Information Technology Governance on Audit Technology Performance among Malaysian Public Sector Auditors

Abstract

:1. Introduction

2. Motivation of Study

3. Literature Reviews

3.1. The Concept of Governance in Information Technology

3.2. IT Governance (ITG) Effectiveness

3.3. Audit Technology Performance

3.4. IT Governance and Performance

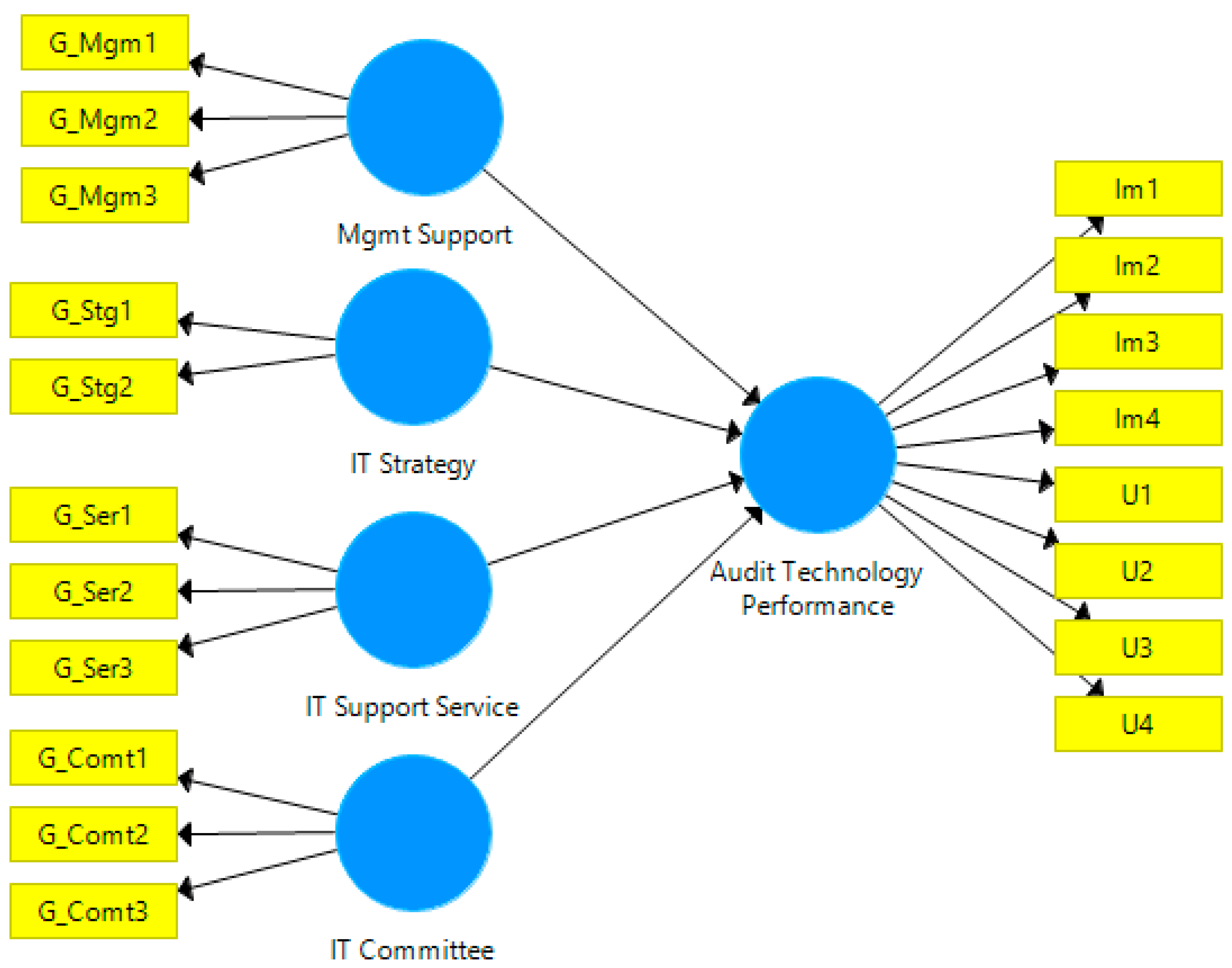

4. Hypothesis Development and Research Model

5. Research Method

6. Data Analysis

6.1. Respondents’ Profile

6.2. Assessment of Measurement Model

6.3. Assessment of Structural Model

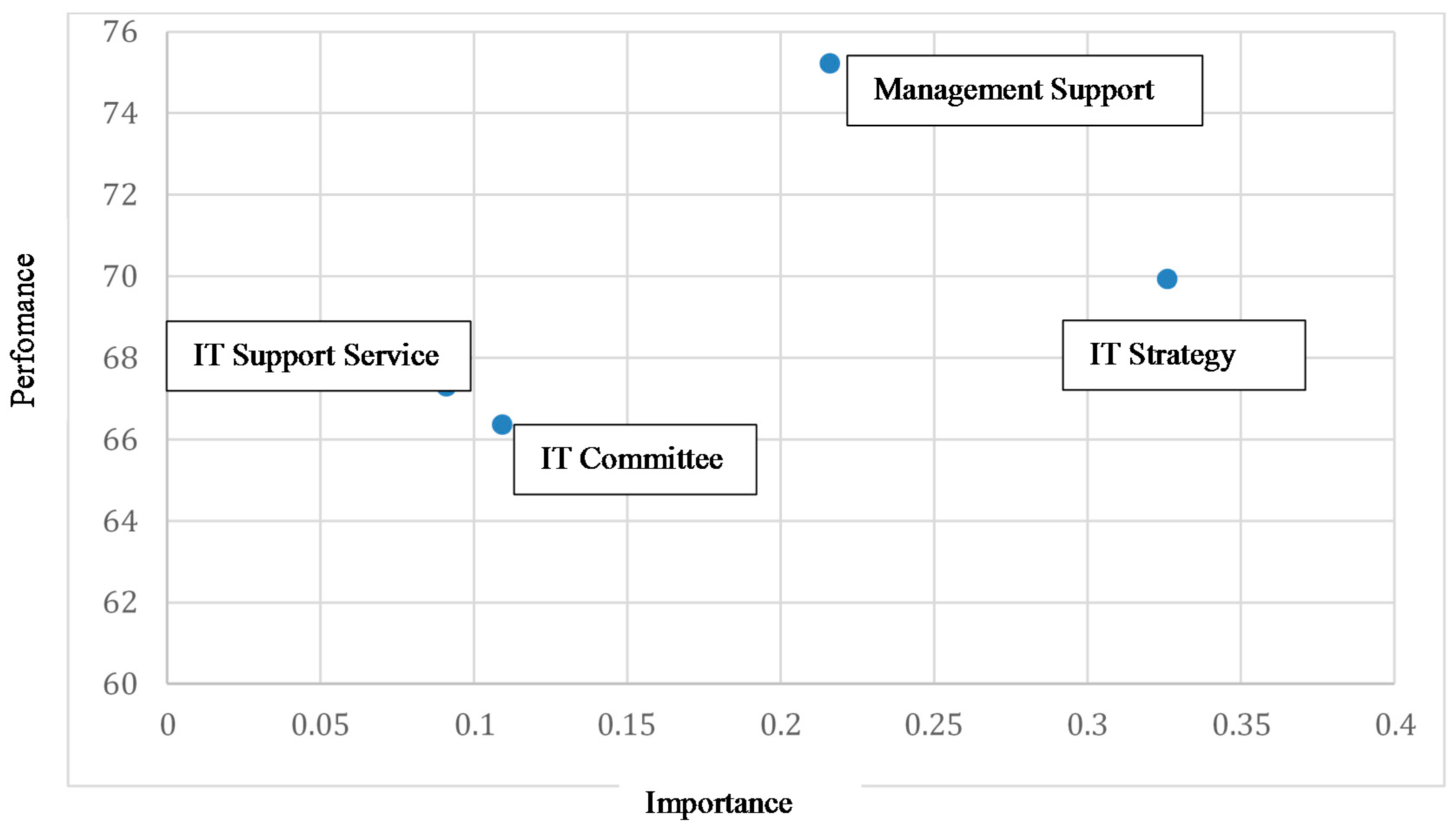

6.4. Importance Performance Matrix Analysis (IPMA)

7. Discussion and Conclusions

7.1. Discussion

7.2. Contribution

7.3. Limitations and Future Research Direction

Author Contributions

Funding

Conflicts of Interest

References

- Ahmi, Aidi, and Simon Kent. 2013. The utilisation of generalized audit software (GAS) by external auditors. Managerial Auditing Journal 28: 88–113. [Google Scholar] [CrossRef]

- Ali, Syaiful, and Peter Green. 2012. Effective information technology (IT) governance mechanisms: An IT outsourcing perspective. Information Systems Frontiers 14: 179–93. [Google Scholar] [CrossRef]

- Al Omari, Loai, and Paul Barnes. 2014. IT governance stability in a political changing environment: Exploring potential impacts in the public sector. Journal of Information Technology Management 25: 41–53. [Google Scholar]

- Amid, Amin, Morteza Moalagh, and Ahad Zare Ravasan. 2012. Identification and classification of ERP critical failure factors in Iranian industries. Information Systems 37: 227–37. [Google Scholar] [CrossRef]

- Bagozzi, Richard P., and Youjae Yi. 1988. On the evaluation of structural equation models. Journal of the Academy of Marketing Science 16: 74–94. [Google Scholar] [CrossRef]

- Bhattacharjya, Jyotirmoyee, and Vaneesa Chang. 2007. Evolving IT governance practices for aligning IT with business—A case study in an Australian institution of higher education. Journal of Information Science and Technology 4: 24–46. [Google Scholar]

- Bierstaker, James, Diane Janvrin, and David Jordan Lowe. 2014. What factors influence auditors’ use of computer-assisted audit techniques? Advances in Accounting 30: 67–74. [Google Scholar] [CrossRef]

- Baruch, Yehuda, and Brooks C. Holtom. 2008. Survey response rate levels and trends in organizational research. Human Relations 61: 1139–60. [Google Scholar] [CrossRef]

- Buang, Ambrin. 2015. Country paper leveraging technology to enhance audit quality and effectiveness National Audit Department of Malaysia. Paper presented at the 6th ASOSAI Symposium, Kuala Lumpur, Malaysia, February 12. [Google Scholar]

- Buchwald, Arne, Nils Urbach, and Frederik Ahlemann. 2014. Business value through controlled IT: Toward an integrated model of IT governance success and its impact. Journal of Information Technology 29: 128–47. [Google Scholar] [CrossRef]

- Chin, Wynne W., Barbara L. Marcolin, and Peter R. Newsted. 2003. A partial least squares latent variable modeling approach for measuring interaction effects: Results from a Monte Carlo simulation study and an electronic-mail emotion/adoption study. Information Systems Research 14: 189–217. [Google Scholar] [CrossRef]

- Cohen, Jacob. 1988. Statistical Power Analysis for the Behavioral Sciences, 2nd ed. Hillsdale: Lawrence Earlbaum Associates. [Google Scholar]

- DeLone, William H., and Ephraim R. McLean. 1992. Information systems success: The quest for the dependent variable. Information Systems Research 3: 60–95. [Google Scholar] [CrossRef]

- DeLone, William H., and Ephraim R. McLean. 2003. The DeLone and McLean model of information systems success: A ten-year update. Journal of Management Information Systems 19: 9–30. [Google Scholar]

- Dubnick, Melvin J., and H. George Frederickson. 2010. Accountable agents: Federal performance measurement and third-party government. Journal of Public Administration Research and Theory 20: i143–59. [Google Scholar] [CrossRef]

- Ferguson, Colin, Peter Green, Ravi Vaswani, and Gang Wu. 2013. Determinants of effective information technology governance. International Journal of Auditing 17: 75–99. [Google Scholar] [CrossRef]

- Floropoulos, Jordan, Charalambos Spathis, Dimitrios Halvatzis, and Maria Tsipouridou. 2010. Measuring the success of the Greek taxation information system. International Journal of Information Management 30: 47–56. [Google Scholar] [CrossRef]

- Fornell, Claes, and David F. Larcker. 1981. Structural equation models with unobservable variables and measurement error: Algebra and statistics. Journal of Marketing Research 18: 382–88. [Google Scholar] [CrossRef]

- Geisser, Seymour. 1974. A predictive approach to the random effect model. Biometrika 61: 101–7. [Google Scholar] [CrossRef]

- Ghobakhloo, Morteza, and Sai Hong Tang. 2015. Information system success among manufacturing SMEs: Case of developing countries. Information Technology for Development 21: 573–600. [Google Scholar] [CrossRef]

- Gold, Andrew H., Arvind Malhotra, and Albert H. Segars. 2001. Knowledge management: An organizational capabilities perspective. Journal of Management Information Systems 18: 185–214. [Google Scholar] [CrossRef]

- Gorla, Narasimhaiah, Toni M. Somers, and Betty Wong. 2010. Organizational impact of system quality, information quality, and service quality. The Journal of Strategic Information Systems 19: 207–28. [Google Scholar] [CrossRef]

- Grover, Varun, and Rajiv Kohli. 2012. Cocreating IT value: New capabilities and metrics for multifirm environments. MIS Quarterly 36: 225–32. [Google Scholar]

- Haes, Steven De, and Wim Van Grembergen. 2009. An exploratory study into IT governance implementations and its impact on business/IT alignment. Information Systems Management 26: 123–37. [Google Scholar] [CrossRef]

- Hair, Joseph F., Jr., William C. Black, Barry J. Babin, and Rolph E. Anderson. 2010. Multivariate Data Analysis, 7th ed. London: Pearson. [Google Scholar]

- Hair, Joseph F., Jr., G. Tomas M. Hult, Christian Ringle, and Marko Sarstedt. 2014. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM). Los Angeles: Sage Publications. [Google Scholar]

- Hair, Joseph F., Jr., G. Tomas M. Hult, Christian Ringle, and Marko Sarstedt. 2016. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM), 2nd ed. Thousand Oaks: Sage Publications. [Google Scholar]

- Hall, James A. 2015. Information Technology Auditing, 4th ed. Boston: Cengage Learning. [Google Scholar]

- Havelka, Douglas, and Jeffrey W. Merhout. 2013. Internal information technology audit process quality: Theory development using structured group processes. International Journal of Accounting Information Systems 14: 165–92. [Google Scholar] [CrossRef]

- Heart, Tsipi, Hanan Maoz, and Nava Pliskin. 2010. From governance to adaptability: The mediating effect of IT executives’ managerial capabilities. Information Systems Management 27: 42–60. [Google Scholar] [CrossRef]

- Henseler, Jörg, Christian Ringle, and Marko Sarstedt. 2015. A new criterion for assessing discriminant validity in variance-based structural equation modeling. Journal of the Academy of Marketing Science 43: 115–35. [Google Scholar] [CrossRef]

- Huang, Rui, Robert W. Zmud, and R. Leon Price. 2010. Influencing the effectiveness of IT governance practices through steering committees and communication policies. European Journal of Information Systems 19: 288–302. [Google Scholar] [CrossRef]

- Hussein, Ramlah, Nor Shahriza Abdul Karim, and Mohd Hasan Selamat. 2007. The impact of technological factors on information systems success in the electronic-government context. Business Process Management Journal 13: 613–27. [Google Scholar] [CrossRef]

- Ifinedo, Princely. 2011. Examining the influences of external expertise and in-house computer/IT knowledge on ERP system success. Journal of Systems and Software 84: 2065–78. [Google Scholar] [CrossRef]

- Ilebrand, Nicklas, Tor Mesøy, and Remco Vlemmix. 2010. Using IT to enable a lean transformation. McKinsey on Business Technology 18: 1–3. [Google Scholar]

- Information System Audit and Controls Association (ISACA). 2009. In Summary: The Taking Governance Forward Mapping Initiative. ISACA Journal 1: 1–10. [Google Scholar]

- IT Governance Institute (ITGI). 2003. Board Briefing on IT Governance, 2nd ed. Rolling Meadows: Information Systems Assurance and Control Association (ISACA). [Google Scholar]

- Kim, Hyo-Jeong, Michael Mannino, and Robert J. Nieschwietz. 2009. Information technology acceptance in the internal audit profession: Impact of technology features and complexity. International Journal of Accounting Information Systems 10: 214–28. [Google Scholar] [CrossRef]

- Kline, Rex. 2011. Principles and Practice of Structural Equation Modeling, 3rd ed. New York: Guilford Press. [Google Scholar]

- Kock, Ned, and Gary Lynn. 2012. Lateral collinearity and misleading results in variance-based SEM: An illustration and recommendations. Journal of the Association for Information Systems 13: 546–80. [Google Scholar] [CrossRef]

- Kovaľová, Marcela. 2016. People in the Process of Innovation and as the Factor Increasing Business Performance. Forum Scientiae Oeconomia 4: 15–26. [Google Scholar]

- Law, Chuck C. H., Charlie C. Chen, and Bruce J. P. Wu. 2010. Managing the full ERP life-cycle: Considerations of maintenance and support requirements and IT governance practice as integral elements of the formula for successful ERP adoption. Computers in Industry 61: 297–308. [Google Scholar] [CrossRef]

- Li, Xiaolin, Sharma Pillutla, Huaming Zhou, and Dong-Qing Yao. 2015. Drivers of adoption and continued use of e-procurement systems: Empirical evidence from China. Journal of Organizational Computing and Electronic Commerce 25: 262–88. [Google Scholar] [CrossRef]

- Liang, Ting-Peng, Yi-Chieh Chiu, Shelly P. J. Wu, and Deimar Straub. 2011. The impact of IT governance on organizational performance. Paper presented at the 7th Americas Conference on Information Systems, Detroit, MI, USA, August 4–7. [Google Scholar]

- Low, Chinyao, Yahsueh Chen, and Mingchang Wu. 2011. Understanding the determinants of cloud computing adoption. Industrial Management and Data Systems 111: 1006–23. [Google Scholar] [CrossRef]

- Lunardi, Guilherme Lerch, Joao Luiz Becker, Antonio Carlos Gastaud Maçada, and Pietro Cunha Dolci. 2014. The impact of adopting IT governance on financial performance: An empirical analysis among Brazilian firms. International Journal of Accounting Information Systems 15: 66–81. [Google Scholar] [CrossRef]

- Lunardi, Guilherme Lerch, Antonio Carlos Gastaud Maçada, João Luiz Becker, and Wim Van Grembergen. 2017. Antecedents of IT Governance effectiveness: An empirical examination in Brazilian firms. Journal of Information Systems 31: 41–57. [Google Scholar] [CrossRef]

- Mahzan, Nurmazilah, and Andy Lymer. 2014. Examining the adoption of computer-assisted audit tools and techniques: Cases of generalized audit software use by internal auditors. Managerial Auditing Journal 29: 327–49. [Google Scholar] [CrossRef]

- Mahzan, Nurmazilah, and Farida Veerankutty. 2011. IT auditing activities of public sector auditors in Malaysia. African Journal of Business Management 5: 1551–63. [Google Scholar]

- Maijoor, Steven. 2000. The internal control explosion. International Journal of Auditing 4: 101–9. [Google Scholar] [CrossRef]

- Masli, Adi, Gary F. Peters, Vernon J. Richardson, and Juan Manuel Sanchez. 2010. Examining the potential benefits of internal control monitoring technology. The Accounting Review 85: 1001–34. [Google Scholar] [CrossRef]

- Mukhtar, Ramlah, and Noor Azman Ali. 2011. Quality governance of human aspects of quality initiatives in the public service sector. Current Issues of Business and Law 6: 111–28. [Google Scholar] [CrossRef]

- National Audit Department of Malaysia (NADM). 2015. IT Audit-Issues, Lesson Learnt and Actions for A Successful IT System Implementation. Paper presented at the 24th Meeting of the INTOSAI Working Group on IT Audit, Warsaw, Poland, June 29–July 1. [Google Scholar]

- Nawi, Haslinda Sutan Ahmad, Azizah Abdul Rahman, and Othman Ibrahim. 2011. Government’s ICT project failure factors: A revisit. Paper presented at International Conference on Research and Innovation in Information Systems (ICRIIS), Kuala Lumpur, Malaysia, November 23–24. [Google Scholar]

- Nfuka, Edephonce N., and Lazar Rusu. 2010. Critical success factors for effective IT governance in the public sector organizations in a developing country: The case of Tanzania. Paper presented at European Conference on Information Systems, Pretoria, South Africa, August 4–7. [Google Scholar]

- Nfuka, Edephonce N., and Lazar Rusu. 2011. The effect of critical success factors on IT governance performance. Industrial Management and Data Systems 111: 1418–48. [Google Scholar] [CrossRef]

- Nkhoma, Mathews Z., and Duy P. T. Dang. 2013. Contributing factors of cloud computing adoption: A Technology-Organisation-Environment framework approach. International Journal of Information Systems and Engineering 1: 38–49. [Google Scholar]

- Paprocki, Wojciech. 2016. Industry 4.0 Concept and Its Application in the Conditions of the Digital Economy. Digitization of the Economy and Society. Opportunities and Challenges for Infrastructure Sectors. Gdańsk: European Financial Congress, pp. 39–57. [Google Scholar]

- Peirson, Graham. 1990. A Report on Institutional Arrangements for Accounting Standard Setting in Australia. Melbourne: Australian Accounting Research Foundation. [Google Scholar]

- Protiviti. 2016a. Arriving at Internal Audit’s Tipping Point Amid Business Transformation: Assessing the Results of the 2016 Internal Audit Capabilities and Needs Survey—And a Look at Key Trends over the Past Decade. Available online: http://www.protiviti.com/en-US/Documents/Surveys/2016-Internal-Audit-Capabilities-and-Needs-Survey-Protiviti.pdf (accessed on 31 March 2017).

- Protiviti. 2016b. A Global Look at IT Audit Best Practices: Assessing the International Leaders in an Annual ISACA/Protiviti Survey. Available online: http://www.protiviti.com/en-US/Documents/Surveys/5th-Annual-IT-Audit-Benchmarking-Survey-ISACA-Protiviti.pdf (accessed on 31 March 2017).

- Protiviti. 2018. Analytic in Auditing Is a Game Changer. Available online: https://www.protiviti.com/sites/default/files/united_kingdom/insights/2018-internal-audit-capabilities-and-needs-survey-protiviti-global_version.pdf (accessed on 29 July 2018).

- Ramayah, Thurasamy, Jason Wai Chow Lee, and Julie Boey Chyaw. 2011. Network collaboration and performance in the tourism sector. Service Business 5: 411. [Google Scholar] [CrossRef]

- Ringle, Christian M., Sven Wende, and Jan-Michael Becker. 2015. SmartPLS 3. Boenningstedt, Germany. Available online: http://www.smartpls.com (accessed on 28 July 2016).

- Rose, Anna M., Jacob M. Rose, Kerri-Ann Sanderson, and Jay C. Thibodeau. 2017. When should audit firms introduce analyses of Big Data into the audit process? Journal of Information Systems 31: 81–99. [Google Scholar] [CrossRef]

- Rosli, Khairina, Paul H. P. Yeow, and Siew Eu-Gene. 2013. Adoption of audit technology in audit firms. Paper presented at 24th Australasian Conference on Information Systems (ACIS), Melbourne, Australia, December 4–6. [Google Scholar]

- Saunders, Mark, Philip Lewis, and Andrian Thornhill. 2009. Research Methods for Business, 5th ed. Harlow: Prentice Hall. [Google Scholar]

- Schillemans, Thomas, and Madalina Busuioc. 2015. Predicting public sector accountability: From agency drift to forum drift. Journal of Public Administration Research and Theory 25: 191–215. [Google Scholar] [CrossRef]

- Sekaran, Uma, and Roger Bougie. 2010. Research Method for Business, 5th ed. New York: John Wiley and Sons. [Google Scholar]

- Ślusarczyk, Beata. 2018. Industry 4.0—Are we ready? Polish Journal of Management Studies 17: 232–48. [Google Scholar]

- Soral, G., and Monika Jain. 2011. Impact of ERP system on auditing and internal control. The International Journal’s Research: Journal of Social Sciences and Management 1: 16–23. [Google Scholar]

- Stone, Mervyn. 1974. Cross-validatory choice and assessment of statistical predictions. Journal of the Royal Statistical Society. Series B (Methodological) 36: 111–47. [Google Scholar]

- Sullivan, Gail M., and Richard Feinn. 2012. Using effect size—Or why the P value is not enough. Journal of Graduate Medical Education 4: 279–82. [Google Scholar] [CrossRef] [PubMed]

- Tsai, Wen-Hsien, Yu-Wei Chou, Jun-Der Leu, Der Chao Chen, and Tsen-Shu Tsaur. 2015. Investigation of the mediating effects of IT governance-value delivery on service quality and ERP performance. Enterprise Information Systems 9: 139–60. [Google Scholar] [CrossRef]

- United Nations Development Programme (UNDP). 1997. Governance for Sustainable Human Development: A Policy Document. New York: United Nations, Available online: http://pogar.org/publications/other/undp/governance/undppolicydoc97-e.pdf (accessed on 30 January 2016).

- Urbach, Nils, Stefan Smolnik, and Gerold Riempp. 2010. An empirical investigation of employee portal success. The Journal of Strategic Information Systems 19: 184–206. [Google Scholar] [CrossRef]

- Vasarhelyi, Miklos A., and Silvia Romero. 2014. Technology in audit engagements: A case study. Managerial Auditing Journal 29: 350–65. [Google Scholar] [CrossRef]

- Wang, Yu-Min, Yi-Shun Wang, and Yong-Fu Yang. 2010. Understanding the determinants of RFID adoption in the manufacturing industry. Technological Forecasting and Social Change 77: 803–15. [Google Scholar] [CrossRef]

- Weill, Peter, and Jeanne W. Ross. 2004. IT Governance: How Top Performers Manage IT Decision Rights for Superior Results. Boston: Harvard Business School Press. [Google Scholar]

- Widuri, Rindang, Brendan O’Connell, and Prem W. S. Yapa. 2014. Adoption and use of generalized audit software by Indonesian audit firms: Some preliminary findings. Paper presented at the 4th Annual International Conference on Accounting and Finance (AF 2014), Singapore, April 28–29. [Google Scholar]

- Wilkin, Carla L., and Robert H. Chenhall. 2010. A review of IT governance: A taxonomy to inform accounting information systems. Journal of Information Systems 24: 107–46. [Google Scholar] [CrossRef]

- Yeap, Jasmine A. L., Thurasamy Ramayah, and Pedro Soto-Acosta. 2016. Factors propelling the adoption of m-learning among students in higher education. Electronic Markets 26: 323–38. [Google Scholar] [CrossRef]

- Smidt, Louis, Aidi Ahmi, Leandi Steenkamp, D. P. van der Nest, and Dave Lubbe. 2018. A Maturity-level Assessment of Generalised Audit Software: Internal Audit Functions in Australia. Australian Accounting Review. forthcoming. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

| Code | Item Measurement | Adapted from |

|---|---|---|

| G1-IT Committee | IT Committee | |

| G_Com1 | IT steering committee provides strategic direction for IT related audit engagement that is in line with the strategic directions of the organisation | (Ferguson et al. 2013) |

| G_Com1 | IT steering committee provides a mechanism for coordinating IT related audit engagement | (Ferguson et al. 2013) |

| G_Com1 | IT steering committee provides leadership in managing IT related activities | (Ferguson et al. 2013) |

| G2-IT Strategy | IT Strategy | |

| G_Stg1 | IT strategy provides strategic direction and the alignment of IT and organisation activities | (Ali and Green 2012) |

| G_Stg1 | IT strategy provides direction for sourcing and use of IT resources, skills and infrastructure to meet the strategic objective | (Ali and Green 2012) |

| G3-IT Support | IT Support Service | |

| G_Ser1 | Auditors assisted by strong IT support from IT staff | (Ahmi and Kent 2013) |

| G_Ser2 | Auditors aided through the availability of internal IT audit expertise | (Ahmi and Kent 2013) |

| G_Ser3 | Auditors aided by external technical support | (Kim et al. 2009) |

| G4-Mgmt Support | Management Support | |

| G_Mgm1 | Senior managements believe the use of audit technology is a good idea. | (Li et al. 2015) |

| G_Mgm2 | Senior managements are interested in audit technology usage during the audit task | (Li et al. 2015) |

| G_Mgm3 | Senior managements support the use of audit technology in audit task | (Li et al. 2015) |

| Respondent Profiles | Frequency | Percentage | |

|---|---|---|---|

| Audit Structure | Federal Government | 105 | 34.0 |

| State Government | 125 | 40.4 | |

| Statutory Bodies | 79 | 25.6 | |

| Gender | Male | 72 | 23.3 |

| Female | 237 | 76.7 | |

| Job Position | Senior Management | 31 | 10.0 |

| Middle Management | 68 | 22.0 | |

| Support Staff | 210 | 68.0 | |

| Age | From 21 to 30 years | 56 | 18.1 |

| From 31 to 40 years | 174 | 56.3 | |

| From 41 to 50 years | 52 | 16.8 | |

| From 51 to 60 years | 27 | 8.8 | |

| Experience in auditing | Less than 2 years | 5 | 1.6 |

| From 2 to 4 years | 35 | 11.3 | |

| From 5 to 9 years | 125 | 40.5 | |

| From 10 to 15 years | 80 | 25.9 | |

| More than 15 years | 64 | 20.7 | |

| Experience using audit technology | Less than 2 years | 96 | 31.1 |

| From 2 to 4 years | 74 | 23.9 | |

| From 5 to 9 years | 80 | 25.9 | |

| From 10 to 15 years | 38 | 12.3 | |

| More than 15 years | 21 | 6.8 | |

| Perceived level of IT skill | Very Basic | 17 | 5.5 |

| Basic | 100 | 32.4 | |

| Adequate | 104 | 33.7 | |

| Good | 78 | 25.2 | |

| Very Good | 10 | 3.2 | |

| Constructs | Measurement Items | Loading Range | Cronbach’s Alpha | Composite Reliability | Average Variance Extracted |

|---|---|---|---|---|---|

| Audit Technology Performance | Im1, Im2, Im3, Im4, U1, U2, U3, U4 | 0.773–0.826 | 0.913 | 0.930 | 0.623 |

| IT Committee | G_Comt1, G_Comt2, G_Comt3 | 0.967–0.971 | 0.967 | 0.979 | 0.939 |

| IT Strategy | G_Stg1, G_Stg2 | 0.989–0.990 | 0.979 | 0.990 | 0.979 |

| IT support service | G_Ser1, G_Ser2, G_Ser3 | 0.940–0.966 | 0.949 | 0.967 | 0.908 |

| Management Support | G_Mgm1, G_Mgm2, G_Mgm3 | 0.920–0.940 | 0.931 | 0.956 | 0.878 |

| Constructs | Audit Technology Performance | IT Committee | IT Strategy | IT Support Service | Management Support |

|---|---|---|---|---|---|

| Audit Technology Performance | |||||

| IT Committee | 0.483 | ||||

| IT Strategy | 0.569 | 0.625 | |||

| IT Support Service | 0.389 | 0.551 | 0.471 | ||

| Management Support | 0.499 | 0.398 | 0.425 | 0.271 |

| Hypothesis | Relationship | Std Beta | Std Error | t-Value | Decision | R2 | f2 | Q2 |

|---|---|---|---|---|---|---|---|---|

| H1a | IT Committee → Audit Technology Performance | 0.109 | 0.069 | 1.548 | Not Supported | 0.010 | ||

| H1b | IT Strategy → Audit Technology Performance | 0.325 | 0.070 | 4.894 * | Supported | 0.098 | ||

| H1c | IT support service → Audit Technology Performance | 0.091 | 0.062 | 1.437 | Not Supported | 0.009 | ||

| H1d | Management Support → Audit Technology Performance | 0.266 | 0.059 | 4.403 * | Supported | 0.381 | 0.093 | 0.232 |

© 2018 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Veerankutty, F.; Ramayah, T.; Ali, N.A. Information Technology Governance on Audit Technology Performance among Malaysian Public Sector Auditors. Soc. Sci. 2018, 7, 124. https://doi.org/10.3390/socsci7080124

Veerankutty F, Ramayah T, Ali NA. Information Technology Governance on Audit Technology Performance among Malaysian Public Sector Auditors. Social Sciences. 2018; 7(8):124. https://doi.org/10.3390/socsci7080124

Chicago/Turabian StyleVeerankutty, Farida, Thurasamy Ramayah, and Noor Azman Ali. 2018. "Information Technology Governance on Audit Technology Performance among Malaysian Public Sector Auditors" Social Sciences 7, no. 8: 124. https://doi.org/10.3390/socsci7080124