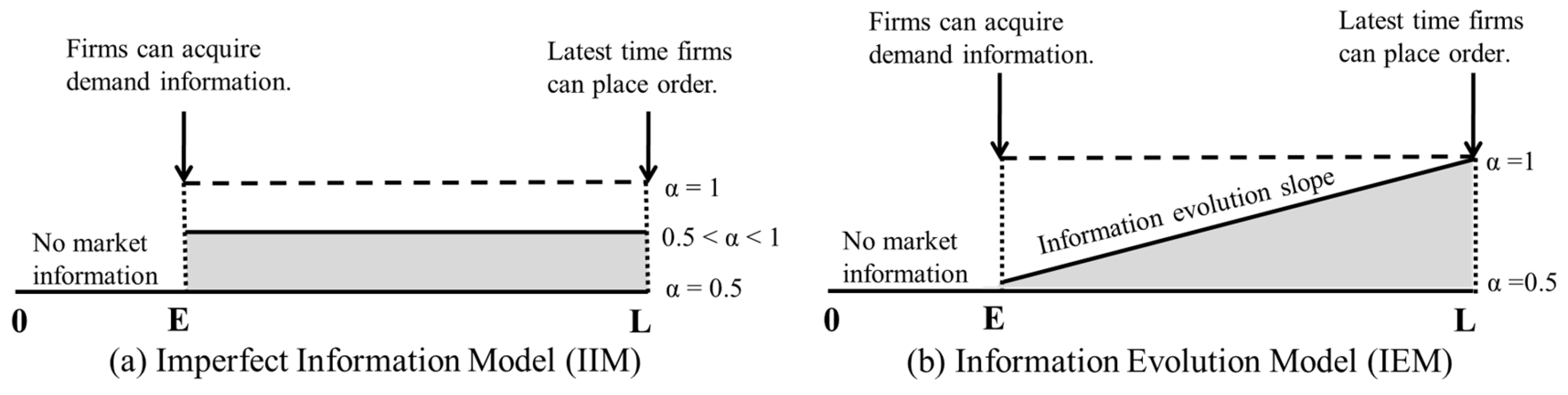

Our model considers the effects of imperfect information and information evolution on competition and order timing. We examine a supply chain comprising two asymmetric retailers sharing a common supplier. Both retailers specialize in producing seasonal products that serve as perfect substitutes. With an uncertain intercept , we assume a linear and downward-sloping demand curve (). The inverse demand curve for each product i is as follows:

where is the quantity of firm i’s product in the market. For analytical simplicity, we introduce uncertainty into the demand intercept , which may have one of two values: represents a high demand state with probability p, while represents a low demand state with probability (1 − p). These probabilities are assumed to be common information among the competing firms. The demand structure essentially captures the effect of demand uncertainty and demand-forecast applications, such as optimistic and pessimistic scenarios [15,29]. The parameter represents the degree of information imprecision, indicating the level of belief accuracy. The better-informed firm possesses certain belief regarding the market demand but lacks precise knowledge; also reflects the private information of demand forecast accuracy 1, observable to competitors through the common supplier by placing orders earlier than the less-informed firm. This scenario is called an imperfect information model (IIM). Furthermore, we explore the scenario where evolves and ultimately converges to near perfection ( by a later order. This scenario is referred to as an information evolution model (IEM). Consequently, in the IEM, if the better-informed firm delays its order, it observes the realization of the random intercept . The mean demand intercept, , is calculated as and is considered to be common knowledge. The demand interval is represented by . It is assumed that all retailers and the supplier are profit maximizers and exhibit risk-neutral behavior.

The informed firms can only obtain imperfect market information at an early time denoted as the Early point. The latest feasible time for order placement, taking into account manufacturing and delivery lead times, is designated as the Later point. Uncertain demand is resolved upon the commencement of the sales season, subsequent to the Later point 2. The better-informed firm may gain early access to market information (at the Early point) through various market research activities. However, given the pre-season timeframe, resources available for acquiring high-quality market information are limited. Consequently, the better-informed firm’s market information remains imperfect and subject to noise (with strictly less than 1). Additionally, we presume that this imprecision evolves along a variable trajectory as the selling season approaches (at the Later point) in the context of the information evolution model (IEM). We also assume that the supplier possesses adequate production capacity. Figure 1 illustrates the timing of events and the information structure for the competing retailers.

The sequence of events unfolds in the following way: Both the better-informed and less-informed firms face two ordering options: the Early point or the Later point. Each firm makes its decision prior to the Early point. Subsequently, the supplier initiates production immediately upon receiving the retailers’ purchase orders and ensures product delivery before the onset of the selling season (post the Later point). At the beginning of the imperfect information model (IIM), only the better-informed firm can acquire market demand information, albeit imperfect. The better-informed firm has a vested interest in disclosing information to the supplier, and their strategic decision making is characterized by an observable commitment [32]. This implies that upon placing a purchase order, the competing firm observes the better-informed firm’s order (based on ) through various channels [33] such as a common supplier or media reports in the market. We can set the wholesale price, w, to zero in both the IIM and IEM without loss of generality. By demonstrating the scenario with a zero-wholesale price, we can trivially establish that the conclusions follow from this assumption.

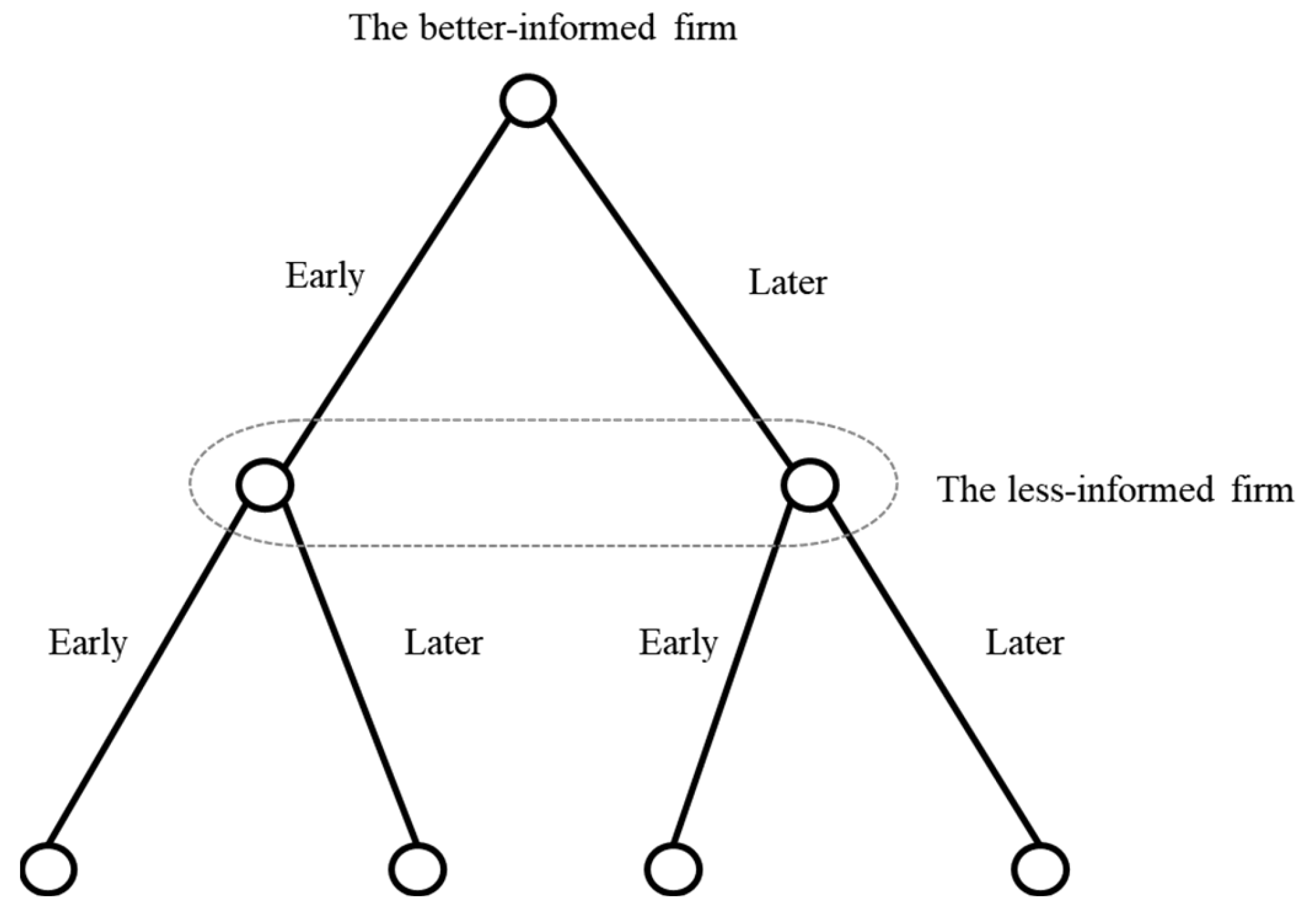

Our model structure can be interpreted as an endogenous sequencing game between the two competing retailers. Once each competitor commits to their order timing, we expect to encounter four distinct scenarios regarding the placement of orders as illustrated in Figure 2, leading to varying quantities based on their information:

Scenario 1: (E, E)–Both firms place orders simultaneously at the Early point.

Scenario 2: (E, L)–At the Early point, the better-informed firm places a purchase order, prompting the supplier to start production upon receipt of the order from the better-informed firm. Subsequently, at the Later point, the less-informed firm places its order, utilizing the information it has observed.

Scenario 3: (L, E)–At the Early point, the less-informed firm submits an order, leveraging common knowledge of μ. The supplier begins production upon receipt of the order from the less-informed firm. Subsequently, at the Later point, the better-informed firm places its order, taking into account the latest demand information.

Scenario 4: (L, L)–Both firms place orders simultaneously at the Later point.

Scenarios 1 (E, E) and 4 (L, L) could be conceptualized as Cournot’s simultaneous move games characterized by imperfect and incomplete information. Scenarios 2 (E, L) and 3 (L, E) can be considered as Stackelberg’s sequential move games. In Scenarios 2, the better-informed firm assumes the role of the Stackelberg leader by entering the market first, followed by the less-informed firm. Conversely, in Scenario 3, the less-informed firm acts as the Stackelberg leader, entering the market first and relying solely on public market information, followed by the better-informed firm. We identify the dominant strategy among the four scenarios for the two firms.

A pivotal aspect of the model lies in its incorporation of a realistic information framework. None of the firms possess perfect market information well before the selling season (prior to the Early point). This information becomes available only as the selling season approaches, particularly within the context of the information evolution model (IEM). We examine an information structure characterized by imperfections and incompleteness, wherein only one firm receives a noisy signal. To evaluate the impact of imperfect and evolving information, we further assume that the less-informed firm possesses solely general market information () throughout the duration of the time horizon. The perfect Bayesian Nash equilibrium is the most suitable equilibrium concept for capturing the dynamics of the game with incomplete and imperfect information.

4. Baseline Model Analysis: The IIM

Suppose that the better-informed firm holds certain beliefs about demand but lacks precise information. To account for this, we introduce the imprecision factor , where This indicates that the better-informed firm’s understanding of true demand is affected by a noise factor . Using Bayes’ theorem [34], we show that , , , . For example, the high-type informed firm’s expected pay-off reads as follows 3:

Lemma 1 explains the equilibrium outcome of the sequential move game under imperfect information; a comprehensive proof is available in Appendix A.

Lemma 1.

(i) The outcome resulting from the subgame-perfect Nash equilibrium (SPNE) in a simultaneous move scenario within the framework of imperfect information is as follows:

(ii) The SPNE outcome for the sequential move game within the framework of imperfect information is as follows:

Our model is an endogenous sequence game with two players. Before analyzing each scenario of the game, we summarize each player’s preferences as follows. If the imprecision factor () exceeds one-half, a low-type better-informed firm consistently opts for the sequential move, placing the order at the Early point. Certain high-type better-informed firms may favor simultaneous ordering at the Later point while withholding information. The less-informed firm favors the sequential move, placing an order at the Later point, within a particular range of p.

We investigate whether four potential timings of orders represent equilibrium outcomes within an imperfect information framework. By defining each player’s belief, we assess whether any unilateral deviation by a player results in increased profitability. A crucial factor in the equilibrium analysis is that even when the better-informed firm receives an imperfect signal at the Early point, its advantage as the first mover remains dominant as long as it possesses superior information compared to the less-informed firm. When the observed market demand information is low, the better-informed firm of the low type strategically opts to disclose its information to the less-informed firm at the earliest possible opportunity. This strategic decision guarantees that the better-informed firm of the low type consistently initiates order at the Early point considering the inherent noise in the information. In contrast, the high-type better-informed firm opts to delay its ordering until the Later point, especially when the observed market demand is high. If the better-informed firm abstains from placing an order at the Early point, the less-informed firm infers a scenario of high demand according to its belief structure, as no action in the signaling game is considered a meaningful action [35]. Consequently, the game evolves into a simultaneous move with complete information, where the pay-off of the better-informed firm of the high type is lower than the initial profit obtained from ordering at the Early point 4. Therefore, in the IIM model, the better-informed firm consistently opts to place orders at the Early point.

The less-informed firm must consider the trade-off between (a) placing simultaneous orders at the Early point without updated market information and (b) opting for the Later point order, thereby ceding the first mover’s advantage to the better-informed competitor. The less-informed firm can obtain demand information by placing orders at the Later point by observing the order of the better-informed firm. We discover that the less-informed firm’s deviation from placing orders at the Early point (and instead placing them at the Later point) becomes profitable upon observing the better-informed firm’s commitment. However, the reverse deviation from the Later point to the Early point does not yield profits. The rationale for this lies in the fact that while the information gained from the Later point orders may be less valuable compared to a scenario with perfect information for the less-informed firm, the presence of an information gap between the two firms remains crucial in establishing equilibrium. Therefore, if the information imprecision parameter exceeds a certain threshold value, the sequential move (E, L) becomes the dominant strategy for the competing firms.

Proposition 1.

In the game characterized by imperfect information and the imprecision parameter α, equilibrium exists for all values of

:

- (i)

- At the Early point, the better-informed firm initiates an order. The quantity of the order is as follows:

- (ii)

- At the Later point, the less-informed firm observes the order of the better-informed firm and then orders at the Later point. Its order quantity is as follows:

- (iii)

- The profits of the two firms are as follows:

5. Extension: Analysis of the IEM

Suppose an early ordering better-informed firm observes a signal with high noise about demand where the level of α is marginally above one-half. The better-informed firm obtains a clearer picture of the demand by delaying its order. As the selling season approaches, the demand signal becomes more accurate, and information imprecision is resolved at the Later point (. This implies that the better-informed firm knows the actual demand by waiting until the Later point. However, its delayed order puts the better-informed firm at a disadvantage, as it acts as a market follower compared to the less-informed firm. The less-informed firm can access the common market and demand information throughout the available order time horizon [E, L]. Therefore, if the less-informed firm also delays placing its order, it will still lack a more accurate demand signal unless it observes the order of the better-informed firm. However, by initiating an order at the Early point, the less-informed firm could seize the first mover’s advantage. The critical aspect in the IEM is that when the demand state is low, the better-informed firm still prefers to place order at the Early point, despite receiving better information later. If it does prefer to order at the Early point, the equilibrium path mirrors that of the IIM. If not, the less-informed firm is unable to adjust its belief structure in instances where the better-informed firm refrains from placing an order at the Early point. Let us suppose that the better-informed firm makes a purchase at the Later point simultaneously with the less-informed firm. In that case, the less-informed firm remains uncertain about whether the demand is high or low. As a result, they engage in a game of simultaneous moves with incomplete information in this scenario.

Lemma 2.

and the expected profits are as follows:

and the expected profits are as follows:

(i) In the IEM, when the better-informed firm initiates its order at the Early point, it conforms with Lemma 1 of the IIM. The resolved imprecision parameter

does not affect the strategy of the better-informed firm that orders at the Early point.

(ii) If both firms place orders at the Later point, the game transitions into a game of simultaneous moves with incomplete information. The SPNE quantities for the two competing firms are as follows:

(iii) If the less-informed firm initiates a purchase order at the Early point, while the better-informed firm opts for the Later point, the game follows a sequential move structure. SPNE quantities for the better-informed and less-informed firms are as follows:

In this section, we investigate whether all possible scenarios regarding the timing of orders are sustainable equilibria in the IEM. By accurately defining the belief structures and considering each firm’s trade-offs, we assess the profitability of unilateral deviations for each player. Given that the sole equilibrium of the IIM entails the better-informed firm ordering at the Early point and the less-informed firm ordering at the Later point (i.e., (E, L)), we initially analyze the (E, L) scenario as the proposed equilibrium and ascertain the profitability of potential deviations for each player.

5.1. The Early Order by the Better-Informed Firm, Followed by the Later Order by the Less-Informed Firm: (E, L)

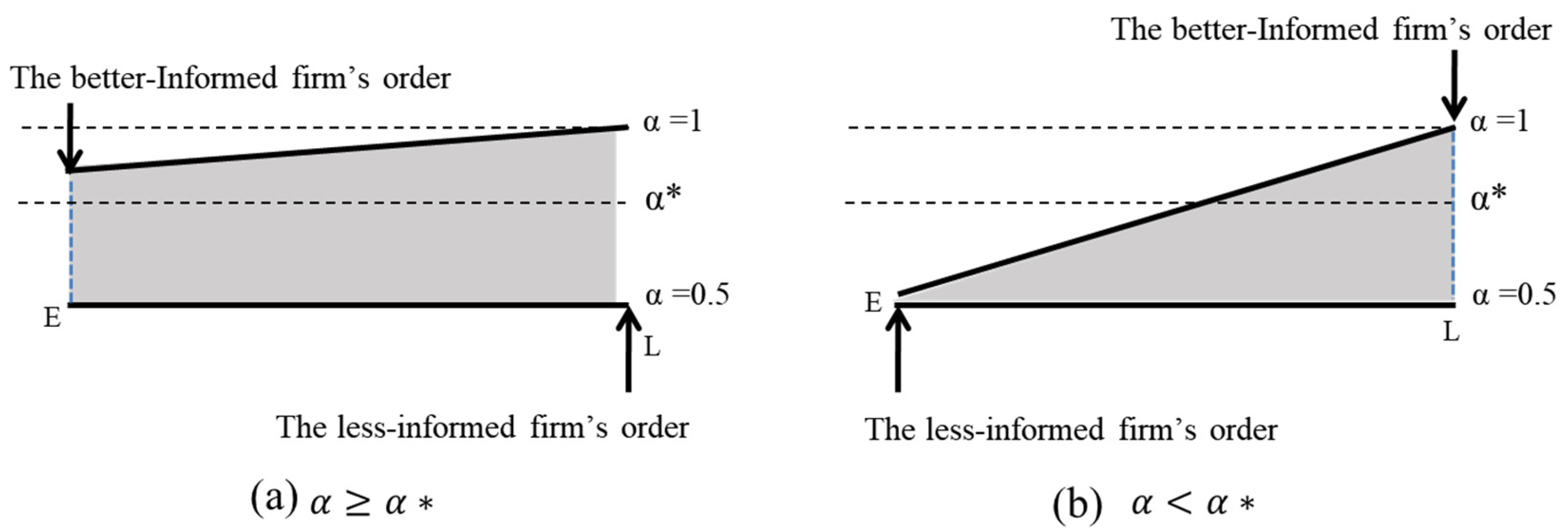

We examine the preference of the better-informed firm concerning the order timing. In the baseline model of IIM, the low-type better-informed firm consistently opts to place its order at the Early point. However, within the framework of the information evolution model, this is not always the case. There exists a critical threshold, denoted as , where the better-informed firm opts to delay its order, even when the demand signal is low, aligning its strategy with that of a better-informed firm with a high demand signal. This threshold, , is discerned by comparing the anticipated profits of the low-type of better-informed firm’s purchase order at the Early point (while the less-informed firm orders at the later point) against the anticipated profits when it delays its order (alongside the less-informed firm). When is equal to or exceeds , the low-type better-informed firm consistently favors early order placement. This critical value can be ascertained through:

For instance, consider the scenario where AH = 30, AL = 10, and p = 0.5. In this case, the threshold is calculated to be 0.87. Similarly, when AH = 50, AL = 10, and p = 0.5, is determined to be 0.95. Hence, when is greater than or equal to , and the better-informed firm opts to shift from the Early point to the Later point, it prompts the less-informed firm to reassess its belief structure, deducing that it indicates a high-demand state. Consequently, the game transitions into a scenario of complete information. Conversely, if is less than , the less-informed firm remains unable to adjust its belief structure due to both high- and low-type better-informed firms favoring late orders. Ultimately, the deviation of the better-informed firm is advantageous below . Thus, it can be concluded that with a threshold value of , the better-informed firm tends to place orders early; conversely, below , it deviates towards the Later point. Employing the same rationale, deviation of the less-informed firm from the Later point to the Early point is deemed non-profitable, given its inability to gather valuable information. Consequently, we verify that the equilibrium of the Early point order of the better-informed firm and the Later point order of the less-informed firm (E, L) holds if exceeds the threshold value ; otherwise, it fails to constitute an equilibrium.

Corollary 1.

If the initial information imprecision factor

is greater than or equal to the certain threshold level

in IEM, the sequential move game of (E, L) holds for the two asymmetric firms. The threshold

represents the point at which the demand signal is low, prompting the better-informed firm to initiate an order at the Early point.

5.2. The Later Order by the Better-Informed Firm, and the Early Order by the Less-Informed Firm: (L, E)

When the less-informed firm opts for an Early point order while the better-informed firm chooses the Later point, the anticipated profits for both firms are outlined in Lemma 2(iii). Upon deviating, the actual profit is explicitly less than the initial profit secured through the Later point ordering when falls below (A detailed proof is provided in Appendix A). This outcome implies that while the less-informed firm does not concede the first mover’s advantage to the competitor, the better-informed firm can only access noisy market information. Furthermore, the less-informed firm’s deviation does not yield profitability. Given its inability to benefit from order postponement, it forfeits the first mover’s advantage 5. Consequently, (L, E) stands as an equilibrium, provided the information imprecision factor remains strictly below the threshold value .

5.3. The Early Order by Both Firms: (E, E)

If two conditions are met, the less-informed firm will transition from the Early point to the Later point: (i) the better-informed firm possesses superior information, and (ii) the better-informed firm opts for an Early point order. Assuming the better-informed firm indeed holds better information and chooses the Early point, deviation of the less-informed firm from the Early point to the Later point consistently proves profitable. The expected profit, in Proposition 1, invariably exceeds the initial profit in Lemma 1(i). Consequently, (E, E) fails to qualify as an equilibrium.

5.4. The Later Order by Both Firms: (L, L)

It is obvious that deviation of the less-informed firm from the Later point to the Early point consistently yields a profit. When such a deviation occurs, the profit maximizing order quantity for the less-informed firm, acting as a Stackelberg leader, stands at , resulting in an expected profit of if the better-informed firm opts for the Later point order. This realized profit consistently surpasses the profit gained from the Later point order (). Hence, this scenario does not constitute an equilibrium. Finally, we deduce that two potential equilibria arise contingent upon the information imprecision factor :

Proposition 2.

Upon reaching a threshold value

, where a low-type informed firm consistently favors ordering at the Early point while the less-informed firm opts for the Later point, the equilibrium is established for α, Ѳ, and p, as outlined below:

Case A.

consistent with its beliefs that:

If ≥

- (i)

- At the Early point, the better-informed firm initiates an order. The quantity of the order is as follows:

- (ii)

- At the Later point, the less-informed firm observes the order of the better-informed firm and then orders. Its order quantity is as follows:

- (iii)

- The profits of both firms are as follows:

Case B.

When < ,

- (i)

- At the Early point, the less-informed firm initiates an order. The quantity of the order is as follows:

- (ii)

- At the Later point, the better-informed firm then orders after acquiring an accurate picture of demand

- (iii)

- The profits of profits of both firms are as follows:

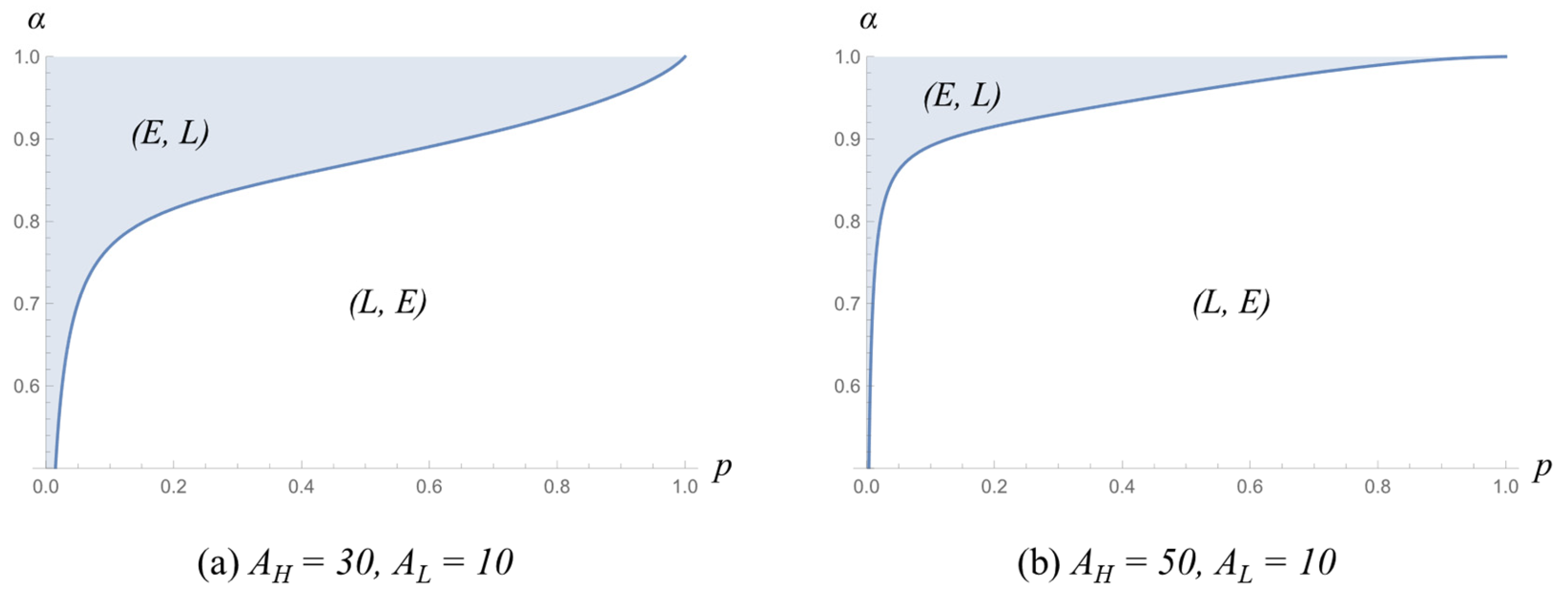

As shown in Figure 3, we identify two significant equilibria with managerial implications. In the first scenario, despite encountering a certain level of noise regarding market demand, the better-informed firm opts to place an order at the Early point. The persistence of the first mover’s advantage for the better-informed firm remains apparent, provided that the information imprecision factor exceeds the threshold level . Even in cases where the better-informed firm may access superior information later, the dominance of the first mover’s advantage outweighs the benefits of delayed ordering within the competitive landscape. Conversely, in the second scenario, the better-informed firm defers its order placement to the Later point, thereby granting the first mover’s advantage to the competitor. These two equilibria underscore the critical importance of retailers’ timing in the ordering process within the equilibrium of information evolution slope. When there is a significant enhancement in the predictive analytics system’s performance within a specific timeframe, enabling a high degree of information evolution, the better-informed firm may opt to delay its order until the information imprecision is resolved. However, in scenarios where the quality of information gradually improves or remains stagnant, the better-informed firm tends to place its order at the Early point, notwithstanding the presence of some degree of noise.

Figure 4 illustrates the two equilibria in the IEM with different parameter values. Recall that p represents the probability of the demand state being high (), where . As the proxy for the demand interval Ѳ (=AH/AL) increases, the region of (L, E) also increases. Hence, when Ѳ is low (AH = 30, AL = 10) in Figure 4a indicating a correspondingly low market potential, the likelihood of the better-informed firm preempting the first mover’s advantage increases. However, if there is even a slight possibility that the market potential is high (AH = 50, AL = 10) in Figure 4b, the right strategy is to delay the order by observing the evolution of information.

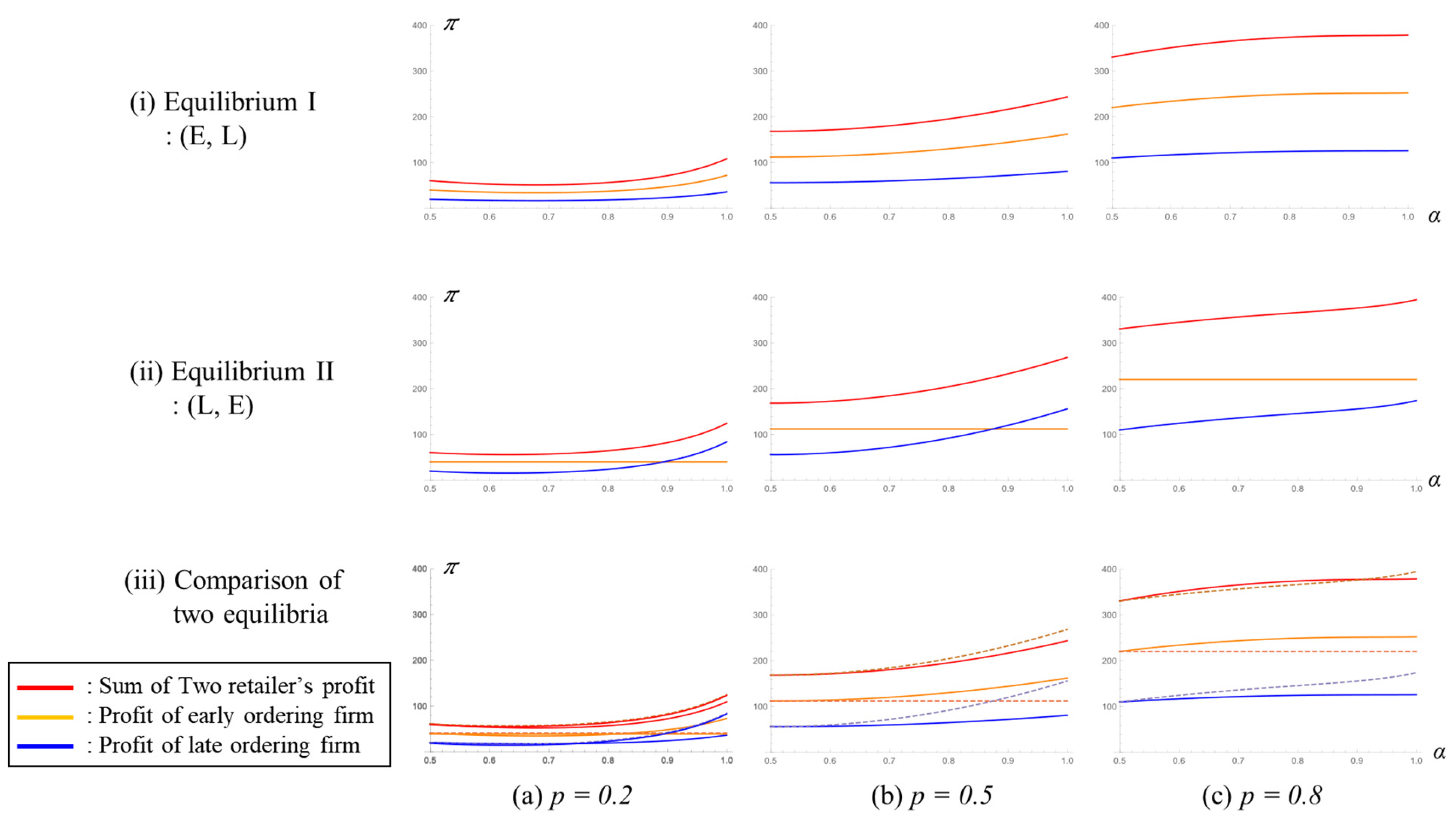

5.5. Supply-Chain Performance with Two Equilibria

We further illustrate the results of the previous section with numerical analysis with overall supply-chain performance. As shown in Figure 5(i), the equilibrium of Case A in Proposition 2 is the traditional Stackelberg leader–follower outcome. The equilibrium in Case B, Figure 5(ii), implies that the less-informed firm gains the first mover’s advantage, even if it only receives publicly available demand information. The better-informed firm orders at the Later point, with a clear picture of the market demand. In the case of a pessimistic market (i.e., (a) p = 0.2) or very high demand uncertainty (i.e., (b) p = 0.5), the second mover’s late order (with improved information) could entail a higher profit than the less-informed firm’s early order (with high parameter α). The sum of the two retailers’ expected payoffs in Case B may be higher than that of Case A due to the high profit of the better-informed firm’s late order. This result has several implications. First, improved demand information, achieved by various market research activities with a predictive analytics system, allows firms to increase profitability even in the presence of competition. However, a firm might fail to achieve the first mover’s advantage. Second, the second mover’s strategy may be efficient as long as high-performance predictive analytics systems substantially improve market demand forecast accuracy. As shown in Figure 4b, the market follower’s profit is higher than that of the leader if the demand uncertainty is high enough; its profit may even be higher than that obtained by the leader of case A equilibrium. Finally, all the graphs in Figure 4 show an upward curve, implying that more accurate demand information, with substantial increases in α, enhance horizontally competing firms’ overall profits.

6. Conclusions

In industries characterized by lengthy production and delivery lead times, such as apparel and fashion, accurately gauging market demand well ahead of the selling season is a significant challenge. Despite employing management practices like Quick Response [36,37] to mitigate information uncertainty, industries with extended lead times struggle to optimize their order timing effectively. Given these circumstances, competing firms may adopt different strategies for order placement timing based on available market demand information. Typically, firms tend to receive more precise market demand information as the selling season becomes closer, sourcing insights from diverse channels. Consequently, it is common for most firms to contend with inaccurate market information early on, with information imprecision often resolving as the selling season approaches. We investigate the equilibrium regarding the timing of order placement within a single period, considering the potential impact of imperfect information and information evolution, employing a game-theoretic approach. Unlike much of the existing literature, which typically assumes that the firm possesses perfect information and that the sequence of events is predetermined, we investigate scenarios where firms lack perfect information, yet one firm maintains an information advantage over the other. Our findings on endogenous sequencing, wherein the better-informed firm opts for early ordering, remain valid under conditions where (i) both firms lack perfect information, provided that one has superior information compared to the other, and (ii) the initially acquired information surpasses a certain threshold of quality, even in the presence of ongoing information evolution. Consequently, the better-informed firm retains the market leader’s advantage, while the less-informed firm can enhance its demand information by delaying its order.

We also illustrate that, under conditions of substantial information evolution influenced by the predictive analytics system’s effectiveness, the less-informed firm tends to place early orders while the better-informed firm delays its orders. When the better-informed firm initially receives low-quality market signals, the less-informed firm seizes the opportunity of being the first mover but may opt to wait for more precise demand information. Hence, a dilemma arises between benefiting from the first mover’s advantage and waiting for a more accurate demand signal. While the better-informed firm gains from enhanced market insights, the less-informed firm capitalizes on its position as the market leader. Furthermore, advancements in demand information gathered through diverse market research practices and predictive analytics empower firms to strengthen their profitability in competitive markets. However, the first mover’s advantage may not always exist, similar to the results of [10]. Moreover, in scenarios where a highly effective predictive analytics system is present, the timing of the better-informed firm’s orders may become less critical. Additionally, we ascertain that a simultaneous move game fails to establish equilibrium in an endogenous sequencing game with diverse information structures.

Our research opens avenues for several potential extensions. While our model primarily explores the dynamics of demand information updates and retailers’ strategic order timing, there remain significant aspects yet to be explored. For instance, considering scenarios where suppliers face constraints in fulfilling retailers’ orders, whether due to capacity limitations, equipment malfunctions, or raw material shortages, can provide insights into how such disruptions influence market equilibrium and the strategies adopted by supply-chain participants. Furthermore, future inquiries could investigate the impacts of emerging technologies like artificial intelligence (AI) and big data on information evolution dynamics. Leveraging these advanced tools may enable supply-chain members to receive and process information more effectively, thereby reshaping their decision-making processes. Exploring optimal ordering strategies for firms in environments enriched by AI and big data represents a promising avenue for further investigation.

Funding

This work was supported by Hankuk University of Foreign Studies Research Fund.

Data Availability Statement

Data sharing is not applicable to this article. No new data were created or analyzed in this study.

Conflicts of Interest

The author declares no conflicts of interest.

Appendix A

Proof of Lemma 1.

where

(i) The payoff functions of two competing firm for the Cournot’s simultaneous move game with imperfect information model are as follows:

Each player’s equilibrium order quantity and pay-off are as noted.

(ii) The payoff functions of two competing firms for the Stackelberg’s sequential move game are:

where

Each player’s equilibrium order quantity and pay-off are as noted. □

Proof of Lemma 2.

(i) The payoff functions of two competing firms for the Cournot’s simultaneous move game at the Later point for information evolution model are the same with Lemma 1(i). The parameter value is improved.

Each player’s equilibrium order quantity and pay-off are as noted.

(iii) The payoff functions for the sequential move game with the Early point order of the less-informed firm and the Later point order of the better-informed firm are:

where

Each player’s equilibrium order quantity and pay-off are as noted. □

Appendix A.1. Equilibrium Analysis of Possible Scenarios

The Later order by the better-informed firm, and the Early order by the less-informed firm: (L, E).

If the better-informed firm deviates from the Later point to the Early point, objective functions of each type of informed firm are as follows:

and optimal order quantity and profits are:

and it is worse off than initial profits in Lemma 2(iii) when is lower than .

Appendix A.2. The Early Order by Both Firms: (E, E)

The initial profit for both players is shown in Lemma 1(i).

If the less-informed firm deviates from the Early point to the Later point, the less-informed firm’s profit functions after deviation are:

The expected profit, is always greater than the initial profit .

| 1 | When , the game becomes a perfect information game. |

| 2 | “The early point” also refers to the point at which a first mover’s advantage can be taken, emphasizing the importance of placing orders before competitors. Achieving a first mover’s advantage over competitor entails setting order timing to the earliest possible moment (the first period in the case of a multiple period model), constituting an equilibrium. Conversely, for obtaining more accurate market information, setting order timing to the latest possible moment (the later point) is optimal, with period N being the optimal timing in an N-period model. |

| 3 | We index a well-informed retailer as the “incumbent (i)”, the less-informed retailer as the “entrant (e)”, and the supplier (s), respectively. High-type and low-type actors are denoted by H and L, respectively. |

| 4 | |

| 5 | If the less-informed firm deviates from the Early point to the Later point, the game transitions into a scenario of simultaneous moves with incomplete information. The anticipated profit for the less-informed firm then equals , indicating a distinct reduction compared to the initial profit. |

References

- Fildes, R.; Ma, S.; Kolassa, S. Retail forecasting: Research and practice. Int. J. Forecast. 2019, 38, 1283–1318. [Google Scholar] [CrossRef]

- Wen, X.; Choi, T.-M.; Chung, S.-H. Fashion retail supply chain management: A review of operational models. Int. J. Prod. Econ. 2019, 207, 34–55. [Google Scholar] [CrossRef]

- GAP Inc. 2020 Annual Report; GAP Inc.: San Francisco, CA, USA, 2020. [Google Scholar]

- Ren, S.; Chan, H.L.; Siqin, T. Demand forecasting in retail operations for fashionable products: Methods, practices, and real case study. Ann. Oper. Res. 2020, 291, 761–777. [Google Scholar] [CrossRef]

- Raguseo, E.; Vitari, C.; Pigni, F. Profiting from big data analytics: The moderating roles of industry concentration and firm size. Int. J. Prod. Econ. 2020, 229, 107758. [Google Scholar] [CrossRef]

- Ghani, N.A.; Hamid, S.; Hashem, I.A.T.; Ahmed, E. Social media big data analytics: A survey. Comput. Hum. Behav. 2019, 101, 417–428. [Google Scholar] [CrossRef]

- Wang, T.; Atasu, A.; Kurtuluş, M. A Multiordering Newsvendor Model with Dynamic Forecast Evolution. Manuf. Serv. Oper. Manag. 2012, 14, 472–484. [Google Scholar] [CrossRef]

- Biçer, I.; Seifert, R.W. Optimal Dynamic Order Scheduling under Capacity Constraints Given Demand-Forecast Evolution. Prod. Oper. Manag. 2017, 26, 2266–2286. [Google Scholar] [CrossRef]

- Suarez, F.; Lanzolla, G. The half-truth of first-mover advantage. Harv. Bus. Rev. 2005, 83, 121–127. [Google Scholar]

- Gal-Or, E. First Mover Disadvantages with Private Information. Rev. Econ. Stud. 1987, 54, 279. [Google Scholar] [CrossRef]

- Ferguson, M.E.; DeCroix, G.A.; Zipkin, P.H. Commitment decisions with partial information updating. Nav. Res. Logist. (NRL) 2005, 52, 780–795. [Google Scholar] [CrossRef]

- Lu, X.; Song, J.-S.; Regan, A. Inventory Planning with Forecast Updates: Approximate Solutions and Cost Error Bounds. Oper. Res. 2006, 54, 1079–1097. [Google Scholar] [CrossRef]

- Ziarnetzky, T.; Mönch, L.; Uzsoy, R. Rolling horizon, multi-product production planning with chance constraints and forecast evolution for wafer fabs. Int. J. Prod. Res. 2018, 56, 6112–6134. [Google Scholar] [CrossRef]

- Shen, B.; Zhang, T.; Xu, X.; Chan, H.; Choi, T. Preordering in luxury fashion: Will additional demand information bring negative effects to the retailer? Decis. Sci. 2022, 53, 681–711. [Google Scholar] [CrossRef]

- Demirag, O.C.; Xue, W.; Wang, J. Retailers’ Order Timing Strategies under Competition and Demand Uncertainty. Omega 2021, 101, 102256. [Google Scholar] [CrossRef]

- Taylor, T.A. Sale Timing in a Supply Chain: When to Sell to the Retailer. Manuf. Serv. Oper. Manag. 2006, 8, 23–42. [Google Scholar] [CrossRef]

- Shin, H.; Tunca, T.I. Do Firms Invest in Forecasting Efficiently? The Effect of Competition on Demand Forecast Investments and Supply Chain Coordination. Oper. Res. 2010, 58, 1592–1610. [Google Scholar] [CrossRef]

- Oh, S.; Özer, Ö. Mechanism Design for Capacity Planning under Dynamic Evolutions of Asymmetric Demand Forecasts. Manag. Sci. 2013, 59, 987–1007. [Google Scholar] [CrossRef]

- Zhang, J.; Li, S.; Zhang, S.; Dai, R. Manufacturer encroachment with quality decision under asymmetric demand information. Eur. J. Oper. Res. 2019, 273, 217–236. [Google Scholar] [CrossRef]

- Chen, J.; Pun, H.; Zhang, Q. Eliminate demand information disadvantage in a supplier encroachment supply chain with information acquisition. Eur. J. Oper. Res. 2023, 305, 659–673. [Google Scholar] [CrossRef]

- Shen, B.; Choi, T.-M.; Minner, S. A review on supply chain contracting with information considerations: Information updating and information asymmetry. Int. J. Prod. Res. 2019, 57, 4898–4936. [Google Scholar] [CrossRef]

- Vosooghidizaji, M.; Taghipour, A.; Canel-Depitre, B. Supply chain coordination under information asymmetry: A review. Int. J. Prod. Res. 2020, 58, 1805–1834. [Google Scholar] [CrossRef]

- Ferguson, M.E. When to commit in a serial supply chain with forecast updating. Nav. Res. Logist. (NRL) 2003, 50, 917–936. [Google Scholar] [CrossRef]

- Liu, B.; Ma, S.; Guan, X.; Xiao, L. Timing of sales commitment in a supply chain with manufacturer-quality and retailer-effort induced demand. Int. J. Prod. Econ. 2018, 195, 249–258. [Google Scholar] [CrossRef]

- Perdikaki, O.; Kostamis, D.; Swaminathan, J.M. Timing of service investments for retailers under competition and demand uncertainty. Eur. J. Oper. Res. 2016, 254, 188–201. [Google Scholar] [CrossRef]

- Zhang, Q.; Chen, J.; Lin, J. Interaction between innovation choice and market-entry timing in a competitive fashion supply chain. Int. J. Prod. Res. 2023, 61, 1606–1623. [Google Scholar] [CrossRef]

- Luo, H.; Niu, B. Impact of competition type on a competitive manufacturer’s preference of decision timing. Int. J. Prod. Econ. 2022, 251, 108548. [Google Scholar] [CrossRef]

- Arcelus, F.J.; Kumar, S.; Srinivasan, G. Pricing, rebate, advertising and ordering policies of a retailer facing price-dependent stochastic demand in newsvendor framework under different risk preferences. Int. Trans. Oper. Res. 2006, 13, 209–227. [Google Scholar] [CrossRef]

- Kim, Y. Retailers’ endogenous sequencing game and information acquisition game in the presence of information leakage. Int. Trans. Oper. Res. 2021, 28, 809–838. [Google Scholar] [CrossRef]

- Mailath, G.J. Endogenous Sequencing of Firm Decisions. J. Econ. Theory 1993, 59, 169–182. [Google Scholar] [CrossRef]

- Tomaru, Y.; Kiyono, K. Endogenous timing in mixed duopoly with increasing marginal costs. J. Institutional Theor. Econ. (JITE)/Z. Gesamte Staatswiss. 2010, 166, 591–613. [Google Scholar] [CrossRef]

- Normann, H.-T. Endogenous Timing with Incomplete Information and with Observable Delay. Games Econ. Behav. 2002, 39, 282–291. [Google Scholar] [CrossRef]

- Song, J.; Yao, D.D. Supply Chain Structures: Coordination, Information and Optimization; Springer Science & Business Media: Berlin/Heidelberg, Germany, 2013; Volume 42. [Google Scholar]

- Efron, B. Bayes’ Theorem in the 21st Century. Science 2013, 340, 1177–1178. [Google Scholar] [CrossRef] [PubMed]

- Gibbons, R.S. Game Theory for Applied Economists; Princeton University Press: Princeton, NJ, USA, 1992. [Google Scholar]

- Cachon, G.P.; Swinney, R. Purchasing, Pricing, and Quick Response in the Presence of Strategic Consumers. Manag. Sci. 2009, 55, 497–511. [Google Scholar] [CrossRef]

- Choi, T. Quick response in fashion supply chains with retailers having boundedly rational managers. Int. Trans. Oper. Res. 2017, 24, 891–905. [Google Scholar] [CrossRef]

Figure 1.

Information structure and timing of events.

Figure 2.

The reduced extensive form of the game.

Figure 3.

Illustration of the two equilibria in the IEM.

Figure 4.

The two equilibria in the IEM with different parameter values.

Figure 5.

Illustration of the two equilibria in the IEM and expected payoff comparison (parameter values: AH = 50, AL = 10. In figure (iii), the solid line represents the (E, L) equilibrium (i), while the dotted line represents the (L, E) equilibrium (ii)).

Figure 5.

Illustration of the two equilibria in the IEM and expected payoff comparison (parameter values: AH = 50, AL = 10. In figure (iii), the solid line represents the (E, L) equilibrium (i), while the dotted line represents the (L, E) equilibrium (ii)).

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the author. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

MDPI and ACS Style

Kim, Y. Optimal Timing Strategies in the Evolutionary Dynamics of Competitive Supply Chains. Systems 2024, 12, 114. https://doi.org/10.3390/systems12040114

AMA Style

Kim Y. Optimal Timing Strategies in the Evolutionary Dynamics of Competitive Supply Chains. Systems. 2024; 12(4):114. https://doi.org/10.3390/systems12040114

Chicago/Turabian StyleKim, Yongjae. 2024. "Optimal Timing Strategies in the Evolutionary Dynamics of Competitive Supply Chains" Systems 12, no. 4: 114. https://doi.org/10.3390/systems12040114

Note that from the first issue of 2016, this journal uses article numbers instead of page numbers. See further details here.