Adoption of the Green Economy through Branchless Rural Credit Banks during the COVID-19 Pandemic in Indonesia

, ,

, ,  and

and

Abstract

:1. Introduction

2. Theoretical Foundation

2.1. Technology Acceptance Model

2.2. Green Economics

3. Methods

4. Results and Discussion

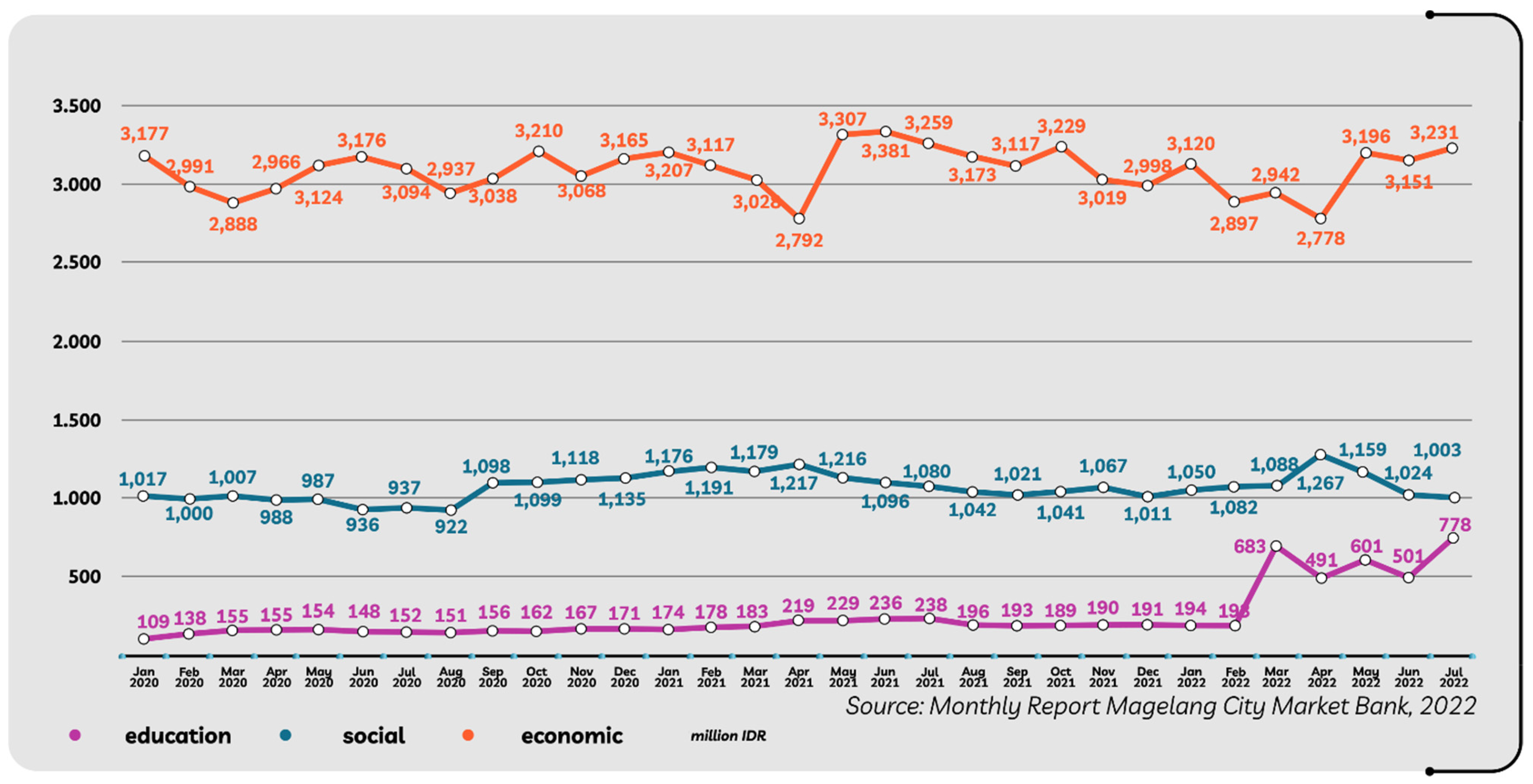

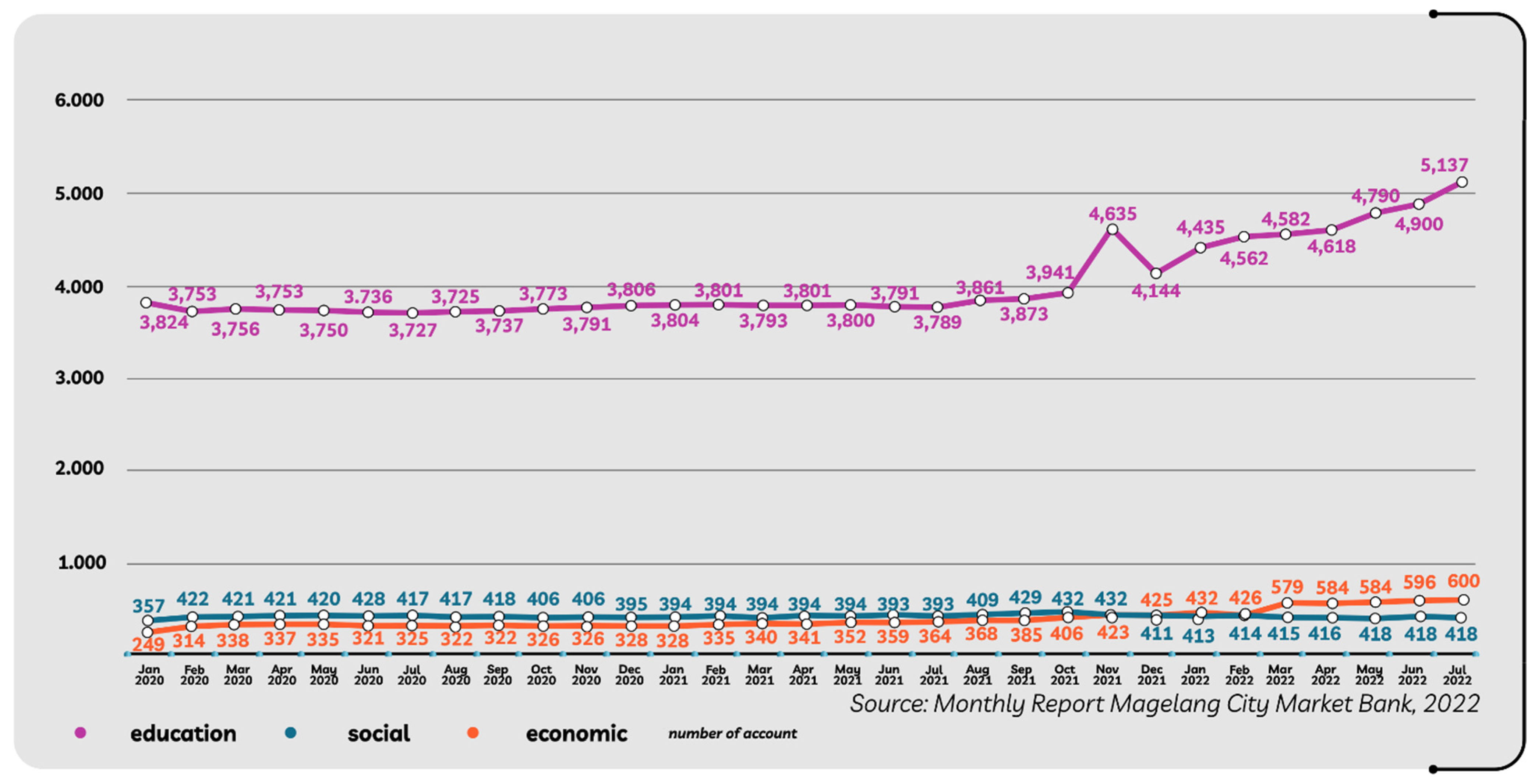

4.1. Branchless Banking in Urban Residents

4.2. Quantity of COVID-19 in Magelang City

4.3. COVID-19 Victims vs. Branchless Banking Customers

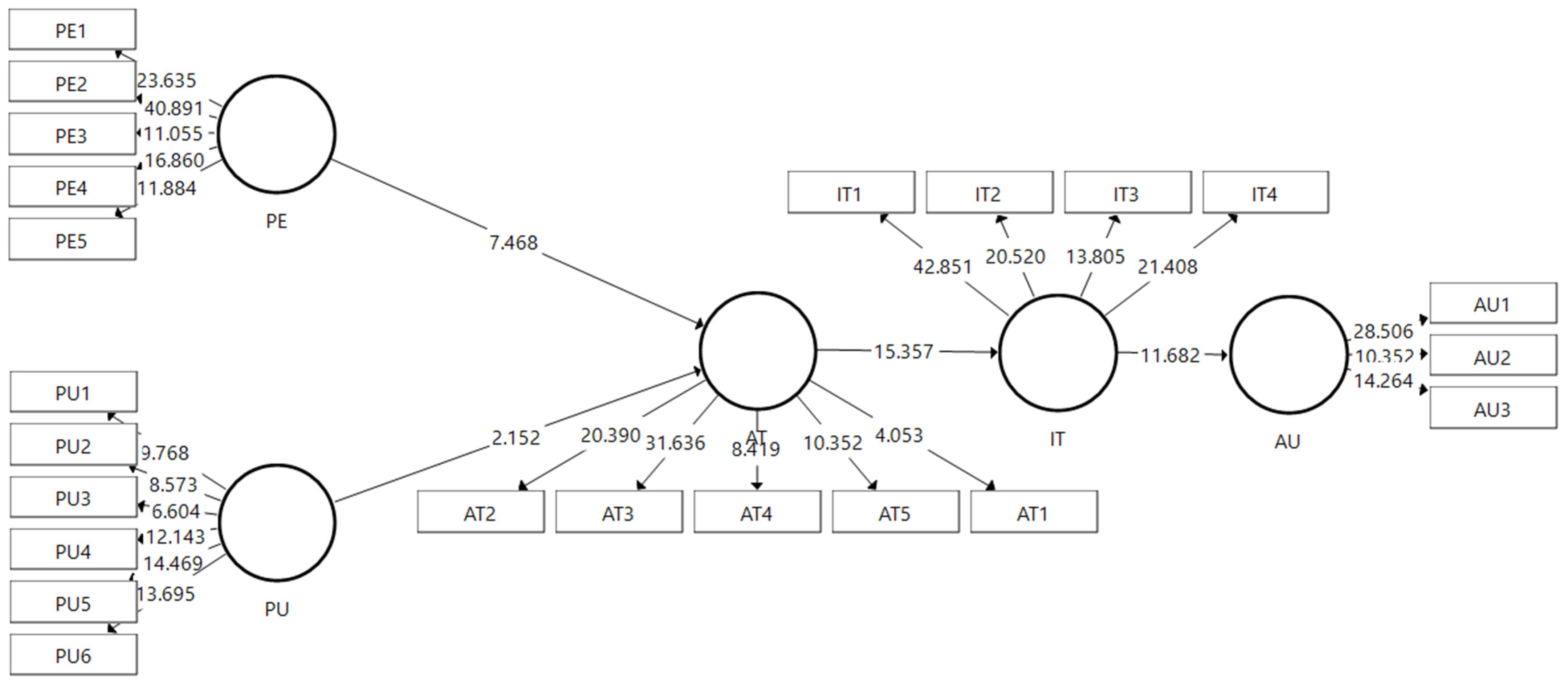

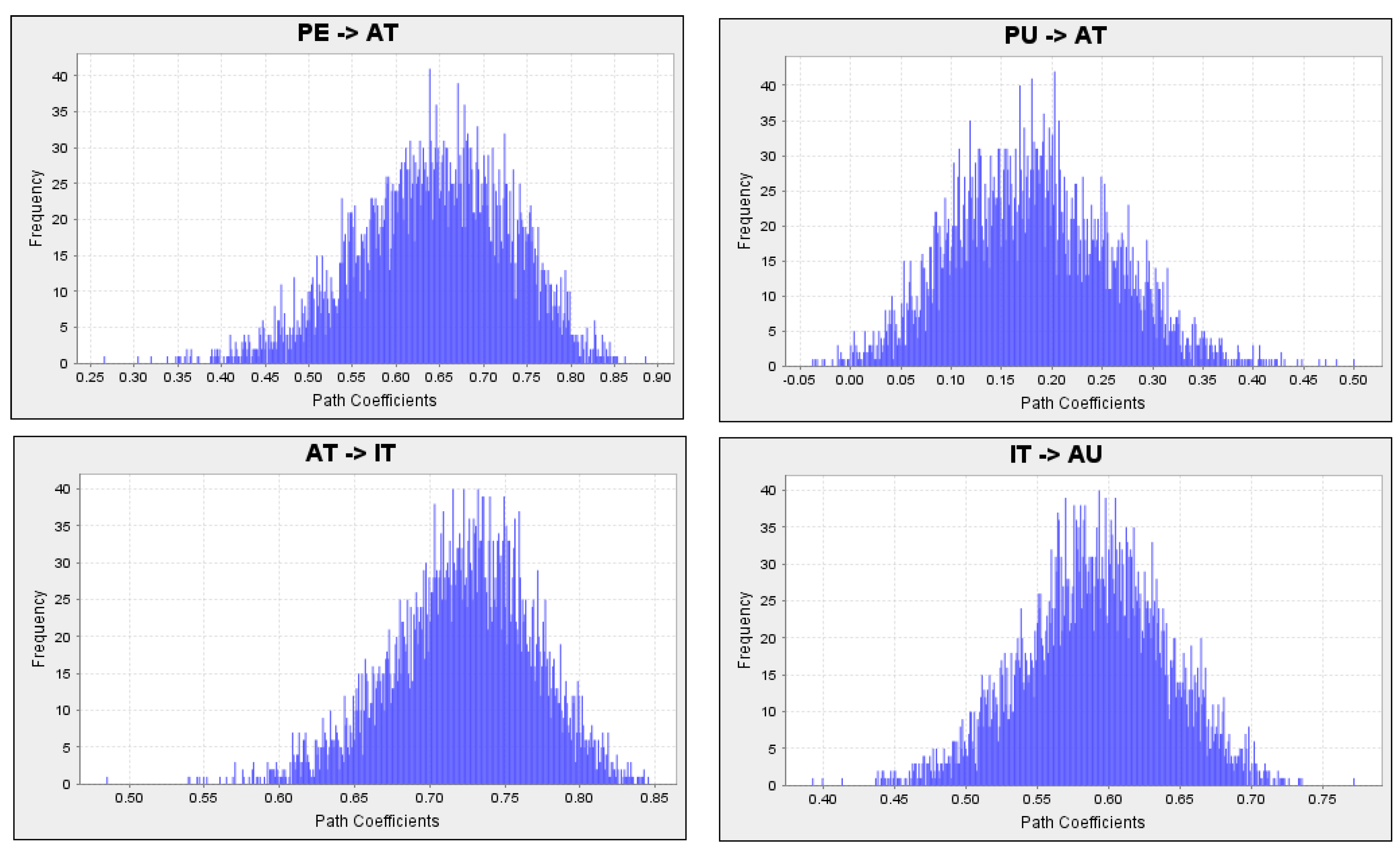

4.4. Path Analysis

4.5. Discussion

4.6. Customer Satisfaction with Branchless Banking

4.7. Branchless Banking Effectiveness in the Green Economy

5. Conclusions, Implication, and Suggestion

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Stukalo, N.; Simakhova, A. Social Dimensions of Green Economy. Filos. Sociol. 2019, 30, 91–99. [Google Scholar] [CrossRef]

- Yudiana, F.E. Modifikasi Branchless Banking Pada Perbankan Syariah Di Indonesia Berdasarkan Kearifan Lokal. Muqtasid. J. Ekon. Dan Perbank. Syariah 2018, 9, 14. [Google Scholar] [CrossRef]

- Djakasaputra, A.; Wijaya, O.Y.A.; Utama, A.S.; Yohana, C.; Romadhoni, B.; Fahlevi, M. Empirical Study of Indonesian SMEs Sales Performance in Digital Era: The Role of Quality Service and Digital Marketing. Int. J. Data Netw. Sci. 2021, 5, 303–310. [Google Scholar] [CrossRef]

- Afandi, M.A. Contribution of Islamic Commercial Bank Financing to East Java Economic Growth in the Era of Branchless Banking. J. Econ. Res. Soc. Sci. 2021, 5, 1–12. [Google Scholar] [CrossRef]

- Kasztelan, A. Green Growth, Green Economy and Sustainable Development: Terminological and Relational Discourse. Prague Econ. Pap. 2017, 26, 487–499. [Google Scholar] [CrossRef]

- Sukhdev, P.; Varma, K.; Bassi, A.M.; Allen, E.; Mumbunan, S. The Use of Green Economy Indicators in the Indonesia Green Economy Model (I-GEM); UNDP: Jakarta, Indonesia, 2014. [Google Scholar]

- Mikhno, I.; Koval, V.; Shvets, G.; Garmatiuk, O.; Tamošiūnienė, R. Green Economy in Sustainable Development and Improvement of Resource Efficiency. Cent. Eur. Bus. Rev. 2021, 10, 99–113. [Google Scholar] [CrossRef]

- Ali, E.B.; Anufriev, V.P.; Amfo, B. Green Economy Implementation in Ghana as a Road Map for a Sustainable Development Drive: A Review. Sci. Afr. 2021, 12, e00756. [Google Scholar] [CrossRef]

- Kasayanond, A.; Umam, R.; Jermsittiparsert, K. Environmental Sustainability and Its Growth in Malaysia by Elaborating the Green Economy and Environmental Efficienc. Int. J. Energy Econ. Policy 2019, 9, 465–473. [Google Scholar] [CrossRef]

- Bergius, M.; Benjaminsen, T.A.; Maganga, F.; Buhaug, H. Green Economy, Degradation Narratives, and Land-Use Conflicts in Tanzania. World Dev. 2020, 129, 104850. [Google Scholar] [CrossRef]

- Prasetyo, A.; Gartika, D.; Hartopo, A.; Harwijayanti, B.P.; Sukamsi, S.; Fahlevi, M. Capacity Development of Local Service Organizations Through Regional Innovation in Papua, Indonesia After the COVID-19 Pandemic. Front Psychol. 2022, 13, 1–8. [Google Scholar] [CrossRef]

- Prasetyo, A.; Putri Harwijayanti, B.; Ikhwan, M.N.; Lukluil Maknun, M.; Fahlevi, M. Interaction of Internal and External Organizations in Encouraging Community Innovation. Front Psychol. 2022, 13, 1–9. [Google Scholar] [CrossRef] [PubMed]

- OJK. Strategi Nasional Keuangan Inklusif; Otoritas Jasa Keuangan: Jakarta, Indonesia, 2016. [Google Scholar]

- OJK. Roadmap Tim Percepatan Akses Keuangan Daerah 2021–2025; Otoritas Jasa Keuangan: Jakarta, Indonesia, 2020. [Google Scholar]

- Wardani, T.; Astuti, R.F. Perilaku Pengelolaan Keuangan Berbasis Green Economy. Ekuitas J. Pendidik. Ekon. 2022, 10, 138–144. [Google Scholar]

- Petrosillo, N.; Viceconte, G.; Ergonul, O.; Ippolito, G.; Petersen, E. COVID-19, SARS and MERS: Are They Closely Related? Clin. Microbiol. Infect. 2020, 26, 729–734. [Google Scholar] [CrossRef] [PubMed]

- Fahlevi, M.; Alharbi, N.S. The Used of Technology to Improve Health Social Security Agency Services in Indonesia. In Proceedings of the 3rd International Conference on Cybernetics and Intelligent Systems, ICORIS 2021, Makasar, Indonesia, 25–26 October 2021; Institute of Electrical and Electronics Engineers Inc.: Makassar, Indonesia. [Google Scholar]

- Alharbi, N.S.; Alghanmi, A.S.; Fahlevi, M. Adoption of Health Mobile Apps during the COVID-19 Lockdown: A Health Belief Model Approach. Int. J. Environ. Res. Public Health 2022, 19, 4179. [Google Scholar] [CrossRef]

- Fahlevi, M.; Alharbi, N.S. Adoption of E-Payment System to Support Health Social Security Agency. Int. J. Data Netw. Sci. 2021, 5, 737–744. [Google Scholar] [CrossRef]

- Alharbi, N.S.; Alghanmi, A.S.; Fahlevi, M. Public Awareness, Uses, and Acceptance towards Government Health Mobile Apps during the COVID-19 Lockdown: The Case of Saudi Arabia. ICIC Express Lett. Part B Appl. 2022, 13, 887–895. [Google Scholar] [CrossRef]

- Alharbi, N.S.; Alsubki, N.; Altamimi, S.R.; Alonazi, W.; Fahlevi, M. COVID-19 Mobile Apps in Saudi Arabia: Systematic Identification, Evaluation, and Features Assessment. Front. Public Health 2022, 10, 803677. [Google Scholar] [CrossRef]

- Gumantan, A.; Mahfud, I.; Yuliandra, R. Tingkat Kecemasan Seseorang Terhadap Pemberlakuan New Normal Dan Pengetahuan Terhadap Imunitas Tubuh. Sport Sci. Educ. J. 2020, 1, 18–27. [Google Scholar] [CrossRef]

- Taufik, T.; Warsono, H. Birokrasi Baru Untuk New Normal: Tinjauan Model Perubahan Birokrasi Dalam Pelayanan Publik Di Era COVID-19. Dialogue J. Ilmu. Adm. 2020, 2, 1–18. [Google Scholar] [CrossRef]

- Jamaludin, S.; Azmir, N.A.; Mohamad Ayob, A.F.; Zainal, N. COVID-19 Exit Strategy: Transitioning towards a New Normal. Ann. Med. Surg. 2020, 59, 165–170. [Google Scholar] [CrossRef]

- Corpuz, J.C.G. Correspondence: Adapting to the Culture of “New Normal”: An Emerging Response to COVID-19. J. Public Health 2021, 43, E344–E345. [Google Scholar] [CrossRef]

- Currie, G.M. A Lens on the Post-COVID-19 “New Normal” for Imaging Departments. J. Med. Imaging Radiat. Sci. 2020, 51, 361–363. [Google Scholar] [CrossRef] [PubMed]

- Handariastuti, R.; Achmad, Z.A. Controversy on the Terminationof Large-Scale Social Restrictions in Greater Surabaya at Kompas.Com and Suarasurabaya.Net. JOSAR J. Stud. Acad. Res. 2020, 5, 111–125. [Google Scholar] [CrossRef]

- Davis, F.D. Perceived Usefulness, Perceived Ease of Use, and User Acceptance of Information Technology. MIS Q. 1989, 13, 319–340. [Google Scholar] [CrossRef]

- Venkatesh, V.; Morris, M.G.; Davis, G.B.; Davis, F.D. User Acceptance of Information Technology: Toward a Unified View. MIS Q. 2003, 27, 425–478. [Google Scholar] [CrossRef]

- Bhattacherjee, A.; Sanford, C. Influence Processes for Information Technology Acceptance: An Elaboration Likelihood Model. MIS Q. 2006, 30, 805–825. [Google Scholar] [CrossRef]

- Venkatesh, V.; Bala, H. Technology Acceptance Model 3 and a Research Agenda on Interventions. Decis. Sci. 2008, 39, 273–315. [Google Scholar] [CrossRef]

- Baghla, S.; Gupta, G. Performance Evaluation of Various Classification Techniques for Customer Churn Prediction in E-Commerce. Microprocess. Microsyst. 2022, 94, 104680. [Google Scholar] [CrossRef]

- Byun, D.-H.; Finnie, G. Evaluating Usability, User Satisfaction and Intention to Revisit for Successful e-Government Websites. Electron. Gov. Int. J. 2011, 8, 1–19. [Google Scholar] [CrossRef]

- Fishbein, M.; Ajzen, I. Predicting and Understanding Consumer Behavior: Attitude-Behavior Correspondence. Underst. Attitudes Predict. Soc. Behav. 1980, 1, 148–172. [Google Scholar]

- Ajzen, I.Y.F.; Fishbein, M. Understanding Attitudes and Predicting Social Behavior; ScienceOpen, Inc.: Burlington, MA, USA, 1980. [Google Scholar]

- Ajzen, I. The Theory of Planned Behavior. Organ. Behav. Hum. Decis. Process 1991, 50, 179–211. [Google Scholar] [CrossRef]

- Cao, X.; Yu, L.; Liu, Z.; Gong, M.; Adeel, L. Understanding Mobile Payment Users’ Continuance Intention: A Trust Transfer Perspective. Internet Res. 2018, 28, 456–476. [Google Scholar] [CrossRef]

- Huang, C.; Kao, Y. UTAUT2 Based Predictions of Factors Influencing the Technology Acceptance of Phablets by DNP. Math. Probl. Eng. 2015, 2015, 1–23. [Google Scholar] [CrossRef]

- Swainson, L.; Mahanty, S. Green Economy Meets Political Economy: Lessons from the “Aceh Green” Initiative, Indonesia. Glob. Environ. Change 2018, 53, 286–295. [Google Scholar] [CrossRef]

- Loiseau, E.; Saikku, L.; Antikainen, R.; Droste, N.; Hansjürgens, B.; Pitkänen, K.; Leskinen, P.; Kuikman, P.; Thomsen, M. Green Economy and Related Concepts: An Overview. J. Clean Prod. 2016, 139, 361–371. [Google Scholar] [CrossRef]

- Merino-Saum, A.; Clement, J.; Wyss, R.; Baldi, M.G. Unpacking the Green Economy Concept: A Quantitative Analysis of 140 Definitions. J. Clean Prod. 2020, 242, 118339. [Google Scholar] [CrossRef]

- Georgeson, L.; Maslin, M.; Poessinouw, M. The Global Green Economy: A Review of Concepts, Definitions, Measurement Methodologies and Their Interactions. Geo 2017, 4, e00036. [Google Scholar] [CrossRef]

- Qureshi, M.H.; Hussain, T. Green Banking Products: Challenges and Issues in Islamic and Traditional Banks of Pakistan. J. Account. Financ. Emerg. Econ. 2020, 6, 703–712. [Google Scholar] [CrossRef]

- Yu, W.; Chavez, R.; Feng, M.; Wong, C.Y.; Fynes, B. Green Human Resource Management and Environmental Cooperation: An Ability-Motivation-Opportunity and Contingency Perspective. Int. J. Prod. Econ. 2020, 219, 224–235. [Google Scholar] [CrossRef]

- Meiryani, M.; Delvin Tandyopranoto, C.; Emanuel, J.; Lindawati, A.S.L.; Fahlevi, M.; Aljuaid, M.; Hasan, F. The Effect of Global Price Movements on the Energy Sector Commodity on Bitcoin Price Movement during the COVID-19 Pandemic. Heliyon 2022, 8, e10820. [Google Scholar] [CrossRef]

- Hair, J.F.; Hult, G.T.M.; Ringle, C.M.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM), 3rd ed.; SAGE: Thousand Oaks, CA, USA, 2022. [Google Scholar]

- Chawla, D.; Joshi, H. The Moderating Role of Gender and Age in the Adoption of Mobile Wallet. Foresight 2020, 22, 483–504. [Google Scholar] [CrossRef]

- Singh, N.; Srivastava, S.; Sinha, N. Consumer Preference and Satisfaction of M-Wallets: A Study on North Indian Consumers. Int. J. Bank Mark. 2017, 35, 944–965. [Google Scholar] [CrossRef]

- Mangani, K.S.; Syaukat, Y.; Arifin, B.; Tambunan, M. The Role of Branchless Banking in Performance of Households’ Micro and Small Enterprises: The Evidence from Indonesia. Econ. Sociol. 2019, 12, 114–131. [Google Scholar] [CrossRef]

- Dinas Komunikasi Informatika dan Statistik Data Strategis Kota Magelang, Semester I Tahun 2021. Available online: https://datago.magelangkota.go.id/frontend/elibrary/default/view?id=26 (accessed on 11 August 2022).

- Hair, J.F.; Hult, G.T.M.; Ringle, C.M.; Sarstedt, M. A Primer on Partial Least Squares Structural Equation Modeling (PLS-SEM), 2nd ed.; Sage: Thousand Oaks, CA, USA, 2017; ISBN 97814-8337-7445. [Google Scholar]

- Al Arif, M.N.R.; Cahyani, U.T. Branchless Banking and Profitability in the Indonesian Islamic Banking Industry. J. Ekon. Keuang. Islam 2021, 7, 154–160. [Google Scholar] [CrossRef]

- Mangani, K.S.; Heatubun, A.B.; Tambunan, M.E. Branchless Banking Process in Rural Areas: A Price Barrier? J. Public Adm. Gov. 2021, 11, 317. [Google Scholar] [CrossRef]

- Shahabi, V.; Azar, A.; Faezy Razi, F.; Fallah Shams, M.F. Simulation of the Effect of COVID-19 Outbreak on the Development of Branchless Banking in Iran: Case Study of Resalat Qard–al-Hasan Bank. Rev. Behav. Financ. 2021, 13, 85–108. [Google Scholar] [CrossRef]

- Rachmawati, R.; Farda, N.M.; Rijanta, R.; Setiyono, B. The Advantages and Analysis of the Location of Branchless Banking in Urban and Rural Areas in Yogyakarta Special Region, Indonesia. J. Urban Reg. Anal. 2019, 11, 53–68. [Google Scholar] [CrossRef]

- Ashraf, M.A. Comprehending the Intention to Use Branchless Banking by Rural People during the Corona Pandemic: Evidence from Bangladesh. J. Financ. Serv. Mark. 2022, 1–18. [Google Scholar] [CrossRef]

- Setiyono, C.; Shihab, M.R.; Azzahro, F. The Role of Initial Trust on Intention to Use Branchless Banking Application: Case Study of Jenius. J. Phys. Conf. Ser. 2019, 1193, 012022. [Google Scholar] [CrossRef]

- Reaves, B.; Bowers, J.; Scaife, N.; Bates, A.; Bhartiya, A.; Traynor, P.; Butler, K.R.B. Mo(Bile) Money, Mo(Bile) Problems: Analysis of Branchless Banking Applications. ACM Trans. Priv. Secur. 2017, 20, 1–31. [Google Scholar] [CrossRef]

- Mulyati, E. The Agreement of Bank Cooperation with Agent in Providing Branchless Banking with The Realization of Inclusive Finance. Fiat Justisia J. Ilmu. Huk. 2021, 15, 301–326. [Google Scholar] [CrossRef]

- Chipeta, C.; Muthinja, M.M. Financial Innovations and Bank Performance in Kenya: Evidence from Branchless Banking Models. South Afr. J. Econ. Manag. Sci. 2018, 21, 1–11. [Google Scholar] [CrossRef]

- Zahid, M.; Rahman, H.U.; Ullah, Z.; Muhammad, A. Sustainability and branchless banking: The development and validation of a distinct measurement scale. Technol. Soc. 2021, 67, 101764. [Google Scholar] [CrossRef]

- Missiame, A.; Nyikal, R.A.; Irungu, P. What is the impact of rural bank credit access on the technical efficiency of smallholder cassava farmers in Ghana? An endogenous switching regression analysis. Heliyon 2021, 7, e07102. [Google Scholar] [CrossRef]

- Kochar, A. Branchless banking: Evaluating the doorstep delivery of financial services in rural India. J. Dev. Econ. 2018, 135, 160–175. [Google Scholar] [CrossRef]

- Chu, Y.; Li, Z. Banking relationship, information reusability, and acquisition loans. J. Bank. Financ. 2022, 138, 106449. [Google Scholar] [CrossRef]

- Mukhtisar, M.; Tarigan, I.R.R.; Evriyenni, E. Pengaruh Efisiensi, Keamanan Dan Kemudahan Terhadap Minat Nasabah Bertransaksi Menggunakan Mobile Banking (Studi Pada Nasabah Bank Syariah Mandiri Ulee Kareng Banda Aceh). Jihbiz: Global J. Islam. Bank. Financ. 2021, 3, 56–72. [Google Scholar] [CrossRef]

- Liu, F. Macroeconomic effects of microsavings programs for the unbanked. J. Econ. Behav. Organ. 2018, 154, 75–99. [Google Scholar] [CrossRef]

- Mazumder, S.; Rao, R. Social Trust and the Choice between Bank Debt and Public Debt: Evidence from International Data. J. Multinatl. Financ. Manag. 2022, 100781. [Google Scholar] [CrossRef]

- Dang, V.D. Liquidity injection, bank lending, and security holdings: The asymmetric effects in Vietnam. J. Econ. Asymmetries 2021, 24, e00212. [Google Scholar] [CrossRef]

- Windasari, N.A.; Kusumawati, N.; Larasati, N.; Amelia, R.P. Digital-only banking experience: Insights from gen Y and gen Z. J. Innov. Knowl. 2022, 7, 100170. [Google Scholar] [CrossRef]

- Aitken, M.; Ng, M.; Horsfall, D.; Coopamootoo, K.P.; van Moorsel, A.; Elliott, K. In pursuit of socially-minded data-intensive innovation in banking: A focus group study of public expectations of digital innovation in banking. Technol. Soc. 2021, 66, 101666. [Google Scholar] [CrossRef]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Constructs | Definition | Dimension | Item | Scale |

|---|---|---|---|---|

| Attitude (AT) [28,29] | Attitude toward adoption is a cognitive process that describes a potential adopter’s positive or negative attitude about adopting a foreign technology | Strength | I don’t think I need help from other people in accessing branchless banking (AT1) | Likert |

| Accessibility | I believe the branchless banking step-by-step navigation is easy to understand (AT2) | |||

| I believe learning to use branchless banking is easy (AT3) | ||||

| Ambivalence | I like it when payments can be made quickly (AT4) | |||

| I believe it’s easy to transfer money through branchless banking because the steps are quite practical (AT5) | ||||

| Intention (IT) [29] | Behavioral intention to use is a behavioral tendency to continue to use a technology. BI refers to the consumer’s intention of effective use of a future product or service | Customer Loyalty | I want to make transactions using branchless banking in the near future (IT1) | Likert |

| It is very possible to use my smartphone for branchless banking (IT2) | ||||

| Willing to Pay More | I will use branchless banking a lot in the future (IT3) | |||

| Word of Mouth (WOM) | I intend to recommend others to use branchless banking (IT4) | |||

| Perceived Ease of Use (PE) [47] | Perceived ease of use is a belief about the decision-making process in using information technology. A person’s perception of the ease of use of information technology shows the extent to which that person believes that using a technology can facilitate the completion of work/tasks | Clear and Understandable | I believe the use of the branchless banking application is easy to understand (PE1) | Likert |

| I believe learning to use branchless banking is easy (PE2) | ||||

| Mental Effort | I like the fact that payments made via online require minimum effort (PE3) | |||

| Easy to Use | I am sure of the ease of online payment for all transactions (PE4) | |||

| Overall, branchless banking is easier to use than transactions at traditional banks (PE5) | ||||

| Perceived Usefulness (PU) [48] | Perceived usefulness is defined as an individual’s perception of using new technology that can improve performance. Applying this definition to the context of a digital wallet in its use refers to the degree to which consumers believe using a digital wallet as a medium will increase their performance or productivity, thereby enhancing the outcome of their shopping experience | Performance Outcome | I think using branchless banking allows me to complete transactions faster (PU1) | Likert |

| I believe branchless banking wallets are useful for making online transactions (PU2) | ||||

| Personal Outcome | I believe using branchless banking increases the efficiency of my online transactions (PU3) | |||

| In my opinion, branchless banking is acceptable in all e-commerce (PU4) | ||||

| Instrinsic Motivation | I believe branchless banking improves the quality of online transactions (PU5) | |||

| Overall, I think branchless banking improves my performance (PU6) | ||||

| Actual Usage (AU) [47] | Actualization of use is a real condition of system application. Someone will feel happy to use the system if they believe that the system is not difficult to use and proven to increase their productivity, which is reflected in the actual conditions of use | Continuity | I do transactions in branchless banking quite often on a daily basis (AU1) | Likert |

| Activity | I use branchless banking actively at the time of the transaction (AU2) | |||

| I will choose branchless banking for online transactions (AU3) |

| Description | Economic Field | Social Field | Education Field | Grand Total |

|---|---|---|---|---|

| Transactions per month (IDR) | 3,087,933,632 | 1,069,989,495 | 246,289,595 | 4,404,212,721 |

| Per customer/month (IDR) | 7,552,660 | 2,877,845 | 58,572 | 917,020 |

| Transactions per day (IDR) | 102,012,973 | 35,361,992 | 8,134,703 | 145,509,668 |

| Per customer/day (IDR) | 249,473 | 95,117 | 1934 | 30,294 |

| Original Sample (O) | Sample Mean (M) | Standard Deviation (STDEV) | T Statistics (|O/STDEV|) | p Values | |

|---|---|---|---|---|---|

| AT -> IT | 0.720 | 0.722 | 0.047 | 15,357 | 0.000 |

| IT -> AU | 0.584 | 0.590 | 0.050 | 11,682 | 0.000 |

| PE -> AT | 0.652 | 0.642 | 0.087 | 7468 | 0.000 |

| PU -> AT | 0.168 | 0.181 | 0.078 | 2152 | 0.016 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2023 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Marhaeni, A.A.I.N.; Jermsittiparsert, K.; Sudarmo; Indrawati, L.R.; Prasetyo, A.; Fuada, N.; Rachmadhani, A.; Raharjo, T.W.; Wahyudianto, H.; Harwijayanti, B.P.; et al. Adoption of the Green Economy through Branchless Rural Credit Banks during the COVID-19 Pandemic in Indonesia. Sustainability 2023, 15, 2723. https://doi.org/10.3390/su15032723

Marhaeni AAIN, Jermsittiparsert K, Sudarmo, Indrawati LR, Prasetyo A, Fuada N, Rachmadhani A, Raharjo TW, Wahyudianto H, Harwijayanti BP, et al. Adoption of the Green Economy through Branchless Rural Credit Banks during the COVID-19 Pandemic in Indonesia. Sustainability. 2023; 15(3):2723. https://doi.org/10.3390/su15032723

Chicago/Turabian StyleMarhaeni, A. A. I. N., Kittisak Jermsittiparsert, Sudarmo, Lucia Rita Indrawati, Andjar Prasetyo, Noviati Fuada, Arnis Rachmadhani, Tri Weda Raharjo, Heri Wahyudianto, Bekti Putri Harwijayanti, and et al. 2023. "Adoption of the Green Economy through Branchless Rural Credit Banks during the COVID-19 Pandemic in Indonesia" Sustainability 15, no. 3: 2723. https://doi.org/10.3390/su15032723