Introducing the World’s First Global Producer Price Indices for Beef Cattle and Sheep

Abstract

:Simple Summary

Abstract

1. Introduction

2. Materials and Methods

2.1. The Global PPIs Identified in the Study

2.2. Countries Involved in the PPIs and Data Sources

2.3. Price Index Formula

- : the price of the ith product in year t

- : the price of the ith product in the base year.

- : the production value share of the ith product in the total production value of all products in the basket in the base period, that is: /.

- : the production quantity of the ith product in the base year.

- : the production price in the ith country in year t.

- : the production price in the ith country as an average price over the three-year base period 2014–2016.

- : the share of the production volume of the ith country in the total production volume of all countries in the base period, that is: /.

- : the production quantity in the ith country as an average over the three-year base period 2014–2016.

3. Results and Discussion

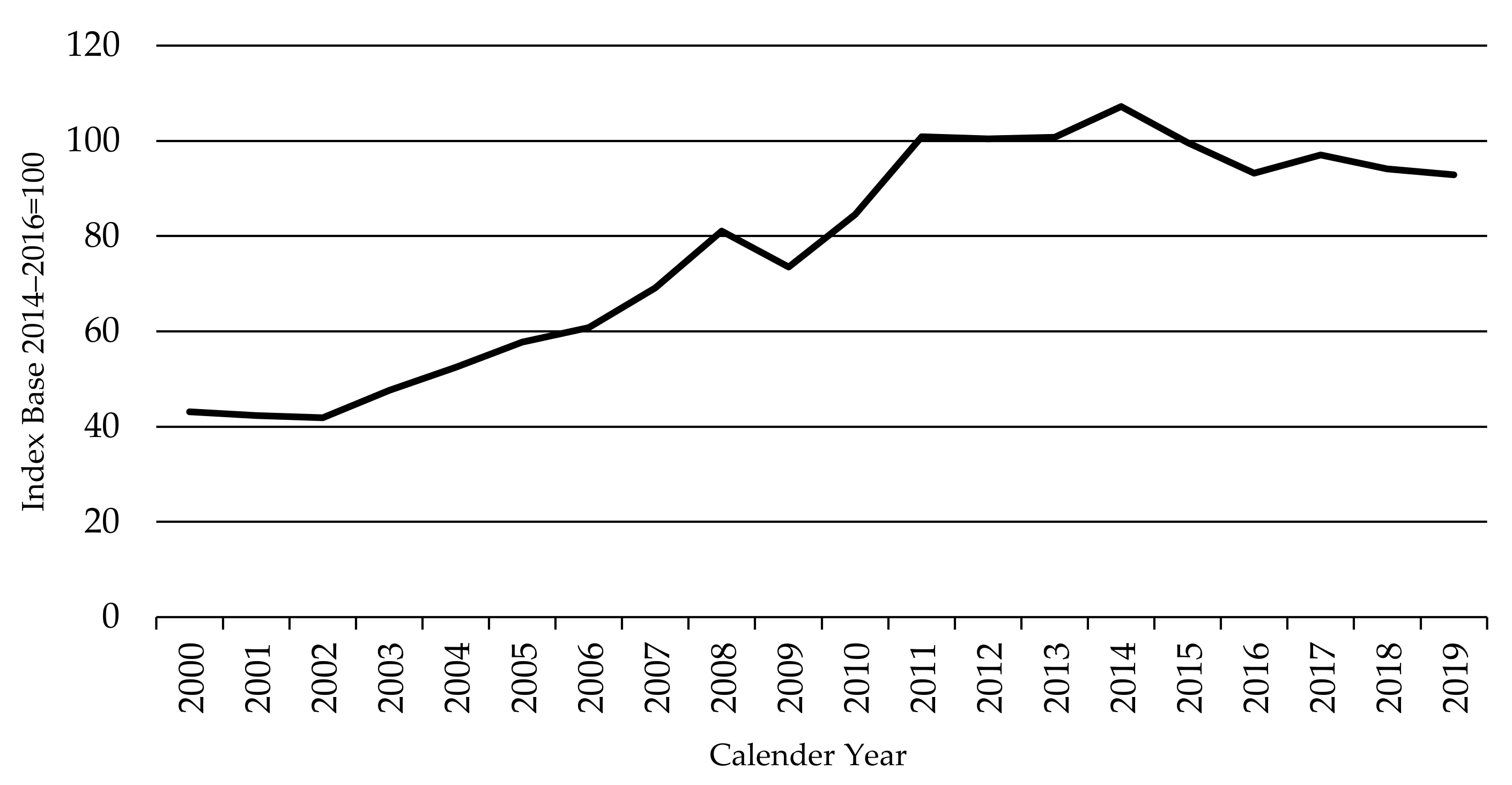

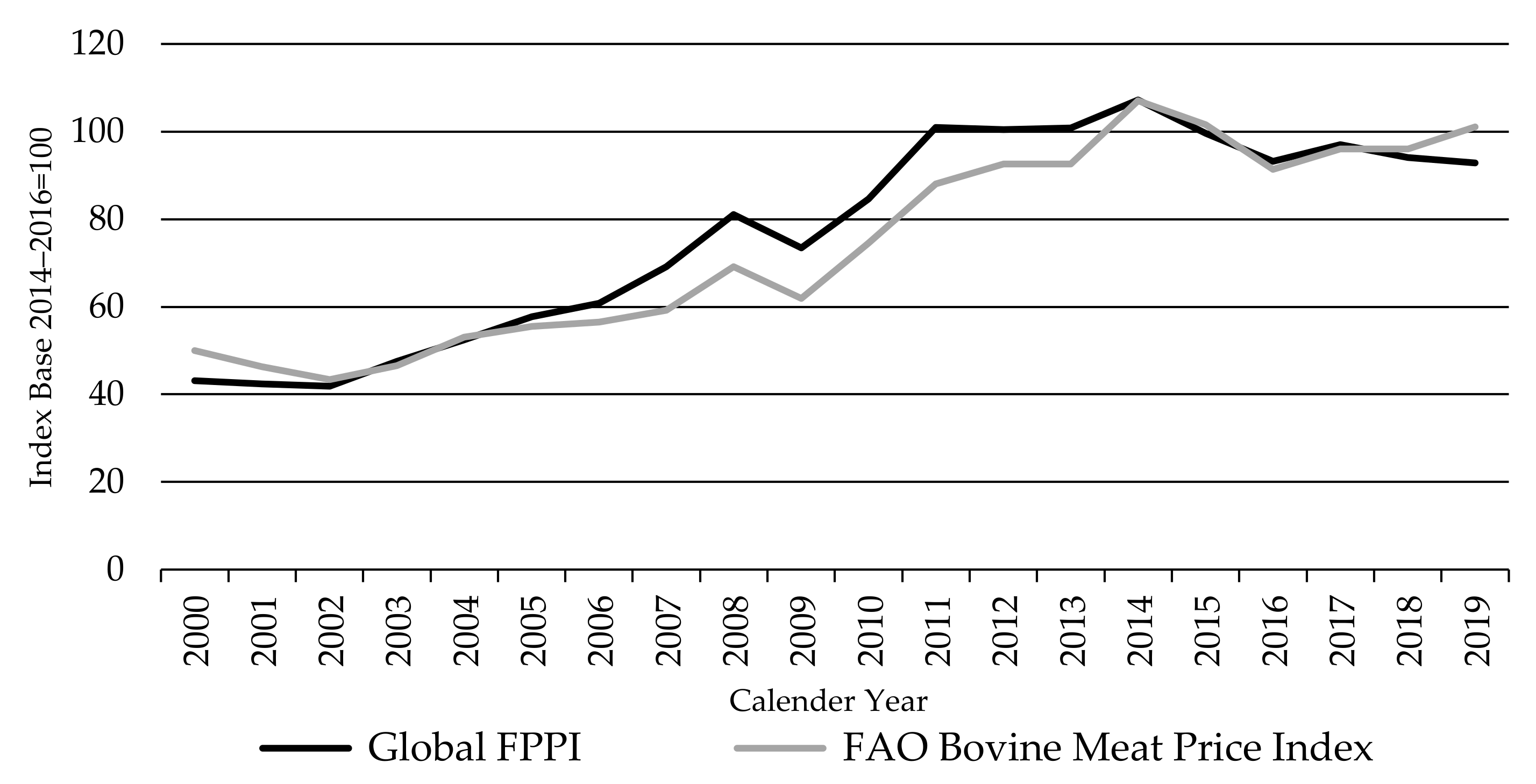

3.1. The Global Finished Cattle Producer Price Index FPPI

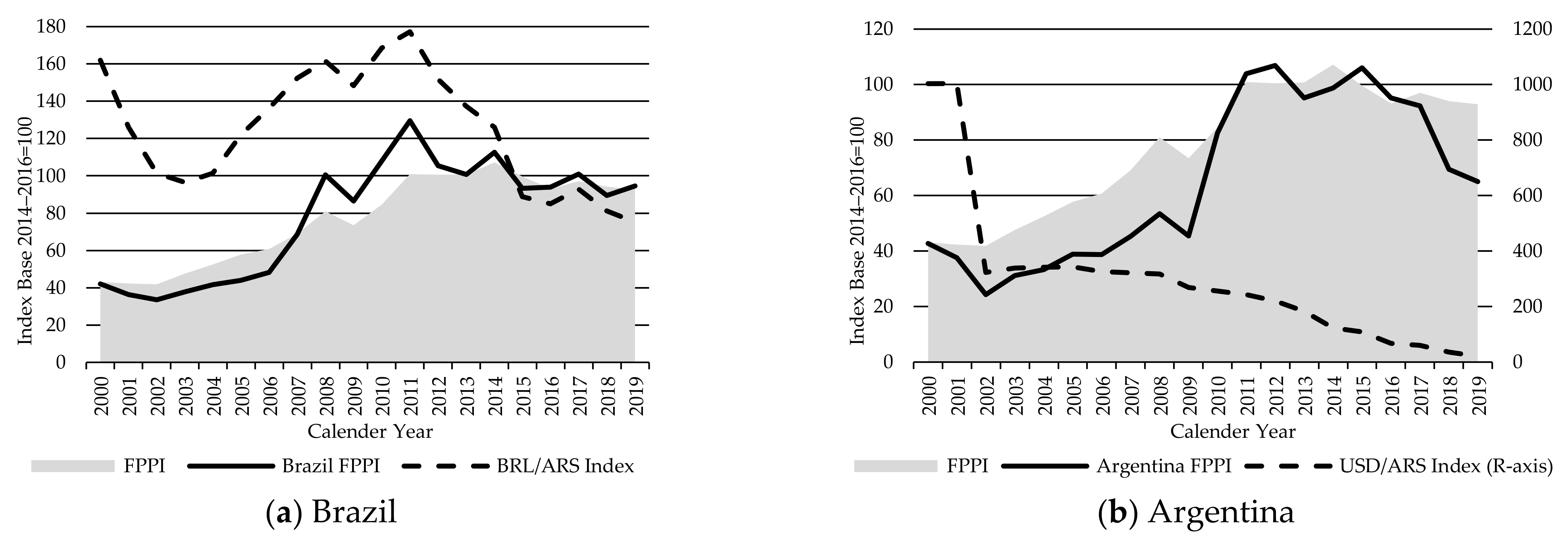

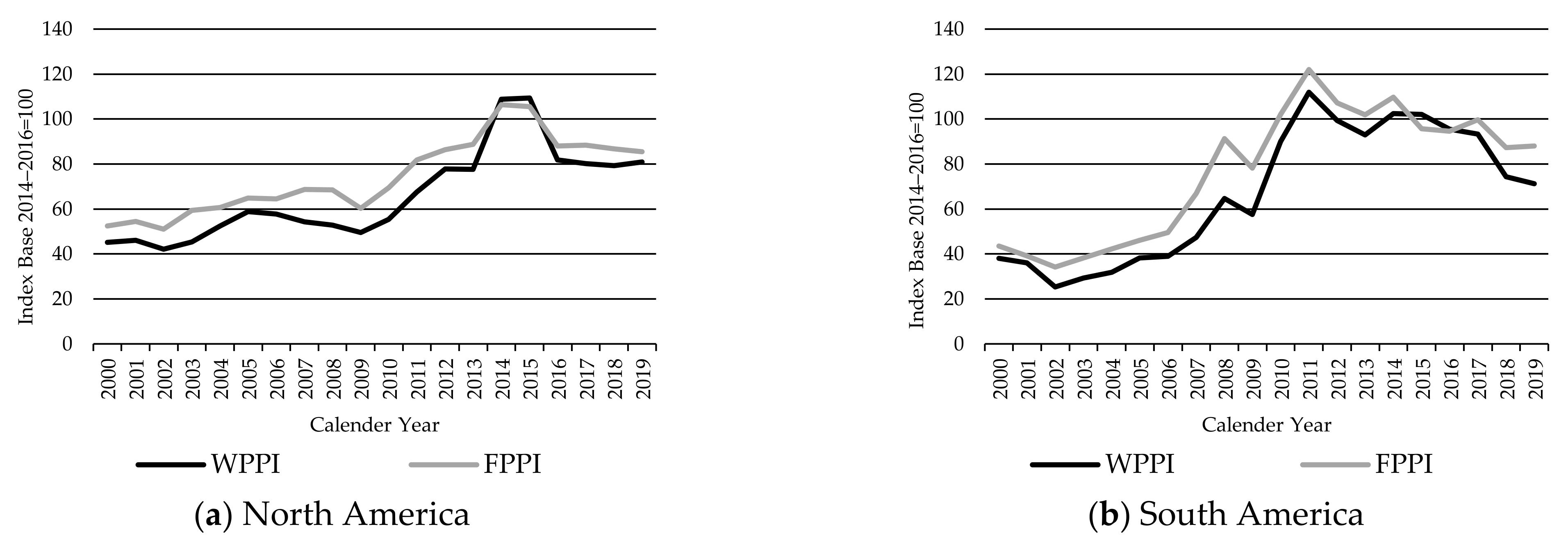

3.1.1. The North America FPPI

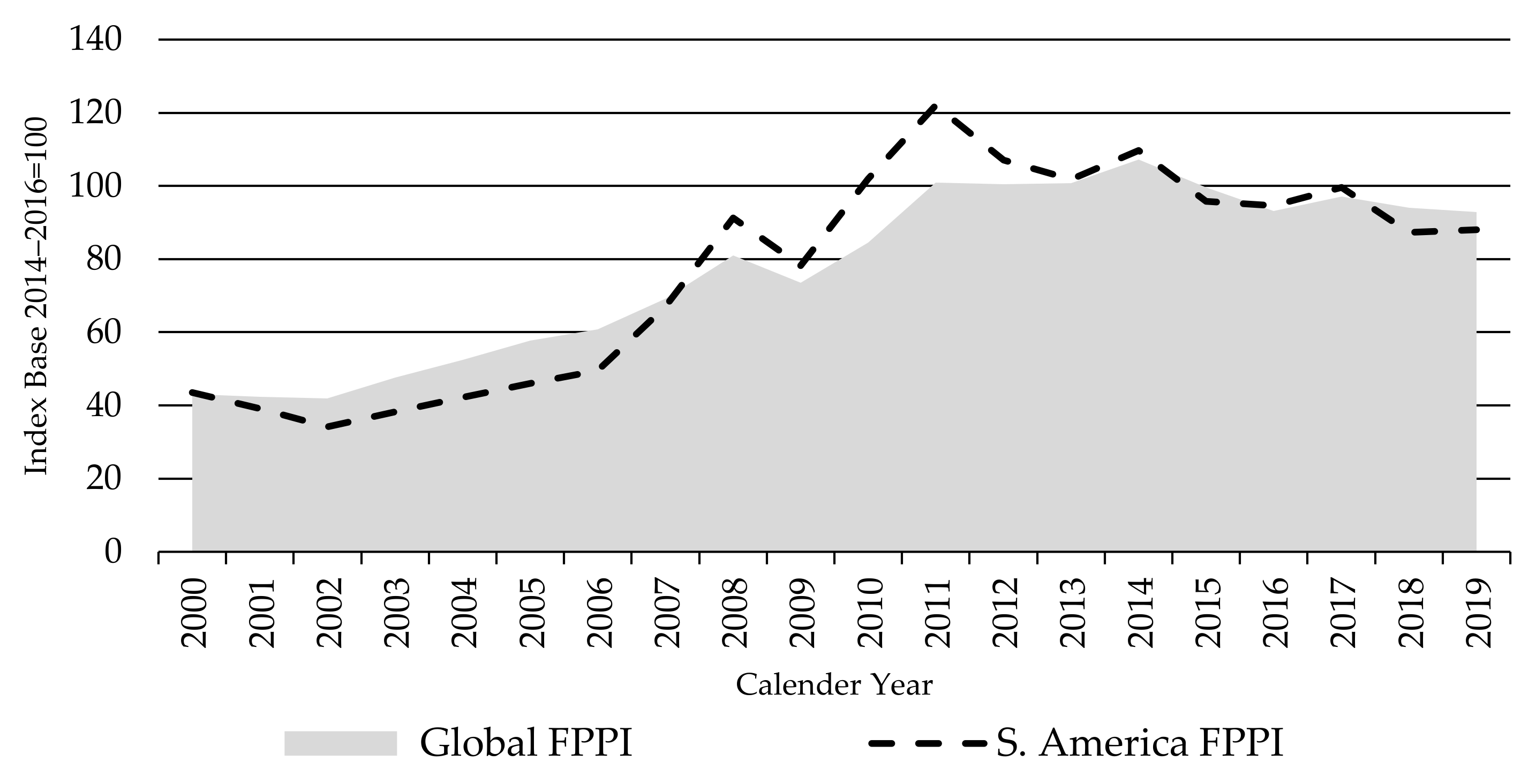

3.1.2. The South America FPPI

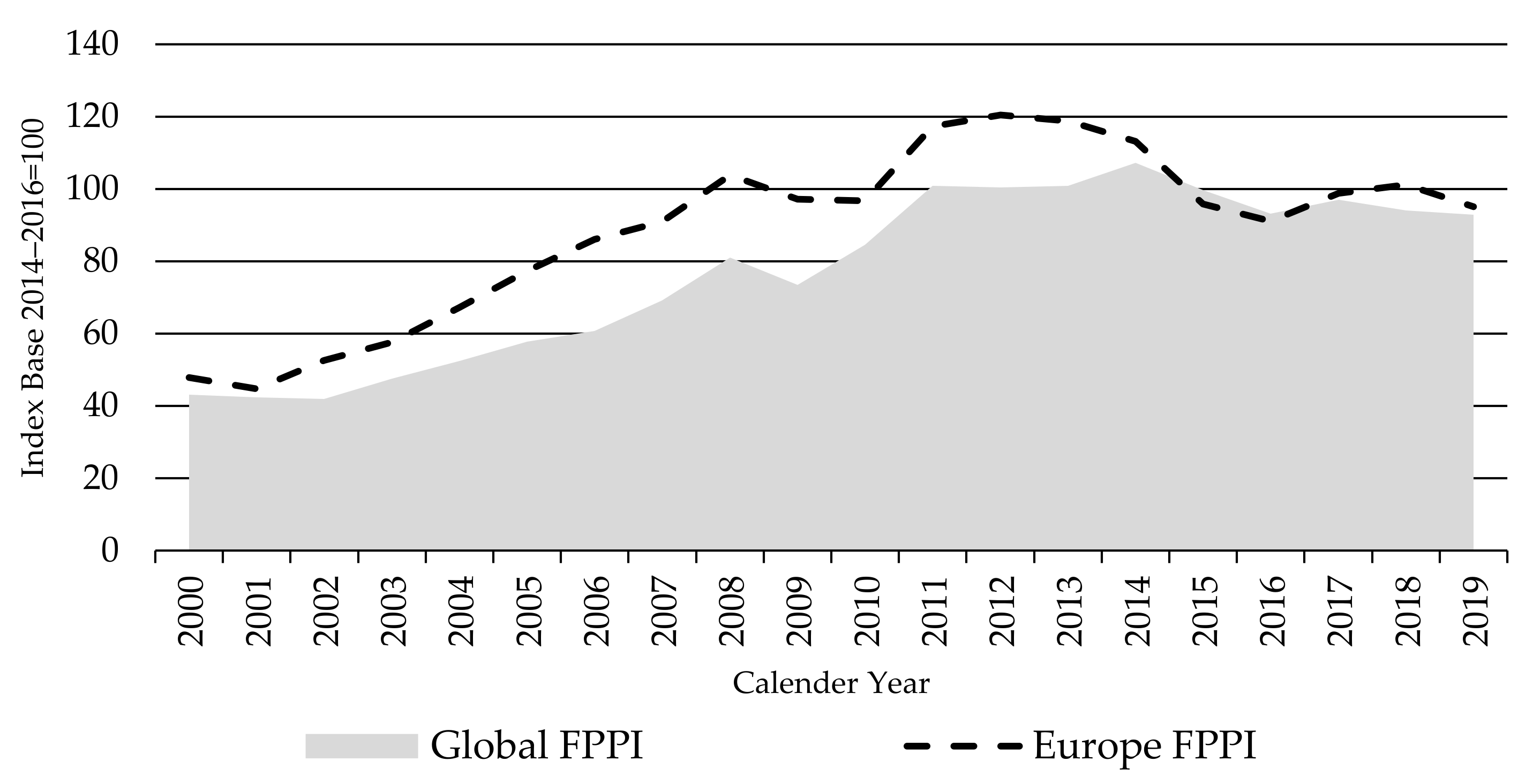

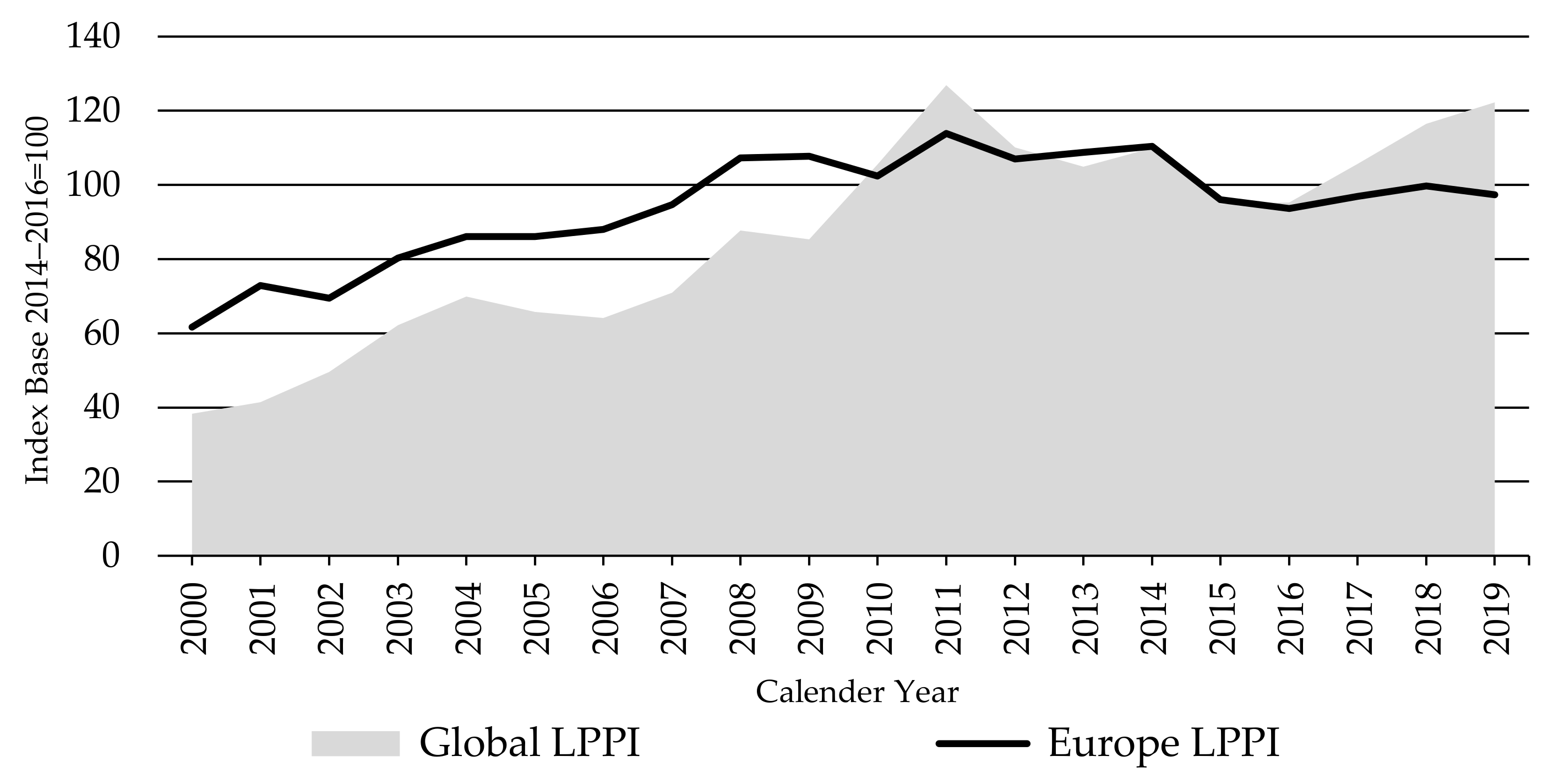

3.1.3. The Europe FPPI

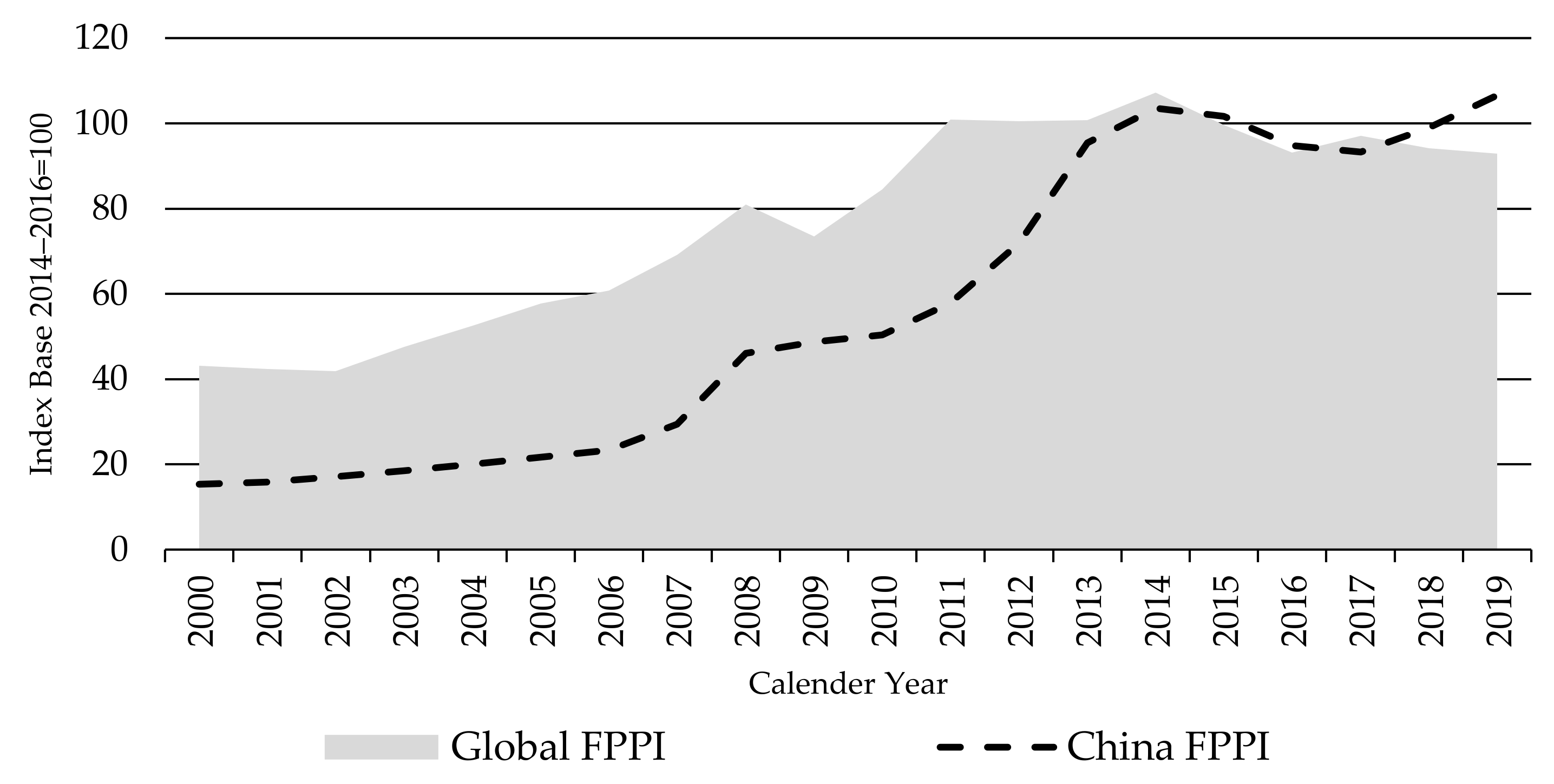

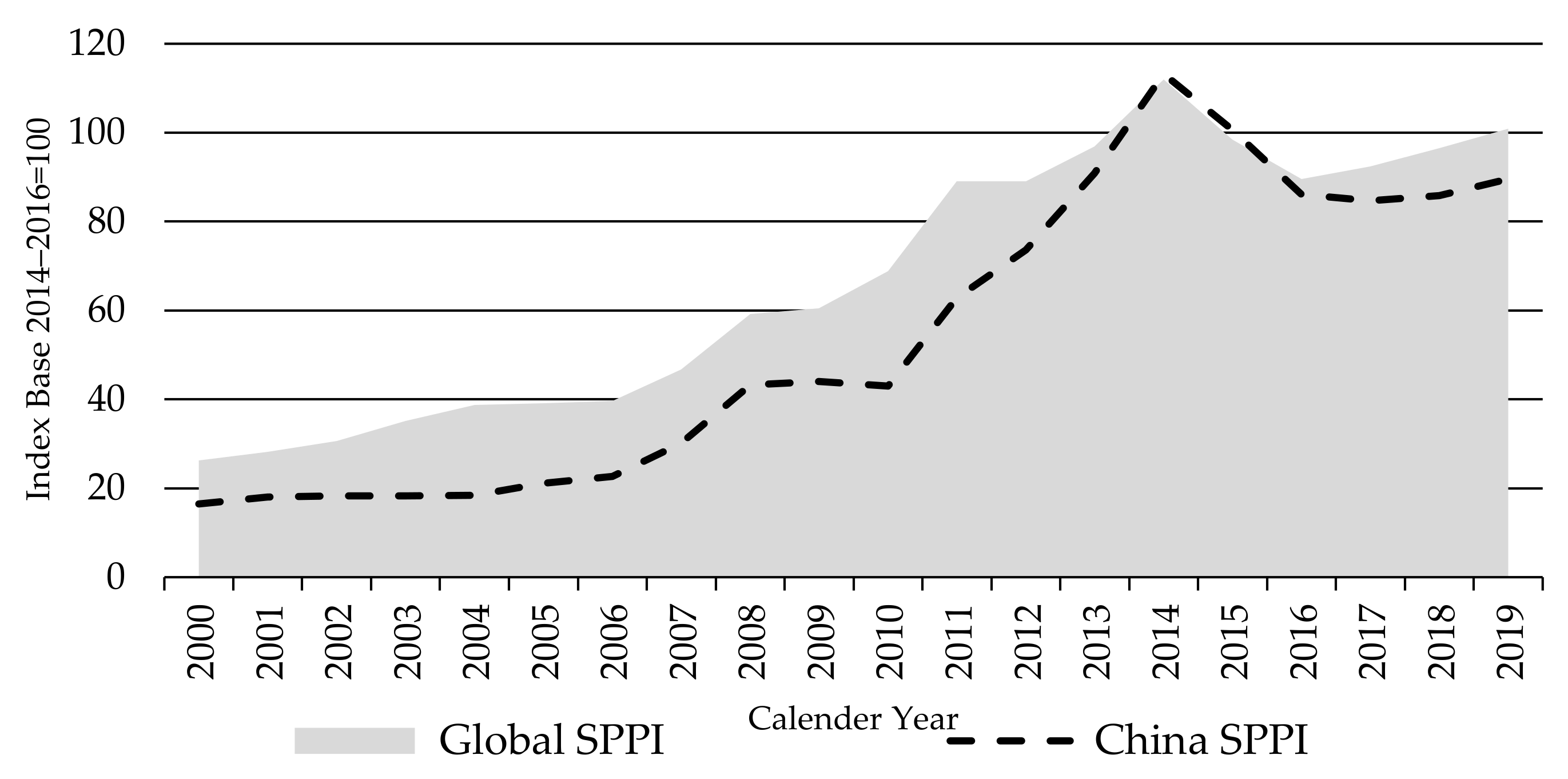

3.1.4. The China FPPI

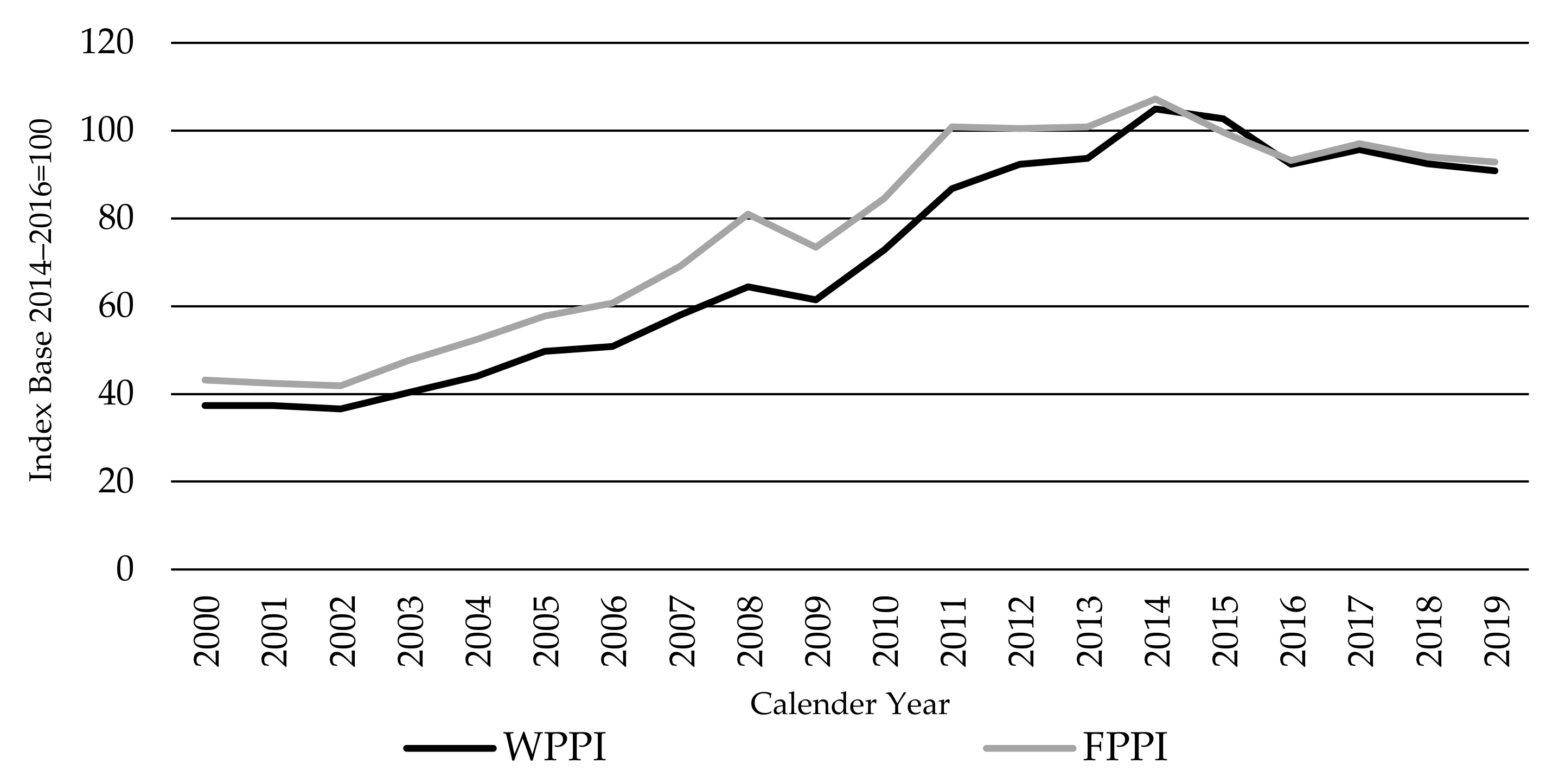

3.2. The Global Weaner Cattle Producer Price Index WPPI

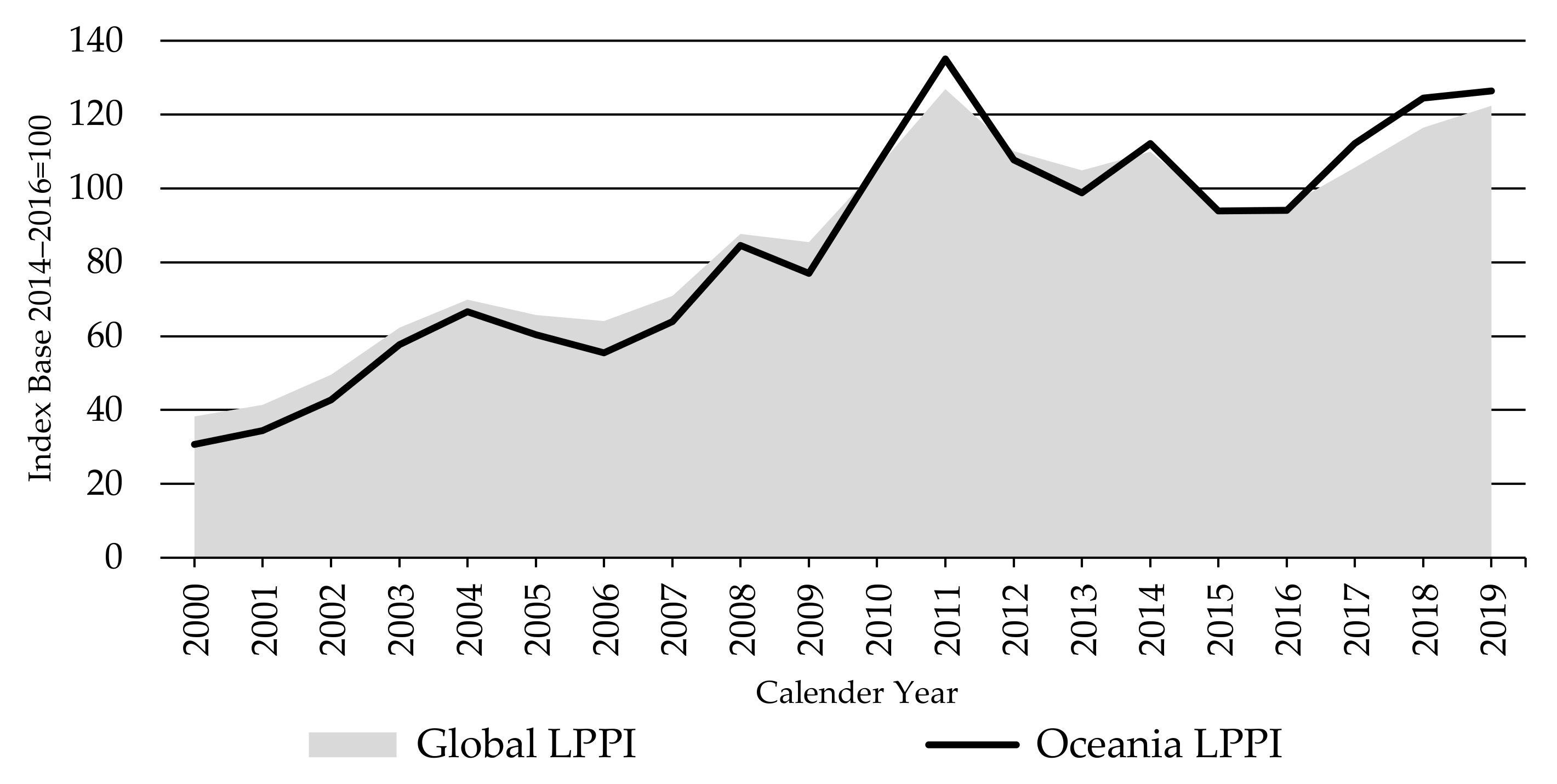

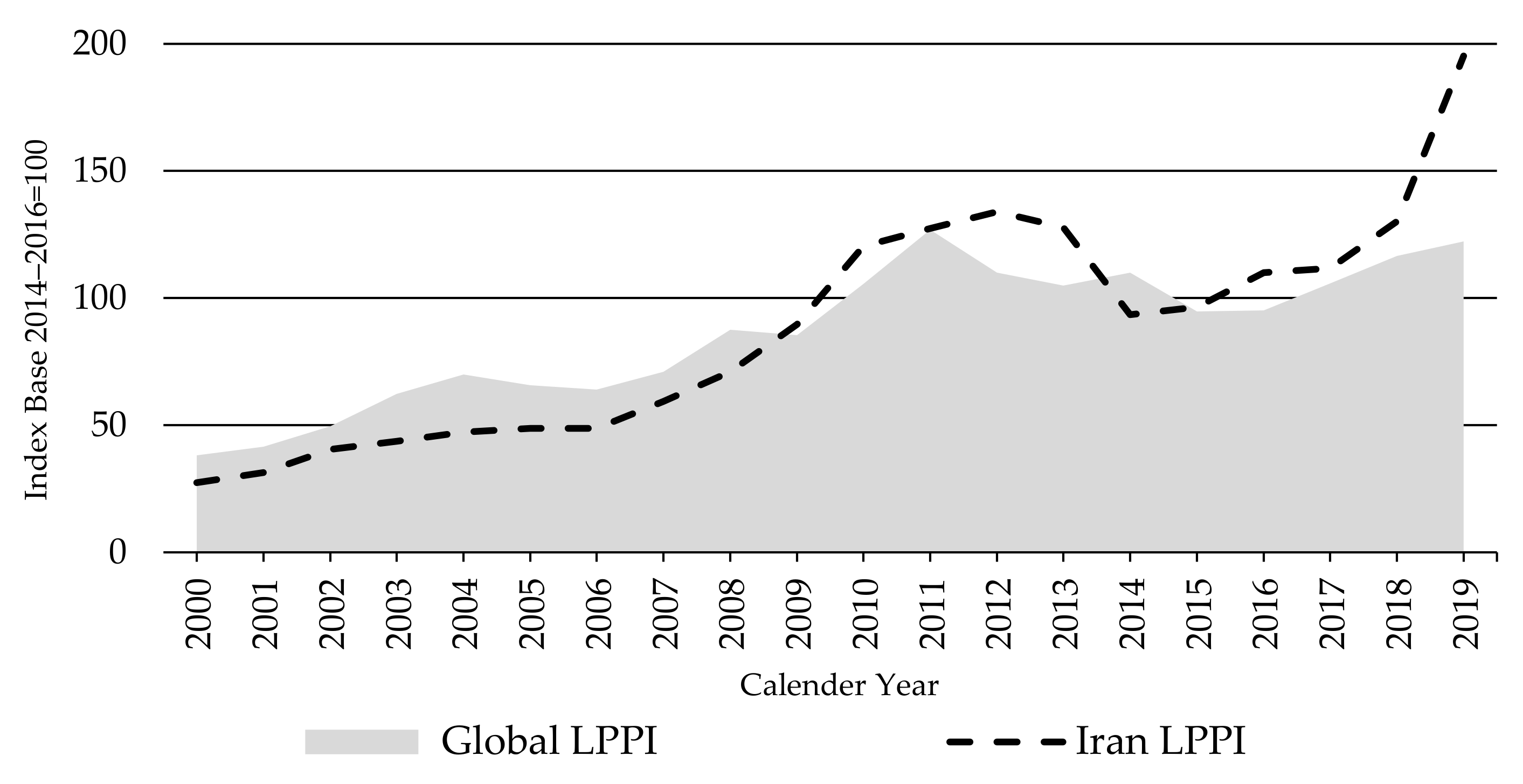

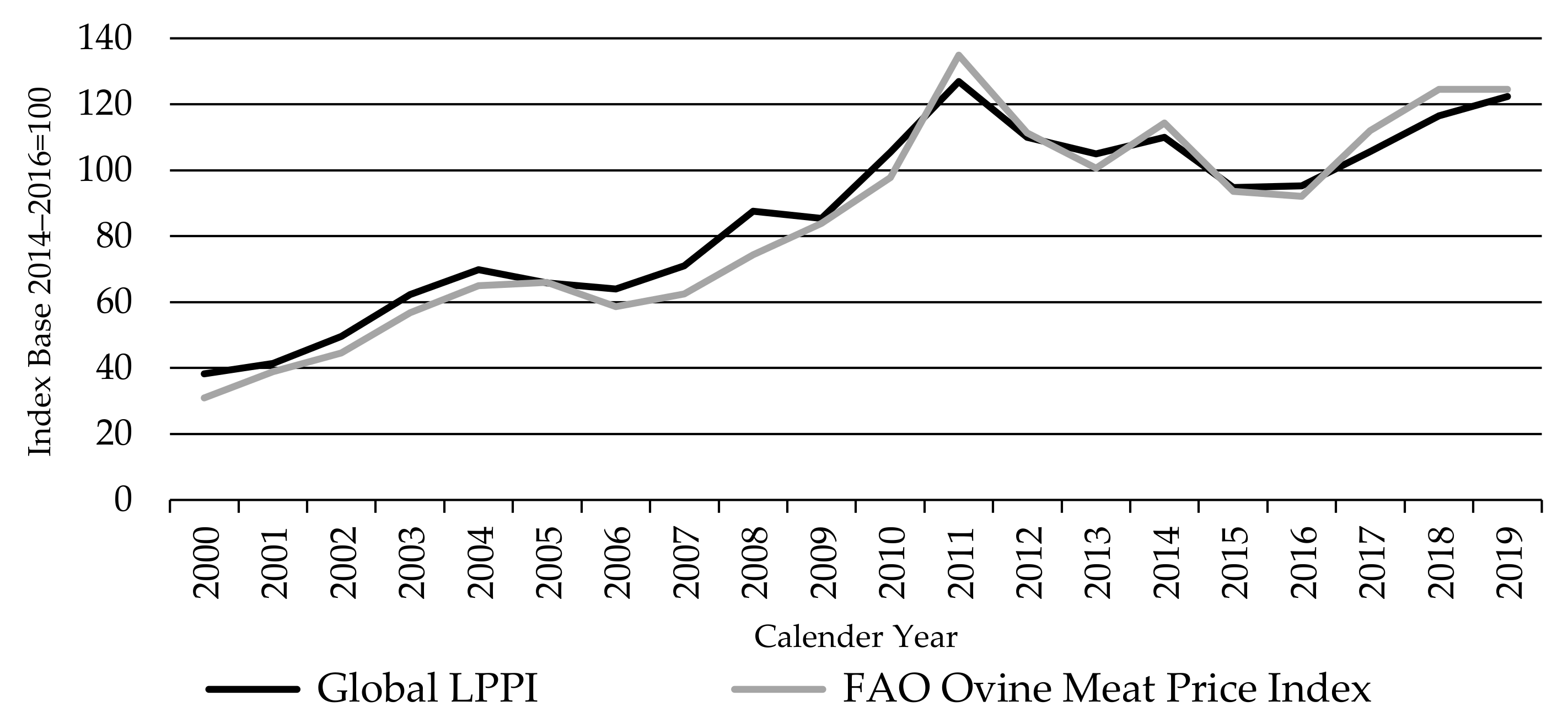

3.3. The Global Lambs Producer Price Index LPPI

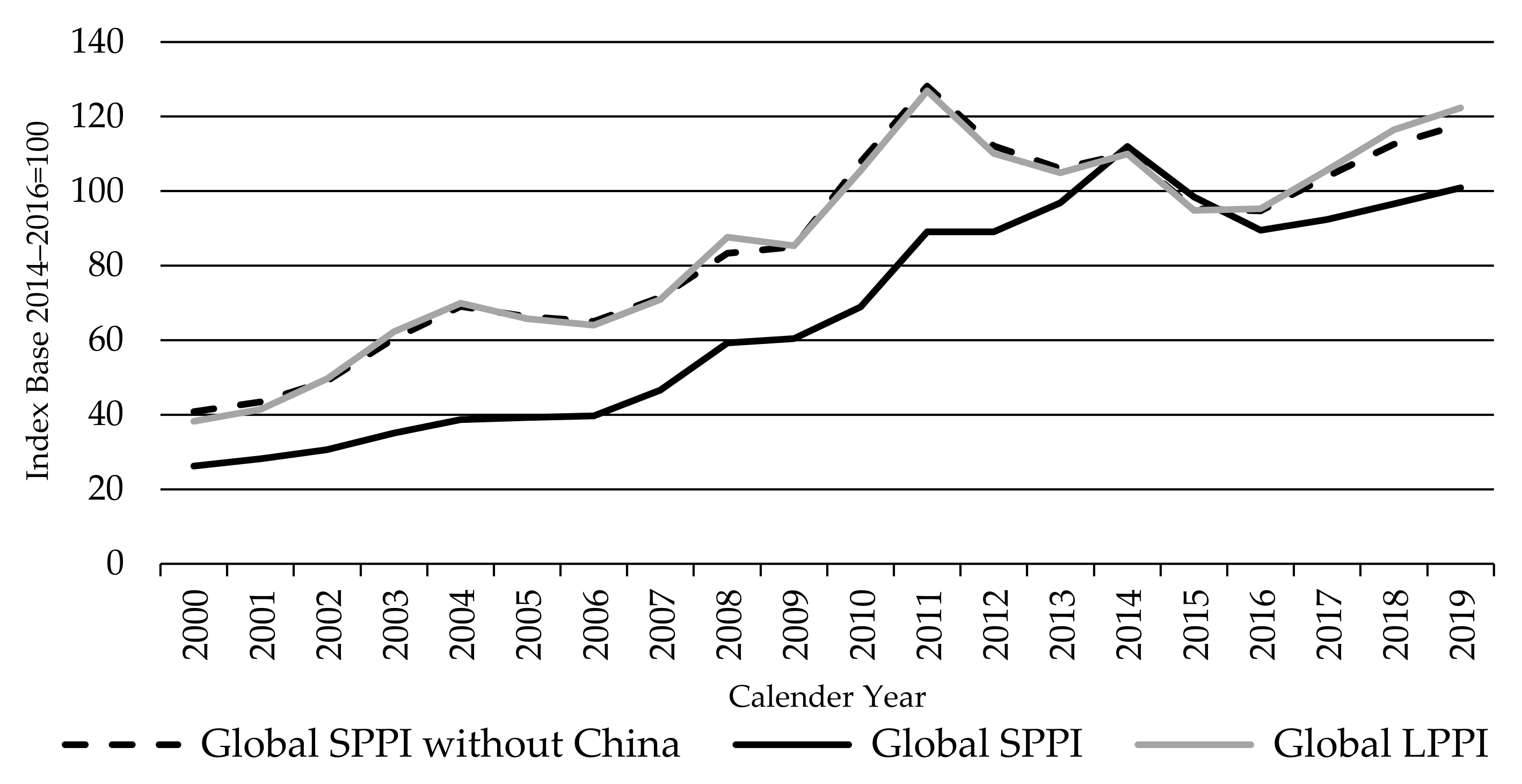

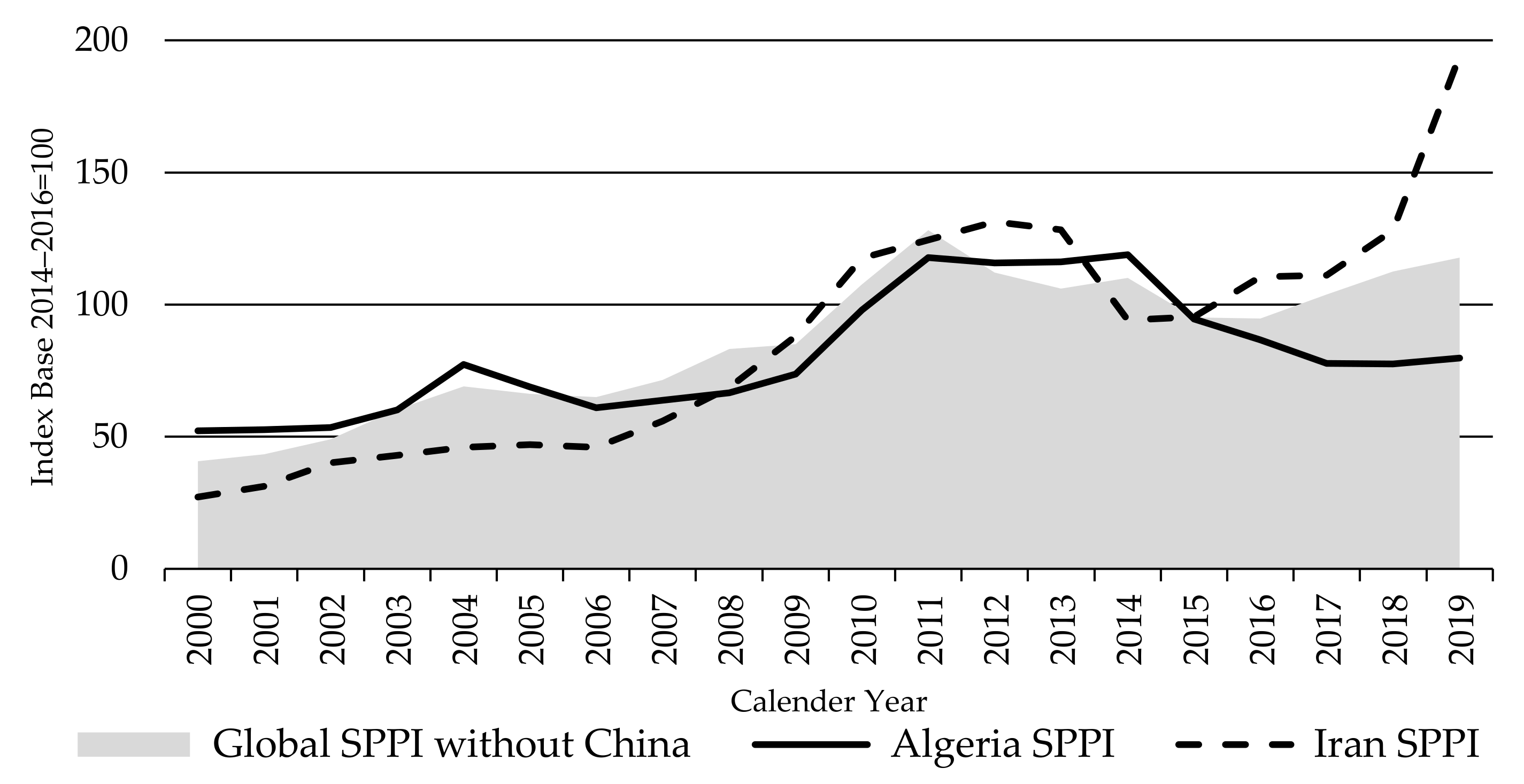

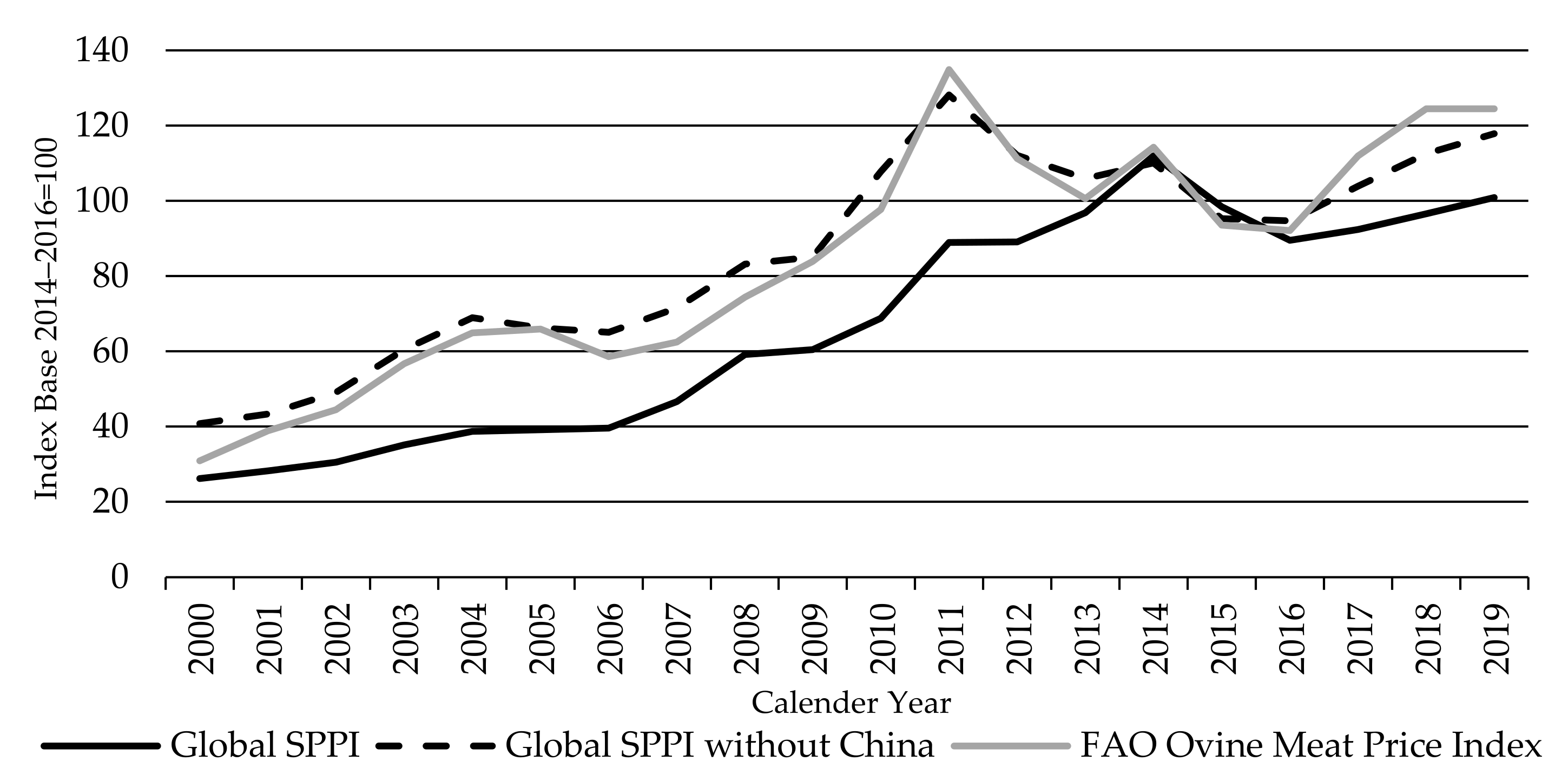

3.4. The Global Sheep Meat Producer Price Index SPPI

3.5. Relativity of the Global PPIs to the FAO Export Meat Price Indices

4. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Country | FPPI | WPPI | LPPI | SPPI |

|---|---|---|---|---|

| Algeria | ✓ | |||

| Argentina | ✓ | ✓ | ||

| Australia | ✓ | ✓ | ✓ | ✓ |

| Austria | ✓ | ✓ | ||

| Brazil | ✓ | ✓ | ✓ | |

| Canada | ✓ | ✓ | ||

| China | ✓ | ✓ | ✓ | |

| Colombia | ✓ | ✓ | ||

| Czechia | ✓ | |||

| Finland | ✓ | |||

| France | ✓ | ✓ | ✓ | ✓ |

| Germany | ✓ | ✓ | ✓ | ✓ |

| Indonesia | ✓ | |||

| Iran | ✓ | ✓ | ✓ | |

| Ireland | ✓ | ✓ | ✓ | ✓ |

| Italy | ✓ | ✓ | ||

| Jordan | ✓ | |||

| Kazakhstan | ✓ | |||

| Mexico | ✓ | ✓ | ✓ | |

| Morocco | ✓ | ✓ | ||

| Namibia | ✓ | ✓ | ✓ | |

| New Zealand | ✓ | ✓ | ✓ | |

| Paraguay | ✓ | |||

| Peru | ✓ | |||

| Poland | ✓ | ✓ | ||

| Portugal | ✓ | ✓ | ✓ | ✓ |

| Russia | ✓ | |||

| South Africa | ✓ | ✓ | ✓ | |

| Spain | ✓ | ✓ | ✓ | ✓ |

| Tunisia | ✓ | ✓ | ✓ | |

| UK | ✓ | ✓ | ✓ | ✓ |

| Ukraine | ✓ | ✓ | ||

| Uruguay | ✓ | ✓ | ✓ | |

| US | ✓ | ✓ | ||

| Switzerland | ✓ | ✓ |

| Country | Finished Cattle | Lambs | Sheep Meat |

|---|---|---|---|

| Algeria | Lambs and mutton sheep | ||

| Argentina | Steers (British) | ||

| Australia | Trade steer 330–400 kg cwt | Eastern States trade lambs 18–22 kg cwt | Lambs and mutton sheep Mutton sheep 18–24 kg cwt |

| Austria | Bulls R3 | ||

| Brazil | Slaughter steers | Northeast and south ewe | |

| Canada | Slaughter steers | ||

| China | Beef | Lambs and mutton sheep | |

| Colombia | Steers 1st class | ||

| Czechia | Bulls SEU | ||

| Finland | Bulls O2 | ||

| France | Bulls R3 | Lambs | Lambs and mutton sheep |

| Germany | Bulls R3 | Lambs | Lambs and mutton sheep |

| Indonesia | Beef | ||

| Iran | Beef | Lambs | Lambs and mutton sheep |

| Ireland | Steers R3 | Heavy lambs | Mart sheep 50–59 kg LW |

| Italy | Male R2 < 24 months | ||

| Jordan | Lambs and mutton sheep | ||

| Kazakhstan | Beef | ||

| Mexico | Beef | Lambs and mutton sheep | |

| Morocco | Beef A-Grade | Lambs and mutton sheep | |

| Namibia | Steers R3 | Lambs | Lambs and mutton sheep |

| New Zealand | Steers & heifers | Lambs and mutton sheep | |

| Paraguay | Steers | ||

| Peru | Steers | Lambs | |

| Poland | Bulls | ||

| Portugal | Cattle 12–18 months | Lambs ˂ 28 Kg LW | Lambs and mutton sheep |

| Russia | Bulls | ||

| South Africa | Steers A-Grade | Lambs and mutton sheep | |

| Spain | Male yearling AR3 | Lambs 10–13 kg CW | Mutton sheep 12–16 kg CW |

| Switzerland | Bulls (MT) T3 | ||

| Tunisia | Bulls dairy cross, 15 months | Lambs and mutton sheep | |

| UK | Steers all categories | Lambs | Lambs and mutton sheep |

| Ukraine | Beef | Lambs and mutton sheep | |

| Uruguay | Steers | Lambs and mutton sheep | |

| US | Steers all grades |

References

- FAO. FAOSTAT Statistical Database; FAO: Rome, Italy, 2020. [Google Scholar]

- FAO. The Future of Food and Agriculture—Trends and Challenges; FAO: Rome, Italy, 2017; ISBN 978-92-5-109551-5. [Google Scholar]

- OECD/FAO. OECD-FAO Agricultural Outlook 2020–2029; FAO: Rome, Italy; OECD Publishing: Paris, France, 2020. [Google Scholar] [CrossRef]

- Smith, S.B.; Gotoh, T.; Greenwood, P.L. Current situation and future prospects for global beef production: Overview of special issue. Asian-Australas. J. Anim. Sci. 2018, 31, 927. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Gerber, P.J.; Mottet, A.; Opio, C.I.; Falcucci, A.; Teillard, F. Environmental impacts of beef production: Review of challenges and perspectives for durability. Meat Sci. 2015, 109, 2–12. [Google Scholar] [CrossRef] [PubMed]

- Dyck, J.H.; Nelson, K.E. Structure of the Global Markets for Meat; U.S. Department of Agriculture, Economic Research Service: Washington, DC, USA, 2003; Agriculture Information Bulletin No. 785. Available online: https://www.ers.usda.gov/webdocs/publications/42513/30787_aib785_002.pdf?v=0 (accessed on 7 January 2021).

- Ritchie, H.; Roser, M. Environmental Impacts of Food Production; Our world in data; The Global Change Data Lab: 2020. Available online: https://ourworldindata.org/environmental-impacts-of-food (accessed on 9 January 2021).

- Díaz-Bonilla, E. Volatile volatility: Conceptual and measurement issues related to price trends and volatility. In Food Price Volatility and Its Implications for Food Security and Policy; Kalkuhl, M., von Braun, J., Torero, M., Eds.; Springer: Cham, Switzerland, 2016. [Google Scholar] [CrossRef] [Green Version]

- FAO. FAO Food Price Index; World Food Situation; FAO: Rome, Italy, 2021; Available online: http://www.fao.org/worldfoodsituation/foodpricesindex/en/ (accessed on 10 February 2021).

- Larson, D.F. Food prices and food price volatility. In Commodities: Markets, Performance, and Strategies; Baker, H.K., Filbeck, G., Harris, J.H., Eds.; Oxford University Press: New York, NY, USA, 2018. [Google Scholar] [CrossRef]

- Diewert, W.E. Index numbers. In The New Palgrave Dictionary of Economics, 2nd ed.; Durlauf, S., Blume, L.E., Eds.; Palgrave Macmillan, a Division of Macmillan Publishers Limited: London, UK, 2008; ISBN 978-0-230-22638-8. [Google Scholar]

- Hamid, S.A.; Dhakar, T.S.; Thirunavukkarasu, A. The Behavior of US Producer Price Index: 1913 to 2004; Southern New Hampshire University; Working Paper No. 2006-04; 2006; Available online: https://academicarchive.snhu.edu/bitstream/handle/10474/1665/cfs2006-04.pdf?sequence=1&isAllowed=y (accessed on 16 January 2021).

- IMF. Producer Price Index Manual: Theory and Practice; International Monetary Fund: Washington, DC, USA, 2004; ISBN 9781589063044. [Google Scholar]

- Yamarone, R. The Trader’s Guide to Key Economic Indicators; John Wiley & Sons, Inc.: Hoboken, NJ, USA, 2012; Volume 151. [Google Scholar]

- Cachia, F. Regional Food Price Inflation Transmission; FAO Statistics Division: Rome, Italy, 2014; Working Paper Series: ESS/14-01; Available online: http://www.fao.org/3/a-i3718e.pdf (accessed on 25 January 2021).

- FAO. Food Price Index Revisited; Food Outlook, Special Features; FAO: Rome, Italy, 2013; Available online: http://www.fao.org/fileadmin/templates/worldfood/Reports_and_docs/Special_feature_FFPI_en.pdf (accessed on 2 December 2020).

- FAO. Revisions to the FAO Food Price Indices; Food Outlook, Special Features; FAO: Rome, Italy, 2020; Available online: http://www.fao.org/3/ca9509en/index.pdf (accessed on 2 December 2020).

- FAO. Meat Prices Table; FAO: Rome, Italy, 2020; Available online: http://www.fao.org/fileadmin/templates/est/COMM_MARKETS_MONITORING/Meat/Documents/Meat_Prices_table.pdf (accessed on 2 December 2020).

- INSEE. Agricultural Produced Price Index IPPAP.; Institut National de la Statistique et des Études Économiques: Paris, France, 2021; Available online: https://www.insee.fr/en/metadonnees/source/indicateur/p1657/description (accessed on 10 January 2021).

- Chibanda, C.; Agethen, K.; Deblitz, C.; Zimmer, Y.; Almadani, M.I.; Garming, H.; Rohlmann, C.; Schütte, J.; Thobe, P.; Verhaagh, M.; et al. The typical farm approach and its application by the Agri Benchmark network. Agriculture 2020, 10, 646. [Google Scholar] [CrossRef]

- Agri Benchmark Beef and Sheep Network Data Based; Thünen Institute of Farm Economics: Braunschweig, Germany, 2020; Available online: http://www.agribenchmark.org/beef-and-sheep.html (accessed on 12 November 2020).

- SNA. System of National Accounts. 1993. Available online: https://unstats.un.org/unsd/nationalaccount/docs/1993sna.pdf (accessed on 12 November 2020).

- Laspeyres, E. Die Berechnung Einer Mittleren Waarenpreissteigerung. Jahrbücher Für Natl. Stat. 1871, 16, 296–318. [Google Scholar] [CrossRef]

- ILO/IMF/OECD/UNECE/Eurostat/The World Bank. Consumer Price Index Manual: Theory and Practice; International Labour Office: Geneva, Switzerland, 2004; ISBN 92-2-113699-X. [Google Scholar]

- Khan, K.; Su, C.W.; Tao, R.; Chu, C.C. Is there any relationship between producer price index and consumer price index in the Czech Republic? Econ. Res. Ekon. Istraživanja 2018, 31, 1788–1806. [Google Scholar] [CrossRef]

- OECD. Producer Price Indices—Comparative Methodological Analysis; Methodological Publications: Paris, France, 2011; Available online: http://www.oecd.org/std/prices-ppp/48370389.pdf (accessed on 5 January 2021).

- Tveterås, S.; Asche, F.; Bellemare, M.F.; Smith, M.D.; Guttormsen, A.G.; Lem, A.; Lien, K.; Vannuccini, S. Fish is food-the FAO’s fish price index. PLoS ONE 2012, 7, e36731. [Google Scholar] [CrossRef] [PubMed]

- USDA. Sector at a Glance; U.S. Department of Agriculture, Economic Research Service, Cattle & Beef, Topics: Washington, DC, USA, 2021. Available online: https://www.ers.usda.gov/topics/animal-products/cattle-beef/sector-at-a-glance/ (accessed on 8 February 2021).

- Brooks, K.; Nogueira, L.; Birch, J.U.S. Beef Trade Disruptions; Agricultural Economics Department; University of Nebraska—Lincoln: 2014; Cornhusker Economics 701; Available online: https://digitalcommons.unl.edu/cgi/viewcontent.cgi?article=1701&context=agecon_cornhusker (accessed on 20 December 2020).

- Matsuo, Y. Japan Scraps Mad Cow Import Restrictions on US Beef; Nikkei Asia; Economy; Nikkei Inc.: Tokyo, Japan, 2019; Available online: https://asia.nikkei.com/Economy/Japan-scraps-mad-cow-import-restrictions-on-US-beef (accessed on 2 February 2021).

- Drouillard, J.S. Current situation and future trends for beef production in the United States of America—A review. Asian-Australas. J. Anim. Sci. 2018, 31, 1007. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- USDA. Overview of the U. S. Cattle Industry; USA, Economics, Statistics and Market Information Syatem: Washington, DC, USA, 2017; Special Report. Available online: https://usda.library.cornell.edu/concern/publications/8s45q879d (accessed on 8 January 2021).

- Mathews, K.; Haley, M. Livestock, Dairy, and Poultry Outlook; Situation and Outlook; U.S. Department of Agriculture, Economic Research Service: Washington, DC, USA, 2015; LDP-M-256. Available online: https://www.ers.usda.gov/webdocs/outlooks/37633/54210_ldpm-256.pdf?v=277 (accessed on 8 January 2021).

- Spilimbergo, M.A.; Srinivasan, M.K. Brazil: Boom, Bust, and the Road to Recovery; International Monetary Fund: Washington, DC USA, 2019; ISBN 9781484339749. [Google Scholar] [CrossRef]

- Dwyer, B. Latin America: An End to Boom and Bust? EUROMONEY Article; Euromoney Institutional Investor PLC: London, UK, 2019; Available online: https://www.euromoney.com/article/b1dd4cf9mv160j/latin-america-an-end-to-boom-and-bust (accessed on 13 January 2021).

- OANDA Corporation. Historical Exchange Rates; OANDA Corporation: New York, NY, USA, 2020; Available online: https://www.oanda.com/fx-for-business/historical-rates (accessed on 15 May 2020).

- Díaz-Bonilla, E. Macroeconomics, Agriculture, and Food Security—A Guide to Policy Analysis in Developing Countries; A Peer-Reviewed Publication; International Food Policy Research Institute: Washington, DC, USA, 2015. [Google Scholar] [CrossRef]

- Hyde, M.; Thorpe, S.; Waring, A.; Moir, B.; Gunning-Trant, C. South America: An Emerging Competitor for Australia’s Beef Industry; Australian Bureau of Agricultural and Resource Economics and Sciences ABARES: Canberra, Australia, 2016; Research Report 16.14. Available online: https://www.agriculture.gov.au/abares/research-topics/trade/south-america-beef#read-the-report (accessed on 7 April 2021).

- CEPAL, N. The Outlook for Agriculture and Rural Development in the Americas: A Perspective on Latin America and the Caribbean 2017–2018; ECLAC, FAO, IICA: San Jose, Costa Rica, 2017; ISBN 978-92-9248-735-5. Available online: http://www.fao.org/3/i8048en/I8048EN.pdf (accessed on 12 November 2020).

- Romanzini, E.P.; Barbero, R.P.; Reis, R.A.; Hadley, D.; Malheiros, E.B. Economic evaluation from beef cattle production industry with intensification in Brazil’s tropical pastures. Trop. Anim. Health Prod. 2020, 52, 2659–2666. [Google Scholar] [CrossRef] [PubMed]

- Barbero, R.P.; Malheiros, E.B.; Nave, R.L.; Mulliniks, J.T.; Delevatti, L.M.; Koscheck, J.F.; Romanzini, E.P.; Ferrari, A.C.; Renesto, D.M.; Berchielli, T.T.; et al. Influence of post-weaning management system during the finishing phase on grasslands or feedlot on aiming to improvement of the beef cattle production. Agric. Syst. 2017, 153, 23–31. [Google Scholar] [CrossRef]

- AHDB. UK and EU Cow Numbers; Agriculture and Horticulture Development Board, Market and Prices: Kenilworth, UK, 2020; Available online: https://ahdb.org.uk/dairy/uk-and-eu-cow-numbers (accessed on 1 March 2021).

- Schierhorn, F.; Meyfroidt, P.; Kastner, T.; Kuemmerle, T.; Prishchepov, A.V.; Müller, D. The dynamics of beef trade between Brazil and Russia and their environmental implications. Glob. Food Secur. 2016, 11, 84–92. [Google Scholar] [CrossRef]

- Prikhodko, D.; Davleyev, A. Russian Federation: Meat Sector Review; FAO Investment Centre Division: Rome, Italy, 2014; Report No. 15; Available online: http://www.fao.org/publications/card/en/c/df9b6d48-2611-4ddd-8667-962f3f86bb3d/ (accessed on 1 February 2021).

- USDA—FAS. Russia 2017 Livestock and Products Annual; U.S. Department of Agriculture, Foreign Agricultural Services: Washington, DC, USA, 2017; GAIN Report No. RS1757. Available online: https://gain.fas.usda.gov/Recent%20GAIN%20Publications/Livestock%20and%20Products%20Annual_Moscow_Russian%20Federation_11-28-2017.pdf (accessed on 1 March 2021).

- Augere-Granier, M. The EU Dairy Sector. Main Features, Challenges and Prospects; European Parliament Research Service EPRS: Bruxelles, Belgium, Briefing: PE 630.345—December 2018; pp. 1–12. Available online: http://www.europarl.europa.eu/RegData/etudes/BRIE/2018/630345/EPRS_BRI(2018)630345_EN.pdf (accessed on 24 January 2021).

- Li, X.Z.; Yan, C.G.; Zan, L.S. Current situation and future prospects for beef production in China—A review. Asian-Australas. J. Anim. Sci. 2018, 31, 984. [Google Scholar] [CrossRef] [PubMed]

- Chen, H. The Beef Market in China. Market Overview of China’s Beef Market; Agriculture and Horticulture Development Board AHDB: Kenilworth, UK, 2020; Agri-Food Report; Available online: https://projectblue.blob.core.windows.net/media/Default/What%20we%20do/Exports/ChinaBeefReport_200617_WEB.pdf (accessed on 17 February 2021).

- Deblitz, C.; Almadani, M.I. International Comparison Beef. In Proceedings of the 18th Agri Benchmark Beef and Sheep Conference, Online Conference, Prague, Czech Republic, 12–17 June 2020; Available online: http://www.agribenchmark.org/beef-and-sheep/conferences/2020-online-conference.html (accessed on 15 November 2020).

- Almadani, M.I. The Latest Developments. In Proceedings of the 15th Agri Benchmark Beef and Sheep Conference, Saskatoon, SK, Canada, 17–23 June 2017; Available online: http://www.agribenchmark.org/beef-and-sheep/conferences/2017-canada.html (accessed on 15 November 2020).

- Colby, L. World Sheep Meat Market to 2025; Agriculture and Horticulture Development Board AHDB Beef & Lamb and the International Meat Secretariat IMS: Kenilworth, UK; Paris, France, 2015; Joint report 2015; ISBN 978-1-904437-95-6. Available online: http://www.dmia.nl/images/world_sheep_meat_market_to_2025___ims_report_august_2016.pdf (accessed on 18 January 2021).

- MLA. Meat & Livestock Australia—Annual Report 2010–2011; Meat & Livestock Australia: North Sydney, NSW, Australia, 2011; ISBN 9781741915990. Available online: https://www.mla.com.au/globalassets/mla-corporate/generic/about-mla/anual-report-2010-11-final.pdf (accessed on 30 January 2021).

- Weeks, P.D. Latest Developments in Australia: Severe Droughts and Floods. In Proceedings of the 17th Agri Benchmark Beef and Sheep Conference, Windhoek, Namibia, 7–12 June 2019; Available online: http://www.agribenchmark.org/beef-and-sheep/conferences/2019-namibia.html (accessed on 15 November 2020).

- Weeks, P.D.; Weeks Consulting Services Pty Ltd., Sydney, NSW, Australia. The Impact of Severe Droughts on the Australian Cattle Herd. Personal communication, 2021. [Google Scholar]

- MLA. Market Supplier Snapshot Sheepmeat—New Zealand; Meat & Livestock Australia, Industry Insights: North Sydney, NSW, Australia, 2018; Available online: https://www.mla.com.au/globalassets/mla-corporate/prices--markets/documents/os-markets/red-meat-market-snapshots/mla-ms-nz-snapshot-2018.pdf (accessed on 30 January 2021).

- B+LNZ. Annual Report—2013-14. Beef + Lamb New Zealand, Wellington, New Zealand. 2015, Annual Report. Available online: https://beeflambnz.com/sites/default/files/content-pages/2013-14-blnz-annual-report.pdf (accessed on 11 January 2021).

- Herranz García, E.H. Report on the Current Situation and Future Prospects for the Sheep and Goat Sectors in the EU.; European Parliament, Committee on Agriculture and Rural Development: Bruxelles, Belgium, 2018; Report A8-0064/2018; Available online: https://www.europarl.europa.eu/doceo/document/A-8-2018-0064_EN.html (accessed on 19 January 2021).

- Ansari-Renani, H.R. An investigation of organic sheep and goat production by nomad pastoralists in southern Iran. Pastoralism 2016, 6, 1–9. [Google Scholar] [CrossRef] [Green Version]

- Keshavarz, M.; Karami, E.; Vanclay, F. The social experience of drought in rural Iran. Land Use Policy 2013, 30, 120–129. [Google Scholar] [CrossRef]

- Bourse & Bazaar. Iranians Forced to Forgo Meat Staples as Prices Soar; Bourse & Bazaar Economy, Bourse & Bazaar Foundation: London, UK, 2019; Available online: https://www.bourseandbazaar.com/articles/2019/5/8/iranians-forced-to-forgo-meat-staples-as-prices-soar (accessed on 28 January 2021).

- USMEF. China’s Sheep Meat Market. Weak, Due to Increased Domestic and Foreign Supplies; U.S. Meat Export Federation: Denver, CO, USA, 2016. Available online: https://www.usmef.org/chinas-sheep-meat-market-weak-due-to-increased-domestic-and-foreign-supplies/ (accessed on 9 January 2021).

- MLA. Market. Snapshot—Beef & Sheepmeat—Greater China; Meat & Livestock Australia: North Sydney, NSW, Australia, 2020; Market Snapshot; Available online: https://www.mla.com.au/globalassets/mla-corporate/prices—markets/documents/os-markets/red-meat-market-snapshots/2020/greater-china_2020-mla-mi-snapshot-28092020-distribution.pdf (accessed on 6 May 2021).

- FAO. FAO Meat Price Indices—Total Series; FAO: Rome, Italy, 2021; Available online: http://www.fao.org/fileadmin/templates/est/COMM_MARKETS_MONITORING/Meat/Documents/FAO_MeatPriceIndices_totalseries.xls (accessed on 5 April 2021).

| North America | South America | Europe | China | |

| Countries | CA, MX, USA | AR, BR, CO, PE, PY, UY | AT, CH, CZ, DE, ES, FI, FR, IE, IT, PT, PL, RU, UK | China mainland |

| Production share of total FPPI countries over 2014–2016 | 28% USA: 22% | 28% BR: 18% | 20% RU: 9% | 12% |

| Prices’ correlation range value | 0.74–0.97 value ˂ 0.001 | 0.74–0.97 value ˂ 0.001 | 0.81–0.99 value ˂ 0.001 |

| Oceania | Europe | Iran | |

| Countries | AU, NZ | DE, ES, FR, IE, PT, UK | Iran |

| Production share of total LPPI countries over 2014–2016 | 56% AU: 32%, NZ: 24% | 31% UK: 16% | 11% |

| Prices’ correlation range Value | 0.95 value ˂ 0.001 | 0.80–0.96 value ˂ 0.001 |

| China | Oceania | Europe | |

| Countries | China mainland | AU, NZ | DE, ES, FR, IE, PT, UK |

| Production share of total SPPI countries over 2014–2016 | 60% | 16% AU: 10% | 8% UK: 4% |

| Prices’ correlation range Value | 0.95 value ˂ 0.001 | 0.84–0.95 value ˂ 0.001 |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Almadani, M.I.; Weeks, P.; Deblitz, C. Introducing the World’s First Global Producer Price Indices for Beef Cattle and Sheep. Animals 2021, 11, 2314. https://doi.org/10.3390/ani11082314

Almadani MI, Weeks P, Deblitz C. Introducing the World’s First Global Producer Price Indices for Beef Cattle and Sheep. Animals. 2021; 11(8):2314. https://doi.org/10.3390/ani11082314

Chicago/Turabian StyleAlmadani, Mohamad Isam, Peter Weeks, and Claus Deblitz. 2021. "Introducing the World’s First Global Producer Price Indices for Beef Cattle and Sheep" Animals 11, no. 8: 2314. https://doi.org/10.3390/ani11082314