1. Introduction

As China’s urbanization and industrialization continue to advance, green development is being challenged. As an essential player in the market economy, enterprises are responsible for coordinating economic growth with environmental protection [

1]. Green innovation can reduce pollution emissions in the production process [

2], which is critical to eliminating the conflict between China’s economic growth and environmental pollution [

3]. However, the high risk of green innovation poses some challenges to itself. Green technologies are more capital-intensive and risky than general innovations, making them more challenging to finance [

4]. Since commercial banks are the primary source of external financing for most companies in China, exploring how to increase the credit of commercial banks for corporate green innovation is of great practical importance for developing a green economy.

The attitude of commercial banks toward corporate innovation has evolved from aversion to tolerance. Early studies concluded that commercial banks have an aversion to innovative corporate behavior [

5]. On the one hand, commercial banks have an adversarial attitude toward risk, while corporate technology innovation is inherently high risk. On the other hand, commercial banks require companies to have stable cash flow that can repay principal and interest over a certain period, but technological innovation activities require continuous cash investment. However, many subsequent studies have found that commercial banks do indeed finance corporate innovation [

6]. Commercial banks are somewhat tolerant of this innovative behavior. In a fully competitive market environment, technological innovation becomes the key for enterprises to cultivate competitive advantages and eliminate the “homogenization trap” of products [

7]. Commercial banks recognize that sustained growth through technological innovation is the only way for companies to obtain sufficient cash flow to repay debt and interest [

8]. Commercial banks can identify with the practical logic of ‘technological innovation for business growth’, embrace the risk of innovation, and lend to innovative enterprises [

6]. The sustainable growth of enterprises through technological innovation has become a common goal for banks and enterprises. This ‘target binding effect’ provides sufficient evolutionary motivation for the commercial bank attitude to change from ‘innovation aversion’ to ‘innovation inclusion’. In the current context of advocating green development, achieving the green development of enterprises through green innovation has become a new common goal between enterprises and commercial banks [

9]. However, although commercial banks can accommodate the innovative activities of enterprises, to some degree, many enterprises face credit rationing due to information asymmetry and lack of collateral [

10].

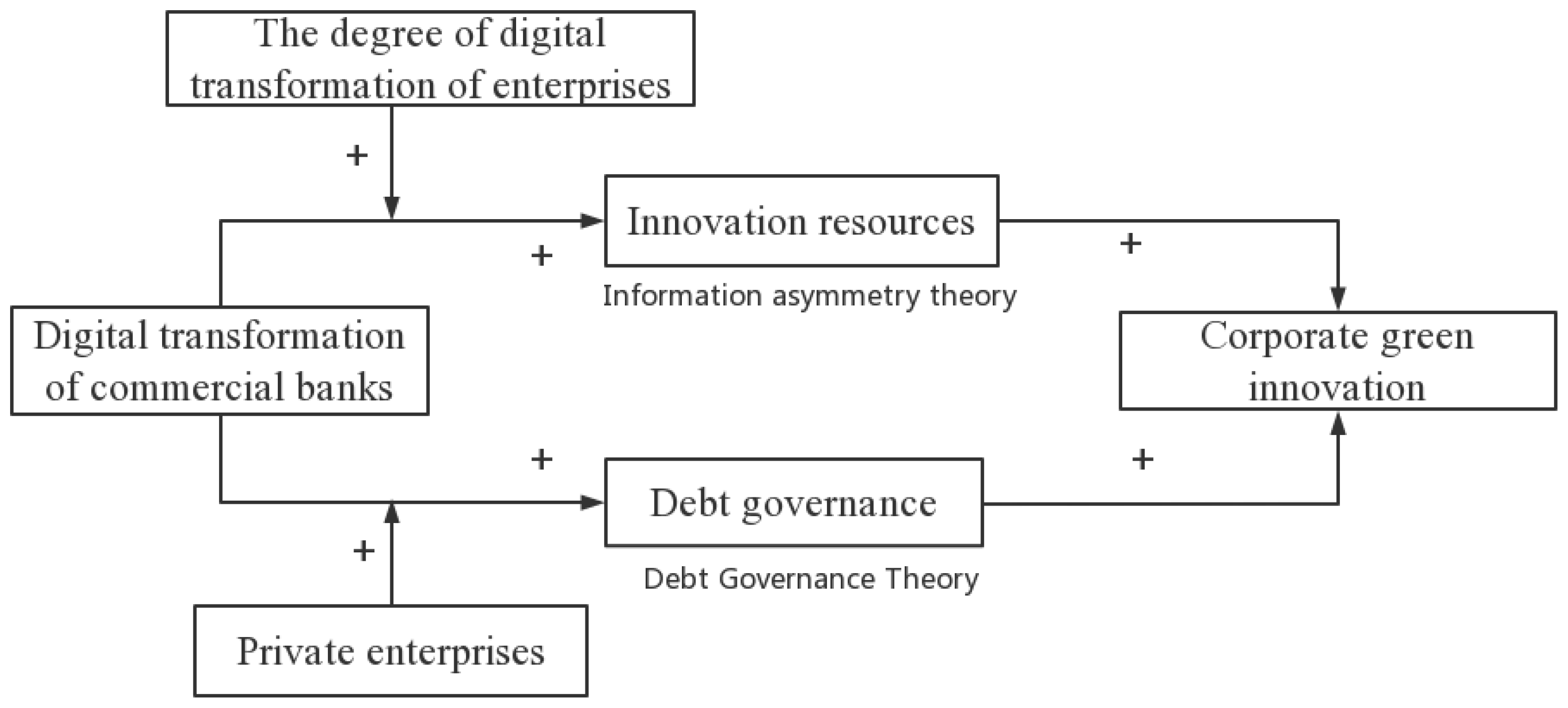

The digital transformation of commercial banks (DTCB) is conducive to improving their ability to serve the real economy and can affect green innovation. DTCB refers to the application of digital technologies, such as big data, cloud computing, blockchain technology, the Internet of things, and artificial intelligence by commercial banks to realize the online, intelligent, scenario-based, and platform-based banking business [

11]. Currently, commercial banks are beginning to implement digital transformation at a rapid pace [

12]. National commercial banks implement digital transformation by setting up fintech subsidiaries, while urban and rural commercial banks implement digital transformation by cooperating with fintech companies [

13]. DTCB can reduce information asymmetry and increase credit supply to enterprises [

14]. So, can DTCB promote green innovation by increasing lending to enterprises? If DTCB can effectively promote the green innovation of companies, exploring the effect of the green innovation of DTCB is vital to improving the environment.

Studies have been conducted to explore the impact of digital transformation on green innovation at both the macro and micro levels, respectively. At the macro level, ref. [

15] and ref. [

16] have found that the development of the digital economy promotes green innovation using data from the city panel at the prefecture level in China. Ref. [

17] has discovered that digital economy development can promote green innovation by promoting economic openness, optimizing the industrial structure, and expanding the market potential. From the micro level, ref. [

18] has found that the digital transformation of enterprises promotes green innovation by optimizing the human capital structure and strengthening the cooperation between industry and academia. Ref. [

19] has found that the digital transformation of enterprises promotes green innovation by enhancing the level of information sharing and resource allocation efficiency. Some studies focus on the green innovation effects of the digital transformation of financial institutions. Ref. [

20] and ref. [

21] have found that the development of fintech companies can significantly improve green innovation. The digital transformation of financial institutions includes the development of fintech companies and DTCB. In fact, fintech companies serve individual entrepreneurs and micro and small enterprises [

22] and engage less in green innovation. DTCB can increase lending to enterprises, which may promote the green innovation of enterprises. However, the existing research has mainly studied the relationship between fintech companies and green innovation, ignoring the relationship between DTCB and green innovation.

In summary, from the micro level, studies on the effects of digital transformation on green innovation have mainly focused on exploring the impact of the digital transformation of enterprises and fintech companies on green innovation of enterprises, and little literature has focused on the impact of DTCB on green innovation. Therefore, this paper fills this gap by exploring the effect of DTCB on the green innovation of enterprises.

The marginal contributions of this study are as follows. First, the research object of digital finance is extended to the banking system, enriching the research on the effect of digital finance on green innovation. Current research focuses on exploring the effect of fintech companies on green innovation, while the impact of DTCB on green innovation is yet to be studied. Under China’s bank-based financial system, ignoring the effect of DTCB on green innovation will make it difficult to clarify the effect of digital finance on green innovation. Second, it expands the research on the economic consequences of DTCB. The existing literature has mainly explored the impact of DTCB on the credit scale and credit structure, and the impact of DTCB on green innovation is yet to be studied. Hence, this paper further expands the economic consequences of DTCB. Third, the heterogeneity of DTCB affecting green innovation is explored. We have found that DTCB can only promote the green innovation of enterprises with a high degree of digital transformation, which provides a basis for government departments to further promote the digital transformation of enterprises to facilitate their green development.

5. Conclusions

The development of digital finance has changed the way financial services are provided and improved the ability of the financial system to serve the real economy. Many scholars have focused on the impact of digital finance on green innovation and have drawn some useful conclusions. However, existing studies only discuss the impact of the development of fintech companies on green innovation, ignoring the impact of the digital transformation of commercial banks (DTCB) on green innovation. Therefore, this paper fills this gap and explores the impact of DTCB on corporate green innovation. Based on the data of listed companies from 2010 to 2019, this study explores the impact of DTCB on enterprise green innovation. We find that DTCB has significantly promoted enterprise green innovation. Mechanism analysis shows that DTCB can promote green innovation by increasing R&D expenditures and reducing agency costs. The heterogeneity analysis indicates that DTCB can only promote green innovation in private enterprises and enterprises with a high degree of digital transformation, but it cannot promote green innovation in state-owned enterprises and enterprises with a low degree of digital transformation.

The following recommendations can be derived from our study, based on the above conclusions. First, the government should focus on solving the problem of the inadequate sharing of enterprise-related information. The mechanism analysis shows that the DTCB increases loans to enterprises by reducing information asymmetry, thus promoting green innovation. At present, enterprise-related information is scattered, so the government should broaden the information sources of commercial banks by building enterprise-related information sharing platforms and allowing DTCB to play a full role in promoting green innovation. The information sharing platform can collect and share the information within the purview of local governments, such as enterprise tax payment information, real estate information, compulsory administrative information, and water and electric fee payment information. Second, the government should guide and support the digital transformation of enterprises. The heterogeneity analysis shows that only when the digital transformation of enterprises reaches a certain level can DTCB significantly promote green innovation. Therefore, the government should guide and support enterprises to implement digital transformation. The government can give full play to the guiding role of central financial funds and encourage local governments to provide preferential support to the digital transformation of these enterprises. In addition, the government can build some platforms to provide enterprises with digital services, such as transformation consulting and software applications.

This paper clarifies the impact of DTCB on environmental green innovation. However, due to the difficulty in obtaining the digital transformation level of commercial banks that provide loans to unlisted companies, this paper does not explore the impact of DTCB on unlisted companies. In the future, if we obtain the digital transformation index of commercial banks that provide loans to unlisted companies, we will further test to determine the impact of DTCB on green environmental innovation in unlisted companies to deepen and expand our findings.

{kind=link}

{kind=link}