Islamic Social Funds to Foster Yunusian Social Business and Conventional Social Enterprises

{kind=link}

Abstract

:1. Introduction

2. Value-Based Intermediation (VBI)

2.1. Yunusian Social Business

2.2. Economic Implications

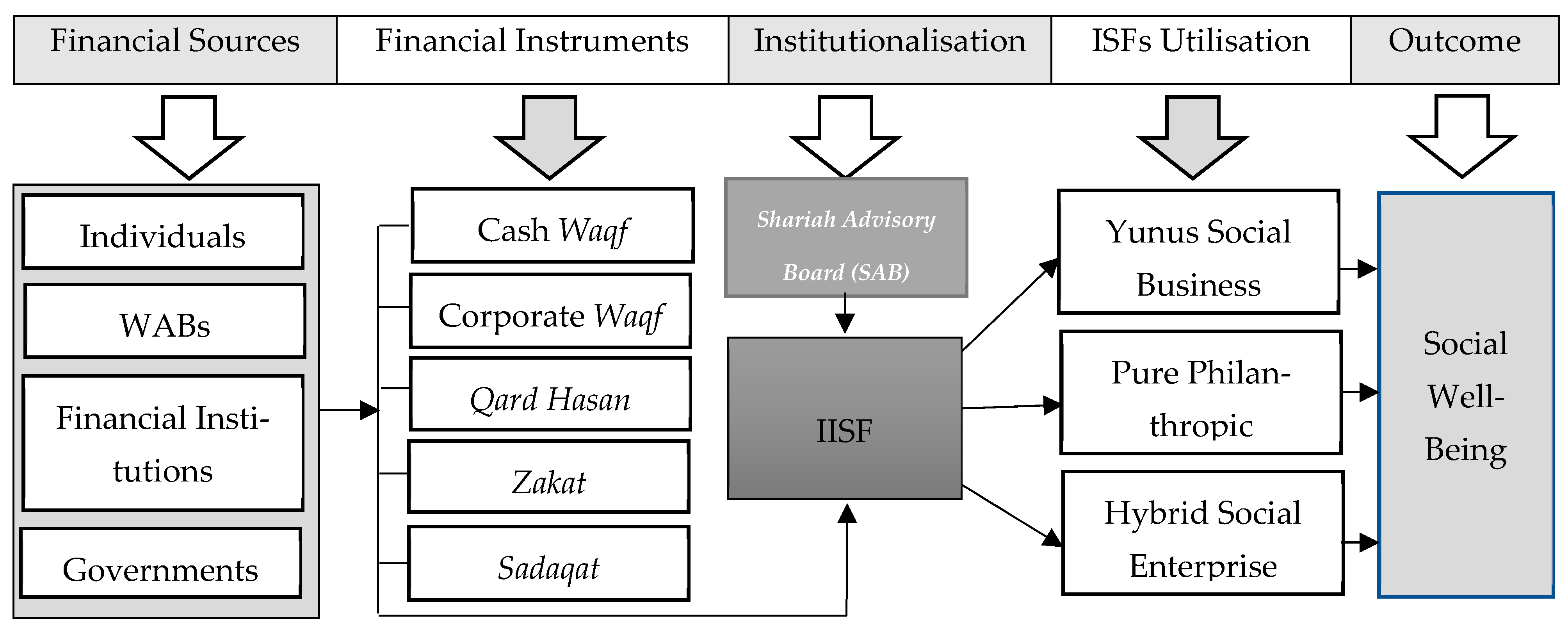

2.3. ISFs for the Socially Responsible Businesses

2.4. Usages of Qard Hasan

“If you give Allah Qard Hasan … he will grant you forgiveness” (Qur’an 64:17).“Establish regular prayer and give regular charity and give Allah Qard Hasan” (Qur’an 73:20).“Who is he that will give Allah Qard Hasan? For Allah will increase it manifold to his credit” (Qur’an 57:11).[Translation: (Islamic Relief Worldwide n.d.)]

2.5. Usages of Cash and Corporate Waqf

2.6. Social Enterprise (SE)

2.7. ISFs for Social Enterprises

3. Materials and Method

4. Institutionalisation of ISFs

4.1. Odds and Nexus between YSB and ISFs

4.2. Implications of YSB and SEs to Rejuvenate a Pandemic-Stricken Society

5. Conclusions

5.1. Originality of the Paper

5.2. Limitations

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Abadli, Riad, and Chokri Kooli. 2022. Sustainable Energy Policies in Qatar: On the Green Path. In Sustainable Energy-Water-Environment Nexus in Deserts. Cham: Springer. [Google Scholar]

- Adnan, Muhammad. n.d. If Someone Is Refusing to Pay His Debt. Available online: https://islamqa.org/hanafi/daruliftaa-birmingham/135932/if-someone-is-refusing-to-pay-his-debt/ (accessed on 1 January 2021).

- Aldeen, Khaled Nour, Inayah Swasti Ratih, and Risa Sari Pertiwi. 2021. Cash waqf from the millennials’ perspective: A case of Indonesia. ISRA International Journal of Islamic Finance 14: 20–37. [Google Scholar] [CrossRef]

- Ambrose, Azniza Hartini Azrai Azaimi, and Fadhilah Abdullah Asuhaimi. 2021. Cash waqf risk management and perpetuity restriction conundrum. ISRA International Journal of Islamic Finance 13: 162–76. [Google Scholar] [CrossRef]

- Andriyani, Lilik, Nurodin Usman, and Zulfikar Bagus Pambuko. 2020. Antecedents of Social Funds Productivity of Islamic Banks in Indonesia. Humanities & Social Sciences Reviews 8: 488–94. [Google Scholar] [CrossRef] [Green Version]

- Aydin, Necati. 2015. Islamic social business for sustainable development and subjective wellbeing. International Journal of Islamic and Middle Eastern Finance and Management 8: 491–507. [Google Scholar] [CrossRef]

- BNM. 2018. Value-Based Intermediation: Strengthening the Roles and Impact of Islamic Finance. Bank Negara Malaysia (BNM/RH/DP 034–2). Available online: https://www.bnm.gov.my/documents/20124/761682/Strategy+Paper+on+VBI.pdf/b299fc38-0728-eca6-40ee-023fc584265e?t=1581907679482 (accessed on 12 August 2021).

- Chowdhury, Md Shahedur Rahaman, Mohd Fahmi bin Ghazali, and Mohd Faisol Ibrahim. 2011. Economics of Cash WAQF management in Malaysia: A proposed Cash WAQF model for practitioners and future researchers. African Journal of Business Management 5: 12155–63. [Google Scholar]

- Çizarça, Murat. 1995. Cash waqfs of Bursa, 1555–1823. Journal of the Economic and Social History of the Orient 38: 313–54. [Google Scholar] [CrossRef]

- Dacin, Peter A., M. Tina Dacin, and Margaret Matear. 2010. Social entrepreneurship: Why we don’t need a new theory and how we move forward from here. Academy of Management Perspectives 24: 37–57. [Google Scholar]

- Dees, J. Gregory, Jed Emerson, and Peter Economy. 2001. Enterprising Non-Profits: A Toolkit for Social Entrepreneurs. New York: Wiley. [Google Scholar]

- Dong, Feng, Ying Wang, Bin Su, Yifei Hua, and Yuanqing Zhang. 2019. The process of peak CO2 emissions in developed economies: A perspective of industrialisation and urbanisation. Resources, Conservation and Recycling 141: 61–75. [Google Scholar] [CrossRef]

- Faza, Amarta Risna Diah. 2022. Social Business Contribution of Grameen Bank Muhammad Yunus in The Development of Poverty Reduction Discourse in Indonesia. International Economic and Finance Review 1: 54–84. [Google Scholar] [CrossRef]

- Goda, Thomas, Özlem Onaran, and Engelbert Stockhammer. 2017. Income inequality and wealth concentration in the recent crisis. Development and Change 48: 3–27. [Google Scholar] [CrossRef] [Green Version]

- Hakim, Andi, and Zuliani Dalimunthe. 2022. The Probability of the Financing Sustainability of Micro-firms Supported by Islamic Social Fund. Etikonomi 21: 127–38. [Google Scholar] [CrossRef]

- Islamic Relief Worldwide. n.d. Qard Hasan (Benevolent Loan). Available online: https://islamic-relief.org/qard-hassan-benevolent-loan/ (accessed on 26 March 2023).

- Ismail Abdel Mohsin, Magda. 2014. Corporate Waqf: From Principle to Practice: A New Innovation for Islamic Finance. Kuala Lumpur: Pearson Malaysia Sdn Bhd. [Google Scholar]

- Issa, Jabbar Sehen, Mohammad Reza Abbaszadeh, and Mahdi Salehi. 2022. The Impact of Islamic Banking Corporate Governance on Green Banking. Administrative Sciences 12: 1–20. [Google Scholar]

- Karmakar, Asim K., and Sebak K. Jana. 2022. Globalisation, Income Inequality, and Wealth Disparity: Issues and Evidence Globalisation, Income Distribution and Sustainable Development. Bingley: Emerald Publishing Limited. [Google Scholar]

- Kickul, Jill, Siri Terjesen, Sophie Bacq, and Mark Griffiths. 2012. Social business education: An interview with Nobel laureate Muhammad Yunus. Academy of Management Learning & Education 11: 453–62. [Google Scholar]

- Kooli, Chokri. 2020. Islamic financing initiatives stimulating SMEs creation in Muslim Countries. Journal of Islamic Research 31: 266–79. [Google Scholar] [CrossRef]

- Kooli, Chokri, Mohammed Shanikat, and Raed Kanakriyah. 2022. Towards a new model of productive Islamic financial mechanisms. International Journal of Business Performance Management 23: 17–33. [Google Scholar] [CrossRef]

- Mair, Johanna, and Ignasi Marti. 2006. Social entrepreneurship research: A source of explanation, prediction, and delight. Journal of World Business 41: 36–44. [Google Scholar] [CrossRef]

- Majid, Rifaldi. 2021. The Model of Islamic Social Fund (Zakah, Infaq, Sadaqah, and Waqf) Utilisation through Synergy of the Mosque-Baitul Maal Wat Tamwil as an Economic Stimulus for Micro and Small Enterprises. In Islamic Sosial Finance and Its Role for Achieving Sustainable Development Goals: Islamic Economics Winter Course. Kota Bogor: PT Penerbit IPB Press, p. 227. [Google Scholar]

- Messabia, Nabil, Paul-Rodrigue Fomi, and Chokri Kooli. 2022. Managing restaurants during the COVID-19 crisis: Innovating to survive and prosper. Journal of Innovation & Knowledge 7: 100234. [Google Scholar]

- Nurrachmi, R. 2012. Implication of cash waqf in the society. AL-INFAQ 3: 150–55. [Google Scholar]

- Saad, Norma Md, Suhaimi Mhd Sarif, Ahmad Zamri Osman, Zarinah Hamid, and Muhammad Yusuf Saleem. 2017. Managing corporate Waqf in Malaysia: Perspectives of selected SEDCs and SIRCs. Jurnal Syariah 25: 91–116. [Google Scholar] [CrossRef]

- Saiti, Buerhan, and Adam Abdullah. 2016. Prohibited elements in Islamic financial transactions: A comprehensive review. Al-Shajarah: Journal of the International Institute of Islamic Thought and Civilization (ISTAC) 21: 139–43. [Google Scholar]

- Sánchez-Páramo, Carolina, Ruth Hill, Daniel Gerszon Mahler, Ambar Narayan, and Nishant Yonzan. 2021. COVID-19 Leaves a Legacy of Rising Poverty and Widening Inequality. Available online: https://blogs.worldbank.org/developmenttalk/covid-19-leaves-legacy-rising-poverty-and-widening-inequality (accessed on 15 January 2023).

- Sgambati, Stefano. 2022. Who owes? Class struggle, inequality and the political economy of leverage in the 21st century. Finance and Society 8: 1–23. [Google Scholar] [CrossRef]

- Smith, Nicola. 2023. Neoliberalism. Bitannica. Available online: https://www.britannica.com/topic/neoliberalism (accessed on 30 March 2023).

- Sugahara, Cibele Roberta, Giovanni Moreira Rocha Campos, Marina Ardito Massaioli, Bruna Nunes Fantini, and Denise Helena Lombardo Ferreira. 2021. Social business: A report on social impacts. Independent Journal of Management & Production 12: 15–31. [Google Scholar]

- Sugianto, Sugianto, Andri Soemitra, Muhammad Yafiz, Ahmad Amin Dalimunthe, and Reza Nurul Ichsan. 2022. The implementation of waqf planning and development through Islamic financial institutions in Indonesia. JPPI (Jurnal Penelitian Pendidikan Indonesia) 8: 275–88. [Google Scholar] [CrossRef]

- The World Bank. 2022. Poverty. Available online: https://www.worldbank.org/en/topic/poverty/overview#:~:text=The%20number%20of%20people%20in,steepest%20costs%20of%20the%20pandemic (accessed on 6 March 2023).

- Uddin, Md Akther. 2015. Principles of Islamic finance: Prohibition of riba, gharar and maysir. Munich Personal RePEc Archive 67711: 1–8. [Google Scholar]

- UNICEF. 2019. UNICEF and the Islamic Development Bank Launch First Global Muslim Philanthropy Fund for Children. Available online: https://www.unicef.org/press-releases/unicef-and-islamic-development-bank-launch-first-global-muslim-philanthropy-fund#:~:text=It%20is%20estimated%20that%20global,to%20help%20achieve%20the%20SDGs (accessed on 15 January 2023).

- Volkmann, Ch, K. Tokarski, and Kati Ernst. 2012. Social Entrepreneurship and Social Business. An Introduction and Discussion with Case Studies. Wiesbaden: Gabler. [Google Scholar]

- Wang, Zhaohua, Yasir Rasool, Bin Zhang, Zahoor Ahmed, and Bo Wang. 2020. Dynamic linkage among industrialisation, urbanisation, and CO2 emissions in APEC realms: Evidence based on DSUR estimation. Structural Change and Economic Dynamics 52: 382–389. [Google Scholar] [CrossRef]

- Widiastuti, Tika, Sri Ningsih, Ari Prasetyo, Imron Mawardi, Sri Herianingrum, Anidah Robani, Muhammad Ubaidillah Al Mustofa, and Aufar Fadlul Hady. 2022. Developing an integrated model of Islamic social finance: Toward an effective governance framework. Heliyon 8: e10383. [Google Scholar] [CrossRef]

- Yazdi, Najmoddin, Ali Marvi, and Ali Maleki. 2021. Iran and COVID-19: An alternative crisis management system based on bottom-up Islamic social finance and faith-based civic engagement. In COVID-19 and Islamic Social Finance. London: Routledge. [Google Scholar]

- Yunus Social Business. 2019. The Social Business Revolution: Why Is Venture Philanthropy the Most Effective Form of Giving? Available online: https://www.yunussb.com/articles/the-social-business-revolution-why-is-venture-philanthropy-the-most-effective-form-of-giving#:~:text=Our%20Chairman%20and%20Co%2DFounder,of%20a%20traditional%20charity%20donation (accessed on 7 January 2023).

- Yunus, Muhammad. 2010. Building Social Business: The New Kind of Capitalism that Serves Humanity’s Most Pressing Needs. New York City: PublicAffairs. [Google Scholar]

- Yunus, Muhammad, Bertrand Moingeon, and Laurence Lehmann-Ortega. 2010. Building Social Business Models: Lessons from the Grameen Experience. Long Range Planning 43: 308–25. [Google Scholar] [CrossRef]

- Zimon, Grzegorz, Hossein Tarighi, Mahdi Salehi, and Adam Sadowski. 2022. Assessment of Financial Security of SMEs Operating in the Renewable Energy Industry during COVID-19 Pandemic. Energies 15: 9627. [Google Scholar] [CrossRef]

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Islam, R.; Omar, M.; Rahman, M. Islamic Social Funds to Foster Yunusian Social Business and Conventional Social Enterprises. Adm. Sci. 2023, 13, 102. https://doi.org/10.3390/admsci13040102

Islam R, Omar M, Rahman M. Islamic Social Funds to Foster Yunusian Social Business and Conventional Social Enterprises. Administrative Sciences. 2023; 13(4):102. https://doi.org/10.3390/admsci13040102

Chicago/Turabian StyleIslam, Reazul, Mustaffa Omar, and Mahfuzur Rahman. 2023. "Islamic Social Funds to Foster Yunusian Social Business and Conventional Social Enterprises" Administrative Sciences 13, no. 4: 102. https://doi.org/10.3390/admsci13040102