1. Introduction

As global technological change and industrial competition continue to intensify, innovation is a must for China’s high-quality economic development. SOEs are integral components of the socialist economy with Chinese characteristics, so improving a high level of innovation is crucial for SOEs to fulfill their mission of promoting high-quality economic and social development in China [

1]. In fact, the State Council has issued a notice to encourage foreign shareholders to participate in the mixed-ownership reform of SOEs and support SOEs in introducing advanced technology and experience in 2017. During the Three-Year Action Plan for the Reform of State-Owned Enterprises (2020–2022) of the Chinese government, SOEs are required to play a leading role in innovation and contribute more to research and development. It is obvious that how to promote the optimization of the governance structure of SOEs and enhance the level of innovation through mixed-ownership reform should be a key problem to be solved.

In the context of mixed-ownership reform, the academic research on the relationship between mixed-ownership reform and SOE innovation is mainly carried out from the view of efficiency, grounded in principal-agent theory, and the complementary view from the perspective of resource-dependence theory [

2,

3]. However, previous studies have two limitations: (1) Although domestic and foreign scholars believe that mixed-ownership reform is an important way to promote the process of the internationalization of enterprises [

4], there are few studies on the impact of foreign ownership on SOE innovation through the process of internationalization as an important way of mixed-ownership reform encouraged by the Chinese government [

5]. This study believes that the influence of foreign ownership on innovation, through an internationalization process, is in line with empirical intuition and practical observations. This research gap needs to be filled urgently, as it will help SOEs to achieve high-quality development through mixed-ownership reform and the OFDI reverse technology spillover. (2) Innovation should be an important explanatory variable in the reform of SOEs and OFDI reverse technology spillover. Previous studies did not take innovation into account in the relationship between mixed-ownership reform and OFDI reverse technology spillover [

6]. The introduction and results of these research objectives will help countries in their transformation and development, laying the foundation for enhancing micro-independent innovation capabilities through SOE reform and reverse technology spillover. Thus, from the angle of OFDI reverse technology spillover, the study of the relationship among foreign ownership, the internationalization process and SOE innovation need to be explored [

7]. On the other hand, OFDI in developed or developing countries has been proven to generate positive reverse technology spillover effects through R&D, complementary resource acquisition or revenue feedback mechanisms [

8]. Therefore, under the Chinese government’s policy of building a market-oriented technology innovation system in 2020, it is urgent to study how to exert the comparative advantages of foreign shareholders to improve SOE reverse technology spillovers in OFDI. This involves leveraging foreign shareholders’ international experience, information advantages and capabilities to promote the optimization of SOEs’ governance structures and high-quality innovative development.

Thus, this paper integrates the relationships between foreign ownership, the internationalization process and SOE innovation into a theoretical framework, and it innovatively divides foreign ownership into two dimensions: the ownership dispersion degree after the entry of foreign shareholders and the foreign ownership participation level. This paper attempts to construct an integrated conceptual model that includes both home-country incentives and host-country facilitators. Firstly, this paper focuses on the direct impact of foreign ownership on the innovation of OFDI SOEs. Furthermore, by combining the two variables of government innovation subsidies and the host country’s innovation level, this paper studies the mechanism and pathway through which foreign ownership influences the innovation OFDI SOEs. On the one hand, the role of home-country incentives is to promote OFDI SOEs and seek technological advantages by strengthening government innovation subsidies. Based on SOE reform theory and government intervention theory, this paper focuses on examining the moderating role of government innovation subsidies between these theories. On the other hand, the role of host-country facilitators is to promote the reverse technology spillover and innovation transformation efficiency of OFDI SOEs by developing the host-country’s innovation resources. Based on the location advantage theory and technology gap theory, this paper focuses on the mediating role of the host country’s innovation level in the relationship between foreign ownership and the innovation of OFDI SOEs.

Therefore, from the angle of reverse technology spillover, this paper studies the effects of foreign ownership on the innovation of OFDI SOEs from the different angles of the ownership dispersion degree after the entry of foreign shareholders and the foreign ownership participation level. Based on the firm heterogeneity perspective of the neo-neo trade theory, compared with state-holding SOEs and other industries, this paper examines that whether the effect is different in non-state-holding enterprises and highly polluting industries. Further, does the innovation level in the host country mediate the relationship between the foreign ownership and SOE innovation? Do government innovation subsidies moderate the above relationship? To answer the above research questions, this paper aims to expand the research field on the relationship between mixed-ownership reform and OFDI SOE innovation and provide theoretical implications for SOEs to promote reverse technology spillovers through governance structure changes.

The following parts of the paper are arranged as follows:

Section 2 is the literature review and hypothesis development;

Section 3 presents the data and empirical model;

Section 4 presents the results;

Section 5 is a further mechanism test;

Section 6 is the conclusion;

Section 7 is the managerial implications; and the

Section 8 is the limitations and future research.

2. Literature Review and Hypothesis Development

2.1. Foreign Ownership and OFDI SOE Innovation

According to innovation theory, participation from foreign shareholders can help to resolve SOEs’ problems of owner and principal agent absence and to take advantage of their comparative advantages, complementary resources and international experience to enhance the business performance and innovation capability of SOEs [

9].

Firstly, whether OFDI in developed or developing countries has been proven to generate positive reverse technology spillover effects through R&D, complementary resource acquisition or revenue feedback mechanisms is examined in this paper [

10]. Therefore, with the increase in the degree of ownership dispersion after the entry of foreign shareholders, SOEs can avoid the lower decision-making quality caused by a high ownership concentration, make use of complementary resources to enhance innovation capabilities [

11] and take advantage of the synergistic role of foreign shareholders in terms of technology, capital and information to promote the two-way flow of innovation resources and technologies between domestic and foreign markets [

12]. Secondly, whether SOEs invest in the foreign shareholders’ homeland or others, the local advantages and extensive international social networks of foreign shareholders are conducive to enhancing their organizational legitimacy [

13], which in turn improves their efficiency in searching, absorbing and transforming innovation resources and technologies overseas. Finally, compared with the degree of ownership dispersion degree after the entry of foreign shareholders, with the increase in the foreign ownership participation level, SOEs will have more voice and influence by appointing board members and facilitating their implementation of the OFDI SOEs’ technology-seeking strategies. In turn, the international experience and information advantages of foreign shareholders can be fully utilized to improve the risk-taking capability and innovation efficiency of SOEs. Therefore, against the backdrop of a significant gap between the level of technology of the host country and that of developed countries, the willingness and motivation of SOEs to pursue OFDI technology-seeking strategies and to implement them will increase as the degree of ownership dispersion after the entry of foreign shareholders and the foreign ownership participation level increase, which will help the SOEs to enhance the reverse technology spillovers in a more open pattern. Thus, we have the following hypotheses:

H1a. The degree of ownership dispersion after the entry of foreign shareholders has a positive impact on the innovation of OFDI SOEs.

H1b. The foreign ownership participation level also has a positive impact on the innovation of OFDI SOEs.

2.2. Mediating Effects of Host Country’s Innovation Level

The technology gap theory suggests that the generation and application of advanced technologies and products first appear in developed countries. A particular technological potential gap is needed between countries for latecomer firms to have the opportunity to acquire advanced technology and knowledge [

14]. Thus, imitating countries can learn new products and technologies from the host country through outward direct investment, import and export. On the one hand, when the host country has a high level of innovation, the local technological progress will promote changes in the consumption habits of the host country’s residents and enhance the local market’s demand for innovative products from foreign enterprises in these areas. On the other hand, host countries with high innovation levels can increase the locational development advantages of foreign enterprises in terms of access to innovation resources and advanced technologies, which have a higher level of R&D factors, scientific and technological talent, innovation policies and infrastructure.

From the perspective of combining mixed-ownership reform and OFDI reverse technology spillovers, as the ownership dispersion degree after the entry of foreign shareholders and the foreign ownership participation level increase, SOEs will pay more attention to the voice and influence of the foreign shareholders and the synergies in terms of their international experience and information advantages. They will increase their propensity to invest in the high innovation level of host countries in order to absorb advanced technologies and innovation resources that they do not possess. Firstly, the consumers’ perceptions of products and their product-seeing behavior in such innovation locations are conducive to the creation of an innovative market environment by SOEs, which will inevitably contribute to local continuation or transformation and the upgrading of their technological development trajectory. Secondly, the higher level of accumulation of R&D resources and innovation in the host country can make it easier for SOEs to access scarce technology talent, and their reverse technology spillover is mainly dependent on the efficiency and research capacity of R&D personnel in the region [

15]. Finally, the efficiency of the technology-seeking strategies OFDI SOEs and their reverse technology spillovers are closely related to the host country’s infrastructural support for innovation-related activities. The accumulation of R&D elements, innovation policies and infrastructural conditions in host countries with high innovation levels creates a superior innovation resource for SOEs [

16], which helps them integrate innovation resources and optimize their allocation within the group, therefore contributing to the effectiveness of these reverse technology spillovers [

17]. Thus, we have the following hypothesis:

H2. The host country’s innovation level mediates the positive impact of foreign ownership on the innovation of SOEs.

2.3. Moderating Effects of Government Innovation Subsidies

According to the resource-dependency theory, the survival and development of enterprises require the support of a large amount of resources. Innovative activities by enterprises require additional management costs. From the perspective of resource allocation, government innovation subsidies can effectively alleviate the financial pressure on enterprises and thus promote better innovative activities [

18]. Among them, government innovation subsidies can influence the innovation of OFDI SOEs in two ways: direct innovation incentives and indirect signaling. On the one hand, from the perspective of direct innovation incentives, the investment of innovation subsidies can have an incentive effect on the management of SOEs, compensating for their lack of motivation due to the lack of realization of innovation activities in the short term [

19]. At the same time, sufficient subsidy funds can increase the R&D intensity of SOEs, which can integrate enough funds and resources from internal and external sources to further increase R&D investment and guide their future innovation development [

20]. On the other hand, from the perspective of indirect signaling, the fact that an enterprise receives innovation subsidies indicates to a certain extent that it has received recognition from the government, which undoubtedly releases the signal of government “approval” to the market [

21] and alleviates the information asymmetry between SOEs and external investors, thus facilitating SOEs’ access to external quality resources. This will, in turn, help SOEs to obtain external high-quality resources, expand their financing channels and promote innovation and development [

22].

Therefore, the moderating role of government innovation subsidies in exploring the impact of foreign ownership on the innovation of OFDI SOEs should not be overlooked. From the angle of reverse technology spillover, the participation of foreign shareholders with more mature innovation awareness will strengthen the initiative of SOEs to search, learn and absorb advanced technologies in the international market through OFDI. As the level of foreign participation and shareholding increases, SOEs will make use of the foreign shareholders’ international experience. In that case, government innovation subsidies can play a positive role as a policy incentive and resource supplement in this process. In addition, the signal of government innovation subsidies can also alleviate the information asymmetry between SOEs and external investors, which in turn can facilitate their access to expand their financing channels and further external high-quality resources. Thus, the positive effect of government innovation subsidies can significantly increase the efficiency of SOEs in coping with the risk of innovation and promoting reverse technology spillovers during OFDI. Thus, we have the following hypothesis:

H3. Government innovation subsidies play a positive moderating role between foreign ownership and the innovation of SOEs.

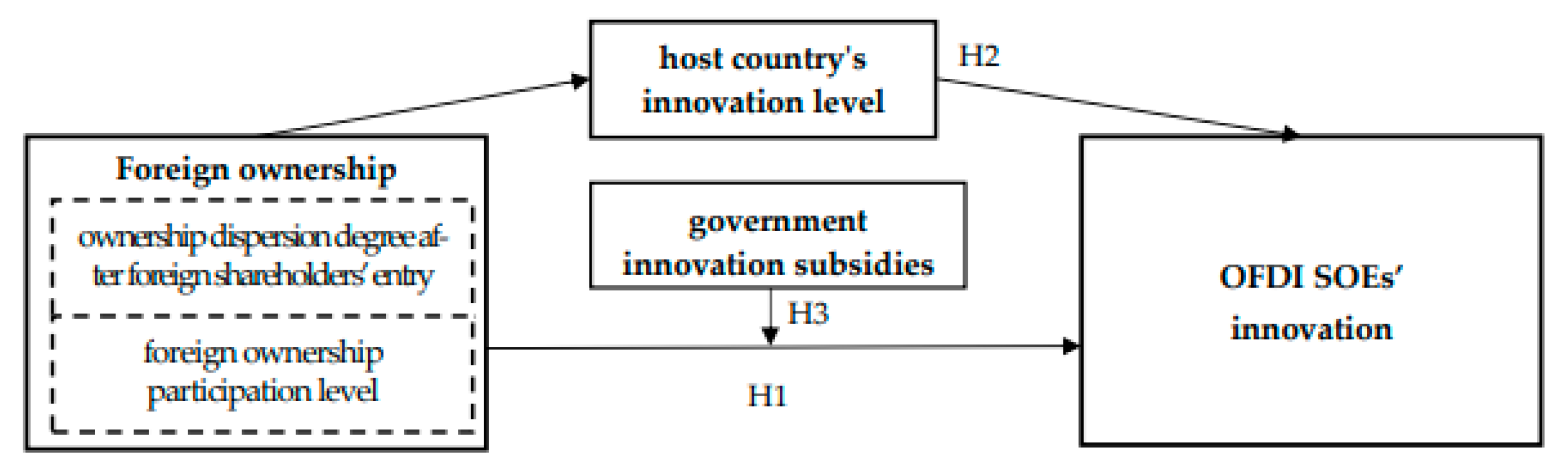

Shown in

Figure 1 is a model of the relationship between foreign ownership, the host country’s innovation level, government innovation subsidies and the innovation of SOEs based on the above analysis and hypothesis.

3. Data and Empirical Model

3.1. Sample and Data

To empirically assess the effect of foreign ownership, we collected financial data from the A-share listed hybrid OFDI state-owned industrial companies of Shanghai and Shenzhen in China and used the annual data of these listed companies in 2007–2019. The reason why we selected industrial enterprises is that innovation activities play a more critical role in this industry. Moreover, considering the time lag of the OFDI SOE innovation effect, innovation performance was measured by the number of newly added invention patents for three consecutive years after OFDI of these SOEs.

3.2. Definition of Main Variable

3.2.1. Dependent Variable: SOE Innovation

The natural logarithm of the number of new invention patent applications for three consecutive years (Lnpat) is used in this paper to measure the innovation of OFDI SOEs. On the one hand, patent examination is objectively consistent in terms of the novelty and utility of the inventions [

23,

24]. On the other hand, this measurement is in line with the current research practice on the reverse technology spillover effect of OFDI firms in China. It facilitates the identification and effective measurement of patent classification numbers (IPC) published by the State Intellectual Property Office (SIPO). And with the help of the list of patent classification numbers on the official website of the World Intellectual Property Organization (WIPO), it can also reflect a firm’s quality of innovation in terms of the number of invention patent applications.

3.2.2. Explanatory Variable: Foreign Ownership

This paper uses the ownership dispersion degree after the entry of foreign shareholders and the foreign ownership participation level to measure the effect of foreign ownership.

(1) In terms of the ownership dispersion degree after the entry of foreign shareholders, this paper adopts Herfindahl’s inverse index to measure the ownership dispersion degree after the entry of major foreign shareholders, i.e., , where Ki represents the proportion of the number of shareholdings of category i among the top ten shareholders, i.e., in addition to the major foreign shareholders, the other members are classified into state-owned legal person shareholders, collective shareholders, private shareholders and other shareholders according to the nature of the shareholders.

(2) In terms of the foreign ownership participation level, this paper measures the impact by using three indicators of increasing the degree of the foreign ownership participation level [

25].

① The first indicator is whether foreign shareholders have entered (WZ), and it is set as a dummy variable: it is 1 if there is foreign shareholder ownership in SOEs and 0 otherwise.

② The second indicator is whether foreign major shareholders have entered (WZ10), and it is a dummy variable: it is 1 if there are foreign shareholders with shareholdings more significant than 10% in the SOEs (taking into account the shareholdings acting in concert) and 0 otherwise. This is mainly based on the Company Law of the People’s Republic of China (amended in 2018), which stipulates that shareholders with more than this percentage of voting rights have the right of temporarily proposing a general meeting of stockholders, etc.

③ The third indicator is the participation level of foreign ownership (Rate_WZ), and this variable is measured by the ratio of the shareholding of major foreign shareholders to the total shareholding of the top ten shareholders.

3.2.3. Mediation Variable: Host Country’s Innovation Level

This paper measures the host country’s innovation level (HIL) by taking the proportion of high-tech product exports to the total exports in the World Bank database.

3.2.4. Moderation Variable: Government Innovation Subsidies

Government innovation subsidies (GIS) is used as a dummy variable in this paper. The median of the logarithm of the amount of innovation subsidies from government departments to enterprises is used as the standard [

26]: it is 1 if it is above the median, representing a high level of government innovation subsidies, and it is 0 otherwise, representing a low level of government innovation subsidies.

3.2.5. Control Variables

Following the existing literature [

27,

28,

29,

30], variables that may affect the innovation and internationalization of SOEs are controlled as below: ① Enterprise size (Lnsize). In general, the size of the enterprise directly affects its sensitivity to market changes and its efficiency of technological innovation. The logarithm of the total assets of OFDI SOEs is used to reflect Lnsize. ② Enterprise growth (Growth). It has been found that enterprise growth is positively correlated with innovation. This variable is measured by the OFDI SOEs’ growth rate of their main business income. ③ R&D intensity (RD). Generally speaking, the more R&D investment there is, the more innovation vitality will be found in the SOEs. This paper uses the ratio of R&D expenditure to the primary business income of OFDI SOEs. ④ Asset specificity (FSP). Investment in particularly high-innovation assets can promote the innovation vitality of enterprises. This variable is calculated by the ratio of fixed assets to total assets of OFDI SOEs. ⑤ International experience (FSTS). The improvement in SOEs’ international experience can promote the accumulation of innovative resources, such as human capital and material capital, and it has a positive effect on reverse technology spillover. This variable is measured by the ratio of overseas operating income to the total revenue of OFDI SOEs. ⑥ Board meeting intensity (BOD). The intensity of board meetings is positively correlated with R&D intensity, which will promote enterprise innovation. This variable is indicated by the number of board meetings of OFDI SOEs. ⑦ Host country’s economic stability (INF). A better level of economic development in the host country can provide a suitable environment for enterprise development and promote reverse technology spillover. The inflation rate of the host country is obtained from the World Bank’s World Development Index (WDI) database. ⑧ Host country political stability (PI). The stable market environment of the host country can reduce the risk of outbound investment. These indicators are derived from the World Bank’s Corporate Governance Database.

4. Results

4.1. Descriptive Statistics and Correlation Analysis

The mean, standard deviation (S.D.) and correlation are shown in

Table 1 and

Table 2. The correlation coefficients between the variables were all less than 0.6. Moreover, the VIF was found to be less than the critical value of 10 in all the subsequent regression models by the variance inflation factor test, which rules out the problem of multicollinearity.

4.2. Baseline Regression

Hypothesis H1 posited that foreign ownership has a positive impact on the innovation of OFDI SOEs. In

Table 3, model 1 shows that the ownership dispersion degree after the entry of foreign shareholders had a positive effect on the innovation of OFDI SOEs (β = 0.522,

p < 0.01); model 2 reflects that foreign ownership had a positive effect on the innovation of OFDI SOEs (β = 0.264,

p < 0.05); model 3 indicates that foreign majority shareholder ownership had a positive effect on the innovation of OFDI SOEs (β = 1.024,

p < 0.01); model 4 proves that the foreign ownership participation level had a positive effect on the innovation of OFDI SOEs (β = 2.356,

p < 0.01). It can be seen that, apart from the significant positive effect of the ownership dispersion degree after the entry of foreign shareholders, the positive impact of the participation level was the largest among the three types of indicators measuring the depth of foreign ownership participation. This suggests that the positive impact of foreign shareholder participation can only be seen once a certain degree of ownership dispersion has been achieved after the entry of foreign shareholders. Moreover, only when the shareholding ratio deepened to a certain level could the influence of foreign shareholders appear, leading to supervision and balance enhancing the OFDI SOEs’ reverse technology spillover, which was consistent with hypothesis H1.

Further, considering the significant differences and influence patterns of the above four explanatory variables, this paper selected the ownership dispersion degree after the entry of foreign shareholders and the foreign ownership participation level for the subsequent series of tests and analyses.

4.3. Endogeneity Analysis

To further mitigate endogeneity, we employed the instrumental variable (IV) approach. This method alleviates endogeneity by reducing reverse causality, unobserved heterogeneity and possible measurement errors. A corporate pyramid hierarchy (Layer) and fiscal surplus (Surplus) were adopted as the instruments. When the ultimate controller of the SOE directly controlled the listed company, Layer was one. When there was also an intermediate controller between them, Layer was two, and so on [

31]. Surplus denotes the fiscal surplus of the province where the enterprise is located in the current year. The reason for choosing both as the instrumental variables was that the willingness of local governments to delegate gradually increases as the control of direct government controllers weakens and the number of pyramid layers within the enterprise increases. Similarly, a higher government fiscal surplus represents less government intervention, such as tax pressure on SOEs, and SOEs have a higher willingness and incentive to cooperate with non-state shareholders. Such macro policy variables generally do not directly affect firm innovation, but they indirectly influence firms’ innovative behavior through the increased willingness of local governments to decentralize and further increase their desire to participate in mixed-ownership reform and cooperate with foreign shareholders. This satisfies the instrumental variable correlation and homogeneity conditions.

Table 4 shows the results. Model 1 and model 2 are the first-stage regression, where the dependent variables were HHI_WZ and Rate_WZ, respectively. The coefficients of Layer and Surplus were positive and highly significant. Model 3 and model 4 are the second-stage regression. HHI_HAT and Rate_HAT were formed from the instrumented first stage of HHI_WZ and Rate_WZ, respectively. The coefficients of HHI_HAT and Rate_HAT were positive and significant, confirming the results documented earlier. Furthermore, the Lagrange multiplier (LM) statistic and Wald F statistic reject the null hypothesis that the correlation between the instrumental variable and endogenous variable was weakly recognized, which verifies the validity of the instrumental variables.

4.4. Heterogeneity Test

The neo-neo trade theory suggests that firm heterogeneity in terms of productivity is the most critical driver of internationalization and performance [

32]. It reveals that a strong ownership structure and industry attributes should play a role in the contextual trade-off between firm internationalization and performance. Therefore, the following section of this paper examines and analyzes heterogeneity in terms of both the type of state capital control and whether it is a highly polluting industry.

The regression results of state capital participation are shown in column (1) and column (3) in

Table 5, and the regression results of state capital control are shown in column (2) and column (4). The coefficient of HHI_WZ was positive and significant at the 5% level, as shown in column (1), and the coefficient of Rate_WZ was positive and effective at the 1% level, as shown in Column (3). This suggests that non-state-holding enterprises are more conducive to foreign ownership to improving innovation than state-holding enterprises. Therefore, considering the phenomenon that state participation is superior to state control, reducing government intervention in many competitive fields can help to improve the discourse power and influence of foreign shareholders in SOEs so as to promote OFDI SOEs’ technology-seeking strategies and reverse technology spillover.

The regression results of high-polluting industries are shown in column (5) and column (7) in

Table 5, and the regression results of other sectors are shown in column (6) and column (8). The coefficient of HHI_WZ and Rate_WZ were positive and significant at the 1% level, as shown in column (5) and column (7). This suggests that when OFDI SOEs are in highly polluting industries, foreign ownership is more conducive to enhancing innovation. Compared with other sectors, the effect of greater environmental compliance in high-pollution industries is conducive to SOEs giving full play to the comparative advantages of foreign shareholders and promoting their OFDI to seek strategic and reverse technology spillover effects.

5. Further Mechanism Test

From the theoretical analysis conducted in this paper, foreign ownership promotes innovation in OFDI SOEs through the mediating effect of the host country’s innovation level. This study used a three-step method to examine the mechanisms. According to relevant research, this study designed the following mediating model.

Here, HIL is the mediating variable and denotes the host country’s level of innovation.

To test the moderating effect of government innovation subsidies, this study constructed a model (4) based on the research of Yang et al. [

33].

Here, GIS is the moderating variable and denotes government innovation subsidies.

5.1. The Host Country’s Innovation Level Mechanism Test

Based on the above models, the mediating mechanism of the host country’s innovation level was examined and is shown in

Table 6. The results of model 1 show that ownership dispersion degree after the entry of foreign shareholders was positively associated with the host country’s innovation level (β = 2.957,

p < 0.01). The results of model 2 present that the impact of the ownership dispersion degree after the entry of foreign shareholders on innovation in OFDI SOEs was still significant after adding the host country’s innovation level (β = 0.294,

p < 0.01), and the impact of the host country’s innovation level on innovation in OFDI SOEs was significant (β = 0.010,

p < 0.01). This suggests that the host country’s innovation level is a partial mediator between the ownership dispersion degree after the entry of foreign shareholders and innovation in OFDI SOEs. Model 3 and model 4 show that the host country’s innovation level exerted a partial mediating effect between the foreign ownership participation level and innovation in OFDI SOEs, which was consistent with hypothesis H2.

To further confirm hypothesis H2, bias-corrected bootstrapping was adopted to test the significance of the mediation effect. This method not only evaluated the Beta coefficient from the indirect impacts but also demonstrated the statistical significance of the coefficients with bootstrapped, bias-corrected confidence intervals (BC-CIs) using 1000 duplicate samples. The mediating effect occurred when the BC-CIs of the indirect parameters did not contain a zero, as shown in

Table 7. Moreover, compared with the indirect impact of the ownership dispersion degree after the entry of foreign shareholders, the mediating impact of the foreign ownership participation level was significantly enhanced. Thus, H2 is further supported.

5.2. The Government Innovation Subsidies Mechanism Test

Table 8 presents the test results of the government innovation subsidies mechanism. It shows that the interaction coefficients (HHI_WZ × GIS, Rate_WZ × GIS) of the ownership dispersion degree after the entry of foreign shareholders and the foreign ownership participation level and government innovation subsidies were significantly positive, respectively, (β = 0.659,

p < 0.01; β = 1.133,

p < 0.01). Moreover, compared with the moderating effects of government innovation subsidies on integration after the entry of foreign shareholders, the moderating effects of government innovation subsidies on the foreign ownership participation level were significantly enhanced. This suggests that the impact of foreign ownership on innovation in OFDI SOEs is more significant in cases with high government subsidy incentives than in situations with low government subsidy incentives, which is consistent with hypothesis H3.

5.3. Robustness Test

5.3.1. Alternative Model Test

Considering that innovation of OFDI SOEs is a censoring variable with a lower limit of 0, this paper used the Tobit model to verify the robustness of the results. In

Table 9, the results of model 1 show that the ownership dispersion degree after the entry of foreign shareholders was significantly and positively associated with the host country’s innovation level (β = 3.230,

p < 0.01). The results of model 2 show that the impact of the ownership dispersion degree after the entry of foreign shareholders on the innovation of OFDI SOEs was still significant after adding the host country’s innovation level (β = 0.261,

p < 0.05), and the impact of the host country’s innovation level on the innovation of OFDI SOEs was significant (β = 0.008,

p < 0.01). This suggests that the host country’s innovation level exerts a partial mediating effect between the ownership dispersion degree after the entry of foreign shareholders and the innovation of OFDI SOEs. The results of model 3 and model 4 suggest that the host country’s innovation level plays a partial mediating role between the foreign ownership participation level and the innovation of OFDI SOEs. Model 5 and model 6 proved that the impact of foreign ownership on the innovation of OFDI SOEs is more significant in cases with high government innovation subsidies than in situations with low government innovation subsidies. Thus, the test results of hypothesis H2 and hypothesis H3 are robust and reliable.

5.3.2. Alternative Variables Test

This paper replaced the mediating and moderating variables with the technology gap (GAP) and government subsidies (GS), respectively. Among them, the technology gap (GAP) was measured by taking the difference between China’s and the host country’s proportion of high-tech product exports in their total exports in the World Bank database. Government subsidies (GS) was used as a dummy variable. The median of the logarithm of the amount of subsidies from government departments to enterprises was used as the standard: it was 1 if it was above the median, representing high government subsidies, and it was 0 otherwise, representing low government subsidies.

As shown in

Table 10, the results of model 1 show that the ownership dispersion degree after the entry of foreign shareholders was significantly and positively associated with the technology gap (β = 2.997,

p < 0.01). The results of model 2 show that the impact of the ownership dispersion degree after the entry of foreign shareholders on the innovation of OFDI SOEs was still significant after adding the technology gap (β = 0.363,

p < 0.05), and the impact of the technology gap on the innovation of OFDI SOEs was significant (β = 0.012,

p < 0.05). This suggests that the technology gap exerts a partial mediating effect between the ownership dispersion degree after the entry of foreign shareholders and the innovation of OFDI SOEs. The results of model 3 and model 4 suggest that the technology gap plays a partial mediating role between the foreign ownership participation level and the innovation of OFDI SOEs. Model 5 and model 6 proved that the impact of foreign ownership on the innovation of OFDI SOEs is more significant in cases with high government subsidies than in situations with low government subsidies. Thus, the test results of hypothesis H2 and hypothesis H3 are robust and reliable.

6. Conclusions

Based on the present literature, this paper expands the research field by examining the impact of foreign ownership on the innovation of OFDI SOEs. From the perspectives of the ownership dispersion degree after the entry of foreign shareholders and the foreign ownership participation level, this paper took Chinese hybrid OFDI state-owned listed industrial companies as examples to study the impact of foreign ownership on the innovation of OFDI SOEs. Compared with the ownership dispersion degree after the entry of foreign shareholders, we found that the foreign ownership participation level plays a more active role in the innovation of OFDI SOEs, and the positive effect is more substantial for enterprises which are non-state-holding and in high-pollution industries. Further analysis revealed that the relationship between foreign ownership and the innovation of SOEs is mediated and moderated by the host country’s innovation level and government innovation subsidies, respectively. In addition, compared with the ownership dispersion degree after the entry of foreign shareholders, the mediating effect of the host country’s innovation level and the moderating effects of government innovation subsidies are significantly enhanced by the foreign ownership participation level. These findings can promote the study of the relationship between mixed-ownership reform and the innovation of Chinese SOEs and facilitate the policy design of promoting SOE reverse technology spillovers through reform of their governance structure.

7. Managerial Implications

As mixed-ownership reform can promote the technology-seeking behavior and innovative development of OFDI SOEs, in order to facilitate the innovation of SOEs, foreign shareholders’ comparative advantages should be well exploited. In the future, Chinese hybrid OFDI SOEs can continuously improve their governance structure, strategic behavior and incentive policies through the following three aspects.

(1) The synergy of the comparative advantages of foreign shareholders should be well exploited. In addition, compared to the complementary function of a higher ownership dispersion degree after the entry of foreign shareholders, SOEs should take good advantage of the higher foreign ownership participation level to create a more conducive internal and external innovation environment for the technology-seeking strategic decisions and reverse technology spillovers.

(2) The pivotal role of the investment location should be actively developed to take advantage of the situation. SOEs should make good use of the international experience, information advantages and expertise of foreign shareholders to choose the host country, which has more complementary innovation resources available to support the upgrading of the technological development trajectories of SOEs and to enhance the effect of their reverse technology spillovers.

(3) The incentive policies provided by government innovation subsidies should be well exploited. Foreign shareholders with mature innovation awareness and technology development experience can help SOEs to make the most of government innovation subsidies, which can help SOEs to search for overseas technology and innovation exploration. In this way, SOEs can further obtain external high-quality resources and finance channels and enhance the absorption and transformation of advanced technologies and knowledge.

8. Limitations and Future Research

There are still some limitations which need to be further studied. First, studies could consider further expansion to non-listed companies in China’s Industrial Database to enhance the sample size and the validity of the test. Secondly, there may be other important contextual factors influencing the relationship between foreign ownership and the innovation of OFDI SOEs. Therefore, the market entry mode and cultural distance could be added to the future research framework to conduct further analysis.

Author Contributions

Conceptualization, C.W.; methodology, M.Y.; software, M.Y.; validation, C.W., M.Y. and F.H.; formal analysis, M.Y.; investigation, M.Y.; resources, C.W.; data curation, M.Y.; writing—original draft preparation, M.Y.; writing—review and editing, C.W., M.Y., F.H. and S.W.; visualization, C.W. and F.H.; supervision, C.W. and F.H.; project administration, C.W. and F.H.; funding acquisition, C.W. All authors have read and agreed to the published version of the manuscript.

Funding

This research was funded by the Social Science Foundation of Jiangsu Province (23EYB003) and the Social Science Foundation of Jiangsu Province (22EYB025).

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

Data are contained within the article.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Zhang, X.Q.; Yu, M.Q.; Chen, G.Q. Does mixed-ownership reform improve SOEs’ innovation? Evidence from state ownership. China Econ. Rev. 2020, 61, 101450. [Google Scholar] [CrossRef]

- Ullah, F.; Jiang, P.; Elamer, A.A.; Owusu, A. Environmental performance and corporate innovation in China: The moderating impact of firm ownership. Technol. Forecast. Soc. Change 2022, 184, 121990. [Google Scholar] [CrossRef]

- Shi, X.; Cao, X.; Hou, Y.; Xu, W. Mixed ownership reform and environmental sustainable development—Based on the perspective of carbon performance. Sustainability 2023, 15, 9809. [Google Scholar] [CrossRef]

- Xie, F.S.; Yang, P.X. Research on the impact of mixed reform of state-owned enterprises on enterprise performance—Based on PSM-DID method. Sustainability 2023, 15, 3122. [Google Scholar] [CrossRef]

- Kong, D.; Zhu, L.; Yang, Z. Effects of foreign investors on energy firms’ innovation: Evidence from a natural experiment in China. Energy Econ. 2020, 92, 105011. [Google Scholar] [CrossRef]

- Wach, K. Exploring the role of ownership in international entrepreneurship: How does ownership affect internationalisation of polish firms? Entrep. Bus. Econ. Rev. 2017, 5, 205–224. [Google Scholar] [CrossRef]

- Zhou, Y.Y.; Lei, C.; Jiménez, A. Foreign shareholders’ social responsibility, R&D innovation, and international competitiveness of Chinese SOEs. Sustainability 2022, 14, 1746. [Google Scholar]

- Seyoum, M.; Wu, R.S.; Yang, L. Technology spillovers from Chinese outward direct investment: The case of Ethiopia. China Econ. Rev. 2015, 33, 35–49. [Google Scholar] [CrossRef]

- Bena, J.; Ferreira, M.A.; Matos, P.; Pires, P. Are foreign investors locusts? The long-term effects of foreign institutional ownership. J. Financ. Econ. 2017, 126, 122–146. [Google Scholar] [CrossRef]

- Ren, X.Y.; Yang, S.L. Empirical study on location choice of Chinese OFDI. China Econ. Rev. 2020, 61, 101428. [Google Scholar] [CrossRef]

- Luong, H.; Moshirian, F.; Nguyen, L.; Tian, X.; Zhang, B. How Do Foreign Institutional Investors Enhance Firm Innovation. J. Financ. Quant. Anal. 2017, 52, 1449–1490. [Google Scholar] [CrossRef]

- Sytse, D.; George, R.J.; Kabir, R. Foreign and Domestic Ownership, Business Groups, and Firm Performance: Evidence from a Large Emerging Market. Strateg. Manag. J. 2006, 27, 637–657. [Google Scholar]

- Wang, J.; Wang, X. Benefits of foreign ownership: Evidence from foreign direct investment in China. J. Int. Econ. 2015, 97, 325–338. [Google Scholar] [CrossRef]

- Kumar, S.; Russell, R.R. Technological change, technological catch-up, and capital deepening: Relative contributions to growth and convergence. Am. Econ. Rev. 2002, 92, 527–548. [Google Scholar] [CrossRef]

- Schmidt, S.; Balestrin, A.; Edelman, N.R. The influence of innovation environments in R&D results. Rev. Adm. 2016, 51, 397–408. [Google Scholar]

- Raymond, W.; Mairesse, J.; Mohnen, P. Dynamic models of R&D, innovation and productivity: Panel data evidence for dutch and French manufacturing. Eur. Econ. Rev. 2015, 78, 28–306. [Google Scholar]

- Wu, J.; Wang, C.; Hong, J. Internationalization and innovation performance of emerging market enterprises: The role of host-country institutional development. J. World Bus. 2016, 51, 251–263. [Google Scholar] [CrossRef]

- Wu, A.H. The signal effect of Government R&D Subsidies in China: Does ownership matter. Technol. Forecast. Soc. Change 2017, 117, 339–345. [Google Scholar]

- Luo, L.J.; Yang, Y.; Luo, Y.Z.; Liu, C. Export, subsidy and innovation: China’s state-owned enterprises versus privately-owned enterprises. Econ. Political Stud. 2016, 4, 137–155. [Google Scholar] [CrossRef]

- Lin, J.; Wu, H.M.; Wu, H.W. Could government lead the way? Evaluation of China’s patent subsidy policy on patent quality. China Econ. Rev. 2021, 69, 101663. [Google Scholar] [CrossRef]

- Kleer, R. Government R&D subsidies as a signal for private investors. Res. Policy 2010, 39, 1361–1374. [Google Scholar]

- Castells, P.A. Persistence in R&D Performance and its Implications for the Granting of Subsidies. Rev. Ind. Organ. 2013, 43, 193–220. [Google Scholar]

- Sytch, M.; Tatarynowicz, A. Exploring the locus of invention: The dynamics of network communities and firms’ invention productivity. Acad. Manag. J. 2014, 57, 249–279. [Google Scholar] [CrossRef]

- Boone, C.; Lokshin, B.; Guenter, H. Top management team nationality diversity, corporate entrepreneurship, and innovation in multinational firms. Strateg. Manag. J. 2019, 40, 277–302. [Google Scholar] [CrossRef]

- Chen, J.; Heng, C.S.; Tan, B.C.; Lin, Z. The distinct signaling effects of R&D subsidy and non-R&D subsidy on IPO performance of IT entrepreneurial firms in China. Res. Policy 2018, 47, 108–120. [Google Scholar]

- Chen, Z.A.; Du, J.M.; Li, D.H.; Ouyang, R. Does foreign institutional ownership increase return volatility? Evidence from China. J. Bank. Financ. 2013, 37, 660–669. [Google Scholar] [CrossRef]

- Ho, T.T.; Tran, X.H.; Nguyen, Q.K. Tax revenue-economic growth relationship and the role of trade openness in developing countries. Cogent Bus. Manag. 2023, 10, 2213959. [Google Scholar] [CrossRef]

- Nguyen, Q.K. Ownership structure and bank risk-taking in ASEAN countries: A quantile regression approach. Cogent Econ. Financ. 2020, 8, 1809789. [Google Scholar] [CrossRef]

- Nguyen, Q.K.; Dang, V.C. The Effect of FinTech Development on Financial Stability in an Emerging Market: The Role of Market Discipline. Res. Glob. 2022, 5, 100105. [Google Scholar]

- Brouthers, K.D.; Brouthers, L.E.; Werne, R.S. Trans action cost enhanced entry mode choices and firm performance. Strateg. Manag. J. 2003, 24, 1239–1248. [Google Scholar] [CrossRef]

- Fan, J.P.H.; Wong, T.J.; Zhang, T. Institutions and Organizational Structure: The Case of State-Owned Corporate Pyramids. Journal of Law. Econ. Organ. 2013, 6, 1253–1278. [Google Scholar] [CrossRef]

- Helpman, E.; Melitz, M.; Yeaple, S. Export versus FDI with heterogeneous firms. Am. Econ. Rev. 2004, 94, 300–316. [Google Scholar] [CrossRef]

- Yang, X.Q.; Ren, X.Y.; Yang, Z. Does the mixed ownership reform of state-owned enterprises optimize the diversified behavior. Acc. Res. 2020, 390, 58–75. [Google Scholar]

| Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

{kind=link}