A Kinetic Theory Model of the Dynamics of Liquidity Profiles on Interbank Networks

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

- The overall state of the system under consideration, a stylized financial market in the present paper, is described by a probability distribution over the micro-scale state of the active particles whose state includes, in addition to mechanical variables, a variable called activity, which describes the state of each individual entity. Hence, the said probability distribution is the dependent variable, while the activity is the micro-state. In the following we will specify what activity represents in our model, specifically referring to liquidity of assets.

- Interactions are modeled by mathematical tools of stochastic game theory. The output depends on the micro-state of the interacting entities and on the strategy they adopt to reach their pay-off, which is heterogeneously distributed over the active particles. In general, interactions are nonlocal and nonlinearly additive and that is the case of our model.

- The KTAP approach allows for transferring the interactions output into the dynamics, across time and space, of the dependent variable, accounting both for “rational” or even “irrational” strategies (see [1] for a detailed discussion on this point that is widely debated in the economic literature).

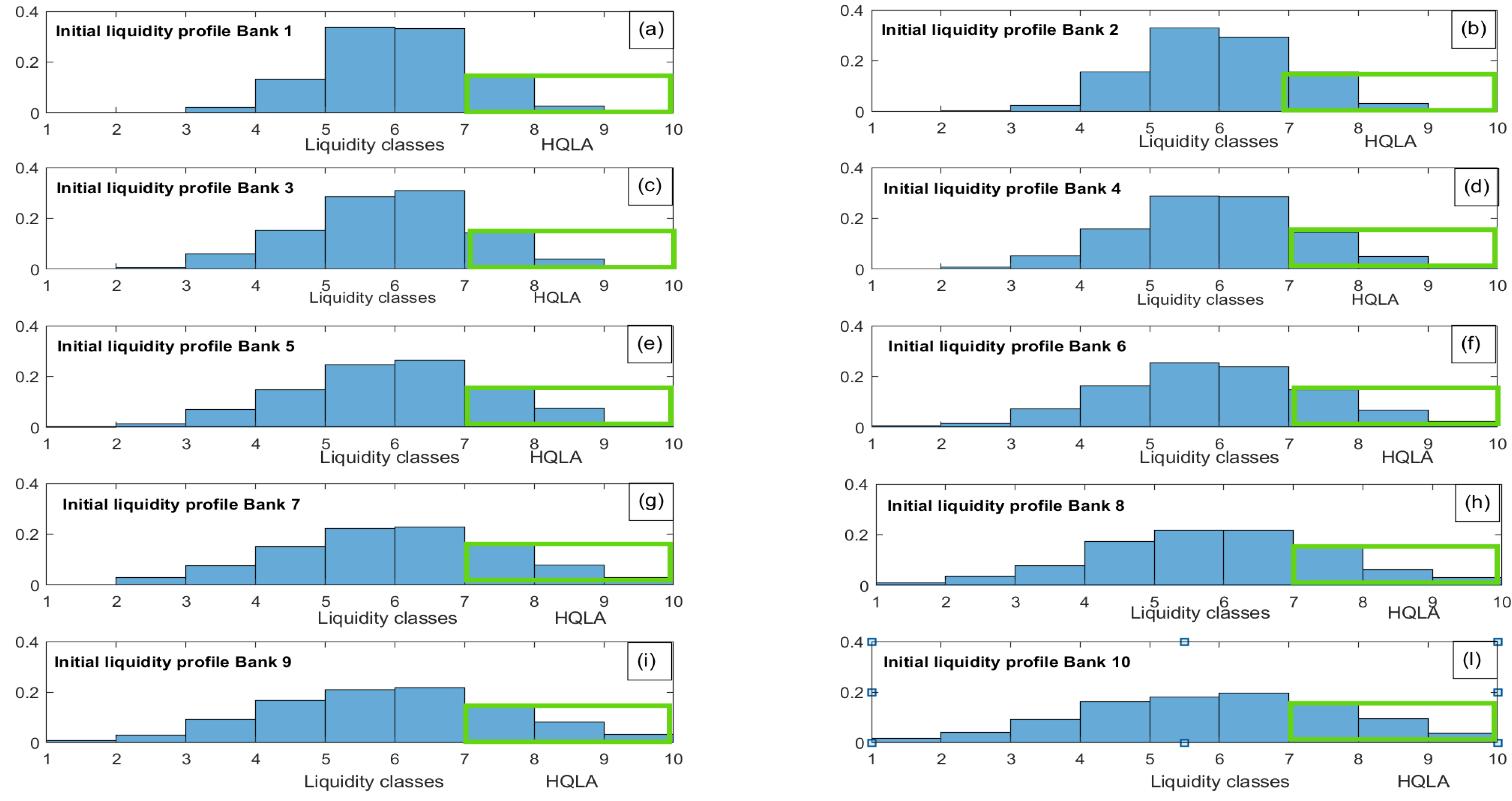

2. Liquidity Profile of Financial Institutions and Regulation Policies for Banks

2.1. Banks’ Assets and Dynamics of Liquidity Profiles

2.2. The Liquidity Coverage Ratio

3. The Model

3.1. The Modelling Framework

3.2. Modelling the Interactions

- Interaction between agents belonging to functional subsystems characterized by the same value for the dummy variable:(either or ):

- Competitive interaction (, ):

- :

- :(the last assumption is mathematically introduced to set properly the interactions at the edges of the domain of the activity variable)

- Cooperative interaction (, ),

- Functional subsystems, that is, the nodes of the network, characterized by the same value for the dummy variable: (either or ) are not linked:representing the fact that no financial transactions possibly determing liquidity dynamics take place.

- Functional subsystems such that competitive interactions between the agents take place (, ) are not linked if the interaction is such that

- , i.e.,and are linked instead if

- , i.e.,:

- Cooperative interaction (, )representing in both cases the fact that there occurs, between involved pair of nodes, a financial transaction possibly inducing liquidity dynamics.

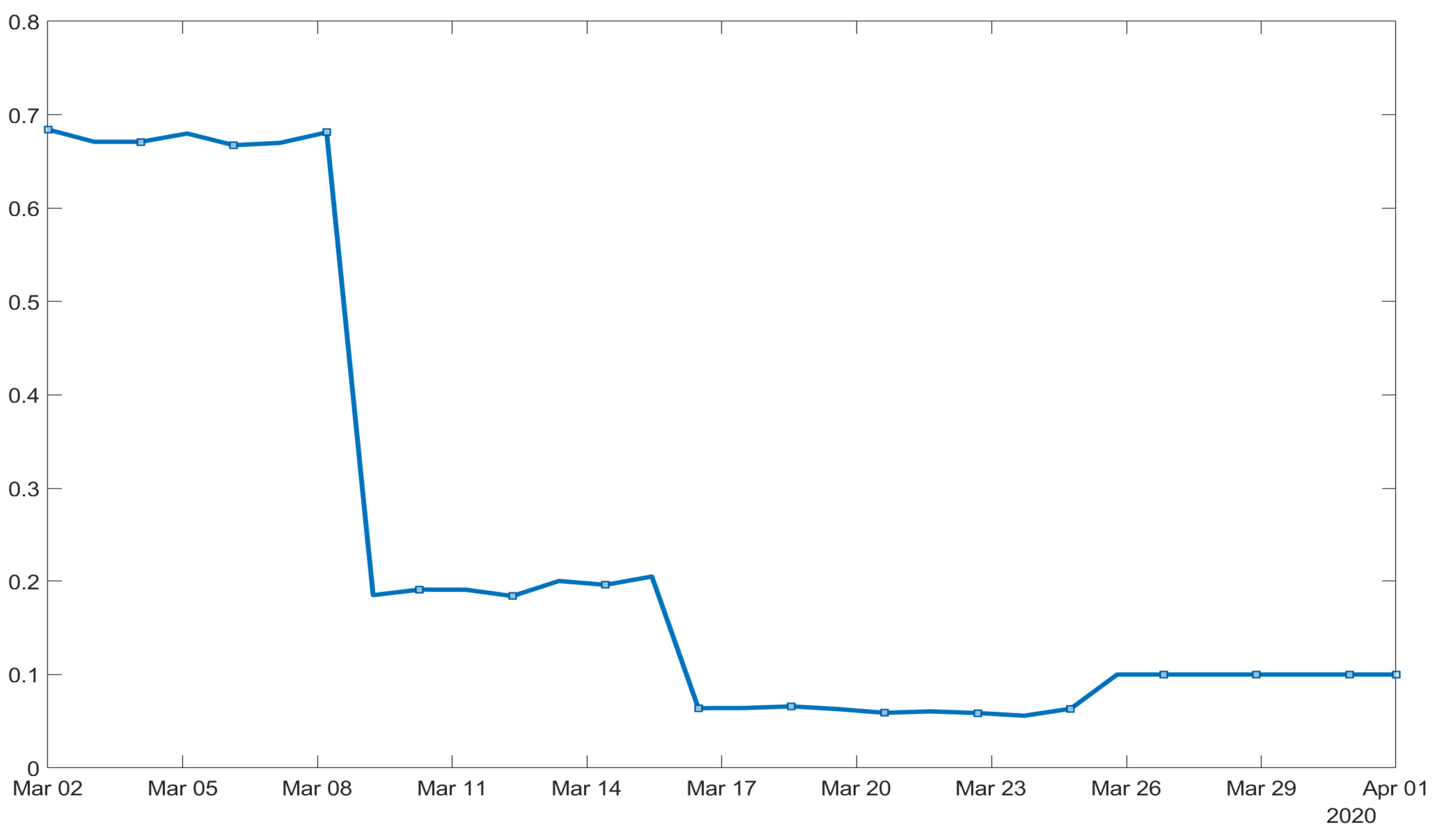

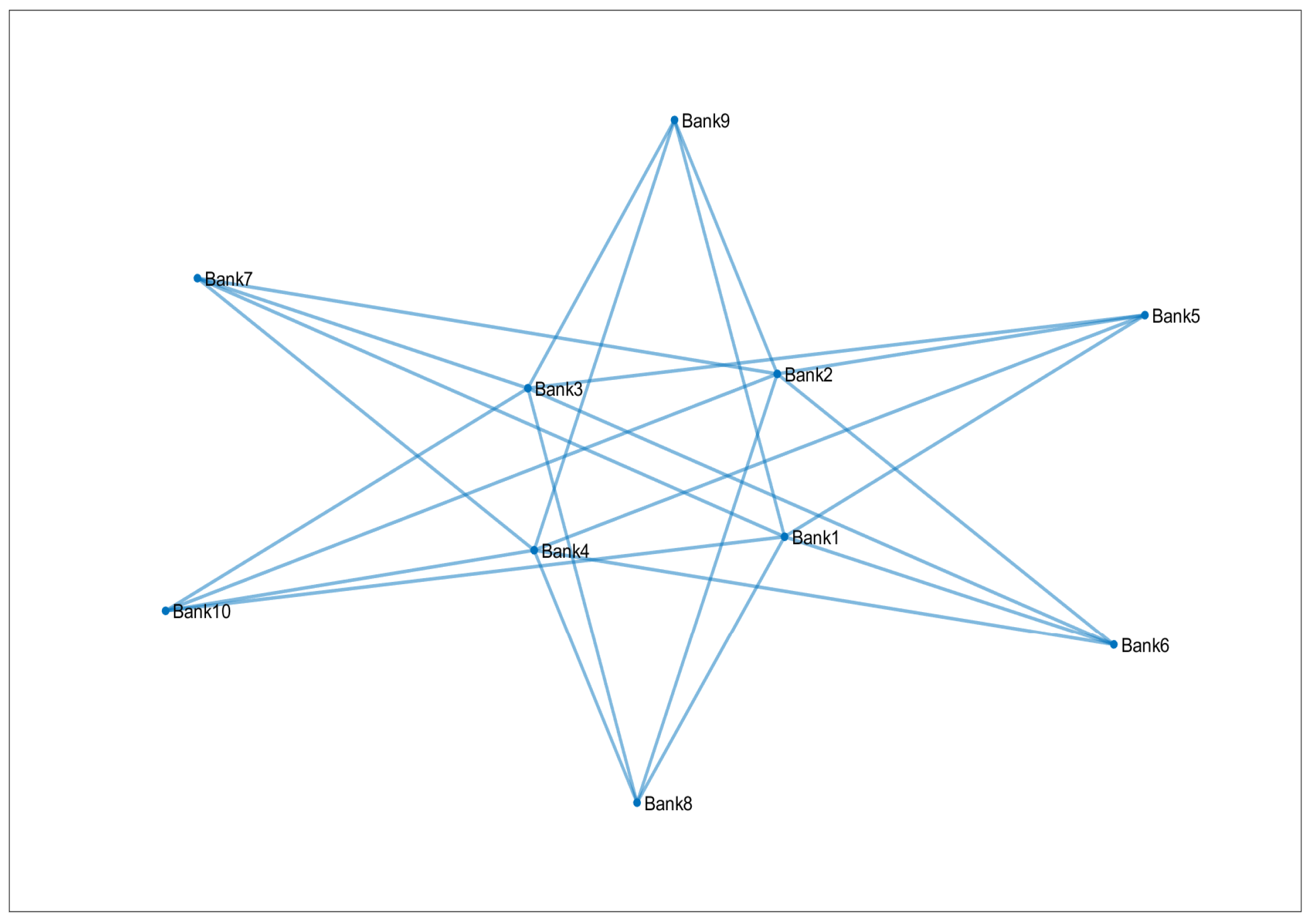

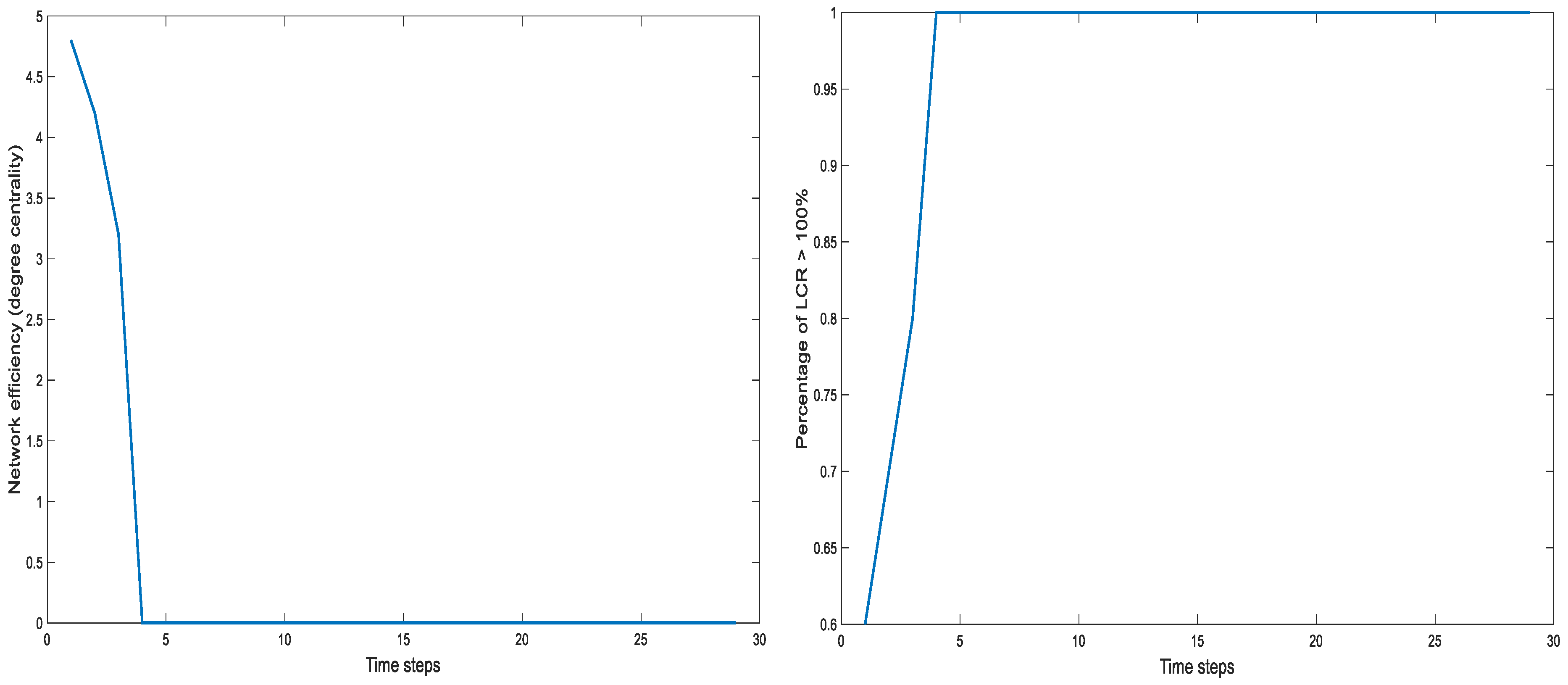

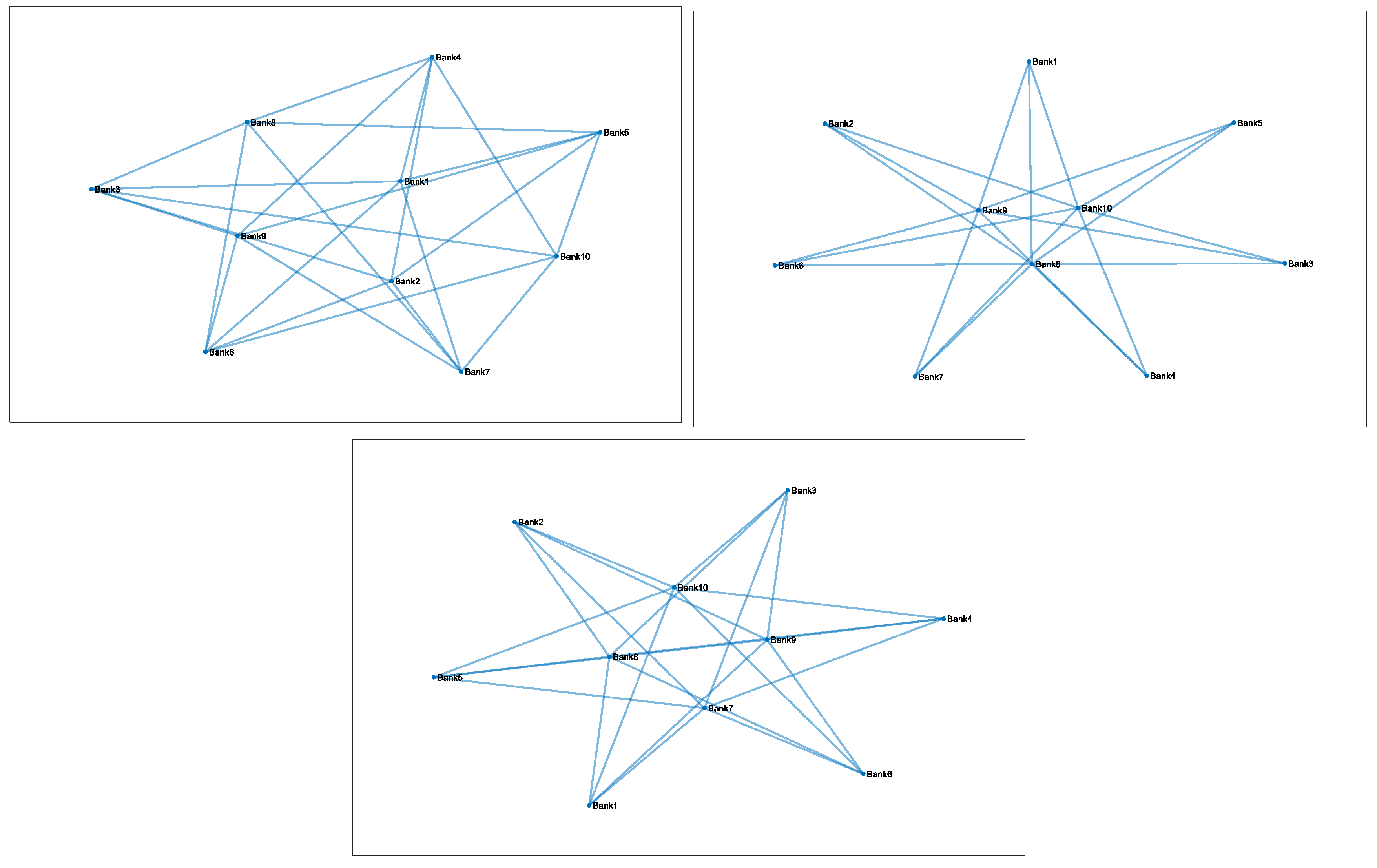

4. Numerical Experiment on Strategic Interbank Network Formation

Case Study II: Penalty for Excesses of Liquidity Reserves

5. Conclusions and Research Perspectives

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

Appendix A. Equilibrium Conditions for the Distribution of High Quality Liquid Assets on the Network

References

- Dolfin, M.; Leonida, L.; Outada, N. Modeling human behavior in economics and social science. Phys. Life Rev. 2017, 22, 1–21. [Google Scholar] [CrossRef] [Green Version]

- Dolfin, M.; Knopoff, D.; Limosani, M.; Xibilia, M.G. Credit risk contagion and systemic risk on networks. Mathematics 2019, 7, 1055. [Google Scholar] [CrossRef] [Green Version]

- Bellomo, N.; Bellouquid, A.; Gibelli, L.; Outada, N. A Quest Towards a Mathematical Theory of Living Systems; Birkhäuser; Springer: New York, NY, USA, 2017. [Google Scholar]

- Ajmone Marsan, G.; Bellomo, N.; Gibelli, L. Stochastic evolutionary differential games toward a systems theory of behavioral social dynamics. Math. Model. Methods Appl. Sci. 2016, 26, 1051–1093. [Google Scholar] [CrossRef]

- Kwon, H.R.; Silva, E.A. Mapping the Landscape of Behavioral Theories: Systematic Literature Review. J. Plan. Lit. 2019, 1051–1093. [Google Scholar] [CrossRef] [Green Version]

- Ball, P. Why Society Is a Complex Matter; Springer: Heidelberg, Germany, 2012. [Google Scholar]

- Burini, D.; De Lillo, S. On the complex interaction between collective learning and social dynamics. Symmetry 2019, 29, 967. [Google Scholar] [CrossRef] [Green Version]

- Lachowicz, M.; Leszczyński, H.; Puźniakowska–Galuch, E. Diffusive and anti-diffusive behavior for kinetic models of opinion dynamics. Symmetry 2019, 11, 1024. [Google Scholar] [CrossRef] [Green Version]

- Dolfin, D.; Leonida, L.; Muzzupappa, E. Forecasting Efficient Risk/Return Frontier for Equity Risk with a KTAP Approach: Case Study in Milan Stock Exchange. Symmetry 2019, 11, 1055. [Google Scholar] [CrossRef] [Green Version]

- Eftimie, R.; Gibelli, L. A kinetic theory approach for modelling tumour and macrophages heterogeneity and plasticity during cancer progression. Math. Model. Methods Appl. Sci. 2020, 30, 659–683. [Google Scholar] [CrossRef]

- Calvo, J.; Nieto, J.; Zagour, M. Kinetic Model for Vehicular Traffic with Continuum Velocity and Mean Field Interactions. Symmetry 2019, 11, 1093. [Google Scholar] [CrossRef] [Green Version]

- Aylaj, B.; Bellomo, N.; Gibelli, L.; Reali, A. On a unified multiscale vision of behavioral crowds. Math. Model. Methods Appl. Sci. 2020, 30, 1–22. [Google Scholar] [CrossRef]

- Bellomo, N.; Gibelli, L.; Outada, N. On the interplay between behavioral dynamics and social interactions in human crowds. Kinet. Relat. Mod. 2019, 12, 397–409. [Google Scholar] [CrossRef] [Green Version]

- Elaiw, A.; Al-Turki, Y.; Alghamdi, M. A critical analysis of behavioural crowd dynamics: From a modelling strategy to kinetic theory methods. Symmetry 2019, 11, 851. [Google Scholar] [CrossRef] [Green Version]

- Kim, D.; Quaini, A. A kinetic theory approach to model pedestrian dynamics in bounded domains with obstacles. Kinet. Relat. Mod. 2019, 12, 1273–1296. [Google Scholar] [CrossRef] [Green Version]

- Knopoff, D.; Nieto, J.; Urrutia, L. Numerical simulation of a multiscale cell motility model based on the kinetic theory of active particles. Symmetry 2019, 11, 1003. [Google Scholar] [CrossRef] [Green Version]

- Lachowicz, M.; Leszczyński, H. Modeling Asymmetric Interactions in Economy. Mathematics 2020, 8, 523. [Google Scholar] [CrossRef] [Green Version]

- Burini, D.; Chouhad, N. A Multiscale view of nonlinear diffusion in biology: from cells to tissues. Math. Model. Methods Appl. Sci. 2019, 11, 967. [Google Scholar] [CrossRef]

- Elaiw, A.; Al-Turki, Y. Particle methods simulations by kinetic theory models of human crowds accounting for stress conditions. Symmetry 2019, 12, 14. [Google Scholar] [CrossRef] [Green Version]

- Ardekani, A.M.; Distinguin, I.; Tarazi, A. Do banks change their liquidity ratios based on network characteristics? Eur. J. Oper. Res. 2020, 285, 789–803. [Google Scholar] [CrossRef]

- Bellomo, N.; Ha, S.-Y.; Outada, N. Towards a Mathematical Theory of Behavioral Swarms. ESAIM Control. Theory Var. Calc. 2020, 26, 125. [Google Scholar] [CrossRef]

- Knopoff, D.; Terna, P.; Secchini, V.; Virgillito, M.E. Cherry picking: consumer choices in swarm dynamics, considering price and quality of goods. Symmetry 2020, 12, 1912. [Google Scholar] [CrossRef]

- Pareschi, L.; Toscani, G. Interacting Multiagent Systems: Kinetic Equations and Monte Carlo Methods; Oxford University Press: Oxford, UK, 2013. [Google Scholar]

- Basel III: The Liquidity Coverage Ratio and Liquidity Risk Monitoring Tools; Bank for International Settlements: Basel, Switzerland, 2013.

- Principles for Sound Liquidity Risk Management and Supervision; Bank for International Settlements: Basel, Switzerland, 2008.

- Bai, J.; Krishnamurthy, A.; Weymuller, C.H. Measuring liquidity mismatch in the banking sector. J. Financ. 2018, LXXIII, 51–92. [Google Scholar] [CrossRef]

- Berger, A.N.; Bouwman, C.H.S. Bank Liquidity Creation and Financial Crises; Academic Press: Amsterdam, The Netherlands, 2015. [Google Scholar]

- Iori, G.; De Masi, G.; Precup, O.V.; Gabbi, G.; Caldarelli, G. A network analysis of the Italian overnight money market. J. Econ. Dyn. Control 2008, 32, 259–278. [Google Scholar] [CrossRef]

- Haldane, A. Rethinking the Financial Network, Speech by Mr Andrew G Haldane at at the Financial Student Association, Amsterdam, 28 April 2009. Available online: https://www.bis.org/review/r090505e.pdf (accessed on 26 November 2020).

- Stiglitz, J.E. The contributions of the economics of information to twentieth century economics. Q. J. Econ. 2000, 115, 1441–1478. [Google Scholar] [CrossRef]

- Schweitzer, F.; Fagiolo, G.; Sornette, D.; Vega-Redondo, F.; Vespignani, A.; White, D.R. Economic networks: the New Challenges. Science 2009, 325, 422–425. [Google Scholar] [CrossRef]

- Jackson, M.O. Social and Economic Networks; Princeton University Press: Princeton, NJ, USA; Oxford, UK, 2008. [Google Scholar]

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Dolfin, M.; Leonida, L.; Muzzupappa, E. A Kinetic Theory Model of the Dynamics of Liquidity Profiles on Interbank Networks. Symmetry 2021, 13, 363. https://doi.org/10.3390/sym13020363

Dolfin M, Leonida L, Muzzupappa E. A Kinetic Theory Model of the Dynamics of Liquidity Profiles on Interbank Networks. Symmetry. 2021; 13(2):363. https://doi.org/10.3390/sym13020363

Chicago/Turabian StyleDolfin, Marina, Leone Leonida, and Eleonora Muzzupappa. 2021. "A Kinetic Theory Model of the Dynamics of Liquidity Profiles on Interbank Networks" Symmetry 13, no. 2: 363. https://doi.org/10.3390/sym13020363