The Effects of Monetary Policy on Macroeconomic Variables through Credit and Balance Sheet Channels: A Dynamic Stochastic General Equilibrium Approach

Abstract

:1. Introduction

2. Literature Review

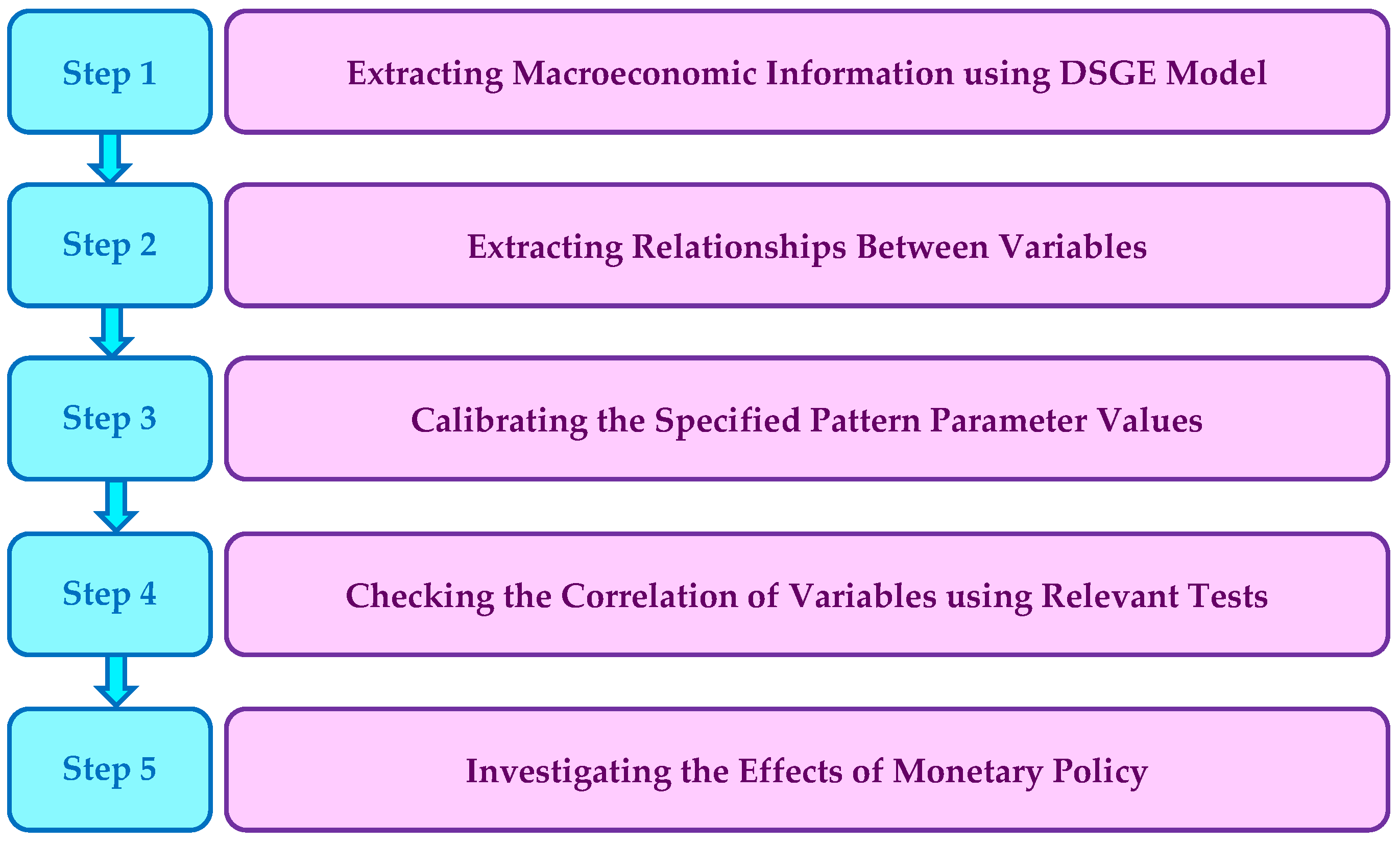

3. Methodology

3.1. Household

3.1.1. Risk-Avoiding Households

3.1.2. Risky Households

3.2. Manufacturers of Intermediate Goods

3.3. Manufacturers of Final Goods and Capital

3.4. Demand for Loans and Deposits

3.5. Labor Market

3.6. Banks

3.7. Monetary Policy Maker

3.8. Market Clearing Condition

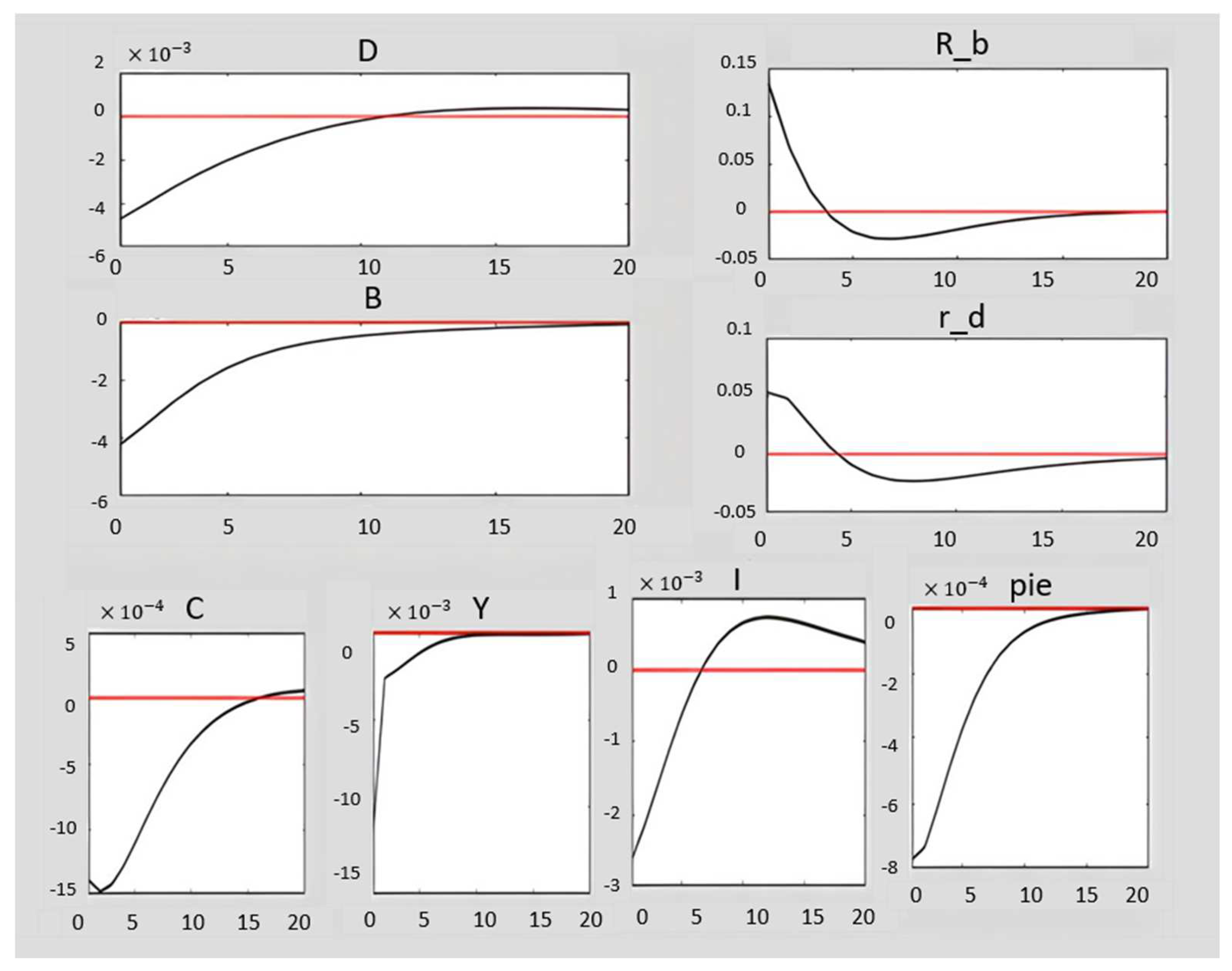

4. Results

5. Conclusions and Future Research Directions

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Pérez-Moreno, S.; Martín-Fuentes, N.; Albert, J. Rethinking Monetary Policy in the Framework of Inclusive and Sustainable Growth. In Economic Policies for Sustainability and Resilience; Springer: Berlin/Heidelberg, Germany, 2022; pp. 319–364. [Google Scholar]

- Ahmed, Z.; Asghar, M.M.; Malik, M.N.; Nawaz, K. Moving towards a sustainable environment: The dynamic linkage between natural resources, human capital, urbanization, economic growth, and ecological footprint in China. Resources Policy 2020, 67, 101677. [Google Scholar] [CrossRef]

- Jiang, Q.; Khattak, S.I.; Ahmad, M.; Ping, L. A new approach to environmental sustainability: Assessing the impact of monetary policy on CO2 emissions in Asian economies. Sustain. Dev. 2020, 28, 1331–1346. [Google Scholar]

- Kiseľáková, D.; Filip, P.; Onuferová, E.; Valentiny, T. The Impact of Monetary Policies on the Sustainable Economic and Financial Development in the Euro Area Countries. Sustainability 2020, 12, 9367. [Google Scholar] [CrossRef]

- Abdullah, S.; Morley, B. Environmental taxes and economic growth: Evidence from panel causality tests. Energy Econ. 2014, 42, 27–33. [Google Scholar] [CrossRef] [Green Version]

- Watkiss, P.; Hunt, A. Projection of economic impacts of climate change in sectors of Europe based on bottom up analysis: Human health. Clim. Change 2012, 112, 101–126. [Google Scholar] [CrossRef] [Green Version]

- Morley, B. Causality between economic growth and immigration: An ARDL bounds testing approach. Econ. Lett. 2006, 90, 72–76. [Google Scholar] [CrossRef]

- Özatay, F. Sustainability of fiscal deficits, monetary policy, and inflation stabilization: The case of Turkey. J. Policy Model. 1997, 19, 661–681. [Google Scholar] [CrossRef]

- Faza’, M.; Badwan, N. The Risk of Capital Flight on Economic Growth and National Solvency: An Empirical Evidence from Palestine. Asian J. Econ. Bus. Account. 2023, 23, 28–48. [Google Scholar] [CrossRef]

- Zungu, L.T.; Greyling, L. Exploring the Dynamic Shock of Unconventional Monetary Policy Channels on Income Inequality: A Panel VAR Approach. Soc. Sci. 2022, 11, 369. [Google Scholar] [CrossRef]

- Mosconi, R.; Paruolo, P. A Conversation with Katarina Juselius. Econometrics 2022, 10, 20. [Google Scholar] [CrossRef]

- Ascari, G.; Haber, T. Non-Linearities, State-Dependent Prices and the Transmission Mechanism of Monetary Policy. Econ. J. R. Econ. Soc. 2022, 132, 37–57. [Google Scholar] [CrossRef]

- Xiang, G.; Tang, J.; Yao, S.H. The Characteristics of the Housing Market and the Goal of Stable and Healthy Development in China’s Cities. J. Risk Financ. Manag. 2022, 15, 450. [Google Scholar] [CrossRef]

- Papadamou, S.; Kyriazis, N.A.; Tzeremes, P.G. Unconventional monetary policy effects on output and inflation: A meta-analysis. Int. Rev. Financ. Anal. 2019, 61, 295–305. [Google Scholar] [CrossRef]

- Yıldız, B.F.; Gökmenoğlu, K.K.; Wong, W.K. Analysing Monetary Policy Shocks by Sign and Parametric Restrictions: The Evidence from Russia. Economies 2022, 10, 239. [Google Scholar] [CrossRef]

- Oyeleke, O.J.; Oyelami, L.O.; Ogundipe, A.A. Investigating the monetary and fiscal policy regimes dominance for inflation determination in Nigeria: A Bayesian TVP-VAR analysis. Int. J. Comput. Econ. Econom. 2022, 12, 223–240. [Google Scholar] [CrossRef]

- Azad, N.A.; Serletis, A.; Xu, L. COVID-19 and monetary–fiscal policy interactions in Canada. Q. Rev. Econ. Financ. 2021, 81, 376–384. [Google Scholar] [CrossRef]

- Madhou, A.; Sewak, T.; Moosa, I.; Ramiah, V.; Gerth, F. Towards Full-Fledged Inflation Targeting Monetary Policy Regime in Mauritius. J. Risk Financ. Manag. 2021, 14, 126. [Google Scholar] [CrossRef]

- Ofoi, M. The Monetary Policy Transmission Mechanism in Papua New Guinea: A Structural Vector Autoregressive (SVAR) Approach. IUP J. Appl. Econ. 2021, 20, 7–39. [Google Scholar]

- Rohoia, A.B.; Sharma, P. Do Inflation Expectations Matter for Small, Open Economies? Empirical Evidence from the Solomon Islands. J. Risk Financ. Manag. 2021, 14, 448. [Google Scholar] [CrossRef]

- Asshoff, S.; Belke, A.; Osowski, T. Unconventional monetary policy and inflation expectations in the Euro area. Econ. Model. 2021, 102, 105564. [Google Scholar] [CrossRef]

- Simmons, R.; Dini, P.; Culkin, N.; Littera, G. Crisis and the Role of Money in the Real and Financial Economies—An Innovative Approach to Monetary Stimulus. J. Risk Financ. Manag. 2021, 14, 129. [Google Scholar] [CrossRef]

- Li, L.; Feng, L.; Guo, X.; Xie, H.; Shi, W. Complex Network Analysis of Transmission Mechanism for Sustainable Incentive Policies. Sustainability 2020, 12, 745. [Google Scholar] [CrossRef] [Green Version]

- Reid, M.; Siklos, P.; Guetterman, T.; Du Plessis, S. The role of financial journalists in the expectations channel of the monetary transmission mechanism. CAMA Work. Pap. Res. Int. Bus. Financ. 2020, 55, 101320. [Google Scholar] [CrossRef]

- Lhuissier, S.; Szczerbowicz, U. Monetary Policy and Corporate Debt Structure. Work. Pap. 2018, 84, 497–515. [Google Scholar] [CrossRef] [Green Version]

- Castro, A.E.; Teixeira, J.F. The Formation of New Monetary Policies: Decisions of Central Banks on the Great Recession. Economies 2014, 2, 109–123. [Google Scholar] [CrossRef] [Green Version]

- Cristi, S.; Mihai, N. Monetary Policy Transmission Mechanism in Romania Over the Period 2001 to 2012: A Bvar Analysis. Sci. Ann. Econ. Bus. Sciendo 2013, 60, 1–12. [Google Scholar]

- Gurrib, I. GCC Economic Integration: Statistical Harmonization for an Effective Monetary Union. In The GCC Economies, Stepping Up to Future Challenges; Springer: Berlin/Heidelberg, Germany, 2012; pp. 21–32. [Google Scholar]

- Bhattarai, S.; Neely, C.J. An Analysis of the Literature on International Unconventional Monetary Policy. J. Econ. Lit. 2022, 60, 527–597. [Google Scholar] [CrossRef]

- Bianchi, J.; Bigio, S. Banks, Liquidity Management, and Monetary Policy. Econometrica 2022, 90, 391–454. [Google Scholar] [CrossRef]

- Davoodalhosseini, M. Central bank digital currency and monetary policy. J. Econ. Dyn. Control. 2022, 142, 104150. [Google Scholar] [CrossRef]

- Wang, Y.; Whited, T.M.; Wu, Y.; Xiao, K. Bank Market Power and Monetary Policy Transmission: Evidence from a Structural Estimation. J. Am. Financ. Assoc. 2022, 77, 2093–2141. [Google Scholar] [CrossRef]

- Bianchi, F.; Lettau, M.; Ludvigson, S.C. Monetary Policy and Asset Valuation. J. Am. Financ. Assoc. 2022, 77, 967–1017. [Google Scholar] [CrossRef]

- Kekre, R.; Lenel, M. Monetary Policy, Redistribution, and Risk Premia. Econometrica 2022, 90, 2249–2282. [Google Scholar] [CrossRef]

- Drechsler, I.; Savov, A.; Schnabl, P.H. How monetary policy shaped the housing boom. J. Financ. Econ. 2022, 144, 992–1021. [Google Scholar] [CrossRef]

- Bauer, M.D.; Lakdawala, A.; Mueller, P. Market-Based Monetary Policy Uncertainty. Econ. J. 2022, 132, 1290–1308. [Google Scholar] [CrossRef]

- Eichenbaum, M.; Rebelo, S.; Wong, A. State-Dependent Effects of Monetary Policy: The Refinancing Channel. Am. Econ. Rev. 2022, 112, 721–761. [Google Scholar] [CrossRef]

- Correa, R.; Paligorova, T.; Sapriza, H.; Zlate, A. Cross-Border Bank Flows and Monetary Policy. Rev. Financ. Stud. 2022, 35, 438–481. [Google Scholar] [CrossRef]

- Lepetit, A.; Fuentes-Albero, C. The limited power of monetary policy in a pandemic. Eur. Econ. Rev. 2022, 147, 104168. [Google Scholar] [CrossRef]

- Gali, J. Insider–Outsider Labor Markets, Hysteresis, and Monetary Policy. J. Money Credit. Bank. 2022, 54, 53–88. [Google Scholar] [CrossRef]

- Gootjes, B.; de Haan, J. Procyclicality of fiscal policy in European Union countries. J. Int. Money Financ. 2022, 120, 102276. [Google Scholar] [CrossRef]

- Ai, H.; Han, L.J.; Pan, X.N.; Xu, L. The cross section of the monetary policy announcement premium. J. Financ. Econ. 2022, 143, 247–276. [Google Scholar] [CrossRef]

- Zhang, T. Monetary Policy Spillovers through Invoicing Currencies. J. Am. Financ. Assoc. 2022, 77, 129–161. [Google Scholar] [CrossRef]

- Cochrane, J.H. A fiscal theory of monetary policy with partially-repaid long-term debt. Rev. Econ. Dyn. 2022, 45, 1–21. [Google Scholar] [CrossRef]

- Colciago, A.; Silvestrini, R. Monetary policy, productivity, and market concentration. Eur. Econ. Rev. 2022, 142, 103999. [Google Scholar] [CrossRef]

- Ampudia, M.; Van den Heuvel, S.J. Monetary Policy and Bank Equity Values in a Time of Low and Negative Interest Rates. J. Monet. Econ. 2022, 130, 49–67. [Google Scholar] [CrossRef]

- Wen, H.; Lee, C.H.; Zhou, F. How does fiscal policy uncertainty affect corporate innovation investment? Evidence from China’s new energy industry. Energy Econ. 2022, 105, 105767. [Google Scholar] [CrossRef]

- Hamano, M.; Zanetti, F. Monetary policy, firm heterogeneity, and product variety. Eur. Econ. Rev. 2022, 144, 104089. [Google Scholar] [CrossRef]

- Neely, C.J. How persistent are unconventional monetary policy effects? J. Int. Money Financ. 2022, 126, 102653. [Google Scholar] [CrossRef]

- Mahmood, H.; Adow, A.H.; Abbas, M.; Iqbal, A.; Murshed, M.; Furqan, M. The Fiscal and Monetary Policies and Environment in GCC Countries: Analysis of Territory and Consumption-Based CO2 Emissions. Sustainability 2022, 14, 1225. [Google Scholar] [CrossRef]

- Zenchenko, S.; Strielkowski, W.; Smutka, L.; Vacek, T.; Radyukova, Y.; Sutyagin, V. Monetization of the Economies as a Priority of the New Monetary Policy in the Face of Economic Sanctions. J. Risk Financ. Manag. 2022, 15, 140. [Google Scholar] [CrossRef]

- Dai, Y. Monetary Policy and Financial Sustainability in a Two-State Open Economy. Sustainability 2022, 14, 4825. [Google Scholar] [CrossRef]

- Desalegn, G.; Fekete-Farkas, M.; Tangl, A. The Effect of Monetary Policy and Private Investment on Green Finance: Evidence from Hungary. J. Risk Financ. Manag. 2022, 15, 117. [Google Scholar] [CrossRef]

- Petrakis, N.; Lemonakis, C.; Floros, C.; Zopounidis, C. Eurozone Stock Market Reaction to Monetary Policy Interventions and Other Covariates. J. Risk Financ. Manag. 2022, 15, 56. [Google Scholar] [CrossRef]

- Ribba, A. Monetary Policy Shocks in Open Economies and the Inflation Unemployment Trade-Off: The Case of the Euro Area. J. Risk Financ. Manag. 2022, 15, 146. [Google Scholar] [CrossRef]

- Cortes, G.S.; Gao, G.P.; Silva, F.B.; Song, Z. Unconventional monetary policy and disaster risk: Evidence from the subprime and COVID–19 crises. J. Int. Money Financ. 2022, 122, 102543. [Google Scholar] [CrossRef]

- Siregar, I.; Rahmadiyah, F.; Siregar, A.F.Q. Linguistic Intervention in Making Fiscal and Monetary Policy. Int. J. Arts Humanit. Stud. 2021, 1, 50–56. [Google Scholar] [CrossRef]

- Chishti, M.Z.; Ahmad, M.; Rehman, A.; Kamran Khan, M. Mitigations pathways towards sustainable development: Assessing the influence of fiscal and monetary policies on carbon emissions in BRICS economies. J. Clean. Prod. 2021, 292, 126035. [Google Scholar] [CrossRef]

- Khalid, U.; Okafor, L.E.; Burzynska, K. Does the size of the tourism sector influence the economic policy response to the COVID-19 pandemic? Curr. Issues Tour. 2019, 24, 19. [Google Scholar] [CrossRef]

- Zhenghui, L.; Junhao, Z. Impact of economic policy uncertainty shocks on China’s financial conditions. Financ. Res. Lett. 2020, 35, 101303. [Google Scholar]

- Luo, S.; Zhou, G.; Zhou, J. The Impact of Electronic Money on Monetary Policy: Based on DSGE Model Simulations. Mathematics 2021, 9, 2614. [Google Scholar] [CrossRef]

- Wang, R. Evaluating the Unconventional Monetary Policy of the Bank of Japan: A DSGE Approach. J. Risk Financ. Manag. 2021, 14, 253. [Google Scholar] [CrossRef]

- Sohail, M.T.; Xiuyuan, Y.; Usman, A.; Majeed, M.T.; Ullah, S. Renewable energy and non-renewable energy consumption: Assessing the asymmetric role of monetary policy uncertainty in energy consumption. Environ. Sci. Pollut. 2021, 28, 31575–31584. [Google Scholar] [CrossRef] [PubMed]

- Le, H. The Impacts of Credit Standards on Aggregate Fluctuations in a Small Open Economy: The Role of Monetary Policy. Economies 2021, 9, 203. [Google Scholar] [CrossRef]

- Miranda-Agrippino, S.; Ricco, G. The Transmission of Monetary Policy Shocks. Am. Econ. J. Macroecon. 2021, 13, 74–107. [Google Scholar] [CrossRef]

- Luetticke, R. Transmission of Monetary Policy with Heterogeneity in Household Portfolios. Am. Econ. J. Macroecon. 2021, 13, 1–25. [Google Scholar] [CrossRef]

- Bernanke, B.S. The New Tools of Monetary Policy. Am. Econ. Rev. 2021, 110, 943–983. [Google Scholar] [CrossRef] [Green Version]

- Zhang, X.; Zhang, Y.; Zhu, Y. COVID-19 Pandemic, Sustainability of Macroeconomy, and Choice of Monetary Policy Targets: A NK-DSGE Analysis Based on China. Sustainability 2021, 13, 3362. [Google Scholar] [CrossRef]

- Jarociński, M.; Karadi, P. Deconstructing Monetary Policy Surprises—The Role of Information Shocks. Am. Econ. J. Macroecon. 2020, 12, 1–43. [Google Scholar] [CrossRef] [Green Version]

- Ottonello, P.; Winberry, T. Financial Heterogeneity and the Investment Channel of Monetary Policy. Econometrica 2020, 88, 2473–2502. [Google Scholar] [CrossRef]

- Altavilla, C.; Brugnolini, L.; Gürkaynak, R.S.; Motto, R.; Ragusa, G. Measuring euro area monetary policy. J. Monet. Econ. 2019, 108, 162–179. [Google Scholar] [CrossRef]

- Yin, X.; Xu, X.; Chen, Q.; Peng, J. The Sustainable Development of Financial Inclusion: How Can Monetary Policy and Economic Fundamental Interact with It Effectively? Sustainability 2019, 11, 2524. [Google Scholar] [CrossRef] [Green Version]

- Auclert, A. Monetary Policy and the Redistribution Channel. Am. Econ. Rev. 2019, 109, 2333–2367. [Google Scholar] [CrossRef] [Green Version]

- Marfatia, H.A.; Gupta, R.; Lesame, K. Dynamic Impact of Unconventional Monetary Policy on International REITs. J. Risk Financ. Manag. 2021, 14, 429. [Google Scholar] [CrossRef]

- Tran, L.M.; Mai, C.H.; Le, P.H.; Vu Bui, C.L.; Nguyen, L.V.P.; Huynh, T.L.D. Monetary Policy, Cash Flow and Corporate Investment: Empirical Evidence from Vietnam. J. Risk Financ. Manag. 2019, 12, 46. [Google Scholar] [CrossRef] [Green Version]

- Jiang, Y.; Li, C.; Zhang, J.; Zhou, X. Financial Stability and Sustainability under the Coordination of Monetary Policy and Macroprudential Policy: New Evidence from China. Sustainability 2019, 11, 1616. [Google Scholar] [CrossRef] [Green Version]

- Lütkepohl, H.; Netšunajev, A. The Relation between Monetary Policy and the Stock Market in Europe. Econometrics 2018, 6, 36. [Google Scholar] [CrossRef] [Green Version]

- Botshekan, M.H.; Takaloo, A.; Soureh, R.H.; Abdollahi Poor, M.S. Global Economic Policy Uncertainty (GEPU) and Non-Performing Loans (NPL) in Iran’s Banking System: Dynamic Correlation using the DCC-GARCH Approach. J. Money Econ. 2021, 16, 187–212. [Google Scholar] [CrossRef]

- Hsing, Y. Effects of Fiscal Policy and Monetary Policy on the Stock Market in Poland. Economies 2013, 1, 19–25. [Google Scholar] [CrossRef] [Green Version]

- Mishchenko, V.; Naumenkova, S.; Mishchenko, S. Assessing the efficiency of the monetary transmission mechanism channels in Ukraine. Banks Bank Syst. 2021, 16, 48–62. [Google Scholar] [CrossRef]

- Oddo, L.; Bosnjak, M. A comparative analysis of the monetary policy transmission channels in the U.S.: A wavelet-based approach. Appl. Econ. Taylor Fr. J. 2021, 53, 4448–4463. [Google Scholar] [CrossRef]

- Bulir, A.; Vlcek, J. Monetary transmission: Are emerging market and low-income countries different? J. Policy Model. 2021, 43, 95–108. [Google Scholar] [CrossRef]

- Kabundi, A.; Rapapali, M. The Transmission of Monetary Policy in South Africa Before and After the Global Financial Crisis. SAGE 2019, 87, 464–489. [Google Scholar] [CrossRef]

- Atgur, M.; Altay, N.O. Examination of the exchange rate and interest rate channels of the monetary transmission mechanism during the inflation targeting: Turkey and Mexico countries examples. Theor. Appl. Econ. 2017, XXIV, 137–160. [Google Scholar]

- Cambazoğlu, B.; Karaalp, H. The External Finance Premium and the Financial Accelerator: The Case of Turkey. Int. J. Econ. Sci. Appl. Res. 2013, 6, 103. [Google Scholar]

- Boivin, J.; Kiley, M.T.; Mishkin, F.S. How Has the Monetary Transmission Mechanism Evolved Over Time? Handb. Monet. Econ. 2010, 3, 369–422. [Google Scholar]

- Ganev, G.Y.; Molnar, K.; Rybinski, K.; Wozniak, P. Transmission Mechanism of Monetary Policy in Central and Eastern Europe. CASE Netw. Rep. 2002, 1–33. [Google Scholar] [CrossRef] [Green Version]

- Juselius, K. A Theory-Consistent CVAR Scenario for a Monetary Model with Forward-Looking Expectations. Econometrics 2022, 10, 16. [Google Scholar] [CrossRef]

- Habibi, Z.; Habibi, H.; Aqa Mohammadi, M. The Potential Impact of COVID-19 on the Chinese GDP, Trade, and Economy. Economies 2022, 10, 73. [Google Scholar] [CrossRef]

- Ahmad, M.S.; Szczepankiewicz, E.I.; Yonghong, D.; Ullah, F.; Ullah, I.; Loopesco, W.E. Does Chinese Foreign Direct Investment (FDI) Stimulate Economic Growth in Pakistan? An Application of the Autoregressive Distributed Lag (ARDL Bounds) Testing Approach. Energies 2022, 15, 2050. [Google Scholar] [CrossRef]

- Jena, P.R.; Majhi, J.; Kalli, R.; Managi, S.; Majhi, B. Impact of COVID-19 on GDP of major economies: Application of the artificial neural network forecaster. Econ. Anal. Policy 2021, 69, 324–339. [Google Scholar] [CrossRef]

- Oravský, R.; Tóth, P.; Bánociová, A. The Ability of Selected European Countries to Face the Impending Economic Crisis Caused by COVID-19 in the Context of the Global Economic Crisis of 2008. J. Risk Financ. Manag. 2020, 13, 179. [Google Scholar] [CrossRef]

- Blanchard, O. Public Debt and Low Interest Rates. Am. Econ. Rev. 2019, 109, 1197–1229. [Google Scholar] [CrossRef] [Green Version]

- Maddah, M.; Ghaffari Nejad, A.H.; Sargolzaei, M. Natural resources, political competition, and economic growth: An empirical evidence from dynamic panel threshold kink analysis in Iranian provinces. Resour. Policy 2022, 78, 102928. [Google Scholar] [CrossRef]

- Iacoviello, M.; Navarro, G. Foreign effects of higher U.S. interest rates. J. Int. Money Financ. 2019, 95, 232–250. [Google Scholar] [CrossRef]

- Altavilla, C.; Boucinha, M.; Peydró, J.L. Monetary policy and bank profitability in a low interest rate environment. Econ. Policy 2018, 33, 531–586. [Google Scholar] [CrossRef] [Green Version]

- Brissimis, S.N.; Papafilis, M.P. The Credit Channel of Monetary Transmission in the Us: Is it a Bank Lending Channel, a Balance Sheet Channel, or Both, or Neither? Bank Greece Work. Pap. 2022, 300. [Google Scholar]

- Tayem, G. Credit Constraints and Investment-Cash Flow Sensitivity in Declining Economic Conditions: The Role of Reliance on Bank Debt. Economies 2022, 10, 288. [Google Scholar] [CrossRef]

- Kozak, S. The Impact of COVID-19 on Bank Equity and Performance: The Case of Central Eastern South European Countries. Sustainability 2021, 13, 11036. [Google Scholar] [CrossRef]

- Ghanbari, H.; Fooeik, A.; Eskorouchi, A.; Mohammadi, E. Investigating the effect of US dollar, gold and oil prices on the stock market. J. Future Sustain. 2022, 2, 97–104. [Google Scholar] [CrossRef]

- Soltani, S.; Falihi, N.; Mehrabiyan, A.; Amiri, H. Investigating the Effects of Monetary and Financial Shocks on the Key Macroeconomic Variables, focusing on the Intermediary Role of Banks Using DSGE Models. J. Monet. Econ. 2021, 16, 477–500. [Google Scholar] [CrossRef]

- Boroumand, S.; Mohamadi, T.; Memar Nejad, A.; Baghfalaki, F. The Effect of External Shocks on Macroeconomic Variables for the Iranian Economy in the form of New Keynesian DSGE Model. Q. J. Econ. Res. Policies 2020, 28, 93–121. [Google Scholar] [CrossRef]

- Saadat Nezhad, A.; Tabatabaienasab, Z.; Abtahi, S.Y.; DehghanTafti, M. The Foreign Exchange Intervention Impact on Macroeconomic Variables in Iran: DSGE Approach. Econ. Strategy 2020, 8, 79–115. [Google Scholar]

- Rafiee, S.; Emami, K.; Ghaffari, F. The Effect of Monetary Policies on Performance of Banks: A Dynamic Stochastic General Equilibrium (DSGE) Approach. Econ. Res. 2019, 19, 1–36. [Google Scholar]

- Shah Hosseini, S.; Bahrami, J. Macroeconomic fluctuations and monetary transmission mechanism in Iran (DSGE model approach). Econ. Res. Pap. 2014, 60, 1–40. [Google Scholar]

- Shahmoradi, A.; Ebrahimi, I. Evaluating the effects of monetary policies in Iran’s economy in the form of a New Keynesian stochastic dynamic model. J. Monet. Bank. Res. 2010, 3, 31–56. [Google Scholar]

- Gurrib, I. The Relationship Between a Unified Financial Condition Index and The Most Actively Traded USD Based Foreign Currency Pairs. Inst. Econ. 2020, 12, 93–127. [Google Scholar]

- Bernanke, B.N.; Gertler, M. Monetary policy and asset price volatility. Econ. Rev. Fed. Reserve Bank Kans. City 1999, 84, 17–51. [Google Scholar]

- Bernanke, B.N.; Gertler, M. Inside the Black Box: The Credit Channel of Monetary Policy Transmission. J. Econ. Perspect. Am. Econ. Assoc. 1995, 9, 27–48. [Google Scholar] [CrossRef] [Green Version]

- Gurrib, I. Measuring Risk for Large Hedgers and Large Speculators in Major US Futures Markets. J. Risk 2010, 12, 79–103. [Google Scholar] [CrossRef]

- Batten, J.A.; Choudhury, T.; Kinateder, H.; Wagner, N. Volatility impacts on the European banking sector: GFC and COVID-19. Ann. Oper. Res. 2022, 1–26. [Google Scholar] [CrossRef]

- Bernanke, B.S.; Gertler, M.; Gilchrist, S. The financial accelerator in a quantitative business cycle framework. Handb. Macroecon. 1999, 1, 1341–1393. [Google Scholar]

- Iacoviello, M.; Neri, S. Housing market spillovers: Evidence from an estimated DSGE model. Am. Econ. Assoc. 2010, 2, 125–164. [Google Scholar] [CrossRef] [Green Version]

- Ullah, A.; Zhao, X.; Kamal, M.A.; Riaz, A.; Zheng, B. Exploring asymmetric relationship between Islamic banking development and economic growth in Pakistan: Fresh evidence from a non-linear ARDL approach. Int. J. Financ. Econ. 2021, 26, 6168–6187. [Google Scholar] [CrossRef]

- Ullah, A.; Zhao, X.; Kamal, M.A.; Zheng, J. Modeling the relationship between military spending and stock market development (a) symmetrically in China: An empirical analysis via the NARDL approach. Phys. Stat. Mech. Appl. 2020, 554, 124106. [Google Scholar] [CrossRef]

- Chowdhury, A.; Hamid, M.K.; Akhi, R.A. Impact of Macroeconomic Variables on Economic Growth: Bangladesh Perspective. Inf. Manag. Comput. Sci. (IMCS) 2021, 2, 19–22. [Google Scholar] [CrossRef]

- Aysun, U. Bank Size and Macroeconomic Shock Transmission: Are There Economic Volatility Gains from Shrinking Large, Too Big to Fail Banks? Working Papers, University of Central Florida, Department of Economics: Orlando, FL, USA, 2013. [Google Scholar]

- Yagihashi, T. How costly is a misspecified credit channel DSGE model in monetary policymaking? Econ. Model. 2018, 68, 484–505. [Google Scholar] [CrossRef] [Green Version]

- Taguchi, H.; Gunbileg, G. Monetary Policy Rule and Taylor Principle in Mongolia: GMM and DSGE Approaches. Int. J. Financ. Stud. 2020, 8, 71. [Google Scholar] [CrossRef]

- De Jesus, D.P.; Besarria, C.N.; Maia, S.F. The macroeconomic effects of monetary policy shocks under fiscal constrained: An analysis using a DSGE model. J. Econ. Stud. 2020, 47, 805–825. [Google Scholar] [CrossRef]

- Nguyen, T.D.; Le, A.H.; Thalassinos, E.I.; Trieu, L.K. The Impact of the COVID-19 Pandemic on Economic Growth and Monetary Policy: An Analysis from the DSGE Model in Vietnam. Economies 2022, 10, 159. [Google Scholar] [CrossRef]

- Zhang, B.; Ai, X.; Fang, X.; Chen, S. The Transmission Mechanisms and Impacts of Oil Price Fluctuations: Evidence from DSGE Model. Energies 2022, 15, 6038. [Google Scholar] [CrossRef]

- Li, Y.; Wang, M. Capital regulation, monetary policy and asymmetric effects of commercial banks’ efficiency. China Financ. Rev. Int. 2012, 2, 5–26. [Google Scholar] [CrossRef]

- Farvaque, E.; Stanek, P.; Vigeant, S. On the performance of monetary policy committees. Kyklos 2014, 67, 177–203. [Google Scholar] [CrossRef] [Green Version]

- Seyed Esmaeili, F.S. The efficiency of MSBM model with imprecise data (interval). Int. J. Data Envel. Anal. 2014, 2, 343–350. [Google Scholar]

- Peykani, P.; Mohammadi, E.; Seyed Esmaeili, F.S. Measuring performance, estimating most productive scale size, and benchmarking of hospitals using DEA approach: A case study in Iran. Int. J. Hosp. Res. 2018, 7, 21–41. [Google Scholar]

- Nouri, M.; Mohammadi, E.; Rahmanipour, M. A novel efficiency ranking approach based on goal programming and data envelopment analysis for the evaluation of Iranian banks. Int. J. Data Envel. Anal. 2019, 7, 57–80. [Google Scholar]

- Peykani, P.; Mohammadi, E.; Emrouznejad, A.; Pishvaee, M.S.; Rostamy-Malkhalifeh, M. Fuzzy data envelopment analysis: An adjustable approach. Expert Syst. Appl. 2019, 136, 439–452. [Google Scholar] [CrossRef]

- Peykani, P.; Seyed Esmaeili, F.S.; Hosseinzadeh Lotfi, F.; Rostamy-Malkhalifeh, M. Estimating most productive scale size in DEA under uncertainty. In Proceedings of the 11th National Conference on Data Envelopment Analysis, Shiraz, Iran, 28 August 2019. [Google Scholar]

- Wanke, P.; Azad, M.A.K.; Emrouznejad, A.; Antunes, J. A dynamic network DEA model for accounting and financial indicators: A case of efficiency in MENA banking. Int. Rev. Econ. Financ. 2019, 61, 52–68. [Google Scholar] [CrossRef] [Green Version]

- Žaja, M.M.; Kordić, G.; Kedžo, M.G. The analysis of the contextual variables affecting the fiscal rules efficiency in the EU. Croat. Oper. Res. Rev. 2019, 10, 153–164. [Google Scholar] [CrossRef]

- Henriques, I.C.; Sobreiro, V.A.; Kimura, H.; Mariano, E.B. Two-stage DEA in banks: Terminological controversies and future directions. Expert Syst. Appl. 2020, 161, 113632. [Google Scholar] [CrossRef]

- Magnani, V.M.; da Costa Gomes, M.; Antônio, R.M.; Gatsios, R.C. Impact of Monetary Policy Changes on Brazilian Banking Efficiency during Crises. Theor. Econ. Lett. 2020, 10, 1019. [Google Scholar] [CrossRef]

- Peykani, P.; Mohammadi, E.; Farzipoor Saen, R.; Sadjadi, S.J.; Rostamy-Malkhalifeh, M. Data envelopment analysis and robust optimization: A review. Expert Syst. 2020, 37, e12534. [Google Scholar] [CrossRef]

- Peykani, P.; Mohammadi, E.; Jabbarzadeh, A.; Rostamy-Malkhalifeh, M.; Pishvaee, M.S. A novel two-phase robust portfolio selection and optimization approach under uncertainty: A case study of Tehran stock exchange. PLoS ONE 2020, 15, e0239810. [Google Scholar] [CrossRef] [PubMed]

- Seyed Esmaeili, F.S.; Rostamy-Malkhalifeh, M.; Hosseinzadeh Lotfi, F. Two-stage network DEA model under interval data. Math. Anal. Convex Optim. 2020, 1, 103–108. [Google Scholar] [CrossRef]

- Arabjazi, N.; Rostamy-Malkhalifeh, M.; Hosseinzadeh Lotfi, F.; Behzadi, M.H. Stochastic sensitivity analysis in data envelopment analysis. Fuzzy Optim. Model. J. 2021, 2, 52–64. [Google Scholar]

- Hu, Y.; Li, B.; Zha, Y.; Zhang, D. How monetary policies and ownership structure affect bank supply chain efficiency: A DEA-based case study. Ind. Manag. Data Syst. 2021, 121, 750–769. [Google Scholar] [CrossRef]

- Peykani, P.; Farzipoor Saen, R.; Seyed Esmaeili, F.S.; Gheidar-Kheljani, J. Window data envelopment analysis approach: A review and bibliometric analysis. Expert Syst. 2021, 38, e12721. [Google Scholar] [CrossRef]

- Peykani, P.; Mohammadi, E.; Emrouznejad, A. An adjustable fuzzy chance-constrained network DEA approach with application to ranking investment firms. Expert Syst. Appl. 2021, 166, 113938. [Google Scholar] [CrossRef]

- Okeke, I.C.; Chukwu, K.O. Effect of monetary policy on the rate of unemployment in Nigerian economy (1986–2018). J. Glob. Account. 2021, 7, 1–13. [Google Scholar]

- Seyed Esmaeili, F.S.; Rostamy-Malkhalifeh, M.; Hosseinzadeh Lotfi, F. A hybrid approach using data envelopment analysis, interval programming and robust optimisation for performance assessment of hotels under uncertainty. Int. J. Manag. Decis. Mak. 2021, 20, 308–322. [Google Scholar]

- Tan, Y.; Wanke, P.; Antunes, J.; Emrouznejad, A. Unveiling endogeneity between competition and efficiency in Chinese banks: A two-stage network DEA and regression analysis. Ann. Oper. Res. 2021, 306, 131–171. [Google Scholar] [CrossRef]

- Peykani, P.; Namakshenas, M.; Arabjazi, N.; Shirazi, F.; Kavand, N. Optimistic and pessimistic fuzzy data envelopment analysis: Empirical evidence from Tehran stock market. Fuzzy Optim. Model. J. 2021, 2, 12–21. [Google Scholar]

- Peykani, P.; Seyed Esmaeili, F.S. Malmquist productivity index under fuzzy environment. Fuzzy Optim. Model. J. 2021, 2, 10–19. [Google Scholar]

- Antunes, J.; Hadi-Vencheh, A.; Jamshidi, A.; Tan, Y.; Wanke, P. Bank efficiency estimation in China: DEA-RENNA approach. Ann. Oper. Res. 2022, 315, 1373–1398. [Google Scholar] [CrossRef]

- Arabjazi, N.; Rostamy-Malkhalifeh, M.; Hosseinzadeh Lotfi, F.; Behzadi, M.H. Determining the exact stability region and radius through efficient hyperplanes. Iran. J. Manag. Stud. 2022, 15, 287–303. [Google Scholar]

- Arabjazi, N.; Rostamy-Malkhalifeh, M.; Hosseinzadeh Lotfi, F.; Behzadi, M.H. Stability analysis with general fuzzy measure: An application to social security organizations. PLoS ONE 2022, 17, e0275594. [Google Scholar] [CrossRef]

- Peykani, P.; Hosseinzadeh Lotfi, F.; Sadjadi, S.J.; Ebrahimnejad, A.; Mohammadi, E. Fuzzy chance-constrained data envelopment analysis: A structured literature review, current trends, and future directions. Fuzzy Optim. Decis. Mak. 2022, 21, 197–261. [Google Scholar] [CrossRef]

- Peykani, P.; Emrouznejad, A.; Mohammadi, E.; Gheidar-Kheljani, J. A novel robust network data envelopment analysis approach for performance assessment of mutual funds under uncertainty. Ann. Oper. Res. 2022, 1–27. [Google Scholar] [CrossRef]

- Li, Z.; Feng, C.; Tang, Y. Bank efficiency and failure prediction: A nonparametric and dynamic model based on data envelopment analysis. Ann. Oper. Res. 2022, 315, 279–315. [Google Scholar] [CrossRef]

- Seyed Esmaeili, F.S.; Rostamy-Malkhalifeh, M.; Hosseinzadeh Lotfi, F. Interval network Malmquist productivity index for examining productivity changes of insurance companies under data uncertainty: A case study. J. Math. Ext. 2022, 16, 9. [Google Scholar]

- Peykani, P.; Gheidar-Kheljani, J.; Farzipoor Saen, R.; Mohammadi, E. Generalized robust window data envelopment analysis approach for dynamic performance measurement under uncertain panel data. Oper. Res. Int. J. 2022, 22, 5529–5567. [Google Scholar] [CrossRef]

- Zaman, M.S.; Bhandari, A.K. Stressed assets, off-balance sheet business activities and performance of Indian banking sector: A DEA double bootstrap approach. Stud. Econ. Financ. 2022, 39, 572–592. [Google Scholar] [CrossRef]

- Peykani, P.; Memar-Masjed, E.; Arabjazi, N.; Mirmozaffari, M. Dynamic performance assessment of hospitals by applying credibility-based fuzzy window data envelopment analysis. Healthcare 2022, 10, 876. [Google Scholar] [CrossRef] [PubMed]

- Peykani, P.; Seyed Esmaeili, F.S.; Mirmozaffari, M.; Jabbarzadeh, A.; Khamechian, M. Input/Output Variables Selection in Data Envelopment Analysis: A Shannon Entropy Approach. Mach. Learn. Knowl. Extr. 2022, 4, 688–699. [Google Scholar] [CrossRef]

- Gao, S.; Sun, H.; Wang, R. Audit Evaluation and Driving Force Analysis of Marine Economic Development Quality. Sustainability 2022, 14, 6822. [Google Scholar] [CrossRef]

- Jiang, Y.; Wang, Y.; Wang, R. Coupling and Coordination Relationship between Economic and Ecologic-Environmental Developments in China’s Key State-Owned Forest Areas. Sustainability 2022, 14, 15899. [Google Scholar] [CrossRef]

- Thaker, K.; Charles, V.; Pant, A.; Gherman, T. A DEA and random forest regression approach to studying bank efficiency and corporate governance. J. Oper. Res. Soc. 2022, 73, 1258–1277. [Google Scholar] [CrossRef]

- Li, M.; Zhu, N.; He, K.; Li, M. Operational Efficiency Evaluation of Chinese Internet Banks: Two-Stage Network DEA Approach. Sustainability 2022, 14, 14165. [Google Scholar] [CrossRef]

- Sari, S.; Ajija, S.R.; Wasiaturrahma, W.; Ahmad, R.A.R. The Efficiency of Indonesian Commercial Banks: Does the Banking Industry Competition Matter? Sustainability 2022, 14, 10995. [Google Scholar] [CrossRef]

- Fukuyama, H.; Tsionas, M.; Tan, Y. Dynamic network data envelopment analysis with a sequential structure and behavioural-causal analysis: Application to the Chinese banking industry. Eur. J. Oper. Res. 2023, 307, 1360–1373. [Google Scholar] [CrossRef]

- Wanke, P.; Rojas, F.; Tan, Y.; Moreira, J. Temporal dependence and bank efficiency drivers in OECD: A stochastic DEA-ratio approach based on generalized auto-regressive moving averages. Expert Syst. Appl. 2023, 214, 119120. [Google Scholar] [CrossRef]

- Sohn, S.Y.; Ju, Y. Mission Efficiency Analysis of For-Profit Microfinance Institutions with Categorical Output Variables. Sustainability 2023, 15, 2732. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Parameter | Symbol | Value |

|---|---|---|

| Interest Rate of Risk-Averse Household | 0.994 | |

| Interest Rate of Risky Household | 0.979 | |

| Share of Risk-Averse Households in Labor Supply | 0.975 | |

| Importance of Housing in Household Utility | 0.1 | |

| Share of Capital in Production | 0.412 | |

| Depreciation Rate of Physical Capital | 0.023 | |

| Production Growth Rate | 6 | |

| Wage Increase in Labor Market | 5 | |

| Ratio of Loans to the Value of Households Assets | 0.7 | |

| Ratio of Loans to the Value of Corporates Assets | 0.3 | |

| Optimal Capital Adequacy Ratio | 0.08 | |

| Growth Rate of Granting Lending Services to Households | 2.93 | |

| Growth Rate of Granting Lending Services to Corporates | 2.93 | |

| Cost of Bank Capital | 0.023 | |

| Adjustment Cost of Capacity Utilization | ξ | 0.047 |

| Variable | Standard Deviation | Correlation with Non-Oil Production | ||

|---|---|---|---|---|

| Real World | Model | Real World | Model | |

| Non-Oil Production | 0.03 | 0.04 | 1 | 1 |

| Consumption | 0.04 | 0.02 | 0.605 | 0.567 |

| Loan | 0.062 | 0.07 | 0.702 | 0.452 |

| Deposit | 0.066 | 0.09 | 0.3 | 0.53 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Peykani, P.; Sargolzaei, M.; Takaloo, A.; Valizadeh, S. The Effects of Monetary Policy on Macroeconomic Variables through Credit and Balance Sheet Channels: A Dynamic Stochastic General Equilibrium Approach. Sustainability 2023, 15, 4409. https://doi.org/10.3390/su15054409

Peykani P, Sargolzaei M, Takaloo A, Valizadeh S. The Effects of Monetary Policy on Macroeconomic Variables through Credit and Balance Sheet Channels: A Dynamic Stochastic General Equilibrium Approach. Sustainability. 2023; 15(5):4409. https://doi.org/10.3390/su15054409

Chicago/Turabian StylePeykani, Pejman, Mostafa Sargolzaei, Amir Takaloo, and Shahla Valizadeh. 2023. "The Effects of Monetary Policy on Macroeconomic Variables through Credit and Balance Sheet Channels: A Dynamic Stochastic General Equilibrium Approach" Sustainability 15, no. 5: 4409. https://doi.org/10.3390/su15054409