How Does the Degree of Competition in an Industry Affect a Company’s Environmental Management and Performance?

Abstract

:1. Introduction

2. Literature Review and Hypothesis Development

2.1. Environmental Management and Corporate Performance

2.2. Environmental Management Considering Industry Competition

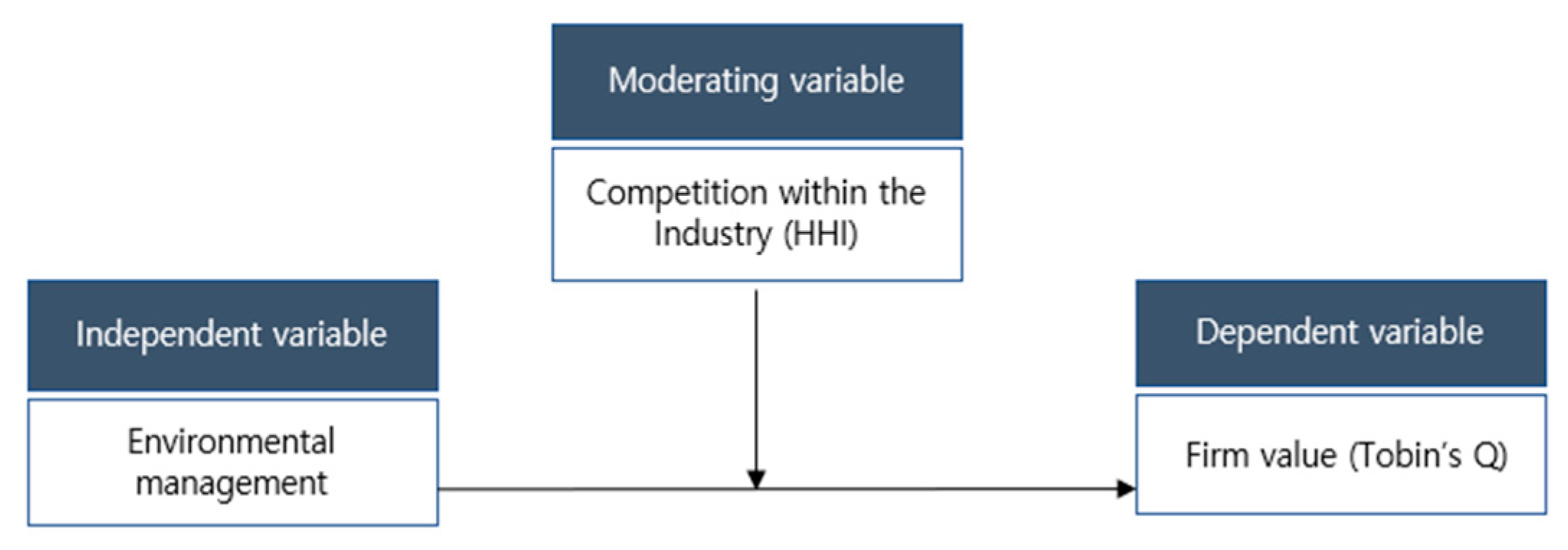

2.3. Theoretical Framework

3. Materials and Methods

3.1. Model Construction

3.2. Model Variables

3.3. Data Collection

4. Results

4.1. Extraction of Environmental Variables

4.2. Descriptive Statistics and Correlation Analysis

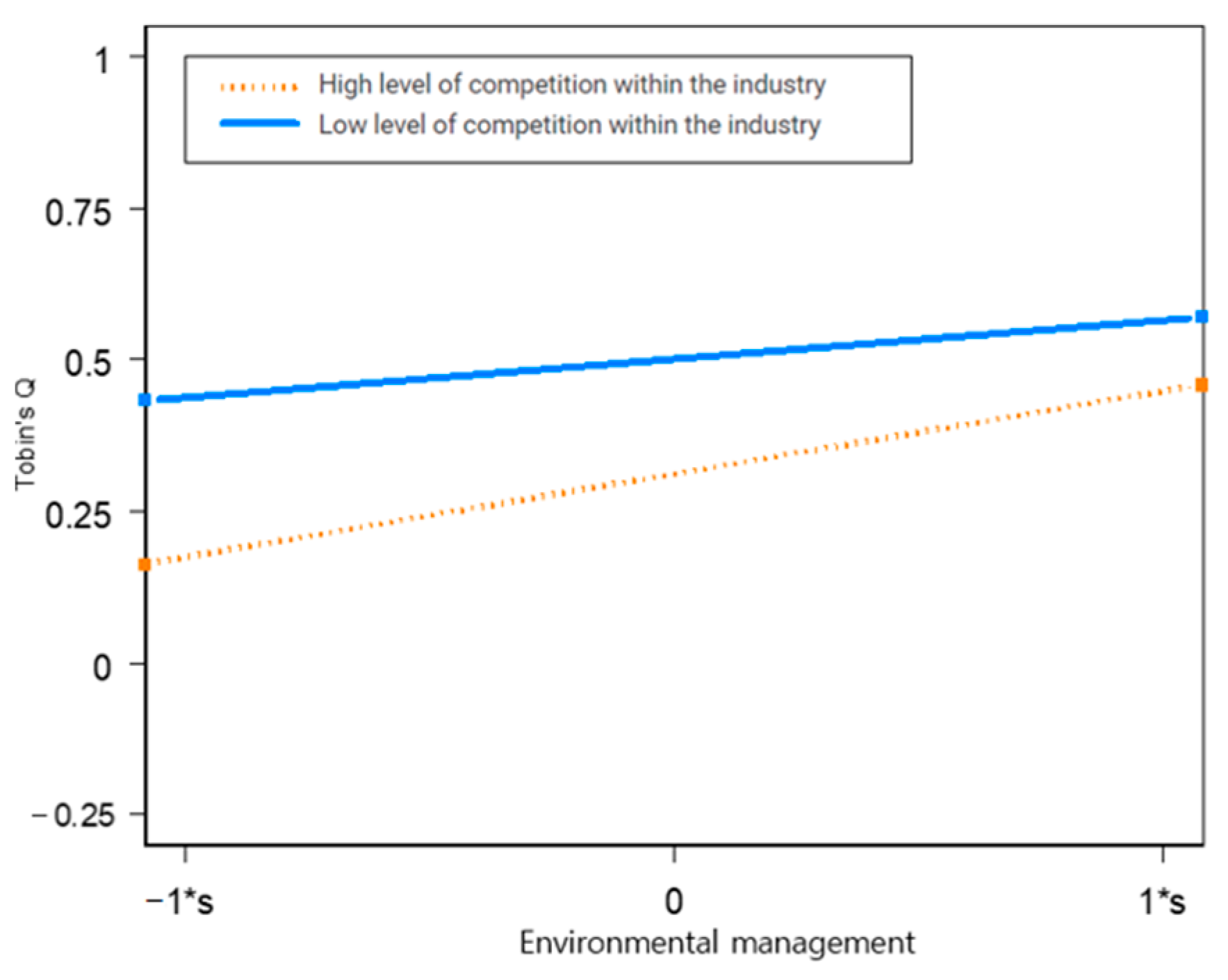

4.3. Regression Analysis Results

4.4. Further Analysis (Analysis of Environmental Management Mean Differences According to Competition within the Industry)

5. Conclusions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

References

- Yadav, P.L.; Han, S.H.; Rho, J.J. Impact of environmental performance on firm value for sustainable investment: Evidence from large US firms. Bus. Strategy Environ. 2016, 25, 402–420. [Google Scholar] [CrossRef]

- Younis, H.; Sundarakani, B. The impact of firm size, firm age and environmental management certification on the relationship between green supply chain practices and corporate performance. Benchmarking Int. J. 2020, 27, 319–346. [Google Scholar] [CrossRef]

- Xue, B.; Zhang, Z.; Li, P. Corporate environmental performance, environmental management and firm risk. Bus. Strategy Environ. 2020, 29, 1074–1096. [Google Scholar] [CrossRef]

- Micah, A.E.; Bhangdia, K.; Cogswell, I.E.; Lasher, D.; Lidral-Porter, B.; Berezvai, Z.; Gaál, P.; Joó, T.; Lám, J.; Palicz, T.G. Global investments in pandemic preparedness and COVID-19. Lancet Glob. Health 2023, 11, e385–e413. [Google Scholar] [CrossRef]

- Tchetchik, A.; Kaplan, S.; Blass, V. Recycling and consumption reduction following the COVID-19 lockdown: The effect of threat and coping appraisal, past behavior and information. Resour. Conserv. Recycl. 2021, 167, 105370. [Google Scholar] [CrossRef]

- Koh, H.-K.; Burnasheva, R.; Suh, Y.G. Perceived ESG (environmental, social, governance) and consumers’ responses: The mediating role of brand credibility, Brand Image, and perceived quality. Sustainability 2022, 14, 4515. [Google Scholar] [CrossRef]

- Birkland, T.A. In the wake of the Exxon Valdez: How environmental disasters influence policy. Environ. Sci. Policy Sustain. Dev. 1998, 40, 4–32. [Google Scholar] [CrossRef]

- South, D.; Vangala, S.; Hung, K. The Biden Administration’s Approach to Addressing Climate Change. Clim. Energy 2021, 37, 8–18. [Google Scholar] [CrossRef]

- Cai, Y.; Jo, H.; Pan, C. Doing well while doing bad? CSR in controversial industry sectors. J. Bus. Ethics 2012, 108, 467–480. [Google Scholar] [CrossRef]

- Keefe, J.F. From SRI to sustainable investing. GreenMoney J. 2007, 66. [Google Scholar]

- Milliken, F.J. Three types of perceived uncertainty about the environment: State, effect, and response uncertainty. Acad. Manag. Rev. 1987, 12, 133–143. [Google Scholar] [CrossRef]

- Porter, M.E. Competitive Strategy: Creating and Sustaining Superior Performance; The Free Press: New York, NY, USA, 1985. [Google Scholar]

- Porter, M.E.; Kramer, M.R. The competitive advantage of corporate philanthropy. Harv. Bus. Rev. 2002, 80, 56–68. [Google Scholar] [PubMed]

- Green, W.; Li, Q. Evidence of an expectation gap for greenhouse gas emissions assurance. Account. Audit. Account. J. 2011, 25, 146–173. [Google Scholar] [CrossRef]

- Hart, S.L. A natural-resource-based view of the firm. Acad. Manag. Rev. 1995, 20, 986–1014. [Google Scholar] [CrossRef]

- Shrivastava, P. Environmental technologies and competitive advantage. Strateg. Manag. J. 1995, 16, 183–200. [Google Scholar] [CrossRef]

- Russo, M.V.; Fouts, P.A. A resource-based perspective on corporate environmental performance and profitability. Acad. Manag. J. 1997, 40, 534–559. [Google Scholar] [CrossRef]

- Berman, S.L.; Wicks, A.C.; Kotha, S.; Jones, T.M. Does stakeholder orientation matter? The relationship between stakeholder management models and firm financial performance. Acad. Manag. J. 1999, 42, 488–506. [Google Scholar] [CrossRef]

- Al-Najjar, B.; Anfimiadou, A. Environmental policies and firm value. Bus. Strategy Environ. 2012, 21, 49–59. [Google Scholar] [CrossRef]

- Wang, L.; Li, S.; Gao, S. Do greenhouse gas emissions affect financial performance?–an empirical examination of Australian public firms. Bus. Strategy Environ. 2014, 23, 505–519. [Google Scholar] [CrossRef]

- Epstein, M.J.; Schnietz, K.E. Measuring the cost of environmental and labor protests to globalization: An event study of the failed 1999 Seattle WTO talks. Int. Trade J. 2002, 16, 129–160. [Google Scholar] [CrossRef]

- Branco, M.C.; Rodrigues, L.L. Issues in corporate social and environmental reporting research: An overview. Issues Soc. Environ. Account. 2007, 1, 72–90. [Google Scholar] [CrossRef]

- Baumgartner, R.J. Managing corporate sustainability and CSR: A conceptual framework combining values, strategies and instruments contributing to sustainable development. Corp. Soc. Responsib. Environ. Manag. 2014, 21, 258–271. [Google Scholar] [CrossRef]

- Kohli, A.K.; Jaworski, B.J. Market orientation: The construct, research propositions, and managerial implications. J. Mark. 1990, 54, 1–18. [Google Scholar] [CrossRef]

- Nikolaeva, R.; Bicho, M. The role of institutional and reputational factors in the voluntary adoption of corporate social responsibility reporting standards. J. Acad. Mark. Sci. 2011, 39, 136–157. [Google Scholar] [CrossRef]

- Fernández-Kranz, D.; Santaló, J. When necessity becomes a virtue: The effect of product market competition on corporate social responsibility. J. Econ. Manag. Strategy 2010, 19, 453–487. [Google Scholar] [CrossRef]

- Siegel, D.S.; Vitaliano, D.F. An empirical analysis of the strategic use of corporate social responsibility. J. Econ. Manag. Strategy 2007, 16, 773–792. [Google Scholar] [CrossRef]

- Bhattacharya, C.B.; Sen, S. Doing better at doing good: When, why, and how consumers respond to corporate social initiatives. Calif. Manag. Rev. 2004, 47, 9–24. [Google Scholar] [CrossRef]

- Campbell, J.L. Why would corporations behave in socially responsible ways? An institutional theory of corporate social responsibility. Acad. Manag. Rev. 2007, 32, 946–967. [Google Scholar] [CrossRef]

- Flammer, C. Does product market competition foster corporate social responsibility? Evidence from trade liberalization. Strateg. Manag. J. 2015, 36, 1469–1485. [Google Scholar] [CrossRef]

- Hox, J.J.; Maas, C.J.; Brinkhuis, M.J. The effect of estimation method and sample size in multilevel structural equation modeling. Stat. Neerl. 2010, 64, 157–170. [Google Scholar] [CrossRef]

- Raudenbush, S.W.; Bryk, A.S. Hierarchical Linear Models: Applications and Data Analysis Methods; Sage: New York, NY, USA, 2002; Volume 1. [Google Scholar]

- Chung, K.H.; Pruitt, S.W. A simple approximation of Tobin’s q. Financ. Manag. 1994, 23, 70–74. [Google Scholar] [CrossRef]

- Alajlani, S.E.; Posecion, O.T. Measuring market valuation of Amman stock exchange industrial sectors: Tobin’s Q ratio as investors’ market performance indicator. Res. J. Financ. Account. 2018, 9, 77–84. [Google Scholar]

- Jinji, N.; Zhang, X.; Haruna, S. Does a firm with higher Tobin’sq prefer foreign direct investment to foreign outsourcing? N. Am. J. Econ. Financ. 2019, 50, 101044. [Google Scholar] [CrossRef]

- Dhaliwal, D.; Huang, S.; Khurana, I.K.; Pereira, R. Product market competition and conditional conservatism. Rev. Account. Stud. 2014, 19, 1309–1345. [Google Scholar] [CrossRef]

- Bushee, B.J.; Noe, C.F. Corporate disclosure practices, institutional investors, and stock return volatility. J. Account. Res. 2000, 38, 171–202. [Google Scholar] [CrossRef]

- Scholtens, B. A note on the interaction between corporate social responsibility and financial performance. Ecol. Econ. 2008, 68, 46–55. [Google Scholar] [CrossRef]

- Mishra, S.; Suar, D. Does corporate social responsibility influence firm performance of Indian companies? J. Bus. Ethics 2010, 95, 571–601. [Google Scholar] [CrossRef]

- Monda, B.; Giorgino, M. Corporate Governance and shareholder value in listed firms: An empirical analysis in five countries (France, Italy, Japan, UK, USA). Corp. Ownersh. Control 2013, 10, 36–50. [Google Scholar] [CrossRef]

- Gregory, A.; Whittaker, J.; Yan, X. Corporate social performance, competitive advantage, earnings persistence and firm value. J. Bus. Financ. Account. 2016, 43, 3–30. [Google Scholar] [CrossRef]

- Boubaker, S.; Cellier, A.; Manita, R.; Saeed, A. Does corporate social responsibility reduce financial distress risk? Econ. Model. 2020, 91, 835–851. [Google Scholar] [CrossRef]

- Griffith, R. Product Market Competition, Efficiency and Agency Costs: An Empirical Analysis; IFS Working Papers; Institute for Fiscal Studies: London, UK, 2001. [Google Scholar]

- Kulic, N.; Dotti Sani, G.M.; Strauss, S.; Bellani, L. Economic disturbances in the COVID-19 crisis and their gendered impact on unpaid activities in Germany and Italy. Eur. Soc. 2021, 23, S400–S416. [Google Scholar] [CrossRef]

- Atkins, J.; Doni, F.; Gasperini, A.; Artuso, S.; La Torre, I.; Sorrentino, L. Exploring the effectiveness of sustainability measurement: Which ESG metrics will survive COVID-19? J. Bus. Ethics 2022, 1–18. [Google Scholar] [CrossRef] [PubMed]

{kind=link}

{kind=link}

| Item | Factor |

|---|---|

| Greenhouse Gas Emission Reduction | 0.525 |

| Waste Discharge Reduction | 0.767 |

| Recycling Rate | 0.520 |

| Environmental Investment Costs | 0.684 |

| Variable | Mean | SD | Minimum | Maximum |

|---|---|---|---|---|

| Energy Consumption Reduction (TJ) | −4640 | 144,710 | −1,475,037 | 2,369,125 |

| GHG Emissions Reduction (tCO2eq) | −42,180 | 501,700 | −4,317,504 | 8,084,702 |

| Waste Amount Reduction (TON) | −10,183 | 257,691 | −4,534,000 | 1,937,200 |

| Recycling Rate (%) | 0.68 | 0.25 | 0.02 | 1.00 |

| Environmental Investment Cost | 59,430 | 327,390 | 1.00 | 4,858,500 |

| R&D for Ecosystems (%) | 0.03 | 0.05 | 0.00 | 0.41 |

| Assets | 15.52 | 1.41 | 10.75 | 19.20 |

| Employees | 11,600 | 9200 | 169 | 310,000 |

| Foreign Equity (%) | 24.14 | 16.18 | 0 | 65 |

| Industry concentration (%) | 0.46 | 0.21 | 0.27 | 1.00 |

| Tobin’s Q | 1.12 | 1.01 | 0.07 | 6.74 |

| Variable | Environment | Assets | Employees | Foreign Equity | Industry Concentration | Tobin’s Q |

|---|---|---|---|---|---|---|

| Environment | 1 | |||||

| Assets | −0.074 | 1 | ||||

| Employees | −0.168 ** | 0.502 *** | 1 | |||

| Foreign Equity | −0.032 | 0.492 ** | 0.397 *** | 1 | ||

| Industry Concentration | −0.131 ** | 0.124 * | 0.063 | 0.021 | 1 | |

| Tobin’s Q | 0.138 ** | −0.192 | 0.004 | 0.374 *** | 0.387 *** | 1 |

| Dependent Variable | Model 1 | Model 2 | Model 3 | Model 4 |

|---|---|---|---|---|

| Null Model | ||||

| Constant | 0.135 (6.521 ***) | 0.328 (4.589) *** | 0.305 (5.804) *** | 0.310 (5.904) *** |

| Environment | 0.101 (2.589) * | 0.094 (2.488) * | 0.264 (2.814) ** | |

| Assets | −0.325 (−7.448) *** | −0.311 (−7.223) *** | −0.310 (−7.220) *** | |

| Employees | 0.004 (1.236) | 0.003 (1.191) | 0.003 (1.184) | |

| Foreign Equity | 0.036 (12.221) *** | 0.036 (12.209) *** | 0.033 (10.828) *** | |

| Industry Concentration | 0.211 (2.705) ** | 0.191 (2.324) * | ||

| Environment x Industry Concentration | −0.074 (−2.641) ** | |||

| σ2 | 0.82289 | 0.52766 | 0.52899 | 0.52875 |

| τ | 0.23206 | 0.16845 | 0.15171 | 0.15508 |

| Deviance | 1794.06 | 1214.28 | 1210.22 | 1205.65 |

| Concentration | Mean | SD | t | p | |

|---|---|---|---|---|---|

| Environmental management | High * | −0.42 | 0.86 | 15.07 | 0.000 |

| Low | 0.56 | 0.89 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Chang, Y.J.; Yoo, J.W. How Does the Degree of Competition in an Industry Affect a Company’s Environmental Management and Performance? Sustainability 2023, 15, 7675. https://doi.org/10.3390/su15097675

Chang YJ, Yoo JW. How Does the Degree of Competition in an Industry Affect a Company’s Environmental Management and Performance? Sustainability. 2023; 15(9):7675. https://doi.org/10.3390/su15097675

Chicago/Turabian StyleChang, Yu Jin, and Jae Wook Yoo. 2023. "How Does the Degree of Competition in an Industry Affect a Company’s Environmental Management and Performance?" Sustainability 15, no. 9: 7675. https://doi.org/10.3390/su15097675