1. Introduction

The classical stochastic volatility diffusion models such as [

1,

2] have played an important role in volatility modelling specifically to match for the smile or skew effect (variation of implied volatility with respect to strike price) as displayed in the empirical implied volatility [

3]. However, the shortcoming of using these stochastic volatility models is their inability o generate reasonable shape for the term-structure (variation of implied volatility with respect to maturity time) in the implied volatility. Generally speaking, the classical stochastic volatility diffusion models have a skew slope of

, whereas the implied volatility based on empirical observations has a skew slope of

[

4,

5,

6] with

as the time to maturity, therefore they are not compatible as market models. In response to the shortcoming, the stochastic volatility jump diffusion models such as Bates model [

7] were also introduced to fit the empirical short-time skew. Moderate but insufficient improvement was made to the problem by using the stochastic volatility jump diffusion model.

Recently, the academic contribution by [

8] enables us to price assets accurately by considering rough volatility in our framework. The term “rough volatility” indicates that the volatility term is driven by fractional Brownian motion (fBm) [

9] with Hurst exponent of

, where

H controls the roughness of the fBm (the lower the

H, the rougher the trajectories of fBm). Intuitively, the term “rough volatility” came from its roughness behavior or anti-persistency effect. Accordingly, the empirical findings made by [

8] were possible due to the contribution from [

10], where the author has displayed that the volatility in stochastic volatility model driven by the fractional Brownian motion with Hurst exponent

H is capable of generating an at-the-money volatility skew of the form

for small

time. This subsequently motivated the authors of [

8] to model volatility using fBm with Hurst parameter of

. Prior to the discovery, we wish to note that there is a good attempt made by [

11]. In particular, the authors utilized Malliavin calculus techniques to obtain the short-time behavior of at-the-money implied volatility skew for the generalization of Bates model and subsequently, considered fractional stochastic volatility models that included the case of Hurst parameter

which is capable of capturing the short-time behavior of skew slopes similar to those displayed in the financial market. Furthermore, before the use of rough volatility (fractional Brownian motion with Hurst parameter

), authors of [

12] have proposed the fractional stochastic volatility model with Hurst parameter of

, where it intends to capture the long memory effect displayed by the assets movement in the financial market. Subsequently, the stochastic volatility model with mixed fractional Brownian motion [

13] was also proposed as an attempt to model assets movement better.

After the discovery of rough volatility, rough Heston model and its characteristic function have been proposed and derived in [

14] by continuing the work of [

15] where they have found that microscopic model for the price of an asset with leverage effect follows the rough Heston model. Coincidentally, it is found that the classical Riccati equation in the classical Heston model [

2] has been replaced with fractional Riccati equation in the rough Heston model. Unlike the classical version of Riccati equation where the exact solution exists and the solution for the classical Heston can be obtained easily in an efficient manner, there is no explicit-form solution for the fractional Riccati equation as of now. This poses a huge disadvantage to use the rough Heston model for obtaining the call option price as we have to rely on numerical methods now. Unfortunately, it is also noted that to acquire an accurate solution, the computational costs originated from the lack of an explicit solution for the fractional Riccati equation which is a part of the characteristic function of the rough Heston model. It can be seen as a huge sacrifice for the sake of incorporating rough volatility in its framework.

Besides the direct confrontation on the computation of rough Heston model using Fourier-type method, it is possible to use hybrid Brownian semistationary (BSS) method [

16] as an efficient simulation method. In particular, the method involves the usage of appropriate power function to approximate when the kernel function near zero and Riemann-sum discretization elsewhere. It is found that the hybrid BSS scheme is able to reproduce the fine properties of rough Brownian semistationary process, but practical implementation remains hard. A variance reduction technique [

17] took advantage of the hybrid BSS scheme for obtaining the solution of the rough Bergomi model. Furthermore, authors of [

18] have proposed a multifactor approximation method for the fractional Riccati equation. The specification of the method involves approximating fractional Riccati equation using a

n-dimensional classical Riccati equation with large

n (up to

). A similar time-efficiency method is suggested in [

19] with satisfactory results for the fits to the implied volatility smiles for short maturities with lesser parameters. [

20] managed to approximate the rough Heston model by using scaled “volatility of volatility” parameter in the classical Heston model. The method is somewhat extremely fast to calibrate (follows the time complexity of classical Heston model) with satisfactory accuracy. Besides that, [

21] used a hybrid method that involves the Richardson–Romberg extrapolation method to approximate outside of convergence domain and a short-time series expansion. The authors noted that the hybrid method is both efficient and flexible.

Although it has only been recently discovered that the solution to the fractional Riccati equation is essential for the pricing call option, it has actually been studied extensively for general purposes by many researchers in the past. We first mention two of the most famous methods which are the Adomian decomposition method [

22] and the variational iteration method [

23]. Homotopy perturbation method [

24] and homotopy analysis method [

25] remain popular choices for approximating the analytical solutions. Other methods on approximating fractional Riccati equation include [

26,

27].

The usual algorithm dealing with fractional order differential equation is obtained by using the fractional Adams–Bashforth–Moulton method [

28]. The error analysis is also provided in the paper. We refer to the fractional Adams–Bashforth–Moulton method as fractional Adams method from now onwards. It is noted that [

14] has also demonstrated the use of fractional Adams method in its numerical application section for the rough Heston model. Although it is capable of providing extremely well solution with large time steps, the algorithm complexity to evaluate a call option is at

where the

is the number of space steps used for Fourier-type method and

n is the number of time steps for the fractional Adams method. The sole complexity of the algorithm makes the computation of the call option to a certain accuracy not feasible to most practitioners. We will take advantage of this method by setting a high number of time steps to compare our numerical solution later in this paper.

In this paper, we will also focus heavily on the work of [

29] where it uses multipoint Padé approximants on the asymptotical solutions (

and

) of the fractional Riccati equation and applying it to the rough Heston model. This is needed as the typical method (fractional Adams method) requires great computational effort, i.e., not feasible to most practitioners or perhaps even researchers. Before that, we wish to discuss some of the general aspects and history of Padé approximation method. Specifically, it was developed by Henri Padé in the 1890s with the constructing idea credited to Georg Frobenius where he investigated the usage of rational approximations of the power series. Coincidentally, Padé approximation turns out to be a great approximation to many application in physics, e.g., nuclear physics [

30], kinetic electron model [

31], quantum resonances [

32] and many more [

33]. We follow closely on the literature from [

29], we note that the theory of convergence of Padé approximants can be found in [

34]. Also, as noted in [

33], one of the theorems (Montessus de Ballore’s theorem) states that if

f is analytical in a ball centered at zero except for multiples of

n, the sequence of

for a fixed

n, converges uniformly to

f in compact subsets omitting the poles.

Furthermore, since we are dealing with

diagonal Padé approximants for our fractional Riccati equation later on, it is only fair that we mention its convergence properties too. As noted in [

35], Baker–Gammel–Wills conjecture speculates that under some certain condition, the

diagonal Padé approximant

converges uniformly to

f. Taken from [

34], a counterexample for the Baker–Gammel–Wills conjecture is provided. Consequently, Nutall–Pommerenke’s theorem is provided where it states that there exists a subsequence of

where it converges almost everywhere. Coupled with Monstessus de Ballor’s theorem, we should be extremely careful when dealing with

diagonal Padé approximant in our work. One of the functions we will mention later is the Mittag–Leffler function

. The uniform convergence of Mittag–Leffler function has been proven in [

36] on the compact set

. However, it is not necessarily compatible with the asymptotic behavior of the Mittag–Leffler function for large

t, although it performs better than their corresponding truncated Taylor series.

We now move to the discussion on the multipoint Padé approximation method. The method was originally derived in [

37] as a global rational approximant. As mentioned previously, it aims to match asymptotical points of

f using

Padé approximant. In addition, it has been successfully applied to both the Mittag–Leffler function [

38] and generalized Mittag–Leffler function [

39]. The authors of [

29] demonstrated the use of global rational approximations for the fractional Riccati equation and found the excellent performance of the multipoint Padé approximation

especially when

H is close to 0. However, the imaginary part of the solution deteriorates as

or

. This poses a challenge in terms of accuracy of the model and it would be erroneous to employ the same method to approximate the solution for the fractional Riccati equation when

H is somewhat near

. In addition, we take a step further to investigate the accuracy of

for small

u values as it plays an important role for the computation of option price. Consequently, we further confirm that the multipoint Padé (3,3) approximation method performs incredibly well at small

u values as compared to fractional Adams method, thereby enabling practitioners to price their options using a low computational cost method with similar accuracy.

Organization of the Paper

We have provided a short introduction to the Riemann–Liouville fractional calculus in the

Appendix A and Mittag–Leffler function in

Appendix B as preliminaries for interested readers. Furthermore, we intend to organize our paper as following:

Section 2: Fractional Adams–Bashforth–Moulton method and its error analysis.

Section 3: Black Scholes equation, implied volatility, classical Heston, rough Heston model, their characteristic functions and their connection to call option pricing.

Section 4: Small and long time expansion of solution for the fractional Riccati equation.

Section 5: Padé, multipoint Padé approximation method and its application to the asymptotical solutions of the fractional Riccati equation.

Section 6: Numerical experiments and performances.

5. Multipoint Padé Approximation Method for Fractional Riccati Equation

As we have mentioned before, the main issue for the rough Heston model is at its high computational cost. Coupled with fractional Adams method, in order to compute for the option price, a computation complexity of

is needed, where

is the number of space steps for Equation (

28) and

N arises from the use of fractional Adams method noted in

Section 2. One of the important advancements for rough Heston model belongs to the use of multipoint Padé method for obtaining the fractional Riccati equation’s solution at

complexity. This is a huge leap in computational aspect as [

29] has shown virtually that

20,000 would result to a satisfactory solution indifferent from the

50,000 case. By employing the multipoint Padé method, the computational complexity of the evaluation for option price using Equation (

28) reduces to only

, the same as the case of the classical Heston model.

We first introduce the work of [

38] which concerns with the global rational approximation on

:

where

and we make the substitution

on both Equations (

29) and (

36). Based on the argument for [

29], we note that only diagonal Padé approximation is admissible. This is due to the fact when

, Padé approximation should approach as following

where

only if

. Notice that if

and

,

will either not admit constant other than zero or does not exist (involves

∞ or

. Furthermore, Equation (

41) corresponds to an assumption we made at

Section 4.2. The possibilities of choosing

equals to some constant is endless. However, the authors [

29] have noted that

and

do not perform well for the fractional Riccati equation case. Fortunately, the case

does produce excellent quality of solution for the fractional Riccati equation, at least for the

solution. Therefore, we will work out the case for multipoint Padé approximation method for

in this section. When we mention multipoint Padé approximation method, we intend to refer it as multipoint Padé approximation method using

for the rest of the discussion in this paper. We follow closely from the presentation of [

29] on this section.

Remember that we have set

for the rest of our discussion. Suppose that from Equation (

29), we obtain the small time expansion in the form of

and from Equation (

36), we have the series expansion for small time on the solution of fractional Riccati equation as

The Padé

approximation can be written as

with

set to 1. Matching the coefficients to Equations (

29) and (

36) using Padé approximation method, we have the system of equations as

Accordingly, we obtain the constants

as

Note that the solutions can be easily obtained using solve function in MATLAB in less than one second. Now that we have the required multipoint Padé method, it is time we test it against the general approach (fractional Adams method).

6. Numerical Experiment And Performances

In the previous sections, we have demonstrated the fractional Adams method and the multipoint Padé approximation method. Therefore, it is time that we conduct some numerical experiment on the fractional Riccati equation. In particular, we have decided to compare the result of the fractional Riccati equation using fractional Adams method and the multipoint Padé approximation on a different scale of the Hurst parameter H.

The parameters used in our numerical studies are as following unless specifically stated otherwise:

where

N belongs to the time steps of fractional Adams method. Although we have given the

value, note that if we use

x in

as a substitute of

and

t for the fractional Adams method and multipoint Padé method, we will not directly be affected by the value

is computation for the plotting of

and

x.

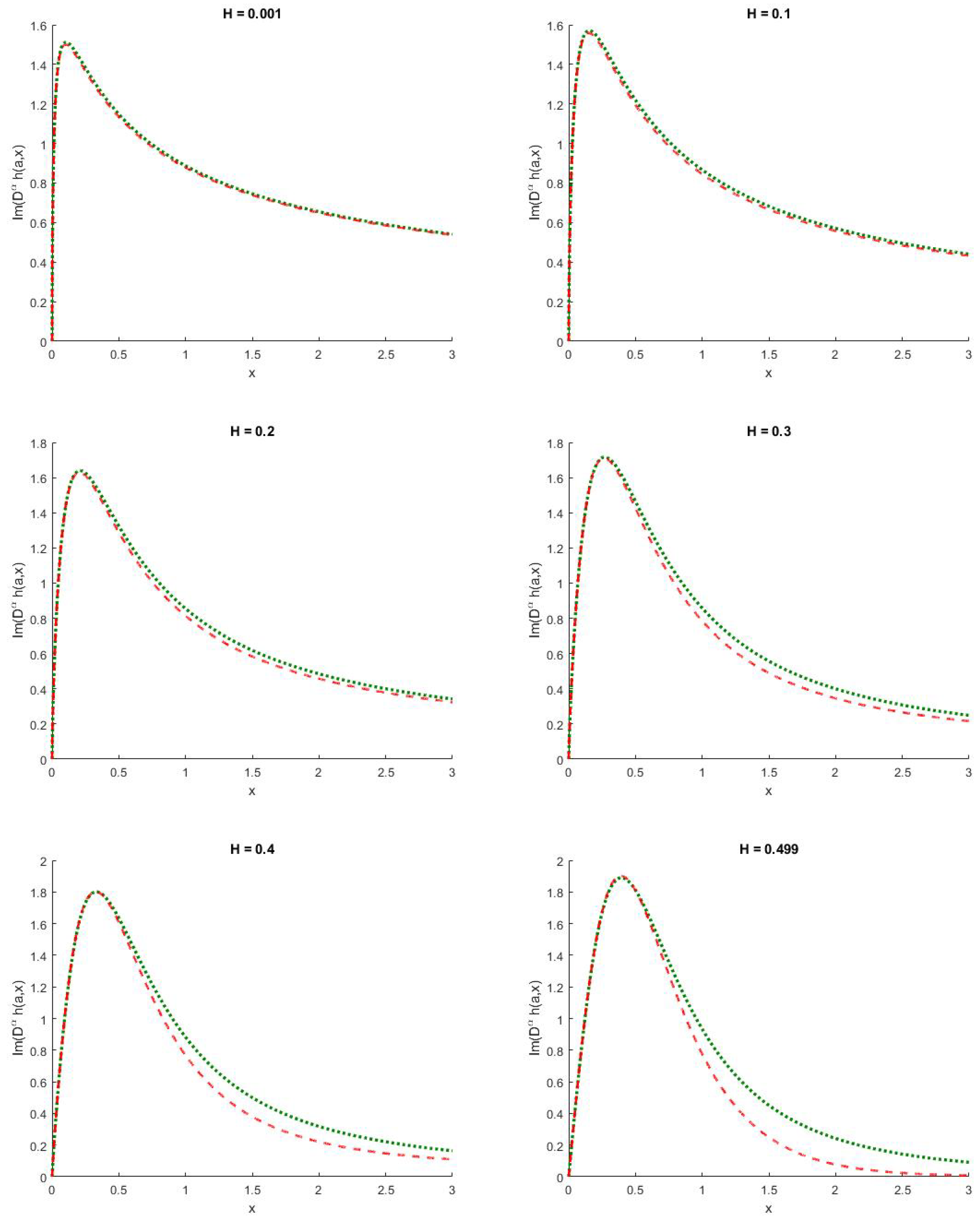

For perspective, we first display the Re

for

and

in

Figure 1. Notice that the solution for the real part of the

performs extremely well for small

H and moderate for

. The following observation is taken from [

29]. In particular, the deterioration effect is deeply enlarged when we observe for the imaginary part of

as seen in

Figure 2. This in turn would provide an erroneous result for the option price if not fixed. In general, the performance of multipoint Padé approximation method should not be too surprising as we have matched on only two points which are

and

. Supposedly, we should also understand the importance of smaller

u values in

from Equation (

28), smaller

u values have higher contribution to the computation of the call option price due to the

term in the integral. In the subsequent part of this section, we will evaluate

in a more robust setting which concerns the choices of

u values at an overall scale of Hurst parameter

H. We first introduce some of the notations for the purpose of computing errors.

We start with the Euclidean Norm Distance of the fractional Riccati equation’s solution:

and the percentage error of the fractional Riccati equation’s solution:

where

u is our parameter of this study,

is the imaginary number,

is the multipoint Padé (3,3) approximation at time

and

is the solution at time

generated from the fractional Adams method using parameters in Equation (

46) with a slight modification of

such that

(we generate step size of

). We find that

is a sufficient time steps for fractional Adams method with reasonable computing time.

is from Equation (

27) and note that

with

H as the Hurst parameter. Furthermore, Re

and Im

denote the real part and imaginary part of the solution. Equations (

47) and (48) give an overall error computation of fractional Riccati equation’s solution using the multipoint Padé approximation method at different time

up to

, whereas Equations (

49) and (50). Furthermore, in order to evaluate the quality of

solution over different values of the Hurst parameter

H, we have decided to iterate through different

H for our study. Suppose we introduce

to achieve our final numerical computation result as follows:

where we iterate through

(we have decided to let the last

H value to be 0.499 instead of 0.5). Consequently, from

Table 1, we can observe that multipoint Padé approximation method does a great job in obtaining solution for various

u values. Notably,

and

both have incredibly low values especially at

with virtually no errors. This is significant as it is what we needed—an accurate

solution at low

u values. Besides, we wish to emphasize that the large errors were made by the multipoint Padé approximation method when

whereas the market estimated Hurst parameter

H values are around 0.1 [

8,

20]. As such, multipoint Padé approximation method would be able to perform extremely well with low computing cost. Out of the ordinary,

and

appear to be large across the values of

u in

Table 1, and upon investigation this is due to the fact that Re(

) and Im(

) tend to approach zero as

during the computation, therefore incurring large percentage error. This is further verified by the consistent low

and

values. In short, the multipoint Padé approximation method performs similarly to the fractional Adams method in low computational errors manner while still retaining the low computational cost advantage.

7. Concluding Remarks

First of all, we have provided the brief history and literature review for the general stochastic volatility model, rough volatility, rough Heston model and ways to obtain solution for the rough Heston model. In particular, a large part of the literature review is dedicated to numerical methods of solving for the fractional Riccati equation where it can be used to obtain the option prices. Note that the introductory level of the fractional calculus and Mittag–Leffler function are located in the appendix for interested readers. They are subsequently used in describing the dynamics of rough Heston model and represented as the solution of fractional Riccati equation. Later, the fractional Adams–Bashforth–Moulton method and its error analysis are provided. The fractional Adams method still remains a classical and frequently used method of solving any fractional ordinary differential equation. Unfortunately, the fractional Adams method typically requires a large number of time steps which in turn requires large computational cost. But before that, we have introduced some recent advancements in the option pricing theory. Classical Black–Scholes option pricing models, classical Heston model, and the newly rough Heston models have been discussed subsequently. In addition, we gave a slight touch on the implied volatility topic in case readers are keen on testing the models on real data. Furthermore, the characteristic functions and their inversions to the option prices were given. Since the multipoint Padé approximation method requires some expansion on multiple points for matching purposes, we introduce some literature on the small and large time expansion of the solution of the fractional Riccati equation which is being used in the characteristic function of rough Heston model. We later then discuss the required multipoint Padé method

, as suggested by some authors, in a great effort of using the small and large time expansion to obtain the solution on fractional Riccati equation. Finally, we test the multipoint Padé

method on a setting and compare it with the fractional Adams method. Lastly, we have further investigated the possible outcomes on

u values in

, which is the key component in Equation (

28). Consequently, the errors computation of different

u values in

further agrees that multipoint Padé

approximation method performs extremely consistent with the fractional Adams method. This enables practitioners to price their options with reasonable confidence such that the solution to fractional Riccati equation obtained using multipoint Padé

approximation method will be identical to the ones produced by the fractional Adams method, while enjoying the benefit of low computational cost. Accordingly, what we have found coincides with the previous authors such that multipoint Padé method

performed extremely well with

but not the

case. Above all, we wish to make a minor recommendation on this issue—since the solution for the classical Riccati equation or fractional Riccati equation with

exists, in our opinion, we believe it is possible for an attempt of using a hybrid model between the existing multipoint Padé method and the exact solution for the classical Riccati equation. An attempt to match it at

and

would result in a more robust setting and applicable to altering volatility behavior.

{kind=link}

{kind=link}