1. Introduction

The construction industry plays a vital role in the development of any country and the Kingdom of Saudi Arabia is no exception. The country has been undergoing a period of rapid urbanization, with a growing population and an increasing demand for housing. Therefore, the government has implemented the Saudi Building Code (SBC) for residential buildings, which set standards for the design, construction, maintenance, and occupancy of buildings in Saudi Arabia. The SBC was first implemented in 1986 and has been updated several times since then. The SBC has been shown to have a significant impact on residential construction costs. Ref. [

1] identified a lack of integration between the Saudi Building Code and current construction methods, suggesting a need for the incorporation of factors and elements into the code. Ref. [

2] found that leading international environmental and sustainability assessment schemes were not fully applicable to the Saudi built environment, leading to the development of a new assessment scheme. Ref. [

3] evaluated the impact of energy efficiency building codes in the GCC including Saudi Arabia and suggested a comprehensive evaluation of the relationship between sustainable building codes and their economic feasibility. Ref. [

4] examined the current status of sustainability in the Saudi building sector and identified barriers to achieving sustainable residential buildings, providing design and non-design strategies for improvement. A study by [

5] found that the SBC made it more difficult for low-income Saudi citizens to afford housing. The study found that the cost of constructing a villa in compliance with the SBC was 20% higher than the cost of constructing a villa that did not comply with the code. These papers collectively highlight the knowledge gap regarding the impact of the Saudi Building Code on residential construction costs.

The SBC aims to ensure the safety, health, and welfare of the inhabitants and the public while promoting the conservation of energy and resources.

However, the implementation of the SBC may also impact the costs of construction, which can be passed on to citizens in the form of higher housing prices. In addition, there may be an economic impact on the construction industry and overall economy. Therefore, it is important to study the additional costs imposed on citizens and the economic impact of the SBC.

This study examined the additional costs imposed on citizens and the economic impact of implementing the SBC in residential buildings. This was carried out by surveying building developers, architects, and citizens to gather data on the costs associated with adhering to the code such as the material and labor costs. Furthermore, the potential impact on the economy in terms of job creation and gross domestic product (GDP) were analyzed.

The data collected through the survey were analyzed to determine the average cost increase for building developers, architects, and citizens. Moreover, the potential impact on the economy was estimated by considering factors such as job creation, GDP growth, and the overall construction industry.

This study employed both quantitative and qualitative methods. The quantitative method involved a survey of building developers, architects, and citizens to gather data on the costs associated with adhering to the SBC. The qualitative method involved interviews with experts in the construction industry such as architects and engineers to gather their perspectives on the impact of the SBC.

The findings of this study are expected to provide valuable insights for policymakers and stakeholders in the construction industry because they consider the implementation and enforcement of building codes in the Kingdom of Saudi Arabia. By understanding the potential costs and benefits of the SBC, policymakers and stakeholders can make informed decisions that balance the safety and welfare of citizens with the country’s economic well-being.

2. Literature Review

The implementation of building codes is important for ensuring the safety, health, and welfare of the public while ensuring the conservation of energy and resources. The SBC is a set of standards for the design, construction, and maintenance of residential buildings in the Kingdom of Saudi Arabia. However, the implementation of building codes may affect the costs of construction, which can be passed on to the citizens in the form of higher housing prices. Additionally, there may be an economic impact on the construction industry and overall economy. Therefore, it is important to study the additional costs imposed on citizens and the economic impact of the SBC.

Several studies have been conducted on the implementation of building codes and their impacts on the construction industry and economy. Ref. [

6] examined the costs and benefits of implementing the SBC in the city of Jeddah. The study found that the implementation of the SBC increased the construction costs, with the average cost increase for building developers being 5.8%. The study also found that the SBC had a positive impact on the economy, with an estimated increase of 1.1% in GDP.

Another study by [

7] examined the impact of building codes on the construction industry in the Gulf Cooperation Council (GCC) countries. They found that the implementation of building codes positively impacted the construction industry, with an increase in the number of construction projects and the value of construction contracts. They also found that building codes positively influenced the economy, with an increase in GDP and employment in the construction industry.

Ref. [

8] examined the impact of building codes on the energy efficiency of residential buildings in the GCC countries. They found that the implementation of building codes improved the energy efficiency of residential buildings, with an average reduction of 15% in energy consumption. Furthermore, the building codes were found to have a positive impact on the environment, with a reduction in greenhouse gas emissions.

In addition to these studies, ref. [

9] examined the impact of building codes on housing affordability in the Kingdom of Saudi Arabia. They found that the implementation of building codes positively affected the housing affordability, with a reduction in average housing prices. They also found that building codes had a positive impact on the economy, with an increase in GDP and employment in the construction industry.

Refs. [

10,

11] emphasized the role of thermal insulation in reducing energy consumption and carbon footprint, with potential savings of up to 30–40% in air conditioning and heating devices. Ref. [

12] also emphasized the importance of building insulation and airtightness in achieving energy savings.

The studies reviewed in this literature review demonstrate that the implementation of building codes can have both positive and negative impacts on the construction industry and economy. The implementation of building codes can result in an increase in construction costs but can also have a positive impact on the economy, with an increase in GDP and employment in the construction industry. In addition, building codes can positively affect energy efficiency and housing affordability.

The literature review suggests that the implementation of building codes in the Kingdom of Saudi Arabia such as the SBC has both positive and negative impacts on the construction industry and economy. The implementation of building codes can increase the cost of construction while having a positive impact on the economy, energy efficiency, and housing affordability. Furthermore, the studies included in this literature review provide valuable insights for policymakers and stakeholders in the construction industry because they consider the implementation and enforcement of building codes in the Kingdom of Saudi Arabia.

3. Operation and Maintenance in the Kingdom of Saudi Arabia

The government’s interest is evident in the large amount of spending compared to their regional and global counterparts, as seen from the five-year development plans, the resulting development, and a comprehensive urban renaissance for the Kingdom. However, maintenance projects in the Kingdom of Saudi Arabia are still plagued by low efficiency despite 15% of the 2019 budget being allocated to facility management [

13]. A study prepared by the National Committee for Standardization of Operation and Maintenance (O&M) Work in the Kingdom of Saudi Arabia (2018) showed that the cost of operation and maintenance work exceeded, on average, international standards by 20% compared to similar facilities globally. However, the quality was lower by approximately 60%. The study indicated that light maintenance represented 46% and heavy maintenance represented 54% of the total government expenditure on various facility management works. Moreover, the same study noted that if O&M work was conducted in accordance with the international standards of best practices, the accumulated costs due at the present value would be less than SAR 500 billion over the next 15 years. This can decrease the average life of residential buildings, which ranges between 40 and 50 years, whereas the average service life of buildings in European countries is 100 years because of the increased and intensified building maintenance [

14]. The lack of interest in the O&M of housing in the Kingdom of Saudi Arabia increases spending, as Saudi families spend an average of 22.3% per month on the internal elements of the O&M of their homes, according to the Household Expenditure and Income Survey for the year 1428 AH. This percentage increased to 27.1% during the Survey of Expenditure and Income of Saudi Households in 1434 AH (increase of nearly 22%), confirming the importance of the O&M of housing.

4. Importance of Maintenance

The importance of the O&M process lies in the fact that it constitutes the longest phase of the project during its life cycle; therefore, the largest part of the expenditure occurs during the O&M phase, constituting approximately 60% of the total cost. In contrast, less than 15% of the total costs occur during design and implementation. The studies also note that the periodic maintenance of residential units results in a longer service life and is more economically feasible than replacement while contributing to maintaining a high market value for the building, raising the financial efficiency of managing residential units, and ensuring efficient house operation. Consequently, housing cost calculations must consider the building and construction costs along with the ongoing maintenance costs. This is because poor maintenance often causes deterioration, leading to wear and tear that result in deterioration and a lower service life of the house [

15].

Maintenance significantly affects the performance of a house, and maintenance problems that occur during the life of a building can be reduced by using more maintenance to reduce the replacement costs. Many researchers have pointed out that neglecting the maintenance of residential buildings is one of the primary reasons for poor housing in many cities worldwide, requiring urgent attention and treatment. This is because the housing quality is affected by increased maintenance costs, which can become a financial burden for low-income families. O&M practices also have an important impact on the health, safety, and comfort of the building’s occupants, the overall long-term environmental benefits, and positively impact its financial performance [

14].

Consequently, many researchers [

16,

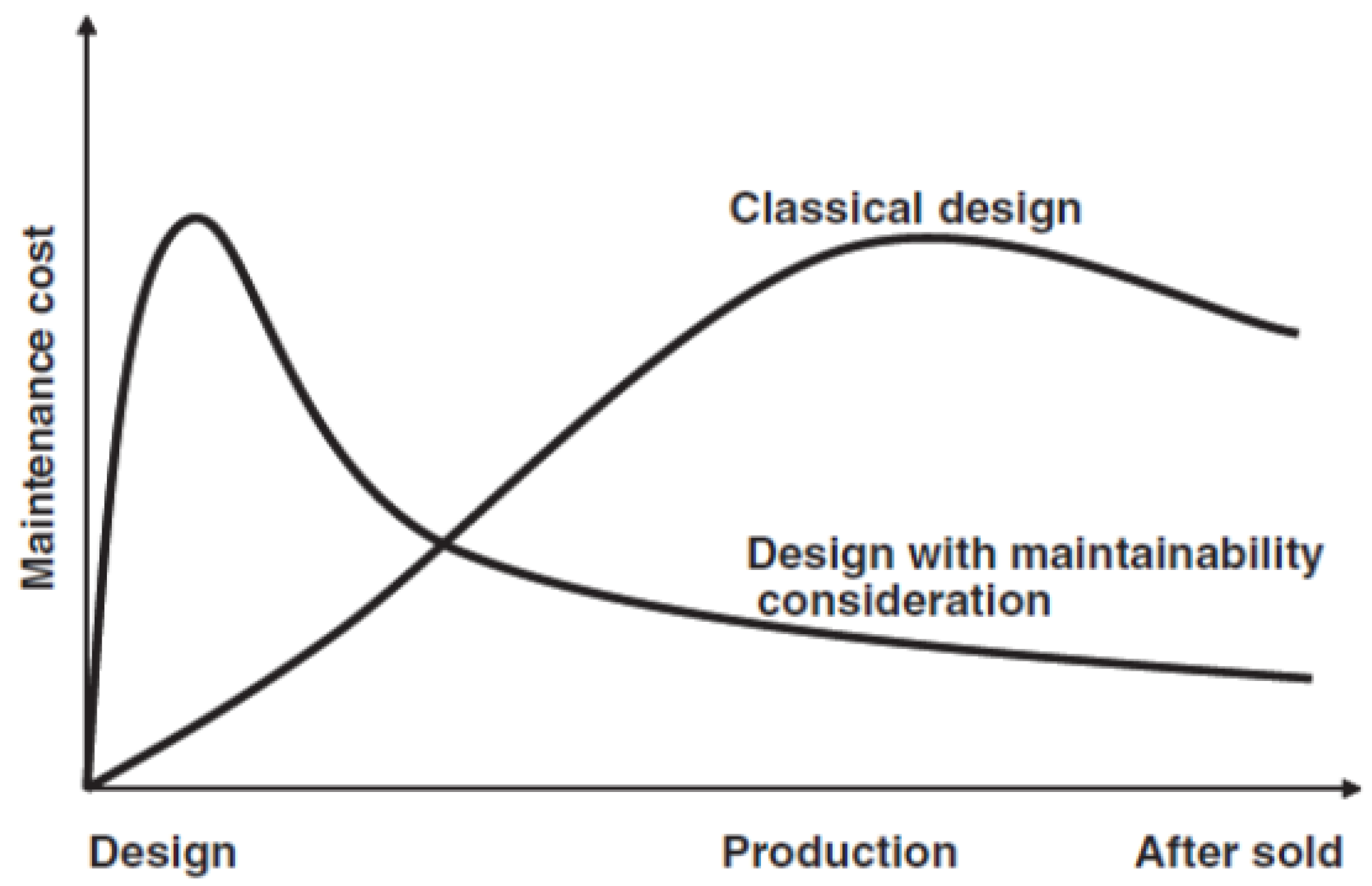

17] have recommended that there should be a binding building code that helps achieve harmonization among the diversity and complexity of engineering systems in housing units, the maintenance requirements, and an optimal operation and maintenance budget in a way that does not affect the aspirations and expectations of its residents. Therefore, the existence of a building code at the national level for designing houses in Saudi Arabia is dependent on the standards that help architects reduce the costs of housing units and increase the life of assets to achieve the highest levels of operational efficiency before the operation stage, as shown in

Figure 1. This indicates that relying on operational maintenance standards is the best methodology that an architect can follow to reduce costs and improve the performance of operational housing units by linking design processes with O&M processes and policies [

18].

5. Cost Estimation for the Operation and Maintenance of the Study Cases

The government of the Kingdom of Saudi Arabia is developing several housing programs aimed at enabling Saudi families to own their first home through several housing options and financing solutions that are compatible with the needs of Saudi families. These programs include self-construction, ready-made villas offered by the Ministry of Housing, units under construction, and units purchased from the market. Through these programs, the Ministry of Housing has succeeded in serving 111,568 Saudi families through various housing programs since the beginning of 2021, of which 87,896 live in their own homes [

19].

However, despite the great success achieved by the Ministry of Housing, the diversity and complexity of engineering systems in homes [

20], the high maintenance costs, limited budgets allocated to maintain these units for Saudi families, high aspirations and expectations of users, high and varied maintenance defects resulting from operation [

21], and increasing concerns regarding security and safety issues in homes [

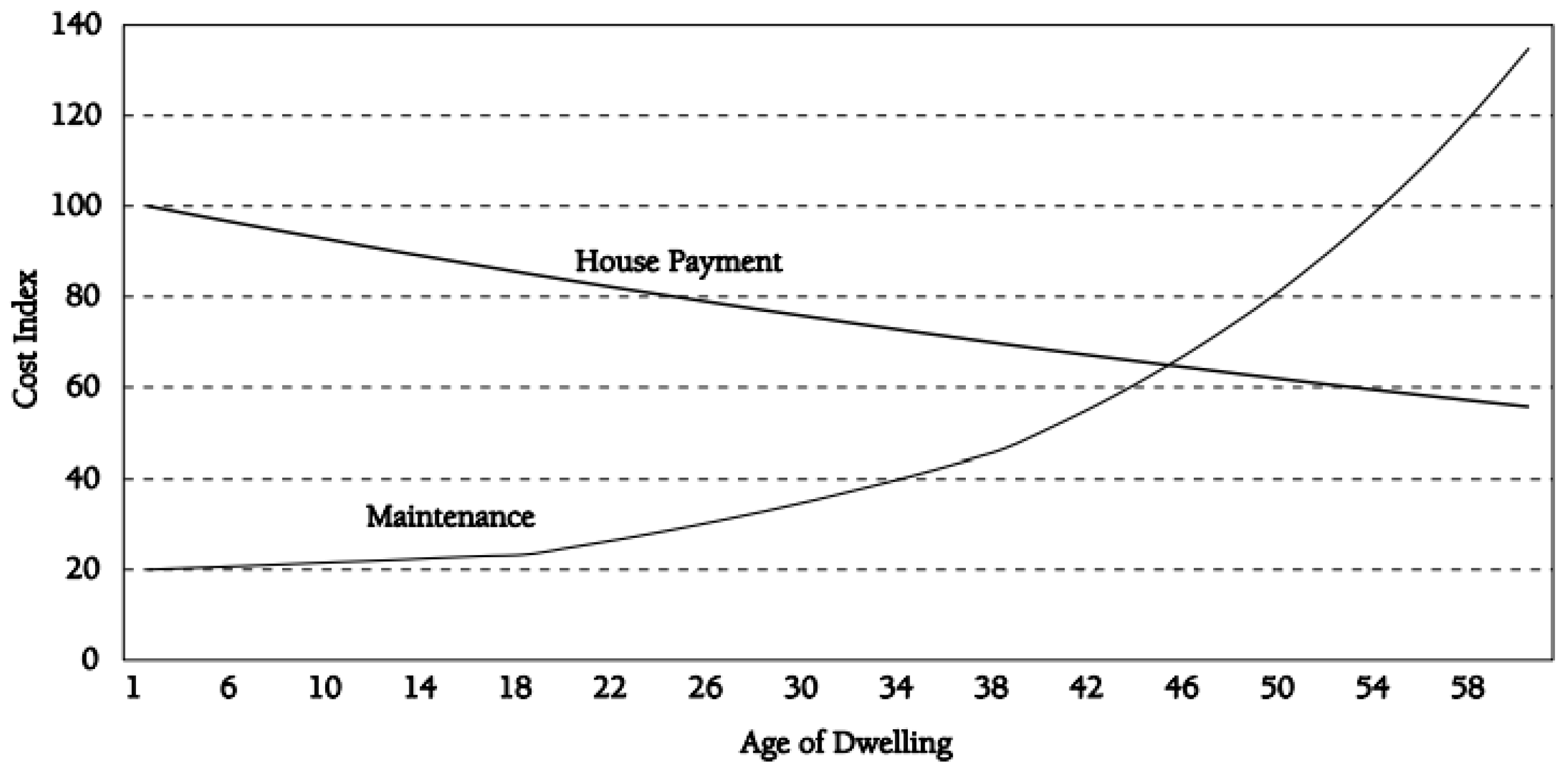

22] have become major pressure factors in the budgets of the maintenance and operation of homes for Saudi families. One of the most important criteria that has resulted in the emergence of many of the aforementioned problems is that Saudi families usually do not pay attention to O&M issues (the process of harmonizing the diversity and complexity of engineering systems in homes, the maintenance costs that gradually increase with time, limited allocated budgets, and high aspirations and expectations of users) when considering the financial costs of a home including the design and construction costs [

23,

24] as shown in

Figure 2. This has led many homeowners to face endless O&M problems, thereby preventing them from achieving their goals. As noted by [

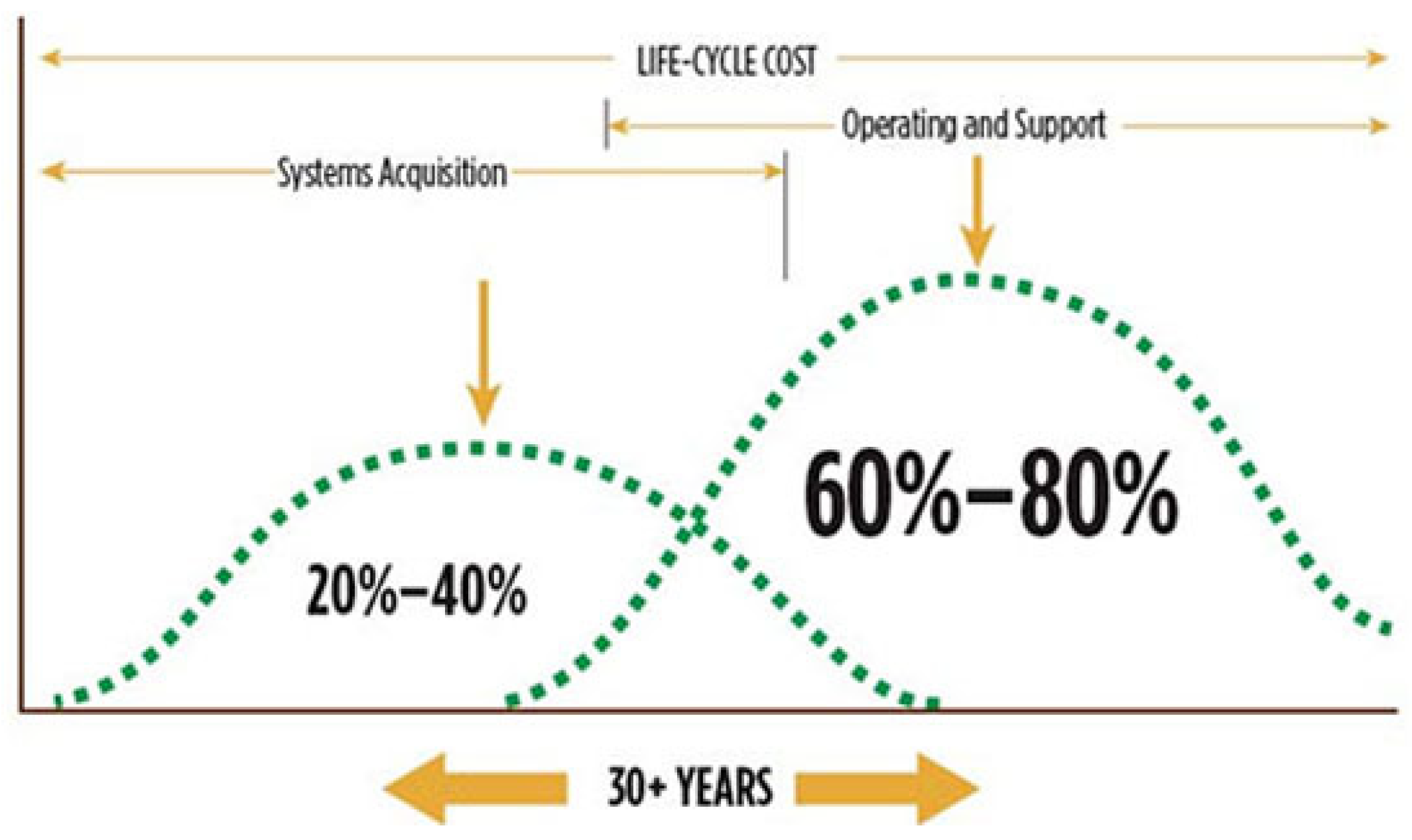

23], typically 60–80% of the total cost is spent on the O&M phases, as shown in

Figure 3.

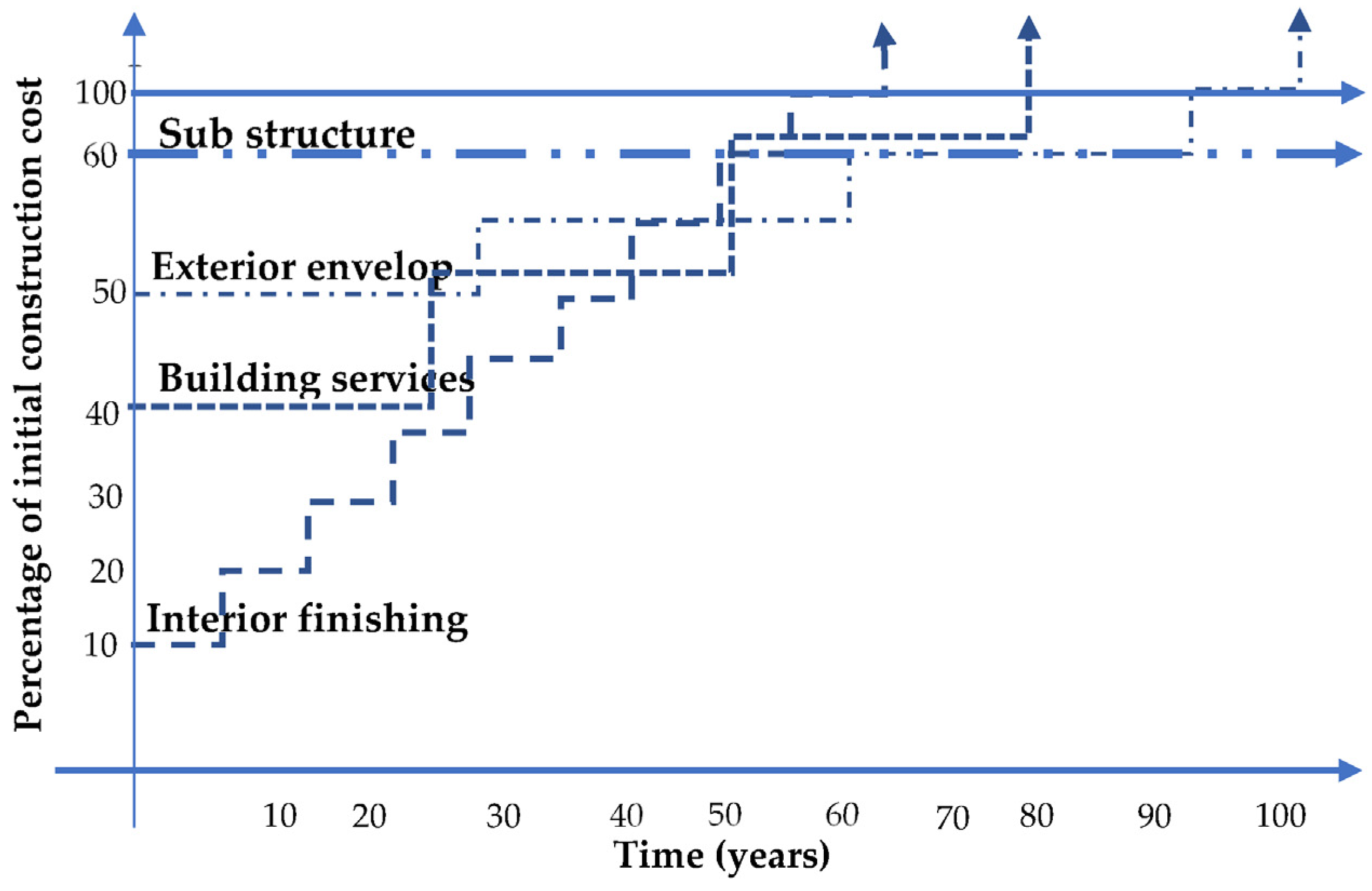

From

Figure 4, we note that the interior finishing system is renewed every seven years according to the study; thus, the total cost of renewing this system is approximately 10% of the initial cost. Construction services must be replaced every 27 years, which may account for up to 20% of the initial costs. In addition, the outer shell costs 10% of the initial construction costs after 32 years. In the event that the structure is implemented according to the codes, no additional changes occur; therefore, there are no additional costs if maintenance is performed periodically for previous works.

6. Methodology

This study employed a mixed-methods approach, utilizing both quantitative and qualitative data collection and analysis techniques.

Quantitative Data Collection

A survey was administered to a sample of building developers, architects, and citizens to gather data on the costs associated with adhering to the SBC. The survey instrument included questions on the following topics:

Quantitative Data Analysis

The survey data were analyzed to determine the average cost increase for building developers, architects, and citizens. Descriptive statistics such as means, medians, and standard deviations were calculated for each cost category.

Qualitative Data Collection

Interviews were conducted with experts in the construction industry such as architects and engineers to gather their perspectives on the impact of the SBC. The interview guide included questions on the following topics:

The overall impact of SBC on construction costs;

The specific impact of SBC on different types of construction projects;

The potential for energy efficiency savings to offset the increased costs of adhering to the SBC.

Qualitative Data Analysis

The interview data were analyzed using thematic analysis. Themes were identified by coding the interview transcripts for key phrases and concepts. The themes were then analyzed to identify patterns and insights.

Case Study

A case study was conducted considering a residential villa in the city of Riyadh with a land area of 320 m2. The villa was designed to meet the requirements of the SBC. The project costs were tracked to determine the impact of the SBC on the overall cost of the project.

Findings

The quantitative data analysis revealed that the average cost increase for building developers, architects, and citizens was 18%. The qualitative data analysis revealed that the experts believe that the SBC will have a positive impact on the construction industry in the long run, as it will lead to the construction of more energy-efficient buildings. The case study found that the cost of adhering to the SBC was 2% of the overall project cost.

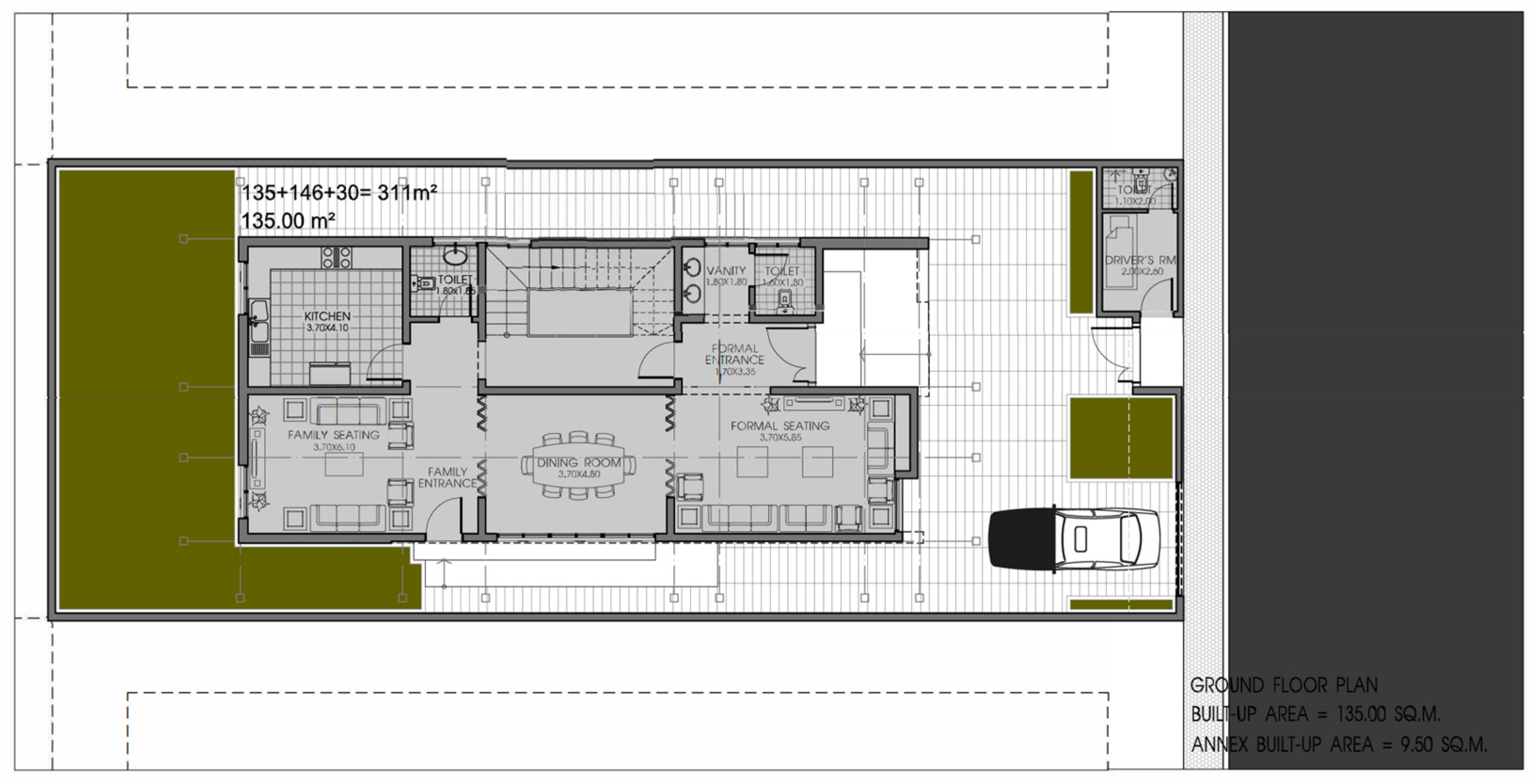

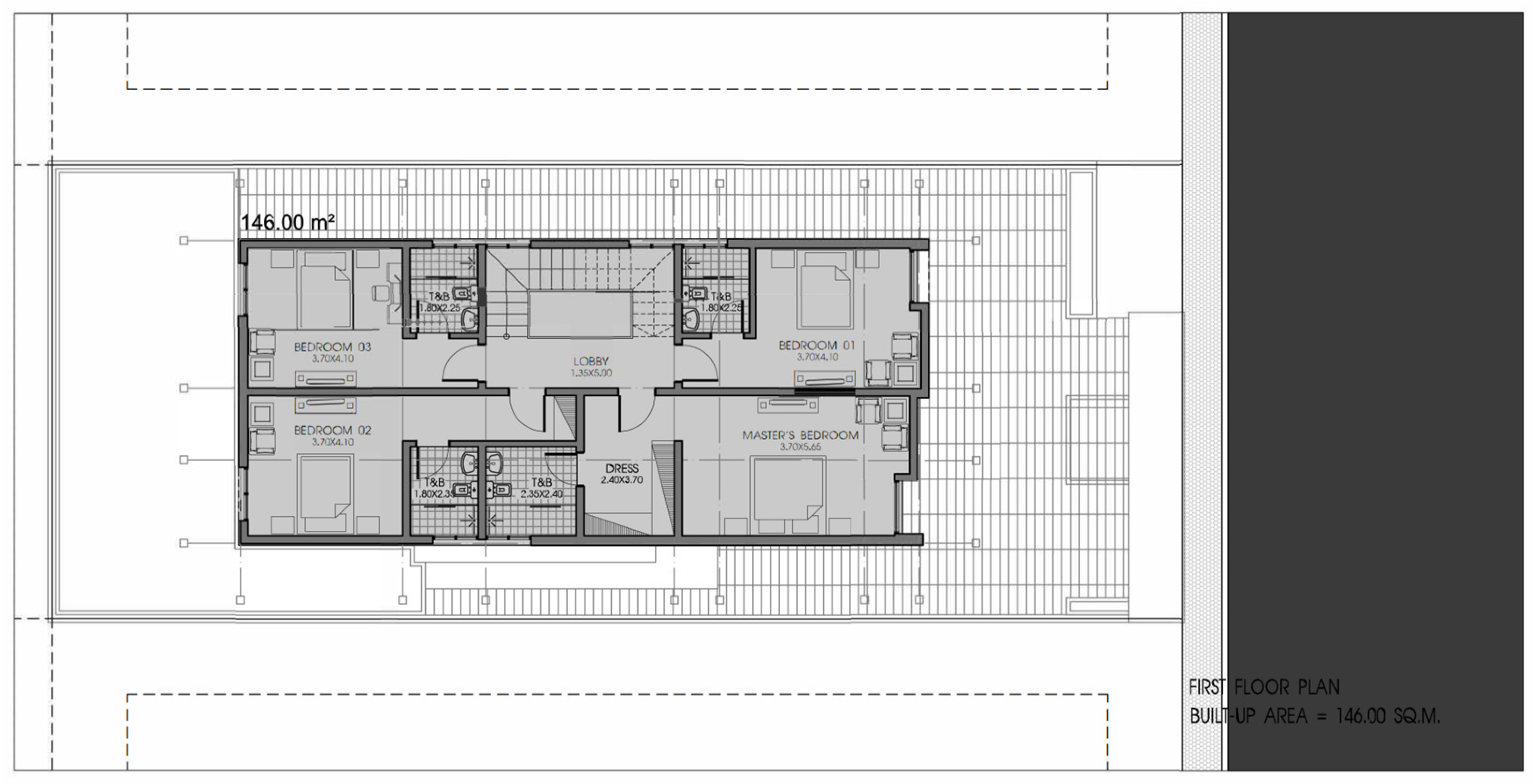

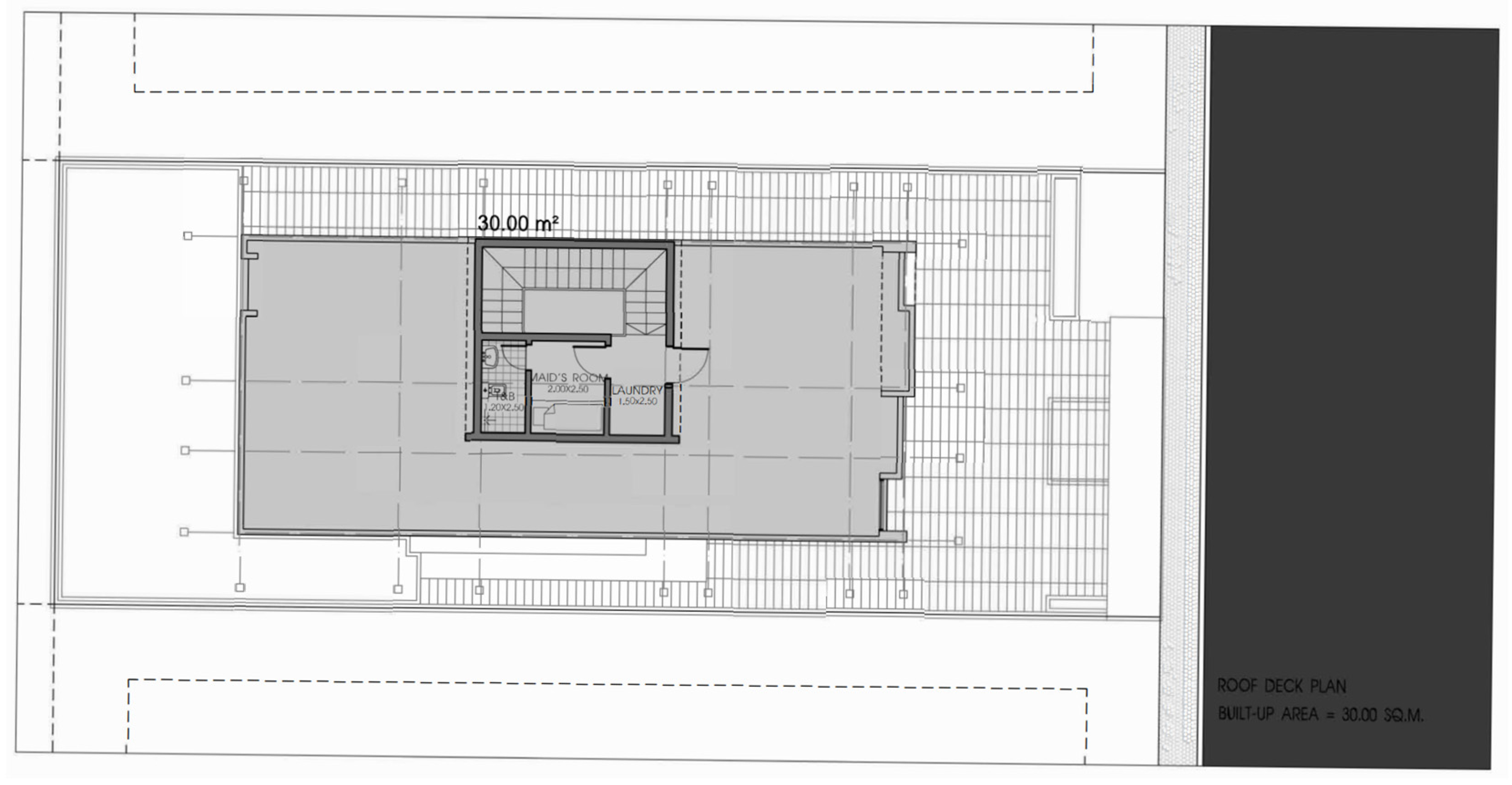

7. Case Study

A case study was conducted considering a residential villa in the city of Riyadh with a land area of 320 m

2 due to its suitability in terms of cost for the largest sector of Saudi families who wish to own suitable housing units. The majority of plots of land offered for trading in the market approximated the model proposed for the survey (

Figure 5,

Figure 6,

Figure 7,

Figure 8,

Figure 9 and

Figure 10), which was developed by the National Center for Building and Construction in King Abdulaziz City for Science and Technology. The ground floor, first floor, and annex areas were 218, 205, and 100 m

2, respectively.

7.1. Estimating the Primary and Secondary Costs of the Two Study Cases

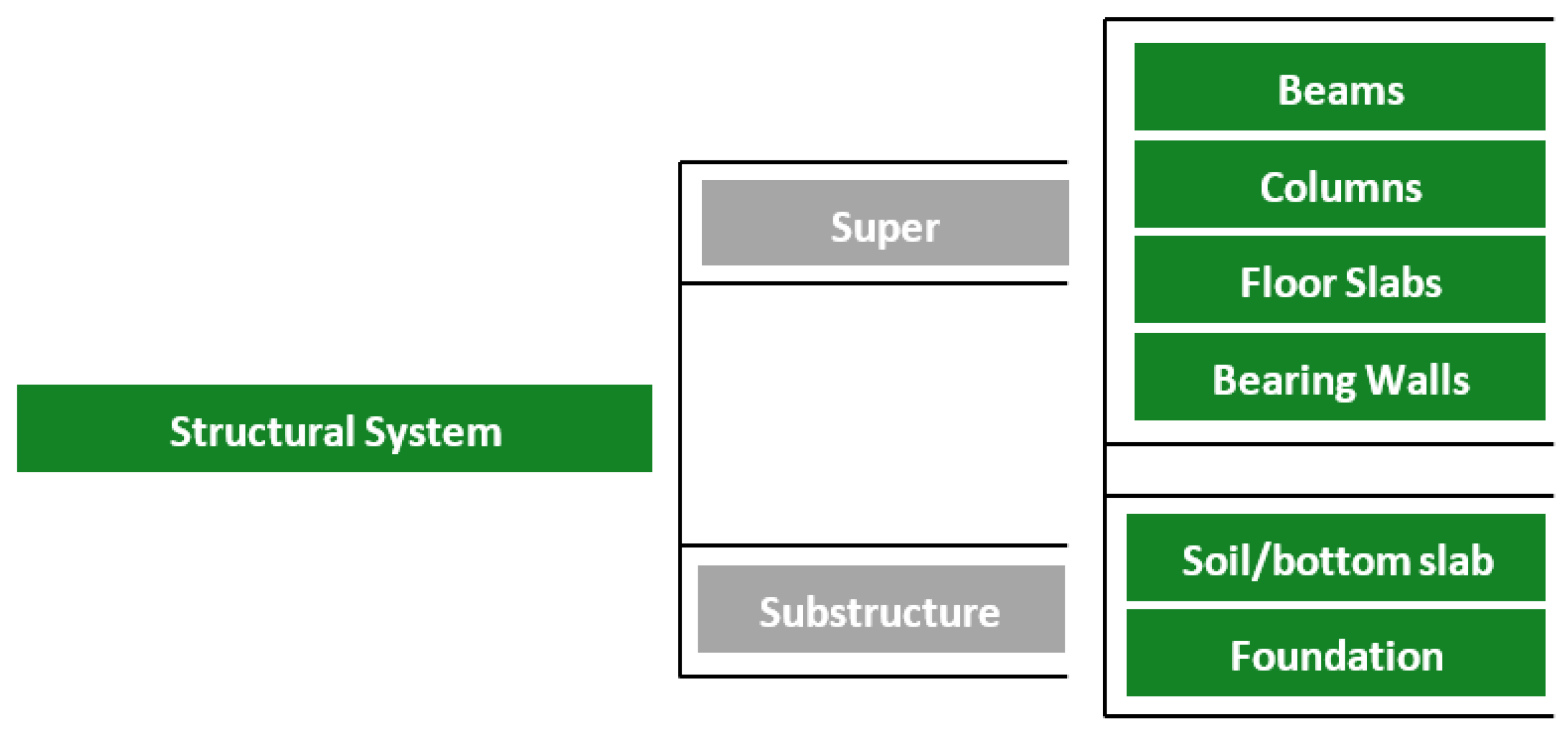

In the framework of cost estimation for the case study, we used the Standard Uniform Costing System, which is a model for cost estimates developed by specialized organizations in the United States of America, who referred to it as the Uniformat model for the purpose of preparing a budget for the project. To estimate the cost of implementation, this system divides the components of the project into 12 main sections based on the functional area. This distinguishes the system from other systems such as the Construction Specifications Institute (CSI), referred to as the Master Format, which is suitable for the implementation and late stages of design.

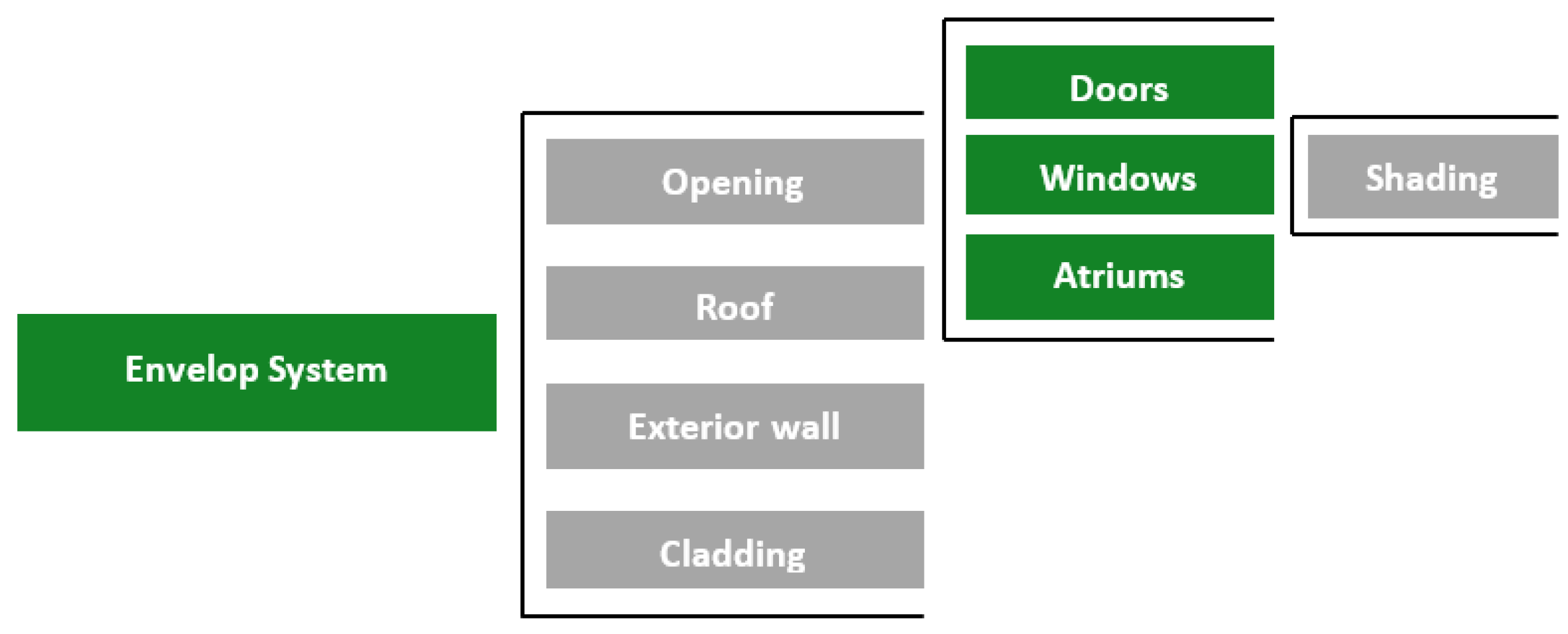

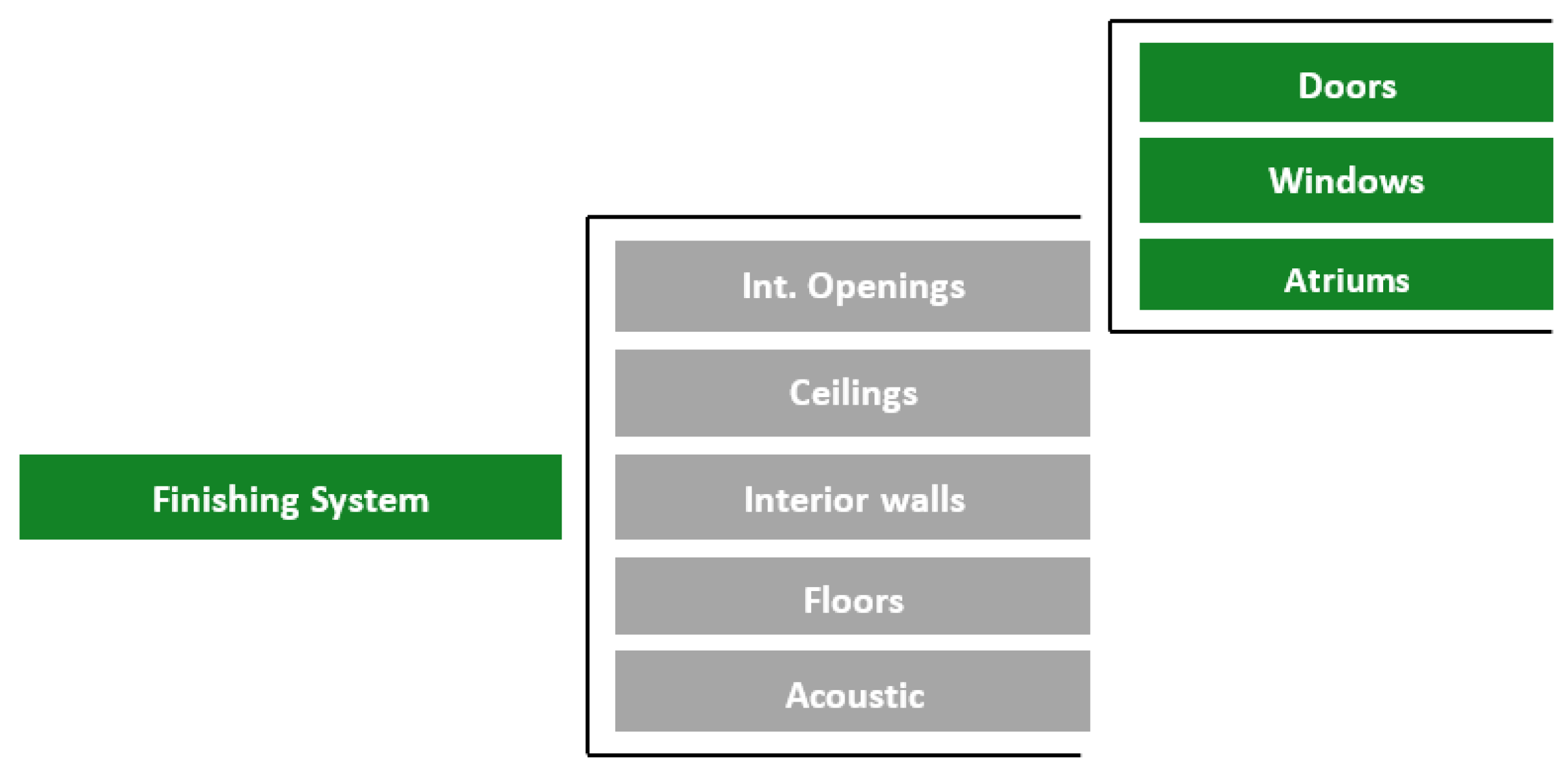

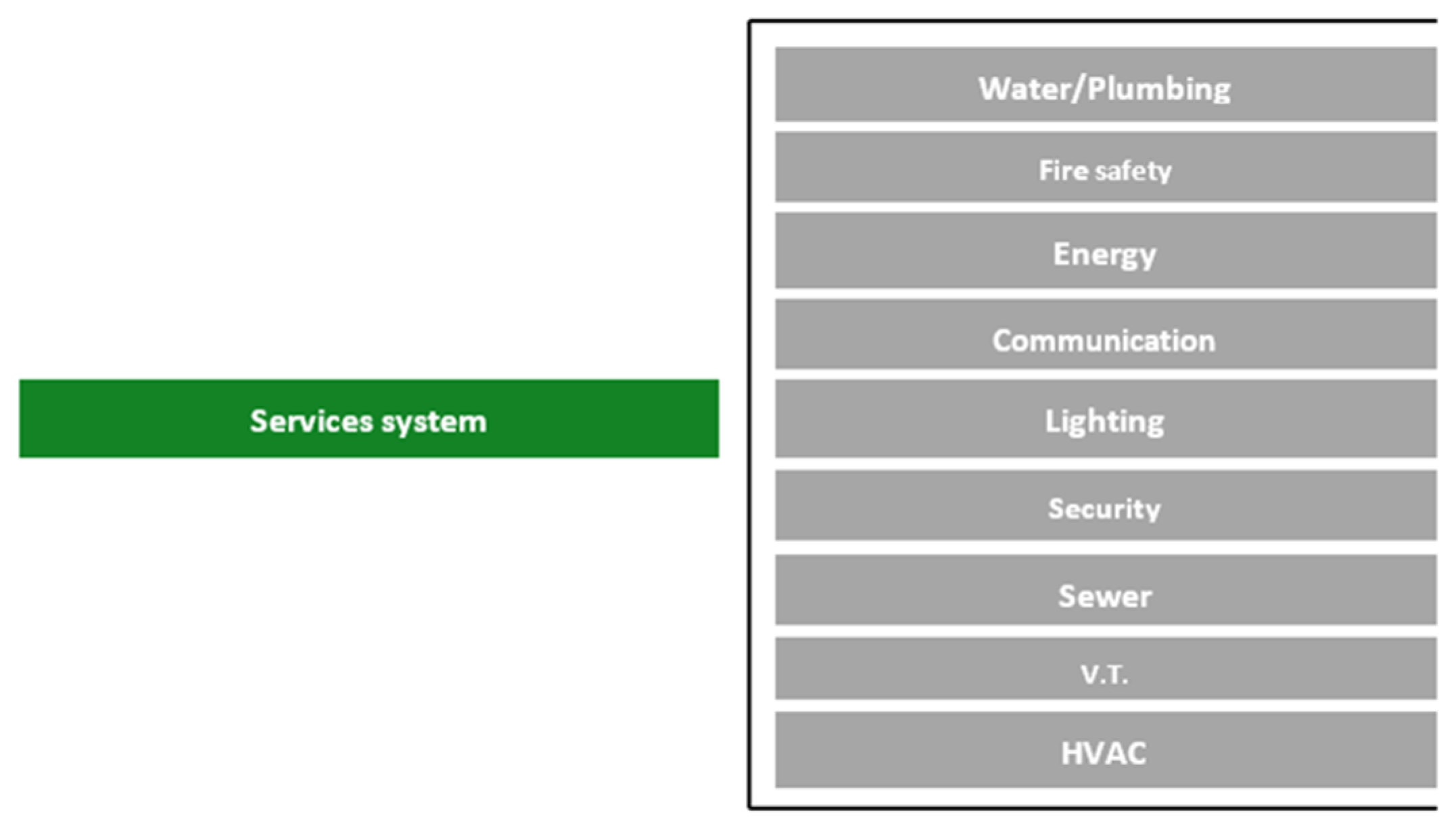

There is a second version of the System Costing Uniform Standard, referred to as the ASTM Uniformat II Classification for Buildings [

27], which divides the cost of any building into seven main groups in the first level (A–G), groups of elements in the second level, and independent elements in the third level (

Figure 11,

Figure 12,

Figure 13 and

Figure 14).

The cost can be summarized in the systems according to the details presented in

Table 1.

The costs can also be calculated by linking them to those associated with fulfilling the required requirements and the accompanying administrative and legal requirements to achieve the code.

Architectural terms and requirements refer to architectural works, building types, and building construction systems including special detailed requirements based on the use and occupancy, areas and heights of buildings (interior finishes; internal environment; external walls; rooftop construction panels of glass, gypsum, and plaster; plastics; elastomers), and additional accessibility requirements. Moreover, these are designed against rodents.

Structural conditions and requirements are related to analysis, structural design, and necessary examinations. These involve structural tests and checks of the soil, foundations, and retaining walls. Furthermore, safety requirements during construction using concrete structures, masonry bricks, and steel structures are considered.

Electrical terms and requirements are those pertaining to the design, construction, installation, operation, maintenance, and safety of building systems, devices, and electrical installations. Electrical installations and internal and external lighting include control panels, grounding systems, fire alarms, lightning-protection systems, and elevators.

Mechanical terms and requirements are those related to the design, construction, installation, operation, maintenance, and safety of systems, devices, and mechanical extensions of buildings including ventilation and expulsion. Furthermore, cooling and heating, extension of ventilation, water heaters and boilers, solar energy systems, elevators and maintenance conditions, requirements for energy conservation, and water saving are important aspects.

Health conditions and requirements are those related to the design, construction, installation, maintenance, and safety of systems, devices, and sanitary installations in buildings including water supply, sewage, rainwater drainage, fire-extinguishing water, and gray water reuse systems.

Gas terms and requirements include gas installations.

Fire protection requirements are those related to the design, construction, installation, maintenance, and safety of fire protection systems including fire protection systems. Furthermore, ways to escape, design for fire protection, and the fragmentation and separation of fire areas are other important aspects.

7.2. Calculating Costs and Comparing the Two Case Studies

7.2.1. Calculation of Pre-Construction Costs

The work required is assigned to an engineering office approved by the owner, who communicates with the insurance company, which informs them of the basic requirements. Consequently, the owner must submit approved and code-compliant designs and prepare the structural and mechanical design, based on which the building permit is issued and the contractor is awarded the contract, as shown in

Table 2.

Soil must be examined for every 300 m2 of the building area including at the corners. The cost ranges from SAR 3000 to 5000.

The cost of conducting studies and preparing designs to satisfy the needs and requests of the owner in accordance with the SBC were estimated at SAR 30,000, according to opinion polls and market studies.

The cost of preparing survey drawings through a classified survey engineering office is estimated to be SAR 1500.

Next is the supervision costs incurred by a classified supervising engineering office, which was assigned by the owner to conduct supervision work. This includes 11–15 visits. The cost of each visit ranges from SAR 500 to 1500; the total cost of supervision ranges between SAR 15,000 and 22,500. By monitoring and following the market, this amount may double to SAR 45,000 due to the additional supervision process as a result of applying the code and its consequences in terms of fines and financial benefits.

Structural insurance amounts to 1–1.5% of the building construction costs (Malaath Company, Riyadh, Saudi Arabia)

The municipality fees for obtaining a building permit is SAR 4 per m2. Thus, the cost of issuing a license is SAR 2092 (SAR 4 × 523 m2 = SAR 2092).

7.2.2. Calculation of Construction Phase Costs

As

Table 3 and

Table 4 shown, the initial cost of the project (direct and indirect costs) includes the costs of the structure, building materials, fixtures, and subsequent finishes as well as the costs of the mechanical, sanitary, and electrical work.

The structural cost of SAR 650 per m2 of the case study area was estimated at 533 m2 (523 m2 for building, and 10 m2 for the guard’s room).

Next was the cost of the structure and finishing of the walls of the residential villa (48 m) at a price of SAR 1100 per m2.

The structural cost of the underground water tank (18 m2) was SAR 1300 per m2.

The cost of finishing the building at a rate of SAR 1150 per m2 was estimated for 533 m2 of the study area.

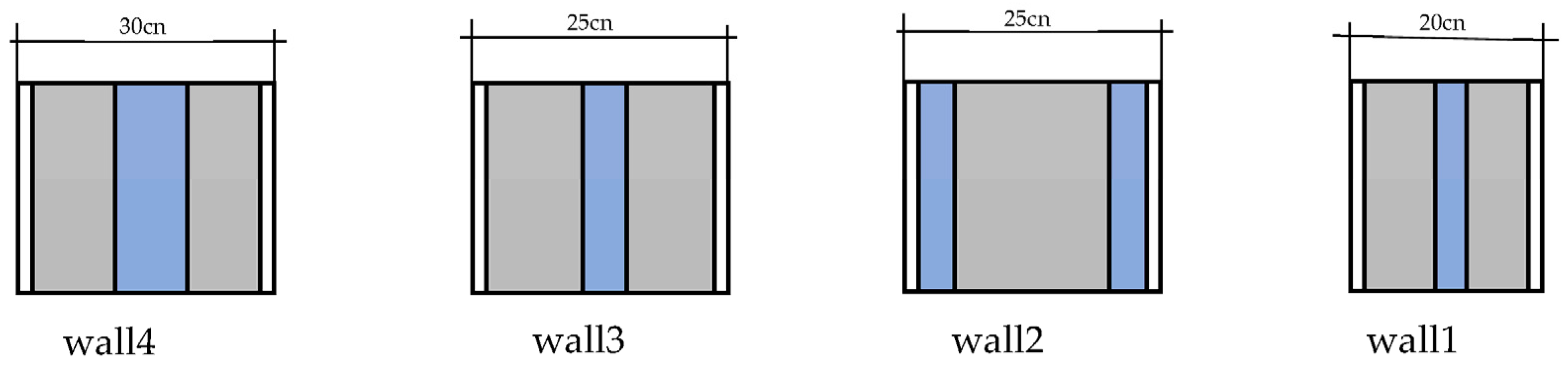

Finally, as

Figure 15 shown that the total costs of thermal insulation for the external perimeter and roof of the residential villa were considered. The thickness of the thermal insulation was determined based on the value of the thermal transfer coefficient according to the SBC for residential buildings (SBC1102) by measuring several wall thicknesses of various materials using Ansys Multiphysics 19.2 and Comsol Multiphysics 5.5. The results are presented in

Table 5. Only Wall No. 3 cement block was chosen (this is the most suitable locally according to the market and field surveys) with 5 cm-thick thermal insulation (25 cm thick). Regarding the case study that did not apply the code, the walls were determined to be 20 cm thick and insulated according to the market and field surveys (Wall No. 1–Table No. 5).

7.2.3. Calculating Post-Construction Costs

According to [

23], the post-construction stage, which includes the operating and maintenance costs, represents more than 60% of the total costs due to the duration of this stage and its significance during the life cycle of the structure. This was SAR 1,067,733.15 for the first study case, which did not apply the code, while it was estimated as SAR 1,263,753.15 for the study case that applied the SBC (an increase of SAR 196,020.00). Furthermore, considering the savings in constructing the residential building according to the correct principles, the benefits of using the SBC would be in choosing building materials in the right quantities, the ease of maintenance of the building, electricity and water consumption as a result of thermal insulation, and the use of good materials in electric and plumbing systems. In addition, the state has been keen to reassure citizens in terms of two primary factors: monitoring the executive authorities or suppliers of building materials to eliminate monopolistic practices and the application of value engineering to provide alternatives to materials and technologies capable of reducing the costs and raising the quality.

8. Results and Analysis

In this study, the LCC was used to calculate the total costs during the life cycle of the building from the design to disposal of the housing unit. The LCC steps include stages A0–C4 (pre-construction costs, maintenance, replacement, operation, and end-of-life costs). The LCC was conducted using the building economics equations, which cover the analysis of the costs involved in the life of a building, from pre-construction to end-of-life. The LCC phases are listed in

Table 6.

The initial investment costs for building materials and fixtures were estimated from the local supplier, whereas other costs specific to the building such as land purchases, municipality licenses, taxes, and insurance companies were estimated according to the current market prices. In the estimated combined stages (A0–A5), the construction stage included investment-related costs comprising unit A0 showing the pre-construction costs for land purchase, municipal permits, and taxes; the A1–A3 modules include the costs of building materials and fixtures as well as their transfer to the manufacturer and the packaging and distribution process. The costs incurred during the construction process at the building site (A4, A5) include labor costs, energy costs for site work, transportation costs to the building site (indirectly included as a lump sum), the cost of equipment used during the installation process, and wastage costs. The utilization phase comprises the operating costs during the occupation of the building including the cost of replacements, energy, and water. Maintenance costs are presented as a lump sum based on the average costs in Saudi Arabia and are included in modules B1–B3. The projected replacement rates based on Saudi best practices and default data for building materials and fixtures were included in the calculations within the bulk module (B4, B5). The operational costs during building occupancy included the electricity (B6) and water (B7) costs. Based on the cost calculations for climate, building physics, occupancy, and energy systems, the end-of-life costs (C1–C4) were calculated as 2.5% of the capital costs based on the hypothetical data. This stage included the combined calculated costs. Costs represent the energy consumed and waste generated during the demolition and disposal of building materials in landfills.

To calculate the LCC, the present value (PV) formula was used to discount future cash flows to present values:

PV = Present value;

t = Time in unit of year;

Ft = Future cash amount that occur in year t;

d = Discount rate used for discounting future cash amounts to the present value.

To calculate all costs that arise during the life of the building, the present value equation was applied. The general LCC formula for buildings was used to summarize all costs from cradle to grave, as follows:

Repl = Replacement costs;

E = Operational energy costs;

W = Operational water costs;

EOL = End-of-life costs.

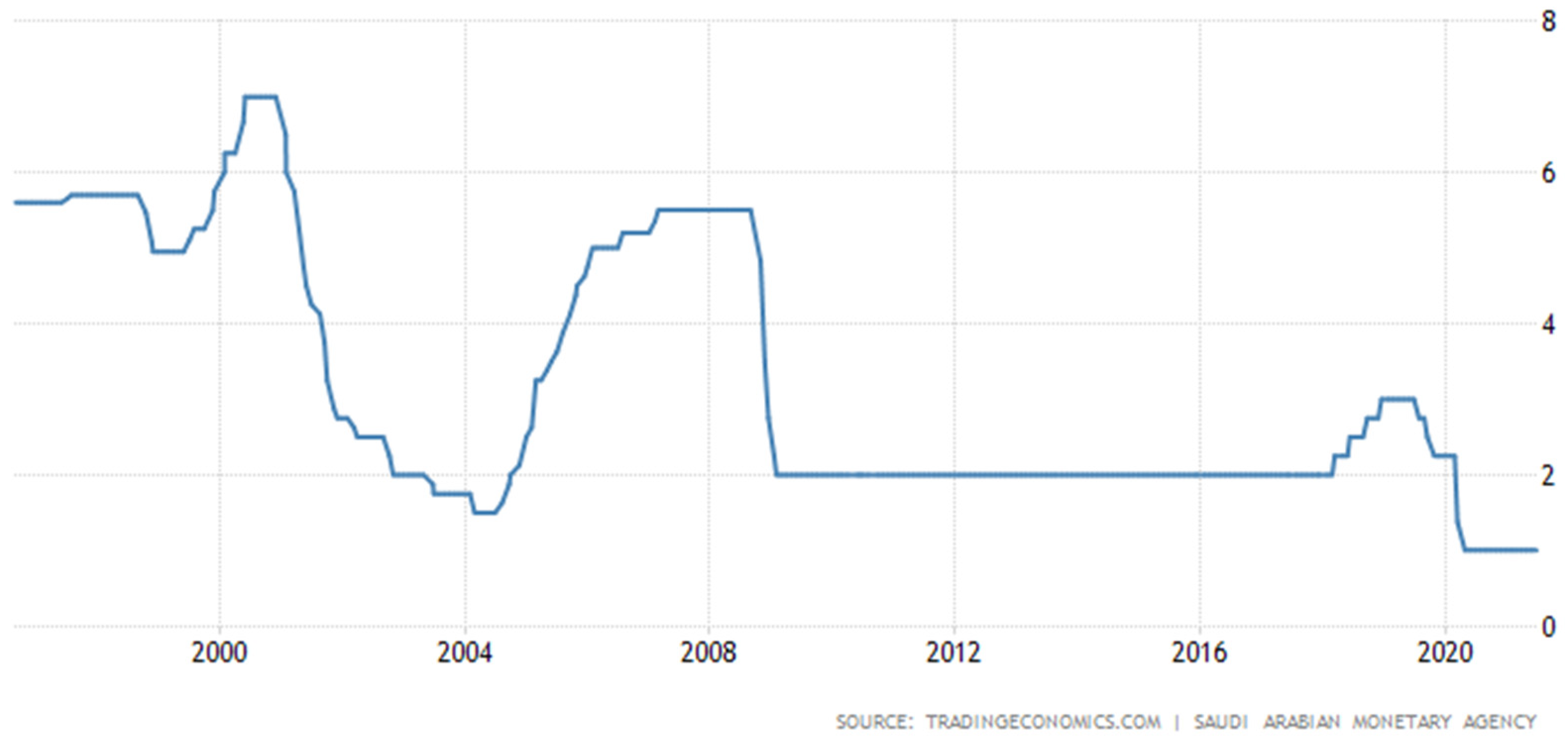

Figure 16 explains that the discount rate is based on the average historical data from 2002 to 2019 provided by the Central Bank of Saudi Arabia, with a nominal discount rate of 3.25%. However, according to trading economics and analyst forecasts, the discount rate in Saudi Arabia is expected to reach 1.00% by the end of the quarter. In the future, we estimate that the interest rate in Saudi Arabia will stand at 1.00 within 12 months. In the long-term, the interest rate in Saudi Arabia is expected to trend at approximately 1.00% by 2022, according to our econometric models. Therefore, a 2% discount rate was adopted as the average discount rate.

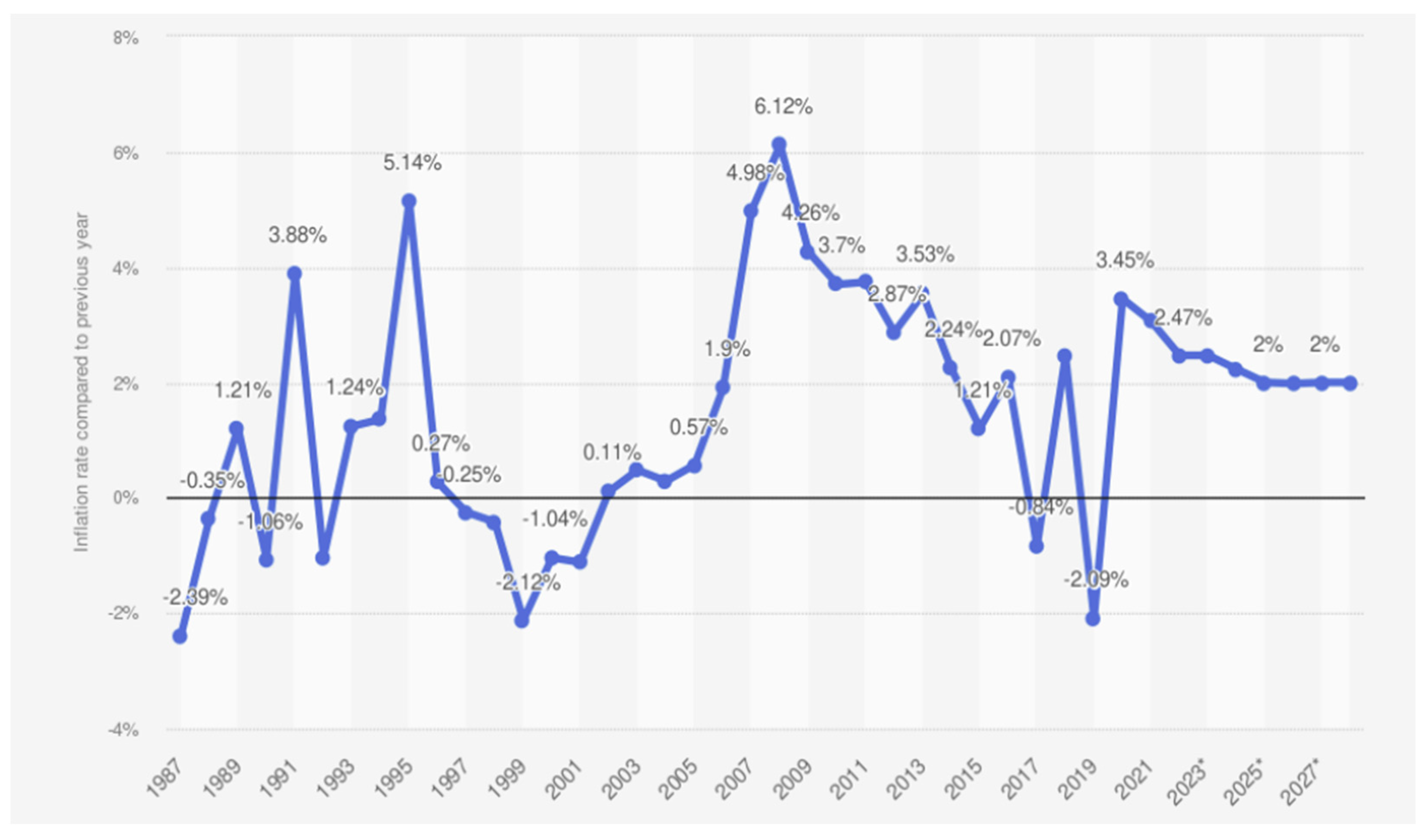

Another important economic factor considered in this study was the inflation rate. According to the Saudi Arabian Monetary Agency, the average inflation rate is 6.2%, and is expected to decline to 2.10% in 12 months. In the long-term, the inflation rate in Saudi Arabia is expected to trend at 2.00% by 2022 as shown in

Figure 17.

Study Hypotheses

This study was built on a set of hypotheses based on indicators and related research studies, which are summarized in

Table 7 and

Table 8.

Statistics show the inflation rate in the Kingdom of Saudi Arabia from 1986 to 2021, with projections up to 2026. In 2020, the average inflation rate was 3.44%, whereas the inflation rate in Saudi Arabia is expected to reach approximately 2.00% by 2022. [

29]

The depreciation tax was estimated at 5%, according to the Saudi tax law imposed on the five categories of capital assets including fixed buildings (Reference No. [

21], p. 188).

In Saudi Arabia, interest rate decisions are made by the Saudi Monetary Agency (SAMA). The central bank’s official interest rate is its official repo rate (ORR). It set an interest rate of 1% in 2020.

In 2018, residential tariffs were amended and applied to only two categories of consumption instead of four categories in 2016. Thus the tariff for residents who consume less than 4000 kWh was estimated at 0.18 SAR/kWh, whereas that for users who consume more than 6000 kWh was estimated at 0.30 SAR/kWh.

The consumption tariff for drinking water in the Kingdom of Saudi Arabia was estimated at 6 SAR/m3 per month, and the consumption tariff for waste was estimated at 3 SAR/m3 per month.

9. Discussion

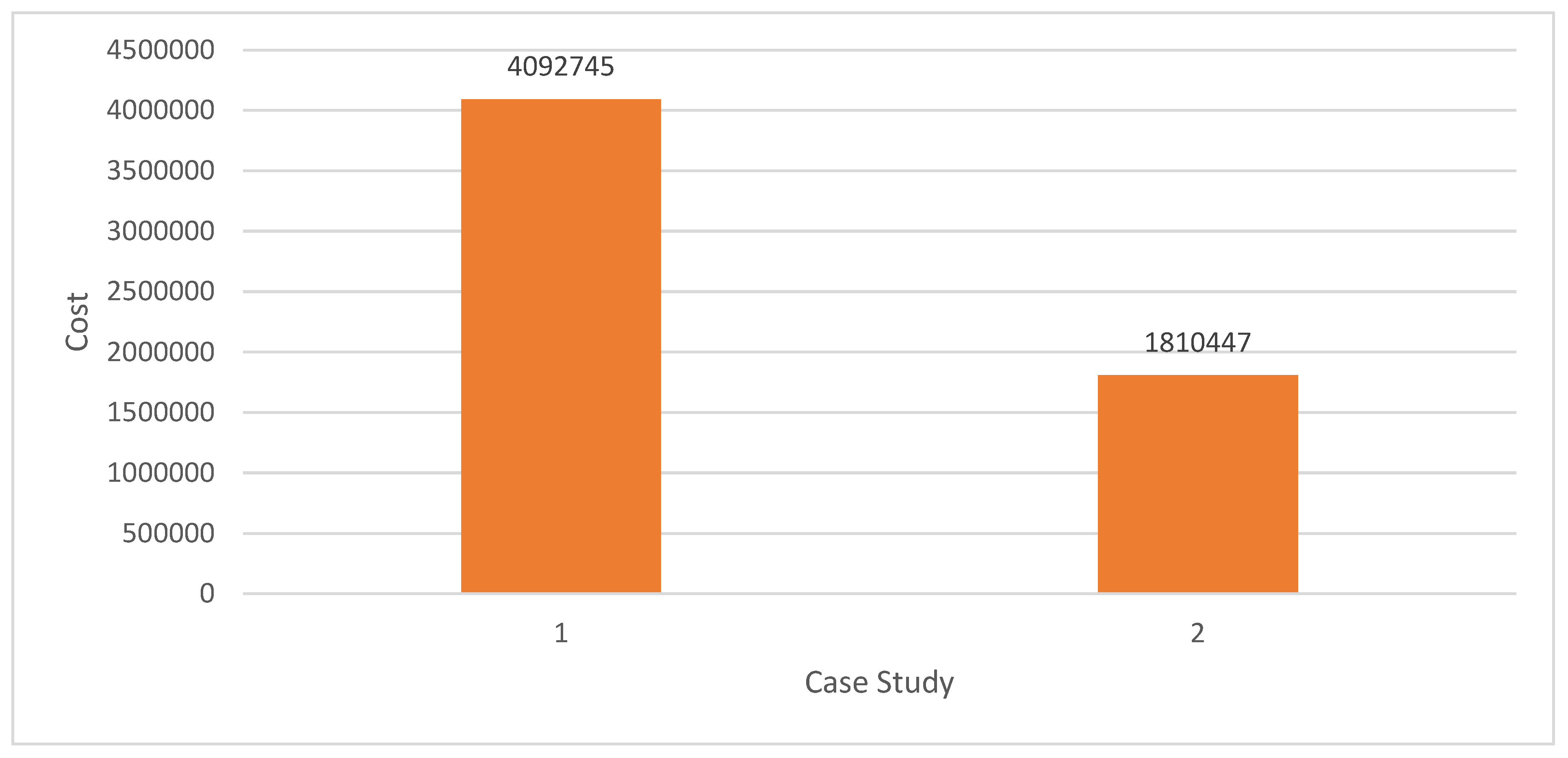

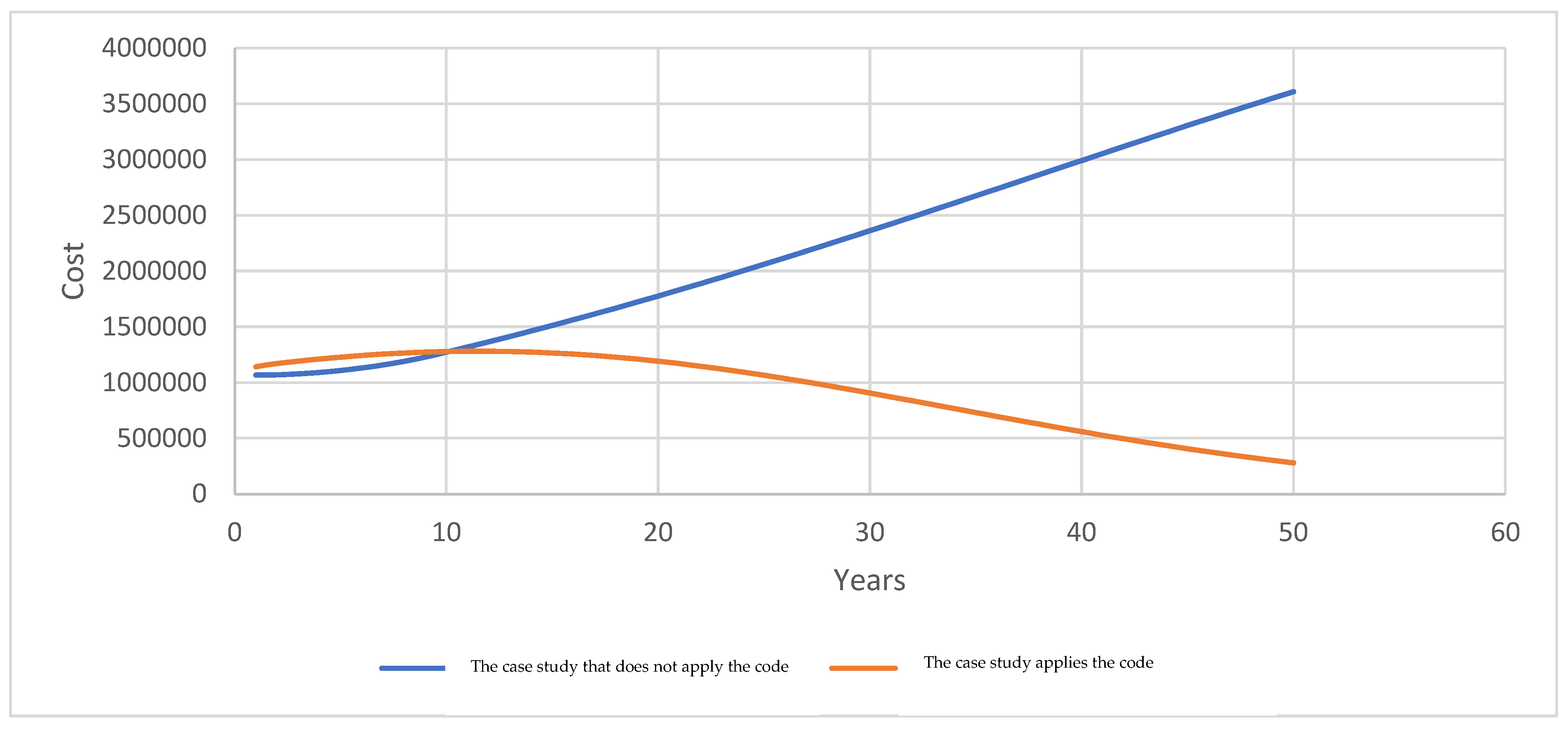

This study found that the SBC plays a significant role in maintaining operating costs. By comparing the two cases, as shown in

Figure 18, it was found that there was a difference in the costs of approximately SAR 2,282,298 between the two study cases in favor of the housing unit that applied the SBC, which was 44% less than the case wherein the code was not applied. By reducing heat transfer through building components (particularly walls, ceilings, and windows) and its external elements, from the inside to the outside, to achieve the “U-value”, the energy efficiency of the building material increased. In particular, many studies have shown that the application of thermal insulation in buildings contributes to reducing the electrical energy consumed in air conditioning and heating devices by 30–40%, and the use of double and heat-reflecting glass reduces the electricity consumption of air conditioners by up to 5%. The use of light exterior colors in a building also helps reduce heat absorption (heat gain).

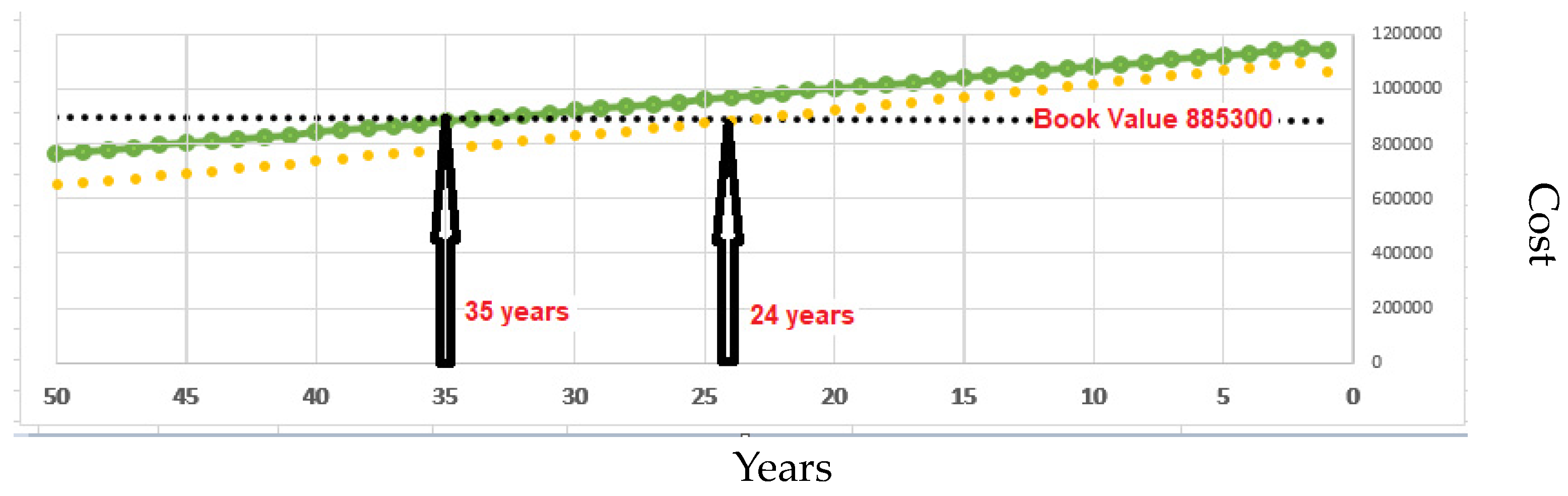

The study concluded that the book value of a building that applied the code, which was estimated at SAR 764,838 at the end of the hypothetical building life cycle after 50 years, increased by SAR 115,344 over the book value of a building that did not apply the code, which was estimated at SAR 649,495 at the end of the hypothetical building life cycle. This implies that the decrement value of a building that applies the code is significantly slower than that of a building that does not apply the code.

By evaluating the two study cases at a book value of SAR 885,300, as shown in

Figure 19, the building that applied the code reached this value after (considering both the accumulated value of O&M and the cumulative rate of depreciation for the building) 35 years compared to 24 years for the building that did not apply the code. Thus, the application of the code provides an equivalent of 11 years in the life cycle of the building; in a clearer sense, it extends the life of the building by more than a decade (11 years).

In

Figure 20 explained most of the repairs related to plumbing and electricity work were high because of poor implementation and non-compliance with specifications and standards that guarantee their validity; this also requires radical reforms at a high cost that certain families are unable to afford. Thus, they resort to temporary repairs, particularly with the scarcity of skilled technical workers. Reforms in non-major cities is guaranteed by the code, particularly in terms of plumbing and electrical work.

While [

6] found that implementation of the SBC increased the construction costs, with the average cost increase for building developers being 5.8%, the study found that a reduction of 44% of the housing unit that applied the SBC was achieved, which outweighs the increased construction costs and is even higher than what has been claimed by [

30] by 22%. The study also supports the finding of [

8], with an average reduction of 15% in energy consumption due to compliance with building codes. Additionally, the paper supports the findings of [

11], who emphasized the role of thermal insulation in reducing the energy consumption and carbon footprint, with potential savings of up to 30–40% in air conditioning and heating devices that could be achieved wherein the code was applied, and [

12], who emphasized the importance of building insulation and airtightness in achieving energy savings. Overall, the study synergies papers that support the idea that building codes can have positive impacts on energy efficiency and housing affordability in Saudi Arabia [

5,

31,

32,

33].

10. Conclusions

The implementation of building codes in the Kingdom of Saudi Arabia such as the SBC can significantly impact the construction industry and economy. The studies reviewed in this literature review have shown that the implementation of building codes can result in an increase in the cost of construction but can also have a positive impact on the economy, energy efficiency, and housing affordability.

The aim of providing housing projects to beneficiaries is to enable them to save on housing costs, use the available funds to develop their families, and improve their economic conditions from one level to another. However, this study showed that the percentage of Saudi families spending, on average, out of their monthly income, exceeded the average international standard by a large percentage, whereas their level of quality was much lower than that of their peers. In the event that the SBC is applied, it will save Saudi families money amounting to not less than 40% of the total cost of the building due to the following reasons:

Maintaining a good operating condition of the facility;

Extending the life of the facility and its existing systems;

Savings in operational cost;

Obtaining high levels of performance and better productivity;

Maintaining the safety of the facility and its employees.

The SBC also ensures that O&M work is conducted in accordance with international standards of best practices to ensure the efficiency of tunnels and the level of quality of life for Saudi families.

These studies also provide valuable insights for policymakers and stakeholders in the construction industry when considering the implementation and enforcement of building codes in the Kingdom of Saudi Arabia.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}