Understanding the Relevance of Sustainability in Mergers and Acquisitions—A Systematic Literature Review on Sustainability and Its Implications throughout Deal Stages

Abstract

:1. Introduction

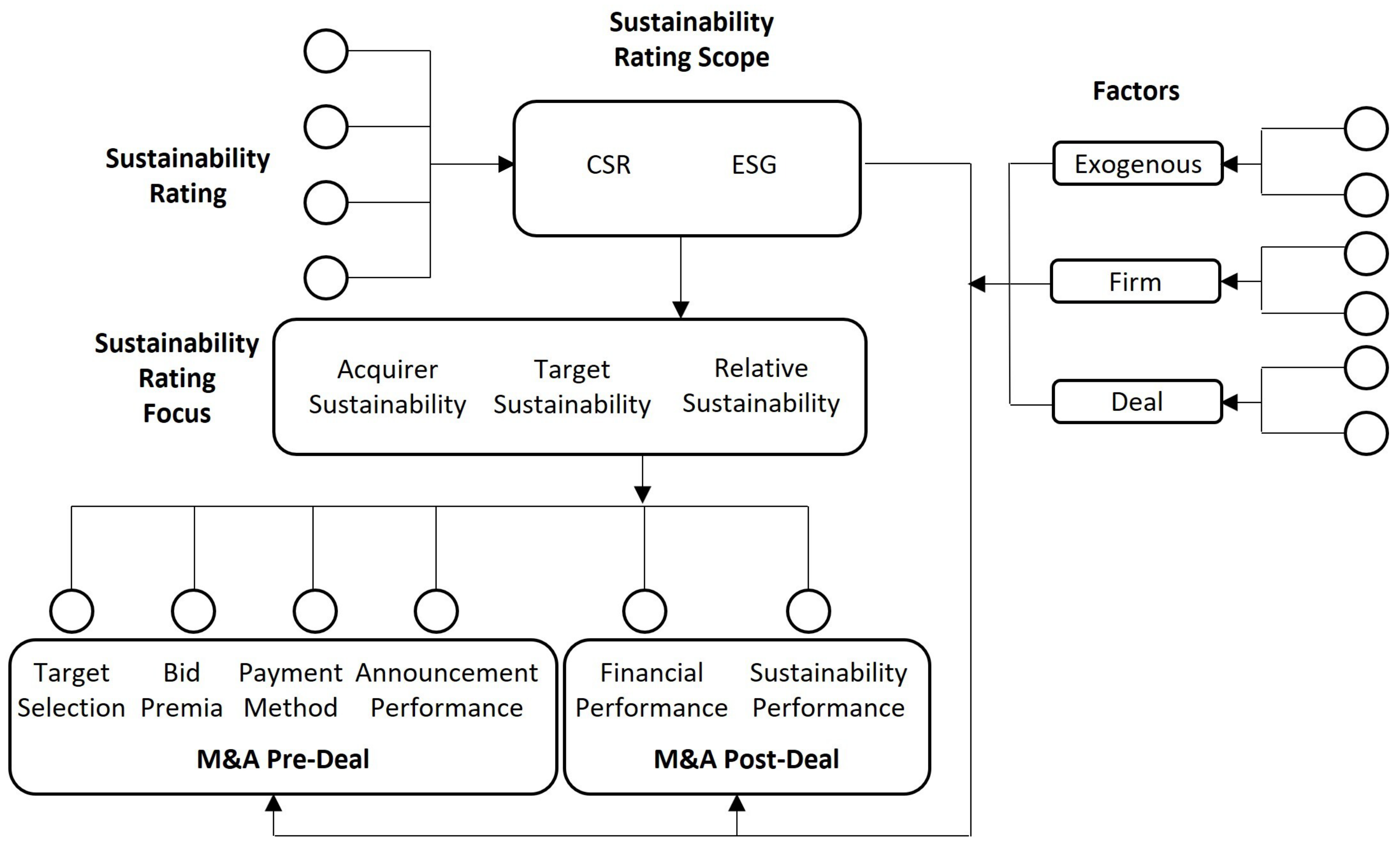

2. Theoretical Background

2.1. Sustainability Terminology

2.2. M&A Terminology

2.3. Linking Sustainability and M&A

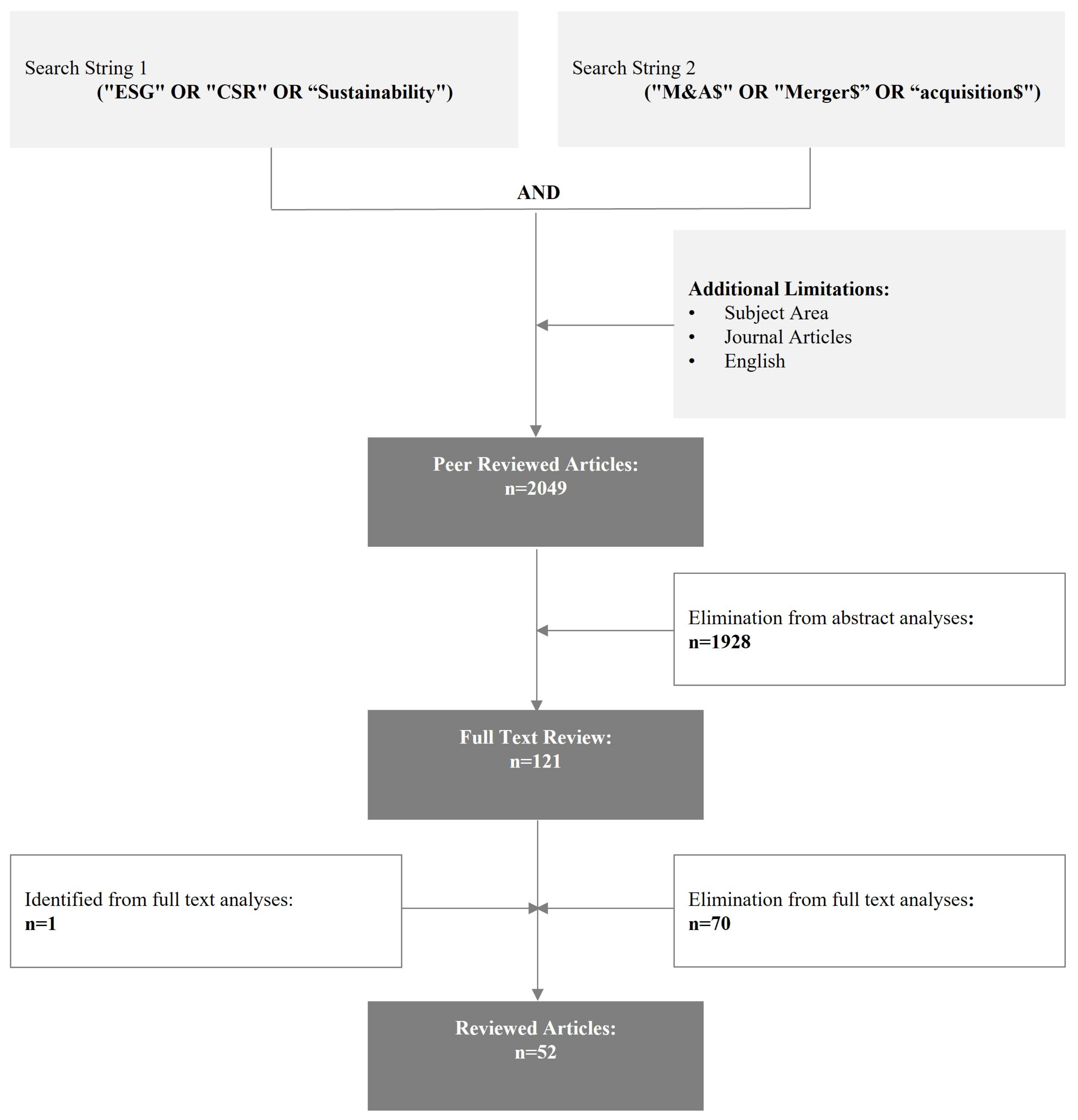

3. Materials and Methods

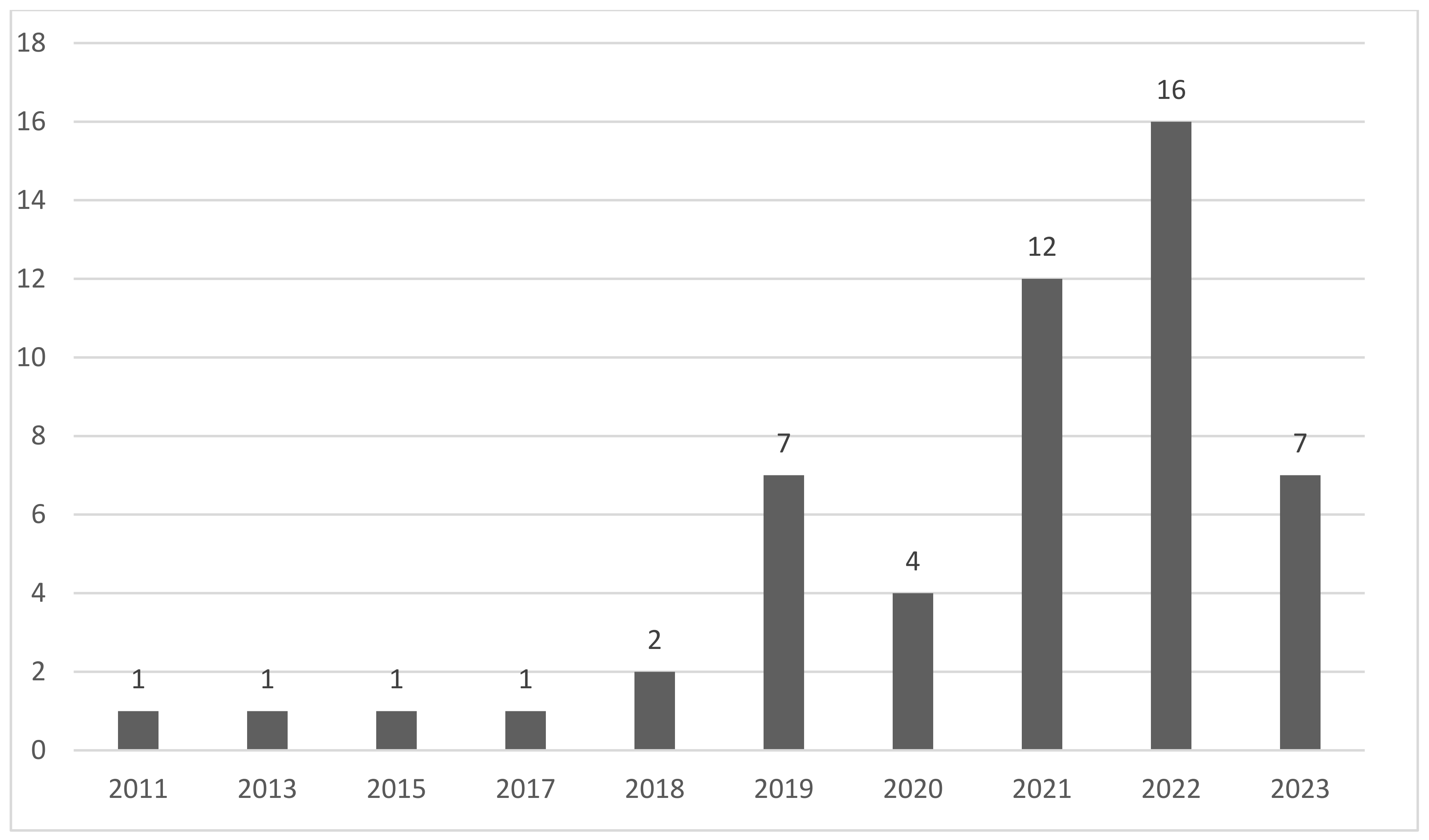

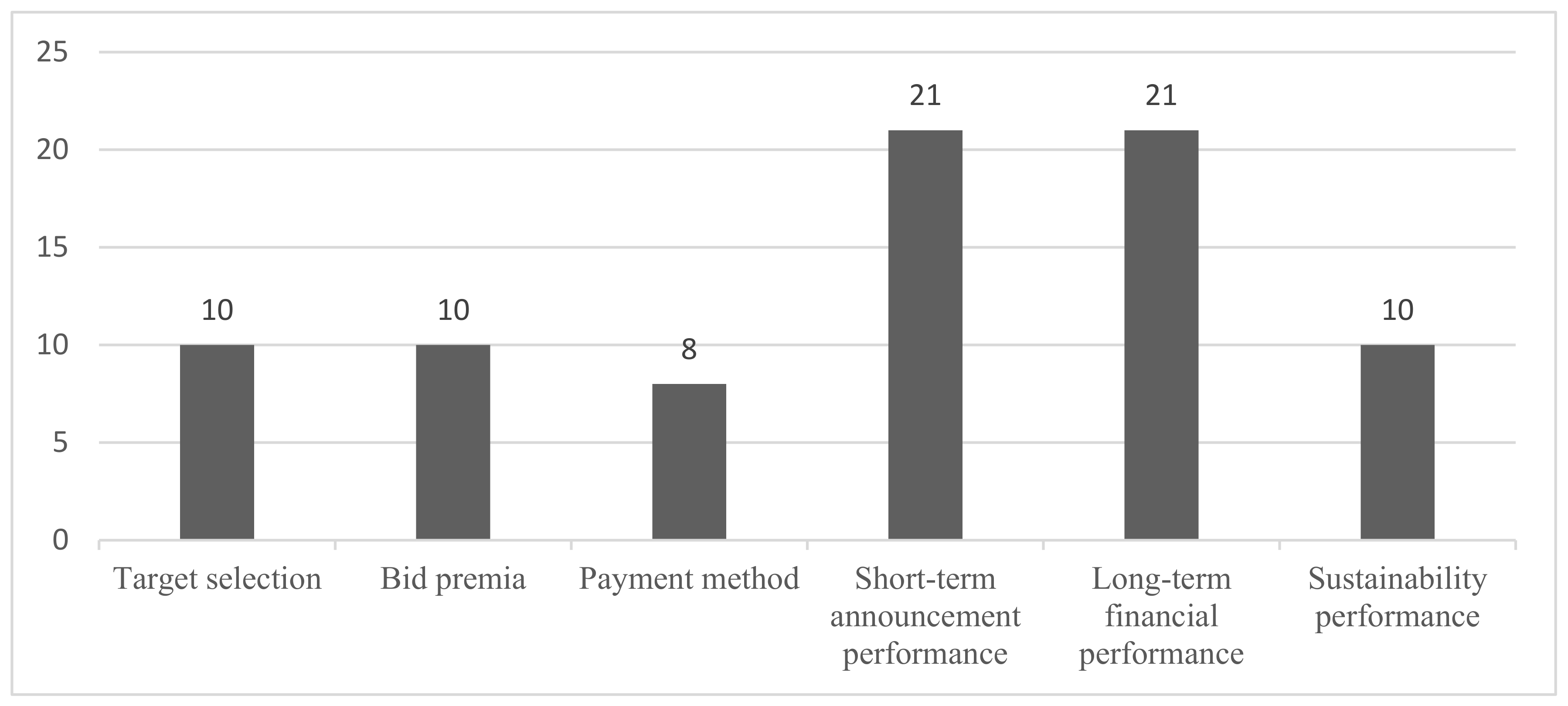

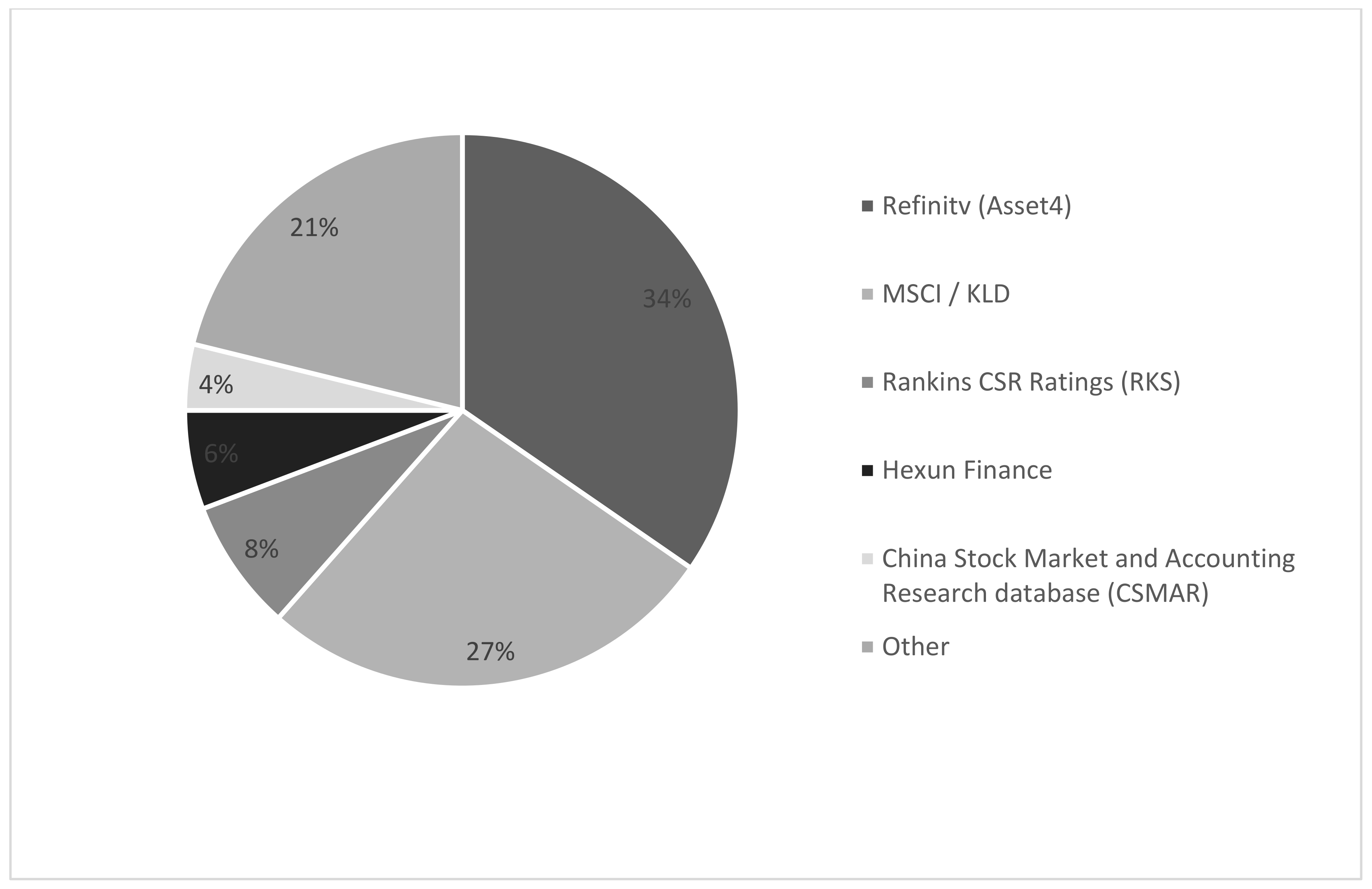

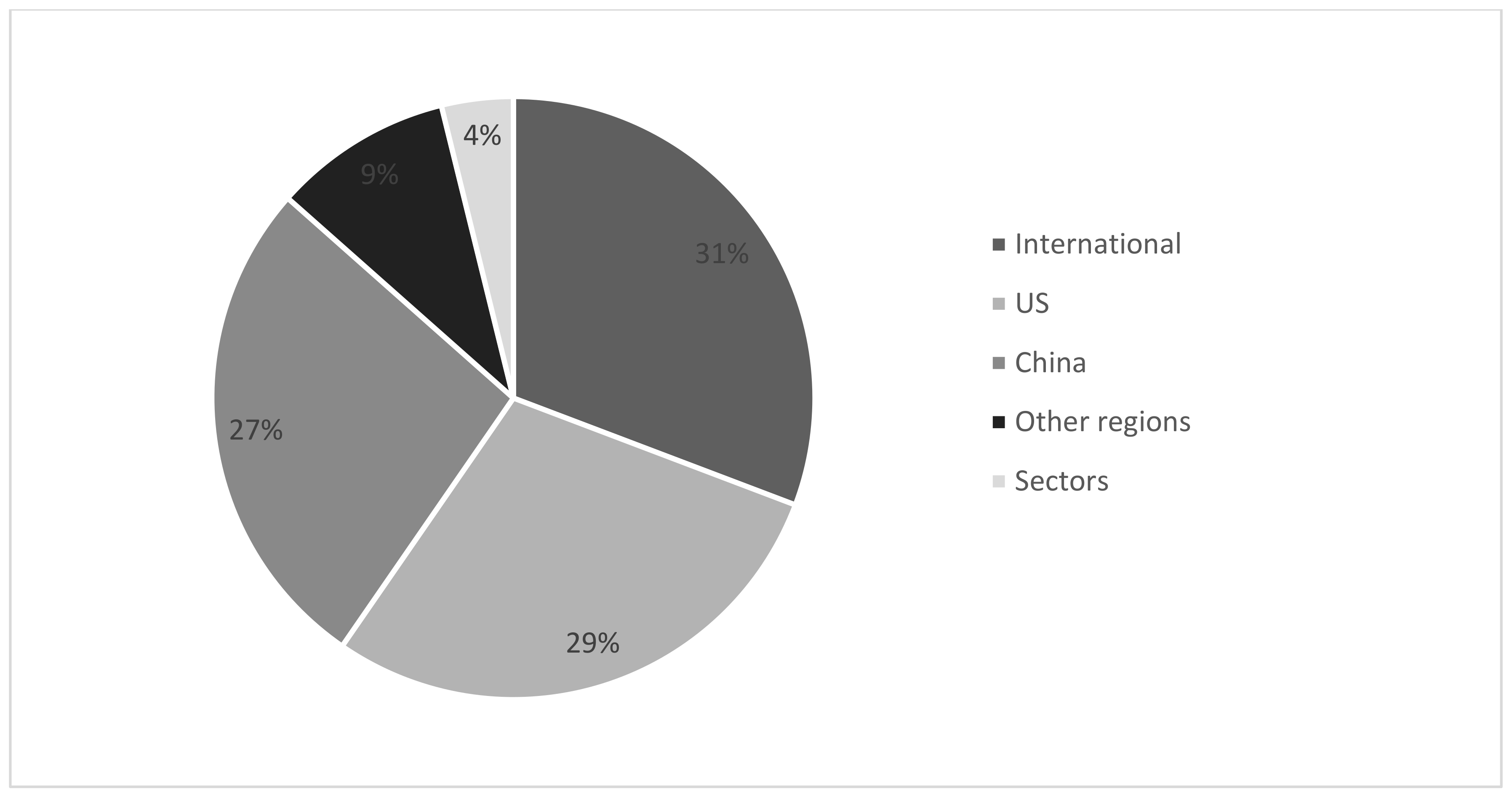

4. Descriptive Statistics of Literature Sample

5. Results

5.1. Pre-Deal Stage

5.1.1. Implications of Sustainability for Target Selection

Acquirer Sustainability Implications for Target Selection

Target Sustainability Implications for Target Selection

Relative Sustainability Implications for Target Selection

5.1.2. Implications of Sustainability for Bid Premium

Acquirer Sustainability Implications for Bid Premium

Target Sustainability Implications for Bid Premium

Relative Sustainability Implications for Bid Premium

5.1.3. Implications of Sustainability for Deal Payment Methods

Acquirer Sustainability Implications for Payment Methods

Target Sustainability Implications for Payment Methods

Relative Sustainability Implications for Payment Methods

5.1.4. Implications of Sustainability for Short-Term Announcement Performance

Acquirer Sustainability Implications for Announcement Performance

Target Sustainability Implications for Announcement Performance

Relative Sustainability Implications for Announcement Performance

5.2. Post-Deal Stage

5.2.1. Implications of Sustainability for Long-Term Financial Performance

Acquirer Sustainability Implications for Financial Performance

Target Sustainability Implications for Financial Performance

Relative Sustainability Implications for Financial Performance

5.2.2. Impact of M&A on Sustainability Performance

Implications of M&A for Acquirer Sustainability

Implications of M&A for Acquirer Sustainability Relative to Target Sustainability

6. Discussion

6.1. Summary and Synthesis

6.2. Limitations and Future Research

6.3. Contribution and Implications

6.3.1. Research and Theoretical Implications

6.3.2. Practical Implications

6.3.3. Regulatory Implications

Author Contributions

Funding

Acknowledgments

Conflicts of Interest

Appendix A. Literature Overview on Relevance and Implications of Sustainability in M&A

| # | Sustainability Focus and Cluster | Authors | Journal | Research Method | Sustainability Rating | Sample | Theory and Perspectives | Finding |

| RQ1: How does sustainability impact target selection? | ||||||||

| Acquirer sustainability | ||||||||

| 1 | M&A activity | Krishnamurti, C; Shams, S; Chowdhury, H, 2021 [63] | Australian Journal of Management | Archival | KLD | US, 1999–2016 | Stakeholder theory; conflict resolution hypothesis | Financially constrained firms that engage in sustainability reduce M&A activity (trade-off); alignment of stakeholders and shareholders for value-maximization purposes |

| 2 | Gul, FA; Krishnamurti, C; Shams, S; Chowdhury, H, 2020 [75] | Journal of Business Research | Archival | KLD | US, 1996–2015 | Agency and stakeholder theoretic perspectives | Sustainability activity at the firm level is negatively related to M&A activity proxying empire-building tendency; CEO overconfidence to increase acquisition activity | |

| 3 | High emission; carbon risks | Bose, S; Minnick, K; Shams, S, 2021 [76] | Journal of Corporate Finance | Archival | ASSET4, CDP | 31 countries, 2006–2018 | Carbon risk mitigation; offshore carbon risk | Increased probabilities of acquiring foreign target for high emission bidders; cross-border M&A as a tool for diversifying carbon emissions risk |

| 4 | Guo, JQ; Cheng, H, 2023 [77] | Environment, Development and Sustainability | Archival | ASSET4 | China, 2002–2021 | World-systems theory | China, rather than developed countries targeted for cross-border activity by acquirers with carbon risks in place, is an effective way to reduce the high costs caused by carbon risks | |

| 5 | Leon-Gonzalez, R; Tole, L, 2015 [78] | Review of Economic Analysis | Archival | Publicly available (e.g., World Bank, ISO), proprietary dataset | Mining industry worldwide, 1994–2006 | Pollution haven hypothesis; environmental stringency in M&A | Countries with weak environmental standards are not attracting companies in the mining industry for foreign investment; industry should focus on policies that improve their environmental record to attract foreign investment | |

| Target sustainability | ||||||||

| 6 | Target probability | Gomes, M, 2019 [26] | Finance Research Letters | Archival | ASSET4 | International, 2003–2014 | Information asymmetry; integration cost; risk reduction | Positive relation between sustainability performance and firms’ probability of being targeted in transactions; negative outcomes decreased; potential cost savings and risk reduction |

| 7 | Ma, X; Xu, XH; Jiang, MB, 2020 [79] | Asia-Pacific Journal of Accounting and Economics | Archival | Rankins CSR Ratings (RKS) | Cross-border China, 2008–2016 | Agency theory; sustainability as a product differentiation device | Likelihood of being targeted in M&A in cross-border deals via enhanced sustainability; sustainability as a product differentiation device in competitive markets | |

| 8 | Fairhurst, D; Greene, DT, 2022 [85] | Journal of Corporate Finance | Archival | KLD | n. a., 1996–2016 | Agency theory; sustainability over- or underinvestment correction | Increasing probability of takeover induced by under- and overinvestment in sustainability; the takeover market acts as an external governance mechanism | |

| 9 | Target social policy | Dicu, RM; Robu, IB; Aevoae, GM; Mardiros, DN, 2020 [84] | Sustainability | Archival | Orbis | Romania, 2010–2018 | Stakeholder theory; cost of employees of a target company hypothesis | Sustainable employee policy as a central interest when acquiring (controlling) interest in a target firm; attention to achieve synergies |

| Relative sustainability | ||||||||

| 10 | Target proximity | Krishnamurti, C; Shams, S; Pensiero, D; Velayutham, E, 2019 [86] | Pacific-Basin Finance Journal | Archival | ASSET4 | Australia, 2000–2016 | Stakeholder theory: minimize social and environmental risks | Higher likelihood of acquiring targets with sustainability practices by sustainability-oriented bidders; better cultural fit; and lower social and environmental risks as motives |

| RQ2: How does sustainability impact bid premia? | ||||||||

| Acquirer sustainability | ||||||||

| 1 | Shareholder expense | Hussaini, M; Hussain, N; Nguyen, DK; Rigoni, U, 2021 [87] | Finance Research Letters | Archival | MSCI | US, 1992–2014 | Agency theory; shareholder expense view | Higher takeover premia paid by acquirers with high sustainability performance; personal objectives as a motivation for management’s sustainability engagement |

| 2 | Ethical attitude | Krishnamurti, C; Shams, S; Pensiero, D; Velayutham, E, 2019 [86] | Pacific-Basin Finance Journal | Archival | ASSET4 | Australia, 2000–2016 | Agency theory; ethically oriented CEOs | Lower likelihood of bid premia by socially responsible firms; ethical attitude of CEOs as a source for high sustainability scores |

| 3 | Trade-off | Krishnamurti, C; Shams, S; Chowdhury, H, 2021 [63] | Australian Journal of Management | Archival | KLD | US, 1999–2016 | Stakeholder theory; conflict resolution view | Companies deciding to trade off between sustainability and M&A investment pay a lower bid premium to target firms for value-creation purposes for acquiring shareholders; the interests of shareholders and stakeholders are aligned by socially responsible managers to promote sustainability while M&A investment levels remain low |

| 4 | Topical complexity | Jost, S; Erben, S; Ottenstein, P; Zulch, H, 2022 [66] | Finance Research Letters | Archival | ASSET4 | International, 2003–2018 | Complexity cannot be fully explained by shareholder or stakeholder theory alone | Size of M&A premia impacted by neither acquirers’ nor targets’ sustainability performance alone; mitigation potential of agency concerns as M&A premia negatively associated with acquirers’ governance quality and sustainability performance |

| Target sustainability | ||||||||

| 5 | Information asymmetry | Gomes, M; Marsat, S, 2018 [64] | Finance Research Letters | Archival | ASSET4 | International, 2003–2014 | Information asymmetry; mitigate the amount of additional risk | Targets’ overall sustainability performance is positively associated with acquisition premium (positive signals, lower specific risk); only in cross-border deals impacted by social performance |

| 6 | Competitive advantage | Qiao, L; Wu, JF, 2019 [92] | Sustainability | Archival | KLD | International cross-border, 1991–2016 | Resourced-based view; better social image; and larger social networks | Higher likelihood of acquisition premium in cases of socially responsible target (sustained competitive advantage); increasing number of fellow acquisitions; institutional and cultural distance to weaken effect |

| 7 | Signaling | Ozdemir, O; Binesh, F; Erkmen, E, 2022 [65] | Review of Managerial Science | Archival | KLD | US Service industry, 1996–2018 | Signaling theory; intangibility of industry | Sustainability performance of targets with increasing effect on deal premia; intangibility of industry to strengthen relations (service firms with more profound effects compared to non-service firms) |

| Relative sustainability | ||||||||

| 8 | Target spread | Cho, K; Han, SH; Kim, HJ; Kim, S, 2021 [60] | Corporate Social Responsibility and Environmental Management | Archival | KLD | US, 1993–2016 | Stakeholder theory: knowledge will increase or maintain relations | Stronger target sustainability performance relative to the acquirer (target spread) to induce a higher premium; takeovers by well-governed acquirers to pronounce sustainability effect in valuation |

| 9 | Synergy and insurance | Li, K; He, CH; Dbouk, W; Zhao, K; 2021 [68] | Sustainability | Archival | China Stock Market and Accounting Research (CSMAR) | China, 2007–2018 | Synergy and post-merger effects; risk mitigation (insurance) | Higher payment of prices and acquisition premia for socially responsible targets; high-sustainability performance of acquirers to reinforce the effect |

| 10 | Pollution haven | Ahmad, MF; Aziz, S; Michiels, Y; Nguyen, DK, 2023 [94] | European Financial Management | Archival | Environmental Performance Index (EPI) | International cross-border, 1991–2016 | Resourced-based view; pollution haven hypothesis | With greater environmental differences between acquirer and target countries, acquirer firms pay higher merger premiums; association is reinforced for both the acquirer and the target firm when deals are conducted in polluting industries |

| RQ3: How does sustainability impact payment methods? | ||||||||

| Acquirer sustainability | ||||||||

| 1 | Agency cost; risk reduction | Krishnamurti, C; Shams, S; Pensiero, D; Velayutham, E, 2019 [86] | Pacific-Basin Finance Journal | Archival | ASSET4 | Australia, 2000–2016 | Stakeholder value maximization view | Cash-only payments in acquisitions have a higher likelihood when the acquirer is a high-sustainability firm |

| 2 | Hussaini, M; Rigoni, U; Perego, P, 2023 [67] | Business Strategy and the Environment | Archival | KLD | US, 1992–2014 | Information asymmetry | The likelihood of cash offers increasing with the sustainability coverage of acquirers and a positive relationship between cash offers and acquirer sustainability concerns | |

| 3 | Regional investor preference | Li, K; He, CH; Dbouk, W; Zhao, K, 2021 [68] | Sustainability | Archival | China Stock Market and Accounting Research (CSMAR) | China, 2007–2018 | Information asymmetry; agency theory; deal risks | Equity payments are preferred by acquirers with high sustainability performance; there is a higher probability of financing being performed as cash payments when the target company has higher sustainability performance |

| 4 | Economic downturn | Kanungo, RP, 2021 [95] | Industrial Marketing Management | Archival | CSRHub database | UK, 2007–2010 | Information asymmetry | Choice of payment is influenced by the financial crisis; the likelihood of stock payments is higher for sustainability-pursuing acquirers during crises |

| Target sustainability | ||||||||

| 5 | Information asymmetry, investor concerns | Hussaini, M; Rigoni, U; Perego, P, 2023 [67] | Business Strategy and the Environment | Archival | KLD | US, 1992–2014 | Information asymmetry | Cash offers are positively associated with sustainability when covered by targets (incremental information reduces information asymmetry); there is no effect of target sustainability strength on payment type |

| 6 | Li, K; He, CH; Dbouk, W; Zhao, K, 2021 [68] | Sustainability | Archival | China Stock Market and Accounting Research (CSMAR) | China, 2007–2018 | Information asymmetry; agency theory; risk | Equity payments are preferred by acquirers with high sustainability performance; there is a higher probability of financing being performed as cash payments when the target company has higher sustainability performance | |

| Relative sustainability | ||||||||

| 7 | Portability; exposure to governance standards | Hussain, T; Shams, S, 2022 [96] | International Review of Financial Analysis | Archival | Refinitiv | International, 2003–2016 | Portability theory: stock deals as an instrument for governance changes | Bidder companies with better pre-deal sustainability than the target company use stock payments to enable governance changes in line with the portability of good sustainability standards |

| 8 | Culture fit; uncertainties | Alexandridis, G; Hoepner, AGF; Huang, ZY; Oikonomou, I, 2022 [62] | British Accounting Review | Archival | EIRIS | 22 International markets, 2004–2012 | Corporate cultural divergence; cultural clash hypothesis | Higher probability of cash payments for deals when divergence of corporate social culture between acquirer and target is widening |

| RQ4: How does sustainability impact short-term announcement (financial) performance? | ||||||||

| Acquirer sustainability | ||||||||

| 1 | Stakeholder view | Deng, X; Kang, JK; Low, BS, 2013 [52] | Journal of Financial Economics | Archival | KLD | US, 1992–2007 | Stakeholder theory | Higher merger announcement return realization by high-sustainability acquirers: the value-weighted portfolio of the acquirer and the target realize higher announcement returns |

| 2 | Shi, JY; Yu, CH; Li, YX, 2022 [100] | Emerging Markets Finance and Trade | Archival | China Stock Market and Accounting Research (CSMAR) | China cross-border, 2010–2018 | Stakeholder and shareholder theory complementarity; two long competitive theories | Higher CAR realization by acquirers having extremely low or high levels of sustainability; non-linear U-shaped relation around the announcement of cross-border deals; net reaction to be interpreted as the net result of positive and negative reactions | |

| 3 | Arouri, M; Gomes, M; Pukthuanthong, K, 2019 [98] | Journal of Corporate Finance | Archival | ASSET4 | International M&A, 2004–2016 | Stakeholder theory | Market M&A outcome assessment is influenced by sustainability; perceived risk surrounding M&A operations is determined by sustainability; strong sustainability reduces M&A completion risk | |

| 4 | Li, JJ; Wu, XM, 2022 [120] | Applied Economics Letters | Archival | Hexun Finance: divided CSR into four dimensions | China cross-border, 2010–2019 | Theory of stakeholder interests | Non-unitary impact of sustainability on returns of cross-border M&As in China; promotion of acquirer returns for suppliers; consumer responsibility and social contribution of firms; negative effects of shareholder responsibility and environmental responsibility | |

| 5 | Investor preferences, no sustainability consideration | Li, MH; Lan, FQ; Zhang, F, 2019 [101] | Sustainability | Archival | Hexun Finance | China, 2010–2017 | Systematic and idiosyncratic risk; investor preferences | There is no significant sustainability impact on CAR; M&A premia are not reduced by better levels of the acquirer’s sustainability; Chinese financial market investors without consideration of sustainability prior to M&A deals |

| 6 | Yen, T.; André, P., 2019 [89] | Quarterly Review of Economics and Finance | Archival | ASSET4 | 23 Emerging markets, 2008–2014 | Investor cost–benefit: neither the positive stakeholder nor the negative shareholder view alone can explain the effects | Response to M&A events driven by the own cost–benefit concerns of investors for acquirers’ pre-merger sustainability performance effects: acquirers’ pre-merger sustainability performance is not considered a signal announcement by market investors with sustainability agency concerns | |

| 7 | Zhang, F; Li, MH; Zhang, ML, 2019 [102] | Sustainability | Archival | Hexun Finance | China, 2010–2017 | Effectiveness of China’s securities market | Acquirers possessing lower sustainability performance in the year prior to a deal are more likely valued by the Chinese investor market; short-term profits of enterprises are in focus, and long-term sustainability is out of focus | |

| 8 | Economic downturn | Tampakoudis, I; Noulas, A; Kiosses, N; Drogalas, G, 2021 [103] | Corporate Governance | Archival | ASSET4 | US, 2018–2020 | Shareholder theory; costs of sustainability activities | Acquiring shareholders experience negative valuation impacts for sustainability performance for the whole sample period and negative impacts exacerbated by the COVID-19 crisis; economic downturns indicate an outweighing of the cost of sustainability activities versus possible gains |

| 9 | Complexity, integration lead time | Caiazza, S; Galloppo, G; Paimanova, V, 2021 [47] | Journal of Cleaner Production | Archival | ASSET4 | Hospitality sector for targets, 2000–2019 | Complexity of the post-merger integration; integration problems | Sustainability and non-sustainability companies are not distinguished by investors on announcements; corporate sustainability capital is a process-winning strategy only for cases with long-term focus and consideration |

| 10 | Huang, CJ; Ke, WC; Chiang, RPY; Jhong, YC, 2023 [48] | Journal of Cleaner Production | Archival | Refinitiv | American acquirer, 2003–2020 | Stakeholder theory; complexity of M&A operations | Synergy does not come immediately, and for short-term performance, sustainability is irrelevant; only one to three years after the announcement of M&A is sustainability relevant | |

| 11 | Hostile takeover | Zhang, TT; Zhang, ZY; Yang, JY, 2022 [99] | Journal of Business Ethics | Archival | ASSET4 | 23 developed economies, 2002–2012 | Stakeholder theory; insurance prevention; hostile takeover as a negative signal | Acquirer returns around announcement windows enhanced with pre-announcement sustainability engagement of an acquirer (insurance-like effect of sustainability engagement); offsetting of the insurance-like effect of the acquirer’s high sustainability in case of hostile takeovers |

| Target sustainability | ||||||||

| 12 | Learning opportunity | Aktas N; de Bodt E; Cousin J; 2011 [30] | Journal of Banking and Finance | Archival | Intangible Value Assessment (IVA); two components of the IVA score: environmental and social ratings | International, 1997–2007 | SRI value-enhancing; learning hypothesis | Positive relation between acquirer abnormal returns and targets’ social and environmental performance; the better the target’s performance on environmental and social dimensions, the higher the gain for shareholders of acquirers |

| 13 | Stakeholder preservation | Tong, L; Wang, HL; Xia, J, 2020 [104] | Academy of Management Journal | Archival | KLD | US, 2000–2012 | Stakeholder theory; stakeholder preservation perspective | Positive relation between the target sustainability and the abnormal return of the acquirer upon the announcements of acquisitions; association reinforced by higher levels of stakeholder value congruence and reduced by higher business similarity of transaction parties |

| 14 | Overinvested target | Wang, ZK; Lu, WJ; Liu, M, 2021 [107] | International Review of Financial Analysis | Archival | KLD (MSCI) | US, 1996–2007 | Agency theory | Significantly declining market reactions to M&A announcements of acquirers when purchasing sustainability-overinvesting targets |

| Relative sustainability | ||||||||

| 15 | Portability channel | Hussain, T; Shams, S, 2022 [96] | International Review of Financial Analysis | Archival | Refinitiv | International, 2003–2016 | Portability theory | Portability of good sustainability standards in mergers as the takeover market works as a vehicle for it; positive stock-market reaction to announcements while distribution of returns is asymmetric for merging firms; bidders gain and targets lose value |

| 16 | Target spread | Teti, E; Dell’Acqua, A; Bonsi, P, 2022 [105] | Corporate Social Responsibility and Environmental Management | Archival | ASSET4 | International, n.a. | Stakeholder theory: value creation taking over a target of higher sustainability performance | Acquisition of targets with higher sustainability beneficial for bidders (target spread); from the perspective of the stock market, a higher sustainability score to generate value; superior standards in corporate governance with a positive impact on takeover performance |

| 17 | Chen, C; Lu, WJ; Liu, M, 2022 [106] | Asia-Pacific Journal of Accounting and Economics | Archival | KLD | US, 1995–2014 | Sustainability spread and synergy gain; learning from the target’s CSR practices | Acquirer shareholders gain by investing in higher sustainability targets; the higher the acquirer gains, the stronger the target’s sustainability performance relative to the acquirer firm | |

| 18 | Carbon risk; pollution haven | Bose, S; Minnick, K; Shams, S, 2021 [76] | Journal of Corporate Finance | Archival | ASSET4 | Across 31 countries, 2006–2018 | Cost of carbon risk, carbon risk mitigation, and offshoring carbon risk | Acquirers with higher carbon emissions have lower announcement returns (emissions proxies are negative and statistically significant); cross-border acquisition announcement returns are expected to increase for high-carbon emitters acquiring targets located in weak regulation and governance countries with lower prosperity |

| 19 | Ahmad, MF; Aziz, S; Michiels, Y; Nguyen, DK, 2023 [94] | European Financial Management | Archival | Environmental Performance Index (EPI) | International cross-border, 2011–2020 | Pollution haven hypothesis: an indicator of a firm’s commitment or exploitation | Higher cumulative abnormal returns around merger announcements are realized with greater environmental sustainability differences between the acquirer and target countries | |

| 20 | Culture; corporate proximity | Doukas, JA; Zhang, RY, 2021 [61] | Journal of Corporate Finance | Archival | KLD | US, 1992–2017 | Cultural similarity/proximity; managerial ability | M&A synergies are constituted by corporate cultural similarity; higher cultural similarity levels lead to strong positive market reactions |

| 21 | Alexandridis, G; Hoepner, AGF; Huang, ZY; Oikonomou, I, 2022 [62] | British Accounting Review | Archival | EIRIS | 22 international markets, 2004–2012 | Corporate cultural divergence | Lower acquirer announcements and synergistic gains are triggered by a wider divergence between the sustainability corporate cultures of the acquiring and target entities | |

| RQ5: How does sustainability impact long-term financial performance? | ||||||||

| Acquirer sustainability | ||||||||

| 1 | Stakeholder view: marked-based performance | Deng, X; Kang, JK; Low, BS, 2013 [52] | Journal of Financial Economics | Archival | KLD | US, 1992–2007 | Stakeholder value maximization view | Portfolios of high-sustainability acquirers realizing significantly positive abnormal returns for holding periods of two and three years indicate larger improvements in post-merger long-term operations; acquirers’ social performance is identified as an important determinant of merger returns |

| 2 | Bettinazzi, ELM; Zollo, M, 2017 [108] | Strategic Management Journal | Archival | ASSET4 | US, 2002–2010 | Stakeholder-based view | Acquisition performance is positively associated with acquirers’ stakeholder orientation; performance is positively moderated by business-relatedness (importance of knowledge transfer) | |

| 3 | Qiao, MZ; Xu, SW; Wu, GD, 2018 [58] | Sustainability | Archival | Rankins CSR Ratings (RKS) | China, 2012–2014 | Stakeholder and social contracts; geographical differences; synergy and spillover; learning effects | Acquirer’s sustainability performance with a significant and positive effect on long-term M&A performance in China; more significant sustainability effects on M&A performance for related-party M&As; significant differences present across geographical regions in the association context | |

| 4 | Zheng, ZG; Li, JR; Ren, XZ; Guo, JM, 2023 [109] | Pacific-Basin Finance Journal | Archival | Sino-Securities Index (SSI) ESG Rating | China, 2011–2019 | Instrumental stakeholder theory: post-merger synergy creation | Acquirers’ sustainability rating is positively associated with post-M&A performance; sustainability upgrade and downgrade effects depend on sustainability initial levels | |

| 5 | Huang, CJ; Ke, WC; Chiang, RPY; Jhong, YC, 2023 [48] | Journal of Cleaner Production | Archival | Refinitiv | American acquirer, 2003–2020 | Stakeholder theory: long-term synergy creation | Long-term M&A success by acquirers fulfilling environmental and social responsibility such as human rights, working conditions, health and safety, and career development and training; financial performance in M&A mostly impacted by social pillar | |

| 6 | Stakeholder view: accounting-based performance | Caiazza, S; Galloppo, G; Paimanova, V, 2021 [47] | Journal of Cleaner Production | Archival | ASSET4 | Hospitality sector for targets, 2000–2019 | Complexity of the post-merger integration | In the long run, stronger social and sustainability capital involvement is likely associated with an improvement in corporate performance |

| 7 | Kim, BJ; Jung, JY; Cho, SW, 2022 [110] | Borsa Istanbul Review | Archival | KCGS ratings | Korean cross-border, 2012–2018 | Stakeholder theory; business efficiency | Business performance in cross-border M&A is positively impacted by better sustainability engagement, overcoming diversification discounts through a friendly channel of sustainability engagement | |

| 8 | Zheng, ZG; Li, JR; Ren, XZ; Guo, JM, 2023 [109] | Pacific-Basin Finance Journal | Archival | Sino-Securities Index (SSI) ESG Rating | China, 2011–2019 | Instrumental stakeholder theory: post-merger synergy creation | Acquirers’ sustainability rating is positively associated with post-M&A performance; sustainability upgrade and downgrade effects depend on sustainability initial levels | |

| 9 | Huang, CJ; Ke, WC; Chiang, RPY; Jhong, YC, 2023 [48] | Journal of Cleaner Production | Archival | Refinitiv | American acquirer, 2003–2020 | Stakeholder theory: long-term synergy creation | Long-term M&A success by acquirers fulfilling environmental and social responsibility such as human rights, working conditions, health and safety, and career development and training; financial performance in M&A mostly impacted by social pillar | |

| 10 | Trade-off | Krishnamurti, C; Shams, S; Chowdhury, H, 2021 [63] | Australian Journal of Management | Archival | KLD | US, 1999–2016 | Stakeholder theory; conflict resolution view | Linking negative sustainability–M&A relation (trade-off) to value creation proved by long-run stock returns; the tendency of sustainability firms’ low engagements in M&A investments is valid only for firms with no financial slack; firm performance further positive impact of sustainability engagement on Tobin’s Q when firm-level sustainability commitments increase alongside a reduction in the number of M&As |

| 11 | No long-term improvement: shareholder view; passive sustainability | Li, MH; Lan, FQ; Zhang, F, 2019 [101] | Sustainability | Archival | Hexun Finance | China, 2010–2017 | Systematic and idiosyncratic risk; passive sustainability | M&A without improvement in the company’s ROA for a long time; within one year after M&A, sustainability only increases the return on assets of the firm |

| 12 | Yen, T.; André, P., 2019 [89] | Quarterly Review of Economics and Finance | Archival | ASSET4 | 23 Emerging markets, 2008–2014 | Shareholder and synergy hypothesis: short-term market performance based on investors’ rational expectations | In the long run, cross-border deals conducted by emerging market sample acquirers fail to reveal significantly improving post-merger financials; there is a negative association between operating improvements and pre-merger sustainability performance | |

| Target sustainability | ||||||||

| 13 | Host country carbon emission: accounting performance | Liu, K; Wu, SY; Guo, N; Fang, QL, 2021 [111] | Journal of Cleaner Production | Archival | WDI (World Development Indicators) database | Chinese listed companies cross-border, 2007–2016 | Pollution paradise hypothesis; environmental Kuznets curve (EKC) hypothesis | Host country carbon emissions as a source of acquirer performance are evidenced by significant positive ΔROE1, ΔROE2; significant negative association of carbon emission intensity, per capita income, carbon emission intensity, and environmental vulnerability, with indication of increasing environmental vulnerability of the host country to inhibit country carbon emissions as a cross-border M&A performance source |

| 14 | Host country carbon emission: market performance | Liu, K; Wu, SY; Guo, N; Fang, QL, 2021 [111] | Journal of Cleaner Production | Archival | WDI (World Development Indicators) database | Chinese listed companies cross-border, 2007–2016 | Pollution paradise hypothesis; environmental Kuznets curve (EKC) hypothesis | Host country carbon emissions as a source of acquirer performance are evidenced by a significant positive BHAR and a significant negative association of carbon emission intensity, per capita income, carbon emission intensity, and environmental vulnerability, with an indication of the increasing environmental vulnerability of the host country to inhibit country carbon emissions as a cross-border M&A performance source |

| 15 | Overinvested target | Wang, ZK; Lu, WJ; Liu, M, 2021 [107] | International Review of Financial Analysis | Archival | KLD (MSCI) | US, 1996–2007 | Agency theory: sustainability expenditure exceeding the optimal level | Significantly deteriorating financial performance for acquirers when purchasing sustainability-overinvesting targets; combined firm with unnecessary sustainability assets and future company also overinvest in sustainability (value destruction) |

| Relative sustainability | ||||||||

| 16 | Target spread | Tampakoudis, I; Anagnostopoulou, E, 2020 [9] | Business Strategy and the Environment | Archival | ASSET4 | EU, 2003–2017 | Stakeholder theory | Evidence partially provides for a positive association between the post-merger market value of the acquirer firm and the acquisition of a target with superior sustainability (target spread) |

| 17 | Choi, G; Kim, TN, 2022 [112] | Business and Society Review | Archival | KLD | US, 1995–2013 | Stakeholder theory: a supportive relationship with the target’s diverse stakeholders | Higher post-announcement stock returns than others when acquirer firms are supporting targets’ superior overall sustainability | |

| 18 | Chen, C; Lu, WJ; Liu, M, 2022 [106] | Asia-Pacific Journal of Accounting and Economics | Archival | KLD | US, 1995–2014 | Sustainability spread and synergy gain; learning from the target’s practices | Acquisitions of targets with higher sustainability document subsequent acquirer’s improvements in market performance; value generation by learning from their targets with respect to sustainability practices and experiences | |

| 19 | Culture proximity; post-deal integration | Doukas, JA; Zhang, RY, 2021 [61] | Journal of Corporate Finance | Archival | KLD | US, 1992–2017 | Cultural similarity and proximity | Tendency of target acquisition with similar corporate social culture by high-level sustainability companies led by talented managers; significant positive post-merger returns indicate synergy creation in M&A due to cultural similarity |

| 20 | Feng, X, 2021 [113] | Green Finance | Archival | ASSET4 | International, 2000–2020 | Corporate culture similarity; integration cost | Exacerbated ROA decline for low-sustainability acquirers in comparison to relief for high-sustainability acquirers; temporary integration costs are higher for low-sustainability acquirers than for high-sustainability peers in cases where the target’s sustainability level increases | |

| 21 | Alexandridis, G; Hoepner, AGF; Huang, ZY; Oikonomou, I, 2022 [62] | British Accounting Review | Archival | EIRIS | 22 international markets, 2004–2012 | Corporate cultural divergence; cultural clash hypothesis | Lower long-term returns as well as lower synergistic gains are related to a greater divergence between the sustainability corporate cultures of the acquiring and target firms; moreover, increases in the time required for deal finalization | |

| RQ6: How does M&A impact sustainability performance? | ||||||||

| M&A impact on acquirer sustainability | ||||||||

| 1 | Stakeholder view; strategic perspective | Caiazza, S; Galloppo, G; Paimanova, V, 2021 [47] | Journal of Cleaner Production | Archival | ASSET4 | Hospitality sector for targets, 2000–2019 | Stakeholder theory | Up to three years later, the merger acquirer’s sustainability is strongly influenced by the merger; the impact of sustainability on maximizing value for shareholders in the short term is irrelevant |

| 2 | Barros, V; Matos, PV; Sarmento, JM; Vieira, PR, 2022 [8] | Technological Forecasting and Social Change | Archival | ASSET4 (Refinitiv) | 41 countries, 2002–2020 | Strategic perspective of M&A and motivation for increasing sustainability | M&A deals significantly increasing sustainability performance the year following the transaction are considered on their own (not in the year of the deal); similar results for the single pillars of environmental, social, and governance | |

| 3 | Knowledge channel cross-border deals | Li, Z; Wang, P, 2023 [116] | Journal of Business Finance and Accounting | Archival | Rankins CSR Ratings (RKS) | China cross-border, 2009–2017 | Legitimacy and institutional theories | Improvement in acquirers’ subsequent sustainability performance following cross-border M&A activities; sustainability as a vehicle for acquirers from a country possessing low institutional quality to bond themselves for a better reputation |

| 4 | Chen, XM; Liang, X; Wu, H, 2023 [115] | Journal of Business Ethics | Archival | Rankins CSR Ratings (RKS) | China cross-border, 2008–2015 | Signaling theory | Post-cross-border M&A increase in sustainability performance and sustainability spending; via cross-border M&As signaling commitment through cross-border M&As and sustainability know-how obtained | |

| 5 | Yang, N; Zhang, Y; Yu, L; Wang, J; Liu, XM, 2022 [114] | International Review of Economics and Finance | Archival | Chinese Corporate Social Responsibilities Database (CCSR) | China cross-border, 2007–2018 | Learning theory | Chinese acquirers’ sustainability as well as detailed dimensions post-deal are positively impacted by cross-border M&As; regional cultural diversity reinforces the effect as a positive moderator | |

| 6 | Green M&A; green technology | Choi, G; Kim, TN, 2022 [112] | Business and Society Review | Archival | KLD | US, 1995–2013 | Green technology acquisition | Acquirers generally do support the target’s better environmental and product sustainability; any of the target’s greater sustainability issues are not corrected by acquirers |

| 7 | Zhao, XY; Jia, M, 2022 [117] | Environmental Science and Pollution Research | Archival | Calculated rating proxy | China heavy-polluting firms, 2009–2017 | Legitimacy theory | Environmental management improved via corporate green M&A activity; positive associations were alleviated for firms in localities under considerable media scrutiny; state-owned enterprises (SOEs) weakened the relationship | |

| M&A impact on acquirer sustainability relative to target sustainability | ||||||||

| 8 | Target spread | Aktas N; de Bodt E; Cousin J, 2011 [30] | Journal of Banking and Finance | Archival | Intangible Value Assessment (IVA); two components of the IVA score: environmental and social ratings | International, 1997–2007 | Learning hypothesis | Positive relation between the rating spread (between the target and the acquirer) and the change in acquirer rating following M&A; learning channel for acquirers via target’s SRI experiences and practices |

| 9 | Tampakoudis, I; Anagnostopoulou, E, 2020 [9] | Business Strategy and the Environment | Archival | ASSET4 | EU, 2003–2017 | Stakeholder theory: learn and incorporate target practices | Acquirers’ post-merger sustainability performance is positively affected by the pre-merger relative target/acquirer sustainability performance; in the post-merger stage, integration of the target’s sustainability practices into the acquirers’ sustainability | |

| 10 | Chen, C; Lu, WJ; Liu, M, 2022 [106] | Asia-Pacific Journal of Accounting and Economics | Archival | KLD | US, 1995–2014 | Learning theory | The stronger the target spread (target’s sustainability performance relative to the acquirer), the higher the created acquirer gains as well as synergy for acquirers; gain by learning from their targets considering sustainability experiences and practices | |

References

- Kastrinos, N.; Weber, K.M. Sustainable Development Goals in the Research and Innovation Policy of the European Union. Technol. Forecast. Soc. Chang. 2020, 157, 120056. [Google Scholar] [CrossRef]

- Leal Filho, W.; Tripathi, S.K.; Andrade Guerra, J.B.S.O.D.; Giné-Garriga, R.; Orlovic Lovren, V.; Willats, J. Using the Sustainable Development Goals towards a Better Understanding of Sustainability Challenges. Int. J. Sustain. Dev. World Ecol. 2019, 26, 179–190. [Google Scholar] [CrossRef]

- Allen, C.; Metternicht, G.; Wiedmann, T. Initial Progress in Implementing the Sustainable Development Goals (SDGs): A Review of Evidence from Countries. Sustain. Sci. 2018, 13, 1453–1467. [Google Scholar] [CrossRef]

- United Nations Transforming Our World: The 2030 Agenda for Sustainable Development. Available online: https://sdgs.un.org/publications/transforming-our-world-2030-agenda-sustainable-development-17981 (accessed on 20 December 2023).

- United Nations The Paris Agreement. Available online: https://unfccc.int/process-and-meetings/the-paris-agreement (accessed on 20 December 2023).

- Eliasson, K.; Wibeck, V.; Neset, T.S. Opportunities and Challenges for Meeting the Un 2030 Agenda in the Light of Global Change-A Case Study of Swedish Perspectives. Sustainability 2019, 11, 5221. [Google Scholar] [CrossRef]

- Farisyi, S.; Al Musadieq, M.; Utami, H.N.; Damayanti, C.R. A Systematic Literature Review: Determinants of Sustainability Reporting in Developing Countries. Sustainability 2022, 14, 1022. [Google Scholar] [CrossRef]

- Barros, V.; Verga Matos, P.; Miranda Sarmento, J.; Rino Vieira, P. M&A Activity as a Driver for Better ESG Performance. Technol. Forecast. Soc. Chang. 2022, 175, 121338. [Google Scholar] [CrossRef]

- Tampakoudis, I.; Anagnostopoulou, E. The Effect of Mergers and Acquisitions on Environmental, Social and Governance Performance and Market Value: Evidence from EU Acquirers. Bus. Strateg. Environ. 2020, 29, 1865–1875. [Google Scholar] [CrossRef]

- Velte, P. Determinants and Financial Consequences of Environmental Performance and Reporting: A Literature Review of European Archival Research. J. Environ. Manag. 2023, 340, 117916. [Google Scholar] [CrossRef]

- Ben-David, I.; Jang, Y.; Kleimeier, S.; Viehs, M. Exporting Pollution: Where Do Multinational Firms Emit CO2? Econ. Policy 2021, 36, 377–437. [Google Scholar] [CrossRef]

- Salvi, A.; Petruzzella, F.; Giakoumelou, A. Green M&A Deals and Bidders’ Value Creation: The Role of Sustainability in Post-Acquisition Performance. Int. Bus. Res. 2018, 11, 96. [Google Scholar] [CrossRef]

- BCG. Green Deals Gain Steam|The 2022 M&A Report; BCG: Boston, MA, USA, 2022. [Google Scholar]

- Li, M.; Tian, Z.; Liu, Q.; Lu, Y. Literature Review and Research Prospect on the Drivers and Effects of Green Innovation. Sustainability 2022, 14, 9858. [Google Scholar] [CrossRef]

- Cellier, A.; Chollet, P. The Effects of Social Ratings on Firm Value. Res. Int. Bus. Financ. 2016, 36, 656–683. [Google Scholar] [CrossRef]

- Yan, S.; Ferraro, F.; Almandoz, J. The Rise of Socially Responsible Investment Funds: The Paradoxical Role of the Financial Logic. Adm. Sci. Q. 2019, 64, 466–501. [Google Scholar] [CrossRef]

- Zaccone, M.C.; Pedrini, M. ESG Factor Integration into Private Equity. Sustainability 2020, 12, 5725. [Google Scholar] [CrossRef]

- Carroll, A.B. Corporate Social Responsibility: The Centerpiece of Competing and Complementary Frameworks. Organ. Dyn. 2015, 44, 87–96. [Google Scholar] [CrossRef]

- Abad-Segura, E.; Cortés-García, F.J.; Belmonte-Ureña, L.J. The Sustainable Approach to Corporate Social Responsibility: A Global Analysis and Future Trends. Sustainability 2019, 11, 5382. [Google Scholar] [CrossRef]

- González-Torres, T.; Rodríguez-Sánchez, J.-L.; Pelechano-Barahona, E.; García-Muiña, F.E. A Systematic Review of Research on Sustainability in Mergers and Acquisitions. Sustainability 2020, 12, 513. [Google Scholar] [CrossRef]

- Franklin, J. ESG Now a Key Factor in M&A. Int. Financ. Law Rev. 2019. [Google Scholar]

- Ahammad, M.F. The Role of Sustainability in Mergers & Acquisitions: A Literature Review. In Advances in Mergers and Acquisitions; Emerald Publishing Limited: Bingley, UK, 2023; Volume 22, pp. 19–30. [Google Scholar]

- Junni, P.; Teerikangas, S. Mergers and Acquisitions. In Oxford Research Encyclopedia of Business and Management; Oxford University Press: Oxford, UK, 2019. [Google Scholar]

- Gomes, E.; Angwin, D.N.; Weber, Y.; Yedidia Tarba, S. Critical Success Factors through the Mergers and Acquisitions Process: Revealing Pre- and Post-M&A Connections for Improved Performance. Thunderbird Int. Bus. Rev. 2013, 55, 13–35. [Google Scholar] [CrossRef]

- Ahammad, M.F.; Glaister, K.W. The Pre-Acquisition Evaluation of Target Firms and Cross Border Acquisition Performance. Int. Bus. Rev. 2013, 22, 894–904. [Google Scholar] [CrossRef]

- Gomes, M. Does CSR Influence M&A Target Choices? Financ. Res. Lett. 2019, 30, 153–159. [Google Scholar] [CrossRef]

- Ciambotti, M.; Aureli, S.; Demartini, P. Italy: Demand for Social Responsibility in Mergers and Acquisitions. J. Corp. Account. Financ. 2011, 22, 45–50. [Google Scholar] [CrossRef]

- Varaiya, N.P. Determinants of Premiums in Acquisition Transactions. Manag. Decis. Econ. 1987, 8, 175–184. [Google Scholar] [CrossRef]

- Betton, S.; Eckbo, B.E.; Thorburn, K.S. Corporate Takeovers. In Handbook of Empirical Corporate Finance; Elsevier: Amsterdam, The Netherlands, 2008; pp. 291–429. [Google Scholar]

- Aktas, N.; de Bodt, E.; Cousin, J.G. Do Financial Markets Care about SRI? Evidence from Mergers and Acquisitions. J. Bank. Financ. 2011, 35, 1753–1761. [Google Scholar] [CrossRef]

- Zollo, M.; Meier, D. What Is M&A Performance? Acad. Manag. Perspect. 2008, 22, 55–77. [Google Scholar] [CrossRef]

- Kirkulak Uludag, B. Mergers and Acquisitions. In Encyclopedia of Corporate Social Responsibility; Springer: Berlin/Heidelberg, Germany, 2013; pp. 1652–1658. [Google Scholar]

- Calipha, R.; Tarba, S.; Brock, D. Mergers and Acquisitions: A Review of Phases, Motives, and Success Factors. In Advances in Mergers and Acquisitions; Emerald Publishing Limited: Bingley, UK, 2010; Volume 9, pp. 1–24. [Google Scholar]

- Purvis, B.; Mao, Y.; Robinson, D. Three Pillars of Sustainability: In Search of Conceptual Origins. Sustain. Sci. 2019, 14, 681–695. [Google Scholar] [CrossRef]

- Dahlsrud, A. How Corporate Social Responsibility Is Defined: An Analysis of 37 Definitions. Corp. Soc. Responsib. Environ. Manag. 2008, 15, 1–13. [Google Scholar] [CrossRef]

- van Marrewijk, M. Concepts and Definitions of CSR and Corporate Sustainability: Between Agency and Communion. J. Bus. Ethics 2003, 44, 95–105. [Google Scholar] [CrossRef]

- Huang, X.B.; Watson, L. Corporate Social Responsibility Research in Accounting. J. Account. Lit. 2015, 34, 1–16. [Google Scholar] [CrossRef]

- Bansal, P.; Song, H.C. Similar but Not the Same: Differentiating Corporate Sustainability from Corporate Responsibility. Acad. Manag. Ann. 2017, 11, 105–149. [Google Scholar] [CrossRef]

- Freeman, R.E. Strategic Management: A Stakeholder Approach; Cambridge University: Cambridge, UK, 1984; ISBN 978-0273019138. [Google Scholar]

- Chatterji, A.K.; Durand, R.; Levine, D.I.; Touboul, S. Do Ratings of Firms Converge? Implications for Managers, Investors and Strategy Researchers. Strateg. Manag. J. 2016, 37, 1597–1614. [Google Scholar] [CrossRef]

- Berg, F.; Kölbel, J.F.; Rigobon, R. Aggregate Confusion: The Divergence of ESG Ratings. Rev. Financ. 2022, 26, 1315–1344. [Google Scholar] [CrossRef]

- Jámbor, A.; Zanócz, A. The Diversity of Environmental, Social, and Governance Aspects in Sustainability: A Systematic Literature Review. Sustainability 2023, 15, 13958. [Google Scholar] [CrossRef]

- Servaes, H.; Tamayo, A. The Impact of Corporate Social Responsibility on Firm Value: The Role of Customer Awareness. Manag. Sci. 2013, 59, 1045–1061. [Google Scholar] [CrossRef]

- Flammer, C. Does Corporate Social Responsibility Lead to Superior Financial Performance? A Regression Discontinuity Approach. Manag. Sci. 2015, 61, 2549–2568. [Google Scholar] [CrossRef]

- Ioannou, I.; Serafeim, G. The Impact of Corporate Social Responsibility on Investment Recommendations: Analysts’ Perceptions and Shifting Institutional Logics. Strateg. Manag. J. 2015, 36, 1053–1081. [Google Scholar] [CrossRef]

- Dhaliwal, D.S.; Radhakrishnan, S.; Tsang, A.; Yang, Y.G. Nonfinancial Disclosure and Analyst Forecast Accuracy: International Evidence on Corporate Social Responsibility Disclosure. Account. Rev. 2012, 87, 723–759. [Google Scholar] [CrossRef]

- Caiazza, S.; Galloppo, G.; Paimanova, V. The Role of Sustainability Performance after Merger and Acquisition Deals in Short and Long-Term. J. Clean. Prod. 2021, 314, 127982. [Google Scholar] [CrossRef]

- Huang, C.-J.; Ke, W.-C.; Chiang, R.P.-Y.; Jhong, Y.-C. Which of Environmental, Social, and Governance Pillars Can Improve Merger and Acquisition Performance? J. Clean. Prod. 2023, 398, 136475. [Google Scholar] [CrossRef]

- Aerts, W.; Cormier, D.; Magnan, M. Corporate Environmental Disclosure, Financial Markets and the Media: An International Perspective. Ecol. Econ. 2008, 64, 643–659. [Google Scholar] [CrossRef]

- Cormier, D.; Magnan, M. The Impact of Social Responsibility Disclosure and Governance on Financial Analysts’ Information Environment. Corp. Gov. 2014, 14, 467–484. [Google Scholar] [CrossRef]

- Hitt, M.A.; King, D.; Krishnan, H.; Makri, M.; Schijven, M.; Shimizu, K.; Zhu, H. Creating Value Through Mergers and Acquisitions. In The Handbook of Mergers and Acquisitions; Faulkner, D., Teerikangas, S., Joseph, R.J., Eds.; Oxford University Press: Oxford, UK, 2012; pp. 71–113. [Google Scholar]

- Deng, X.; Kang, J.-K.; Low, B.S. Corporate Social Responsibility and Stakeholder Value Maximization: Evidence from Mergers. J. Financ. Econ. 2013, 110, 87–109. [Google Scholar] [CrossRef]

- Jensen, M.C.; Meckling, W.H. Theory of the Firm: Managerial Behavior, Agency Costs and Ownership Structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Harford, J. What Drives Merger Waves? J. Financ. Econ. 2005, 77, 529–560. [Google Scholar] [CrossRef]

- Garfinkel, J.A.; Hankins, K.W. The Role of Risk Management in Mergers and Merger Waves. J. Financ. Econ. 2011, 101, 515–532. [Google Scholar] [CrossRef]

- Homberg, F.; Rost, K.; Osterloh, M. Do Synergies Exist in Related Acquisitions? A Meta-Analysis of Acquisition Studies. Rev. Manag. Sci. 2009, 3, 75–116. [Google Scholar] [CrossRef]

- Bauer, F.; Friesl, M. Synergy Evaluation in Mergers and Acquisitions: An Attention-Based View. J. Manag. Stud. 2022, 61, 37–68. [Google Scholar] [CrossRef]

- Qiao, M.; Xu, S.; Wu, G. Corporate Social Responsibility and the Long-Term Performance of Mergers and Acquisitions: Do Regions and Related-Party Transactions Matter? Sustainability 2018, 10, 2276. [Google Scholar] [CrossRef]

- Friedman, M. The Social Responsibility of Business Is to Increase Its Profits. New York Time Magazine, 13 September 1970; pp. 32–33. [Google Scholar]

- Cho, K.; Han, S.H.; Kim, H.J.; Kim, S. The Valuation Effects of Corporate Social Responsibility on Mergers and Acquisitions: Evidence from U.S. Target Firms. Corp. Soc. Responsib. Environ. Manag. 2021, 28, 378–388. [Google Scholar] [CrossRef]

- Doukas, J.A.; Zhang, R. Managerial Ability, Corporate Social Culture, and M&As. J. Corp. Financ. 2021, 68, 101942. [Google Scholar] [CrossRef]

- Alexandridis, G.; Hoepner, A.G.F.; Huang, Z.; Oikonomou, I. Corporate Social Responsibility Culture and International M&As. Br. Account. Rev. 2022, 54, 101035. [Google Scholar] [CrossRef]

- Krishnamurti, C.; Shams, S.; Chowdhury, H. Evidence on the Trade-off between Corporate Social Responsibility and Mergers and Acquisitions Investment. Aust. J. Manag. 2021, 46, 466–498. [Google Scholar] [CrossRef]

- Gomes, M.; Marsat, S. Does CSR Impact Premiums in M&A Transactions? Financ. Res. Lett. 2018, 26, 71–80. [Google Scholar] [CrossRef]

- Ozdemir, O.; Binesh, F.; Erkmen, E. The Effect of Target’s CSR Performance on M&A Deal Premiums: A Case for Service Firms. Rev. Manag. Sci. 2022, 16, 1001–1034. [Google Scholar] [CrossRef]

- Jost, S.; Erben, S.; Ottenstein, P.; Zülch, H. Does Corporate Social Responsibility Impact Mergers & Acquisition Premia? New International Evidence. Financ. Res. Lett. 2022, 46, 102237. [Google Scholar] [CrossRef]

- Hussaini, M.; Rigoni, U.; Perego, P. The Strategic Choice of Payment Method in Takeovers: The Role of Environmental, Social and Governance Performance. Bus. Strateg. Environ. 2023, 32, 200–219. [Google Scholar] [CrossRef]

- Li, K.; He, C.; Dbouk, W.; Zhao, K. The Value of CSR in Acquisitions: Evidence from China. Sustainability 2021, 13, 3721. [Google Scholar] [CrossRef]

- Fink, A. Conducting Research Literature Reviews: From the Internet to Paper; SAGE: Thousand Oaks, CA, USA, 2014. [Google Scholar]

- Tranfield, D.; Denyer, D.; Smart, P. Towards a Methodology for Developing Evidence-Informed Management Knowledge by Means of Systematic Review. Br. J. Manag. 2003, 14, 207–222. [Google Scholar] [CrossRef]

- Daugaard, D.; Ding, A. Global Drivers for ESG Performance: The Body of Knowledge. Sustainability 2022, 14, 2322. [Google Scholar] [CrossRef]

- Pranckutė, R. Web of Science (WoS) and Scopus: The Titans of Bibliographic Information in Today’s Academic World. Publications 2021, 9, 12. [Google Scholar] [CrossRef]

- Hinze, A.-K.; Sump, F. Corporate Social Responsibility and Financial Analysts: A Review of the Literature. Sustain. Account. Manag. Policy J. 2019, 10, 183–207. [Google Scholar] [CrossRef]

- Krüger, P. Corporate Goodness and Shareholder Wealth. J. Financ. Econ. 2015, 115, 304–329. [Google Scholar] [CrossRef]

- Gul, F.A.; Krishnamurti, C.; Shams, S.; Chowdhury, H. Corporate Social Responsibility, Overconfident CEOs and Empire Building: Agency and Stakeholder Theoretic Perspectives. J. Bus. Res. 2020, 111, 52–68. [Google Scholar] [CrossRef]

- Bose, S.; Minnick, K.; Shams, S. Does Carbon Risk Matter for Corporate Acquisition Decisions? J. Corp. Financ. 2021, 70, 102058. [Google Scholar] [CrossRef]

- Guo, J.; Cheng, H. Acquirers’ Carbon Risk, Environmental Regulation, and Cross-Border Mergers and Acquisitions: Evidence from China. Environ. Dev. Sustain. 2023. [Google Scholar] [CrossRef]

- Leon-Gonzalez, R.; Tole, L. The Determinants of Mergers & Acquisitions in a Resource-Based Industry: What Role for Environmental Sustainability? Rev. Econ. Anal. 2016, 7, 111–134. [Google Scholar] [CrossRef]

- Ma, X.; Xu, X.; Jiang, M. Does a Firm Have to Be Socially Responsible to Become a Target in Cross-Border M&As: Evidence from China. Asia-Pacific J. Account. Econ. 2022, 29, 1417–1438. [Google Scholar] [CrossRef]

- Fisman, R.; Heal, G.; Nair, V.B. A Model of Corporate Philantyropy; Columbia University: New York, NY, USA, 2006. [Google Scholar]

- Dhaliwal, D.S.; Li, O.Z.; Tsang, A.; Yang, Y.G. Voluntary Nonfinancial Disclosure and the Cost of Equity Capital: The Initiation of Corporate Social Responsibility Reporting. Account. Rev. 2011, 86, 59–100. [Google Scholar] [CrossRef]

- van Duuren, E.; Plantinga, A.; Scholtens, B. ESG Integration and the Investment Management Process: Fundamental Investing Reinvented. J. Bus. Ethics 2016, 138, 525–533. [Google Scholar] [CrossRef]

- Cho, S.Y.; Lee, C.; Pfeiffer, R.J. Corporate Social Responsibility Performance and Information Asymmetry. J. Account. Public Policy 2013, 32, 71–83. [Google Scholar] [CrossRef]

- Dicu, R.M.; Robu, I.-B.; Aevoae, G.-M.; Mardiros, D.-N. Rethinking the Role of M&As in Promoting Sustainable Development: Empirical Evidence Regarding the Relation Between the Audit Opinion and the Sustainable Performance of the Romanian Target Companies. Sustainability 2020, 12, 8622. [Google Scholar] [CrossRef]

- Fairhurst, D.; Greene, D.T. Too Much of a Good Thing? Corporate Social Responsibility and the Takeover Market. J. Corp. Financ. 2022, 73, 102172. [Google Scholar] [CrossRef]

- Krishnamurti, C.; Shams, S.; Pensiero, D.; Velayutham, E. Socially Responsible Firms and Mergers and Acquisitions Performance: Australian Evidence. Pacific Basin Financ. J. 2019, 57, 101193. [Google Scholar] [CrossRef]

- Hussaini, M.; Hussain, N.; Nguyen, D.K.; Rigoni, U. Is Corporate Social Responsibility an Agency Problem? An Empirical Note from Takeovers. Financ. Res. Lett. 2021, 43, 102007. [Google Scholar] [CrossRef]

- Hubbard, T.D.; Christensen, D.M.; Graffin, S.D. Higher Highs and Lower Lows: The Role of Corporate Social Responsibility in CEO Dismissal. Strateg. Manag. J. 2017, 38, 2255–2265. [Google Scholar] [CrossRef]

- Yen, T.Y.; André, P. Market Reaction to the Effect of Corporate Social Responsibility on Mergers and Acquisitions: Evidence on Emerging Markets. Q. Rev. Econ. Financ. 2019, 71, 114–131. [Google Scholar] [CrossRef]

- Spence, M. Market Signaling: Informational Transfer in Hiring and Related Screening Processes: Informational Structure of Hiring and Related Processes; Harvard University Press: Cambridge, MA, USA, 1974; ISBN 978-0674549906. [Google Scholar]

- Godfrey, P.C.; Merrill, C.B.; Hansen, J.M. The Relationship between Corporate Social Responsibility and Shareholder Value: An Empirical Test of the Risk Management Hypothesis. Strateg. Manag. J. 2009, 30, 425–445. [Google Scholar] [CrossRef]

- Qiao, L.; Wu, J. Pay for Being Responsible: The Effect of Target Firm’s Corporate Social Responsibility on Cross-Border Acquisition Premiums. Sustainability 2019, 11, 1291. [Google Scholar] [CrossRef]

- Casado-Díaz, A.B.; Nicolau-Gonzálbez, J.L.; Ruiz-Moreno, F.; Sellers-Rubio, R. The Differentiated Effects of CSR Actions in the Service Industry. J. Serv. Mark. 2014, 28, 558–565. [Google Scholar] [CrossRef]

- Ahmad, M.F.; Aziz, S.; Michiels, Y.; Nguyen, D.K. Tracing Environmental Sustainability Footprints in Cross-border M&A Activity. Eur. Financ. Manag. 2023. [Google Scholar] [CrossRef]

- Kanungo, R.P. Payment Choice of M&As: Financial Crisis and Social Innovation. Ind. Mark. Manag. 2021, 97, 97–114. [Google Scholar] [CrossRef]

- Hussain, T.; Shams, S. Pre-Deal Differences in Corporate Social Responsibility and Acquisition Performance. Int. Rev. Financ. Anal. 2022, 81, 102083. [Google Scholar] [CrossRef]

- Hawn, O. How Media Coverage of Corporate Social Responsibility and Irresponsibility Influences Cross-border Acquisitions. Strateg. Manag. J. 2021, 42, 58–83. [Google Scholar] [CrossRef]

- Arouri, M.; Gomes, M.; Pukthuanthong, K. Corporate Social Responsibility and M&A Uncertainty. J. Corp. Financ. 2019, 56, 176–198. [Google Scholar] [CrossRef]

- Zhang, T.; Zhang, Z.; Yang, J. When Does Corporate Social Responsibility Backfire in Acquisitions? Signal Incongruence and Acquirer Returns. J. Bus. Ethics 2022, 175, 45–58. [Google Scholar] [CrossRef]

- Shi, J.; Yu, C.; Li, Y. Beyond Linear: The Relationship between Corporate Social Responsibility and Market Reactions to Cross-Border Mergers and Acquisitions. Emerg. Mark. Financ. Trade 2022, 58, 638–654. [Google Scholar] [CrossRef]

- Li, M.; Lan, F.; Zhang, F. Why Chinese Financial Market Investors Do Not Care about Corporate Social Responsibility: Evidence from Mergers and Acquisitions. Sustainability 2019, 11, 3144. [Google Scholar] [CrossRef]

- Zhang, F.; Li, M.; Zhang, M. Chinese Financial Market Investors Attitudes toward Corporate Social Responsibility: Evidence from Mergers and Acquisitions. Sustainability 2019, 11, 2615. [Google Scholar] [CrossRef]

- Tampakoudis, I.; Noulas, A.; Kiosses, N.; Drogalas, G. The Effect of ESG on Value Creation from Mergers and Acquisitions. What Changed during the COVID-19 Pandemic? Corp. Gov. Int. J. Bus. Soc. 2021, 21, 1117–1141. [Google Scholar] [CrossRef]

- Tong, L.; Wang, H.; Xia, J. Stakeholder Preservation or Appropriation? The Influence of Target CSR on Market Reactions to Acquisition Announcements. Acad. Manag. J. 2020, 63, 1535–1560. [Google Scholar] [CrossRef]

- Teti, E.; Dell’Acqua, A.; Bonsi, P. Detangling the Role of Environmental, Social, and Governance Factors on M&A Performance. Corp. Soc. Responsib. Environ. Manag. 2022, 29, 1768–1781. [Google Scholar] [CrossRef]

- Chen, C.; Lu, W.; Liu, M. Corporate Social Responsibility Learning in Mergers and Acquisitions. Asia-Pacific J. Account. Econ. 2022, 29, 53–76. [Google Scholar] [CrossRef]

- Wang, Z.; Lu, W.; Liu, M. Corporate Social Responsibility Overinvestment in Mergers and Acquisitions. Int. Rev. Financ. Anal. 2021, 78, 101944. [Google Scholar] [CrossRef]

- Bettinazzi, E.L.M.; Zollo, M. Stakeholder Orientation and Acquisition Performance. Strateg. Manag. J. 2017, 38, 2465–2485. [Google Scholar] [CrossRef]

- Zheng, Z.; Li, J.; Ren, X.; Guo, J.M. Does Corporate ESG Create Value? New Evidence from M&As in China. Pacific-Basin Financ. J. 2023, 77, 101916. [Google Scholar] [CrossRef]

- Kim, B.-J.; Jung, J.-Y.; Cho, S.-W. Can ESG Mitigate the Diversification Discount in Cross-Border M&A? Borsa Istanbul Rev. 2022, 22, 607–615. [Google Scholar] [CrossRef]

- Liu, K.; Wu, S.; Guo, N.; Fang, Q. Host Country’s Carbon Emission and Cross-Border M&A Performance: Evidence from Listed Enterprises in China. J. Clean. Prod. 2021, 314, 127977. [Google Scholar] [CrossRef]

- Choi, G.; Kim, T.N. Effect of Acquisitions on Target Firms’ Stakeholder Welfare: Evidence from Corporate Social Responsibility. Bus. Soc. Rev. 2022, 127, 493–529. [Google Scholar] [CrossRef]

- Feng, X. The Role of ESG in Acquirers’ Performance Change after M&A Deals. Green Financ. 2021, 3, 287–318. [Google Scholar] [CrossRef]

- Yang, N.; Zhang, Y.; Yu, L.; Wang, J.; Liu, X. Cross-Border Mergers and Acquisitions, Regional Cultural Diversity and Acquirers’ Corporate Social Responsibility: Evidence from China Listed Companies. Int. Rev. Econ. Financ. 2022, 79, 565–578. [Google Scholar] [CrossRef]

- Chen, X.; Liang, X.; Wu, H. Cross-Border Mergers and Acquisitions and CSR Performance: Evidence from China. J. Bus. Ethics 2023, 183, 255–288. [Google Scholar] [CrossRef]

- Li, Z.; Wang, P. Cross-Border Mergers and Acquisitions and Corporate Social Responsibility: Evidence from Chinese Listed Firms. J. Bus. Financ. Account. 2023, 50, 335–376. [Google Scholar] [CrossRef]

- Zhao, X.; Jia, M. Sincerity or Hypocrisy: Can Green M&A Achieve Corporate Environmental Governance? Environ. Sci. Pollut. Res. 2022, 29, 27339–27351. [Google Scholar] [CrossRef]

- Martynova, M.; Renneboog, L. A Century of Corporate Takeovers: What Have We Learned and Where Do We Stand? J. Bank. Financ. 2008, 32, 2148–2177. [Google Scholar] [CrossRef]

- Aktas, N.; De Bodt, E.; Roll, R. Market Response to European Regulation of Business Combinations. J. Financ. Quant. Anal. 2004, 39, 731–757. [Google Scholar] [CrossRef]

- Li, J.; Wu, X. The Effect of CSR on Acquirer Returns of Cross-Border M&As in an Emerging Market—A Bane or a Boom? Appl. Econ. Lett. 2022, 30, 2607–2612. [Google Scholar] [CrossRef]

- Marks-Anglin, A.; Chen, Y. A Historical Review of Publication Bias. Res. Synth. Methods 2020, 11, 725–742. [Google Scholar] [CrossRef]

- Dumrose, M.; Rink, S.; Eckert, J. Disaggregating Confusion? The EU Taxonomy and Its Relation to ESG Rating. Financ. Res. Lett. 2022, 48, 102928. [Google Scholar] [CrossRef]

- Christensen, D.M.; Serafeim, G.; Sikochi, A. Why Is Corporate Virtue in the Eye of The Beholder? The Case of ESG Ratings. Account. Rev. 2022, 97, 147–175. [Google Scholar] [CrossRef]

- Ovtchinnikov, A.V. Capital Structure Decisions: Evidence from Deregulated Industries. J. Financ. Econ. 2010, 95, 249–274. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| # | Journal | # of Studies |

|---|---|---|

| 1 | Sustainability | 6 |

| 2 | Finance Research Letters | 4 |

| 3 | Journal of Corporate Finance | 4 |

| 4 | Journal of Cleaner Production | 3 |

| 5 | Asia-Pacific Journal of Accounting and Economics | 2 |

| 6 | Business Strategy and the Environment | 2 |

| 7 | Corporate Social Responsibility and Environmental Management | 2 |

| 8 | International Review of Financial Analysis | 2 |

| 9 | Journal of Business Ethics | 2 |

| 10 | Pacific-Basin Finance Journal | 2 |

| Subtotal Top10 | 29 | |

| Other Journals | 23 | |

| Total | 52 |

| M&A Stage | Sustainability Focus | Sustainability Rating | Performance Measure | Result | Conclusion | Sample | Years | Authors |

|---|---|---|---|---|---|---|---|---|

| Pre-deal | ||||||||

| Target Selection | Acquirer sustainability— M&A activity | KLD | Six measures of empire building tendency: (1) number of acquisitions; (2) dummy variable for acquisitions; (3) acquisition ratio; (4) asset growth; (5) capital expenditure growth; (6) property, plant, and equipment growth | Lower propensity to engage | Negative trend | US | 1996–2015 | Gul, FA; Krishnamurti, C; Shams, S; Chowdhury, H [75] |

| KLD | Two measures of M&A investment: (1) number of M&A and (2) M&A ratio | Negative relationship | US | 1999–2016 | Krishnamurti, C; Shams, S; Chowdhury, H [63] | |||

| Bid Premium | Target sustainability | ASSET4 | Premium: the acquisition price per share offered to target shareholders less the target’s stock price 42 days prior to the acquisition announcement, deflated by the target’s stock price 42 days prior to the acquisition | Positive link | Positive trend | International | 2003–2014 | Gomes, M; Marsat, S [64] |

| KLD | The percentage difference between the foreign acquiring firm’s offer price and the target firm’s pre-acquisition market value four weeks prior | Higher premium | International | 1991–2016 | Qiao, L; Wu, JF [92] | |||

| KLD | Deal premium: operationalization of Gomes and Marsat (2018) [64] | Positive link to premium | US, Service Industry | 1996–2018 | Ozdemir, O; Binesh, F; Erkmen, E [65] | |||

| Payment Method | Target sustainability | KLD | Binary variable: value of 1 if the payment method is in cash only form and 0 if the payment method is in the form of stock or combination | Positive association | Positive trend | US | 1992–2014 | Hussaini, M; Rigoni, U; Perego, P [67] |

| CSMAR | Binary variable: equals 1 for cash payment and 0 for share payment | Preference cash payment | China | 2007–2018 | Li, K; He, CH; Dbouk, W; Zhao, K [68] | |||

| Announcement return | Relative sustainability— target spread | ASSET4 | Acquirer’s cumulative abnormal return (CAR) and its standardization (SCAR) for period windows (−5; +5), (−2; +2), and (−1; +1) | Higher value | Positive trend | 20 countries | n.a. | Teti, E; Dell’Acqua, A; Bonsi, P [105] |

| KLD | 5-day cumulative abnormal return for the target (TCAR) and acquirer cumulative abnormal return (ACAR) over event window | Higher gains | US | 1995–2014 | Chen, C; Lu, WJ; Liu, M [106] | |||

| Post-deal | ||||||||

| Long-term financial performance | Acquirer sustainability | KLD | High CSR acquirers’ hedge portfolio abnormal returns for holding periods of one, two and three years | Higher returns | Positive trend/non- negative trend | US | 1992–2007 | Deng, X; Kang, JK; Low, BS [52] |

| ASSET4 | Cumulative Abnormal Returns (CAR) over the 36 months following the acquisition | Positive association | US | 2002–2010 | Bettinazzi, ELM; Zollo, M [108] | |||

| Rankins CSR Ratings | Difference in earnings per share (DiffEPS) between the period from one year before to one year after the M&A deals | Positive effect | China | 2012–2014 | Qiao, MZ; Xu, SW; Wu, GD [58] | |||

| Sino- Securities Index | Buy-and-hold abnormal return (BHAR) and post-M&A accounting performance: RoA, RoE (one year post-M&A) | Positive correlation | China | 2011–2019 | Zheng, ZG; Li, JR; Ren, XZ; Guo, JM [109] | |||

| Refinitiv | Accounting-based performance measure: RoA Market-based performance measure: Tobin’s Q | Improved performance | America | 2003–2020 | Huang, CJ; Ke, WC; Chiang, RPY; Jhong, YC [48] | |||

| ASSET4 | Accounting ratio up to three years after the announcement of the deal | Significantly correlated | Target of hospitality sector | 2000–2019 | Caiazza, S; Galloppo, G; Paimanova, V [47] | |||

| KCGS ratings | Two-year average of the acquiring firm’s year-end net income divided by its total assets after the completion of M&A (ROA) | Positive effect | Korean Stock Price Index | 2012–2018 | Kim, BJ; Jung, JY; Cho, SW [110] | |||

| KLD | Long-run stock returns, both equally weighted and value-weighted returns, for monthly buy-and-hold returns earned by the acquirer for the 36-month period following the acquisition month | Create value | US | 1999–2016 | Krishnamurti, C; Shams, S; Chowdhury, H [63] | |||

| Hexun Finance | Return on asset difference (ROA): 1, 2, 3, 4, and 5 years after M&A | Not Improved | China | 2010–2017 | Li, MH; Lan, FQ; Zhang, F [101] | |||

| ASSET4 | Pre-tax operating cash flow | Not Improved | 23 emerging markets | 2008–2014 | Yen, T; André, P [89] | |||

| Long-term financial performance | Relative sustainability— target spread | ASSET4 | Tobin’s Q as a proxy to measure the acquirer’s market value; change in Tobin’s Q as the ratio of the difference between the acquirer’s Tobin’s Q in the years after and before the merger announcement | Positive relationship | Positive trend | EU | 2003–2017 | Tampakoudis, I; Anagnostopoulou, E [9] |

| KLD | Acquirer buy-and-hold abnormal returns (BHAR) around the deal announcement date: estimated 24 months following the deal announcement date | Higher stock returns | US | 1995–2013 | Choi, G; Kim, TN [112] | |||

| KLD | Changes in Tobin’s Q ratio for the two groups in the 3 years before and after the M&A announcement | Higher acquirer gains | US | 1995–2014 | Chen, C; Lu, WJ; Liu, M [106] | |||

| Long-term financial performance | Relative sustainability— culture proximity | KLD | Acquirer’s long-term performance is measured by one-year buy-and-hold abnormal returns (BHAR) | Significant positive returns | Positive trend | US | 1992–2017 | Doukas, JA; Zhang, RY [61] |

| ASSET4 | Impact of the target’s ESG score on the acquirer’s ROA change | Relieved decline | International deals | 2000–2020 | Feng, X [113] | |||

| EIRIS | Change in return on asset (Δ ROA) one, two, and three years post-deal operating performance regressions | Higher long-run returns | 22 developed markets | 2004–2012 | Alexandridis, G; Hoepner, AGF; Huang, ZY; Oikonomou, I [62] | |||

| Sustainability performance | Acquirer sustainability— cross-border activity | Rankins CSR Ratings (RKS) | Overall measure of CSR performance provided by the RKS rating agency, as in prior empirical studies | Subsequent Improvement | Positive trend | China | 2009–2017 | Li, Z; Wang, P [116] |

| Rankins CSR Ratings (RKS) | Overall measure of CSR performance provided by the RKS rating agency | Significant increase | China | 2008–2015 | Chen, XM; Liang, X; Wu, H [115] | |||

| Chinese Corporate Social Responsibilities data | Three levels of CSR scores based on existing research and the CCSR database | Positive and significant impact | China | 2007–2018 | Yang, N; Zhang, Y; Yu, L; Wang, J; Liu, XM [114] | |||

| Sustainability performance | Relative sustainability—target spread | IVA | Change in acquirer rating subsequent to the announcement of the M&A deal | Positively associated | Positive trend | International | 1997–2007 | Aktas, N; de Bodt, E; Cousin, J [30] |

| ASSET4 | Relative ESG performance of targets and the ratio of the change in acquirers’ ESG performance | Increase following acquisition | EU | 2003–2017 | Tampakoudis, I; Anagnostopoulou, E [9] | |||

| KLD | Change in acquirer’s adjusted CSR scores in the year after M&As compared to those before | Higher acquirer gains | US | 1995–2014 | Chen, C; Lu, WJ; Liu, M [106] |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Kayser, C.; Zülch, H. Understanding the Relevance of Sustainability in Mergers and Acquisitions—A Systematic Literature Review on Sustainability and Its Implications throughout Deal Stages. Sustainability 2024, 16, 613. https://doi.org/10.3390/su16020613

Kayser C, Zülch H. Understanding the Relevance of Sustainability in Mergers and Acquisitions—A Systematic Literature Review on Sustainability and Its Implications throughout Deal Stages. Sustainability. 2024; 16(2):613. https://doi.org/10.3390/su16020613

Chicago/Turabian StyleKayser, Christoph, and Henning Zülch. 2024. "Understanding the Relevance of Sustainability in Mergers and Acquisitions—A Systematic Literature Review on Sustainability and Its Implications throughout Deal Stages" Sustainability 16, no. 2: 613. https://doi.org/10.3390/su16020613