1. Introduction

Over the past decades, organizations have dramatically changed their strategies and processes. The prime motives behind these changes are digitization (

Fang et al. 2021) and the dynamic and turbulent business environment (

Fan et al. 2021). Moreover, the constant development of new technologies has led to high competition (

Ali et al. 2022;

Ali and Johl 2022a). Additionally, the current pandemic situation further accelerates the situation (

Alsharif et al. 2021). Therefore, the competitive nature of the firm environment has further accelerated the need for organizations to articulate strategies that support the firms’ interests and give them competitive advantages (

Isichei et al. 2020). To gain a competitive advantage in this situation, an organization needs deliberate internal behavior that promotes fundamental changes in the process. Consequently, it allows organizational creativity, commitment, and new ideas (

Nguyen et al. 2021). Such internal behavior is referred to as entrepreneurial orientation (EO).

The entrepreneurial orientation (EO) concept emerged in the 1970s, after which it gained considerable attention from researchers and practitioners. According to

Miller (

1983), EO means “entrepreneurial firm engages in product-market innovation, undertakes somewhat risky ventures, and is first to come up with proactive innovations beating competitors to the punch”. The prior literature highlights that entrepreneurial orientation (EO) plays an important role in enhancing firm performance (

Bin Yusoff et al. 2021;

Fang et al. 2021). However, much research has provided varying evidence on the relationship between EO and performance. For instance,

Isichei et al. (

2020) found a positive relationship between EO and performance. Likewise,

Hernandez-Perlines and Cisneros (

2017) found a positive association between EO–performance relationships. On the other hand, some studies found a weak, negative, or no relationship between EO performance (

Shirokova et al. 2016;

Mazhar et al. 2022a). Moreover, some dimensions of EO positively affect performance, and others have no relationship. For instance, the research of

Isichei et al. (

2020) found that two dimensions of EO (innovativeness and proactiveness) have a positive relationship with performance, whereas risk-taking has no significant effect on performance. Similarly,

Rezaei and Ortt (

2018) affirmed that innovativeness and proactiveness (EO) have a positive relationship with performance, and risk-taking negatively affects performance. In a nutshell, the existing studies cannot resolve the contradictions between EO and performance relationships.

Rezaei and Ortt (

2018) and

Wang (

2008) pointed out that past studies on the EO–performance relationship indicated that simply studying EO’s direct effect on performance does not provide a complete picture. Many different mediating variables have been involved in unraveling the mechanism by which EO enhances firm performance. Prior literature has adopted various strategic constructs as mediating variables, such as social media (

Fang et al. 2021;

Fan et al. 2021), marketing communication (

Butkouskaya et al. 2020), outsourcing (

Irwin et al. 2018), and the knowledge creation process (

Li et al. 2009). However, the prior studies ignored the role of a firm competitive strategy as a mediator between the EO–performance relationship, especially cost leadership (

Galbreath et al. 2020). Based on the above discussion, the following research questions have been developed:

RQ1: Does EO has an association with firm performance?

RQ2: Does cost leadership mediate between EO and firm performance?

In the context of this research, the focus area is small- and medium-sized enterprises (SMEs), especially Malaysian SMEs. The selection of SMEs is based on several reasons. First, SMEs contribute more than 70% of the GDP and 80% of the labor market in emerging economies. But still, they lack resources and challenges (

Ali and Johl 2022b;

Fang et al. 2021). Second,

Nguyen et al. (

2021) argued that the industrial society of several emerging economies is based on SMEs that are considered the core elements of a country’s success and failure. Finally, SMEs located in emerging countries usually struggle with their survival. Malaysia, which is an important emerging economy, faces the same dilemma. Therefore, the selection of Malaysian SMEs as the study scope is quite rational.

4. Research Methodology

This study examines the role of EO and cost leadership strategy in achieving SMEs’ performance. Based on the study objectives, the target population is Malaysian service SMEs. According to

SME Corporation Malaysia (

2014), a small enterprise having a regular number of employees between 5 to less than 30 is categorized as small, and a firm having employees between 30 ≤ 75 is categorized as a medium enterprise. The selection of service SMEs is based on factors such as higher establishment and the largest workforce attached to the services sector. Moreover, this sector is a more productive and growth-oriented economic segment. The sampling frame is based on FMM (Federation Malaysian Manufacturers) and CCM (Company Commission Malaysia). The prior literature highlighted that FMM and CCM are considered the sampling frame (

Ali and Johl 2022d). The data are collected from service SMEs in Malaysia’s three states: Selangor, Kula Lumpur, and Johor. According to

Department of Statistics Malaysia (

2020), the economic contributions of these states are more than 50% compared with the rest of the states.

Furthermore, a higher number of SMEs are established in these states. To reach the study population, a simple random sampling technique is adopted. Moreover, the sample size is calculated based on

Krejcie and Morgan (

1970); based on the table, the final sample size is 383. Additionally, the unit of analysis is SME enterprises.

Fan et al. (

2021) argued that the EO concept hovers around the organization rather than individuals. The targeted respondent for this research is SME owner/managers. In the EO–performance literature, researchers argued that SME owners/managers are well informed about the firm internal and external environment and performance. Moreover, they make decisions regarding the adoption of strategy and new technology.

To collect the data from the respondent, a survey technique is adopted. In the survey technique, an online questionnaire was used to collect data. The online questionnaire link was sent to 600 SMEs, and 316 questionnaires were received. The response rate of data collection was 52.6%. After data screening and preliminary data analysis, 283 responses were found valid for further analysis (

Ali and Johl 2022c;

Mazhar et al. 2021). The quantitative method with a cross-sectional design guides the research work. A 5-point Likert scale is adopted to measure the questionnaires, where 1 represents “strongly disagree” and 5 represents “strongly agree”. Before actual data collection, the pretesting and pilot testing steps are performed. The pilot testing results indicate that all the variables achieved the threshold value of reliability—additionally, the PLS-SEM technique was used to analyze the collected data through SmartPLS.

Measures

The structure of the scales was determined by referring to previously used measures. However, to apply to the present study, we made a few minor modifications. To measure the variables, constructs items are adapted from the past literature. Proactiveness was measured through five items adapted from

Le Roux et al. (

2014) and

Li et al. (

2009), which measure the concept of the capability of the firm to foresee shifts in market conditions; in particular, shifts in consumer trends; it consequently refers to a proactive attitude to capitalize on market opportunities. A firm’s propensity to engage in risky endeavors that have unpredictable repercussions, such as exposure to debts and risky investments, is what is meant by the term “risk-taking”. The risk-taking construct was measured through five items adapted from

Le Roux et al. (

2014) and

Li et al. (

2009). The competitive aggressiveness of a company refers to its demeanor when interacting with other businesses in the industry. It consists of continuously monitoring and combating competitors’ techniques (even if it means imitating other companies) to gain a competitive edge and perform more effectively. Competitive aggressiveness was measured through five items adapted from

Le Roux et al. (

2014) and

Li et al. (

2009). The concept of autonomy refers to a tendency toward favorable situations for the creation and, later, the implementation of new ideas. One definition of autonomy in the workplace is a culture that encourages new ventures without stifling creative expression at the individual level. Autonomy was measured through five items adapted from

Alvarez-Torres et al. (

2019) and

Li et al. (

2009). Open innovation refers to a dispersed invention process built on the purposefully managed flow of information across organizational borders. This type of innovation uses monetary and non-monetary incentives, and it is aligned with the firm’s business model. Open innovation was measured through five items adapted from

Fu et al. (

2019). Cost leadership is known to produce services at lower costs than possible competitors to achieve competitiveness. In this research, cost leadership is a mediating variable measured through five items adapted from

Bayraktar et al. (

2017). Finally, firm performance is the dependent variable measured through five items adapted from

Fang et al. (

2021).

6. Discussion and Conclusions

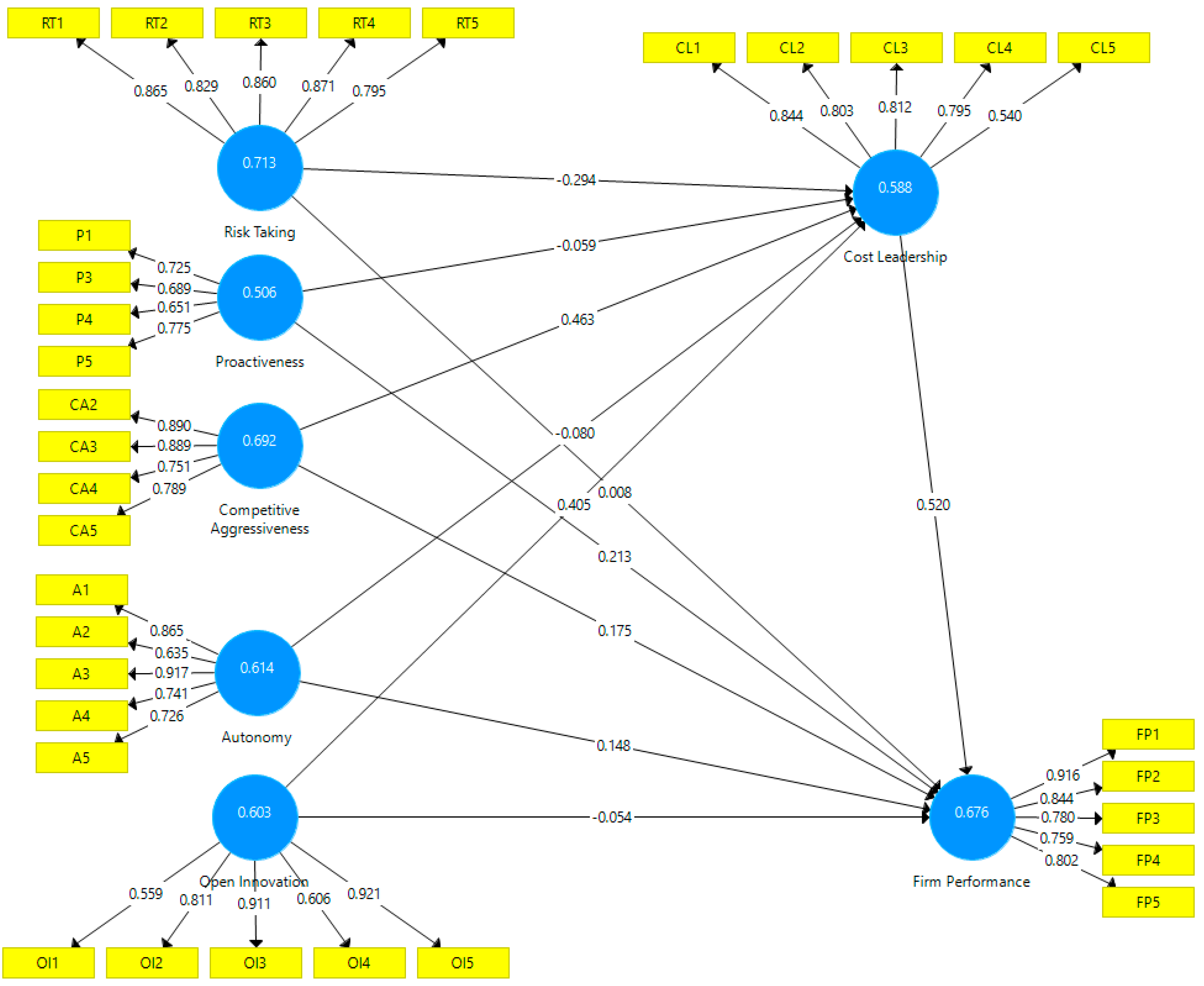

This section presents a discussion of the statistical findings of the current study, the major objective of which is to examine the relationship between the exogenous variables (autonomy, proactiveness, competitive aggressiveness, open innovation, risk-taking) and the dependent variable (firm performance) through the mediating role of cost leadership.

The empirical findings highlight that risk-taking has no direct relationship with Malaysian SMEs’ performance. Thus, H1 has been rejected. Risk-taking and the capacity to have the lowest costs are typically the outcomes of innovativeness, whether incremental or radical, which is one of the reasons for the unfavorable results in this research. To undercut rivals, a cost leadership strategy offers an internal orientation in which the organization focuses on efficiency and cost management. Marketing standardized goods is a common way to save costs (generally of low added value).

As a consequence, investing resources in activities such as experimentation, risk-taking, or innovation may jeopardize the successful execution of a cost leadership strategy (

Dhliwayo 2014). Furthermore, the findings highlight that proactiveness is significantly related to SMEs’ performance.

Fan et al. (

2021) and

Alvarez-Torres et al. (

2019) support this study’s findings. Therefore, H2 has been accepted. Likewise, competitive aggressiveness and autonomy have a positive and significant relationship with SMEs’ performance; thus, H3 and H4 are accepted. These results are supported by the past literature. For instance,

Alvarez-Torres et al. (

2019) found a positive and significant relationship between SMEs’ performance in the Mexican context. The empirical work of

Susanto et al. (

2021) found that EO has a positive relationship with SME performance in developing economies. The empirical findings surprisingly highlight that open innovation and firm performance have no direct association. Hence, H5 has been rejected. The findings are supported by the past literature.

Zhang et al. (

2018) argued that there is a lack of technical work in SMEs. They further argued that education is essential to promote innovation in organizations.

Finally, the study hypothesized that cost leadership strategy has a mediating role between EO and SME performance. The empirical findings highlight that cost leadership has a full mediation between risk-taking, open innovation, and firm performance, and partial mediation between competitive aggressiveness and performance. On the other hand, cost leadership is often based on price competitiveness, in which the business is already aware of market demand and, hence, offers a comparable product at a lower price (

Linton and Kask 2017). However, the research is unclear on how risk-taking and cost leadership interact. As a result, hypothesis 7 proposed that risk-taking is linked to cost leadership. Cost leadership aims to achieve the lowest cost structure for a similar service while also increasing efficiency. A cost-cutting plan requires a framework that prioritizes controls and accountability for outcomes via work standards (

Brock 2014). Small businesses are often characterized by a lack of formalization and simple control systems (

Birley and Norburn 1985;

Lechner and Leyronas 2009), resulting in increased autonomy. A top-down strategy is often related to cost leadership, but bottom-up initiatives are frequently bolstered by autonomy. Autonomy should be limited to adopting a cost leadership approach (

Lechner and Gudmundsson 2014).

6.1. Contributions and Implications

This study addresses the essential need for greater research on the intersection between EO postures, open innovation, and competitive strategy by revealing how these factors interact and affect company performance when they work together. The uniqueness of the current study is using cost leadership as a mediating variable between EO, open innovation, and firm performance. To the best of the researcher’s ability, the limited study adopted cost leadership as a mediating variable between EO, open innovation, and firm performance.

The SMEs sector is often regarded as the most important global economic growth and development driver. It also contributes to poverty alleviation by giving jobs. This study aids and stimulates SMEs to embrace creative concepts and fresh techniques to improve society’s tendencies. Poor and under-supported cultures in developing countries, for example, are often unable to launch large-scale businesses. As a result, EO, open innovation, and strategies may provide new ways to improve performance.

Furthermore, the research has contributed to the area of entrepreneur development strategies. Despite SMEs’ low risk-taking proclivity, government agencies’ efforts to promote healthy growth and development will need to be re-strategized. New methods and techniques must include not just the low risk-taking proclivity of SME entrepreneurs, but also the long-term plan of instilling a higher-risk-taking culture among them. According to a previous study, culture significantly impacts an entrepreneur’s risk-taking behavior; hence, the acculturation of entrepreneurial risk-taking behavior must begin early in the family and community. Efforts to convert Malaysian society toward entrepreneurship must be stepped up, and it would be more successful if the government developed a long-term entrepreneurship strategy to assure a steady supply of dynamic and resilient entrepreneurs and those who are more risk-averse. Once SME entrepreneurs’ risk-taking propensity is greater, it may be easier for the currently existing SMEs to grow into stronger and larger entrepreneurial entities that will help the country’s economic development. In summary, organizations engaged in developing entrepreneurs, ministries, financial institutions, and government economic planners in the nation must build and enhance the risk-taking propensities of entrepreneurs via innovative techniques and tactics (

Salleh and Ibrahim 2013).

6.1.1. Theoretical Contributions

From a theoretical standpoint, it has been shown that combining the various sub-components of EO may result in improved performance. Linton and Kask have proposed this theory (2017). The major sub-components in this research include risk-taking autonomy, competitive aggressiveness, and proactiveness, which vary from the significant sub-components discovered by

Linton and Kask (

2017). This demonstrates that the statistical significance of the EO sub-component varies depending on the data sample. The research on the sub-components of EO reveals that the mix of these components and how they interact together is critical for achieving the best firm performance (

Zhang et al. 2018). The organization must create a supporting framework to guarantee that its staff should have the necessary resources and competencies to support the EO sub-component capability’s drive. Through the sub-components of innovativeness and risk-taking, it is obvious in this research that organizations will profit from not being extremely entrepreneurial. Instead, they should concentrate on the other three sub-components, which are glamorous and positively impact corporate performance.

6.1.2. Practical Implications

This research makes several practical contributions that will be advantageous to SMEs’ owners, managers, and policymakers. From a practical standpoint, the most important management consequence of the research is that SME enterprises must build distinctive cost leadership within their divisions to improve performance and compete in changing marketplaces. Similarly, to improve performance, businesses must foster an entrepreneurial atmosphere. Both variables assist organizations in making balanced investments in various product development activities and avoid large investments in riskier ventures to secure long-term success. For companies operating in developing markets, it is worth noting that EO and cost leadership help them achieve outstanding performance and improve it. Similarly, responsible managers of firms operating in established markets may pay close attention to cost leadership to improve performance. To be more specific, Malaysian businesses must prioritize cost leadership, followed by EO, to grow and survive. The results assist the government and the Small and Medium Enterprises Development Authority in formulating policies and initiating programs for SMEs’ development and sustainability. The importance of SMEs in the country’s economic progress should not be overlooked. Because Malaysia has characteristics of both developing and established markets, the conclusions of this research may assist other nations in altering their policies to enhance SME development and ensure the industrial sector’s survival. For example, the global business sector has a high failure rate, and many businesses fail to survive for lengthy periods. As a result, the researchers believe that a company’s internal skills should be reinforced to adapt to unforeseen shocks and market pressures. This research indicates that EO is more important for performance enhancement. Many enterprises fail in the early stages of development in both developed and emerging economies due to resource constraints. This study allows freshly created businesses to use less costly strategies to improve performance. Furthermore, owing to a lack of assistance and harsh market circumstances, EO and cost leadership are critical for SMEs’ performance.

6.2. Limitations and Future Research Avenues

As with previous studies, this one has recognized several limitations that indicate promising areas for future research and may need to be considered in the future, such as the data and target demographic, as we only looked at one developing market. The current study looked for a direct effect of EO and cost leadership dimensions on performance, although earlier research has shown that various variables may influence the link between EO and SMEs’ performance.

Kantur (

2016), for example, claimed that strategic entrepreneurship has a complete mediating function between EO performance in developing markets or that strategic entrepreneurship mediates between cost leadership and SMEs’ success. Similarly, other researchers have shown that awareness creation (

Li et al. 2009), strategic partnerships (

Brouthers et al. 2015), and other moderators and mediators may exaggerate the association between EO and performance. Furthermore,

Chryssochoidis et al. (

2016) discovered that although competitive strategy does not directly boost performance, it does mediate the connection via internal capacities. As a result, an additional study may be performed to examine the link between EO and cost leadership, as well as other potential moderators, such as financial capacities and executive and owner characteristics, because a company that wants to pursue entrepreneurial activities and differentiated product development methodologies may need financial assistance. Furthermore, since the research is being undertaken in an emerging market, a comparison study may be conducted to acquire useful data from other countries concerning the relevance of EO and cost leadership in financial and non-financial performance. The current study has discovered that different dimensions of EO have different effects on firm functions and performance; it will be interesting to see if these findings hold for a larger population of firms and if there are other dimensions of EO and other functions within the firm that can be distinguished. The approach is now being evaluated for SMEs in Malaysia. Future research might broaden the scope of the study to include bigger enterprises and firms from different nations.

Furthermore, like other EO investigations, the present study used cross-sectional data, which precludes the unequivocal proof of underlying causation between the dimensions of interest. According to

Miller (

2011), the EO literature mostly depends on self-reported and perceptual measurements, which might lead to respondent bias in the sample. The difficulties of retrieving data on SMEs, particularly in cultures such as Malaysia, where most economic activity is done off the books, are well recognized. Still, future studies will benefit from establishing alternative EO metrics that employ archival data. The study is also aware that in countries such as Malaysia, significant differences exist between different parts of the country and the extent to which support for the predictions tested here varies between samples drawn from different regions of the country, which is something that needs to be investigated further in the future.

Similarly, more research is needed to see whether the conclusions of this study can be applied to other growing economies such as Thailand, Indonesia, and India. Furthermore, several contextual elements, such as leadership traits, organizational culture, and internal reward and reinforcement processes, have an impact on a company. These variables will have an impact on the relationship between EO and performance, and they should be investigated further. Evaluating the impact on EO of these many aspects, whether from the environment or inside the organization, might be a suitable starting point for future study.

{kind=link}

{kind=link}

{kind=link}