Green Buildings in Singapore; Analyzing a Frontrunner’s Sectoral Innovation System

Abstract

:1. Introduction

2. Background

2.1. Green Buildings

- Improved glass insulation to reduce solar heating through windows;

- Increased natural light, energy efficient lighting devices, and equipment to control lighting;

- Energy efficient cooling plants and ventilation systems for air conditioning;

- Building management systems to monitor and control equipment and optimize energy use; and

- The use of photovoltaic cells [7].

2.2. Promoting Energy Transition in the Building Sector

2.3. Green Building Rating Tools around the World

2.4. Green Building Rating Tools in Singapore

- It places greater emphasis on energy efficiency;

- It has been tailored for a tropical climate with the cooling of inner spaces using air-conditioning as a key consideration; and

- It has higher standards of measurement and verification, using more precise instruments to monitor equipment performance [47].

2.5. Promoting Energy Transition in the Singaporean Building Sector

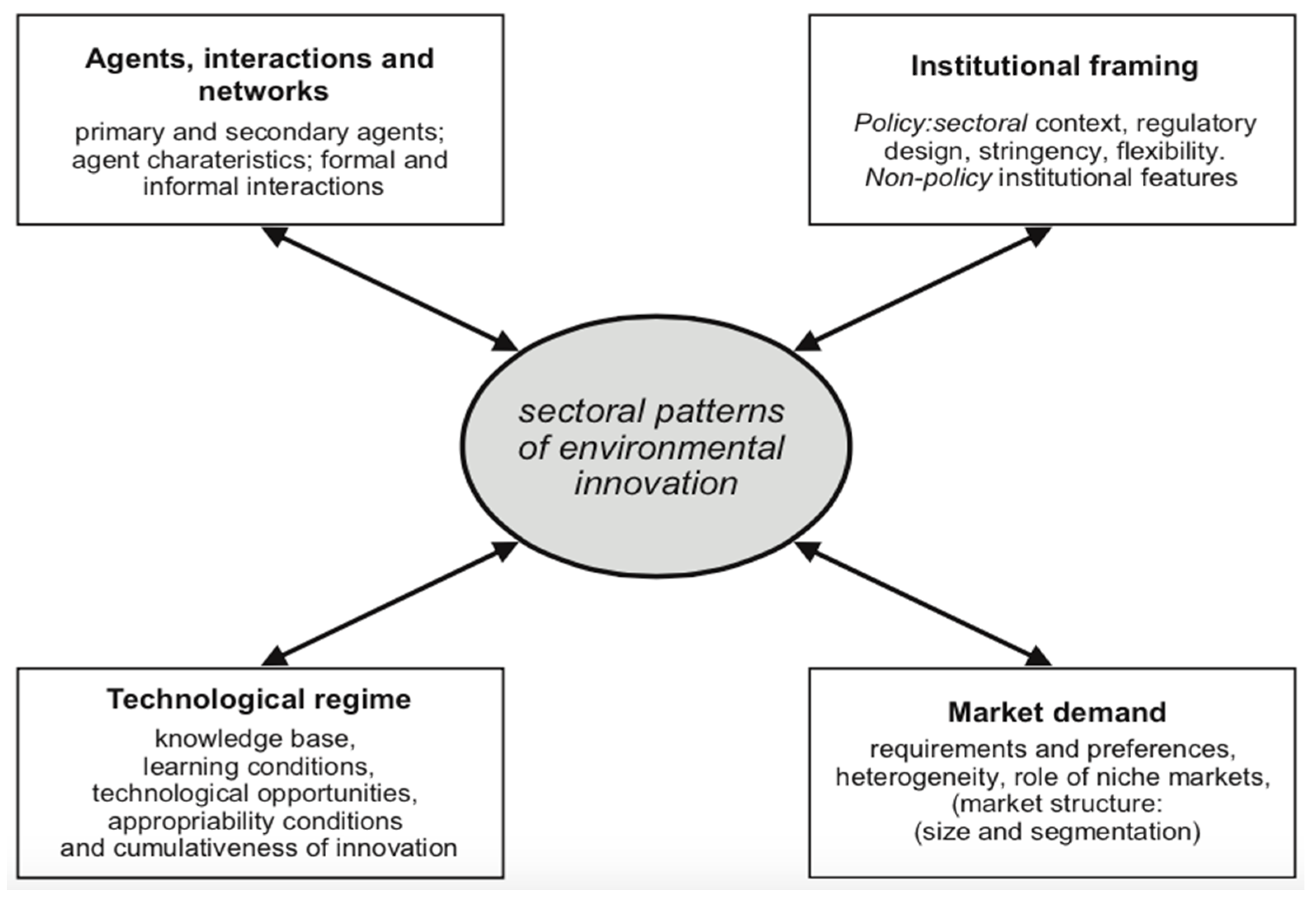

3. Sectoral Innovation Systems

3.1. Technological Regime

- Technology: This refers to the new technologies available, the economic feasibility of these new technologies, and the extent to which implementing these new technologies was successful.

- Complementarities and interdependencies: This refers to whether new technology complements or replaces existing technology, and whether any technology is interdependent on another technology. This could be due to the convergence of previously separate products or the emergence of new demand from existing demand.

- Knowledge base: This refers to the extent of knowledge and the methods by which knowledge is disseminated and communicated.

- Learning conditions: This refers to both the internal and external learning processes, and opportunities.

3.2. Market Demand

3.3. Agents, Interactions and Networks

3.4. Institutional Framework

4. Methods

4.1. Data Collection

4.2. Data Analysis

5. Results

5.1. Technological Regime

5.1.1. Technology

5.1.2. Complementarities and Interdependencies

5.1.3. Knowledge Base

5.1.4. Learning Process

5.2. Market Demand

5.3. Actors, Interactions, and Networks

5.3.1. Actors

5.3.2. Actor Interactions and Networks

5.4. Institutional Framework

5.4.1. Formal Institutions

5.4.2. Informal Institutions

6. Discussion

7. Conclusions

Acknowledgments

Author Contributions

Conflicts of Interest

Appendix A

{kind=link}

| Aspect of SIS | Primary Agents | Secondary Agents |

|---|---|---|

| Technological Regime | Technology

After a project has been completed, whether successfully or not (e.g., the erection of a green building tower)

| Technology

After a project has been completed, whether successfully or not (e.g., the erection of a green building tower)

|

| Market Demand |

|

|

| Agents, interaction and networks | Actors

| Actors

|

| Institutional Framework | Policy

| Policy

|

References

- EIA. U.S. Energy Information Administration—EIA—Independent Statistics and Analysis; U.S. Energy Information Administration—EIA: Washington, DC, USA, 2013.

- Bank, W. Urban Population (% of total); World Bank: Washington, DC, USA, 2013. [Google Scholar]

- BCA. BCA Building Energy Benchmarking Report 2014; Building Construction Agency: Singapore, 2014.

- BCA. Annual Report 2012: Redefining the Built Environment and Industry; Building Construction Authority: Singapore, 2013.

- BCA. Build Green, 2015. Available online: https://www.bca.gov.sg/Publications/BuildGreen/others/BGreen_7_2015.pdf (accessed on 19 May 2017).

- Howe, J.C. Overview of Green Buildings. Available online: https://sallan.org/pdf-docs/CHOWE_GreenBuildLaw.pdf (accessed on 19 May 2017).

- BCA. Singapore: Leading the Way of Green Buildings in the Tropics; Building Construction Authority: Singapore, 2013.

- Bartholomew, S. National systems of biotechnology innovation: Complex interdependence in the global system. J. Int. Bus. Stud. 1997, 28, 241–266. [Google Scholar] [CrossRef]

- Bossink, B.A. Assessment of a national system of sustainable innovation in residential construction: A case study from The Netherlands. Int. J. Environ. Technol. Manag. 2009, 10, 371–381. [Google Scholar] [CrossRef]

- Bossink, B.A. Managing drivers of innovation in construction networks. J. Constr. Eng. Manag. 2004, 130, 337–345. [Google Scholar] [CrossRef]

- Bossink, B.A. Demonstration projects for diffusion of clean technological innovation: A review. Clean Technol. Environ. Policy 2015, 17, 1409–1427. [Google Scholar] [CrossRef]

- Albino, V.; Berardi, U. Green buildings and organizational changes in Italian case studies. Bus. Strategy Environ. 2012, 21, 387–400. [Google Scholar] [CrossRef]

- Butera, F.M. Climatic change and the built environment. Adv. Build. Energy Res. 2010, 4, 45–75. [Google Scholar] [CrossRef]

- Xu, L.; Zhou, B.; Wang, C. Research on Design Technology of Green Building for Environmental Protection. Available online: https://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=1&ved=0ahUKEwiyrdDM34fUAhWQJFAKHSSoB74QFggiMAA&url=http%3A%2F%2Fwww.atlantis-press.com%2Fphp%2Fdownload_paper.php%3Fid%3D18006&usg=AFQjCNH5YrueJlza1iIFbq9coaMKUvpjBw&cad=rjt (accessed on 19 May 2017).

- Svenfelt, Å.; Engström, R.; Svane, Ö. Decreasing energy use in buildings by 50% by 2050—A backcasting study using stakeholder groups. Technol. Forecast. Soc. Chang. 2011, 78, 785–796. [Google Scholar] [CrossRef]

- Ries, R.; Bilec, M.M.; Gokhan, N.M.; Needy, K.L. The economic benefits of green buildings: A comprehensive case study. Eng. Econ. 2006, 51, 259–295. [Google Scholar] [CrossRef]

- Von Paumgartten, P. The business case for high performance green buildings: Sustainability and its financial impact. J. Facil. Manag. 2003, 2, 26–34. [Google Scholar] [CrossRef]

- Heerwagen, J.; Zagreus, L. The Human Factors of Sustainable Building Design: Post Occupancy Evaluation of the Philip Merrill Environmental Center; The Center for the Built Environment: Berkeley, CA, USA, 2005. [Google Scholar]

- Hoffman, J.A.; Henn, R. Overcoming the social and psychological barriers to green building. Organ. Environ. 2008, 21, 390–419. [Google Scholar] [CrossRef]

- Vermeulen, W.J.; Hovens, J. Competing explanations for adopting energy innovations for new office buildings. Energy Policy 2006, 34, 2719–2735. [Google Scholar] [CrossRef]

- Faber, A.; Hoppe, T. Co-constructing a sustainable built environment in the Netherlands—Dynamics and opportunities in an environmental sectoral innovation system. Energy Policy 2013, 52, 628–638. [Google Scholar] [CrossRef]

- Darko, A.; Chan, A.P. Review of Barriers to Green Building Adoption. Sustain. Dev. 2016. [CrossRef]

- Zuo, J.; Zhao, Z.-Y. Green building research–current status and future agenda: A review. Renew. Sustain. Energy Rev. 2014, 30, 271–281. [Google Scholar] [CrossRef]

- Hwang, G.B.; Tan, J.S. Green building project management: Obstacles and solutions for sustainable development. Sustain. Dev. 2012, 20, 335–349. [Google Scholar] [CrossRef]

- Häkkinen, T.; Belloni, K. Barriers and drivers for sustainable building. Build. Res. Inf. 2011, 39, 239–255. [Google Scholar] [CrossRef]

- Gluch, P. Building Green-Perspectives on Environmental Mangagement in Construction. Ph.D. Thesis, Chalmers University of Technology, Gothenburg, Sweden, June 2005. [Google Scholar]

- Pinkse, J.; Dommisse, M. Overcoming barriers to sustainability: An explanation of residential builders’ reluctance to adopt clean technologies. Bus. Strategy Environ. 2009, 18, 515–527. [Google Scholar] [CrossRef]

- Shields, R.; Manseau, A. Building Tomorrow: Innovation in Construction and Engineering; Ashgate: Aldershot Hants, UK, 2005. [Google Scholar]

- Williams, K.; Dair, C. What is stopping sustainable building in England? Barriers experienced by stakeholders in delivering sustainable developments. Sustain. Dev. Bradf. 2007, 15, 135. [Google Scholar]

- Anumba, C.; Ren, Z.; Ugwu, O. Agents and Multi-Agent Systems in Construction; Routledge: Abingdon, UK, 2007. [Google Scholar]

- Berardi, U. Stakeholders’ Influence on the adoption of energy-saving technologies in Italian homes. Energy Policy 2013, 60, 520–530. [Google Scholar] [CrossRef]

- Hoppe, T. Adoption of Innovative Energy Systems in Social Housing; Lessons from eight Large-Scale Renovation Projects in the Netherlands. Energy Policy 2012, 51, 791–801. [Google Scholar] [CrossRef]

- Howarth, B.R.; Andersson, B. Market barriers to energy efficiency. Energy Econ. 1993, 15, 262–272. [Google Scholar] [CrossRef]

- Son, H.; Kim, C.; Chong, W.K.; Chou, J.S. Implementing sustainable development in the construction industry: Constructors’ perspectives in the US and Korea. Sustain. Dev. 2011, 19, 337–347. [Google Scholar] [CrossRef]

- DeCanio, S.J. The efficiency paradox: Bureaucratic and organizational barriers to profitable energy-saving investments. Energy Policy 1998, 26, 441–454. [Google Scholar] [CrossRef]

- SEA. Electricity Supply and Use 2001–2014 (GWh). Statistics Sweden; Swedish Energy Agency: Stockholm, Sweden, 2015. [Google Scholar]

- Persson, J.; Grönkvist, S. Drivers for and barriers to low-energy buildings in Sweden. J. Clean. Prod. 2015, 109, 296–304. [Google Scholar] [CrossRef]

- Techato, K.-A.; Watts, D.J.; Chaiprapat, S. Life cycle analysis of retrofitting with high energy efficiency air-conditioner and fluorescent lamp in existing buildings. Energy Policy 2009, 37, 318–325. [Google Scholar] [CrossRef]

- Menassa, C.C. Evaluating sustainable retrofits in existing buildings under uncertainty. Energy Build. 2011, 43, 3576–3583. [Google Scholar] [CrossRef]

- Ascione, F.; Bianco, N.; De Masi, R.F.; de’Rossi, F.; Vanoli, G.P. Energy retrofit of an educational building in the ancient center of Benevento. Feasibility study of energy savings and respect of the historical value. Energy Build. 2015, 95, 172–183. [Google Scholar]

- Nelson, A.J.; Rakau, O.; Dörrenberg, P. Green Buildings: A Niche Becomes Mainstream. Available online: https://www.dbresearch.com/PROD/DBR_INTERNET_EN-PROD/PROD0000000000256216.pdf (accessed on 19 May 2017).

- Schröder, M.; Ekins, P.; Power, A.; Zulauf, M.; Lowe, R. The KFW Experience in the Reduction of Energy Use in and CO2 Emissions from Buildings: Operation, Impacts and Lessons for the UK. Available online: https://www.igbc.ie/wp-content/uploads/2015/02/KfWFullReport.pdf (accessed on 19 May 2017).

- Shen, L.; He, B.; Jiao, L.; Zhang, X. Research on the development of main policy instruments for improving building energy-efficiency. J. Clean. Prod. 2016, 112, 1789–1803. [Google Scholar] [CrossRef]

- Huang, B.; Mauerhofer, V.; Geng, Y. Analysis of existing building energy saving policies in Japan and China. J. Clean. Prod. 2016, 112, 1510–1518. [Google Scholar] [CrossRef]

- Gou, Z.; Lau, S.S.-Y.; Prasad, D. Market readiness and policy implications for green buildings: Case study from Hong Kong. Coll. Publ. 2013, 8, 162–173. [Google Scholar] [CrossRef]

- Pippin, A.M. Survey of Local Government Green Building Incentive Programs for Private Development. Available online: http://digitalcommons.law.uga.edu/cgi/viewcontent.cgi?article=1010&context=landuse (accessed on 19 May 2017).

- BCA. BCA Green Mark Assessment Criteria and Online Application; Building Construction Agency: Singapore, 2015.

- BCA. 3rd Green Building Masterplan; Building Construction Agency: Singapore, 2014.

- Deng, Y.; Li, Z.; Quigley, J.M. Economic returns to energy-efficient investments in the housing market: Evidence from Singapore. Reg. Sci. Urban Econ. 2012, 42, 506–515. [Google Scholar] [CrossRef]

- Li, Y.Y.; Chen, P.-H.; Chew, D.A.S.; Teo, C.C. Exploration of critical resources and capabilities of design firms for delivering green building projects: Empirical studies in Singapore. Habitat Int. 2014, 41, 229–235. [Google Scholar] [CrossRef]

- Rogers, E.M. Diffusion of Innovations, 5th Revised Edition; Simon & Schuster Ltd.: New York, NY, USA, 2003. [Google Scholar]

- Dieperink, C.; Brand, I.; Vermeulen, W. Diffusion of energy-saving innovations in industry and the built environment: Dutch studies as inputs for a more integrated analytical framework. Energy Policy 2004, 32, 773–784. [Google Scholar] [CrossRef]

- Geels, F. Technological transitions as evolutionary reconfiguration processes: A multi-level perspective and a case-study. Res. Policy 2002, 31, 1257–1274. [Google Scholar] [CrossRef]

- Raven, R.; van den Bosch, S.; Weterings, R. Transitions and strategic niche management: Towards a competence kit for practitioners. Int. J. Technol. Manag. 2010, 51, 57–74. [Google Scholar] [CrossRef]

- Raven, R. Strategic Niche Management for Biomass; Technical University Eindhoven (TU/E): Eindhoven, The Netherlands, 2005. [Google Scholar]

- Hoogma, R. Experimenting for Sustainable Transport: The Approach of Strategic Niche Management; Taylor & Francis: London, UK, 2002. [Google Scholar]

- Kemp, R.; Schot, J.; Hoogma, R. Regime shifts to sustainability through processes of niche formation: The approach of strategic niche management. Technol. Anal. Strateg. Manag. 1998, 10, 175–198. [Google Scholar] [CrossRef]

- Markard, J.; Raven, R.; Truffer, B. Sustainability transitions: An emerging field of research and its prospects. Res. Policy 2012, 41, 955–967. [Google Scholar] [CrossRef]

- Markard, J.; Truffer, B. Technological innovation systems and the multi-level perspective: Towards an integrated framework. Res. Policy 2008, 37, 596–615. [Google Scholar] [CrossRef]

- Murphy, L.; Meijer, F.; Visscher, H. A qualitative evaluation of policy instruments used to improve energy performance of existing private dwellings in the Netherlands. Energy Policy 2012, 45, 459–468. [Google Scholar] [CrossRef]

- Tambach, M.; Visscher, H. Towards Energy-neutral New Housing Developments. Municipal Climate Governance in The Netherlands. Eur. Plan. Stud. 2012, 20, 111–130. [Google Scholar]

- Hoppe, T.; Coenen, F.; van den Berg, M. Illustrating the use of concepts from the discipline of policy studies in energy research: An explorative literature review. Energy Res. Soc. Sci. 2016, 21, 12–32. [Google Scholar] [CrossRef]

- Malerba, F. Sectoral Systems of Innovation: Concepts, Issues and Analyses of Six Major Sectors in Europe; Cambridge University Press: Cambridge, UK, 2004. [Google Scholar]

- Malerba, F. Sectoral systems of innovation and production. Res. Policy 2002, 31, 247–264. [Google Scholar] [CrossRef]

- Jain, M.; Hoppe, T.; Bressers, H. Analyzing Sectoral niche formation: The case of Net-Zero Energy Buildings in India. Environ. Innov. Soc. Transit. 2016, in press. [Google Scholar] [CrossRef]

- Edquist, C. Systems of innovation: Perspectives and challenges. Afr. J. Sci. Technol. Innov. Dev. 2011, 2, 14–43. [Google Scholar]

- Malerba, F. Sectoral Systems, The Oxford Handbook of Innovation; Oxford University Press: Oxford, UK, 2005; pp. 380–406. [Google Scholar]

- Dosi, G. Technological paradigms and technological trajectories: A suggested interpretation of the determinants and directions of technical change. Res. Policy 1982, 11, 147–162. [Google Scholar] [CrossRef]

- Nelson, R.R.; Winter, S.G. An Evolutionary Theory of Economic Change; Harvard University Press: Cambridge, MA, USA, 2009. [Google Scholar]

- Malerba, F.; Orsenigo, L. Technological regimes and sectoral patterns of innovative activities. Ind. Corp. Chang. 1997, 6, 83–118. [Google Scholar] [CrossRef]

- Yin, R. Case Study Research; Design and Methods; Sage Publications: London, UK, 2003. [Google Scholar]

- Gerring, J. Case Study Research. Principles and Practices; Cambridge University Press: Cambridge, UK, 2007. [Google Scholar]

- World Business Council for Sustainable Development. Energy Efficiency in Buildings: Business Realities and Opportunities; World Business Council for Sustainable Development Geneva: Geneva, Switzerland, 2007. [Google Scholar]

- Mulchand, A. S’pore has world’s largest district cooling plant. In The Traits Times; Asia One; Singapore Press Holdings Ltd.: Singapore, 2013. [Google Scholar]

- Othman, L. World’s biggest underground district cooling network now at Marina Bay. Today, 31 May 2017. [Google Scholar]

- Johnston, J.G. Singapore Reaches Retail Grid Parity For Solar. The 9 Billion, 2012. Available online: http://www.the9billion.com/2012/10/24/singapore-reaches-retail-grid-parity-for-solar/ (accessed on 19 May 2017).

- Siau, M.E. HDB ramps up solar leasing with latest tender. In Today Singapore; Media Corp Press: Singapore, 2014. [Google Scholar]

- NLB. Singapore Standards; National Library Board: Singapore, 2011.

- Hoppe, T.; Bressers, H.; Lulofs, K. Energy conservation in Dutch housing renovation projects. In The Social and Behavioural Aspects of Climate Change; Martens, P., Ting Chiang, C., Eds.; Greenleaf: Sheffield, UK, 2010; pp. 68–95. [Google Scholar]

- Hoppe, T.; Bressers, J.T.A.; Lulofs, K.R.D. Local government influence on energy conservation ambitions in existing housing sites—Plucking the low-hanging fruit? Energy Policy 2011, 39, 916–925. [Google Scholar] [CrossRef]

- Higgins, A.; Syme, M.; McGregor, J.; Marquez, L.; Seo, S. Forecasting uptake of retrofit packages in office building stock under government incentives. Energy Policy 2014, 65, 501–511. [Google Scholar] [CrossRef]

| SIS Component | Results |

|---|---|

| Technological regime | Technology:

|

| Market demand | Risk aversion to new technology

|

| Actors, networks, and interactions | Actors:

|

| Institutional framework | Formal institutions:

|

© 2017 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Siva, V.; Hoppe, T.; Jain, M. Green Buildings in Singapore; Analyzing a Frontrunner’s Sectoral Innovation System. Sustainability 2017, 9, 919. https://doi.org/10.3390/su9060919

Siva V, Hoppe T, Jain M. Green Buildings in Singapore; Analyzing a Frontrunner’s Sectoral Innovation System. Sustainability. 2017; 9(6):919. https://doi.org/10.3390/su9060919

Chicago/Turabian StyleSiva, Vidushini, Thomas Hoppe, and Mansi Jain. 2017. "Green Buildings in Singapore; Analyzing a Frontrunner’s Sectoral Innovation System" Sustainability 9, no. 6: 919. https://doi.org/10.3390/su9060919