1. Introduction

With the development of the new economy, digitalization has become an essential trend [

1]. Digital transformation (DT) has been used as a tool for countries and industries to obtain competitive advantages [

2,

3]. DT is a fundamental change into a completely new form, function, or structure through the adoption of digital technologies that create new value [

4]. It has been key for companies to remain competitive [

5]. The DT of an enterprise implies changing the way that digital technologies are used to develop new digital business models that contribute toward creating and distributing greater value to the company [

6].

The existing literature has explored the effects of the overall level of DT in firms. The impacts of DT on the financial performance of firms [

7,

8,

9], environmental performance of companies [

10,

11], carbon performance of enterprises [

12], operational efficiency of firms [

13], relationship with innovation in firms [

14,

15], and so on have been examined. Very few scholars have focused on the impacts and mechanisms of DT regarding corporate sustainability [

16]. There are limitations to studying the outcomes of DT in enterprises from a holistic perspective alone [

17]. Therefore, it is particularly critical to focus on the impact of DT in different dimensions on corporate sustainability.

DT includes the optimization and enhancement of existing business operations and internal processes and the innovation of business models to create new business opportunities [

18,

19]. A review of the existing literature reveals that digital transformation is carried out from two main perspectives [

17,

20]. From the perspective of internal activities, digital transformation can facilitate the deep integration of traditional production factors with digital technologies, helping enterprises to optimize existing business processes, reduce costs, and increase productivity. From the perspective of the external environment of enterprises, digital transformation can change their own business models and reshape the ways in which they compete and cooperate with each other [

21]. It is easy to see that the first perspective of digital transformation is more inclined to rely on digital technology to make improvements within the enterprise, and the second perspective of digital transformation is more inclined to make changes to the external market of the enterprise. In this context, this study divides DT into technology- (TDT) and market-based digital transformation (MDT), in order to examine the impact of both dimensions on corporate sustainability.

DT has changed the way in which companies do business [

22,

23], as it requires them to reposition their innovation to address the opportunities and challenges that it brings about [

24]. Therefore, it is crucial to explore how to accelerate the adoption of digital technologies from an innovation perspective [

25]. In recent years, ambidextrous innovation has become an important topic in the field of innovation [

26]. It comprises exploratory innovation, a process in which firms pursue new knowledge and domains to meet the changing needs of the market, and developmental innovation, which builds on existing knowledge and helps to improve the effectiveness of the methods and technologies owned by firms as a means to increase competitiveness [

27,

28]. In this study, the ambidextrous innovation capabilities of firms are used as boundary conditions to explore how they affect the relationship between DT and firm sustainability.

Taking enterprises in the Chinese context as the entry point, this study selects A-share listed companies in China from 2013 to 2021 to explore the impact of different dimensions of DT—that is, TDT and MDT—on enterprise sustainability. From the perspective of corporate innovation, we explore how the level of corporate ambidextrous innovation affects the relationship between different types of DT and corporate sustainable development.

The contributions of this study are as follows. First, it divides DT into TDT and MDT and examines the impact of both on corporate sustainability. The findings validate the research on digital transformation based on resource-based theory and complement the multidimensional research on digital transformation. Second, it uses ambidextrous innovation as a moderating variable to discuss how it affects the relationship among different dimensions of DT and corporate sustainability. The study finds that high levels of both corporate exploratory and exploitative innovation significantly promote the positive influence of different dimensions of DT on corporate sustainability, which supports corporate innovation theory. Finally, the conclusions provide empirical support for business practitioners to develop different types of DT strategies and theoretical references for policymakers to draw a blueprint for the development of DT.

2. Theoretical Background and Hypotheses

In recent times, there has been a great deal of attention paid to how DT contributes to the sustainability of enterprises [

29,

30]. DT uses advanced digital technologies to optimize business and provide internalized growth opportunities, and it enables business transformation to enhance the company’s performance [

31]. Advanced digital technologies are a key element in DT, and digital technologies drive the optimization of internal processes, products, and services and the improvement of business models [

32,

33]. DT stimulates firms to develop new business models and value creation paths that result in major changes in their core processes, services, and products, which can either be endogenous, stemming from the purposeful implementation of strategic initiatives to exploit the opportunities offered by digital technologies, or exogenous, arising from competitive threats from within and outside the industry [

34]. Whether endogenous or exogenous, DT is capable of changing a firm’s value proposition by refining its business model and market changes, leading to innovation in products or services and ultimately improved firm performance [

35].

To summarize, digital transformation is indeed beneficial to the operation and development of enterprises. However, the existing research only explores the impact of the overall digital transformation level of enterprises and does not pay attention to the impact of digital transformation in different dimensions, resulting in research gaps. According to the characteristics of digital transformation and drawing on existing research [

17], DT is conceptualized in this context as two types: TDT and MDT. The former refers to the use of new digital technologies such as artificial intelligence (AI) and blockchain to achieve significant improvements in business, enhance the customer experience, and streamline operational processes [

36], and focuses on the application of digital technologies in their own business processes. The latter refers to the innovation of business models to match the pace of digital technology development [

37] and focuses on the practical application of digital technology in external scenarios of the enterprise.

2.1. TDT and Corporate Sustainability

According to resource-based theory, the resources and capabilities of an enterprise are essential in attaining a competitive advantage and sustainable development [

38]. TDT enables the application of digital technologies, such as AI, cloud computing, big data, and blockchain technology, in an enterprise’s business processes [

39], which helps it to obtain rich and valuable information resources, improve its ability to acquire and transfer knowledge, optimize the efficiency of its resource allocation, and promote the matching and utilization of its own resources [

40]. This ability to acquire information and integrate resources is in line with the rare resources and capabilities advocated by resource-based theory, and, with the help of this ability, enterprises can achieve their own sustainable development to a certain extent [

41]. Meanwhile, the application of digital technologies in DT leads to improvements in business economic activities and reductions in business costs, such as replication and transportation costs, in order to improve business productivity [

42]. This can help enterprises to increase their operating income, reduce costs and expenses, and promote the sustainable development of their financial operations. TDT promotes product and service flexibility by facilitating the continuous evolution of the range, functionality, and value of products and services, which contributes remarkably to corporate competitiveness [

43,

44]. This can help enterprises to quickly update their products and services so that they can maintain stable competitiveness, become market leaders [

45], and promote enterprises to establish a competitive advantage and achieve sustainable development. Thus, the following hypothesis is proposed:

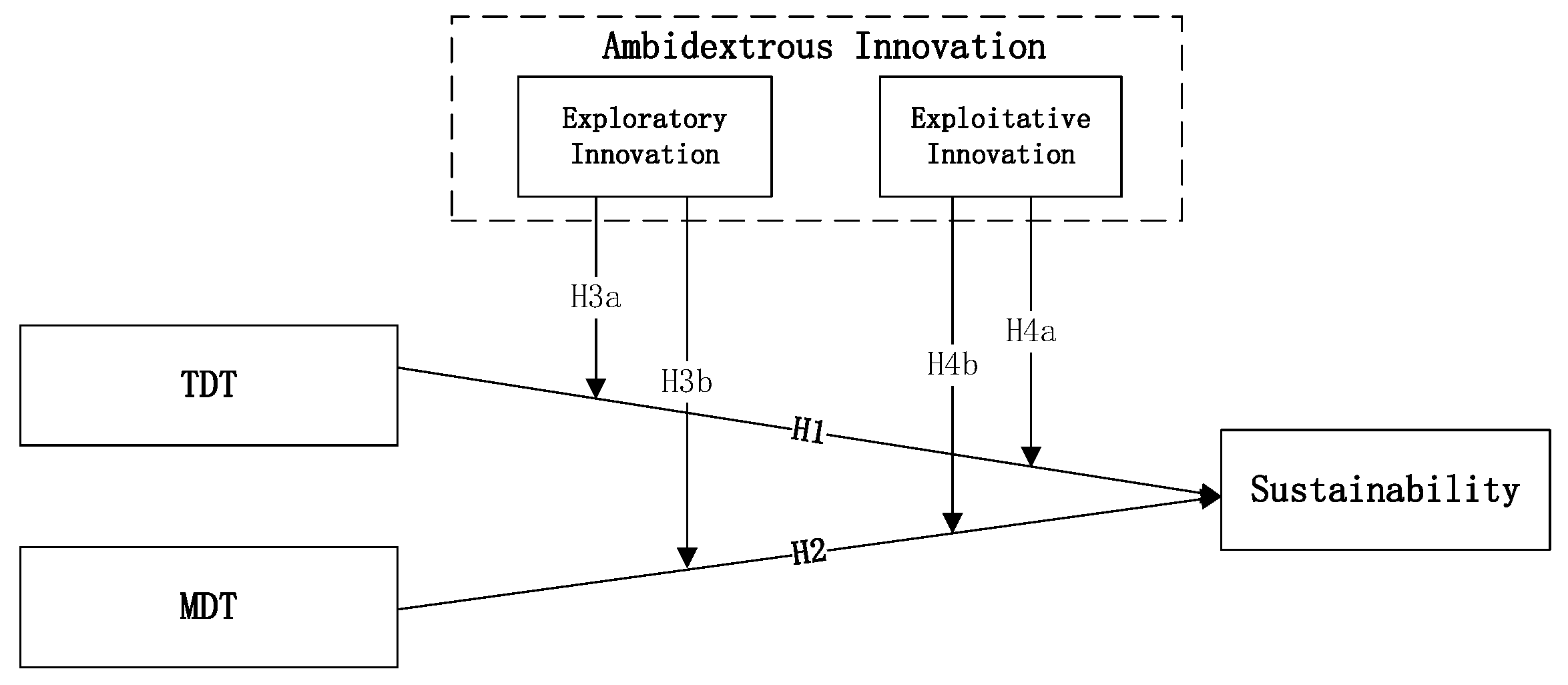

Hypothesis 1 (H1). TDT has a positive impact on corporate sustainability.

2.2. MDT and Corporate Sustainability

Resource-based theory believes that enterprises can obtain a competitive advantage and excellent performance by acquiring valuable and unique resources and capabilities and promoting their sustainable development [

38]. MDT focuses on the practical application of digital technologies in external scenarios of the enterprise, such as Internet technology applications, fintech, and intelligent applications [

17]. This enables enterprises to use innovation and advanced digital technologies to enhance and optimize external service processes, and it helps enterprises and customers to use more advanced applications and software to carry out and update their business, thus enhancing customer service and improving their competitive advantage [

46]. This valuable capability can enable enterprises to obtain continuous advantages and thus promote sustainable development, which is also consistent with the view of resource-based theory. In line with the dynamic capabilities framework, the ability to identify opportunities and integrate the use of resources can provide support for firms to successfully innovate and capture sufficient value to attain long-term superiority. MDT can improve this ability. For example, the application of Internet technology promotes the sharing of innovative knowledge among industries and strengthens the integration of information and resources within enterprises [

47]. In line with information asymmetry theory, information asymmetry is a vital issue in business decision making. MDT can mitigate this problem. For example, fintech mitigates corporate information asymmetry by increasing the number of information channels and sources and improving the availability and accuracy of their information to facilitate more informed decision making and improve the investment efficiency for sustainable business growth [

48]. More importantly, in the era of digital transformation, the means of interacting with customers has changed greatly, and the business model and market competition mode in the market are also gradually changing, which poses challenges to enterprises in ensuring or enhancing their competitive strength [

49]. According to the resource-based view, if enterprises wish to achieve sustainable development in this context, they must ensure that they have valuable resources or capabilities [

38]. MDT can enable enterprises to obtain greater market expansion and faster strategic activities to adapt to the digital era [

50]. This optimizes business models for firms and identifies market opportunities to better reconfigure organizations with new value propositions to increase the market shares and competitive advantage for firms [

51]. This is consistent with what the resource-based view asserts. Thus, the following hypothesis is proposed:

Hypothesis 2 (H2). MDT has a positive impact on corporate sustainability.

2.3. The Moderating Role of Exploratory Innovation

Innovation is essential for firms to maintain a competitive advantage and obtain superior performance [

52]. Exploratory innovation is the dynamic ability of a firm to explore new possibilities for the production of new products or services and enables the improvement of existing products and services [

53]. It manifests in the search for new areas of opportunity to facilitate the cross-fertilization and generation of new knowledge [

54]. A high level of exploratory innovation illustrates the expansion of a firm’s knowledge base, which means that firms have sufficient potential to apply new technologies and develop new routes, have greater opportunities to enter emerging markets, and seize new opportunities [

55], while offering great possibilities for the application of digital technologies in firms. Developing new markets, products, and services through exploratory innovation has been a major step for enterprises to break out of the existing technological orbit and gain a competitive advantage and sustainability [

56], which serves to provide a strong guarantee for successful and effective DT by applying new digital technologies. A higher level of exploratory innovation indicates that enterprises have the ability to learn and integrate information to enter a new field [

57], which can improve the ability of enterprises to learn and apply new digital technologies to accomplish TDT and enhance the ability of enterprises to adjust in order to refine their business models in response to market changes, promote MDT, and ultimately achieve enterprise development goals. Thus, the following hypotheses are proposed:

Hypothesis 3a (H3a). Exploratory innovation positively moderates the impact of TDT on corporate sustainability.

Hypothesis 3b (H3b). Exploratory innovation positively moderates the impact of MDT on corporate sustainability.

2.4. The Moderating Effect of Exploitative Innovation

Exploitative innovation is the dynamic innovation capability of a firm to modify a product or service using identified production increments. Its essence is the search for incremental and continuous change [

53]. It enables enterprises to promote the efficiency of using their existing knowledge and technology, enhance their ability to apply innovation, reduce their costs, and improve the efficiency of using and transforming their resources [

58], which can, to some extent, reduce the risks associated with the digital paradox [

59] and achieve cost reductions and efficiency in the process of DT. Unlike exploratory innovation, which expands the existing knowledge base, exploitative innovation significantly increases the depth of an organization’s core knowledge base and enhances its ability to use existing knowledge and integrate resources [

60], which provides a strong guarantee for TDT to optimize its own processes through the use of new digital technologies. When companies undergo MDT, they need to innovate their business models in response to market changes and customer needs. This process can be disruptive and carries a particular risk of uncertainty [

61], which can be precisely compensated for by the firm’s exploitative innovation. Higher levels of exploitative innovation can reduce the uncertainty of existing business strategies and technology applications [

62] and enhance the stability of the firm in order to improve its performance [

63]. Thus, the following hypotheses are proposed:

Hypothesis 4a (H4a). Exploitative innovation has a positive impact on the relationship between TDT and corporate sustainability.

Hypothesis 4b (H4b). Exploitative innovation has a positive impact on the relationship between MDT and corporate sustainability.

The research framework is shown in

Figure 1.

3. Methods

3.1. Data and Sample

Since 2013, emerging digital technologies such as the Internet, big data, and AI have been widely developed and advanced in China, and a wave of corporate DT has followed [

64]. This study selected A-share listed companies in China from 2013 to 2021 as the research sample to explore the impact of DT on corporate sustainability. To ensure the accuracy of the study, data were selected and processed according to the following standards: (1) data of companies in the financial sector were excluded; (2) data of companies classified as ST, ST*, or PT were excluded owing to their abnormal financial status; and (3) data of companies with serious abnormal observations were excluded. Finally, 20,419 sample observations were obtained. To avoid the effect of extreme values, all continuous-type variables (except for the date) were shrunk at the 1% level in this study. The data were obtained from the Wind Database, China Stock Market & Accounting Research Database, and Chinese Research Data Services. They were processed using Stata 17.0 and Python 3.8.

3.2. Definition and Measurement of Variables

3.2.1. Explained Variable

Corporate sustainability is the ability of a corporation to attain sustainable operations, maintain a competitive advantage, and grow steadily. Most studies have used the models proposed by Higgins [

65] or James C. Van Horne (1988) for the measurement of corporate sustainability. Although the sustainable growth model proposed by Higgins is more convenient and simple to calculate, it does not consider dynamic growth [

66]. Therefore, this study used the sustainable growth model proposed by James C. Van Horne (1988) to measure corporate sustainability in terms of profitability and competitive advantage, which is calculated as follows:

3.2.2. Explanatory Variables

Studies on the measurement of DT have included textual analysis [

67] and questionnaires [

9,

68]. However, questionnaire surveys may suffer from methodological or subjective bias, which is highly likely to lead to inaccurate conclusions. On the one hand, the source of sample data used in the questionnaire survey is too singular [

69]. On the other hand, the sample results are highly susceptible to the subjective judgment of the respondents [

70]. At the same time, the annual reports of listed companies can effectively and accurately reflect the strategic positioning of enterprises, and the terms related to digital transformation will also be reflected in the annual reports of enterprises [

71]. Therefore, this study used textual analysis to quantitatively measure the DT of enterprises based on annual report data. The methodological steps were as follows:

- (1)

To construct a proper keyword lexicon for digital transformation, this study combed through the literature of existing studies that used content analysis to measure digital transformation [

5,

17,

67,

72]. The results showed that there were two main keywords related to DT: basic digital technology and digital technology application scenarios [

73]. Meanwhile, this study compared and screened the digital transformation keywords used in the literature with those published in the China Stock Market and Accounting Research Database. Finally, 76 digital transformation keywords, such as artificial intelligence, blockchain, and cloud computing were compiled. In developing the classification criteria of digital keywords, this study both screened the classification keywords one by one according to the characteristics of the two types of digital transformation and referred to the classification criteria of previous studies to improve the classification criteria of this study. This study used 42 digital technology keywords, such as AI, blockchain, and cloud computing, to measure TDT. Most of these keywords were basic digital technologies, and their frequency reflected, to some extent, the efforts made by companies to optimize their processes in terms of basic DT. Further, 34 digital technology keywords, such as mobile Internet and payment and fintech, were used to measure MDT. Most of these keywords were practical applications of the digital foundation—that is, they were mainly applied to the external scenarios and operation models of enterprises.

Table 1 and

Table 2 show the keywords for TDT and MDT, respectively.

- (2)

The corporate annual reports of Chinese A-share listed companies from 2013 to 2021 were assembled through the Python software, and the text content of all corporate annual reports was extracted through Java PDFbox. MD&A is considered one of the most useful disclosures in financial reports [

74], and it contains more accurate and forward-looking corporate information [

75]. In light of existing studies [

17], this study concentrated the text analysis on the MD&A sections of the annual reports to form a text master that could be searched using the DT keywords. To ensure accuracy, this study used annual reports as the text master in the robustness testing section to test the reliability of the findings.

- (3)

The keywords for the two forms of DT were searched, matched, counted, and summed in the MD&A text database to form the total word frequencies for each type of DT. As the length of the MD&A text in different companies’ annual reports varied greatly, the sum of the two DT word frequencies was divided by the length of the MD&A text to obtain TDT and MDT, respectively.

3.2.3. Moderating Variables

The number of patents is an essential parameter used to measure the level of innovation at a firm [

76]. Invention patents represent the development of products and realization of technological breakthroughs in new markets and can be used to reflect the level of exploratory innovation in a company. Utility models and design patents focus on the improvement of the original technology and are extensions of existing products and technologies, which can reflect the level of exploitative innovation in the enterprise. By referring to the literature [

77], this study measured exploratory innovation (Explor) by adding one to the number of invention patent applications of the firm and taking the natural logarithm. It measured exploitative innovation (Exploi) by adding one to the number of corporate design and utility model patent applications and taking the natural logarithm.

3.2.4. Control Variables

This study controlled for variables that may affect corporate sustainability. Based on recent research [

78,

79,

80,

81], the following variables were controlled for: firm size (Size), asset–liability ratio (Lev), fixed asset ratio (FIXED), TobinQ, firm age (FirmAge), and nature of firm ownership (SOE). The industry (INDUSTRY) and the year (YEAR) dummy variables were set separately in this study. Both took a value of 1 if the firm belonged to the industry and 0 if it did not.

Table 3 presents the definition and measurement of the variables.

3.3. Models

To test the hypotheses, models (1) to (6) were set up. was the explanatory variable, which represented the level of corporate sustainability of firm i in year t. and were explanatory variables, representing the levels of TDT and MDT of enterprise i in year t, respectively. and represented the exploratory and exploitative innovation levels of enterprise i in year t, respectively. and represented the year and industry dummy variables, respectively, indicating that the research model controlled for industry and year. represented the residual term.

As shown in models (1) and (2), the impacts of

TDT and

MDT on corporate sustainability (SGR) were examined. If

was positive and passed the significance test, it meant that DT had a positive impact on the sustainable development of enterprises and that research hypothesis 1 was valid. If

did not pass the significance test or

was negative and passed the significance test, research hypothesis 1 was not valid.

As shown in models (3) to (6), the moderating effects of exploratory (Explor) and exploitative innovation (Exploi) on the relationship between TDT and MDT and corporate sustainability were examined separately. In models (3) to (6), the interaction terms of the two types of DT and ambidextrous innovation were added to test the moderating effect. Taking model (3) as an example,

represents the moderating effect of corporate exploratory innovation (Explor) on TDT and corporate sustainability. If

is positive and passes the significance test, while

is also positive and passes the significance test, the exploratory innovation of enterprises positively moderates the positive effect of TDT on corporate sustainability, at which point H3a holds. The coefficients of models (4) to (6) were the same as those of model (3) and will not be repeated.

3.4. Statistical Methods

The statistical methods used in this study were as follows. First, descriptive statistics were used to observe the distribution characteristics of the sample data, to avoid the possibility that the sample data did not meet the requirements of linear regression, and to improve the feasibility of linear regression. Second, correlation analysis was conducted to apply the Pearson correlation coefficient to initially determine the correlations between variables. The variance inflation factor was also calculated to prevent the problem of multicollinearity and improve the accuracy of the linear analysis. Third, before conducting linear regression, a Hausman test was performed to determine whether a random-effects model or a fixed-effects model should be used to ensure the applicability of the research model to the sample. Finally, the two-stage least squares method was used to perform linear regression on the research sample again to ensure the robustness of the research results.

5. Conclusions and Discussion

5.1. Discussion

With the development and maturity of digital technology, all enterprises are facing the challenge of digitalization, but the speed, scale, and scope of digitalization’s impacts on enterprises are different or even contrasting. For example, some scholars have found that digital transformation can effectively improve the performance of enterprises [

93], while others have found that the direction and intensity of digitalization cannot contribute to the financial performance of enterprises [

94]. In fact, the impact of digitalization on enterprises is complex, heterogeneous, comprehensive, and long-term, and studies are only able judge the impact of digital transformation through short-term financial performance. Obviously, it is necessary to clarify the impact of digital transformation on enterprises, especially the sustainable development of enterprises [

95]. This study examines the relationship between digital transformation and the sustainable development of enterprises, which has important implications for the transition of enterprises to more sustainable development models.

Digital transformation means the integration of multiple digital technologies [

31]. In the existing research, some scholars have discussed the relationship between a specific digital technology and sustainable development in the context of digital transformation, such as cloud-based ERP technology [

96], big data analysis technology [

97], and blockchain technology [

98]. Some scholars have discussed the relationship between the overall digital transformation level of enterprises and sustainable development [

99]. It is not difficult to see that academia has discussed the relationship between the overall digital transformation of enterprises or a specific digital technology and sustainable development, but it has obviously ignored the impact of different dimensions of digital transformation on sustainable development. This study aims to fill this gap.

By reviewing the research literature on digital transformation [

17,

20], this study finds that digital transformation is mainly carried out from two perspectives. On the one hand, digital transformation can help enterprises to optimize existing business processes and improve productivity. On the other hand, digital transformation can change the business models of enterprises and reshape the ways in which competition and cooperation between enterprises are obtained [

21]. Obviously, from the first perspective, digital transformation is more inclined to rely on digital technology to improve the internal enterprise, while, from the second perspective, digital transformation is more inclined to change the external market of the enterprise. Based on this, this study divides digital transformation into technology-oriented digital transformation and market-oriented digital transformation to explore the impact on the sustainable development of enterprises, respectively. This study finds that both types of digital transformation have a positive impact on the sustainable development of enterprises, which is conducive to comprehensively grasping the logical relationship between different dimensions of digital transformation and improving the dimensional research on digital transformation. At the same time, for policymakers, a certain type of digital policy can be more targeted. For enterprises, they can adjust their digital transformation strategy in a timely manner and choose a certain type of digital transformation in a targeted manner.

Innovation capability has a positive impact on enterprises’ ability to maintain a competitive advantage. From the perspective of enterprise innovation, this study chooses ambidextrous innovation as the moderating variable to discuss the moderating effect of exploratory innovation and exploitative innovation on the relationship between different types of digital transformation and sustainable development. This attempt reveals the logical relationship between different types of digital transformation and different types of innovation. The research shows that enterprise ambidexterity innovation does promote the positive impact of the two types of digital transformation on the sustainable development of enterprises, which also proves the importance of innovation for the success of enterprises’ strategies.

In addition, the reason for choosing Chinese listed companies as the research subject in this study is that China’s digital transformation has received considerable attention in recent years [

100]. The Chinese digital transformation is highly representative and typical, and with the Chinese context as the research background, the research findings are more informative and valuable to study.

5.2. Conclusions

DT has become the new normal. Research on the overall effects of DT in enterprises is mature, but the effects of DT in different dimensions remain unclear. This study divided DT into TDT and MDT and used a two-way fixed-effects model to examine the impact of both types on corporate sustainability for A-share listed companies in China between 2013 and 2021. The boundary condition of corporate ambidextrous innovation was used to explore how the level of ambidextrous innovation affects the relationship between DT and corporate sustainability in different dimensions.

First, this study finds that technology-oriented digital transformation can positively promote the sustainable development of enterprises. According to the resource-based view, when enterprises acquire valuable and unique resources and capabilities, they can gain competitive advantages, achieve excellent performance, and promote sustainable development. Technology-oriented digital transformation, by applying a variety of advanced digital technologies to the internal operations of enterprises, optimizes their business processes and improves their operational efficiency so that they can obtain superior resources and promote sustainable development. Second, market-oriented digital transformation has a positive impact on the sustainable development of enterprises. This is also consistent with the previous theoretical analysis. Market-oriented digital transformation can reshape the business models of enterprises through digital technology, improve the ways in which they cooperate with customers, and realize a new business model.

At the same time, this study finds that the ambidextrous innovation of enterprises can positively promote the relationship between digital transformation and sustainable development. The exploratory innovation level of an enterprise represents its ability to explore new fields and apply new technologies. The level of enterprise exploitative innovation represents the ability of enterprises to use and integrate their existing resources, which provides the possibility for digital technology to optimize their business processes and reshape their business models. Obviously, enterprise ambidexterity innovation can provide a suitable enterprise environment and sufficient innovation resources for enterprises to apply digital technology and realize digital transformation.

Based on the above conclusions, this study believes that enterprises should actively use digital technology to promote their sustainable development. Moreover, enterprises strive to improve the level of ambidexterity in innovation, which provides strong environmental conditions for the development of enterprises’ digital strategies.

5.3. Implications

The theoretical implications are as follows. First, most studies have analyzed the value effect of DT from a holistic perspective and have used the composite index of enterprise DT to represent enterprise DT and explore its impact on enterprise value. This study distinguished between and examined the impact of TDT and MDT on firm value. This expands the multidimensional research on DT and provides new ideas for a comprehensive and detailed understanding of DT. Second, studies have focused on the value effects of DT; for example, it has an impact on enterprise performance, innovation, and operational efficiency [

5,

101,

102]. However, few have explored the relationship between DT and corporate sustainability. This study enriches the literature on the impact of different types of digital research on corporate sustainability and validates DT research by relying on a resource-based view. Third, this study considers enterprise innovation as the boundary condition of DT application, and it shows that ambidextrous innovation facilitates the positive relationship between enterprise DT and corporate sustainability, which broadens the boundary condition of enterprise DT application and enriches the relevant literature on enterprise innovation theory.

The practical implications are as follows. First, the findings support the active policies and measures of the government and related departments on DT and provide a reference for the next step of DT-related policy guidance and development. Second, the findings suggest that enterprises should continue to persist in developing DT, which is beneficial for them to gain a long-term competitive advantage. Third, the study shows the significance of corporate innovation and indicates that a high level of corporate innovation capability is of great benefit both for the direct and indirect impacts on corporate value and corporate development strategies, respectively.

5.4. Limitations and Future Research

First, both MDT and TDT had a positive impact on the sustainable development of enterprises. However, the research object was listed companies in China and the conclusions may have local characteristics of Chineseization, which means that extensive research must be conducted on companies in different countries and regions to verify the validity of the conclusions. Second, this study used a thesaurus of DT keywords constructed based on Chinese digitalization-related policy documents and the characteristics of China’s DT development. Therefore, the applicability and timeliness of the thesaurus have a few limitations, which means that future research must update and expand the digital text analysis thesaurus according to the characteristics of the research object. Finally, this study classified DT into two categories based on its characteristics. However, classifications go far beyond the binary, and more detailed classifications can be created in the future based on the characteristics of DT in order to expand and deepen the multidimensional study of DT.

{kind=link}