1. Introduction

The Fourth Industrial Revolution has leveraged advanced information systems, including artificial intelligence and the Internet of Things, as general-purpose technologies to drive innovation across industries. This integration with various business models has enabled the fulfillment of entirely new demands. Furthermore, the exponential pace of technological development is expected to catalyze unprecedented innovation, granting access to infinite knowledge and information through hyperconnectivity, hyperconvergence, and hyperintelligence. These advancements are expected to induce structural transformations in production, management, and governance on a global scale [

1].

In this context, while technology serves as a catalyst for the economic structural innovations of the Fourth Industrial Revolution, there will inevitably be limitations to relying solely on technology to generate positive structural shocks and new value. In particular, it is crucial to thoroughly consider rapid changes in social structure, as they not only signify social issues such as deepening inequality but also contribute to the depletion of natural resources and exert negative impacts on the environment [

2]. In order to achieve successful sustainable innovation in this situation, support must be provided to solve ecological and social problems that may arise, along with the introduction and operation of technology. In other words, the role of complementary assets is necessary for sustainable innovation. Within the service industry, knowledge-intensive business services (KIBS) fulfill this role. Professional services contribute to the creation, accumulation, and dissemination of new knowledge, thereby fostering the generation of freshly added value. As entities have engaged in business activities related to emerging technology, KIBSs not only act as users of new technology but also serve as producers driving technological innovation and innovators [

3,

4,

5,

6,

7].

KIBSs are an industry positioned to act as a complementary asset essential for the key technologies of the Fourth Industrial Revolution and to generate value and transform the economic system appropriately. While the definition of KIBSs may vary among scholars and institutions, Miles et al. (1995) identified three primary characteristics that align with the consensus of most experts: (1) heavy reliance on expert knowledge, (2) serving as the main source of information and knowledge or utilizing knowledge to provide intermediate services necessary for the customer’s production process, and (3) primarily supplying businesses with a competitive advantage [

3]. KIBS entities play a central role in fostering innovation as knowledge operators, producers, and mediators within national and regional economies [

8,

9,

10,

11,

12]. Moreover, they possess characteristics such as a heightened awareness of knowledge activities, the ability to interpret and resolve various problems, and the ability to provide services. Catalyzing constant systemic change, KIBSs, particularly professional producers and users in the knowledge-intensive service industry, have led to transformations within complex innovation systems [

6].

Research on KIBSs is primarily centered on industries driven by companies seeking KIBS support [

13,

14,

15,

16,

17,

18,

19]. This research spans the regional and national levels [

20,

21,

22] and has been conducted over several years, examining various types of innovations. Additionally, research has been conducted on the mediating role of sustainable innovation in the green economy related to the energy and resource sectors [

23,

24,

25,

26]. The results of these studies consistently underscore the role of KIBSs in supporting sustainable innovation within target units [

25,

26,

27,

28,

29,

30,

31,

32]. Specifically, the findings reveal variations based on factors such as the degree of connectivity and concentration of KIBSs, the skill level of the labor force, and the age and size of entities utilizing the KIBSs within a given region.

As KIBSs are a knowledge-intensive industry, there are limitations when analyzing results obtained within a short period; therefore, research has been conducted in regions with mature industries over a long period. However, as national economies become globalized and knowledge transfer methods diversify, interest in KIBSs is growing even in developing countries, and research is being conducted on regions and industries in various countries. In addition, because the size and characteristics of the economy vary in each region and country, how KIBSs operate may also differ [

6]. Therefore, although KIBS research has been conducted for a long time, it is meaningful to measure the role and degree of influence of KIBSs depending on the country and period.

Since we are currently undergoing significant socio-structural changes due to advanced information technology, it is essential to discuss KIBSs as a critical intermediary industry in promoting sustainable innovation. In particular, examining the impact and role of KIBSs within a specific country is crucial for the effective utilization of these services.

Therefore, this study investigates the impact of knowledge-intensive business services (KIBSs) on the Korean economy. The focus is on analyzing and contrasting the level of influence and contribution of the overall KIBS sector, T-KIBSs (new technology-based professional services), P-KIBSs (traditional professional services), and their respective subsectors within the Korean economy.

For this analysis, information on how much the KIBSs sector invests in other industries and how output occurs in other industries must be considered. Therefore, this study applied the demand inducement model, supply inducement model, and interlinkage effects method to an industry linkage table. Through this analysis, one can see how all the sectors covered by the KIBSs sector play a role in the Korean economy and how much influence they have.

3. Data and Methodologies

This study is an analysis and comparison of the degree of influence and role of the entire KIBS sector, T-KIBSs (a new technology-based professional service), P-KIBSs (a traditional professional service), and sub-sectors on the Korean economy. For this purpose, among the input–output analysis methodologies, an analysis was conducted on the industry linkage effect, which involved an examination of the forward and backward effects of each research target industry, the production inducement effect of the demand inducement model, the value-added inducement effect, and the supply shortage effect of the supply inducement model. In addition, an exogenous specification method was used to distinguish between the indirect ripple effect of the industry under analysis in other industries and the direct ripple effect of the subject of analysis [

51].

3.1. Input–Output Table

The input–output table is a comprehensive statistical table that records the inter-industry trade relationships of goods and services produced in a country over a period of time [

45]. Input–output analysis using this method is advantageous for analyzing the economic structure based on inter-industry relationships [

52]. In addition, input–output analysis shows how changes in the level of production in one sector generate continuous demand for the products of other sectors; this is a general equilibrium model that emphasizes the link between sales and purchases of inputs. Owing to its nature, it is a useful method for analyzing and predicting the overall economic impact [

52].

Therefore, this study involved an industry linkage analysis using the 2019 industry linkage table published by the Bank of Korea in 2022 to examine the influencing relationships and roles of KIBS sectors on the Korean economy.

3.2. Input–Output Analysis

3.2.1. Demand Inducement Model

This study is based on an examination of the production inducement and value-added inducement effects among detailed demand inducement models. Here, production-inducement effects and value-added inducement effects refer to the direct and indirect production inducement and value-added inducement amounts on the same industry and other industries when KRW 1 is produced or invested in the industry being analyzed. To calculate this effect, Equations (1)–(4) were used.

The input coefficient (

) in Equation (1) is the intermediate input amount (

) of raw materials purchased by each industrial sector from other industrial sectors for the production of the goods and services of that industrial sector divided by the total input amount (

) [

53]. If this is expressed in the same array form as the endogenous part of the input–output table, it becomes the input coefficient matrix (

A). The input coefficient (

) is calculated using the input–output table that reclassifies each of the industries subject to analysis. Equation (1) is as below.

- -

: Input amount in subsector ;

- -

: Input amount in subsector by intermediate input .

The production inducement coefficient converts the industry subject to be analyzed into an exogenous variable and then uses basic Equation (2).

- -

: Row vector of the input coefficients of the reclassified industries subject to analysis;

- -

: Diagonal matrix of 1 (diagonal matrix);

- -

: Input coefficient () matrix.

The value-added coefficient in Equation (3) is the sum of the added value of each industrial sector in the input–output table divided by the total output.

- -

: Added value of subsector .

The added value inducement coefficient, Equation (4), is calculated by multiplying the added value coefficient derived from Equation (3) by the production inducement coefficient derived from Equation (2) [

53]. This refers to the net national economic value that can be obtained from the industry being analyzed.

- -

: Diagonal vector of the value-added coefficient;

- -

: Production inducement coefficient.

3.2.2. Supply Inducement Model

The supply shortage effect indicates the degree of production reduction in other industries, excluding the target industry, when the production of the target industry is not produced by KRW 1 [

51].

To calculate these supply shortage effects, the output coefficient (

) in Equation (5) is first created using the output coefficient table [

51]. This is the number of intermediate inputs, such as raw materials, purchased from other sectors for production in that sector, divided by the total output [

51].

- -

: Output of subsector ;

- -

: Output amount in subsector by intermediate output .

The supply shortage coefficient is calculated by exogenizing the industry subject for analysis and using the following basic model Equation (6).

- -

: Output coefficient horizontal vector of the subsector;

- -

: One diagonal matrix with a diagonal vector 1;

- -

: Output coefficient matrix ().

3.2.3. Industry Linkage Effect

The industry linkage effect consists of backward linkage effects (

) and forward linkage effects (

). Here, the forward linkage effect (

) in Equation (7) is the value calculated by dividing the row sum of the production inducement coefficient (

) matrix of the industry by the average of all industries [

53], which represents all final demands in all sectors as one unit. It indicates the ratio of the units that the

th industry must produce in order to increase the unit to the average value of all industries.

The backward linkage effects (

), Equation (8), are the sum of the columns of the production inducement coefficient matrix of the industry being analyzed divided by the average of all industries. This refers to the influence on all industrial sectors when one unit of final demand for the industry is generated [

53].

3.3. Research Procedure and Reclassification of KIBS

This study investigates the role of KIBSs as a tool for economic system innovation. Utilizing input–output tables for input–output analysis, the research applied the demand inducement model, supply inducement model, and interlinkage effects to examine various economic ripple effects. The objective was to understand the role of the KIBS sector in an economic system and to quantify its economic ripple effects, thereby discerning how the KIBS sector functions as a tool for economic system innovation.

To differentiate this research and provide specificity for the role of KIBSs, we distinguished KIBSs from T-KIBSs and P-KIBSs. This study examined the economic ripple effects and roles of each industry in these classifications. The specific research procedure is detailed in

Figure 1, with the goal of delineating the distinctive roles and economic impacts of T-KIBSs and P-KIBSs.

The steps of this study are illustrated in

Figure 1. Step 1 is a necessary preliminary step in examining the role of the KIBS sector in the Korean economic system. To this end, based on previous works in the literature, KIBSs are classified in detail according to their characteristics, and the industry is reclassified in a form that can be analyzed. Currently, KIBS entities are divided into the entire KIBS industry, technology-based KIBSs, and P-KIBSs, which are classified as traditional professional services. In addition, each detailed KIBS subindustry is classified for analysis.

Step 2 presents the analysis of the status of the KIBS industry. The second step examines the share of the KIBS industry and the value-added output in the KIBS industry, the KIBS industry classifications, and the detailed classifications.

Steps 3–4 examine the impact of KIBSs on the overall Korean economic system and the differences in the economic ripple effects of T-KIBSs and P-KIBSs on the Korean economic system. For this purpose, we analyzed the supply shortage effects, which are the production inducement, value-added inducement, and supply shortage effects of the demand inducement model. Through the results, we can specifically identify which industries the KIBS sector influences in the Korean economic system.

Step 5 analyzes the demand inducement, supply inducement, and interlinkage effects for each sector to examine the roles and ripple effects of each KIBS subcategory in the Korean economic system. We also compared the KIBS, T-KIBS, and P-KIBS results analyzed previously.

Finally, Step 6 uses the literature review and analysis presented above to evaluate the role of KIBSs as a tool for innovation in the Korean economic system.

Table 4 presents the industrial classifications used in this study. First, for industrial linkage analysis, the KIBS sector, the industry subject to analysis, is reclassified and redefined as a single industry. In addition, to understand the impact of the industry being analyzed on other industries, each industry is presented based on the Bank of Korea Input–Output Table of Industrial Representative Classifications.

Looking at the KIBS reclassification, eight industries fall into this category based on the Bank of Korea’s industrial classifications’ subclassifications. Among these, six industries fall under T-KIBSs: J (610)—information services, J (621)—software development supply, J (629)—other IT services, M (700)—R&D, and M (721)—architecture, which includes civil engineering services, and M (729)—other science, technology, and professional services. In addition, P-KIBSs include two industries: M (711)—legal and management support services and M (721)—advertisement.

4. Results

This section presents the results of Steps 3–5 of the analytical process. The data used in the analysis were analyzed using the 2019 industry correlation table published by the Bank of Korea in 2022.

First, in

Section 4.1, we treat the eight sectors of the KIBS industry as a single industry and examine their overall impact on the South Korean economy. Following that, in

Section 4.2 and

Section 4.3, we delve into the individual impacts of T-KIBSs and P-KIBSs on the entire South Korean economy, as well as the mutual influence between the two types of KIBSs. Finally, to understand the roles of specific sectors within the KIBS sector and their impact on the South Korean economy, the economic ripple effects of each sector are compared.

4.1. Results of the Economic Ripple Effect in the KIBS Industry

Table 5 examines the ripple effects of the KIBS sector on the Korean economy through the demand inducement model, production inducement effects, value-added inducement effects, and the supply inducement model’s supply shortage effects.

First, production inducement effects indicate how much production is induced in other industries when KRW 1 of final demand is generated in the sector being analyzed (or can be interpreted as investment). The KIBS sector showed that when the final demand of an industry was KRW 1, the production inducement from other industries was KRW 0.8. At this time, the production inducement effects of the industry were KRW 1.195, showing a total of KRW 1.995 of production inducement effects.

Looking at the sectors in which KIBSs have the largest indirect ripple effect on other industries, C09—computers, electronics, and optics—had the highest at KRW 0.075, followed by C05—chemicals, at KRW 0.063; N—business services, at KRW 0.058; J—broadcasting and newspaper and publishing—showed an effect of KRW 0.055. Conversely, the sectors with the lowest scores were P—education services (KRW 0.001), O—public administration, defense, and social security (KRW 0.001), and others (KRW 0.002). The indirect effect of production inducement on the primary industry was KRW 0.053 for accounting, for a rate of 6.6%; the secondary industry effect, corresponding to the manufacturing industry, was KRW 0.341, accounting for 42.6%; and the tertiary industry effect, corresponding to the service industry, was KRW 0.406, accounting for 50.8%.

Value-added inducement effects indicate how much added value is induced in other industries when KRW 1 of final demand is generated in the sector being analyzed (or can be interpreted as investment). The indirect effect of the KIBS sector on inducing added value in other industries was found to be KRW 0.330, and the added value induced by the industry itself was KRW 0.551, for a total of KRW 0.881. The sector that generated the most added value due to KIBSs was N—business services—with KRW 0.039, followed by C09—computers, electronics, and optics—with KRW 0.030, and L—real estate services—with 0.027. Conversely, the least affected sector was T—others—with a value close to 0, P—education services—with KRW 0.001, and O—public administration, defense, and social security—with KRW 0.001. KIBS’ indirect value-added inducement effects were KRW 0.026 or 7.8% for the primary industry, KRW 0.106 or 32.0% for the secondary industry, and KRW 0.198 or 60.2% for the tertiary industry. Value-added inducement effects were found to have a greater impact on the tertiary industry than production inducement effects.

The following supply shortage effects can be used to determine how much production fails to occur in other industries when the industry being analyzed does not produce KRW 1; that is, when KRW 1 is not supplied. The supply shortage effects of the KIBS sector on other industries totaled KRW 1.144. The most affected sector was C05—chemicals—at KRW 0.113, followed by construction at KRW 0.107, G—wholesale and retail trade services—at KRW 0.086, and C12—transportation equipment—at KRW 0.084. In contrast, the sectors least affected by KIBSs were T—others—at KRW 0.001, minerals (KRW 0.001), and E—water, waste disposal, and recycling services (KRW 0.006). Supply shortage effects were found to affect the primary, secondary, and tertiary industries by 1.2%, 50.7%, and 48.0%, respectively. Compared to the production and value-added inducement effects analyzed previously, the supply shortage effects on the primary industry were found to be low. However, the impacts on secondary and tertiary industries appeared even.

4.2. Results of the Economic Ripple Effect of the T-KIBS Industry

This section is an examination of the ripple effects of T-KIBSs on South Korea’s economy (

Table 6). Through this analysis, the impact of T-KIBSs and their influence on P-KIBSs were investigated. First, looking at production inducement effects, the impact of T-KIBSs on other industries was found to be KRW 0.687, and the effect on their own industry was KRW 1.084, for a total of KRW 1.771. The sector most affected by T-KIBSs was C09—computers, electronics, and optics—at KRW 0.085, followed by C05—chemicals—at KRW 0.053, P-KIBSs at KRW 0.047, and transportation services at KRW 0.042. However, the least affected sectors were P—education services—at KRW 0.001, O—public administration, defense, and social security—at KRW 0.001, and T—others—at KRW 0.002. In addition, the primary industry’s rate was 5.7% with a KRW value of 0.039; for secondary industry, the rate was 45.7% with a KRW value of 0.314; and for tertiary industry, the rate was 48.7%.

The value-added inducement effect of T-KIBSs on other industries was KRW 0.272, the direct effect was KRW 0.654, and the total value-added inducement effect was KRW 0.926. The sector most affected by T-KIBSs was production inducement effects, with C09—computers, electronics, and optics—at KRW 0.034, followed by N—business services—at KRW 0.028, G—wholesale and retail trade services—at KRW 0.021, and L—real estate services—at KRW 0.017. The value-added inducement effect on P-KIBSs was KRW 0.014, showing the seventh largest impact among the 33 industries. In contrast, the least affected sector was T—others—which was close to 0, followed by P—education services—at KRW 0.001, O—public administration, defense, and social security—at KRW 0.001, and C13—other manufacturing products—at KRW 0.001. The primary industry represented KRW 0.019 (6.9%), the secondary industry was KRW 0.099 (36.4%), and the tertiary industry was KRW 0.154 (56.7%), respectively.

In the case of supply shortage effects, the effect of T-KIBSs on other industries was KRW 0.730, of which the most affected sector was construction (KRW 0.104), followed by C12—transportation equipment (KRW 0.056), C05—chemicals (KRW 0.046), and C09—computers, electronics, and optics (KRW 0.046). In addition, the supply shortage effect of T-KIBSs on P-KIBSs was KRW 0.041, the sixth highest. In contrast, the least affected sectors were B—minerals—at KRW 0.001, T—others—at KRW 0.001, and C13—other manufacturing products—at KRW 0.004. The primary, secondary, and tertiary industries accounted for 1.2%, 43.8%, and 55%, respectively.

4.3. Results of the Economic Ripple Effect of the P-KIBS Industry

This section is an examination of the ripple effects of P-KIBSs on the Korean economy (

Table 7). In addition, this study examined the effect of P-KIBSs on T-KIBSs. First, looking at the production inducement effects, the ripple effect of P-KIBSs on other industries was KRW 1.472 and the direct effect was KRW 1.086, resulting in a total effect of KRW 2.558. Looking at the sectors in which P-KIBSs had the greatest impact, J—broadcasting, newspaper, and publishing—had the largest at KRW 0.136, followed by N—business services—at KRW 0.111, T-KIBSs at KRW 0.120, and D—electricity, gas, and steam—at KRW 0.102. Conversely, the industries least affected were P—education services—at KRW 0.002, O—public administration, defense, and social security—at KRW 0.002, and T—others—at KRW 0.003. Among the indirect effects, the impacts on primary, secondary, and tertiary industries were KRW 0.101 (6.8%), KRW 0.471 (32.0%), and KRW 0.901 (61.2%), respectively.

In the case of value-added inducement effects, the indirect effect of P-KIBSs on other industries was KRW 0.646, and the direct effect was KRW 0.301 for a total of KRW 0.947. Among the indirect effects, the sectors that showed the largest effect were N—business services at KRW 0.075; T-KIBSs at KRW 0.067; J—broadcasting and newspapers and publishing—at KRW 0.057; and L—real estate services—at KRW 0.057. In contrast, the least affected sector was T—others—with a value close to 0, followed by P—education services and O—public administration, defense, and social security with KPW 0.001 each, and C06—nonmetallic mineral products—with KRW 0.002. Among the indirect effects, the impacts on the primary, secondary, and tertiary industries were KRW 0.048 (7.5%), KRW 0.141 (21.9%), and KRW 0.457 (70.7%), respectively.

In the case of supply shortage effects, the sectors most affected by P-KIBSs were C05—chemicals—at KRW 0.301, G—wholesale and retail trade services—at KRW 0.234, C12—transportation equipment—at KRW 0.175, and F—construction—at KRW 0.133, while T-KIBSs had an effect of KRW 0.118. It was ranked seventh highest. However, the least affected sectors were T—others—at KRW 0.002, B—minerals—at KRW 0.003, and E—water, waste disposal, and recycling services—at KRW 0.013. Thus, the supply shortage effect of P-KIBSs on other industries was found to total KRW 2.657, of which the primary industry accounted for KRW 0.029 or 1.1%, the secondary industry accounted for 51.5% with an effect of KRW 1.368, and the tertiary industry accounted for 51.5% with an effect of KRW 1.368. This accounted for 47.4% (KRW 1.261).

4.4. Results of the Economic Ripple Effect of KIBS Sectors

4.4.1. Results of Interlinkage Effects by KIBS Sectors

Table 8 presents the interlinkage effects of T-KIBSs, P-KIBSs, and KIBSs. This allowed us to examine the role of each KIBS department in detail. First, the interlinkage effects were divided into forward and backward linkage effects. Here, forward linkage effects view the output of the analysis target as a raw material resource from another industry, while backward linkage effects, on the contrary, view the analysis target as a final good and view other industries as providing raw materials.

Based on this result, Yoo and Yoo (2009) divided the interlinkage effects into four types based on a value of 1 for each backward-linkage effect: “First, if the coefficients of all Backward linkage effects are high, it is a medium-demand manufacturing type. Second, if Backward linkage effects are low and Forward-linkage effects are high, it is a medium-demand primitive industry type. Third, if Forward linkage effects are low and Backward linkage effects are high, it is a medium-demand manufacturing type. If it is high, it is called final demand manufacturing type. Fourth, if both forward linkage effects and backward linkage effects are low, it is called final demand type of primitive industry type” [

51].

Based on this industry classification, the types of KIBS subsectors are classified as shown in

Table 8. First, considering P-KIBSs, both forward and backward chain effects were greater than one; therefore, it was classified as a demand-manufacturing type. Legal and management support services, a detailed division of the P-KIBS sector, also appeared as the first-demand manufacturing type, with both forward and backward chain effects higher than one. Advertisement ranked third, with forward linkage effects lower than one and backward linkage effects higher than one. This is classified as final demand manufacturing. In the case of T-KIBSs, all backward linkage effects showed values lower than one; therefore, they were classified as the fourth final demand type of the primitive industry, and all detailed sectors were classified as the fourth area.

As a result of analyzing the interlinkage effects by reorganizing a total of eight detailed divisions of KIBSs into one division, this was classified as a second medium-demand manufacturing type with forward linkage effects higher than one and backward linkage effects lower than one.

In this way, it can be seen that each of the detailed divisions of KIBSs play a different role in the Korean economic system depending on industrial characteristics and maturity. In particular, this research confirmed that P-KIBSs and T-KIBSs perform distinctly different roles.

4.4.2. Results of Production Inducement Effects by KIBS Sectors

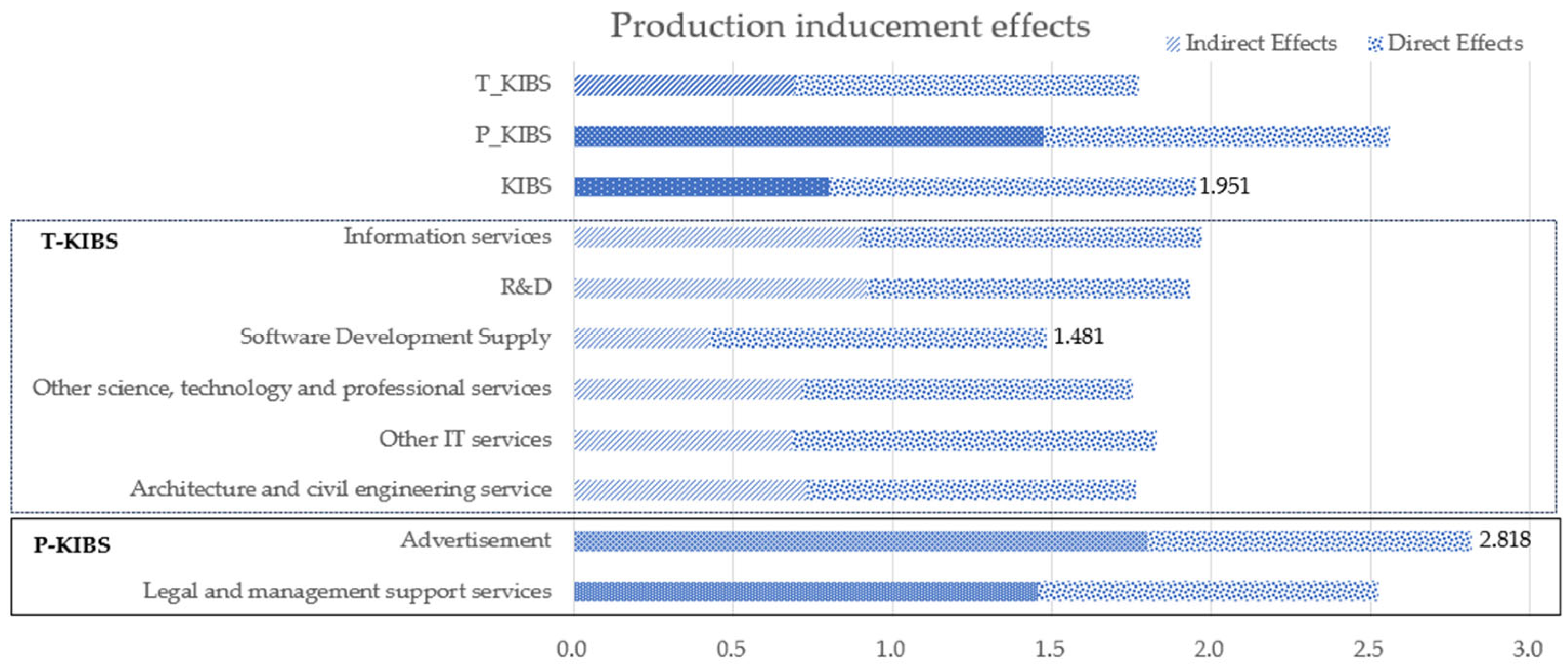

Table 9 compares the production inducement effects of the KIBS divisions. This table focuses on the differences in the indirect effects of each detailed KIBS sector and the proportion of the impact on each industry. First, looking at the indirect effect, advertisement, a subdivision of P-KIBSs, was the highest at KRW 1.801, followed by legal and management support services at KRW 1.455. However, the production inducement effects of T-KIBSs were weaker than those of P-KIBSs alone. Among these, the sector with the highest figure was R&D at KRW 0.920, followed by information services at KRW 0.896, and the sector with the lowest figure was software development supply at KRW 0.422. When P-KIBSs were analyzed as one sector, the production inducement indirect effect was found to be KRW 1.472, which was higher than the T-KIBSs’ KRW 0.687. When these two sectors were reorganized and analyzed as one KIBS sector, they were found to have an effect of KRW 0.800 (

Figure 2).

When examining the production inducement effects of KIBSs on other industries, the impact on primary industries was found to be in the single digits, ranging from 2.8% to 7.6% across all detailed subsectors. In contrast, the effects on secondary industries ranged significantly from 18.9% to 47.6%. Among the detailed subsectors, advertisements within the P-KIBS subcategory had the least impact, whereas the sector had the most substantial influence.

The proportion of impact on tertiary industries varied, with R&D having the lowest at 45.0%, and advertisements showing the highest at 78.3%. When considering P-KIBSs and T-KIBSs as a single category for analysis, P-KIBSs demonstrated a more significant impact on secondary (32.0%) and tertiary industries (61.2%). By contrast, T-KIBSs exhibited a slightly higher influence on the secondary (45.7%) and tertiary industries (48.7%). T-KIBSs had a more balanced impact on both the secondary and tertiary sectors than P-KIBSs.

4.4.3. Results of Value-Added Inducement Effects by KIBS Sector

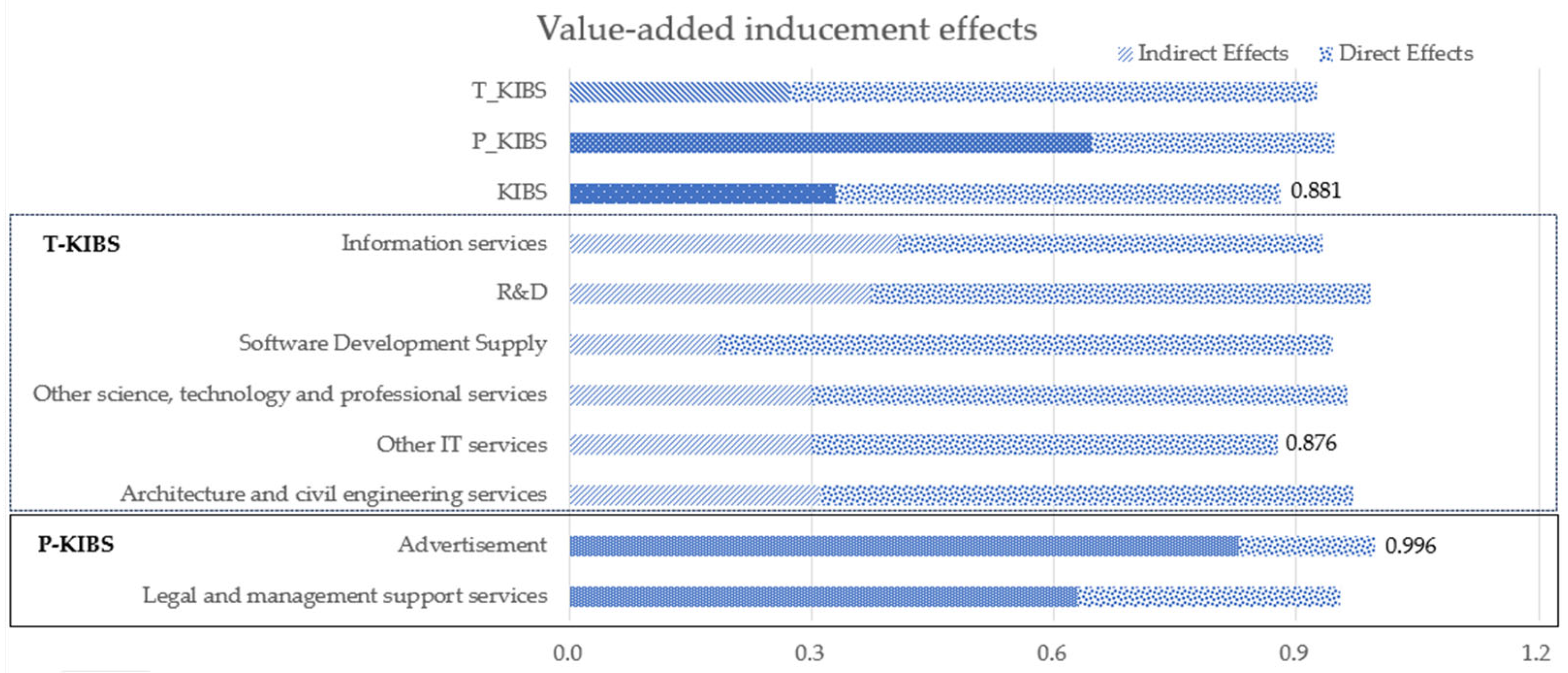

Table 10 compares the value-added inducement effects of the KIBS sectors. First, looking at the indirect effects on other industries, the sector with the greatest impact was advertisement, corresponding to P-KIBSs with a KRW value of 0.828, followed by legal and management support services with a value of KRW 0.63. Conversely, the sector with the least impact was software development supply, which corresponds to T-KIBSs, at KRW 0.184. Overall, the detailed sectors of T-KIBSs showed lower value-added inducement effects on industries other than P-KIBSs. However, when looking at the total effect, considering the sector’s own value-added inducement effects, advertisements showed the highest value at KRW 0.996, but their own value-added inducement effects were the lowest at KRW 0.169. The next was R&D, which was the highest, at KRW 0.991, and architecture and civil engineering services, which had a value of KRW 0.970 (

Figure 3).

Analyzing P-KIBSs and T-KIBSs as one sector each, the value-added inducement effect on other industries for P-KIBSs was KRW 0.646, and for T-KIBSs it was KRW 0.272, which is more than twice the value of P-KIBSs. It showed a high value. However, if you look at the total effect, considering the direct effect, it can be seen that P-KIBSs had a value of KRW 0.947 and T-KIBSs had a value of KRW 0.926, which were approximate figures compared with the indirect effect. P-KIBSs showed a large indirect effect and T-KIBSs showed a larger direct effect; thus, there was no significant difference in the total effect.

Next, when examining the impact that KIBS sectors have on other industry sectors, the influence on primary industries ranged from a minimum of 2.9%, observed in advertisement, to a maximum of 8.5% in legal and management support services. In secondary industry, advertising was the lowest at 12.7%, and R&D was the highest at 37.9%. In tertiary industry, R&D was the lowest at 55.1%, and advertising was the highest at 84.4%. When analyzing P-KIBSs as a single sector, the primary, secondary, and tertiary industries accounted for 7.5%, 21.9%, and 70.7%, respectively. In addition, an analysis of T-KIBSs showed that 6.9%, 36.4%, and 56.7% of the industries were composed of primary, secondary, and tertiary industries, respectively. Both KIBS sectors had a large impact on tertiary industry, and P-KIBSs appeared to have an even greater impact on tertiary industry.

4.4.4. Results of Supply Shortage Effects by KIBS Sector

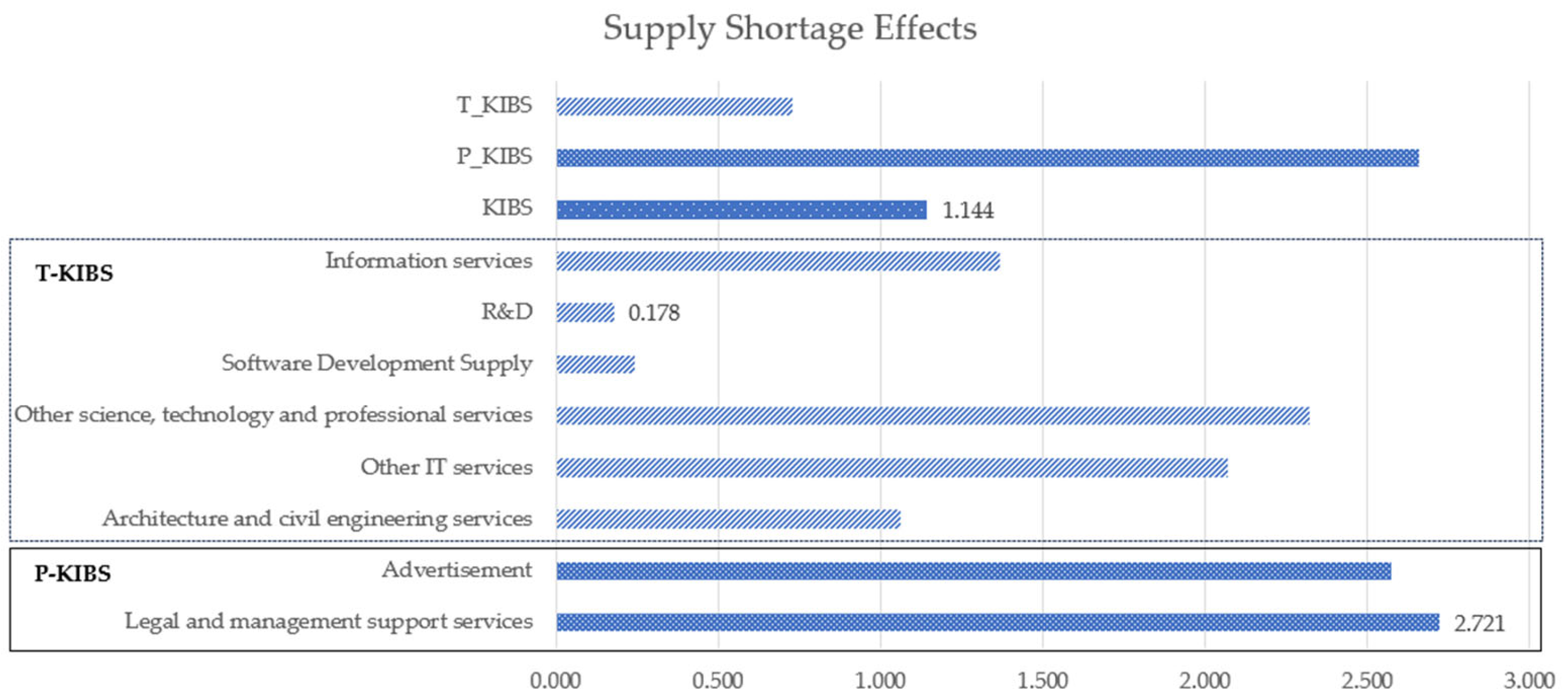

Table 11 compares the value-added inducement effects of the KIBS sectors. Among the KIBS subsectors, the sectors with the greatest supply shortage effects were the two P-KIBS subsectors, with legal and management support services at KRW 2.721 and advertisements at KRW 2.573. Next, other science- and technology-related services earned KRW 2.321 and other IT services earned KRW 2.071. Conversely, R&D showed the lowest figures, at KRW 0.178, and software development supply had a value of KRW 0.242. P-KIBSs showed a high supply shortage effect of KRW 2.657 and T-KIBSs showed KRW 0.730 (

Figure 4).

When examining industry-specific proportions, it is evident that in the primary industry sector, architecture and civil engineering services ranged from 0.1% compared to other science and technology-related services at 1.9%, showing proportions lower than the production and value-added inducement effects. The impact on secondary industry was the lowest at 4.4% for architecture and civil engineering services and the highest at 68.7% for R&D. In the tertiary industry, R&D was the lowest at 30.7% and architecture and civil engineering services had the highest at 95.5%. For P-KIBSs, the primary, secondary, and tertiary industries accounted for 1.1%, 51.5%, and 47.4%, respectively; for T-KIBSs, the primary, secondary, and tertiary industries accounted for 1.2%, 43.8%, and 55%, respectively.

In the case of production and value-added inducement effects, both P-KIBSs and T-KIBSs had a significant impact on tertiary industry, and P-KIBSs had a greater impact on tertiary industry. However, in terms of supply shortage effects, P-KIBSs showed a higher impact on secondary industry, at 51.5%, than on tertiary industry. T-KIBSs showed that tertiary industries accounted for more than the majority (55.0%), but the proportion of influence on secondary industries was also high, at 43.8%.

5. Conclusions

In this study, we investigated the role of KIBSs, a sustainable innovation tool, in Korea’s economic system. For this purpose, the demand inducement, supply inducement, and interlinkage effects were analyzed using the 2019 industry linkage table published by the Bank of Korea for 2022. This method can identify the impact of the KIBS sector on the growth of other industries by analyzing production inducement effects, value-added inducement effects on the Korean economy, and their position in the Korean economic ecosystem through interlinkage effects. This analysis was conducted to compare and analyze each impact by analyzing the overall KIBS sector, T-KIBSs, P-KIBSs, and detailed subsectors of KIBSs. These methodologies and approaches can provide useful information when attempting to foster sustainable innovation in the national economy and enhance the KIBS industry by identifying the impact and role of sustainable innovation in a detailed analysis of KIBS subsectors.

The following implications can be drawn based on the results. First, the results confirmed that KIBSs are growing as an industry in the Korean economy. Examining the proportion of KIBSs allows us to demonstrate that the proportion of added value and job creation is high compared to the total output. In addition, the total output has grown rapidly at an average annual rate of 9.6% over the past 10 years. These results confirm that the demand for KIBSs in other industries is increasing.

Second, when examining the results of the interlinkage effects, indicators have emerged that clearly demonstrate distinct roles within the South Korean economic system based on the type of KIBS. All KIBSs were classified as medium-demand manufacturing, with forward linkage effects higher than the standard value of one and backward linkage effects lower than one. This can be attributed to the significant difference between the P-KIBS and T-KIBS results. This is because T-KIBSs showed a value lower than the previous backward linkage effects’ standard value of one and were classified as a final demand type of primitive industry, whereas P-KIBSs were classified as a demand manufacturing type higher than the standard value of one.

Third, the KIBS sector was confirmed to have different impacts on Korea depending on the impact indicators. In addition, it was confirmed that the differences varied depending on the KIBS type. The KIBS sector was found to have a high production inducement effect on other industries and affected secondary and tertiary industries evenly. Value-added inducement effects had a greater impact on tertiary industries than on secondary ones, and supply shortage effects appeared to have a greater impact on secondary industries than the results obtained through the demand inducement model. Looking at the KIBS details, P-KIBSs had a higher impact on industries than T-KIBSs for all indicators. However, this indicator alone cannot be used to determine the more important type of KIBS.

These results and implications can provide the following additional policy and academic implications. Unlike previous studies that predominantly focused on the manufacturing or service industries, this study explores the ripple effect by examining all sectors within the national economy. In contrast, prior studies have primarily focused on confirming differences in the presence and extent of impact [

16,

20] through econometric approaches. However, this study goes beyond that by investigating which industries are more significantly impacted by KIBS sectors and the specific effects they exert. These insights are substantiated through quantitative figures. Such an approach has proven to be valuable for analyzing KIBSs and providing support for sustainable innovation within the national economic system. The anticipated outcomes are expected to contribute substantially to the formulation of effective economic policies.

This approach became feasible due to the distinctive features of the input–output table and the diverse array of analysis models. Importantly, it holds significance not only for analyzing KIBSs as a collective industry group, utilizing the advantages provided by industry linkage analysis, but also for scrutinizing and comparing sub-detailed sectors. This approach enables a meticulous examination of the influencing relationships between KIBSs and other industries. Consequently, unlike previous studies, the outcomes presented in this study are anticipated to provide increased practical relevance in shaping economic policies, especially in fostering sustainable innovation within the national economy.

Despite these implications, this study has several limitations. First, it is difficult to clarify the reference points for the indicator results because comparisons with other countries have not been made. These issues pose a risk in that the interpretation and application of the results may differ depending on the people who use the data. We did not consider the scale of other industries in this study; therefore, additional research needs to be conducted to apply them to companies or specific industrial units.

{kind=link}

{kind=link}

{kind=link}

{kind=link}