Reprioritising Sustainable Development Goals in the Post-COVID-19 Global Context: Will a Mandatory Corporate Social Responsibility Regime Help?

Abstract

:1. Introduction

2. CSR–SDG Linkages: An Exploration

Indian Companies Act (2013) and SDGs

3. Linking CSR with SDGs: Devising Strategies and Actions in the Post-Pandemic World

4. Conclusions and Imperatives for Research, Policies and Actions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

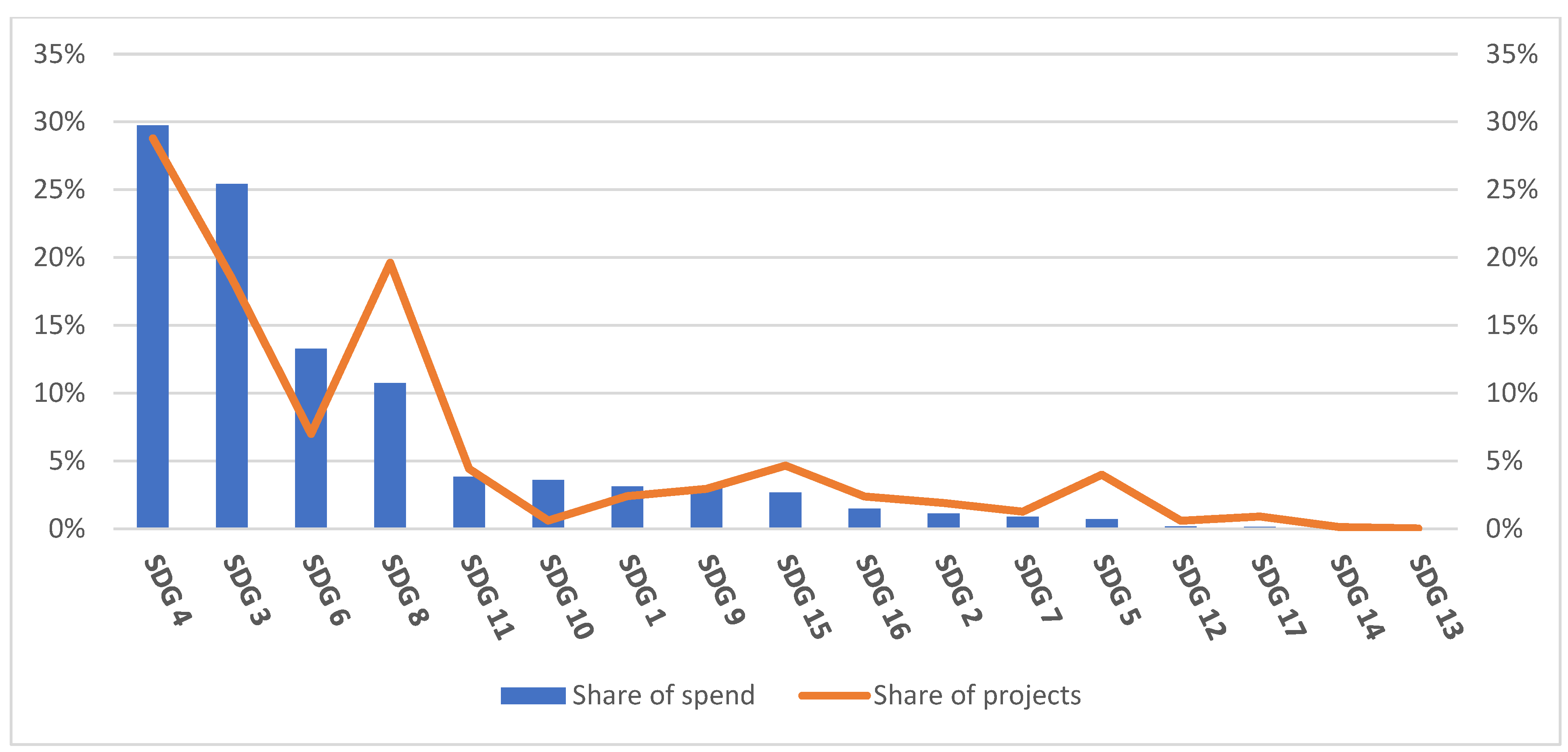

Appendix B. CSR Expenditure by Indian Firms: 2014–2019

| Breakdown of Item 6 | CSR Expenditure by Indian Firms (Amounts in INR Crores. 1 Crore = 10 Million) (USD = INR 73.74) | 5 Year Average | |||||

| 2014–2015 | 2015–2016 | 2016–2017 | 2017–2018 | 2018–2019 | 2019 = 2020 | ||

| SDG 1 and 2—Eradicating Hunger, Poverty and Malnutrition | 274.70 | 1252.08 | 606.55 | 654.80 | 1090.27 | 818.29 | 20% |

| SDG 3—Healthcare | 1847.74 | 2569.43 | 2491.09 | 2210.77 | 3216.41 | 3438.27 | 66% |

| SDG 6—Safe Drinking Water and Sanitation | 403.49 | 811.96 | 569.50 | 473.50 | 652.56 | 608.49 | 15% |

| Source: National CSR Portal, https://www.csr.gov.in/developmentlist.php, accessed on 7 May 2021. | |||||||

| 1 | https://sustainabledevelopment.un.org/?menu=1300 (accessed on 24 September 2021). |

| 2 | USD = INR 73.74. |

| 3 | SDG 10 targets reducing income inequality within and among countries. Arguably, this can be achieved mainly through national-level policies and coordinated efforts of inter-governmental agencies, treaties and initiatives. SDG 17 refers to cooperation between nations and governments rather than companies. |

| 4 | Our observation about extant infrastructure is based on various media that highlighted the dire situation in India (shortage of hospital beds and oxygen). Data of 2015–2019 provide context to the thrust of the paper that despite the attention given to health, even until just prior to the pandemic, the sector was ill equipped to adequately cope with the demands placed on it by the pandemic. |

| 5 | SDG 1: No Poverty; SDG 2: Zero Hunger; SDG 3: Good Health and Well-Being; SDG 4: Quality Education; SDG 5: Gender Equality; SDG 6: Clean Water and Sanitation |

| 6 | Classification code Grey, representing countries that do not meet the thresholds set for inclusion in the analysis, is not included in Table 1. For a detailed description of the methodology used by Sachs et al. (2019), see: https://www.sdgindex.org/reports/sustainable-development-report-2019/ (accessed on 24 September 2021). |

| 7 | BRICS (Brazil, Russia, India, China and South Africa) is a grouping of the world’s leading emerging economies. In 2019, globally they represented 41% of population, 33% of GDP, 19% of exports and 16% of imports (http://infobrics.org/post/31036/#:~:text=The%20share%20of%20BRICS%20in,share%20of%20the%20five%20%D1%81ountries) (accessed on 24 September 2021). |

| 8 | Since the CSR mandate was effective from 1 April 2014, the period 2014–2019 was studied to judge the possible impact of the mandate. For comparative purposes, we also measured the HDI value change over the period 2010–2013 and found that India performed on par with the other countries. Thus, we arrive at a reasonable supposition that the CSR mandate played a role in channelling CSR towards projects that led to an improvement in the HDI of India. |

| 9 | USD-INR = 73.74. |

| 10 | The Council of European Union (2012) defines electronic waste or e-waste as any end-of-life (EoL) piece of equipment that depends on electric currents or electromagnetic fields to function properly and includes all components, sub-assemblies and consumables that constituted the product when discarded. E-waste is generated when electronic and electrical equipment become unfit for their initially planned use or have elapsed the expiry date. Examples of e-wastes are: computers, mainframes, servers, monitors, compact discs (CDs), calculators, fax machines, scanners, printers, copiers, battery cells, cellular phones, transceivers, TVs, iPods, medical apparatus, washing machines, refrigerators and air conditioners. |

References

- Abdelhalim, Khalid, and Amani Gamal Eldin. 2019. Can CSR help achieve sustainable development? Applying a new assessment model to CSR cases from Egypt. International Journal of Sociology and Social Policy 39: 773–95. [Google Scholar] [CrossRef]

- Alon, Titan, Matthias Doepke, Jane Olmstead-Rumsey, and Michèle Tertilt Alon. 2020. The Impact of the Coronavirus Pandemic on Gender Equality. COVID Economics, Centre for Economic Policy Research 4: 62–85. [Google Scholar]

- Alvarado-Herrera, Alejandro, Enrique Bigne, Joaquın Aldas-Manzano, and Rafael Curras-Perez. 2017. A scale for measuring consumer perceptions of corporate social responsibility following the sustainable development paradigm. Journal of Business Ethics 140: 243–62. [Google Scholar] [CrossRef]

- Amaeshi, Kenneth, Emmanuel Adegbite, and Tazeeb Rajwani. 2016. Corporate social responsibility in challenging and non-enabling institutional contexts: Do institutional voids matter? Journal of Business Ethics 134: 135–53. [Google Scholar] [CrossRef] [Green Version]

- Banerjee, Sudeshna Ghosh, Jennifer M. Oetzel, and Rupa Ranganathan. 2006. Private provision of infrastructure in emerging markets: Do institutions matter? Development Policy Review 24: 175–202. [Google Scholar] [CrossRef]

- Bao, Rui, and Acheng Zhang. 2020. Does lockdown reduce air pollution? Evidence from 44 cities in Northern China. Science of the Total Environment 731: 139052. [Google Scholar] [CrossRef]

- Barros, Denise Franca, Joao Felipe Rammelt Sauerbronn, and Alessandra Mello da Costa. 2014. Corporate sustainability discourses in a Brazilian business magazine. Social Responsibility Journal 10: 4–20. [Google Scholar] [CrossRef]

- Bhowmick, Soumya. 2020. COVID-19 ‘Infecting’ Sustainable Development Goals. Asia Times Financial. Available online: https://asiatimes.com/2020/04/COVID-19-infecting-sustainable-development-goals/ (accessed on 7 May 2020).

- Bonin, Sandrine, Wafa Singh, Veena Suresh, Tarek Rashed, Kuiljeit Uppaal, Rajiv Nair, and Rao R. Bhavani. 2021. A priority action roadmap for women’s economic empowerment (PARWEE) amid Covid-19: A co-creation approach. International Journal of Gender and Women’s Empowerment 13: 142–61. [Google Scholar] [CrossRef]

- Broom, Fiona, and Gareth Willmer. 2020. SDG Setback ‘Tremendous’ as COVID-19 Accelerates Slide. SciDevNet. Available online: https://www.scidev.net/global/sdgs/feature/sdg-setback-tremendous-as-COVID-19-accelerates-slide.html?__cf_chl_jschl_tk__=5b61fd3d24c3a2fd7b97b52914fd7088abdd33fe-1592806897-0-AbGT2X0xHZvRldgIuoe5UKtoUeEjzMJIlsreDfaeNVkhwpe91t-SMR-RBTDWKDxbcBtYqF3e8dvtJghvZlLCaNY-7Kdv5qZBmV207mW-gl1Bl9QI9tl8tTxkLROAwkZLhwMQo918rBlVNVMQnCQtnQfrJk-g55LWlq39rTP--BV_caHLDJP37Nx9i_w4t5cAf0xC6RNtKx3k8kz51VUz1KECpYvO6NXNxlMbUlfGAYX3GAiV9V8DIoHHhKqZNXj09sl-o179ED1JixQQFwzBST0s48suabYIy1mxuG2Pd5-rZ5dNE5yocazQos5h_osX4KUFDn6l1q9kp96tN2ErhnklyW_u6PahnVmQ-ZHLQNPSQS6tKZg1k5fW8_3dJQWyTw (accessed on 3 June 2020).

- Bruton, Garry D., Shaker A. Zahra, Andrew H. Van de Ven, and Michael A. Hitt. 2021. Indigenous theory uses, abuses, and future. Journal of Management Studies. Available online: https://onlinelibrary.wiley.com/doi/abs/10.1111/joms.12755 (accessed on 7 May 2020).

- Bulgacov, Sergio, Maria Paola Ometto, and Márcia Ramos May. 2015. Differences in sustainability practices and stakeholder involvement. Social Responsibility Journal 11: 149–60. [Google Scholar] [CrossRef] [Green Version]

- Child, John, and David K. Tse. 2001. China’s transition and its implications for international business. Journal of International Business Studies 32: 5–21. [Google Scholar] [CrossRef]

- Chintrakarn, Pandej, Pornsit Jiraporn, Napatsorn Jiraporn, and Travis Davidson. 2017. Estimating the effect of corporate social responsibility on firm value using geographic identification. Asia-Pacific Journal of Financial Studies 46: 276–304. [Google Scholar] [CrossRef]

- Cohen, Erik, and Scott A. Cohen. 2015. Beyond Eurocentrism in tourism: A paradigm shift to mobilities. Tourism Recreation Research 40: 157–68. [Google Scholar] [CrossRef] [Green Version]

- CRISIL. 2020. Doing Good in Bad Times. Available online: https://www.crisil.com/content/dam/crisil/our-analysis/reports/corporate/documents/2020/06/doing-good-in-bad-times.pdf (accessed on 19 September 2020).

- Delai, Ivete, and Sérgio Takahashi. 2011. Sustainability measurement system: A reference model proposal. Social Responsibility Journal 7: 438–71. [Google Scholar] [CrossRef]

- Doh, Jonathan, Suzana Rodrigues, Ayse Saka-Helmhout, and Mona Makhija. 2017. International business responses to institutional voids. Journal of International Business Studies 48: 293–307. [Google Scholar] [CrossRef]

- ElAlfy, Amr, Nicholas Palaschuk, Dina El-Bassiouny, Jeffrey Wilson, and Olaf Weber. 2020. Scoping the Evolution of Corporate Social Responsibility (CSR) Research in the Sustainable Development Goals (SDGs) Era. Sustainability 12: 5544. [Google Scholar] [CrossRef]

- Galuppo, Laura, Mara Gorli, Giuseppe Scaratti, and Cesare Kaneklin. 2014. Building social sustainability: Multi-stakeholder processes and conflict management. Social Responsibility Journal 10: 685–701. [Google Scholar] [CrossRef]

- Ghosh, Anupam, and Chhanda Chakraborti. 2010. Corporate Social Responsibility: A Developmental Tool for India. IUP Journal of Corporate Governance 9: 40–56. [Google Scholar]

- Gössling, Stefan, Daniel Scott, and C. Michael Hall. 2020. Pandemics, tourism and global change: A rapid assessment of COVID-19. Journal of Sustainable Tourism 29: 1–20. [Google Scholar] [CrossRef]

- Hakovirta, Marko, and Navodya Denuwara. 2020. How COVID-19 Redefines the Concept of Sustainability. Sustainability 12: 3727. [Google Scholar] [CrossRef]

- He, Hongwei, and Lloyd Harris. 2020. The impact of COVID-19 pandemic on corporate social responsibility and marketing philosophy. Journal of Business Research 116: 176–82. [Google Scholar] [CrossRef] [PubMed]

- Hilty, Lorenz M., and Bernard Aebischer. 2015. ICT for Sustainability: An Emerging Research Field. In ICT Innovations for Sustainability. Advances in Intelligent Systems and Computing. Edited by Lorenz M. Hilty and Bernard Aebischer. Cham: Springer, vol. 310. [Google Scholar]

- Hoque, Nazamul, Abdul Rahim Abdul Rahman, Rafiqul Islam Molla, Abu Hanifa Md. Noman, and Mohammad Zahid Hossain Bhuiyan. 2018. Is corporate social responsibility pursuing pristine business goals for sustainable development? Corporate Social Responsibility and Environmental Management 25: 1130–42. [Google Scholar] [CrossRef]

- IICA (Indian Institute of Corporate Affairs). 2020. Business Response to COVID-19 through CSR. Available online: https://iica.nic.in/images/CSR_COVID_Publication.pdf (accessed on 18 October 2020).

- Jayaprakash, Parvathi, and R. Radhakrishna Pillai. 2018. Role of Indian ICT Organisations in Realising Sustainable Development Goals through Corporate Social Engagement. In Digital India. Advances in Theory and Practice of Emerging Markets. Edited by Arpan Kumar Kar and Shuchi Sinha M. P. Gupta. Cham: Springer. [Google Scholar] [CrossRef]

- Kane, Emily W. 1995. Education and Beliefs about Gender Inequality. Social Problems 32: 74–90. [Google Scholar] [CrossRef]

- Palepu, Krishna G., and Tarun Khanna. 1998. Institutional voids and policy challenges in emerging markets. The Brown Journal of World Affairs 5: 71–78. [Google Scholar]

- Kopnina, Helen. 2016. The victims of unsustainability: A challenge to sustainable development goals. International Journal of Sustainable Development and World Ecology 2: 113–21. [Google Scholar] [CrossRef] [Green Version]

- Kumar, Sanjiv, Neeta Kumar, and Saxena Vivekadhish. 2016. Millennium Development Goals (MDGs) to Sustainable Development Goals (SDGs): Addressing Unfinished Agenda and Strengthening Sustainable Development and Partnership. Indian Journal of Community Medicine 41: 1–4. [Google Scholar] [CrossRef] [PubMed]

- Leal Filho, Walter, Franziska Wolf, Amanda Lange Salvia, Ali Beynaghi, Kalterina Shulla, Marina Kovaleva, and Claudio R. P. Vasconcelos. 2020. Heading towards an unsustainable world: Some of the implications of not achieving the SDGs. Discover Sustainability 1: 2. [Google Scholar] [CrossRef]

- Lepoutre, Jan MWN, and Michael Valente. 2012. Fools breaking out: The role of symbolic and material immunity in explaining institutional nonconformity. Academy of Management Journal 55: 285–313. [Google Scholar] [CrossRef]

- Luo, Xueming, and Chitra Bhanu Bhattacharya. 2006. Corporate social responsibility, customer and satisfaction, and market value. Journal of Marketing 70: 1–18. [Google Scholar] [CrossRef]

- Lu, Joanne. 2020. What Will COVID-19 Do to the Sustainable Development Goals? Available online: https://www.undispatch.com/what-will-COVID-19-do-to-the-sustainable-development-goals/ (accessed on 22 May 2020).

- Lu, Jintao, Mengshang Liang, Chong Zhang, Dan Rong, Hailing Guan, Kristina Mazeikaite, and Justas Streimikis. 2021. Assessment of corporate social responsibility by addressing sustainable development goals. Corporate Social Responsibility and Environmental Management 28: 686–703. [Google Scholar] [CrossRef]

- Mair, Johanna, and Ignasi Marti. 2009. Entrepreneurship in and around institutional voids: A case study from Bangladesh. Journal of Business Venturing 24: 419–35. [Google Scholar] [CrossRef]

- MCA (Ministry of Corporate Affairs). 2018. Report of the High Level Committee on Corporate Social Responsibility. Available online: https://www.mca.gov.in/Ministry/pdf/CSRHLC_13092019.pdf (accessed on 15 June 2020).

- Mitra, Nayan, and Bhaskar Chatterjee. 2020. India’s Contribution to the Sustainable Development Goals (SDGs) with Respect to the CSR Mandate in the Companies Act, 2013. In The Future of the UN Sustainable Development Goals, CSR, Sustainability, Ethics & Governance. Edited by Samuel O. Idowu, René Schmidpeter and Liangrong Zu. Cham: Springer, ISBN 978-3-030-21153-0. [Google Scholar] [CrossRef]

- Mukherjee, Sacchidananda. 2020. COVID-19: How to Minimize Uncertainties, Increase Confidence and Achieve Economic Stability in India. In COVID-19: Challenges for the Indian Economy—Trade and Foreign Policy Effects. Edited by AIC-EEPC. New Delhi: ASEAN-India Centre (AIC)—Engineering Export Promotion Council of India (EEPC). [Google Scholar]

- Mulky, Avinash. 2017. Are CSR Activities Directed towards Sustainable Development Goals? A Study in India. Paper presented at International OFEL Conference on Governance, Management and Entrepreneurship, Dubrovnik, Croatia, April 7–8; pp. 266–79. Available online: https://search.proquest.com/docview/1945555843?accountid=38661 (accessed on 21 October 2020).

- Murphy-Graham, Erin, and Cynthia Lloyd. 2016. Empowering adolescent girls in developing countries: The potential role of education. Policy Futures in Education 14: 556–77. [Google Scholar] [CrossRef]

- Nicola, Maria, Zaid Alsafib, Catrin Sohrabic, Ahmed Kerwand, Ahmed Al-Jabird, Christos Iosifidisc, Maliha Aghae, and Riaz Aghaf. 2020. The socio-economic implications of the coronavirus pandemic (COVID-19): A review. International Journal of Surgery 78: 185–93. [Google Scholar] [CrossRef]

- Nurunnabi, Mohammad, Javier Esquer, Nora Munguia, David Zepeda, Rafael Perez, and Luis Velazquez. 2020. Reaching the sustainable development goals 2030: Energy efficiency as approach to corporate social responsibility (CSR). GeoJournal 85: 363–74. [Google Scholar] [CrossRef]

- Osuji, Emeka, and Stanley Emife Nwani. 2020. Achieving Sustainable Development Goals: Does Government Expenditure Framework Matter? International Journal of Management, Economics and Social Sciences 9: 131–60. [Google Scholar] [CrossRef]

- Pieterse, Jan Nederveen. 1996. The development of development theory: Towards critical globalism. Review of International Political Economy 3: 541–64. [Google Scholar] [CrossRef] [Green Version]

- Poddar, Anushree, and Sapna A. Narula. 2020. A Study of Corporate Social Responsibility (CSR) and Sustainable Development Goal (SDG) Practices of the States in India. In Mandated Corporate Social Responsibility, CSR, Sustainability, Ethics & Governance. Edited by Nayan Mitra and Rene Schmidpeter. Cham: Springer. [Google Scholar] [CrossRef]

- Ray, R. Sumantra. 2020. A Glimpse of Hope from Global Investors amidst COVID-19. In COVID-19: Challenges for the Indian Economy—Trade and Foreign Policy Effects. Edited by AIC-EEPC. New Delhi: ASEAN-India Centre (AIC)—Engineering Export Promotion Council of India (EEPC). [Google Scholar]

- Regmi, Kapil Dev, and Pierre Walter. 2017. Modernisation Theory, ecotourism policy, and sustainable development for poor countries of the global south: Perspectives from Nepal. International Journal of Sustainable Development and World Ecology 24: 1–14. [Google Scholar] [CrossRef]

- Sabu, Jithin. 2020. South Asia’s prospects of achieving the SDGs in view of the COVID-19 pandemic. Trade Insight 16: 9–11. [Google Scholar]

- Sachs, Jeffrey, Guido Schmidt-Traub, Christian Kroll, Guillaume Lafortune, and Grayson Fuller. 2019. Sustainable Development Report 2019. New York: Bertelsmann Stiftung and Sustainable Development Solutions Network (SDSN). [Google Scholar]

- Shah, Ruchika. 2020. In the Post COVOD-19 Era, Am Opportunity to Build Back Better. Available online: https://www.forbesindia.com/article/coronavirus/how-has-COVID-19-affected-indias-progress-with-sdgs/59899/1 (accessed on 7 June 2020).

- Shibli, Abdullah. 2020. Sustainable Development Goals: What to Salvage from COVID-19. Inter Press Service. Available online: http://www.ipsnews.net/2020/05/sustainable-development-goals-salvage-COVID-19/ (accessed on 18 June 2020).

- Shingal, Anirudh. 2020. Responding to the COVID-19 Crisis: Policy Priorities for India. In COVID-19: Challenges for the Indian Economy—Trade and Foreign Policy Effects. Edited by AIC-EEPC. New Delhi: ASEAN-India Centre (AIC)—Engineering Export Promotion Council of India (EEPC). [Google Scholar]

- Shulla, Kalterina, Bernd-Friedrich Voigt, Stefan Cibian, Giuseppe Scandone, Edna Martinez, Filip Nelkovski, and Pourya Salehi. 2021. Effects of COVID-19 on the Sustainable Development Goals (SDGs). Discover Sustainability 2: 15. [Google Scholar] [CrossRef]

- Singh, Preet Deep. 2020. MCA Allows COVID-19 under CSR Expenditure: Can/Will Startup Get Money? Invest India: National Investment Promotion and Facilitation Agency. Available online: https://www.investindia.gov.in/team-india-blogs/mca-allows-COVID-19-under-csr-expenditure-can-will-startup-get-money (accessed on 16 August 2020).

- Solberg, Erna, and Nana Addo Dankwa Akufo-Addo. 2020. Why We Can’t Lose Sight of the Sustainable Development Goals during Coronavirus. World Economic Forum. Available online: https://www.weforum.org/agenda/2020/04/coronavirus-pandemic-effect-sdg-un-progress (accessed on 25 May 2020).

- Tsalis, Thomas A., Kyveli E. Malamateniou, Dimitrios Koulouriotis, and Ioannis E. Nikolaou. 2020. New challenges for corporate sustainability reporting: United Nations 2030 Agenda for sustainable development and the sustainable development goals. Corporate Social Responsibility and Environmental Management 27: 1617–29. [Google Scholar] [CrossRef]

- The Council of European Union. 2012. Directive 2012/19/EU of the European Parliament and of the Council of 4 July 2012 on Waste Electrical and Electronic Equipment (WEEE) (Recast). Official Journal of the European Union L 197: 38–71. Available online: http://eur-lex.europa.eu/legal-content/EN/TXT/PDF/?uri=CELEX:32012L0019&from=EN (accessed on 24 September 2021).

- Tjoa, A. Min, and Simon Tjoa. 2016. The Role of ICT to Achieve the UN Sustainable Development Goals (SDG). In ICT for Promoting Human Development and Protecting the Environment. WITFOR 2016. IFIP Advances in Information and Communication Technology. Edited by Francisco J. Mata and Ana Pont. Cham: Springer, vol. 481. [Google Scholar]

- UN.org. 2019. Special Edition: Progress towards the Sustainable Development Goals Report of the Secretary General, Economic and Social Council, Advance Unedited Version. Available online: https://sustainabledevelopment.un.org/content/documents/22700E_2019_XXXX_Report_of_the_SG_on_the_progress_towards_the_SDGs_Special_Edition.pdf (accessed on 24 September 2021).

- UN.org. 2020a. Policy Brief No. 78. Available online: https://www.un.org/development/desa/dpad/wp-content/uploads/sites/45/publication/PB_78.pdf (accessed on 6 June 2020).

- UN.org. 2020b. Policy Brief: The Impact of COVID-19 on Women, 9 April 2020. Available online: https://www.un.org/sites/un2.un.org/files/policy_brief_on_covid_impact_on_women_9_apr_2020_updated.pdf (accessed on 30 September 2020).

- UN.org. 2020c. UN Launches COVID-19 Plan That Could Defeat the Virus and Build a Better World. Available online: https://news.un.org/en/story/2020/03/1060702 (accessed on 8 May 2020).

- UNDESA. 2020. Available online: https://devpolicy.org/with-COVID-19-the-sdgs-are-even-more-important-20200616-2/ (accessed on 9 July 2020).

- Veeramani, C. 2020. COVID-19 Pandemic: Implications for India’s Exports and Global Value Chains. In COVID-19: Challenges for the Indian Economy—Trade and Foreign Policy Effects. Edited by AIC-EEPC. New Delhi: ASEAN-India Centre (AIC)—Engineering Export Promotion Council of India (EEPC). [Google Scholar]

- Venugopalan, Murale, Bettina Lynda Bastian, and P. K. Viswanathan. 2021. The Role of Multi-Actor Engagement for Women’s Empowerment and Entrepreneurship in Kerala, India. Administrative Sciences 11: 31. [Google Scholar] [CrossRef]

- World Economic Forum. 2020. How Big Business Is Joining the Fight against COVID-19. Available online: https://www.weforum.org/agenda/2020/03/big-business-joining-fight-against-coronavirus/ (accessed on 30 May 2020).

- Zambrano-Monserrate, Manuel A., María Alejandra Ruano, and Luis Sanchez-Alcalde. 2020. Indirect effects of COVID-19 on the environment. Science of the Total Environment 728: 138813. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

{kind=link}

| Red Major Challenges (Higher % Is Bad) | Orange Challenges Remain (Higher % Is Bad) | Yellow Significant Challenges (Higher % Is Bad) | Green Goal Achievement (Higher % Is Good) | |

|---|---|---|---|---|

| SDG 1 | 24 | 14 | 26 | 19 |

| SDG 2 | 60 | 33 | 1 | 0 |

| SDG 3 | 54 | 24 | 14 | 4 |

| SDG 4 | 26 | 27 | 37 | 5 |

| SDG 5 | 37 | 45 | 13 | 1 |

| SDG 6 | 41 | 34 | 20 | 1 |

| SDG 7 | 32 | 16 | 37 | 14 |

| SDG 8 | 31 | 39 | 19 | 1 |

| SDG 9 | 56 | 37 | 6 | 1 |

| SDG 10 | 44 | 21 | 14 | 4 |

| SDG 11 | 22 | 45 | 26 | 1 |

| SDG 12 | 22 | 25 | 34 | 15 |

| SDG 13 | 34 | 25 | 34 | 7 |

| SDG 14 | 26 | 39 | 11 | 0 |

| SDG 15 | 11 | 51 | 31 | 3 |

| SDG 16 | 56 | 22 | 11 | 2 |

| SDG 17 | 15 | 31 | 41 | 6 |

| Category | Brazil | Russian Federation | India | China | South Africa |

|---|---|---|---|---|---|

| Panel A: Achievement status of 17 SDGs | |||||

| Red—Major Challenges | 24% | 24% | 53% | 24% | 41% |

| Orange—Significant Challenges | 59% | 41% | 24% | 59% | 47% |

| Yellow—Challenges Remain | 12% | 29% | 24% | 6% | 6% |

| Green—Goal Achievement | 6% | 6% | 0% | 12% | 6% |

| Panel B: Achievement status of focus SDGs | |||||

| Red—Major Challenges | SDG 3 | SDG 3 | SDG 3, 5, 6 | SDG 3 | |

| Orange—Significant Challenges | SDG 4, 5, 6 | SDG 5 | SDG4 | SDG 3, 5, 6 | SDG 4, 6 |

| Yellow—Challenges Remain | SDG 4, 6 | ||||

| Green—Goal Achievement | SDG4 | ||||

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Nair, R.; Viswanathan, P.K.; Bastian, B.L. Reprioritising Sustainable Development Goals in the Post-COVID-19 Global Context: Will a Mandatory Corporate Social Responsibility Regime Help? Adm. Sci. 2021, 11, 150. https://doi.org/10.3390/admsci11040150

Nair R, Viswanathan PK, Bastian BL. Reprioritising Sustainable Development Goals in the Post-COVID-19 Global Context: Will a Mandatory Corporate Social Responsibility Regime Help? Administrative Sciences. 2021; 11(4):150. https://doi.org/10.3390/admsci11040150

Chicago/Turabian StyleNair, Rajiv, P.K Viswanathan, and Bettina Lynda Bastian. 2021. "Reprioritising Sustainable Development Goals in the Post-COVID-19 Global Context: Will a Mandatory Corporate Social Responsibility Regime Help?" Administrative Sciences 11, no. 4: 150. https://doi.org/10.3390/admsci11040150