How Does the Digital Transformation of Banks Improve Efficiency and Environmental, Social, and Governance Performance?

Abstract

:1. Introduction

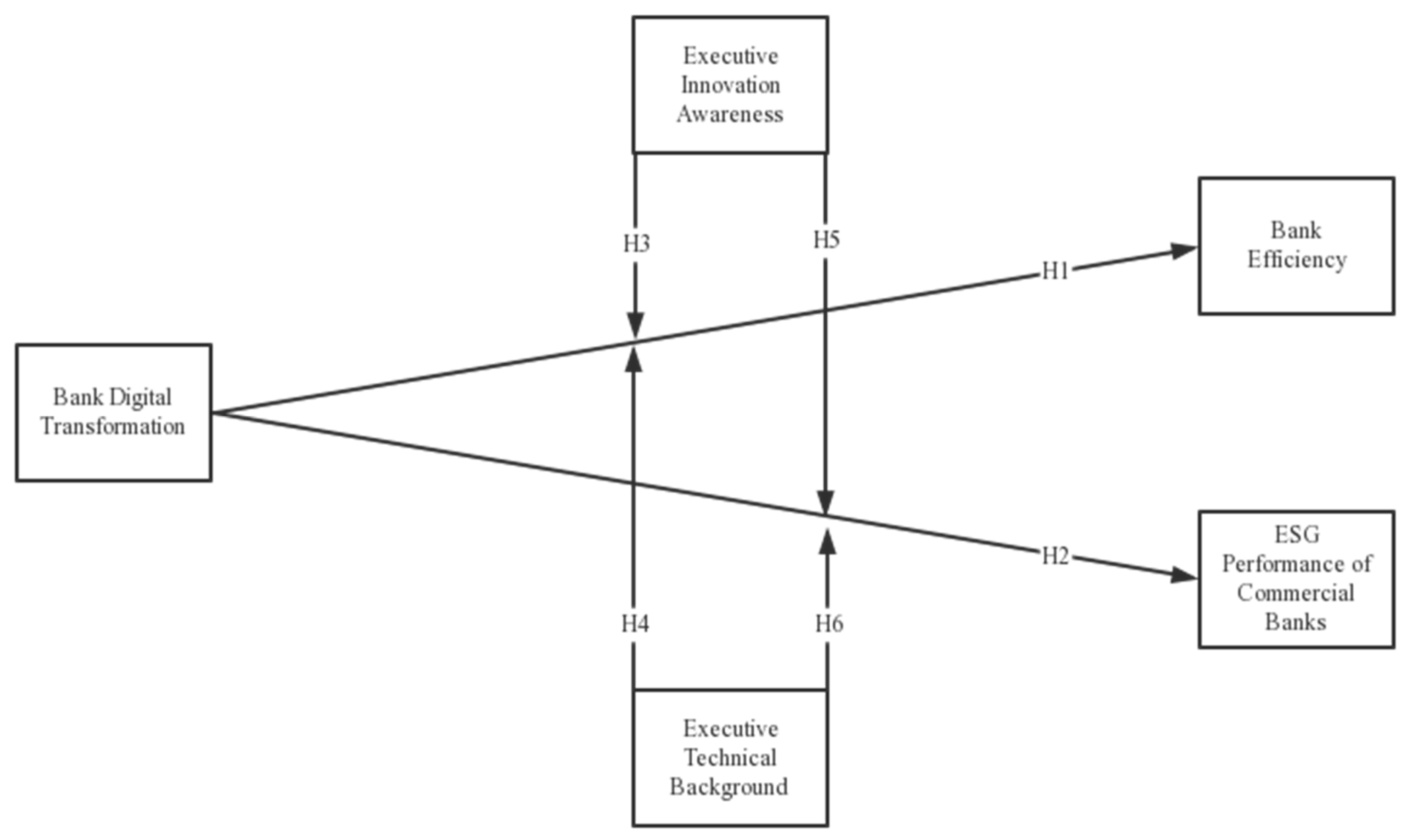

2. Literature Review and Theoretical Hypotheses

3. Research Design

3.1. Sample Selection and Data Sources

3.2. Variable Definition

3.2.1. Dependent Variable Bank Efficiency and ESG Performance of Commercial Banks

3.2.2. Independent Variable Bank Digital Transformation

3.2.3. Moderated Variables

3.2.4. Control Variables

3.2.5. Model Construction

4. Research Results

4.1. Descriptive Statistics

4.2. Correlation Analysis

4.3. Regression Analysis

5. Robustness Check

6. Discussion and Conclusions

6.1. Discussion

6.2. Research Conclusions

6.2.1. Theoretical Contributions

6.2.2. Managerial Contributions

6.3. Limitations and Future Research Directions

Author Contributions

Funding

Data Availability Statement

Conflicts of Interest

References

- Zhou, Y. The Application Trend of Digital Finance and Technological Innovation in the Development of Green Economy. J. Environ. Public Health 2022, 2022, 1064558. [Google Scholar] [CrossRef] [PubMed]

- Su, J.; Su, K.; Wang, S. Does the Digital Economy Promote Industrial Structural Upgrading?—A Test of Mediating Effects Based on Heterogeneous Technological Innovation. Sustainability 2021, 13, 10105. [Google Scholar] [CrossRef]

- Li, G.; Zhang, R.; Feng, S.; Wang, Y. Digital finance and sustainable development: Evidence from environmental inequality in China. Bus. Strategy Environ. 2022, 31, 3574–3594. [Google Scholar] [CrossRef]

- Wang, L.; Wang, Y. Supply chain financial service management system based on block chain IoT data sharing and edge computing. Alex. Eng. J. 2022, 61, 147–158. [Google Scholar] [CrossRef]

- Tian, X.; Zhang, Y.; Qu, G. The Impact of Digital Economy on the Efficiency of Green Financial Investment in China’s Provinces. Int. J. Environ. Res. Public Health 2022, 19, 8884. [Google Scholar] [CrossRef] [PubMed]

- Fan, W.; Wu, H.; Liu, Y.; Gherghina, S.C. Does Digital Finance Induce Improved Financing for Green Technological Innovation in China? Discret. Dyn. Nat. Soc. 2022, 2022, 6138422. [Google Scholar] [CrossRef]

- Zhao, J.; Li, X.; Yu, C.-H.; Chen, S.; Lee, C.-C. Riding the FinTech innovation wave: FinTech, patents and bank performance. J. Int. Money Financ. 2022, 122, 102552. [Google Scholar] [CrossRef]

- Shou, H. In The Impact of Financial Technology on the Operational Efficiency of Commercial Banks. In Proceedings of the 2021 12th International Conference on E-Business, Management and Economics, Beijing, China, 17–19 July 2021; pp. 499–505. [Google Scholar]

- Hoehle, H.; Scornavacca, E.; Huff, S. Three decades of research on consumer adoption and utilization of electronic banking channels: A literature analysis. Decis. Support Syst. 2012, 54, 122–132. [Google Scholar] [CrossRef]

- Chen, K.-C. Implications of Fintech Developments for Traditional Banks. Int. J. Econ. Financ. Issues 2020, 10, 227–235. [Google Scholar] [CrossRef]

- Zhao, H.; Jin, D.; Li, H.; Wang, H. Affiliated bankers on board and firm environmental management: U.S. evidence. J. Financ. Stab. 2021, 57, 100951. [Google Scholar] [CrossRef]

- Weston, P.; Nnadi, M. Evaluation of strategic and financial variables of corporate sustainability and ESG policies on corporate finance performance. J. Sustain. Financ. Investig. 2021, 1–17. [Google Scholar] [CrossRef]

- Zhu, Y.; Jin, S. COVID-19, Digital Transformation of Banks, and Operational Capabilities of Commercial Banks. Sustainability 2023, 15, 8783. [Google Scholar] [CrossRef]

- Li, W.; Chen, G.; Liao, X. Countermeasures of Chinese Traditional Commercial Banks to Meet the Challenges of Internet Finance Based on Big Data Analysis—Evidence from ICBC; Journal of Physics: Conference Series; IOP Publishing: Bristol, UK, 2020; p. 032066. [Google Scholar]

- Leviäkangas, P. Digitalisation of Finland’s transport sector. Technol. Soc. 2016, 47, 1–15. [Google Scholar] [CrossRef]

- Wang, Y.; Xiuping, S.; Zhang, Q. Can fintech improve the efficiency of commercial banks?—An analysis based on big data. Res. Int. Bus. Financ. 2021, 55, 101338. [Google Scholar] [CrossRef]

- Raut, R.D.; Mangla, S.K.; Narwane, V.S.; Dora, M.; Liu, M. Big Data Analytics as a mediator in Lean, Agile, Resilient, and Green (LARG) practices effects on sustainable supply chains. Transp. Res. Part E Logist. Transp. Rev. 2021, 145, 102170. [Google Scholar] [CrossRef]

- Reis, J.; Melao, N. Digital transformation: A meta-review and guidelines for future research. Heliyon 2023, 9, e12834. [Google Scholar] [CrossRef] [PubMed]

- Zhang, Z.; Duan, H.; Shan, S.; Liu, Q.; Geng, W. The Impact of Green Credit on the Green Innovation Level of Heavy-Polluting Enterprises-Evidence from China. Int. J. Environ. Res. Public Health 2022, 19, 650. [Google Scholar] [CrossRef]

- Li, R.; Rao, J.; Wan, L. The digital economy, enterprise digital transformation, and enterprise innovation. Manag. Decis. Econ. 2022, 43, 2875–2886. [Google Scholar] [CrossRef]

- Yao, T.; Song, L. Fintech and the economic capital of Chinese commercial bank’s risk: Based on theory and evidence. Int. J. Financ. Econ. 2021, 28, 2109–2123. [Google Scholar] [CrossRef]

- Liu, X.; Sun, J.; Yang, F.; Wu, J. How ownership structure affects bank deposits and loan efficiencies: An empirical analysis of Chinese commercial banks. Ann. Oper. Res. 2018, 290, 983–1008. [Google Scholar] [CrossRef]

- Tan, Y.; Wanke, P.; Antunes, J.; Emrouznejad, A. Unveiling endogeneity between competition and efficiency in Chinese banks: A two-stage network DEA and regression analysis. Ann. Oper. Res. 2021, 306, 131–171. [Google Scholar] [CrossRef]

- Pantano, E.; Pizzi, G.; Scarpi, D.; Dennis, C. Competing during a pandemic? Retailers’ ups and downs during the COVID-19 outbreak. J. Bus. Res. 2020, 116, 209–213. [Google Scholar] [CrossRef] [PubMed]

- Miralles-Quirós, M.; Miralles-Quirós, J.; Redondo Hernández, J. ESG Performance and Shareholder Value Creation in the Banking Industry: International Differences. Sustainability 2019, 11, 1404. [Google Scholar] [CrossRef] [Green Version]

- Esposito De Falco, S.; Scandurra, G.; Thomas, A. How stakeholders affect the pursuit of the Environmental, Social, and Governance. Evidence from innovative small and medium enterprises. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 1528–1539. [Google Scholar] [CrossRef]

- Miralles-Quirós, M.M.; Miralles-Quirós, J.L.; Redondo-Hernández, J. The impact of environmental, social, and governance performance on stock prices: Evidence from the banking industry. Corp. Soc. Responsib. Environ. Manag. 2019, 26, 1446–1456. [Google Scholar] [CrossRef]

- Fulghieri, P.; García, D.; Hackbarth, D. Asymmetric Information and the Pecking (Dis)Order. Rev. Financ. 2020, 24, 961–996. [Google Scholar] [CrossRef]

- Leyer, M.; Stumpf-Wollersheim, J.; Pisani, F. The influence of process-oriented organisational design on operational performance and innovation: A quantitative analysis in the financial services industry. Int. J. Prod. Res. 2017, 55, 5259–5270. [Google Scholar] [CrossRef]

- Shenhar, A.J. From low- to high-tech project management. RD Manag. 1993, 23, 199–214. [Google Scholar] [CrossRef]

- Song, C.; Nahm, A.Y.; Song, Z. Executive technical experience and corporate innovation quality: Evidence from Chinese listed manufacturing companies. Asian J. Technol. Innov. 2022, 31, 94–114. [Google Scholar] [CrossRef]

- Ji, L.; Sun, Y.; Liu, J.; Chiu, Y.H. Environmental, social, and governance (ESG) and market efficiency of China’s commercial banks under market competition. Environ. Sci. Pollut. Res. Int. 2023, 30, 24533–24552. [Google Scholar] [CrossRef]

- Choi, I.; Chung, S.; Han, K.; Pinsonneault, A. CEO risk-taking incentives and it innovation: The moderating role of a CEO’s it-related human capital. MIS Q. 2021, 45, 2175–2192. [Google Scholar] [CrossRef]

- Chan, J.Y.-L.; Leow, S.M.H.; Bea, K.T.; Cheng, W.K.; Phoong, S.W.; Hong, Z.-W.; Chen, Y.-L. Mitigating the Multicollinearity Problem and Its Machine Learning Approach: A Review. Mathematics 2022, 10, 1283. [Google Scholar] [CrossRef]

- Muharsito, M.; Muharam, H. The Effect of Digital Financial Inclusion on Bank Efficiency. Int. Conf. Res. Dev. 2023, 2, 1–6. [Google Scholar] [CrossRef]

- Zhang, C.; Jin, S. What Drives Sustainable Development of Enterprises? Focusing on ESG Management and Green Technology Innovation. Sustainability 2022, 14, 11695. [Google Scholar] [CrossRef]

- Zhu, Y. Enterprise life cycle, financial technology and digital transformation of banks—Evidence from China. Aust. Econ. Pap. 2023, 62, 1–15. [Google Scholar]

- Xie, X.; Wang, S. Digital transformation of commercial banks in China: Measurement, progress and impact. China Econ. Q. Int. 2023, 3, 35–45. [Google Scholar] [CrossRef]

- Liu, L.; Liu, X.; Guo, Z.; Fan, S.; Li, Y. An Examination of Impact of the Board of Directors’ Capital on Enterprises’ Low-Carbon Sustainable Development. J. Sens. 2022, 2022, 7740946. [Google Scholar] [CrossRef]

- Gao, Y.; Jin, S. Corporate Nature, Financial Technology, and Corporate Innovation in China. Sustainability 2022, 14, 7162. [Google Scholar] [CrossRef]

- Chaparro-Peláez, J.; Acquila-Natale, E.; Hernández-García, Á.; Iglesias-Pradas, S. The Digital Transformation of the Retail Electricity Market in Spain. Energies 2020, 13, 2085. [Google Scholar] [CrossRef] [Green Version]

- Hänninen, M.; Kwan, S.K.; Mitronen, L. From the store to omnichannel retail: Looking back over three decades of research. Int. Rev. Retail Distrib. Consum. Res. 2020, 31, 1–35. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Variable Type | Variable Name | Variable Code | Variable Definitions |

|---|---|---|---|

| Dependent Variable | Bank Efficiency | BE | Business management fee/operating income × (−100%) |

| ESG Performance of Commercial Banks | ESG | Bloomberg ESG score | |

| Independent Variable | Bank Digital Transformation | BDT | Peking University Digital Finance Research Center |

| Moderator | Executive Innovation Awareness | EIA | Dummy variable, the average frequency of innovative words mentioned by executives in commercial bank annual reports, 1 if more excellent than the average, 0 for others |

| Executive Technical Background | ETB | As a dummy variable, executives with technical background take 1, others take 0 | |

| Control Variable | Bank Size | SIZE | The natural logarithm of the total assets at the end of the year |

| Solvency | LEV | Total liabilities at the end of the year/total assets at the end of the year | |

| Growth | GRO | Operating income growth rate | |

| Concentration of Ownership | TOP1 | Shareholding ratio of the largest shareholder | |

| Bank Nature | SOE | Dummy variable, 1 for state-owned holdings, 0 otherwise | |

| Capital Intensity | CI | Total assets/operating income × (−100%) | |

| Net Profit Growth Rate | NPGR | (Net profit for the current period − Net profit for the previous year)/Net profit for the previous year) × 100% | |

| Annual Effect | YEAR | Year dummy variable |

| VARIABLES | N | Mean | Sd | Min | Max |

|---|---|---|---|---|---|

| BE | 253 | −29.60 | 4.534 | −41.78 | −21.86 |

| ESG | 253 | 38.45 | 9.464 | 19.32 | 55.76 |

| BDT | 253 | 99.91 | 38.91 | 23.56 | 169.8 |

| EIA | 253 | 0.407 | 0.492 | 0 | 1 |

| ETB | 253 | 0.344 | 0.476 | 0 | 1 |

| SIZE | 253 | 28.59 | 1.433 | 25.69 | 30.97 |

| LEV | 253 | 0.928 | 0.0104 | 0.908 | 0.948 |

| GRO | 253 | 0.0201 | 0.0528 | −0.0872 | 0.144 |

| TOP1 | 253 | 27.51 | 17.58 | 8.170 | 67.13 |

| SOE | 253 | 0.427 | 0.496 | 0 | 1 |

| CI | 253 | 38.28 | 5.733 | 27.50 | 52.46 |

| NPGR | 253 | 11.86 | 10.82 | −5.885 | 41.62 |

| VARIABLES | BE | ESG | BDT | EIA | ETB | SIZE | LEV | GRO | TOP1 | SOE | CI | NPGR |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| BE | 1 | |||||||||||

| ESG | 0.235 *** | 1 | ||||||||||

| BDT | 0.410 *** | 0.623 *** | 1 | |||||||||

| EIA | −0.0960 | −0.0710 | 0.145 ** | 1 | ||||||||

| ETB | −0.0960 | 0.00800 | 0.118 * | 0.874 *** | 1 | |||||||

| SIZE | 0.231 *** | 0.616 *** | 0.335 *** | −0.426 *** | −0.267 *** | 1 | ||||||

| LEV | −0.251 *** | −0.446 *** | −0.592 *** | −0.108 * | −0.0690 | −0.0940 | 1 | |||||

| GRO | 0.0620 | −0.215 *** | −0.143 ** | 0.0920 | 0.0580 | −0.204 *** | 0.126 ** | 1 | ||||

| TOP1 | −0.0480 | 0.395 *** | 0.0940 | −0.233 *** | −0.163 *** | 0.634 *** | −0.0420 | −0.106 * | 1 | |||

| SOE | −0.104 * | 0.102 | −0.114 * | −0.146 ** | −0.103 | 0.256 *** | 0.154 ** | −0.163 *** | 0.291 *** | 1 | ||

| CI | 0.256 *** | −0.175 *** | 0.213 *** | 0.287 *** | 0.196 *** | −0.220 *** | 0.0110 | 0.0750 | −0.292 *** | −0.177 *** | 1 | |

| NPGR | −0.322 *** | −0.488 *** | −0.571 *** | 0.00900 | 0.0390 | −0.292 *** | 0.504 *** | 0.227 *** | −0.138 ** | 0.0640 | −0.0730 | 1 |

| (1) | (2) | (3) | (4) | (5) | (6) | |

|---|---|---|---|---|---|---|

| VARIABLES | BE | ESG | BE | BE | ESG | ESG |

| BDT | 0.036 *** | 0.049 *** | 0.032 ** | 0.035 *** | 0.042 ** | 0.046 ** |

| (2.67) | (2.67) | (2.44) | (2.62) | (2.29) | (2.53) | |

| EIA | −1.497 ** | 1.548 * | ||||

| (−2.53) | (1.88) | |||||

| BDT *EIA | 0.033 ** | 0.035 * | ||||

| (2.26) | (1.69) | |||||

| ETB | −1.373 ** | 1.518 ** | ||||

| (−2.48) | (1.99) | |||||

| BDT *ETB | 0.027 * | 0.034 * | ||||

| (1.83) | (1.67) | |||||

| SIZE | 0.960 *** | 3.021 *** | 0.873 *** | 0.913 *** | 3.407 *** | 3.191 *** |

| (3.38) | (7.71) | (2.92) | (3.22) | (8.21) | (8.14) | |

| LEV | −101.048 *** | 33.438 | −89.102 ** | −93.994 ** | 32.188 | 33.617 |

| (−2.74) | (0.66) | (−2.44) | (−2.57) | (0.64) | (0.67) | |

| GRO | 15.173 *** | 0.780 | 15.144 *** | 15.304 *** | −0.386 | −0.221 |

| (3.01) | (0.11) | (3.05) | (3.07) | (−0.06) | (−0.03) | |

| TOP1 | −0.053 *** | 0.027 | −0.051 *** | −0.053 *** | 0.016 | 0.020 |

| (−2.85) | (1.06) | (−2.79) | (−2.88) | (0.61) | (0.78) | |

| SOE | −0.311 | 0.776 | −0.230 | −0.170 | 0.788 | 0.916 |

| (−0.59) | (1.06) | (−0.44) | (−0.32) | (1.09) | (1.25) | |

| CI | 0.247 *** | −0.487 *** | 0.226 *** | 0.226 *** | −0.540 *** | −0.530 *** |

| (4.72) | (−6.74) | (4.18) | (4.20) | (−7.19) | (−7.13) | |

| NPGR | 0.003 | −0.109 * | 0.018 | 0.023 | −0.106 * | −0.115 ** |

| (0.07) | (−1.93) | (0.46) | (0.57) | (−1.89) | (−2.03) | |

| Constant | 25.466 | −69.947 | 16.637 | 20.003 | −78.086 * | −73.511 |

| (0.74) | (−1.48) | (0.49) | (0.59) | (−1.66) | (−1.57) | |

| Year FE | YES | YES | YES | YES | YES | YES |

| Observations | 253 | 253 | 253 | 253 | 253 | 253 |

| R-squared | 0.343 | 0.713 | 0.372 | 0.366 | 0.721 | 0.722 |

| (1) | (2) | (3) | |

|---|---|---|---|

| First Stage | Second Stage | ||

| VARIABLES | BDT | BE | ESG |

| LBDT | 0.692 *** | ||

| (13.69) | |||

| BDT | 0.052 *** | 0.079 *** | |

| (2.60) | (2.97) | ||

| SIZE | 4.176 *** | 0.631 * | 2.768 *** |

| (3.84) | (1.79) | (5.95) | |

| LEV | 217.606 | −101.496 ** | 57.526 |

| (1.48) | (−2.49) | (1.07) | |

| GRO | 26.795 | 14.405 *** | 4.242 |

| (1.40) | (2.69) | (0.60) | |

| TOP1 | −0.045 | −0.046 ** | 0.019 |

| (−0.64) | (−2.41) | (0.75) | |

| SOE | −0.612 | −0.364 | 1.372 * |

| (−0.31) | (−0.67) | (1.93) | |

| CI | 0.089 | 0.226 *** | −0.553 *** |

| (0.44) | (4.07) | (−7.57) | |

| NPGR | −0.379 ** | 0.007 | −0.104 * |

| (−2.41) | (0.16) | (−1.75) | |

| Constant | −277.758 ** | 31.011 | −75.111 |

| (−2.03) | (0.80) | (−1.48) | |

| Year FE | Yes | Yes | Yes |

| Observations | 220 | 220 | 220 |

| R-squared | 0.877 | 0.301 | 0.715 |

| Underidentification test (Kleibergen–Paap rk LM statistic) | 46.855(Chi-sq (1) p-val = 0.0000) | ||

| Weak identification test (Cragg–Donald–Wald F statistic) | 187.455 | ||

| (Kleibergen–Paap rk Wald F statistic) | 164.199 | ||

| 10% maximal IV size | 16.38 | ||

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Zhu, Y.; Jin, S. How Does the Digital Transformation of Banks Improve Efficiency and Environmental, Social, and Governance Performance? Systems 2023, 11, 328. https://doi.org/10.3390/systems11070328

Zhu Y, Jin S. How Does the Digital Transformation of Banks Improve Efficiency and Environmental, Social, and Governance Performance? Systems. 2023; 11(7):328. https://doi.org/10.3390/systems11070328

Chicago/Turabian StyleZhu, Yongjie, and Shanyue Jin. 2023. "How Does the Digital Transformation of Banks Improve Efficiency and Environmental, Social, and Governance Performance?" Systems 11, no. 7: 328. https://doi.org/10.3390/systems11070328