Evaluation of Digital Banking Implementation Indicators and Models in the Context of Industry 4.0: A Fuzzy Group MCDM Approach

,

,  ,

,  ,

,  and

and

Abstract

:1. Introduction

- Development of a best–worst multi-criteria decision-making method based on an α-cut analysis and TFNs to obtain the importance of the DB implementation criteria and prioritization of DB trends in an uncertain environment.

- Providing a decision-support framework in a trapezoidal fuzzy environment in order to deal with ambiguity in information, lack of information, insufficient knowledge and doubt in the preferences of decision-makers.

- Providing a fuzzy multi-criteria group decision-making approach that can be used by a group of experts and lead to more reliable results.

- Identifying and ranking the criteria and sub-criteria for DB implementation according to emerging trends and technological advances affected by Industry 4.0, service quality theory, a DB literature review, and experts’ opinions.

- Prioritization of omni-channel, cognitive, social, blockchain, and open DB trends according to the importance of the DB implementation criteria.

2. Literature Review

2.1. Theoretical Background

- Interaction perspective: Service quality is a sign of the inherent excellence of services and the fulfillment of high-level standards in providing services. This view is often used in performing and visual arts. It is argued that people perceive quality only through repeated experience.

- User-centered view: This view is based on the hypothesis that the quality of a service depends on the user’s opinion about it. This definition considers the level of service quality to be equivalent to the level of user satisfaction. This mental perspective and demand-oriented perspective specifies that every customer has different and unique demands and needs.

2.2. Survey of Service Quality and Digital Banking

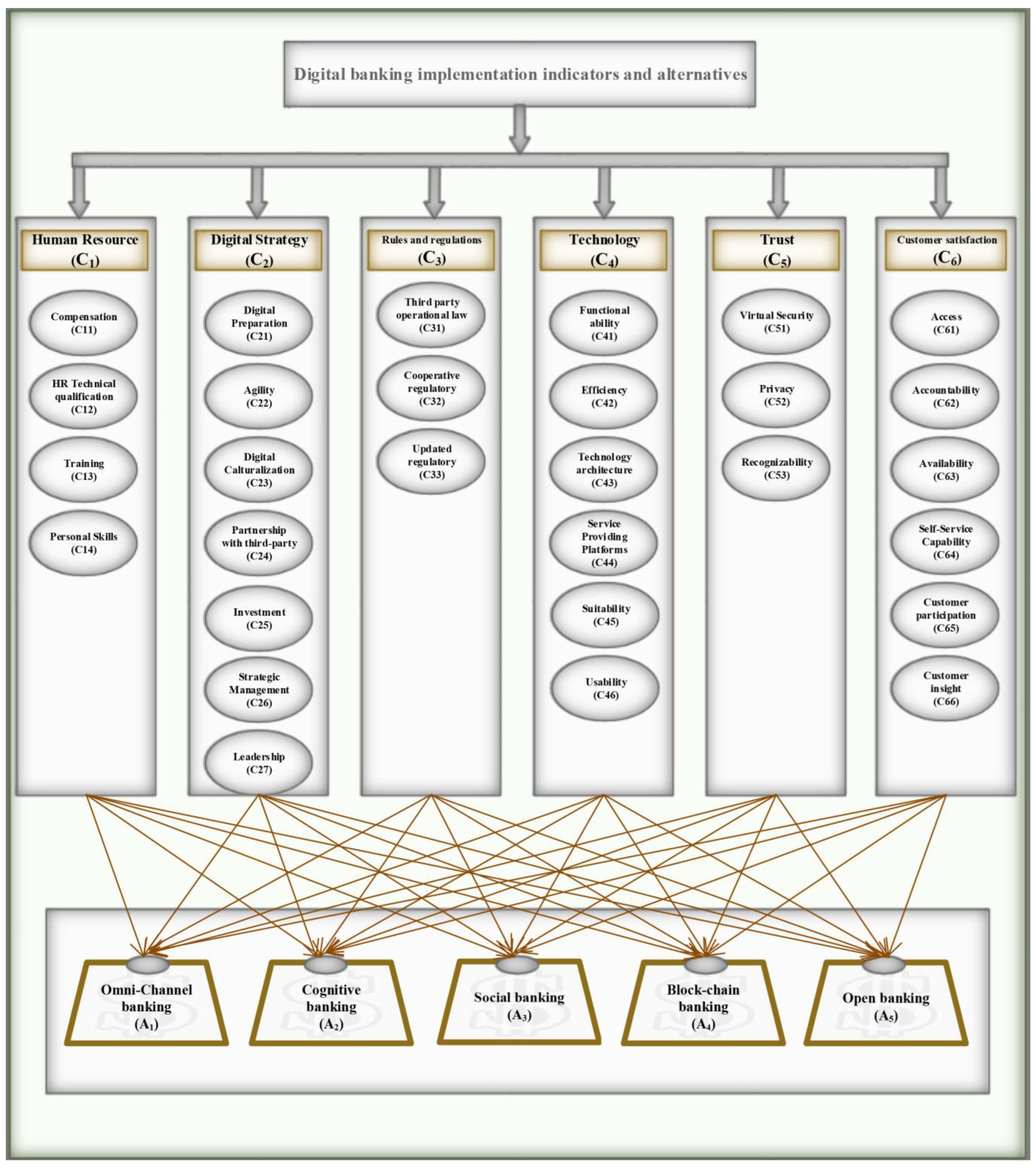

2.3. Digital Banking Implementation Criteria

2.3.1. Human Resources

Compensation

HR Technical Qualification

Training

Personal Skills

2.3.2. Digital Strategy

Digital Preparation

Agility

Digital Culturalization

Partnership with Third-Party

Investment

Strategic Management

Leadership

2.3.3. Regulations and Rules

Third-Party Operational Law

Cooperative Regulation

Updated Regulation

2.3.4. Technologies

Functional Ability

Efficiency

Technology Architecture

Service-Providing Platforms

Suitability

Usability

2.3.5. Trust

Virtual Security

Privacy

Recognizability

2.3.6. Customer Satisfaction

Access

Accountability

Availability

Self-Service Capability

Customer Participation

Customer Insight

2.4. Digital Banking Implementation: Key Trends and Alternatives

{kind=link}

{kind=link}

| Alternative | Explanation | Source |

|---|---|---|

| Omni-channel banking | In omni-channel banking, communication with the customer is conducted uniformly at any time, in any place and on all channels. The customer and the activities he performs are the focus of how to provide the services that are provided to him. Accordingly, the way of serving each customer is personalized based on the activities performed in all portals. With this method, not only the explicit requests of the customer are answered but also his implicit interests and needs are guessed. | [141] |

| Cognitive banking | Cognitive banking begins with the development of the big data platform by collecting, integrating, and extracting structured and unstructured customer data and other useful data, and it incorporates artificial intelligence and advanced data-based analytics. It is worth noting that with the maturity of systems and algorithms based on artificial intelligence, cognitive banking, as a new generation of advanced analytics with learning capabilities, will replace smart banking. | [142] |

| Social banking | Social networks can be used as one of the important platforms for promoting and even selling the products and services of various businesses. This platform creates a good opportunity for banks to, on the one hand, be on the path to transition to a social business model and coordinate with emerging markets, and on the other hand, by analyzing large volumes of customer data and measuring customer behavior, provide better, personalized and new products and services. | [143] |

| Blockchain banking | Due to its nature, blockchain technology can provide the financial system with the tools needed to develop and improve services and products and to facilitate and accelerate the process of DB. Therefore, the use of this technology in the country’s banking industry has advantages such as transparency, security and control, no need for intermediaries, uncertainty of the system, integration and immutability, and reduced costs. According to an international analysis of emerging technologies, disrupting technologies such as blockchain technology are moving beyond unrealistic expectations and gradually entering a large implementation phase. | [144] |

| Open banking | In this model, banking data and information are shared through APIs between different members of the banking ecosystem with the customer’s permission according to specific standards, and this creates various opportunities and threats for the traditional banking system. Based on the transformation caused by the open banking model, banks transfer part of their activities in the banking value chain to other actors and change the situation from the position of bank management to the position of ecosystem management. | [145] |

3. Proposed Approach

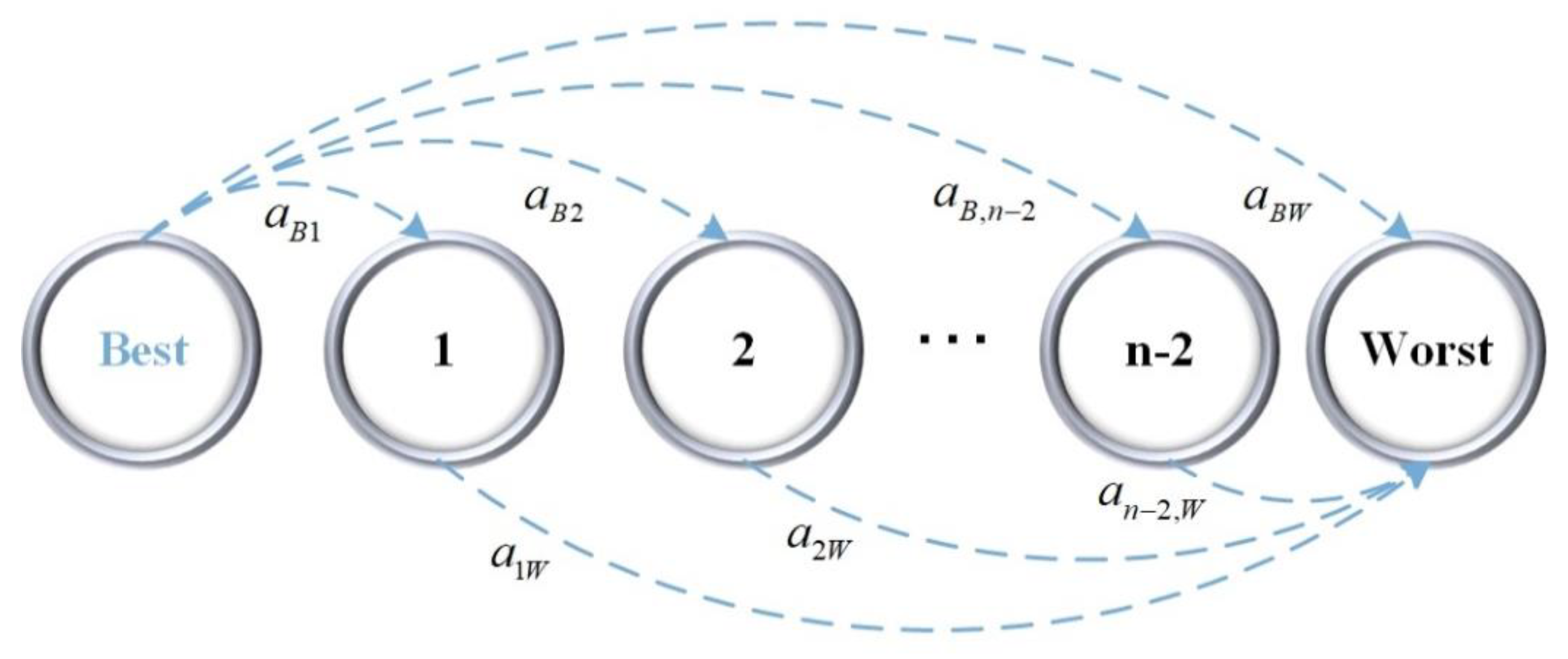

3.1. The Best–Worst Method (BWM)

3.2. The Fuzzy BWM

4. Results

4.1. Calculating the Importance of Each Criterion and Sub-Criterion

4.2. Ranking of Alternatives according to the Importance of Criteria

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A

| Sub-Criteria | Expert | Best and Worst | BO and OW | A1 | A2 | A3 | A4 | A5 |

|---|---|---|---|---|---|---|---|---|

| C11 | Ex 4. | Best: A5 Worst: A2 | BO | SP | EX | SI | MI | EI |

| OW | SI | EI | MP | MP | EX | |||

| Ex 5. | BO | SP | VS | MP | SI | EI | ||

| OW | MI | EI | SI | SI | VS | |||

| C12 | Ex 4. | Best: A4 Worst: A1 | BO | EX | MP | MP | EI | MI |

| OW | EI | MI | SI | EX | SI | |||

| Ex 5. | BO | EX | VS | SP | EI | SI | ||

| OW | EI | SI | MP | EX | MP | |||

| C13 | Ex 4. | Best: A5 Worst: A2 | BO | SI | VS | SP | SP | EI |

| OW | MP | EI | SI | SP | VS | |||

| Ex 5. | BO | VS | EX | SP | MP | EI | ||

| OW | SP | EI | SI | SI | EX | |||

| C14 | Ex 4. | Best: A5 Worst: A1 | BO | SP | SI | MI | MP | EI |

| OW | EI | MI | SI | SI | SP | |||

| Ex 5. | BO | EX | SI | SI | MI | EI | ||

| OW | EI | WI | MP | MP | EX |

| Sub-Criteria | Expert | Best and Worst | BO and OW | A1 | A2 | A3 | A4 | A5 |

|---|---|---|---|---|---|---|---|---|

| C21 | Ex 4. | Best: A3 Worst: A2 | BO | MP | EX | EI | WI | MI |

| OW | MP | EI | EX | SI | SI | |||

| Ex 5. | BO | SP | VS | EI | SI | MP | ||

| OW | SI | EI | VS | SP | SI | |||

| C22 | Ex 4. | Best: A4 Worst: A1 | BO | SP | SI | MP | EI | MP |

| OW | EI | MI | WI | SP | SI | |||

| Ex 5. | BO | VS | SI | MP | EI | MI | ||

| OW | EI | MP | WI | VS | SI | |||

| C23 | Ex 4. | Best: A5 Worst: A1 | BO | EX | SP | SI | MP | EI |

| OW | EI | MP | SI | SP | EX | |||

| Ex 5. | BO | VS | SI | MP | MI | EI | ||

| OW | EI | MI | MP | MP | VS | |||

| C24 | Ex 4. | Best: A3 Worst: A1 | BO | SP | SI | EI | MI | MI |

| OW | EI | MP | SP | SI | SI | |||

| Ex 5. | BO | VS | SP | EI | MP | MP | ||

| OW | EI | MI | VS | MP | SI | |||

| C25 | Ex 4. | Best: A5 Worst: A2 | BO | SP | EX | MP | SI | EI |

| OW | MI | EI | MI | MP | EX | |||

| Ex 5. | BO | SP | EX | SI | MP | EI | ||

| OW | WI | EI | MP | MP | EX | |||

| C26 | Ex 4. | Best: A4 Worst: A1 | BO | VS | MI | MP | EI | SI |

| OW | EI | WI | WI | VS | SI | |||

| Ex 5. | BO | VS | WI | MI | EI | MI | ||

| OW | EI | MI | MP | VS | SP | |||

| C27 | Ex 4. | Best: A3 Worst: A2 | BO | MP | SP | EI | SI | MP |

| OW | SI | EI | SP | MP | SI | |||

| Ex 5. | BO | MP | SP | EI | SI | MP | ||

| OW | SI | EI | SP | MI | MP |

| Sub-Criteria | Expert | Best and Worst | BO and OW | A1 | A2 | A3 | A4 | A5 |

|---|---|---|---|---|---|---|---|---|

| C31 | Ex 4. | Best: A4 Worst: A3 | BO | MP | SP | VS | EI | SP |

| OW | MP | MP | EI | VS | SP | |||

| Ex 5. | BO | SI | MP | SP | EI | MP | ||

| OW | WI | WI | EI | SP | SI | |||

| C32 | Ex 4. | Best: A5 Worst: A2 | BO | SP | EX | SI | SI | EI |

| OW | WI | EI | WI | MP | EX | |||

| Ex 5. | BO | MP | VS | MP | SI | EI | ||

| OW | MP | EI | MI | SP | VS | |||

| C33 | Ex 4. | Best: A5 Worst: A1 | BO | EX | SP | SP | MP | EI |

| OW | EI | MP | MP | SI | EX | |||

| Ex 5. | BO | EX | MP | MI | MI | EI | ||

| OW | EI | SP | SP | SI | EX |

| Sub-Criteria | Expert | Best and Worst | BO and OW | A1 | A2 | A3 | A4 | A5 |

|---|---|---|---|---|---|---|---|---|

| C41 | Ex 4. | Best: A3 Worst: A1 | BO | VS | SI | EI | MP | MI |

| OW | EI | MI | VS | SI | SP | |||

| Ex 5. | BO | EX | SP | EI | SI | SI | ||

| OW | EI | WI | EX | MP | MI | |||

| C42 | Ex 4. | Best: A3 Worst: A2 | BO | MP | SP | EI | MI | MI |

| OW | MI | EI | SP | SI | SI | |||

| Ex 5. | BO | MI | VS | EI | WI | MP | ||

| OW | WI | EI | VS | MP | SI | |||

| C43 | Ex 4. | Best: A5 Worst: A1 | BO | VS | SP | SI | SI | EI |

| OW | EI | MI | MP | SI | VS | |||

| Ex 5. | BO | VS | MP | MI | MI | EI | ||

| OW | EI | WI | MP | WI | VS | |||

| C44 | Ex 4. | Best: A4 Worst: A1 | BO | EX | VS | SP | EI | MP |

| OW | EI | MP | SI | EX | SI | |||

| Ex 5. | BO | SP | MP | MI | EI | MP | ||

| OW | EI | MI | MP | SP | SI | |||

| C45 | Ex 4. | Best: A4 Worst: A1 | BO | SP | MP | MI | EI | MI |

| OW | EI | WI | SI | SP | SI | |||

| Ex 5. | BO | VS | SP | SI | EI | MP | ||

| OW | EI | MI | MP | VS | SI | |||

| C46 | Ex 4. | Best: A3 Worst: A2 | BO | SP | EX | EI | SI | MP |

| OW | MI | EI | EX | MP | SI | |||

| Ex 5. | BO | SP | VS | EI | SI | SI | ||

| OW | MI | EI | VS | MP | SI |

| Sub-Criteria | Expert | Best and Worst | BO and OW | A1 | A2 | A3 | A4 | A5 |

|---|---|---|---|---|---|---|---|---|

| C51 | Ex 4. | Best: A3 Worst: A1 | BO | VS | MP | EI | SI | SI |

| OW | EI | WI | VS | SI | SP | |||

| Ex 5. | BO | SP | MI | EI | MP | MP | ||

| OW | EI | MP | SP | SI | SI | |||

| C52 | Ex 4. | Best: A5 Worst: A3 | BO | SI | MP | SP | MP | EI |

| OW | WI | WI | EI | SI | SP | |||

| Ex 5. | BO | SP | SP | EX | MP | EI | ||

| OW | WI | WI | EI | SI | EX | |||

| C53 | Ex 4. | Best: A5 Worst: A1 | BO | VS | SI | SI | MI | EI |

| OW | EI | WI | WI | MP | VS | |||

| Ex 5. | BO | SP | MI | MP | SI | EI | ||

| OW | EI | MI | MP | MP | SP |

| Sub-Criteria | Expert | Best and Worst | BO and OW | A1 | A2 | A3 | A4 | A5 |

|---|---|---|---|---|---|---|---|---|

| C61 | Ex 4. | Best: A5 Worst: A2 | BO | SP | VS | SI | MP | EI |

| OW | WI | EI | WI | WI | VS | |||

| Ex 5. | BO | SP | VS | SP | MP | EI | ||

| OW | MP | EI | MP | MI | VS | |||

| C62 | Ex 4. | Best: A4 Worst: A2 | BO | SP | EX | SP | EI | MP |

| OW | WI | EI | MP | EX | SP | |||

| Ex 5. | BO | SI | VS | SP | EI | SP | ||

| OW | MP | EI | MP | VS | SI | |||

| C63 | Ex 4. | Best: A4 Worst: A1 | BO | SP | SI | SI | EI | MI |

| OW | EI | WI | MP | SP | SI | |||

| Ex 5. | BO | VS | SP | SI | EI | MP | ||

| OW | EI | MP | MP | VS | SP | |||

| C64 | Ex 4. | Best: A4 Worst: A2 | BO | SP | VS | MP | EI | MP |

| OW | MP | EI | MP | VS | SP | |||

| Ex 5. | BO | MI | SP | MI | EI | SI | ||

| OW | WI | EI | WI | SP | MP | |||

| C65 | Ex 4. | Best: A3 Worst: A1 | BO | VS | SI | EI | MP | MP |

| OW | EI | WI | VS | SI | SI | |||

| Ex 5. | BO | SP | MP | EI | MI | MI | ||

| OW | EI | WI | SP | WI | SI | |||

| C66 | Ex 4. | Best: A5 Worst: A2 | BO | SP | EX | SP | MP | EI |

| OW | MP | EI | SP | MI | EX | |||

| Ex 5. | BO | SP | VS | SI | SI | EI | ||

| OW | WI | EI | MP | SI | VS |

References

- Skinner, C. Digital Bank: Strategies to Launch or Become a Digital Bank; Marshall Cavendish International Asia Pte Ltd.: Singapore, 2014; ISBN 9814561800. [Google Scholar]

- Rogers, D. The Digital Transformation Playbook Rethink Your Business for the Digital Age; Columbia University Press: New York, NY, USA, 2016. [Google Scholar]

- Buvat, J.; KVG, S. Doing Business the Digital Way: How Capital One Fundamentally Disrupted the Financial Services Industry; Capgemini Consulting: Vienna, Austria, 2014; Available online: https://www.capgemini.com (accessed on 8 March 2023).

- Pourebrahimi, N.; Kordnaeij, A.; Hosseini, H.K.; Azar, A. Developing a Digital Banking Framework in the Iranian Banks: Prerequisites and Facilitators. Int. J. E-Bus. Res. (IJEBR) 2018, 14, 65–77. [Google Scholar] [CrossRef]

- Cziesla, T. A literature review on digital transformation in the financial service industry. In Proceedings of the 27th Bled eConference eEcosystems, Bled, Slovenia, 1–5 June 2014. [Google Scholar]

- Yip, A.W.H.; Bocken, N.M.P. Sustainable business model archetypes for the banking industry. J. Clean. Prod. 2018, 174, 150–169. [Google Scholar] [CrossRef]

- Kitsios, F.; Giatsidis, I.; Kamariotou, M. Digital Transformation and Strategy in the Banking Sector: Evaluating the Acceptance Rate of E-Services. J. Open Innov. Technol. Mark. Complex. 2021, 7, 204. [Google Scholar] [CrossRef]

- Kaur, B.; Kiran, S.; Grima, S.; Rupeika-Apoga, R. Digital banking in Northern India: The risks on customer satisfaction. Risks 2021, 9, 209. [Google Scholar] [CrossRef]

- Egala, S.B.; Boateng, D.; Mensah, S.A. To leave or retain? An interplay between quality digital banking services and customer satisfaction. Int. J. Bank Mark. 2021, 39, 1420–1445. [Google Scholar] [CrossRef]

- Grima, S.; Kizilkaya, M.; Rupeika-Apoga, R.; Romānova, I.; Gonzi, R.D.; Jakovljevic, M. A country pandemic risk exposure measurement model. Risk Manag. Healthc. Policy 2020, 13, 2067–2077. [Google Scholar] [CrossRef]

- Shaikh, A.A.; Karjaluoto, H. On some misconceptions concerning digital banking and alternative delivery channels. Int. J. E-Bus. Res. (IJEBR) 2016, 12, 1–16. [Google Scholar] [CrossRef]

- Rezaei, J. Best-worst multi-criteria decision-making method. Omega 2015, 53, 49–57. [Google Scholar] [CrossRef]

- Pakurár, M.; Haddad, H.; Nagy, J.; Popp, J.; Oláh, J. The service quality dimensions that affect customer satisfaction in the Jordanian banking sector. Sustainability 2019, 11, 1113. [Google Scholar] [CrossRef]

- Patel, K.J.; Patel, H.J. Adoption of internet banking services in Gujarat: An extension of TAM with perceived security and social influence. Int. J. Bank Mark. 2018, 36, 147–169. [Google Scholar] [CrossRef]

- Nguyen, O.T. Factors affecting the intention to use digital banking in Vietnam. J. Asian Financ. Econ. Bus. 2020, 7, 303–310. [Google Scholar] [CrossRef]

- Alam, S.S.; Khatibi, A.; Santhapparaj, A.S.; Talha, M. Development and prospects of internet banking in Bangladesh. Compet. Rev. Int. Bus. J. 2007, 17, 56–66. [Google Scholar]

- Kim, H.-S.; Shim, J.-H. The effects of quality factors on customer satisfaction, trust and behavioral intention in chicken restaurants. J. Ind. Distrib. Bus. 2019, 10, 43–56. [Google Scholar] [CrossRef]

- Parasuraman, A.; Zeithaml, V.A.; Berry, L.L. A conceptual model of service quality and its implications for future research. J. Mark. 1985, 49, 41–50. [Google Scholar] [CrossRef]

- Kim, J. Platform quality factors influencing content providers’ loyalty. J. Retail. Consum. Serv. 2021, 60, 102510. [Google Scholar] [CrossRef]

- Uzir, M.U.H.; Hamid, A.B.A.; Latiff, A.S.A. Does customer satisfaction exist in purchasing and usage of electronic home appliances in Bangladesh through interaction effects of social media? Int. J. Bus. Excell. 2021, 23, 113–137. [Google Scholar] [CrossRef]

- Tan, C.-W.; Benbasat, I.; Cenfetelli, R.T. IT-mediated customer service content and delivery in electronic governments: An empirical investigation of the antecedents of service quality. MIS Q. 2013, 37, 77–109. [Google Scholar] [CrossRef]

- Blut, M. E-service quality: Development of a hierarchical model. J. Retail. 2016, 92, 500–517. [Google Scholar] [CrossRef]

- Li, Y.; Shang, H. Service quality, perceived value, and citizens’ continuous-use intention regarding e-government: Empirical evidence from China. Inf. Manag. 2020, 57, 103197. [Google Scholar] [CrossRef]

- Westerman, G.; Bonnet, D.; McAfee, A. Leading Digital: Turning Technology into Business Transformation; Harvard Business Press: Boston, MA, USA, 2014; ISBN 1625272472. [Google Scholar]

- Parasuraman, A.; Berry, L.L.; Zeithaml, V.A. Perceived service quality as a customer-based performance measure: An empirical examination of organizational barriers using an extended service quality model. Hum. Resour. Manag. 1991, 30, 335–364. [Google Scholar] [CrossRef]

- Parasuraman, A.P.; Zeithaml, V.; Berry, L. SERVQUAL: A multiple-Item Scale for measuring consumer perceptions of service quality. J. Retail. 1988, 64, 12–40. [Google Scholar]

- Lovelock, C.H.; Wirtz, J. Services Marketing: People, Technology, Strategy; Pearson Education: London, UK, 2004. [Google Scholar]

- Omarini, A.E. Banks and FinTechs: How to develop a digital open banking approach for the bank’s future. Int. Bus. Res. 2018, 11, 23–36. [Google Scholar] [CrossRef]

- Bouwman, H.; Nikou, S.; Molina-Castillo, F.J.; de Reuver, M. The impact of digitalization on business models. Digit. Policy Regul. Gov. 2018, 20, 105–124. [Google Scholar] [CrossRef]

- Sousa, M.J.; Rocha, Á. Digital learning: Developing skills for digital transformation of organizations. Future Gener. Comput. Syst. 2019, 91, 327–334. [Google Scholar] [CrossRef]

- Liu, D.; Chen, S.; Chou, T. Resource fit in digital transformation. Manag. Decis. 2011, 49, 1728–1742. [Google Scholar] [CrossRef]

- Mbama, C.I.; Ezepue, P.O. Digital banking, customer experience and bank financial performance: UK customers’ perceptions. Int. J. Bank Mark. 2018, 2, 230–255. [Google Scholar] [CrossRef]

- Khanboubi, F.; Boulmakoul, A. Digital Transformation Metamodel in Banking. INTIS 2019, 2019, 8. [Google Scholar]

- Kumar, R.; Singh, R.K.; Dwivedi, Y.K. Application of industry 4.0 technologies in SMEs for ethical and sustainable operations: Analysis of challenges. J. Clean. Prod. 2020, 275, 124063. [Google Scholar] [CrossRef]

- Avelar-Sosa, L.; García-Alcaraz, J.L.; Castrellón-Torres, J.P. The effects of some risk factors in the supply chains performance: A case of study. J. Appl. Res. Technol. 2014, 12, 958–968. [Google Scholar] [CrossRef]

- Büyüközkan, G.; Feyzioğlu, O.; Havle, C.A. Analysis of success factors in aviation 4.0 using integrated intuitionistic fuzzy MCDM methods. In Proceedings of the International Conference on Intelligent and Fuzzy Systems, Istanbul, Turkey, 23–25 July 2019; Springer: Berlin/Heidelberg, Germany, 2019; pp. 598–606. [Google Scholar]

- Büyüközkan, G.; Havle, C.A.; Feyzioğlu, O.; Göçer, F. A combined group decision making based IFCM and SERVQUAL approach for strategic analysis of airline service quality. J. Intell. Fuzzy Syst. 2020, 38, 859–872. [Google Scholar] [CrossRef]

- Li, W.; Yu, S.; Pei, H.; Zhao, C.; Tian, B. A hybrid approach based on fuzzy AHP and 2-tuple fuzzy linguistic method for evaluation in-flight service quality. J. Air Transp. Manag. 2017, 60, 49–64. [Google Scholar] [CrossRef]

- Aydemir, S.D.; Gerni, C. Measuring service quality of export credit agency in Turkey by using Servqual. Procedia-Soc. Behav. Sci. 2011, 24, 1663–1670. [Google Scholar] [CrossRef]

- Al-Neyadi, H.S.; Abdallah, S.; Malik, M. Measuring patient’s satisfaction of healthcare services in the UAE hospitals: Using SERVQUAL. Int. J. Healthc. Manag. 2018, 11, 96–105. [Google Scholar] [CrossRef]

- Kargari, M. Ranking of performance assessment measures at tehran hotel by combining DEMATEL, ANP, and SERVQUAL models under fuzzy condition. Math. Probl. Eng. 2018, 2018, 5701923. [Google Scholar] [CrossRef]

- Jun, M.; Cai, S. The key determinants of internet banking service quality: A content analysis. Int. J. Bank Mark. 2001, 19, 276–291. [Google Scholar] [CrossRef]

- Sari, F.O.; Bulut, C.; Pirnar, I. Adaptation of hospitality service quality scales for marina services. Int. J. Hosp. Manag. 2016, 54, 95–103. [Google Scholar] [CrossRef]

- Caro, L.M.; Garcia, J.A.M. Developing a multidimensional and hierarchical service quality model for the travel agency industry. Tour. Manag. 2008, 29, 706–720. [Google Scholar] [CrossRef]

- Miranda, S.; Tavares, P.; Queiró, R. Perceived service quality and customer satisfaction: A fuzzy set QCA approach in the railway sector. J. Bus. Res. 2018, 89, 371–377. [Google Scholar] [CrossRef]

- Santos, J. E-service quality: A model of virtual service quality dimensions. Manag. Serv. Qual. Int. J. 2003, 13, 233–246. [Google Scholar] [CrossRef]

- Corradini, F. Quality assessment of digital services in E-government with a case study in an Italian region. In Electronic Services: Concepts, Methodologies, Tools and Applications; IGI Global: Hershey, PA, USA, 2010; pp. 1100–1118. [Google Scholar]

- Hartwig, K.; Billert, M.S. Measuring service quality: A systematic literature review. In Proceedings of the Twenty-Sixth European Conference on Information Systems (ECIS2018), Portsmouth, UK, 23–28 June 2018. [Google Scholar]

- Benlian, A.; Koufaris, M.; Hess, T. Service quality in software-as-a-service: Developing the SaaS-Qual measure and examining its role in usage continuance. J. Manag. Inf. Syst. 2011, 28, 85–126. [Google Scholar] [CrossRef]

- Wu, Y.-L.; Tao, Y.-H.; Yang, P.-C. Learning from the past and present: Measuring Internet banking service quality. Serv. Ind. J. 2012, 32, 477–497. [Google Scholar] [CrossRef]

- Hizam, S.M.; Ahmed, W. A conceptual paper on SERVQUAL-framework for assessing quality of Internet of Things (IoT) services. arXiv 2020, arXiv:2001.01840. [Google Scholar] [CrossRef]

- Ardagna, D.; Casale, G.; Ciavotta, M.; Pérez, J.F.; Wang, W. Quality-of-service in cloud computing: Modeling techniques and their applications. J. Internet Serv. Appl. 2014, 5, 1–17. [Google Scholar] [CrossRef]

- Ahmad, M.; Abawajy, J.H. Digital library service quality assessment model. Procedia-Soc. Behav. Sci. 2014, 129, 571–580. [Google Scholar] [CrossRef]

- Al-Hader, M.; Rodzi, A.; Sharif, A.R.; Ahmad, N. Smart city components architicture. In Proceedings of the 2009 International Conference on Computational Intelligence, Modelling and Simulation, Brno, Czech Republic, 7–9 September 2009; IEEE: New York, NY, USA, 2009; pp. 93–97. [Google Scholar]

- Tate, M.; Furtmueller, E.; Gao, H.; Gable, G. Reconceptualizing digital service quality: A call-to-action and research approach. In Proceedings of the 18th Pacific Asia Conference on Information Systems (PACIS), Chengdu, China, 24–28 June 2014; Association for Information Systems (AIS): Atlanta, GA, USA, 2014; pp. 1–11. [Google Scholar]

- Tam, P.T.; Van Thuy, M.B. The Industry 4.0 Factor Affecting the Service Quality of Commercial Banks in Dong Nai Province. Eur. J. Account. Audit. Financ. Res. 2017, 5, 81–91. [Google Scholar]

- Leong, L.-Y.; Hew, T.-S.; Ooi, K.-B.; Wei, J. Predicting mobile wallet resistance: A two-staged structural equation modeling-artificial neural network approach. Int. J. Inf. Manag. 2020, 51, 102047. [Google Scholar] [CrossRef]

- Sardana, V.; Singhania, S. Digital technology in the realm of banking: A review of literature. Int. J. Res. Financ. Manag. 2018, 1, 28–32. [Google Scholar]

- Behbood, V.; Lu, J.; Zhang, G. Fuzzy refinement domain adaptation for long term prediction in banking ecosystem. IEEE Trans. Ind. Inform. 2013, 10, 1637–1646. [Google Scholar] [CrossRef]

- Mahdiraji, H.A.; Zavadskas, E.K.; Kazeminia, A.; Kamardi, A.A. Marketing strategies evaluation based on big data analysis: A CLUSTERING-MCDM approach. Econ. Res. Ekon. Istraživanja 2019, 32, 2882–2892. [Google Scholar] [CrossRef]

- Zhao, Q.; Tsai, P.-H.; Wang, J.-L. Improving financial service innovation strategies for enhancing china’s banking industry competitive advantage during the fintech revolution: A Hybrid MCDM model. Sustainability 2019, 11, 1419. [Google Scholar] [CrossRef]

- Kahveci, E.; Wolfs, B. Digital banking impact on Turkish deposit banks performance. Banks Bank Syst. 2018, 13, 48–57. [Google Scholar] [CrossRef]

- Sharma, S.K.; Mangla, S.K.; Luthra, S.; Al-Salti, Z. Mobile wallet inhibitors: Developing a comprehensive theory using an integrated model. J. Retail. Consum. Serv. 2018, 45, 52–63. [Google Scholar] [CrossRef]

- Veríssimo, J.M.C. Enablers and restrictors of mobile banking app use: A fuzzy set qualitative comparative analysis (fsQCA). J. Bus. Res. 2016, 69, 5456–5460. [Google Scholar] [CrossRef]

- Ondrus, J.; Bui, T.; Pigneur, Y. A foresight support system using MCDM methods. Group Decis. Negot. 2015, 24, 333–358. [Google Scholar] [CrossRef]

- Ali, S.S.; Kaur, R. An empirical approach to customer perception of mobile banking in Indian scenario. Int. J. Bus. Innov. Res. 2015, 9, 272–294. [Google Scholar] [CrossRef]

- Hu, Y.-C.; Liao, P.-C. Finding critical criteria of evaluating electronic service quality of Internet banking using fuzzy multiple-criteria decision making. Appl. Soft Comput. 2011, 11, 3764–3770. [Google Scholar] [CrossRef]

- Liang, D.; Zhang, Y.; Xu, Z.; Jamaldeen, A. Pythagorean fuzzy VIKOR approaches based on TODIM for evaluating internet banking website quality of Ghanaian banking industry. Appl. Soft Comput. 2019, 78, 583–594. [Google Scholar] [CrossRef]

- Tooranloo, H.S.; Ayatollah, A.S. Pathology the internet banking service quality using failure mode and effect analysis in interval-valued intuitionistic fuzzy environment. Int. J. Fuzzy Syst. 2017, 19, 109–123. [Google Scholar] [CrossRef]

- Arias-Oliva, M.; de Andrés-Sánchez, J.; Pelegrín-Borondo, J. Fuzzy set qualitative comparative analysis of factors influencing the use of cryptocurrencies in Spanish households. Mathematics 2021, 9, 324. [Google Scholar] [CrossRef]

- Gupta, S.; Gupta, S.; Mathew, M.; Sama, H.R. Prioritizing intentions behind investment in cryptocurrency: A fuzzy analytical framework. J. Econ. Stud. 2020, 48, 1442–1459. [Google Scholar] [CrossRef]

- Chen, N.-P.; Shen, K.-Y.; Liang, C.-J. Hybrid Decision Model for Evaluating Blockchain Business Strategy: A Bank’s Perspective. Sustainability 2021, 13, 5809. [Google Scholar] [CrossRef]

- Wibowo, S.; Grandhi, L.; Grandhi, S.; Wells, M. A Fuzzy Multicriteria Group Decision Making Approach for Evaluating and Selecting Fintech Projects. Mathematics 2022, 10, 225. [Google Scholar] [CrossRef]

- Chong, A.Y.-L. Predicting m-commerce adoption determinants: A neural network approach. Expert Syst. Appl. 2013, 40, 523–530. [Google Scholar] [CrossRef]

- Siam, A.Z. Role of the electronic banking services on the profits of Jordanian banks. Am. J. Appl. Sci. 2006, 3, 1999–2004. [Google Scholar] [CrossRef]

- Syamsuddin, I.; Hwang, J. A new fuzzy MCDM framework to evaluate e-government security strategy. In Proceedings of the 2010 4th International Conference on Application of Information and Communication Technologies, Kochi, India, 7–9 September 2010; IEEE: New York, NY, USA, 2010; pp. 1–5. [Google Scholar]

- Kaya, T.; Kahraman, C. A fuzzy approach to e-banking website quality assessment based on an integrated AHP-ELECTRE method. Technol. Econ. Dev. Econ. 2011, 17, 313–334. [Google Scholar] [CrossRef]

- Thulani, D.; Tofara, C.; Langton, R. Adoption and use of internet banking in Zimbabwe: An exploratory study. J. Internet Bank. Commer. 1970, 14, 1–13. [Google Scholar]

- Almarashdeh, I.; Bouzkraoui, H.; Azouaoui, A.; Youssef, H.; Niharmine, L.; Rahman, A.A.; Yahaya, S.S.S.; Atta, A.M.A.; Egbe, D.A.; Murimo, B.M. An overview of technology evolution: Investigating the factors influencing non-bitcoins users to adopt bitcoins as online payment transaction method. J. Theor. Appl. Inf. Technol. 2018, 96, 3984–3993. [Google Scholar]

- Wadesango, N.; Magaya, B. The impact of digital banking services on performance of commercial banks. J. Manag. Inf. Decis. Sci. 2020, 23, 343–353. [Google Scholar]

- Kambiz, S.; Saeed, Y.; Mohsen, K. A Mathematical Model Designing to Achieve Cost Management in Value Chain with Combinational Approach of AHP & GP (Case Study: Home Appliance Industries). SOCRATES Int. Multi-Ling. Multi-Discip. Ref. (Peer-Rev.) Index. Sch. J. 2016, 4, 30–51. [Google Scholar]

- Collins, C.J.; Clark, K.D. Strategic human resource practices, top management team social networks, and firm performance: The role of human resource practices in creating organizational competitive advantage. Acad. Manag. J. 2003, 46, 740–751. [Google Scholar] [CrossRef]

- Sivathanu, B.; Pillai, R. Smart HR 4.0–how industry 4.0 is disrupting HR. Hum. Resour. Manag. Int. Dig. 2018, 26, 7–11. [Google Scholar] [CrossRef]

- Carlson, D.S.; Upton, N.; Seaman, S. The impact of human resource practices and compensation design on performance: An analysis of family-owned SMEs. J. Small Bus. Manag. 2006, 44, 531–543. [Google Scholar] [CrossRef]

- Bayraktar, O.; Ataç, C. The effects of Industry 4.0 on Human resources management. In Globalization, Institutions and Socio-Economic Performance; Yıldırım, E., Çeştepe, H., Eds.; Peter Lang Group AG: Lausanne, Switzerland, 2018; pp. 337–359. [Google Scholar]

- Gehrke, L.; Kühn, A.T.; Rule, D.; Moore, P.; Bellmann, C.; Siemes, S.; Dawood, D.; Lakshmi, S.; Kulik, J.; Standley, M. A discussion of qualifications and skills in the factory of the future: A German and American perspective. VDI/ASME Ind. 2015, 4, 1–28. [Google Scholar]

- Hecklau, F.; Galeitzke, M.; Flachs, S.; Kohl, H. Holistic approach for human resource management in Industry 4.0. Procedia Cirp 2016, 54, 1–6. [Google Scholar] [CrossRef]

- Stachová, K.; Papula, J.; Stacho, Z.; Kohnová, L. External partnerships in employee education and development as the key to facing industry 4.0 challenges. Sustainability 2019, 11, 345. [Google Scholar] [CrossRef]

- Sony, M.; Naik, S. Critical factors for the successful implementation of Industry 4.0: A review and future research direction. Prod. Plan. Control 2020, 31, 799–815. [Google Scholar] [CrossRef]

- Chryssolouris, G.; Mavrikios, D.; Mourtzis, D. Manufacturing systems: Skills & competencies for the future. Procedia CIRp 2013, 7, 17–24. [Google Scholar]

- Gobble, M.M. Digital strategy and digital transformation. Res. Technol. Manag. 2018, 61, 66–71. [Google Scholar] [CrossRef]

- Porter, M.E.; Heppelmann, J.E. How smart, connected products are transforming competition. Harv. Bus. Rev. 2014, 92, 64–88. [Google Scholar]

- De Carolis, A.; Macchi, M.; Negri, E.; Terzi, S. A maturity model for assessing the digital readiness of manufacturing companies. In Proceedings of the IFIP International Conference on Advances in Production Management Systems, Hamburg, Germany, 3–7 September 2017; Springer: Berlin/Heidelberg, Germany, 2017; pp. 13–20. [Google Scholar]

- Rajabzadeh, A.; Keramatpanah, M.; Keramatpanah, A. Comparative Modeling of Supply Chain Using Interpretive Structural Modeling and DEMATEL. Organ. Resour. Manag. Res. 2015, 5, 49–71. [Google Scholar]

- Rane, S.B.; Narvel, Y.A.M. Re-designing the business organization using disruptive innovations based on blockchain-IoT integrated architecture for improving agility in future Industry 4.0. Benchmarking Int. J. 2021, 28, 1883–1908. [Google Scholar] [CrossRef]

- Matthiae, M.; Richter, J. Industry 4.0-Induced Change Factors and the Role of Organizational Agility. Universität zu Köln. 28 November 2018. Available online: https://aisel.aisnet.org/ecis2018_rp/53 (accessed on 17 March 2023).

- Dastranj, N.; Ghazinoory, S.; Gholami, A.A. Technology roadmap for social banking. J. Sci. Technol. Policy Manag. 2017, 9, 102–122. [Google Scholar] [CrossRef]

- Okatan, K.; Alankuş, O.B. Effect of organizational culture on internal innovation capacity. J. Organ. Stud. Innov. 2017, 4, 18–50. [Google Scholar]

- Ziaei Nafchi, M.; Mohelská, H. Organizational culture as an indication of readiness to implement industry 4.0. Information 2020, 11, 174. [Google Scholar] [CrossRef]

- Bömer, M.; Maxin, H. Why fintechs cooperate with banks—Evidence from germany. Z. Für Die Gesamte Versicher. 2018, 107, 359–386. [Google Scholar] [CrossRef]

- Dushnitsky, G. Corporate Venture Capital: Past. In The Oxford Handbook of Entrepreneurship; Oxford University Press: Oxford, UK, 2006; p. 387. [Google Scholar]

- Klus, M.F.; Lohwasser, T.S.; Holotiuk, F.; Moormann, J. Strategic alliances between banks and fintechs for digital innovation: Motives to collaborate and types of interaction. J. Entrep. Financ. 2019, 21, 1. [Google Scholar] [CrossRef]

- Pamucar, D.; Chatterjee, K.; Zavadskas, E.K. Assessment of third-party logistics provider using multi-criteria decision-making approach based on interval rough numbers. Comput. Ind. Eng. 2019, 127, 383–407. [Google Scholar] [CrossRef]

- Qian, X.; Fang, S.-C.; Yin, M.; Huang, M.; Li, X. Selecting green third party logistics providers for a loss-averse fourth party logistics provider in a multiattribute reverse auction. Inf. Sci. 2021, 548, 357–377. [Google Scholar] [CrossRef]

- Lee, I.; Shin, Y.J. Fintech: Ecosystem, business models, investment decisions, and challenges. Bus. Horiz. 2018, 61, 35–46. [Google Scholar] [CrossRef]

- Lee, I.; Lee, K. The Internet of Things (IoT): Applications, investments, and challenges for enterprises. Bus. Horiz. 2015, 58, 431–440. [Google Scholar] [CrossRef]

- Cuesta, C.; Ruesta, M.; Tuesta, D.; Urbiola, P. The digital transformation of the banking industry. BBVA Res. 2015, 1, 1–10. [Google Scholar]

- Kane, G.C.; Palmer, D.; Phillips, A.N.; Kiron, D.; Buckley, N. Strategy, Not Technology, Drives Digital Transformation; MIT Sloan Management Review and Deloitte University Press: New York, NY, USA, 2015; Volume 14, pp. 1–25. [Google Scholar]

- Singh, A.; Hess, T. How chief digital officers promote the digital transformation of their companies. In Strategic Information Management; Routledge: New York, NY, USA, 2020; pp. 202–220. ISBN 0429286791. [Google Scholar]

- Guzmán, V.E.; Muschard, B.; Gerolamo, M.; Kohl, H.; Rozenfeld, H. Characteristics and Skills of Leadership in the Context of Industry 4.0. Procedia Manuf. 2020, 43, 543–550. [Google Scholar] [CrossRef]

- Lord, R.G.; Hall, R.J. Identity, deep structure and the development of leadership skill. Leadersh. Q. 2005, 16, 591–615. [Google Scholar] [CrossRef]

- Von Solms, J. Integrating Regulatory Technology (RegTech) into the digital transformation of a bank Treasury. J. Bank. Regul. 2021, 22, 152–168. [Google Scholar] [CrossRef]

- Silvestrov, S.N. The financial stability board as the four pier of the global financial system. Financ. Theory Pract. 2017, 6, 84–91. [Google Scholar]

- Ahmed, U. The Importance of cross-border regulatory cooperation in an era of digital trade. World Trade Rev. 2019, 18, S99–S120. [Google Scholar] [CrossRef]

- González, J.L.; Jouanjean, M.-A. Digital Trade: Developing a Framework for Analysis; OCED Publishing: Paris, France, 2017. [Google Scholar]

- Price, S.; Jewitt, C.; Brown, B. The Sage Handbook of Digital Technology Research; Sage: Thousand Oaks, CA, USA, 2013; ISBN 1446287084. [Google Scholar]

- Arias, M.I.; Maçada, A.C.G. Digital government for e-government service quality: A literature review. In Proceedings of the 11th International Conference on Theory and Practice of Electronic Governance, Galway, Ireland, 4–6 April 2018; pp. 7–17. [Google Scholar]

- LeFevre, A.E.; Mohan, D.; Hutchful, D.; Jennings, L.; Mehl, G.; Labrique, A.; Romano, K.; Moorthy, A. Mobile Technology for Community Health in Ghana: What happens when technical functionality threatens the effectiveness of digital health programs? BMC Med. Inform. Decis. Mak. 2017, 17, 1–17. [Google Scholar] [CrossRef]

- Tansley, R.; Bass, M.; Stuve, D.; Branschofsky, M.; Chudnov, D.; McClellan, G.; Smith, M. The DSpace institutional digital repository system: Current functionality. In Proceedings of the 2003 Joint Conference on Digital Libraries, Houston, TX, USA, 27–31 May 2003; IEEE: New York, NY, USA, 2003; pp. 87–97. [Google Scholar]

- Talluri, S.; Kim, M.K.; Schoenherr, T. The relationship between operating efficiency and service quality: Are they compatible? Int. J. Prod. Res. 2013, 51, 2548–2567. [Google Scholar] [CrossRef]

- Field, J.M.; Ritzman, L.P.; Safizadeh, M.H.; Downing, C.E. Uncertainty reduction approaches, uncertainty coping approaches, and process performance in financial services. Decis. Sci. 2006, 37, 149–175. [Google Scholar] [CrossRef]

- Hyvönen, J. Strategic Leading of Digital Transformation in Large Established Companies—A Multiple Case-Study. Master’s Thesis, Aalto University, Espoo, Finland, 2018. [Google Scholar]

- Shankar, A.; Datta, B. Factors affecting mobile payment adoption intention: An Indian perspective. Glob. Bus. Rev. 2018, 19, S72–S89. [Google Scholar] [CrossRef]

- Shitkova, M.; Holler, J.; Heide, T.; Clever, N.; Becker, J. Towards Usability Guidelines for Mobile Websites and Applications. Wirtsch. Proc. 2015, 107. Available online: https://aisel.aisnet.org/wi2015/107 (accessed on 17 March 2023).

- Mukherjee, A.; Nath, P. A model of trust in online relationship banking. Int. J. Bank Mark. 2003, 21, 5–15. [Google Scholar] [CrossRef]

- Mattila, J. The Blockchain Phenomenon—The Disruptive Potential of Distributed Consensus Architectures; ETLA Working Papers; The Research Institute of the Finnish Economy (ETLA): Helsinki, Finland, 2016. [Google Scholar]

- Omariba, Z.B.; Masese, N.B.; Wanyembi, G. Security and privacy of electronic banking. Int. J. Comput. Sci. Issues (IJCSI) 2012, 9, 432. [Google Scholar]

- Al-Zaben, N.; Onik, M.M.H.; Yang, J.; Lee, N.-Y.; Kim, C.-S. General data protection regulation complied blockchain architecture for personally identifiable information management. In Proceedings of the 2018 International Conference on Computing, Electronics & Communications Engineering (iCCECE), Southend, UK, 16–17 August 2018; IEEE: New York, NY, USA, 2018; pp. 77–82. [Google Scholar]

- Lee, K.C.; Chung, N. Understanding factors affecting trust in and satisfaction with mobile banking in Korea: A modified DeLone and McLean’s model perspective. Interact. Comput. 2009, 21, 385–392. [Google Scholar] [CrossRef]

- Malik, S.; Huet, F. Adaptive fault tolerance in real time cloud computing. In Proceedings of the 2011 IEEE World Congress on Services, Washington, DC, USA, 4–9 July 2011; IEEE: New York, NY, USA, 2011; pp. 280–287. [Google Scholar]

- Wazzan, M.; Fayoumi, A. Service availability evaluation for a protection model in hybrid cloud computing architecture. In Proceedings of the 2012 International Symposium on Telecommunication Technologies, Kuala Lumpur, Malaysia, 26–28 November 2012; IEEE: New York, NY, USA; pp. 307–312. [Google Scholar]

- Lewrén, M.; Murdoch, R.; Johnson, P. The Four Keys to Digital Trust. Don’t be Left Behind. 2014. Available online: https://www.accenture.com/us-en/Pages/insight-accenture-four-keys-digital-trust.aspx (accessed on 11 April 2023).

- Serra, L.C.; Carvalho, L.P.; Ferreira, L.P.; Vaz, J.B.S.; Freire, A.P. Accessibility evaluation of e-government mobile applications in Brazil. Procedia Comput. Sci. 2015, 67, 348–357. [Google Scholar] [CrossRef]

- Ganapathy, S.; Ranganathan, C.; Sankaranarayanan, B. Visualization strategies and tools for enhancing customer relationship management. Commun. ACM 2004, 47, 92–99. [Google Scholar] [CrossRef]

- Norman, A.T.; Russell, C.A. The pass-along effect: Investigating word-of-mouth effects on online survey procedures. J. Comput. Mediat. Commun. 2006, 11, 1085–1103. [Google Scholar] [CrossRef]

- Jin, J.; Liu, Y.; Ji, P.; Liu, H. Understanding big consumer opinion data for market-driven product design. Int. J. Prod. Res. 2016, 54, 3019–3041. [Google Scholar] [CrossRef]

- Sajić, M.; Bundalo, D.; Bundalo, Z.; Pašalić, D. Digital technologies in transformation of classical retail bank into digital bank. In Proceedings of the 2017 25th Telecommunication Forum (TELFOR), Belgrade, Serbia, 21–22 November 2017; IEEE: New York, NY, USA, 2017; pp. 1–4. [Google Scholar]

- Melnychenko, S.; Volosovych, S.; Baraniuk, Y. Dominant ideas of financial technologies in digital banking. Balt. J. Econ. Stud. 2020, 6, 92–99. [Google Scholar] [CrossRef]

- Wewege, L.; Lee, J.; Thomsett, M.C. Disruptions and digital banking trends. J. Appl. Financ. Bank. 2020, 10, 15–56. [Google Scholar]

- Sharifpour, H.; Ghaseminezhad, Y.; Hashemi-Tabatabaei, M.; Amiri, M. Investigating cause-and-effect relationships between supply chain 4.0 technologies. Eng. Manag. Prod. Serv. 2022, 14, 22–46. [Google Scholar] [CrossRef]

- Hamouda, M. Omni-channel banking integration quality and perceived value as drivers of consumers’ satisfaction and loyalty. J. Enterp. Inf. Manag. 2019, 32, 608–625. [Google Scholar] [CrossRef]

- Rodrigues, A.R.D.; Ferreira, F.A.F.; Teixeira, F.J.C.S.N.; Zopounidis, C. Artificial intelligence, digital transformation and cybersecurity in the banking sector: A multi-stakeholder cognition-driven framework. Res. Int. Bus. Financ. 2022, 60, 101616. [Google Scholar] [CrossRef]

- Bohlin, E.; Shaikh, A.A.; Hanafizadeh, P. Social network banking: A case study of 100 leading global banks. Int. J. E-Bus. Res. (IJEBR) 2018, 14, 1–13. [Google Scholar] [CrossRef]

- Guo, Y.; Liang, C. Blockchain application and outlook in the banking industry. Financ. Innov. 2016, 2, 1–12. [Google Scholar] [CrossRef]

- Daiy, A.K.; Shen, K.-Y.; Huang, J.-Y.; Lin, T.M.-Y. A hybrid MCDM model for evaluating open banking business partners. Mathematics 2021, 9, 587. [Google Scholar] [CrossRef]

- Amiri, M.; Hashemi-Tabatabaei, M.; Ghahremanloo, M.; Keshavarz-Ghorabaee, M.; Kazimieras Zavadskas, E.; Antucheviciene, J. A novel model for multi-criteria assessment based on BWM and possibilistic chance-constrained programming. Comput. Ind. Eng. 2021, 156, 107287. [Google Scholar] [CrossRef]

- Biswas, A.; Pal, B.B. Application of fuzzy goal programming technique to land use planning in agricultural system. Omega 2005, 33, 391–398. [Google Scholar] [CrossRef]

- Sengupta, A.; Pal, T.K.; Chakraborty, D. Interpretation of inequality constraints involving interval coefficients and a solution to interval linear programming. Fuzzy Sets Syst. 2001, 119, 129–138. [Google Scholar] [CrossRef]

- Ishibuchi, H.; Morioka, K.; Tanaka, H. A fuzzy neural network with trapezoid fuzzy weights. In Proceedings of the 1994 IEEE 3rd International Fuzzy Systems Conference, Orlando, FL, USA, 26–29 June 1994; IEEE: New York, NY, USA, 1994; pp. 228–233. [Google Scholar]

- Amiri, M.; Tabatabaei, M.H.; Ghahremanloo, M.; Keshavarz-Ghorabaee, M.; Zavadskas, E.K.; Antucheviciene, J. A new fuzzy approach based on BWM and fuzzy preference programming for hospital performance evaluation: A case study. Appl. Soft Comput. 2020, 92, 106279. [Google Scholar] [CrossRef]

- Rezaei, J. Best-worst multi-criteria decision-making method: Some properties and a linear model. Omega 2016, 64, 126–130. [Google Scholar] [CrossRef]

- Amiri, M.; Hashemi-Tabatabaei, M.; Ghahremanloo, M.; Keshavarz-Ghorabaee, M.; Zavadskas, E.K.; Banaitis, A. A new fuzzy BWM approach for evaluating and selecting a sustainable supplier in supply chain management. Int. J. Sustain. Dev. World Ecol. 2020, 28, 125–142. [Google Scholar] [CrossRef]

- Zhang, C.; Ma, C.; Xu, J. A new fuzzy MCDM method based on trapezoidal fuzzy AHP and hierarchical fuzzy integral. In Proceedings of the International Conference on Fuzzy Systems and Knowledge Discovery, Changsha, China, 27–29 August 2005; Springer: Berlin/Heidelberg, Germany, 2005; pp. 466–474. [Google Scholar]

- Amiri, M.; Hashemi-Tabatabaei, M.; Keshavarz-Ghorabaee, M.; Kaklauskas, A.; Zavadskas, E.K.; Antucheviciene, J. A Fuzzy Extension of Simplified Best-Worst Method (F-SBWM) and Its Applications to Decision-Making Problems. Symmetry 2023, 15, 81. [Google Scholar] [CrossRef]

- Dutta, D.; Kumar, P. Fuzzy inventory model without shortage using trapezoidal fuzzy number with sensitivity analysis. IOSR J. Math. 2012, 4, 32–37. [Google Scholar] [CrossRef]

- Tabatabaei, M.H.; Amiri, M.; Ghahremanloo, M.; Keshavarz-Ghorabaee, M.; Zavadskas, E.K.; Antucheviciene, J. Hierarchical Decision-making using a New Mathematical Model based on the Best-worst Method. Int. J. Comput. Commun. Control 2019, 14, 710–725. [Google Scholar] [CrossRef]

- Guo, S.; Zhao, H. Fuzzy best-worst multi-criteria decision-making method and its applications. Knowl. Based Syst. 2017, 121, 23–31. [Google Scholar] [CrossRef]

- Tabatabaei, M.H.; Amiri, M.; Khatami Firouzabadi, S.M.A.; Ghahremanloo, M.; Keshavarz-Ghorabaee, M.; Saparauskas, J. A new group decision-making model based on bwm and its application to managerial problems. Transform. Bus. Econ. 2019, 18, 197–214. [Google Scholar]

- Fenech, R.; Baguant, P.; Ivanov, D. The changing role of human resource management in an era of digital transformation. J. Manag. Inf. Decis. Sci. 2019, 22, 166. [Google Scholar]

- Shaikh, A.A.; Glavee-Geo, R.; Karjaluoto, H. Exploring the nexus between financial sector reforms and the emergence of digital banking culture–Evidences from a developing country. Res. Int. Bus. Financ. 2017, 42, 1030–1039. [Google Scholar] [CrossRef]

- Murinde, V.; Rizopoulos, E.; Zachariadis, M. The impact of the FinTech revolution on the future of banking: Opportunities and risks. Int. Rev. Financ. Anal. 2022, 81, 102103. [Google Scholar] [CrossRef]

- Piyathasanan, B.; Mathies, C.; Wetzels, M.; Patterson, P.G.; de Ruyter, K. A hierarchical model of virtual experience and its influences on the perceived value and loyalty of customers. Int. J. Electron. Commer. 2015, 19, 126–158. [Google Scholar]

- Githuku, W.A.; Kinyuru, R.N. Digital banking and customer relationship in banking industry in Kenya. Int. Acad. J. Hum. Resour. Bus. Adm. 2018, 3, 14–32. [Google Scholar]

- Aldaihani, F.M.F.; Ali, N.A. Bin Impact of social customer relationship management on customer satisfaction through customer empowerment: A study of Islamic Banks in Kuwait. Int. Res. J. Financ. Econ. 2018, 170, 41–53. [Google Scholar]

- Kaur, S.J.; Ali, L.; Hassan, M.K.; Al-Emran, M. Adoption of digital banking channels in an emerging economy: Exploring the role of in-branch efforts. J. Financ. Serv. Mark. 2021, 26, 107–121. [Google Scholar] [CrossRef]

- Banu, A.M.; Mohamed, N.S.; Parayitam, S. Online banking and customer satisfaction: Evidence from India. Asia-Pac. J. Manag. Res. Innov. 2019, 15, 68–80. [Google Scholar] [CrossRef]

- Frei, C. Open Banking: Opportunities and Risks. In Forthcoming in The Fintech Disruption: How Financial Innovation Is Transforming the Banking Industry; Walker, T., Nikbakht, E., Kooli, M., Eds.; Springer: Berlin/Heidelberg, Germany, 2023. [Google Scholar]

- Littlejohn, G.; Boskovich, G.; Prior, R. United Kingdom: The Butterfly Effect. In Open Banking; Oxford University Press: Oxford, UK, 2022; pp. 173–C9.N3. [Google Scholar] [CrossRef]

- Suhaimi, A.I.H.; Hassan, M.S.B.A. Determinants of branchless digital banking acceptance among generation Y in Malaysia. In Proceedings of the 2018 IEEE Conference on e-Learning, e-Management and e-Services (IC3e), Langkawi, Malaysia, 21–22 November 2018; IEEE: New York, NY, USA, 2018; pp. 103–108. [Google Scholar]

- Nasri, W. Acceptance of internet banking in Tunisian banks: Evidence from modified utaut model. Int. J. E-Bus. Res. (IJEBR) 2021, 17, 22–41. [Google Scholar] [CrossRef]

- Shahabi, V.; Azar, A.; Razi, F.F.; Shams, M.F.F. Simulation of the effect of COVID-19 outbreak on the development of branchless banking in Iran: Case study of Resalat Qard–al-Hasan Bank. Rev. Behav. Financ. 2020, 13, 85–108. [Google Scholar] [CrossRef]

- Guerra-Leal, E.M.; Arredondo-Trapero, F.G.; Vázquez-Parra, J.C. Financial inclusion and digital banking on an emergent economy. Rev. Behav. Financ. 2021, 15, 257–272. [Google Scholar] [CrossRef]

- Popova, Y. Economic Basis of Digital Banking Services Produced by FinTech Company in Smart City: Reference: Popova, Y. Economic Basis of Digital Banking Services Produced by FinTech Company in Smart City. J. Tour. Serv. 2021, 23, 86–104. [Google Scholar] [CrossRef]

- Indriasari, E.; Prabowo, H.; Gaol, F.L.; Purwandari, B. Intelligent Digital Banking Technology and Architecture: A Systematic Literature Review. Int. J. Interact. Mob. Technol. 2022, 16, 98–117. [Google Scholar] [CrossRef]

- Ananda, S.; Devesh, S.; Al Lawati, A.M. What factors drive the adoption of digital banking? An empirical study from the perspective of Omani retail banking. J. Financ. Serv. Mark. 2020, 25, 14–24. [Google Scholar] [CrossRef]

- Riza, A.F.; Hafizi, M.R. Customers attitude toward Islamic mobile banking in Indonesia: Implementation of TAM. Asian J. Islam. Manag. (AJIM) 2019, 1, 75–84. [Google Scholar] [CrossRef]

- Mansfield-Devine, S. Open banking: Opportunity and danger. Comput. Fraud Secur. 2016, 2016, 8–13. [Google Scholar] [CrossRef]

- Cucari, N.; Lagasio, V.; Lia, G.; Torriero, C. The impact of blockchain in banking processes: The Interbank Spunta case study. Technol. Anal. Strateg. Manag. 2022, 34, 138–150. [Google Scholar] [CrossRef]

- Rezaei, D.; Aghdasi, M.; Saeedi, F. Identification of Social Banking Approaches and Analysis of Their Effects on the Bank’s. Manag. Res. Iran 2021, 25, 26–49. [Google Scholar]

- Bhutani, A.; Wadhwani, P. Digital Banking Market Size by Type (Retail Banking, Corporate Banking, Investment Banking), By Services (Transactional, Non-Transactional), Regional Outlook, Growth Potential, Competitive Market Share & Forecast, 2018–2024. Glob. Mark. Insights 2018. [Google Scholar]

- Ermakova, E.P.; Frolova, E.E. Legal regulation of digital banking in Russia and foreign countries (European Union, USA, PRC). Perm U. Her. Jurid. Sci. 2019, 46, 606. [Google Scholar] [CrossRef]

- Van Steenis, H. Future of Finance: Review on the Outlook for the UK Financial System: What It Means for the Bank of England; Bank of England: London, UK, 2019. [Google Scholar]

- Victorino, M.L.S. Exploring Digital Banking in the Philippines: An Aid for Digital Financial Inclusion. In Proceedings of the 3rd International Conference on Business and Banking Innovations, Surabaya, Indonesia, 6–7 March 2021. [Google Scholar]

- Jeník, I.; Flaming, M.; Salman, A. Inclusive Digital Banking: Emerging Markets Case Studies; Consultative Group to Assist the Poor Working Paper: Washington, DC, USA, 2020. [Google Scholar]

- Chiu, J.L.; Bool, N.C.; Chiu, C.L. Challenges and factors influencing initial trust and behavioral intention to use mobile banking services in the Philippines. Asia Pac. J. Innov. Entrep. 2017, 11, 246–278. [Google Scholar] [CrossRef]

- Barquin, S.; de Gantès, G.; Vinayak, H.V.; Shrikhande, D. Digital banking in Indonesia: Building loyalty and generating growth. McKinsey Co. Febr. 2019. Available online: https://www.mckinsey.com/industries/financial-services/our-insights (accessed on 10 April 2023).

- Indriasari, E.; Gaol, F.L.; Matsuo, T. Digital banking transformation: Application of artificial intelligence and big data analytics for leveraging customer experience in the Indonesia banking sector. In Proceedings of the 2019 8th International Congress on Advanced Applied Informatics (IIAI-AAI), Toyama, Japan, 7–11 July 2019; IEEE: New York, NY, USA, 2019; pp. 863–868. [Google Scholar]

- Choi, J.; Erande, Y.; Yu, Y. Winning the Digital Banking Battle in the Asia Pacific; Boston Consulting Group: Boston, MA, USA, 2021. [Google Scholar]

| Concept | Reference | Theory Used | Purpose of the Study |

|---|---|---|---|

| Open digital banking | [28] | Open innovation | Review of the evolution of new banking models and open banking platforms |

| Maturity of digital banking | [29] | Theory of corporate strategy | Examining the impacts of digital trends on business models |

| Digital banking project | [31] | Concept of resource fit and resource-based view | Developing a combined view of organizational theories in digital banking |

| Customer experience in digital banking | [32] | Customer perceptions | Designing a conceptual model of customer satisfaction, experience, loyalty and performance of digital banking |

| Digital transformation and meta-model banking | [33] | Meta-model and ontology | Proposing a digitalization road map for financial organizations |

| Sustainable and ethical operations in the era of Industry 4.0 | [34] | Theory of social responsibility and sustainability | Determining the challenges of sustainable and ethical operations of production organizations and determining the relationships between them |

| Digital learning in banking | [35] | Organizational learning | Strategic redesign of new digital organization skills |

| Business Field | Reference | Approaches/Methods | Information Form |

|---|---|---|---|

| Aviation | [36] | IFAHP/IFVIKOR | Triangular fuzzy numbers |

| Transportation | [37] | Intuitionistic fuzzy cognitive mapping | Triangular fuzzy numbers |

| Communication | [38] | Fuzzy AHP/2-tuple fuzzy linguistic method | Triangular fuzzy numbers |

| Financial | [39] | Structural equation modeling | Crisp values |

| Health | [40] | Quantitative approach | Descriptive data |

| Tourism | [41] | Fuzzy ANP | Triangular fuzzy numbers |

| Internet banking | [42] | Content analysis | Qualitative data |

| Boat and small ship | [43] | Multiple regression analysis | Crisp values |

| Travel agency | [44] | Structural equation modeling | Crisp values |

| Railroad transportation | [45] | Multiple regression analysis/fsQCA | Crisp values |

| Field of Study | Reference | Uncertainty | Type of Research |

|---|---|---|---|

| Virtual service quality | [46] | Exploratory study | |

| Service quality in digital government | [47] | Exploratory study | |

| Evaluation of the quality of digital services | [48] | Systematic literature review | |

| Quality of service based on SaaS | [49] | √ | Exploratory study |

| Quality of online banking services | [50] | √ | Exploratory study |

| Service quality of Internet of Things | [51] | Exploratory study | |

| Quality of services on the platform of cloud computing | [52] | √ | Exploratory study |

| Digital library service quality | [53] | Exploratory study | |

| Service quality in the smart city | [54] | Exploratory study | |

| Service quality in the digital age | [55] | Critical study | |

| Service quality in the evolution of Industry 4.0 | [56] | Illustrative case study |

| Trend | Brief Definition | Related Paper | Approaches/Methods | Information Form | Uncertainty |

|---|---|---|---|---|---|

| Digital banking | Refers to using different types of technology, including internet banking, mobile banking and other technological trends, in the form of open banking, etc. [58] | [60] | BWM–COPRAS | Crisp values | |

| [59] | Fuzzy expert system | Triangular fuzzy sets | √ | ||

| [73] | DEMATEL-based analytic network process (DANP) and VIKOR | Crisp values | |||

| [62] | DEA | Crisp values | |||

| Mobile banking | Refers to the execution of transactions on the basis of mobile and Internet-based technology [74] | [64] | A fuzzy set qualitative comparative analysis (fsQCA) | Linguistic data | √ |

| [63] | ISM | Crisp values | |||

| [65] | MCDM methods | Crisp values | |||

| [66] | MCDM methods | Crisp values | |||

| E-banking | Refers to conducting transactions remotely on the Internet [75] | [76] | Fuzzy MCDM | Triangular fuzzy numbers | √ |

| [77] | Fuzzy MCDM | Triangular fuzzy numbers | √ | ||

| Internet banking | Refers to conducting financial transactions on banking websites through the Internet [78] | [67] | AHP–ELECTRE method | Crisp values | |

| [68] | Pythagorean fuzzy VIKOR | Pythagorean fuzzy numbers | √ | ||

| [69] | Fuzzy MCDM | Triangular fuzzy numbers | √ | ||

| Cryptocurrency; Bitcoin banking | Refers to secure financial transactions using cryptocurrencies [79] | [70] | A fuzzy set qualitative comparative analysis (fsQCA) | Linguistic data | √ |

| [71] | Fuzzy AHP | Triangular fuzzy numbers | √ | ||

| [72] | BWM and modified VIKOR | Triangular fuzzy numbers | √ |

| Linguistic Term | Trapezoidal Fuzzy Scale |

|---|---|

| Equal importance (EI) | (1,1,1,1) |

| Weak importance (WI) | (1,2,3,4) |

| Moderate importance (MI) | (2,3,4,5) |

| Moderate plus importance (MP) | (3,4,5,6) |

| Strong importance (SI) | (4,5,6,7) |

| Strong plus importance (SP) | (5,6,7,8) |

| Very strong importance (VS) | (6,7,8,9) |

| Extreme importance (EX) | (7,8,9,10) |

| EI | WI | MI | MP | SI | SP | VS | EX | |

|---|---|---|---|---|---|---|---|---|

| CI | 0 | 1.63 | 2.30 | 3 | 3.73 | 4.47 | 5.23 | 6.00 |

| Expert No. | Education and Work Experience | Organizational Position |

|---|---|---|

| Ex. 1 | Specialized doctorate in financial management, 25 years of teaching, research and management experience in the field of banking | Faculty member of the finance and banking department (full professor) |

| Ex. 2 | Specialized doctorate in financial management, 18 years of experience in the banking industry and bank CEO | Faculty member of the finance and banking department (full professor) |

| Ex. 3 | Specialized doctorate in accounting, 22 years of teaching and research experience | Faculty member of the accounting department (full professor) |

| Ex. 4 | Specialized doctorate in technology management, 15 years of experience in research and development in the banking industry | Bank research and development manager |

| Ex. 5 | Master’s degree in information technology, 20 years of experience in managing branches and information systems | Bank information systems manager |

| Expert | Ex. 1 | Ex. 2 | Ex. 3 | Ex. 4 | Ex. 5 | Rank |

|---|---|---|---|---|---|---|

| Best | C1 | C1 | C1 | C1 | C1 | --- |

| Human resources (C1) | EI | EI | EI | EI | EI | --- |

| Digital strategy (C2) | VS | SP | SI | EX | SP | --- |

| Rules and regulations (C3) | SI | WI | WI | MP | MI | --- |

| Technology (C4) | MP | SI | MP | MI | SI | --- |

| Trust (C5) | MI | WI | WI | MP | MP | --- |

| Customer satisfaction (C6) | SI | MI | MI | MP | MI | --- |

| Human resources (C1) | VS | SP | SI | EX | SP | --- |

| Digital strategy (C2) | EI | EI | EI | EI | EI | --- |

| Rules and regulations (C3) | MI | SI | MP | MI | MP | --- |

| Technology (C4) | MP | WI | WI | MP | WI | --- |

| Trust (C5) | SI | SI | MP | MI | MI | --- |

| Customer satisfaction (C6) | MI | MP | MI | MI | MP | --- |

| Worst | C2 | C2 | C2 | C2 | C2 | --- |

| Final Weights (, = 0.1) | ||||||

| Human resources (C1) | 0.421 | 0.293 | 0.275 | 0.430 | 0.374 | 1 |

| Digital strategy (C2) | 0.028 | 0.045 | 0.062 | 0.043 | 0.057 | 5 |

| Rules and regulations (C3) | 0.115 | 0.184 | 0.194 | 0.138 | 0.178 | 2 |

| Technology (C4) | 0.108 | 0.071 | 0.088 | 0.204 | 0.091 | 4 |

| Trust (C5) | 0.213 | 0.266 | 0.249 | 0.091 | 0.120 | 3 |

| Customer satisfaction (C6) | 0.115 | 0.139 | 0.130 | 0.091 | 0.178 | 2 |

| 0.006 | 0 | 0 | 0 | 0 | --- | |

| CR | 0.0001 | 0 | 0 | 0 | 0 | --- |

| Final Weights (, = 0.9) | ||||||

| Human resources (C1) | 0.444 | 0.344 | 0.341 | 0.440 | 0.416 | 1 |

| Digital strategy (C2) | 0.047 | 0.043 | 0.052 | 0.046 | 0.052 | 5 |

| Rules and regulations (C3) | 0.102 | 0.201 | 0.192 | 0.118 | 0.159 | 2 |

| Technology (C4) | 0.129 | 0.077 | 0.093 | 0.158 | 0.094 | 4 |

| Trust (C5) | 0.173 | 0.201 | 0.192 | 0.118 | 0.118 | 3 |

| Customer satisfaction (C6) | 0.102 | 0.131 | 0.126 | 0.118 | 0.159 | 2 |

| 0.059 | 0.037 | 0.024 | 0.020 | 0.044 | --- | |

| CR | 0.011 | 0.008 | 0.006 | 0.003 | 0.009 | --- |

| Expert | Ex. 1 | Ex. 2 | Ex. 3 | Ex. 4 | Ex. 5 | |

|---|---|---|---|---|---|---|

| Best | C13 | C13 | C13 | C13 | C13 | --- |

| Compensation (C11) | MP | VS | SP | MP | SI | --- |

| HR technical qualification (C12) | MI | MP | SI | WI | MI | --- |

| Training (C13) | EI | EI | EI | EI | EI | --- |

| Personal skills (C14) | WI | MI | MP | MI | MP | --- |

| Compensation (C11) | EI | EI | EI | EI | EI | --- |

| HR technical qualification (C12) | WI | EX | WI | MI | MP | --- |

| Training (C13) | MP | VS | SP | MP | SI | --- |

| Personal skills (C14) | MI | MI | MI | WI | WI | --- |

| Worst | C11 | C11 | C11 | C11 | C11 | --- |

| Local and Global Weights (, = 0.1) | ||||||

| Compensation (C11) | 0.096; 0.010 | 0.042; 0.002 | 0.081; 0.007 | 0.120; 0.024 | 0.080; 0.007 | 0.010 |

| HR Technical qualification (C12) | 0.132; 0.014 | 0.191; 0.013 | 0.143; 0.012 | 0.338; 0.069 | 0.249; 0.022 | 0.013 |

| Training (C13) | 0.568; 0.061 | 0.484; 0.034 | 0.586; 0.051 | 0.372; 0.075 | 0.556; 0.050 | 0.054 |

| Personal skills (C14) | 0.202; 0.021 | 0.282; 0.020 | 0.189; 0.016 | 0.169; 0.034 | 0.113; 0.010 | 0.020 |

| 0 | 0.108 | 0 | 0 | 0 | --- | |

| CR | 0 | 0.020 | 0 | 0 | 0 | --- |

| Local and Global Weights (, = 0.9) | ||||||

| Compensation (C11) | 0.092; 0.011 | 0.044; 0.003 | 0.078; 0.007 | 0.092; 0.014 | 0.076; 0.007 | 0.008 |

| HR technical qualification (C12) | 0.169; 0.021 | 0.180; 0.013 | 0.136; 0.012 | 0.258; 0.040 | 0.216; 0.020 | 0.021 |

| Training (C13) | 0.480; 0.061 | 0.532; 0.040 | 0.613; 0.057 | 0.480; 0.075 | 0.546; 0.051 | 0.056 |

| Personal skills (C14) | 0.258; 0.033 | 0.242; 0.018 | 0.171; 0.015 | 0.169; 0.026 | 0.160; 0.015 | 0.021 |

| 0.009; | 0.171 | 0.056 | 0.009 | 0.081 | --- | |

| CR | 0.003 | 0.032 | 0.012 | 0.003 | 0.021 | --- |

| Expert | Ex. 1 | Ex. 2 | Ex. 3 | Ex. 4 | Ex. 5 | |

|---|---|---|---|---|---|---|

| Best | C23 | C23 | C23 | C23 | C23 | --- |

| Digital preparation (C21) | WI | WI | MI | SI | MP | --- |

| Agility (C22) | MP | MI | MI | MP | MI | --- |

| Digital culturalization (C23) | EI | EI | EI | EI | EI | --- |

| Partnership with third-party (C24) | SI | MP | MP | WI | SI | --- |

| Investment (C25) | SP | SI | SI | VS | SP | --- |

| Strategic management (C26) | MI | WI | MP | MI | WI | --- |

| Leadership (C27) | WI | MI | WI | SP | MP | --- |

| Digital preparation (C21) | SI | MP | MI | WI | MI | --- |

| Agility (C22) | WI | MI | MI | MI | MP | --- |

| Digital culturalization (C23) | SP | SI | SI | VS | SP | --- |

| Partnership with third-party (C24) | WI | WI | WI | MP | WI | --- |

| Investment (C25) | EI | EI | EI | EI | EI | --- |

| Strategic management (C26) | MP | MP | WI | MI | SI | --- |

| Leadership (C27) | SI | MI | MP | WI | MI | --- |

| Worst | C25 | C25 | C25 | C25 | C25 | --- |

| Local and Global Weights (, = 0.1) | ||||||

| Digital preparation (C21) | 0.149; 0.062 | 0.170; 0.050 | 0.101; 0.027 | 0.081; 0.035 | 0.103; 0.038 | 0.042 |

| Agility (C22) | 0.089; 0.037 | 0.115; 0.033 | 0.158; 0.043 | 0.108; 0.046 | 0.153; 0.057 | 0.043 |

| Digital culturalization (C23) | 0.275; 0.116 | 0.243; 0.071 | 0.333; 0.091 | 0.335; 0.144 | 0.322; 0.120 | 0.108 |

| Partnership with third-party (C24) | 0.067; 0.028 | 0.078; 0.022 | 0.099; 0.027 | 0.197; 0.085 | 0.078; 0.029 | 0.038 |

| Investment (C25) | 0.036; 0.015 | 0.055; 0.016 | 0.048; 0.013 | 0.051; 0.022 | 0.046; 0.017 | 0.016 |

| Strategic management (C26) | 0.131; 0.055 | 0.220; 0.064 | 0.107; 0.029 | 0.159; 0.068 | 0.191; 0.071 | 0.057 |

| Leadership (C27) | 0.250; 0.105 | 0.115; 0.033 | 0.149; 0.041 | 0.065; 0.028 | 0.103; 0.038 | 0.049 |

| 0 | 0 | 0 | 0 | 0 | --- | |

| CR | 0 | 0 | 0 | 0 | 0 | --- |

| Local and Global Weights (, = 0.9) | ||||||

| Digital preparation (C21) | 0.183; 0.081 | 0.171; 0.057 | 0.122; 0.041 | 0.080; 0.035 | 0.098; 0.040 | 0.050 |

| Agility (C22) | 0.089; 0.039 | 0.112; 0.038 | 0.122; 0.041 | 0.100; 0.044 | 0.132; 0.055 | 0.043 |

| Digital culturalization (C23) | 0.314; 0.139 | 0.303; 0.104 | 0.332; 0.113 | 0.368; 0.162 | 0.346; 0.144 | 0.132 |

| Partnership with third-party (C24) | 0.071; 0.031 | 0.083; 0.028 | 0.091; 0.031 | 0.206; 0.090 | 0.078; 0.032 | 0.042 |

| Investment (C25) | 0.039; 0.017 | 0.046; 0.015 | 0.050; 0.017 | 0.042; 0.018 | 0.043; 0.018 | 0.017 |

| Strategic management (C26) | 0.119; 0.053 | 0.171; 0.058 | 0.091; 0.031 | 0.135; 0.059 | 0.202; 0.084 | 0.057 |

| Leadership (C27) | 0.183; 0.081 | 0.112; 0.038 | 0.187; 0.064 | 0.066; 0.029 | 0.098; 0.040 | 0.050 |

| 0.033 | 0.021 | 0.023 | 0.023 | 0.037 | --- | |

| CR | 0.007 | 0.005 | 0.006 | 0.004 | 0.008 | --- |

| Expert | Ex. 1 | Ex. 2 | Ex. 3 | Ex. 4 | Ex. 5 | |

|---|---|---|---|---|---|---|

| Best | C31 | C31 | C31 | C31 | C31 | --- |

| Third-party operational law (C31) | EI | EI | EI | EI | EI | --- |

| Cooperative regulation (C32) | MP | MI | SI | SI | MI | --- |

| Updated regulation (C33) | WI | WI | MI | WI | WI | --- |

| Third-party operational law (C31) | MP | MI | SI | SI | MI | --- |

| Cooperative regulation (C32) | EI | EI | EI | EI | EI | --- |

| Updated regulation (C33) | MI | WI | MI | MP | WI | --- |

| Worst | C32 | C32 | C32 | C32 | C32 | --- |

| Local and Global Weights (, = 0.1) | ||||||

| Third-party operational law (C31) | 0.448; 0.012 | 0.419; 0.018 | 0.613; 0.038 | 0.464; 0.019 | 0.419; 0.023 | 0.022 |

| Cooperative regulation (C32) | 0.144; 0.004 | 0.199; 0.008 | 0.094; 0.005 | 0.113; 0.004 | 0.199; 0.011 | 0.006 |

| Updated regulation (C33) | 0.407; 0.011 | 0.381; 0.017 | 0.292; 0.018 | 0.422; 0.018 | 0.381; 0.021 | 0.017 |

| 0 | 0 | 0 | 0 | 0 | --- | |

| CR | 0 | 0 | 0 | 0 | 0 | --- |

| Local and Global Weights (, = 0.9) | ||||||

| Third-party operational law (C31) | 0.578; 0.027 | 0.554; 0.023 | 0.651; 0.033 | 0.585; 0.026 | 0.554; 0.028 | 0.027 |

| Cooperative regulation (C32) | 0.111; 0.005 | 0.153; 0.006 | 0.090; 0.004 | 0.090; 0.004 | 0.153; 0.007 | 0.005 |

| Updated regulation (C33) | 0.310; 0.014 | 0.291; 0.012 | 0.257; 0.013 | 0.324; 0.014 | 0.291; 0.015 | 0.013 |

| 0.011 | 0 | 0.096 | 0.030 | 0 | --- | |

| CR | 0.003 | 0 | 0.025 | 0.008 | 0 | --- |

| Expert | Ex. 1 | Ex. 2 | Ex. 3 | Ex. 4 | Ex. 5 | |

|---|---|---|---|---|---|---|

| Best | C42 | C42 | C42 | C42 | C42 | --- |

| Functional ability (C41) | MP | WI | SP | MI | MP | --- |

| Efficiency (C42) | EI | EI | EI | EI | EI | --- |

| Technology architecture (C43) | MI | SP | MP | WI | MI | --- |

| Service providing platforms (C44) | SI | VS | SI | SI | SP | --- |

| Suitability (C45) | WI | MP | WI | MI | SI | --- |

| Usability (C46) | MI | SI | MP | MP | WI | --- |

| Functional ability (C41) | WI | SI | WI | MI | MI | --- |

| Efficiency (C42) | SI | VS | SI | SI | SP | --- |

| Technology architecture (C43) | MI | MI | MP | MP | MP | --- |

| Service providing platforms (C44) | EI | EI | EI | EI | EI | --- |

| Suitability (C45) | MP | MP | SP | MI | WI | --- |

| Usability (C46) | MI | WI | MP | WI | WI | --- |

| Worst | C44 | C44 | C44 | C44 | C44 | --- |

| Local and Global Weights (, = 0.1) | ||||||

| Functional ability (C41) | 0.095; 0.011 | 0.292; 0.053 | 0.069; 0.013 | 0.106; 0.020 | 0.115; 0.020 | 0.023 |

| Efficiency (C42) | 0.296; 0.034 | 0.373; 0.068 | 0.332; 0.064 | 0.313; 0.060 | 0.358; 0.063 | 0.057 |

| Technology architecture (C43) | 0.142; 0.016 | 0.075; 0.013 | 0.114; 0.022 | 0.281; 0.054 | 0.170; 0.030 | 0.027 |

| Service providing platforms (C44) | 0.067; 0.007 | 0.040; 0.007 | 0.044; 0.008 | 0.047; 0.009 | 0.055; 0.009 | 0.008 |

| Suitability (C45) | 0.257; 0.029 | 0.123; 0.022 | 0.323; 0.062 | 0.149; 0.028 | 0.087; 0.015 | 0.031 |

| Usability (C46) | 0.141; 0.016 | 0.093; 0.017 | 0.114; 0.022 | 0.100; 0.019 | 0.211; 0.037 | 0.022 |

| 0 | 0.104 | 0.023 | 0 | 0 | --- | |

| CR | 0 | 0.019 | 0.006 | 0 | 0 | --- |

| Local and Global Weights (, = 0.9) | ||||||

| Functional ability (C41) | 0.100; 0.010 | 0.246; 0.049 | 0.078; 0.015 | 0.135; 0.015 | 0.112; 0.017 | 0.021 |

| Efficiency (C42) | 0.366; 0.037 | 0.414; 0.083 | 0.387; 0.074 | 0.366; 0.043 | 0.397; 0.063 | 0.060 |

| Technology architecture (C43) | 0.135; 0.013 | 0.079; 0.015 | 0.119; 0.022 | 0.206; 0.024 | 0.151; 0.024 | 0.019 |

| Service providing platforms (C44) | 0.055; 0.005 | 0.044; 0.008 | 0.050; 0.009 | 0.055; 0.006 | 0.049; 0.007 | 0.007 |

| Suitability (C45) | 0.206; 0.021 | 0.119; 0.024 | 0.244; 0.047 | 0.135; 0.015 | 0.089; 0.014 | 0.024 |

| Usability (C46) | 0.135; 0.013 | 0.095; 0.019 | 0.119; 0.022 | 0.100; 0.011 | 0.197; 0.031 | 0.019 |

| 0.026 | 0.053 | 0.078 | 0.026 | 0.042 | --- | |

| CR | 0.006 | 0.010 | 0.020 | 0.006 | 0.009 | --- |

| Expert | Ex. 1 | Ex. 2 | Ex. 3 | Ex. 4 | Ex. 5 | |

|---|---|---|---|---|---|---|

| Best | C53 | C53 | C53 | C53 | C53 | --- |

| Virtual security (C51) | MP | MI | MP | SI | MP | --- |

| Privacy (C52) | MI | WI | WI | MP | MI | --- |

| Recognizability (C53) | EI | EI | EI | EI | EI | --- |

| Virtual security (C51) | EI | EI | EI | EI | EI | --- |

| Privacy (C52) | WI | WI | WI | MI | MI | --- |

| Recognizability (C53) | MP | MI | MP | SI | MP | --- |

| Worst | C51 | C51 | C51 | C51 | C51 | --- |

| Local and Global Weights (, = 0.1) | ||||||

| Virtual security (C51) | 0.179; 0.020 | 0.199; 0.027 | 0.144; 0.018 | 0.104; 0.009 | 0.133; 0.023 | 0.019 |

| Privacy (C52) | 0.264; 0.030 | 0.381; 0.052 | 0.407; 0.052 | 0.218; 0.019 | 0.279; 0.049 | 0.040 |

| Recognizability (C53) | 0.555; 0.063 | 0.419; 0.058 | 0.448; 0.058 | 0.677; 0.061 | 0.587; 0.104 | 0.068 |

| 0 | 0 | 0 | 0 | 0 | --- | |

| CR | 0 | 0 | 0 | 0 | 0 | --- |

| Local and Global Weights (, = 0.9) | ||||||

| Virtual security (C51) | 0.125; 0.012 | 0.153; 0.020 | 0.143; 0.018 | 0.100; 0.011 | 0.111; 0.017 | 0.015 |

| Privacy (C52) | 0.227; 0.023 | 0.291; 0.038 | 0.295; 0.037 | 0.202; 0.023 | 0.247; 0.039 | 0.032 |

| Recognizability (C53) | 0.647; 0.066 | 0.554; 0.072 | 0.560; 0.070 | 0.698; 0.082 | 0.642; 0.102 | 0.078 |

| 0.010 | 0 | 0 | 0.088 | 0.075 | --- | |

| CR | 0.003 | 0 | 0 | 0.023 | 0.025 | --- |

| Expert | Ex. 1 | Ex. 2 | Ex. 3 | Ex. 4 | Ex. 5 | |

|---|---|---|---|---|---|---|

| Best | C61 | C61 | C61 | C61 | C61 | --- |

| Access (C61) | EI | EI | EI | EI | EI | --- |

| Accountability (C62) | SP | MI | MP | MI | MI | --- |

| Availability (C63) | EX | MP | SI | MP | SP | --- |

| Self-service capability (C64) | WI | WI | WI | MI | MP | --- |

| Customer participation (C65) | MP | WI | MI | WI | WI | --- |

| Customer insight (C66) | SI | MI | MP | WI | MI | --- |

| Access (C61) | EX | MP | SI | MP | SP | --- |

| Accountability (C62) | WI | WI | WI | WI | MI | --- |

| Availability (C63) | EI | EI | EI | EI | EI | --- |

| Self-service capability (C64) | SI | MI | MP | WI | WI | --- |

| Customer participation (C65) | MP | MI | MI | MI | MP | --- |

| Customer insight (C66) | MI | WI | WI | MI | MI | --- |

| Worst | C63 | C63 | C63 | C63 | C63 | --- |

| Local and Global Weights (, = 0.1) | ||||||

| Access (C61) | 0.440; 0.093 | 0.410; 0.109 | 0.443; 0.110 | 0.436; 0.039 | 0.421; 0.050 | 0.080 |

| Accountability (C62) | 0.083; 0.017 | 0.087; 0.023 | 0.075; 0.018 | 0.089; 0.008 | 0.112; 0.013 | 0.015 |

| Availability (C63) | 0.044; 0.009 | 0.079; 0.021 | 0.064; 0.015 | 0.073; 0.006 | 0.053; 0.006 | 0.011 |

| Self-service capability (C64) | 0.182; 0.038 | 0.167; 0.044 | 0.207; 0.051 | 0.090; 0.008 | 0.135; 0.016 | 0.031 |

| Customer participation (C65) | 0.141; 0.030 | 0.167; 0.044 | 0.134; 0.033 | 0.155; 0.014 | 0.165; 0.019 | 0.028 |

| Customer insight (C66) | 0.107; 0.022 | 0.087; 0.023 | 0.075; 0.018 | 0.155; 0.014 | 0.112; 0.013 | 0.018 |

| 0 | 0 | 0 | 0 | 0 | --- | |

| CR | 0 | 0 | 0 | 0 | 0 | --- |

| Local and Global Weights (, = 0.9) | ||||||

| Access (C61) | 0.421; 0.072 | 0.336; 0.067 | 0.379; 0.072 | 0.336; 0.039 | 0.375; 0.044 | 0.058 |

| Accountability (C62) | 0.078; 0.013 | 0.118; 0.023 | 0.104; 0.020 | 0.118; 0.013 | 0.134; 0.015 | 0.016 |

| Availability (C63) | 0.041; 0.007 | 0.064; 0.013 | 0.057; 0.011 | 0.064; 0.007 | 0.050; 0.006 | 0.008 |

| Self-service capability (C64) | 0.244; 0.042 | 0.180; 0.036 | 0.214; 0.041 | 0.118; 0.013 | 0.099; 0.011 | 0.028 |

| Customer participation (C65) | 0.119; 0.020 | 0.180; 0.036 | 0.140; 0.026 | 0.180; 0.021 | 0.204; 0.024 | 0.025 |

| Customer insight (C66) | 0.094; 0.016 | 0.118; 0.023 | 0.104; 0.020 | 0.180; 0.021 | 0.134; 0.015 | 0.019 |

| 0.043 | 0.006 | 0.027 | 0.006 | 0.013 | --- | |

| CR | 0.007 | 0.002 | 0.007 | 0.002 | 0.002 | --- |

| Criteria | Ex. 4 | Ex. 5 | Values of Alternatives () | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| A1 | A2 | A3 | A4 | A5 | CR | A1 | A2 | A3 | A4 | A5 | CR | A1 | A2 | A3 | A4 | A5 | |||

| C11 | 0.105 | 0.043 | 0.126 | 0.213 | 0.510 | 0.110 | 0.018 | 0.110 | 0.051 | 0.167 | 0.133 | 0.535 | 0.118 | 0.022 | 0.107 | 0.047 | 0.146 | 0.173 | 0.522 |

| C12 | 0.044 | 0.142 | 0.142 | 0.479 | 0.191 | 0.075 | 0.012 | 0.048 | 0.103 | 0.121 | 0.580 | 0.146 | 0.135 | 0.022 | 0.046 | 0.122 | 0.131 | 0.529 | 0.337 |

| C13 | 0.147 | 0.048 | 0.122 | 0.122 | 0.558 | 0.164 | 0.031 | 0.102 | 0.043 | 0.119 | 0.181 | 0.552 | 0.155 | 0.025 | 0.095 | 0.045 | 0.241 | 0.151 | 0.555 |

| C14 | 0.052 | 0.119 | 0.201 | 0.149 | 0.477 | 0.106 | 0.023 | 0.048 | 0.118 | 0.118 | 0.201 | 0.512 | 0.070 | 0.011 | 0.050 | 0.118 | 0.159 | 0.175 | 0.494 |

| C21 | 0.120 | 0.042 | 0.426 | 0.247 | 0.162 | 0.043 | 0.007 | 0.113 | 0.047 | 0.528 | 0.137 | 0.172 | 0.143 | 0.027 | 0.116 | 0.089 | 0.477 | 0.192 | 0.167 |

| C22 | 0.055 | 0.125 | 0.157 | 0.503 | 0.157 | 0.112 | 0.025 | 0.050 | 0.116 | 0.146 | 0.489 | 0.196 | 0.080 | 0.015 | 0.052 | 0.120 | 0.151 | 0.496 | 0.353 |

| C23 | 0.047 | 0.110 | 0.133 | 0.167 | 0.541 | 0.111 | 0.018 | 0.053 | 0.114 | 0.143 | 0.193 | 0.495 | 0.064 | 0.012 | 0.050 | 0.112 | 0.138 | 0.180 | 0.518 |

| C24 | 0.051 | 0.111 | 0.458 | 0.189 | 0.189 | 0.090 | 0.020 | 0.052 | 0.105 | 0.523 | 0.159 | 0.159 | 0.098 | 0.018 | 0.052 | 0.108 | 0.490 | 0.174 | 0.174 |

| C25 | 0.106 | 0.052 | 0.161 | 0.128 | 0.552 | 0.075 | 0.012 | 0.106 | 0.052 | 0.128 | 0.161 | 0.552 | 0.075 | 0.012 | 0.106 | 0.052 | 0.128 | 0.161 | 0.552 |

| C26 | 0.046 | 0.202 | 0.150 | 0.480 | 0.119 | 0.106 | 0.020 | 0.040 | 0.237 | 0.162 | 0.397 | 0.162 | 0.073 | 0.013 | 0.043 | 0.219 | 0.156 | 0.438 | 0.140 |

| C27 | 0.157 | 0.055 | 0.503 | 0.125 | 0.157 | 0.112 | 0.025 | 0.157 | 0.055 | 0.503 | 0.125 | 0.157 | 0.112 | 0.025 | 0.157 | 0.055 | 0.503 | 0.125 | 0.157 |

| C31 | 0.178 | 0.118 | 0.046 | 0.538 | 0.118 | 0.158 | 0.030 | 0.125 | 0.157 | 0.055 | 0.503 | 0.157 | 0.112 | 0.025 | 0.151 | 0.137 | 0.050 | 0.520 | 0.137 |

| C32 | 0.110 | 0.054 | 0.132 | 0.132 | 0.570 | 0.078 | 0.013 | 0.162 | 0.044 | 0.162 | 0.129 | 0.499 | 0.135 | 0.025 | 0.136 | 0.049 | 0.0147 | 0.130 | 0.534 |

| C33 | 0.051 | 0.110 | 0.110 | 0.167 | 0.560 | 0.090 | 0.015 | 0.039 | 0.138 | 0.186 | 0.186 | 0.448 | 0.092 | 0.015 | 0.045 | 0.146 | 0.148 | 0.176 | 0.504 |

| C41 | 0.048 | 0.117 | 0.486 | 0.148 | 0.199 | 0.091 | 0.017 | 0.054 | 0.110 | 0.570 | 0.132 | 0.132 | 0.078 | 0.013 | 0.051 | 0.113 | 0.528 | 0.140 | 0.165 |

| C42 | 0.134 | 0.052 | 0.449 | 0.181 | 0.181 | 0.076 | 0.017 | 0.167 | 0.041 | 0.410 | 0.256 | 0.124 | 0.076 | 0.014 | 0.150 | 0.046 | 0.429 | 0.218 | 0.152 |

| C43 | 0.053 | 0.114 | 0.138 | 0.138 | 0.555 | 0.122 | 0.023 | 0.053 | 0.129 | 0.173 | 0.173 | 0.469 | 0.035 | 0.006 | 0.053 | 0.121 | 0.155 | 0.155 | 0.512 |

| C44 | 0.048 | 0.098 | 0.115 | 0.561 | 0.175 | 0.121 | 0.020 | 0.050 | 0.145 | 0.195 | 0.463 | 0.145 | 0.103 | 0.022 | 0.049 | 0.121 | 0.155 | 0.512 | 0.160 |

| C45 | 0.052 | 0.134 | 0.181 | 0.449 | 0.181 | 0.076 | 0.017 | 0.054 | 0.108 | 0.131 | 0.541 | 0.164 | 0.101 | 0.019 | 0.053 | 0.121 | 0.156 | 0.495 | 0.172 |

| C46 | 0.107 | 0.050 | 0.548 | 0.129 | 0.162 | 0.086 | 0.014 | 0.114 | 0.053 | 0.555 | 0.138 | 0.138 | 0.122 | 0.023 | 0.110 | 0.051 | 0.551 | 0.133 | 0.150 |

| C51 | 0.046 | 0.168 | 0.516 | 0.134 | 0.134 | 0.140 | 0.026 | 0.050 | 0.195 | 0.463 | 0.145 | 0.145 | 0.103 | 0.023 | 0.048 | 0.181 | 0.489 | 0.139 | 0.139 |

| C52 | 0.125 | 0.157 | 0.055 | 0.157 | 0.503 | 0.112 | 0.025 | 0.110 | 0.110 | 0.051 | 0.166 | 0.561 | 0.088 | 0.014 | 0.117 | 0.133 | 0.053 | 0.161 | 0.482 |

| C53 | 0.059 | 0.114 | 0.114 | 0.192 | 0.519 | 0.038 | 0.007 | 0.054 | 0.198 | 0.147 | 0.117 | 0.481 | 0.094 | 0.021 | 0.056 | 0.156 | 0.130 | 0.154 | 0.500 |

| C61 | 0.099 | 0.066 | 0.120 | 0.150 | 0.562 | 0.026 | 0.004 | 0.111 | 0.055 | 0.111 | 0.168 | 0.553 | 0.104 | 0.019 | 0.105 | 0.060 | 0.115 | 0.159 | 0.557 |